Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 1 (continued)

July 22, 2021

Cash

2,300

Service Revenue (Clinic)

2,300

(Receive cash for mountain bike clinic)

July 24, 2021

Advertising Expense

Cash

(Pay cash for advertising)

July 30, 2021

Cash

4,000

Deferred Revenue

4,000

(Receive cash in advance for kayak clinic)

Aug. 1, 2021

Debit

Credit

Cash

30,000

Notes Payable

30,000

(Obtain loan from city council)

Aug. 4, 2021

Equipment (Kayaks)

28,000

Cash

28,000

(Pay cash for kayaks)

Aug. 10, 2021

Cash

3,000

Deferred Revenue

4,000

Service Revenue (Clinic)

7,000

(Receive cash and hold kayak clinic)

Aug. 17, 2021

Cash

Service Revenue (Clinic)

10,500

(Receive cash and hold kayak clinic)

Accounts Payable

Cash

1,800

(Pay cash on account)

Chapter 3 – The Accounting Cycle: End of the Period

3-118 Financial Accounting, 5e

Additional Perspective 3-1 (continued)

Requirement 1 (concluded)

Sep. 1, 2021

Prepaid Rent

2,400

Cash

2,400

(Pay cash for one-year rental policy)

Sep. 21, 2021

Cash

Service Revenue (Clinic)

(Receive cash for rock climbing clinic)

Oct. 17, 2021

Cash

Service Revenue (Clinic)

(Receive cash for orienteering clinic)

Dec. 8, 2021

Miscellaneous Expense

1,200

Cash

1,200

(Pay cash for race permit)

Dec. 12, 2021

Supplies (Racing)

2,800

Accounts Payable

2,800

(Purchase racing supplies on account)

