Chapter 4 Chapter 4

Implementing Accounting Analysis

Discussion Questions

1. Use the templates in Tables 4-1, 4-2, and 4-3 to recast the financial statements for Nordstrom, Inc.

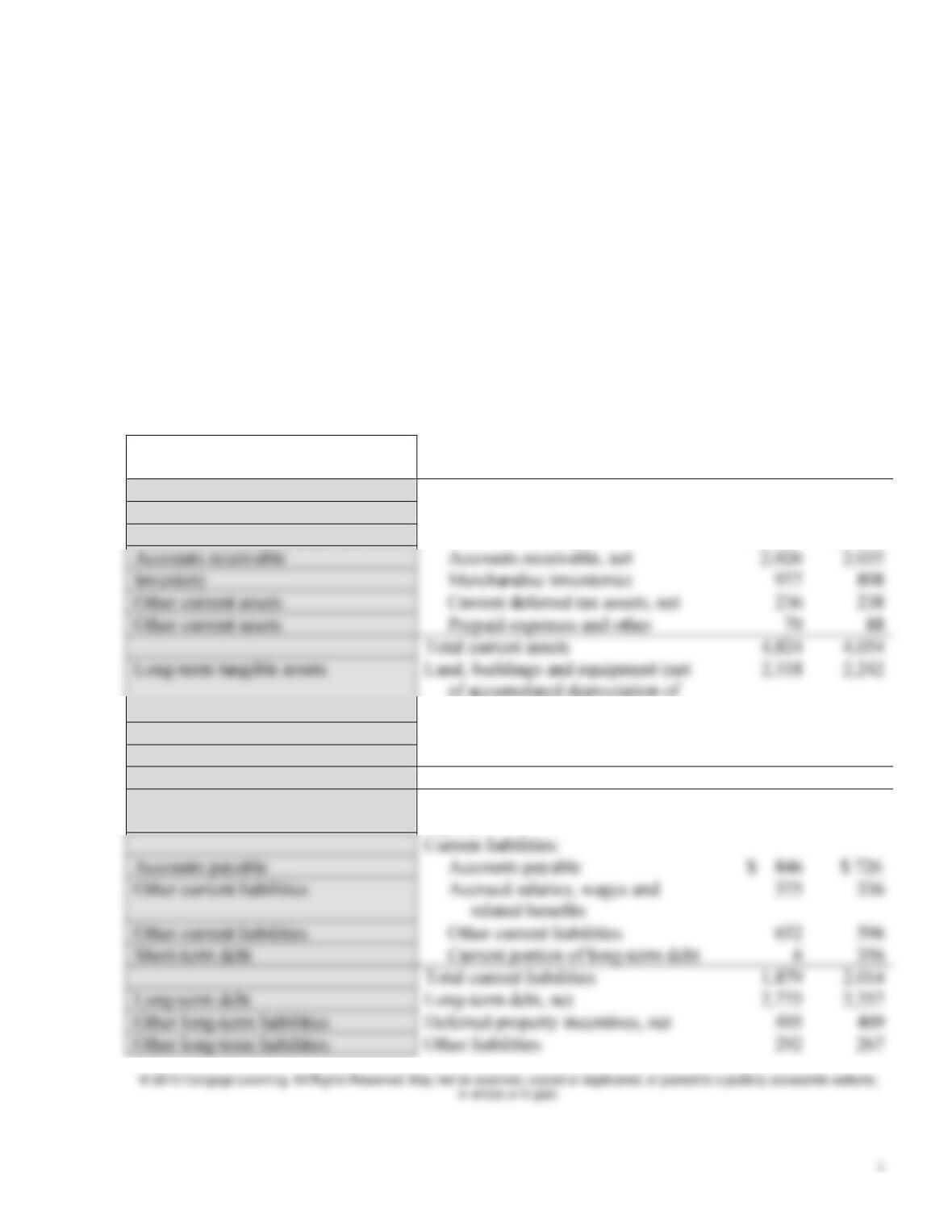

Balance Sheet Standardization

$ in millions

Jan. 29

2011

Jan. 30

2010

Assets

Current assets:

Cash and marketable securities

Cash and cash equivalents

$ 1,506

$ 795

Accounts receivable

Accounts receivable, net

2,026

Inventory

Merchandise inventories

977

898

Other current assets

Current deferred tax assets, net

236

238

Other current assets

Prepaid expenses and other

79

88

Total current assets

$3,520 and $3,316)

Long-term intangible assets

Goodwill

53

53

Other long-term assets

Other assets

267

230

Total assets

$ 7,462

$ 6,579

Liabilities and Shareholders’

Equity

Current liabilities:

Accounts payable

Accounts payable

$ 846

related benefits

Other current liabilities

Other current liabilities

652

596

Short-term debt

Current portion of long-term debt

356

Total current liabilities

Long-term debt

Long-term debt, net

Other long-term liabilities

Deferred property incentives, net

495

469

Other long-term liabilities

Other liabilities

292

267

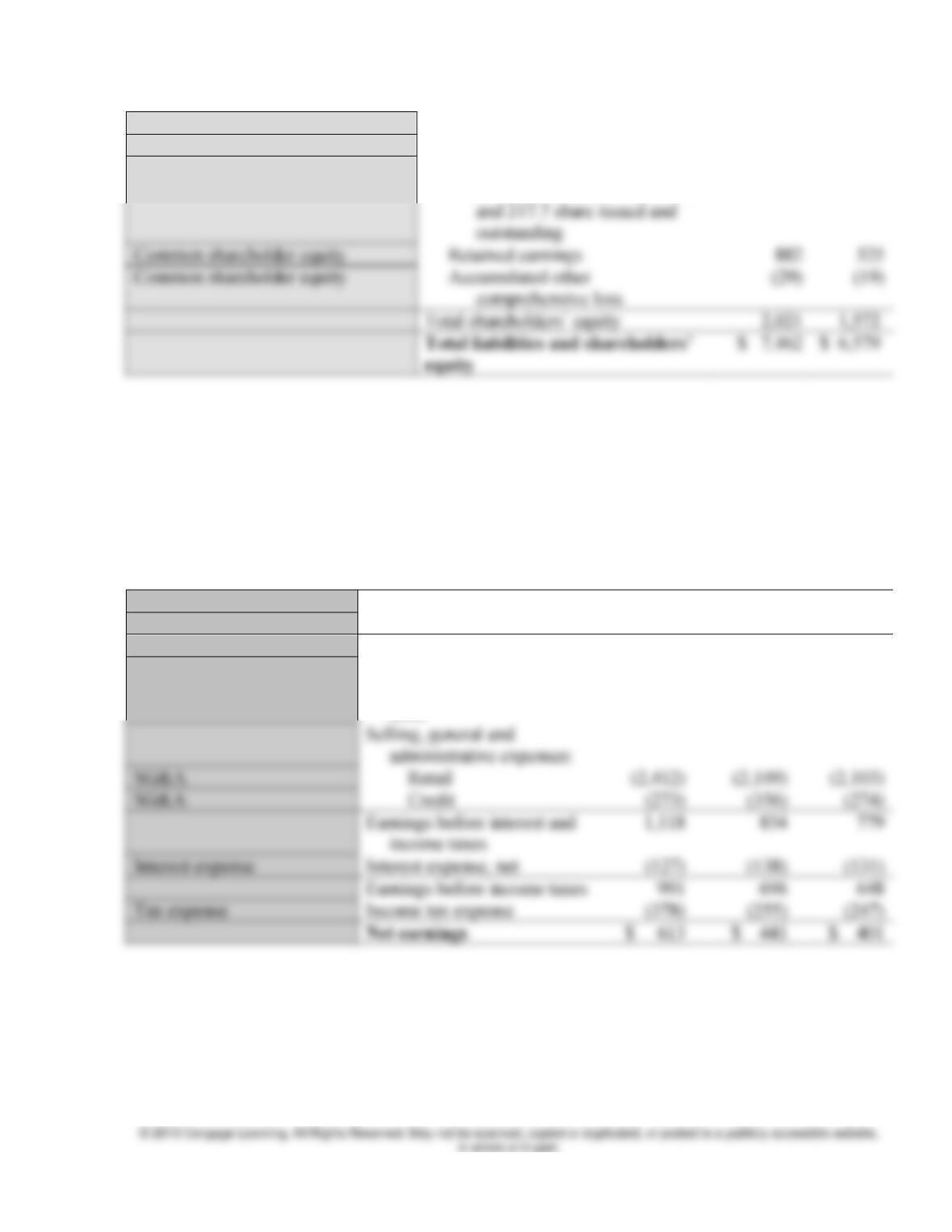

2 Instructor’s Manual

Commitments and contingencies

Shareholders’ equity:

Common shareholder equity

and 217.7 share issued and

outstanding

Common shareholder equity

Retained earnings

882

Common shareholder equity

Accumulated other

comprehensive loss

Total shareholders’ equity

2,021

equity

$ 6,579

Common stock, no par value:

1,000 shares authorized; 218.0

1,168

1,066

Income Statement Standardization

$ in millions

Fiscal year

2010

2009

2008

Sales

Net sales

$ 9,310

$ 8,258

$ 8,272

Sales

Credit card revenues

390

369

301

Total revenues

9,700

8,627

8,573

Cost of sales

Cost of sales and related

buying and occupancy

costs

(5,897)

(5,328)

(5,417)

Selling, general and

administrative expenses:

SG&A

Retail

SG&A

Credit

Earnings before interest and

income taxes

Interest expense

Interest expense, net

Earnings before income taxes

991

696

648

Tax expense

Income tax expense

Net earnings

$ 613

Chapter 4 Implementing Accounting Analysis 3

Cash Flow Statement Standardization

$ in millions

Fiscal year

2010

2009

2008

Operating Activities

Net income

Net earnings

$ 613

$ 441

$ 401

operating activities:

Long-term operating accruals –

depreciation and amortization

Depreciation and amortization of

buildings and equipment

327

313

302

Long-term operating accruals –

depreciation and amortization

Amortization of deferred property

incentives and other, net

(21)

Long-term operating accruals –

other

Deferred income taxes, net

(36)

Long-term operating accruals –

other

Stock-based compensation

expense

42

32

Long-term operating accruals –

Tax benefit from stock-based

15

Adjustments to reconcile net

earnings to net cash provided by

other

compensation

Long-term operating accruals –

other

Excess tax benefit from stock-

based compensation

(16)

(7)

(4)

Net (investment in) or liquidation

of operating working capital

Provision for bad debt expense

149

251

173

liabilities:

Net (investment in) or liquidation

of operating working capital

Accounts receivable

(74)

(93)

Net (investment in) or liquidation

of operating working capital

(80)

(1)

Net (investment in) or liquidation

of operating working capital

Prepaid expenses and other

assets

Net (investment in) or liquidation

of operating working capital

Accounts payable

72

168

Net (investment in) or liquidation

of operating working capital

Accrued salaries, wages and

related benefits

37

120

(54)

Net (investment in) or liquidation

of operating working capital

Other current liabilities

42

81

(48)

of operating working capital

Net (investment in) or liquidation

of operating working capital

Other liabilities

48

(29)

Net cash provided by operating

activities

848

Net (investment in) or liquidation

Deferred property incentives

95

96

119

4 Instructor’s Manual

Investing activities

Net (investment in) or liquidation

of operating long-term assets

Capital expenditures

(360)

Net (investment in) or liquidation

of operating long-term assets

Change in credit card receivables

originated at third parties

(182)

Net (investment in) or liquidation

of operating long-term assets

Other, net

3

1

3

Net cash used in investing activities

Financing activities

Net debt (repayment) or issuance

(Repayments) proceeds from

commercial paper borrowings

—

(275)

275

Net debt (repayment) or issuance

Proceeds from long-term

borrowings, net of discounts

150

Net debt (repayment) or issuance

Principal payments on long-term

borrowings

Net debt (repayment) or issuance

Increase in cash book overdrafts

Dividend (payment)

