CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN)

ACTIVITY-BASED COSTING

DISCUSSION QUESTIONS

1. Management desires accurate product costs so that its decisions regarding products are correct.

Managers are concerned about the accuracy of product costs, which are used for decisions such as

determining product mix, establishing product price, and determining whether to discontinue a

product line.

2. A single plantwide overhead rate will provide accurate product costing if products use production

3. Under the multiple production department rate method, factory overhead rates are determined for

each production department. Factory overhead is allocated to products depending on the amount of

allocation base used in each department. Under the single plantwide rate method, one factory

overhead rate is determined for the whole factory and is allocated to products depending on the

amount of allocation base used in the factory.

5. Under activity-based costing, factory overhead costs are assigned to activity cost pools rather than

production departments. The budgeted factory overhead in the activity pools is allocated to

products based upon their own unique activity rates.

6. These activities are part of selling and administrative expenses, which must be treated as period

expenses under generally accepted accounting principles (GAAP). Thus, they cannot be included

as product costs under GAAP.

8. Calculating product costs using activity rates may result in greater accuracy than using multiple

production department overhead rates when products consume activities in proportions that are

unrelated to departmental allocation bases.

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

BASIC EXERCISES

BE 18–1 (FIN MAN); BE 4–1 (MAN)

a.

Speedboat:

250 units × 12 direct labor hours =

3,000

direct labor hours

Bass boat:

250 units × 12 direct labor hours =

3,000

Total

6,000

direct labor hours

Single plantwide factory overhead rate:

c.

Speedboat:

$100 per direct labor hour × 12 dlh per unit = $1,200 per unit

BE 18–2 (FIN MAN); BE 4–2 (MAN)

a.

Fabrication:

(250 speedboats × 8 dlh) + (250 bass boats × 4 dlh)

= 3,000 direct labor hours

Assembly:

(250 speedboats × 4 dlh) + (250 bass boats × 8 dlh)

= 3,000 direct labor hours

b.

Fabrication Department rate: $420,000 ÷ 3,000 dlh = $140 per dlh

Assembly Department rate: $180,000 ÷ 3,000 dlh = $60 per dlh

c.

Speedboat:

Fabrication Department: 8 dlh × $140 =

Assembly Department: 4 dlh × $60 =

Total factory overhead per speedboat

Bass boat:

Fabrication Department: 4 dlh × $140 =

Assembly Department: 8 dlh × $60 =

Total factory overhead per bass boat

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

BE 18–3 (FIN MAN); BE 4–3 (MAN)

a. Fabrication:

$204,000 ÷ 3,000 direct labor hours = $68 per dlh

Assembly:

$105,000 ÷ 3,000 direct labor hours = $35 per dlh

b.

Activity

Speedboat

Bass Boat

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Fabrication

2,000

dlh

$68

per dlh

$136,000

1,000

dlh

$68

per dlh

$ 68,000

Assembly

1,000

dlh

$35

per dlh

35,000

2,000

dlh

$35

per dlh

70,000

Setup

per setup

per setup

39,000

Inspections

1,100

$90

per insp.

99,000

$90

per insp.

36,000

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

BE 18–4 (FIN MAN); BE 4–4 (MAN)

a. Sales order processing activity:

750 orders × $20 per order =

$15,000

Customer return activity:

80 returns × $100 per return =

8,000

BE 18–5 (FIN MAN); BE 4–5 (MAN)

Guest check-in …………………………………………………

$ 8.00

(1 check-in × $8.00)

Meal service …………………………………………………….

(3 meals × $4.00)

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

EXERCISES

Ex. 18–1 (FIN MAN); Ex. 4–1 (MAN)

Ex. 18–2 (FIN MAN); Ex. 4–2 (MAN)

a. Single Plantwide Factory Overhead Rate =

$2,948,125

11,125 direct labor hours *

= $265 per direct labor hour

* Total direct labor hours:

Budgeted

Production

Volume

Direct Labor

Hours per Unit

Direct Labor

Hours

×

=

Flutes …………………….

2,000 units

×

2.0

=

4,000

b.

Single Plant-

wide Rate

per Direct

Labor Hour

Direct

Labor

Hours

Factory Overhead per Unit

(Factory Overhead ÷

Budgeted Production Volume)

Factory

Overhead

×

=

Flutes ……..

4,000

×

$265

=

$1,060,000

$1,060,000

÷

2,000

units

=

$530

Total ……….

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–3 (FIN MAN); Ex. 4–3 (MAN)

a. Single Plantwide Factory Overhead Rate =

*

**

$156,000

2,400 processing hours

= $65 per processing hour

The selling and administrative expenses are not factory overhead.

** Total processing hours:

Budgeted

Production

Volume

(Cases)

×

Processing

Hours per Case

=

Processing

Hours

Tortilla chips ………………..

3,000

×

0.25

=

750

×

Pretzels ……………………….

3,500

×

0.30

=

1,050

b.

Processing

Hours

Single Plantwide

Factory Over-

head Rate per

Processing

Hour

Factory

Overhead

Factory Overhead per Case

(Factory Overhead ÷

Budgeted Production Volume)

×

=

Tortilla chips …..

750

×

$65

=

$ 48,750

$48,750

÷

3,000 cases = $16.25

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–4 (FIN MAN); Ex. 4–4 (MAN)

a. First, determine the total estimated labor hours consumed by the three products:

Direct Labor

Hours per

Total

Labor

Volume

×

Unit

=

Hours

Pistons …………………………………………………………

6,000

×

0.30

=

1,800

b.