Dec. 15, 2021

Cash

Dec. 16, 2021

2,000

Dec. 31, 2021

Dividend

4,000

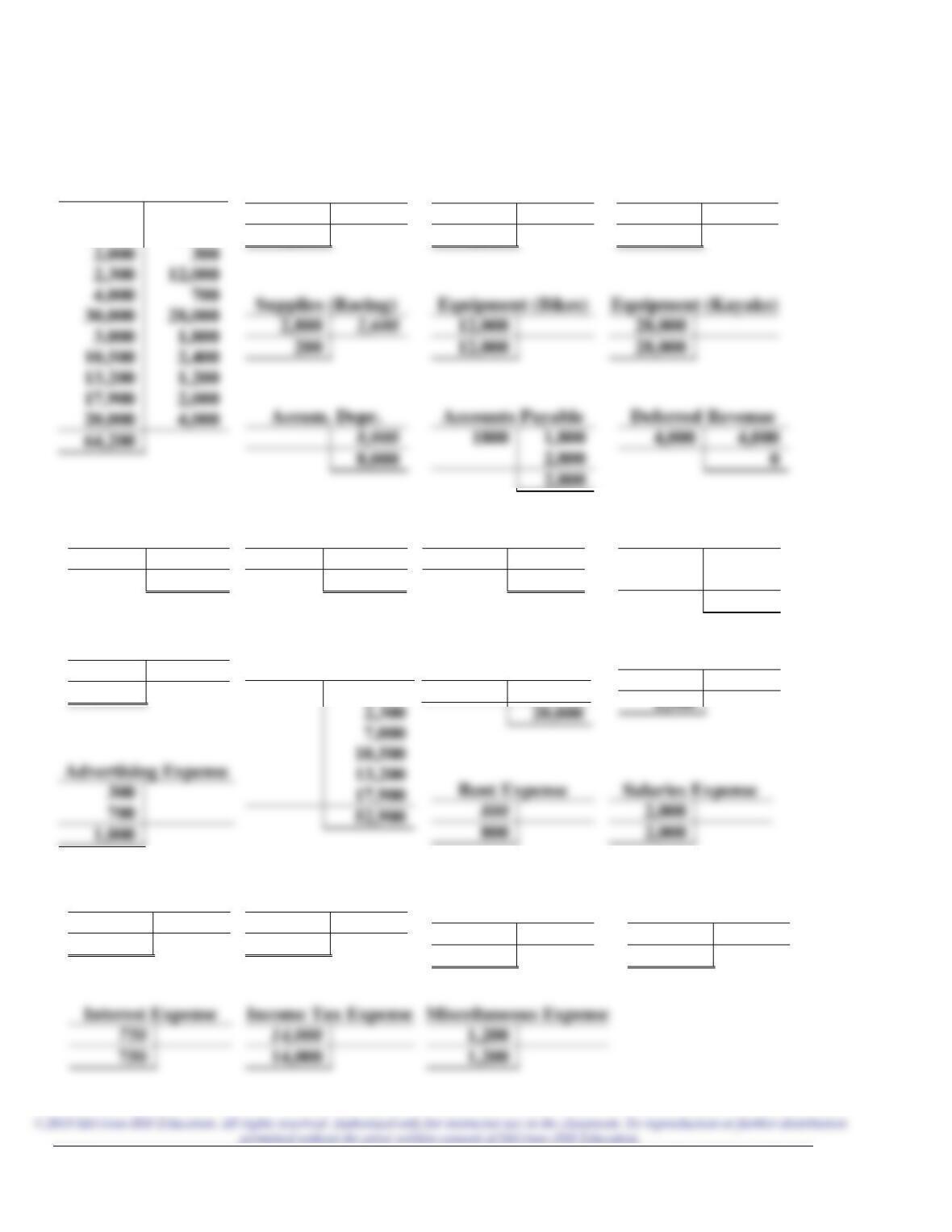

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 2

Dec. 31, 2021

Debit

Credit

Depreciation Expense

8,000

Accumulated Depreciation

8,000

Dec. 31, 2021

Insurance Expense

2,400

Prepaid Insurance

2,400

Dec. 31, 2021

Rent Expense

(Reduce prepaid rent for four months used

Dec. 31, 2021

Supplies Expense (Office)

1,500

Supplies (Office)

1,500

(Office supplies used; $1,800 – $300 =

$1,500)

Dec. 31, 2021

Interest Payable

(Accrue five months interest not yet paid;

Supplies Expense (Racing)

Supplies (Racing)

2,600

(Racing supplies used; $2,800 – $200 =

$2,600)

Income Tax Expense

Income Tax Payable

Chapter 3 – The Accounting Cycle: End of the Period

3-120 Financial Accounting, 5e

Additional Perspective 3-1 (continued)

Requirement 3 (Note: adjusting entries in italics)

Interest Expense

750

14,000

Miscellaneous Expense

Prepaid Insurance

4,800

2,400

2,400

4,000

2,800

2,600

200

8,000

Common Stock

10,000

10,000

20,000

Legal Fees Expense

1,500

1,500

1,000

20,000

Salaries Expense

2,000

2,000

800

Notes Payable

30,000

30,000

Prepaid Rent

2,400

800

1,600

Service Revenue

(Racing)

20,000

Dividends

4,000

4,000

Supplies (Office)

1,800

1,500

300

Interest Payable

750

750

Depr. Expense

8,000

8,000

Insurance Expense

2,400

2,400

Supplies Expense

(Office)

1,500

1,500

Income Tax Payable

14,000

14,000

Service Revenue

(Clinic)

2,000

Supplies Expense

(Racing)

2,600

2,600

Cash

10,000

10,000

4,800

1,500

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 4

Great Adventures, Inc.

Adjusted Trial Balance

December 31, 2021

Accounts

Debit

Credit

Cash

$ 64,200

Prepaid Insurance

2,400

Prepaid Rent

1,600

Supplies (Office)

Supplies (Racing)

Equipment (Bikes)

12,000

Equipment (Kayaks)

28,000

Accumulated Depreciation

Accounts Payable

2,800

Income Tax Payable

14,000

Interest Payable

750

Notes Payable

30,000

Common Stock

20,000

Dividends

4,000

Service Revenue (Clinic)

52,900

Service Revenue (Racing)

20,000

Advertising Expense

1,000

Depreciation Expense

8,000

Income Tax Expense

Insurance Expense

2,400

Interest Expense

Legal Fees Expense

1,500

Miscellaneous Expense

1,200

Rent Expense

Salaries Expense

2,000

Supplies Expense (Office)

1,500

Supplies Expense (Racing)

2,600

$148,450

$148,450

Chapter 3 – The Accounting Cycle: End of the Period

3-122 Financial Accounting, 5e

Additional Perspective 3-1 (continued)