Cash dividends paid

Net stock (repurchase) or issuance

Repurchase of common stock

options

Net stock (repurchase) or issuance

Proceeds from employee stock

purchase plan

13

13

17

Net stock (repurchase) or issuance

Excess tax benefit from stock-

based compensation

16

7

4

Net stock (repurchase) or issuance

Other, net

Net cash (used in) provided by

financing activities

13

Net increase (decrease) in cash and

cash equivalents

Chapter 4 Implementing Accounting Analysis 5

The resulting standardized financial statements are as follows:

Nordstrom Standardized Balance Sheet

$ in millions

January 29, 2011

January 30, 2010

ASSETS

Cash and Marketable Securities

$ 1,506

$ 795

Accounts Receivable

2,026

2,035

Inventory

977

898

Other Current Assets

315

326

4,824

Long-Term Tangible Assets

2,318

Long-Term Intangible Assets

Other Long-Term Assets

267

230

2,638

2,525

$ 7,462

$ 6,579

LIABILITIES

Accounts Payable

$ 846

$ 726

Short-Term Debt

6

356

1,879

2,014

Long-Term Debt

2,775

2,257

Other Long-Term Liabilities

Total Long-Term Liabilities

3,562

2,993

Total Liabilities

Shareholder’s Equity

Preferred Stock

0

0

Common Shareholder’s Equity

2,021

1,572

2,021

1,572

6 Instructor’s Manual

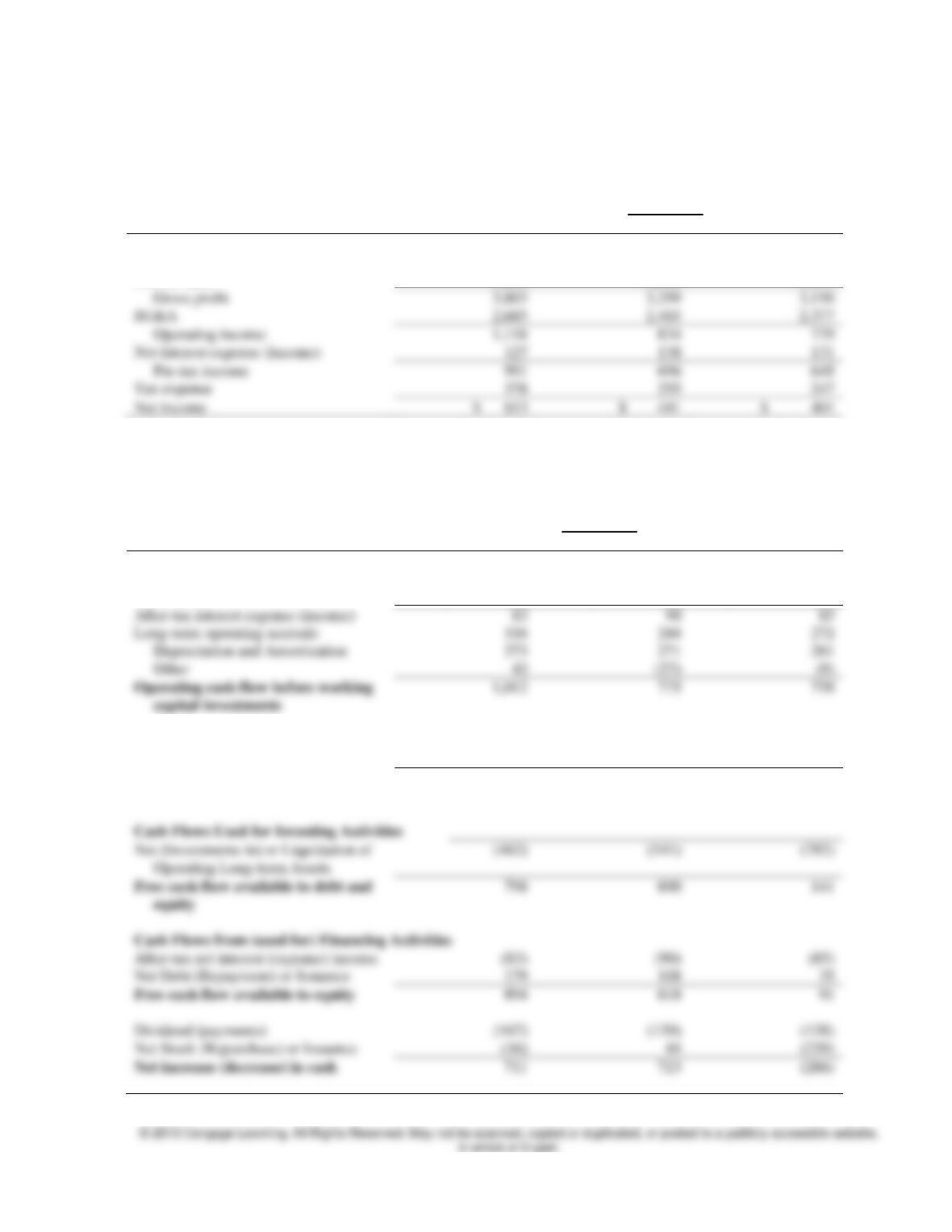

Nordstrom Standardized Income Statement

Fiscal Year

$ in millions

2010

2009

2008

Sales

$ 9,700

$ 8,627

$ 8,573

Cost of sales

5,897

5,328

5,417

Gross profit

3,803

3,299

3,156

SG&A

2,685

2,465

2,377

Operating income

1,118

Net interest expense (income)

Pre-tax income

Tax expense

Net income

Nordstrom Standardized Cash Flow Statement

Fiscal Year

$ in millions

2010

2009

2008

Cash Flows from Operating Activities

Net Income

$ 613

$ 441

$ 401

After-tax interest expense (income)

Long-term operating accruals

Depreciation and Amortization

Other

Operating cash flow before working

capital investments

1,012

775

758

Net (Investments in) or Liquidation of

Operating Working Capital

248

566

175

Operating cash flow before

investment in long-term assets

1,260

1,341

933

Cash Flows Used for Investing Activities

Net (Investments in) or Liquidation of

Operating Long-term Assets

equity

Cash Flows from (used for) Financing Activities

After-tax net interest (expense) income

Net Debt (Repayment) or Issuance