Direct Labor

Hours per

Unit

Factory Overhead

Cost per Unit

($28.00 × Direct

Labor Hours per Unit)

Direct Labor

Cost per Unit

($20.00 × Direct

Labor Hours per Unit)

Pistons ………………………..

0.30

$ 8.40

$ 6.00

Valves………………………….

0.50

14.00

10.00

Cams …………………………..

0.10

2.80

2.00

c.

Isaac Engines Inc.

Product Line Budgeted Gross Profit Reports

For the Year Ended December 31, 20Y2

Pistons

Valves

Cams

Revenues (price × unit volume)

$ 240,0001

$ 273,0002

$ 55,0003

Direct materials (direct materials

cost per unit × unit volume)

$ (54,000)4

$ (65,000)5

$(20,000)6

Direct labor [direct labor cost per

unit (b) × unit volume]

(36,000)7

(130,000)8

(2,000)9

cost per unit (b) × unit volume]

Total product costs

Gross profit percentage of sales

d. Valves have the lowest (and negative) gross profit as a percent of sales. Valves may

require a higher price or lower cost to manufacture in order to achieve a higher

profitability similar to the other two products.

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–5 (FIN MAN); Ex. 4–5 (MAN)

a. Production department factory overhead rates:

Pattern

Department

Cut and Sew

Department

Total factory overhead …………………….

$294,000

$560,000

÷ Direct labor hours ………………………..

42,000

dlh

56,000

dlh

Departmental overhead rate …………….

$ 7.00

per dlh

$ 10.00

per dlh

b.

Product cost allocation:

Small Glove

Pattern Department ……………………

0.20 dir. labor hr. × $7 per dlh =

$ 1.40

Pattern Department ……………………

0.30 dir. labor hr. × $7 per dlh =

$ 2.10

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–6 (FIN MAN); Ex. 4–6 (MAN)

a. Plantwide overhead rate:

Budgeted Factory Overhead $1,080,000

= = $120.00 per dmh

Product costs:

b.

Department factory overhead rates:

Assembly

Department

Testing

Department

Production department overhead ………….

$280,000

$800,000

÷ Direct machine hours ………………………..

4,000

dmh

5,000

dmh

Production department overhead rate……

$ 70.00

per dmh

$ 160.00

per dmh

Product cost allocation:

c. The factory overhead determined under the single plantwide factory overhead

rate and multiple production department factory overhead rate methods are

different. The multiple production department factory overhead rate method

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–7 (FIN MAN); Ex. 4–7 (MAN)

a. Plantwide overhead rate:

Budgeted Factory Overhead $640,000

= = $80 per dlh

Plantwide Allocation Base 8,000 direct labor hours

Product costs:

b.

Department factory overhead rates:

Fabrication

Department

Assembly

Department

Total production department

factory overhead ……………………………………

$440,000

$200,000

÷ Direct labor hours ………………………………….

4,000

dlh

4,000

dlh

Production department overhead rate ………..

$ 110

per dlh

$ 50

per dlh

Product cost allocation:

c. Management should select the multiple department factory overhead rate method

of allocating overhead costs. The single plantwide factory overhead rate method

indicates that both products have the same factory overhead of $800 per unit.

This is because each product uses a total of 10.0 direct labor hours per unit.

However, each product uses these 10.0 direct labor hours much differently. The

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–8 (FIN MAN); Ex. 4–8 (MAN)

Activity

Activity Base

Cafeteria

Number of employees

Customer return processing

Number of customer returns

Electric power

Kilowatt hours used

Human resources

Number of employees

Inventory control

Number of inventory transactions

Invoice and collecting

Number of customer orders

Machine depreciation

Number of machine hours

Materials handling

Number of material moves

Order shipping

Number of customer orders

Number of payroll checks processed

Performance reports

Number of performance reports

Production control

Number of production orders

Production setup

Number of setups

Number of purchase orders

Ex. 18–9 (FIN MAN); Ex. 4–9 (MAN)

a. Sales order processing activity rate:

$250,000 ÷ 50,000 sales orders = $5 per sales order

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–10 (FIN MAN); Ex. 4–10 (MAN)

Activity

Elliptical Machines

Treadmills

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Fabrication

600

mh

$30

per mh

$18,000

400

mh

$30

per mh

$12,000

Assembly

190

dlh

$35

per dlh

6,650

223

dlh

$35

per dlh

7,805

Setup

30

setups

$90

per setup

2,700

30

setups

$90

per setup

2,700

Inspecting

$20

per insp.

$20

per insp.