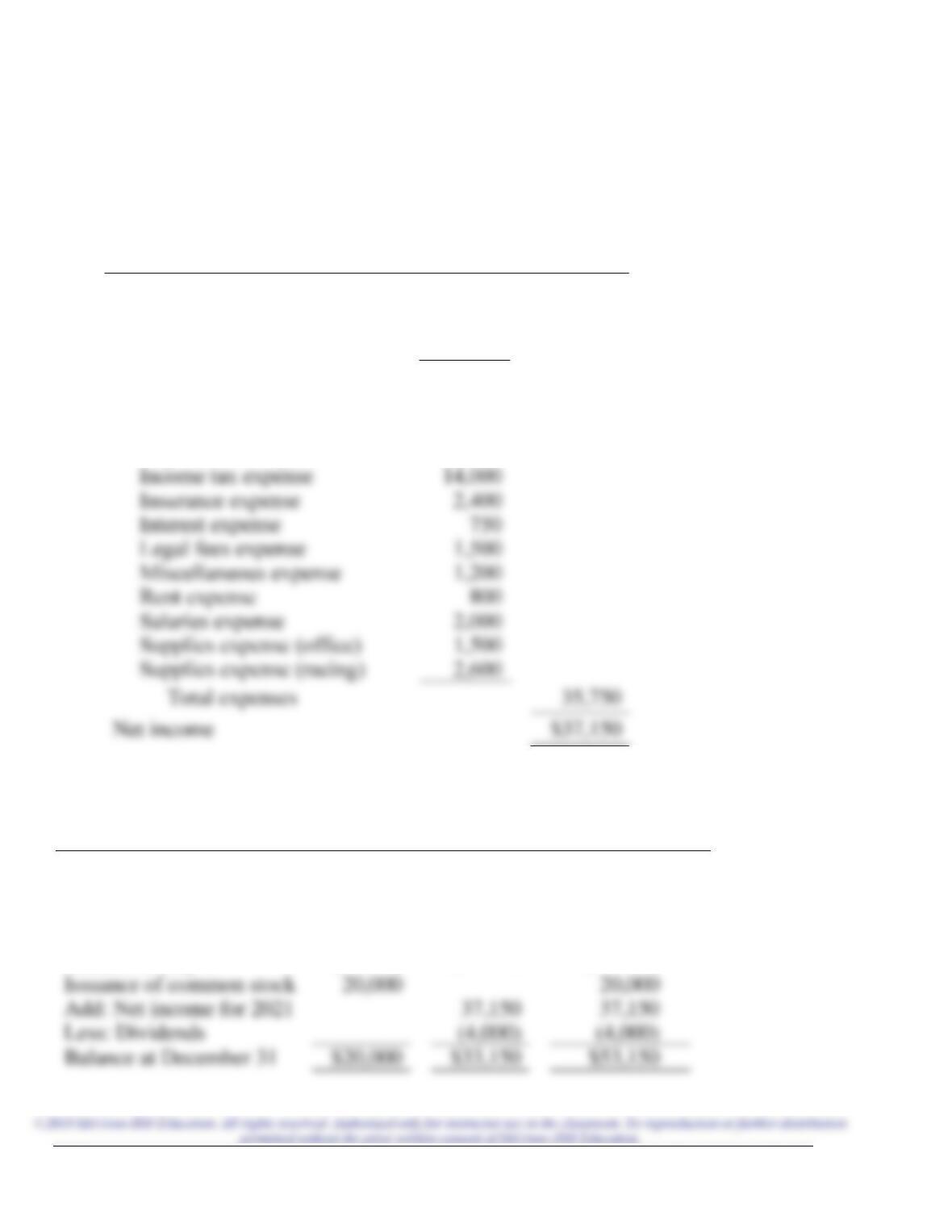

Requirement 5

Great Adventures, Inc.

Income Statement

For the period ended December 31, 2021

Revenues:

Service revenue (clinic)

$52,900

Service revenue (racing)

20,000

Total revenues

$72,900

Expenses:

Advertising expense

1,000

Depreciation expense

8,000

Insurance expense

2,400

Interest expense

Legal fees expense

1,500

Miscellaneous expense

1,200

Salaries expense

2,000

Supplies expense (office)

1,500

Supplies expense (racing)

2,600

Net income

Great Adventures, Inc.

Statement of Stockholders’ Equity

For the period ended December 31, 2021

Common

Stock

Retained

Earnings

Total

Stockholders’

Equity

Balance at July 1

$ 0

$ 0

$ 0

Issuance of common stock

Add: Net income for 2021

Less: Dividends

Balance at December 31

$20,000

$33,150

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 5 (concluded)

Great Adventures, Inc.