Free cash flow available to equity

Dividend (payments)

Net Stock (Repurchase) or Issuance

Chapter 4 Implementing Accounting Analysis 7

2. Refer to the Creative Technology example on delaying write-downs of current assets. How much excess

inventory do you estimate Creative Technology is holding in March 2005 if the firm’s optimal days’

Inventory is 100 days? Calculate the inventory impairment charge for Creative Technology if 50 percent

of this excess inventory is deemed to be worthless. Record the changes to Creative Technology’s financial

statements from adjusting for this impairment.

Creative Technology’s inventory on March 31, 2005 was $451.2 million, equivalent to 158 days. If

3. U.S.-based American International Group Inc. (AIG) is one of the world’s largest insurance

companies, offering property-casualty, life insurance, and retirement services to customers in more than

130 countries. In its 2010 10-K report to the SEC, it discloses the following information on the loss

reserves created for claims originating in 2000:

(in millions)

Net Reserves Held in 2000: $ 26,971

Cumulative net liability paid as of:

Adjustment

($millions)

Assets

Liabilities &

Equity

Balance Sheet

Inventory

–82.8

Deferred Tax Liability

Income Statement

Cost of Sales

Tax Expense

Net Income

8 Instructor’s Manual

Net reserves for 2000 re-estimated as of:

One year later $ 26,979

Two years later 30,696

Three years later 32,732

Was the initial estimate for loss reserves originating in 2000 too low or too high? How has the

firm updated its estimate of this obligation over time? What percentage of the original liability

remains outstanding for 2000 claims at the end of 2010? As a financial analyst, what

questions would you have for the CFO on its 2000 liability?

The estimate for the 2000 liability made in 2000 was $26.97 billion. As can be seen from the re-

The key questions that an analyst would have about the 2000 liability relates to the fact that the

company ex post underestimated the amount. This could arise for a number of reasons –

a. What were the reasons for the underestimate of the 2000 liability? Did the same factors

affect other firms in the industry? Did the same pattern occur for estimates of liability for

other years?

concerns? Do these give management an incentive to manage liabilities?