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

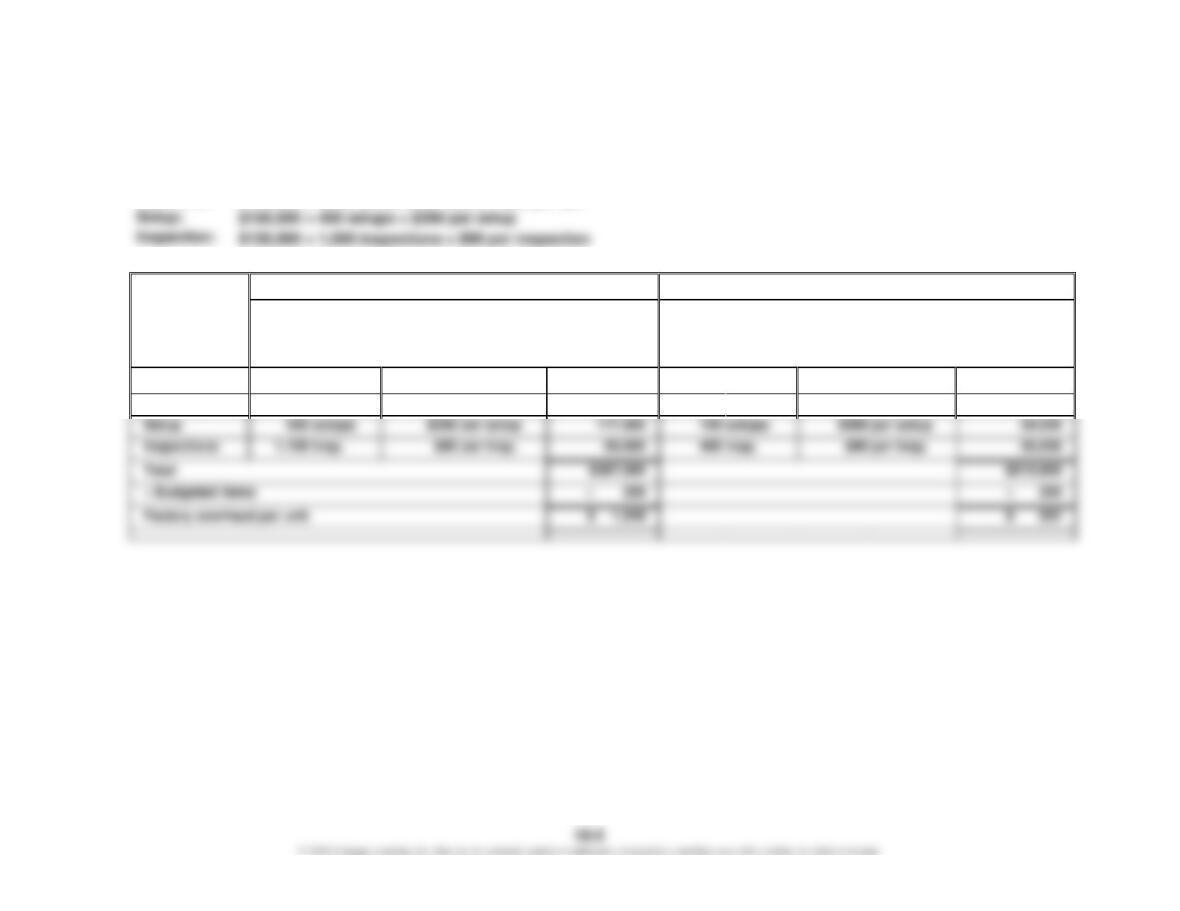

Ex. 18–11 (FIN MAN); Ex. 4–11 (MAN)

a.

Budgeted

Total

Activity

Activity

Activity

Activity

Cost

÷

Base

=

Rate

Casting

$570,000

19,000

mh

$30

per mh

Assembly

dlh

per dlh

Inspecting

insp.

per insp.

Setup

setups

per setup

b.

Activity

Entry Lighting Fixtures

Dining Room Lighting Fixtures

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Casting

6,000

mh

$30

per mh

$180,000

13,000

mh

$30

per mh

$390,000

Assembly

3,000

dlh

$16

per dlh

48,000

2,000

dlh

$16

per dlh

32,000

Inspecting

600

insp.

$42

per insp.

25,200

400

insp.

$42

per insp.