Balance Sheet

December 31, 2021

Assets

Liabilities

Current assets:

Current liabilities:

Cash

$ 64,200

Accounts payable

$ 2,800

Prepaid insurance

2,400

Interest payable

750

Prepaid rent

1,600

Income tax payable

Supplies (office)

Supplies (racing)

Long-term assets:

Equipment (bikes)

Equipment (kayaks)

Total assets

$100,700

Chapter 3 – The Accounting Cycle: End of the Period

3-124 Financial Accounting, 5e

Additional Perspective 3-1 (continued)

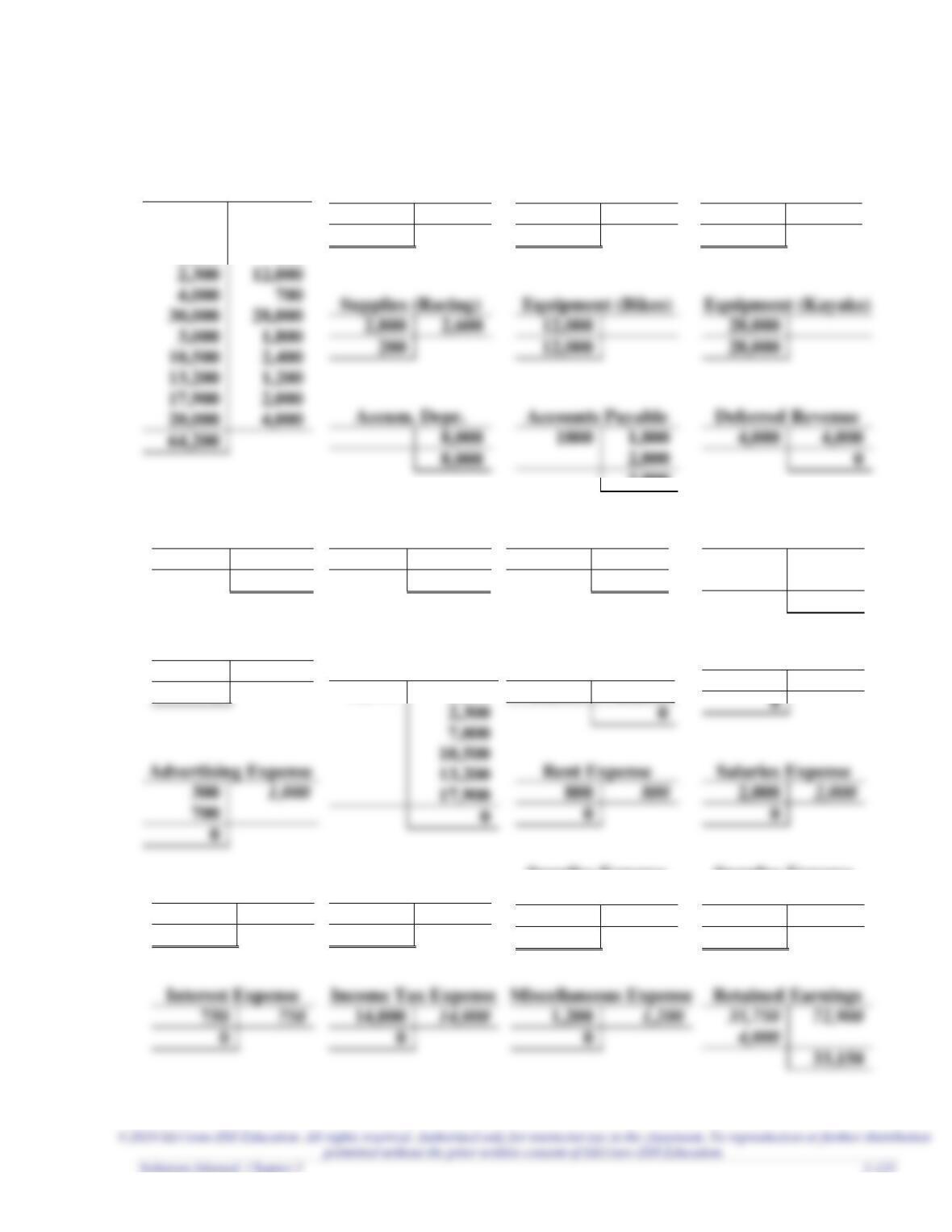

Requirement 6

Dec. 31, 2021

Debit

Credit

Service Revenue (Clinic)

52,900

Service Revenue (Racing)

20,000

Retained Earnings

72,900

(Close revenue accounts)