Chapter 4 Implementing Accounting Analysis 9

4. AMR, parent of American Airlines, provides the following footnote information on its capital and

operating leases:

AMR’s subsidiaries lease various types of equipment and property, primarily aircraft

Year Ending December 31,

Capital Leases

Operating Leases

2011

$ 186

$ 1,254

2012

136

1,068

2013

120

2014

2015

2016 and thereafter

349

6,006

$ 976

$ 10,804

AMR further disclosed that “lease terms vary but are generally 10 to 25 years for aircraft and seven to 40

years for other leased property and equipment.” Assuming all leases are for aircraft with an average lease

term of 15 years, what interest rate does AMR use to capitalize its capital leases? Use this rate to capitalize

AMR’s operating leases at December 31, 2010. Record the adjustment to AMR’s balance sheet to reflect

the capitalization of operating leases. How would this reporting change affect AMR’s Income Statement

in 2011?

To estimate the interest rate that equates the value of capital lease payments to the reported value of

10 Instructor’s Manual

Year

Reported

Payment

Assumed

Payment

PV factor at

10%

PV

2011

$186

$186

0.9009

$168

2012

136

136

0.8116

110

2013

120

120

0.7312

88

2014

0.6587

64

2015

0.5935

52

2016 and thereafter

349

0.5346

19

0.4817

17

0.4339

15

0.3909

14

0.3522

12

0.3173

11

0.2858

10

0.2575

0.2320

0.2090

$604

For operating leases, the average contract life appears to be longer. This is based on the large

balloon value for lease payments for 2016 and beyond. If we assume that the average life of the

operating leases is 20 years, the present value of operating leases using a 11% discount rate is as

follows:

Year

Reported

Payment

Assumed

Payment

PV factor at

11%

PV

2011

$1,254

$1,254

0.9009

1130

2012

$1,068

0.8116

867

2013

0.7312

711

2014

0.6587

547

2015

0.5935

399

2016 and thereafter

400.4

0.5346

214

400.4

0.4817

193

400.4

0.4339

174

400.4

0.3909

157

400.4

0.3522

141

400.4

0.3173

127

400.4

0.2858

114

400.4

0.2575

103

400.4

0.2320

400.4

0.2090

400.4

0.1883

400.4

0.1696

400.4

0.1528

400.4

0.1240

Chapter 4 Implementing Accounting Analysis 11

The adjusted balance sheet for December 31, 2010 is as follows:

Adjustment Dec. 31, 2010

($ millions)

Assets

Liabilities &

Equity

Balance Sheet

Long-term Tangible Assets

Long-Term Debt

For the year ended December 31, 2010, the impact on net income would be as follows:

Income Statement

Tax Expense (35% of sum)

Net Income

Note: The assumption is made that the lease expense for 2010 is the same as the expected lease

payment for 2011.

5. In 2011, Tata became the first Indian brand to be named in the top 50 global brands in Brand

Finance’s 2011 Global 500 report, which assigned the Tata brand a value of $15.8 billion. What

approaches would you use to estimate the value of brands? What assumptions underlie these

approaches? As a financial analyst, what would you use to assess whether the brand value

assigned by Brand Finance was a reasonable reflection of the future benefits from this brand?

What questions would you raise with the firm’s CFO about the firm’s brand assets?

In thinking about how to estimate brand value, an analyst might use any of the following

approaches. First, one might estimate brand value based on the premium price that company’s

12 Instructor’s Manual

Several assumptions underlie the above brand valuation approaches. First, under the price premium

approach, brands will only have value if: (a) the consumers will continue to value branded products

more highly than non-branded in the foreseeable future, (b) companies continue to maintain the

value of their brands, despite potential competition, and (c) premium prices are accompanied by

higher advertising outlays, so that brands create economic value for shareholders.

An analyst should question the company on the amount of any intangible asset reported on its

balance sheet that relates to its brand. Regardless of what Brand Finance is reporting, if the

company carries an intangible asset related to brand, is the company confident that this asset

6. As the CFO of a company, what indicators would you look at to assess whether your firm’s long-term

assets were impaired? What approaches could be used, either by management or an independent

valuation firm, to assess the dollar value of any asset impairment? As a financial analyst, what indicators

would you look at to assess whether a firm’s long-term assets were impaired? What questions would you

raise with the firm’s CFO about any charges taken for asset impairment?