16,800

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

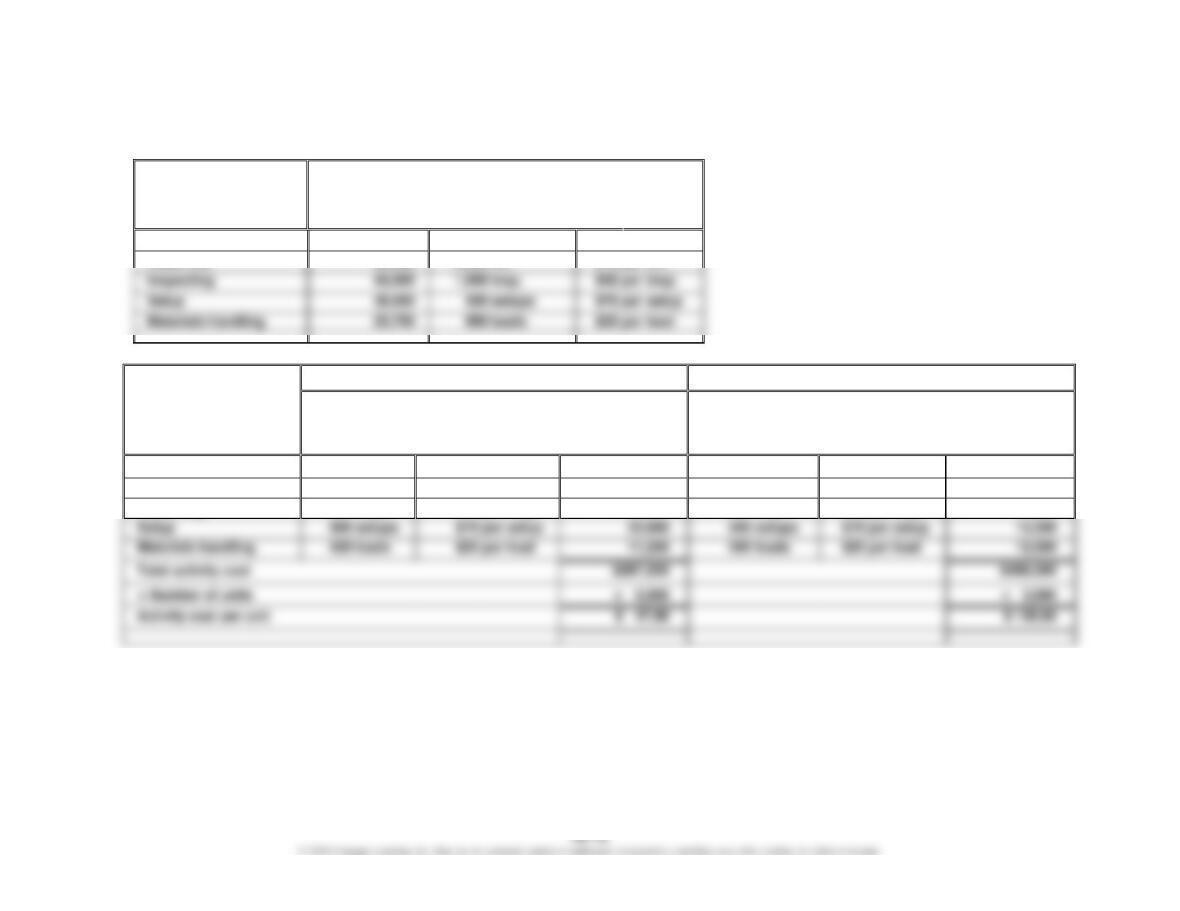

Ex. 18–12 (FIN MAN); Ex. 4–12 (MAN)

a.

Procurement

Scheduling

Materials Handling

Product

Development

Activity rate

Factory overhead

$12,600

$90,000

$11,000

$50,000

* Engineering change order

b.

Ovens

Refrigerators

Activity

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

Activity

Cost

Procurement

400

purch. ords.

$18

per purch. ord.

$ 7,200

300

purch. ords.

$18

per purch. ord.

$ 5,400

Scheduling

800

prod. ords.

$75

per prod. ord.

60,000

400

prod. ords.

$75

per prod. ord.