Dec. 31, 2021

Retained Earnings

35,750

Advertising Expense

1,000

Depreciation Expense

8,000

Income Tax Expense

14,000

Insurance Expense

2,400

Interest Expense

Legal Fees Expense

1,500

Miscellaneous Expense

1,200

Rent Expense

Salaries Expense

2,000

Supplies Expense (Office)

1,500

Supplies Expense (Racing)

2,600

(Close expense accounts)

Dec. 31, 2021

Dividends

(Close dividends account)

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 7 (Note: closing entries in italics)

Interest Expense

750

0

14,000

0

33,150

Miscellaneous Expense

1,200

Prepaid Insurance

4,800

2,400

2,400

Equipment (Bikes)

12,000

12,000

4,000

28,000

28,000

2,800

2,600

200

Accum. Depr.

8,000

8,000

64,200

2,800

Common Stock

10,000

10,000

20,000

Legal Fees Expense

1,500

1,500

0

Advertising Expense

0

Salaries Expense

2,000

2,000

0

Rent Expense

800

0

Notes Payable

30,000

30,000

Prepaid Rent

2,400

800

1,600

Service Revenue

(Racing)

20,000

20,000

Dividends

4,000

4,000

0

Supplies (Office)

1,800

1,500

300

Interest Payable

750

750

Depr. Expense

8,000

8,000

0

Insurance Expense

2,400

2,400

0

Supplies Expense

(Office)

1,500

1,500

0

Supplies Expense

(Racing)

2,600

2,600

0

Income Tax Payable

14,000

14,000

Service Revenue

(Clinic)

52,900

2,000

Cash

10,000

10,000

2,000

4,800

1,500

300

Chapter 3 – The Accounting Cycle: End of the Period

3-126 Financial Accounting, 5e

Additional Perspective 3-1 (concluded)

Requirement 8

Great Adventures, Inc.

Post-closing Trial Balance

December 31, 2021

Accounts

Debit

Credit

Cash

$ 64,200

Prepaid Insurance

2,400

Prepaid Rent

1,600

Supplies (Office)

300

Supplies (Racing)

200

Equipment (Bikes)

Equipment (Kayaks)

Accumulated Depreciation

Accounts Payable

2,800

Income Tax Payable

Interest Payable

750

Notes Payable

Common Stock

Retained Earnings

$108,700

$108,700

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-2

American Eagle

($ in thousands)

Requirement 1

Requirement 3

The change in retained earnings is $107,817 (= $1,883,592 − $1,775,775).

Requirement 4

The amount of net income is $204,163.

Requirement 5

The change in retained earnings typically represents net income for the year less

Chapter 3 – The Accounting Cycle: End of the Period

3-128 Financial Accounting, 5e

Additional Perspective 3-3

Buckle

($ in thousands)

Requirement 1

0.67 (= $97,906 / $146,868).

Requirement 3

The change in retained earnings is $(44,167) (= $246,570 − $290,737).

Requirement 4

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-4

Compare American Eagle and Buckle

Requirement 1

Buckle has the higher ratio of current assets to total assets. For American Eagle, the

Requirement 2

American Eagle has the higher ratio of current liabilities to total liabilities. For

Requirement 3

Buckle has a higher dividend payout ratio. For American Eagle, the dividend payout

ratio is 0.45 (= $90,858 / $204,163). For Buckle, the dividend payout ratio is 1.49 (=

Chapter 3 – The Accounting Cycle: End of the Period

3-130 Financial Accounting, 5e

Additional Perspective 3-5

1. Profits are overstated.

2. Liability.

3. Yes.

Next year the $80,000 cannot be counted again in pretax profits, likely causing a big

4. No.

As the assistant controller (accountant), you should understand that your

responsibilities include accurately recording and reporting the company’s activities.

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-6

(Note to instructor: Answers are based on McDonald’s December 2016 annual report,

and dollar amounts are in millions.)

Requirement 1

Revenues exceed expenses because the company reports net income of $4,686.5 (in

millions).

Requirement 2

Requirement 4

Current liabilities include accounts payable, income taxes, other taxes, accrued

interest, and accrued payroll and other liabilities. Other liabilities include liabilities

that are due in more than one year.

Requirement 5

Retained earnings increased $1,628.2, from $44,594.5 to $46,222.7.

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-7

Requirement 1

Prepaid revenues occur when cash is received before the related revenues are reported.

Requirement 2

The adjusting entry for prepaid expenses includes a debit to an expense and a credit to

Requirement 3

The adjusting entry for accrued expenses includes a debit to an expense and a credit to