Impairment is the loss of a significant portion of the utility of an asset through casualty,

obsolescence, or lack of demand for the asset’s service. A loss should be recognized when an asset

Chapter 4 Implementing Accounting Analysis 13

On the other hand, if the firm cannot assess the current market value of the asset, the impairment

loss amount is calculated as the difference between the old net book value and the expected net

present value of the future cash flows.

A financial analyst should look for the same types of indicators that the CFO looks for, of course

understanding that the CFO, as an insider of the company, has a great deal more information about

such issues as casualty, obsolescence, or lack of demand of certain assets. Indicators of impairment

include sustained declines in a firm’s and/or industry’s return on assets relative to its cost of capital,

7. The cigarette industry is subject to litigation for health hazards posed by its products. The industry has

been in an ongoing process of negotiating a settlement of these claims with state and federal governments.

As the CFO for Altria Group, the parent company of Philip Morris, one of the larger firms in the industry,

what information would you report to investors in the annual report on the firm’s litigation risks? How

would you assess whether the firm should record a liability for this risk, and if so, what approach would

you use to assess the value of this liability? As a financial analyst following Philip Morris, what questions

would you raise with the CEO over the firm’s litigation liability?

The litigation risks that Philip Morris faces are reported as contingent liabilities defined in SFAS 5.

Contingent liabilities arise from events or circumstances occurring before the balance sheet date,

Probable – If it is probable that Philip Morris will lose the lawsuit and the loss can be reasonably

estimated, the estimated loss should be reported as a charge to income and as a liability. If the loss

14 Instructor’s Manual

Reasonably possible – Where the likelihood that Philip Morris will lose the lawsuit is reasonably

possible, no amount needs to be accrued as a liability but the nature of the suit needs to be disclosed

in the footnotes of the annual report.

As a financial analyst following Philip Morris I would push the CEO for as much information as

possible about the likelihood that the company will lose the lawsuits or come to a settlement with

the claimants. This requires that the analysts understand the law and case history for the industry. It

also requires information on the company’s plans to either take the cases to trial or to settle, as well

as the costs of a legal battle, the company’s assessment of its chances of victory, and the costs of a

potential settlement.

8. Refer to the Lufthansa example on asset depreciation estimates. What adjustments would be required

if Lufthansa’s aircraft depreciation were computed using an average life of 25 years and salvage value of

5% (instead of the reported values of 12 years and 15%)? Show the adjustments to the 2008 and 2009

balance sheets, and to the 2009 income statement.

If Lufthansa used a 25-year average aircraft life (rather than 12 years) and a 5% salvage value

Chapter 4 Implementing Accounting Analysis 15

The adjustments to the financial statements would therefore be as follows:

Adj. for Dec. 31, 2008

Adj. for Dec. 31, 2009

(€millions)

Assets

Liabilities &

Equity

Assets

Liabilities &

Equity

Balance Sheet

Long-term Tangible Assets

Deferred Tax Liability

+3,182

+3,182

+302

Adj. for Dec. 31, 2009

Assets

Liabilities &

Equity

Income Statement

Depreciation & Amortization Expense

Tax Expense

Net Income

16 Instructor’s Manual

9. In early 2003, Bristol-Myers Squibb announced that it would have to restate its financial statements as

a result of stuffing as much as $3.35 billion worth of products into wholesalers’ warehouses from 1999

through 2001. The company’s sales and cost of sales during this period was as follows:

2001

2000

1999

Net sales

Cost of products sold

The company’s marginal tax rate during the three years was 35%. What adjustments are required to

correct Bristol-Myers Squibb’s balance sheet for December 31, 2001? What assumptions underlie your

adjustments? How would you expect the adjustments to affect Bristol-Myers Squibb’s performance in the

coming few years?

In the Bristol-Myers Squibb example, the firm’s Accounts Receivable, Sales, and Income are

Adjustments for Dec.31, 2001

($billions)

Assets

Liabilities & Equity

Balance Sheet

Accounts Receivable

Inventory

Deferred Taxes

Income Statement

Sales

Cost of Sales

Tax Expense

Net Income