30,000

Materials handling

300

moves

$22

per move

200

moves

$22

per move

÷ 1,000

Activity cost per unit

$ 93.80

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

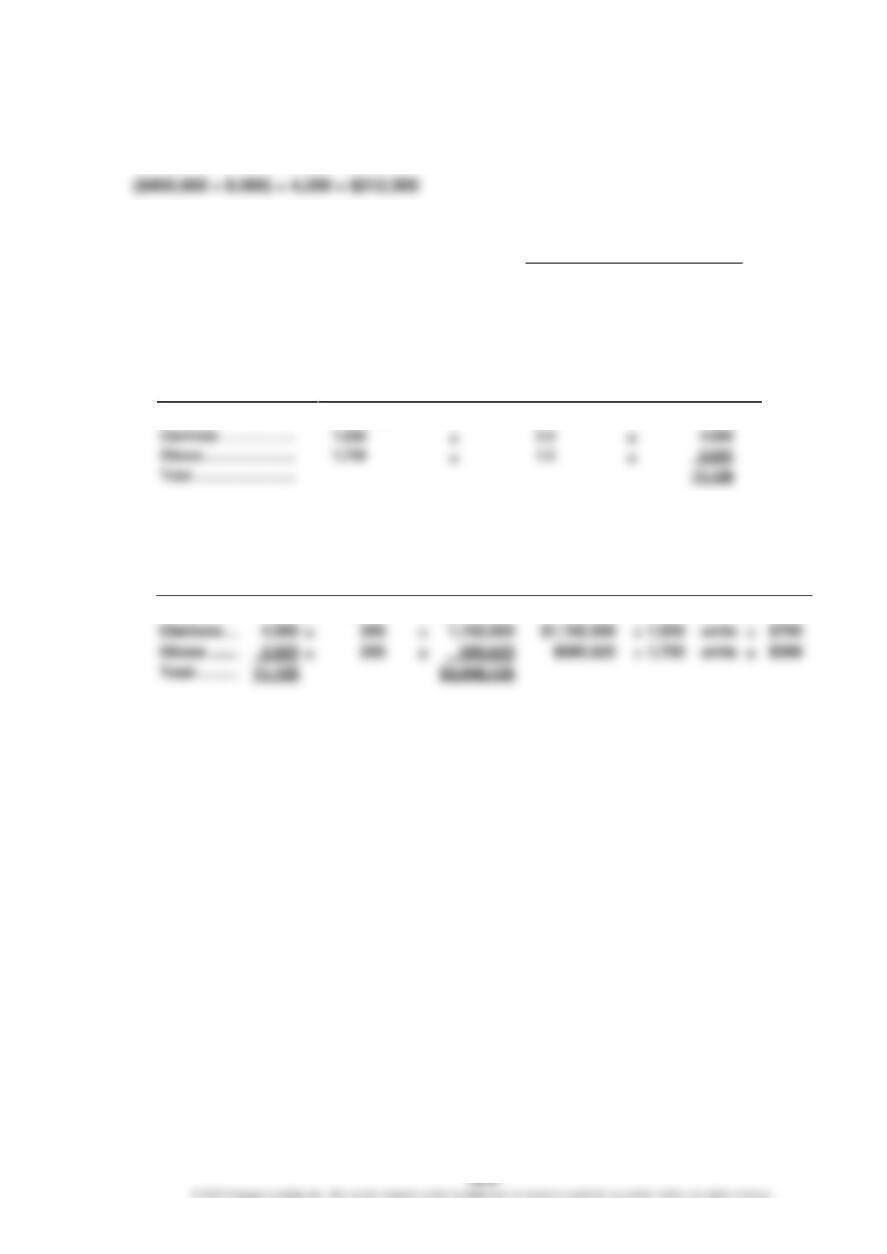

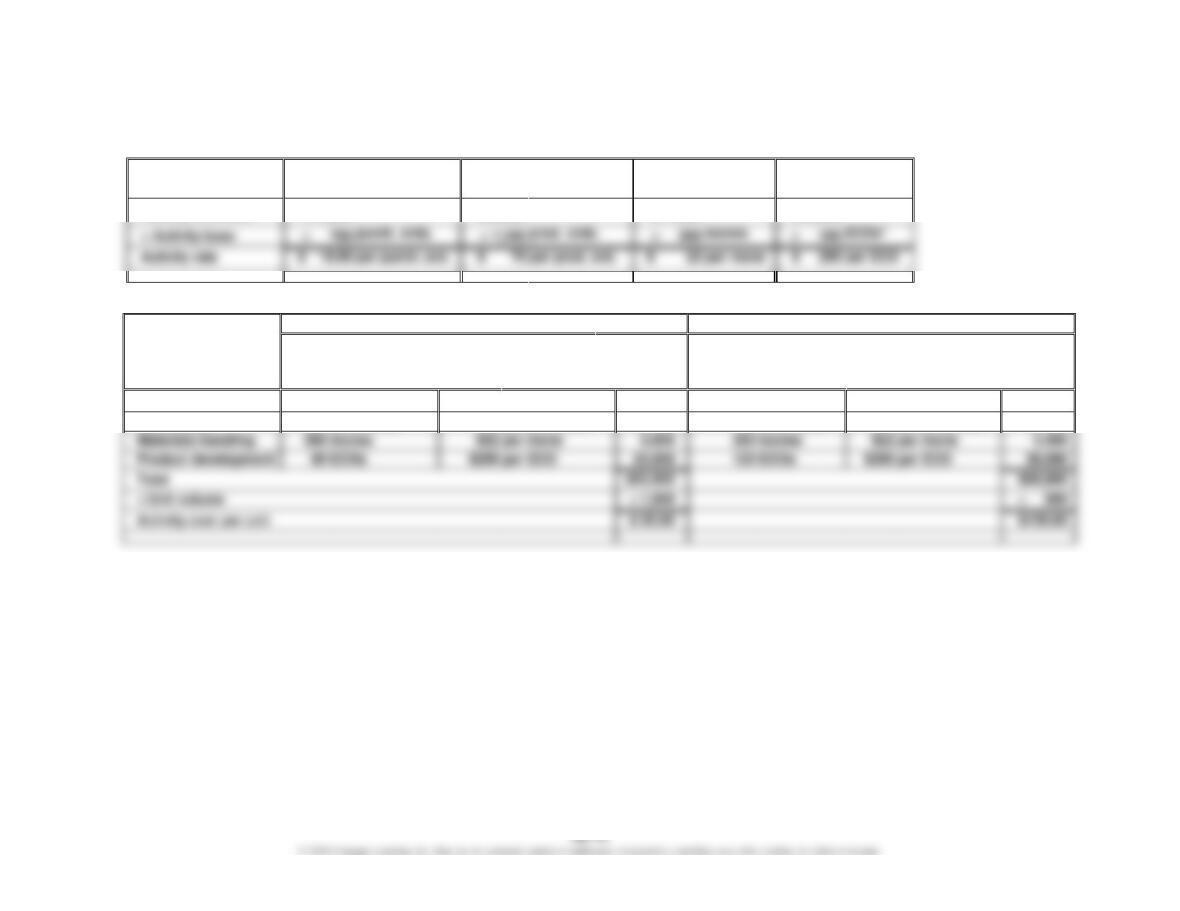

Ex. 18–13 (FIN MAN); Ex. 4–13 (MAN)

a. Single plantwide rate:

Indirect Labor $200,000

=

Plantwide Allocation Base 2,000 direct labor hours

= $100 per direct labor hour

Direct

Labor

Hours

×

Plantwide

Rate

=

Indirect Labor

Cost

÷

Units

=

Indirect

Labor Cost

per Unit

b. Activity-based rates:

Setup

Production

Support

Budgeted activity cost* ……………………

$ 60,000

$140,000

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–13 (FIN MAN); Ex. 4–13 (MAN) (Concluded)

c.

Cell Phones

Tablets

Activity

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Setup

1,200

setups

$15.00

per setup

$18,000

2,800

setups

$15.00

per setup

$ 42,000

Production support

1,000

dlh

$70.00

per dlh

70,000

1,000

dlh

$70.00

per dlh

70,000

Total

$88,000

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

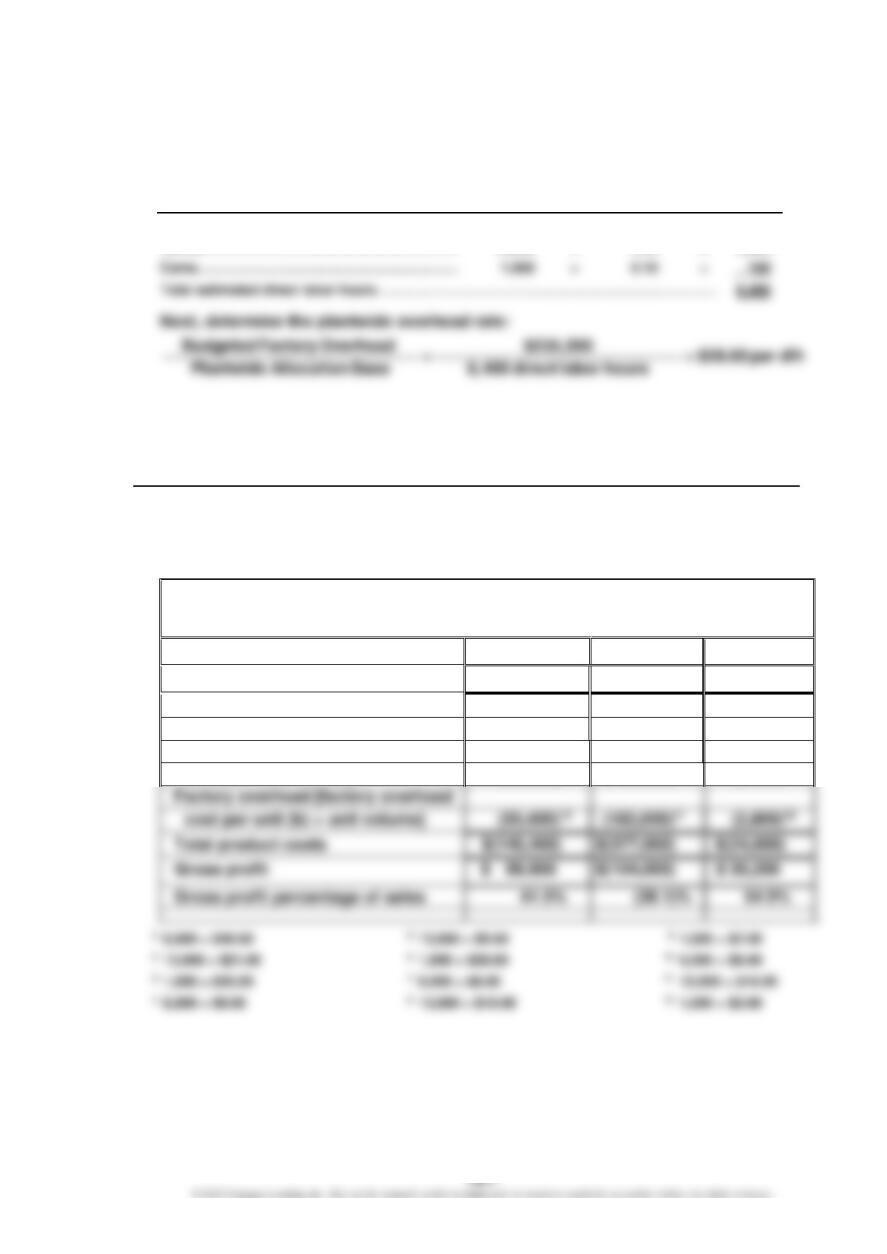

Ex. 18-14 (FIN MAN); Ex. 4-14 (MAN)

a. Production department factory overhead rates:

Assembly

Department

Test and Pack

Department

Factory overhead……………………………………….

$186,000

$120,000

b.

Activity

Blender

Toaster Oven

Allocation-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Allocation-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Assembly Department

750

dlh

$62

per dlh

$ 46,500

2,250

dlh

$62

per dlh

$139,500

Test and Pack Department

dlh

$40

per dlh

90,000

dlh

$40

per dlh

$136,500

$169,500

Factory overhead cost per unit

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

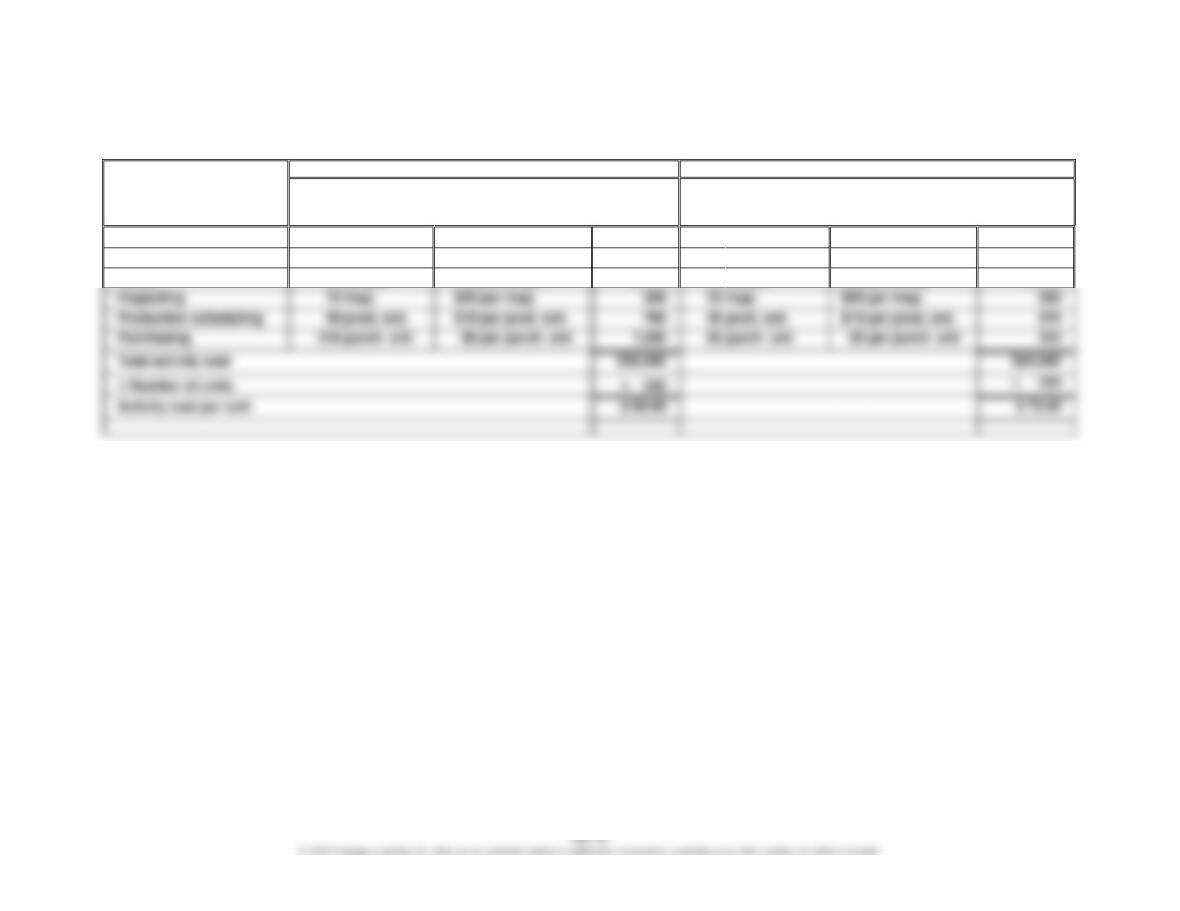

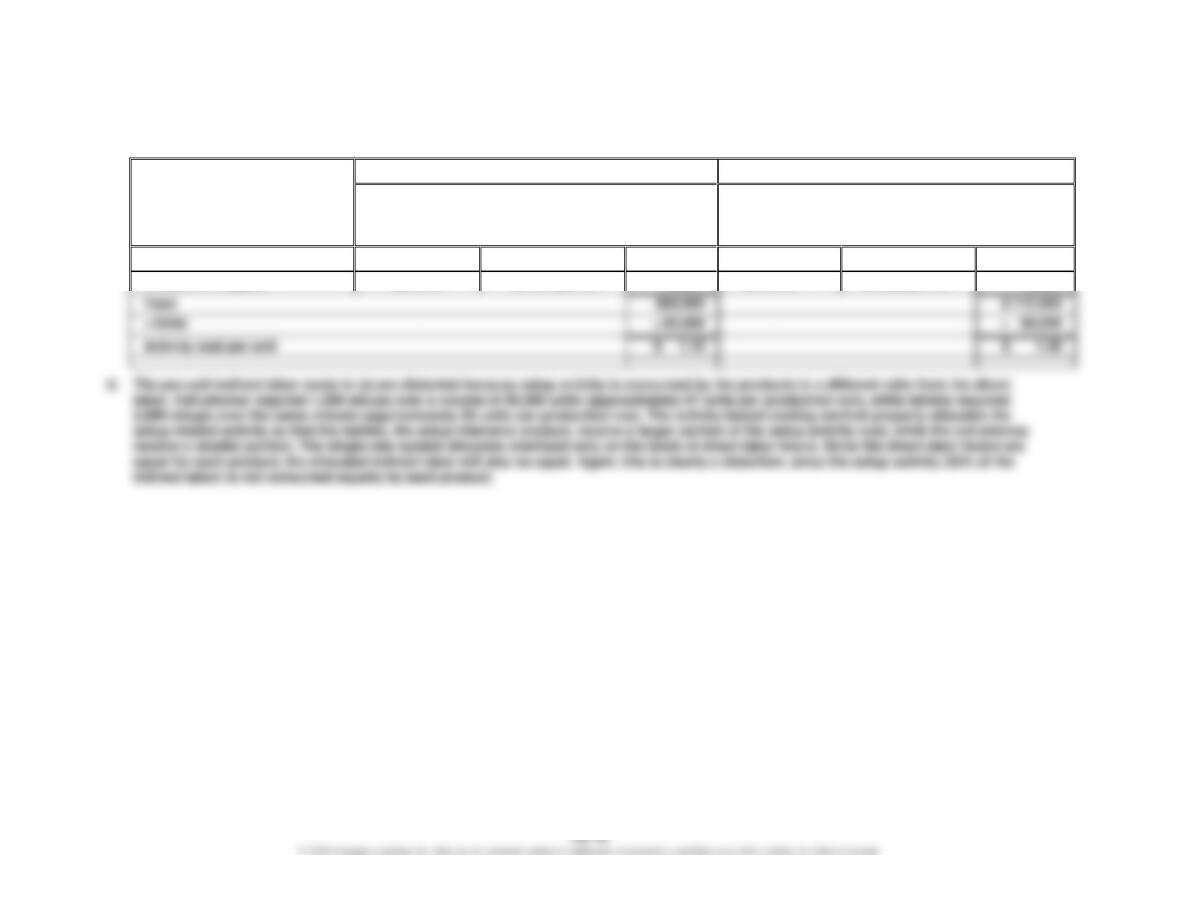

Ex. 18-15 (FIN MAN); Ex. 4-15 (MAN)

a. Activity rates:

Assembly

Activity

Test and Pack

Activity

Setup

Activity

Budgeted activity cost ………………………………………..

$105,000

1

$39,000

2

$162,000

1 $186,000 – $81,000

2 $120,000 – $81,000

b.

Activity

Blender

Toaster Oven

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Test and pack activity

dlh

$13

per dlh

dlh

$13

per dlh

Setup activity

135

$900

per setup

per setup

Factory overhead cost per unit

Assembly activity

750

dlh

$35

per dlh

$ 26,250

2,250

dlh

$35

per dlh

$ 78,750

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–15 (FIN MAN); Ex. 4–15 (MAN) (Concluded)

Note to Instructors: If you assigned both Ex. 18–14 and Ex. 18–15, then you can make

the following observations:

The activity-based costing approach provides unit factory overhead cost information

that is opposite to that of the multiple production department factory overhead rate

method. The reason is that the multiple production department factory overhead rate

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

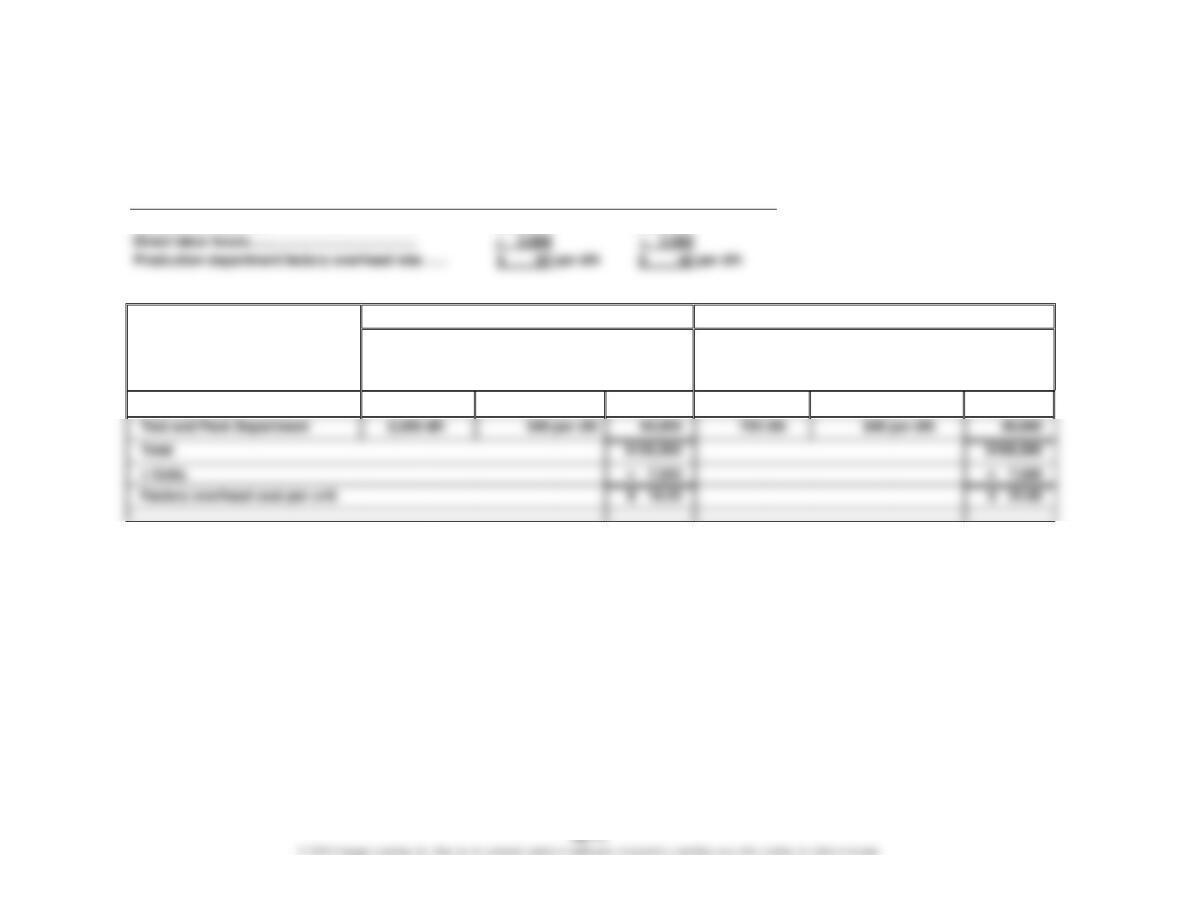

Ex. 18–16 (FIN MAN); Ex. 4–16 (MAN)

a.

Column A

Column B

Column C

Product Volume Class

Single Rate

Overhead

Allocation

per Unit

ABC Overhead

Allocation

per Unit

Percent Change

in Allocation

(Col. B – Col. A)/Col. A

Low

$30.001

$58.062

93.5%

Medium

30.003

29.314

(2.3)%

High

30.005

25.466

(15.1)%

1 (24 hours × $200 per hour) ÷ 160 units

2 [(24 hours × $160 per hour) + (14 setups × $240 per setup) +

b. The machine hour rate is greater under the single-rate method than under the activity-

based method because all the factory overhead is allocated by machine hours under

the single-rate method. However, only a portion of the factory overhead is allocated

under the machine rate method using activity-based costing. The remaining factory

overhead is allocated using the other two activity rates. Thus, the numerator for

determining the machine hour rate under activity-based costing must be less than the

numerator under the single machine hour rate method.

c. Column C indicates that under activity-based costing the low-volume product has a

higher per-unit cost than calculated under the single-rate method. In contrast, under

activity-based costing the high-volume product has a lower per-unit cost than

Note: The sum of the total overhead from Columns A and B is not equal because there

are only three representative products, not all of the products.