Chapter 3 – The Accounting Cycle: End of the Period

Chapter 3

The Accounting Cycle: End of the Period

REVIEW QUESTIONS

Question 3-1 (LO 3-1)

The revenue recognition principle states that we record revenue in the period in which we

Question 3-2 (LO 3-1)

The concept of expense recognition suggests that we recognize expenses in the same period as

Question 3-3 (LO 3-1)

Net income is an important profitability measure used by investors, creditors, and others in

Question 3-4 (LO 3-2)

Under cash-basis accounting, revenues are recorded when cash is received and expenses are

Question 3-5 (LO 3-2)

(1) April 10th.

Question 3-6 (LO 3-2)

(1) March 28th.

Chapter 3 – The Accounting Cycle: End of the Period

3-2 Financial Accounting, 5e

Answers to Review Questions (continued)

Question 3-7 (LO 3-2)

(1) April 10th.

Question 3-8 (LO 3-2)

(1) March 28th.

Question 3-9 (LO 3-3)

One of the primary purposes of adjusting entries is to allow for proper application of the revenue

Question 3-10 (LO 3-3)

Prepayments are cases where cash is received before revenue is recognized or where cash is paid

Question 3-11 (LO 3-3)

A prepaid expense includes the purchase of supplies, prepaid insurance, and prepaid rent. At the

Question 3-12 (LO 3-3)

Deferred revenue includes a customer paying cash before receiving the related product or

Question 3-13 (LO 3-3)

An accrued expense includes incurring an expense before the related cash outflow, such as when

Question 3-14 (LO 3-3)

An accrued revenue includes recording a revenue before the related cash inflow, such as

Chapter 3 – The Accounting Cycle: End of the Period

Answers to Review Questions (continued)

Question 3-15 (LO 3-3)

October 31

Debit

Credit

Question 3-16 (LO 3-3)

Yes. Utilities expense and utilities payable will be understated at the end of September. Utilities

Question 3-17 (LO 3-3)

November 30

Debit

Credit

Question 3-18 (LO 3-3)

Yes. Accounts receivable and service revenue will be understated at the end of May. Accounts

Question 3-19 (LO 3-3)

(a) Prepaid expense: Debit Supplies Expense; credit Supplies.

Question 3-20 (LO 3-4)

The purpose of the adjusted trial balance is to list all accounts and their balances after updating

Question 3-21 (LO 3-5)

Classified indicates that assets are separated into those that provide a benefit over the next year

Chapter 3 – The Accounting Cycle: End of the Period

3-4 Financial Accounting, 5e

Answers to Review Questions (continued)

Question 3-22 (LO 3-5)

Assets

=

Liabilities

+

Stockholders’

equity

$12,000

=

$8,000

+

$X

$12,000

$8,000

=

Question 3-23 (LO 3-6)

The two purposes of closing entries are (1) to transfer the balances of temporary accounts

Question 3-24 (LO 3-6)

To “close” temporary accounts indicates that temporary account balances should be reduced to zero

Question 3-25 (LO 3-6)

The first closing entry transfers revenue transactions to retained earnings by debiting all revenue

accounts (reducing their balances to zero) and crediting retained earnings. The second closing entry

Question 3-26 (LO 3-6)

Net Income

Dividends

Retained

Earnings*

Year 1

$ 300

$200

$ 100

Year 3

Year 4

Chapter 3 – The Accounting Cycle: End of the Period

Answers to Review Questions (continued)

Question 3-27 (LO 3-6)

It is important to understand that transactions are recorded from the company’s perspective. The

Question 3-28 (LO 3-7)

The adjusted trial balance does not include the effect of closing entries while the post-closing

trial balance does. This means that revenues, expenses, and dividends will be reported in the adjusted

Chapter 3 – The Accounting Cycle: End of the Period

3-6 Financial Accounting, 5e

BRIEF EXERCISES

Brief Exercise 3-1 (LO 3-1)

(a) $0; Cash received in advance is recorded as Deferred revenue (liability).

Brief Exercise 3-2 (LO 3-1)

(a) $600.

Brief Exercise 3-3 (LO 3-1)

Chapter 3 – The Accounting Cycle: End of the Period

Brief Exercise 3-4 (LO 3-1, 3-2)

Impact on:

Cash

Balance

Cash-basis

Net Income

Accrual-basis

Net Income

(a)

Receive $1,500 from

customers who were billed

for services in April.

+$1,500

+$1,500

$0

(d)

Pay $600 to workers. $400 is

for work in May and $200 is

for work in April.

−$600

−$600

−$400

Pay $200 to advertise in a

local newspaper in May.

Brief Exercise 3-5 (LO 3-1, 3-2)

Cash-basis

net income

Accrual

adjustments

Accrual-basis

net income

Cash inflows

$50,000

+$6,900*

$56,900

Cash outflows

Chapter 3 – The Accounting Cycle: End of the Period

3-8 Financial Accounting, 5e

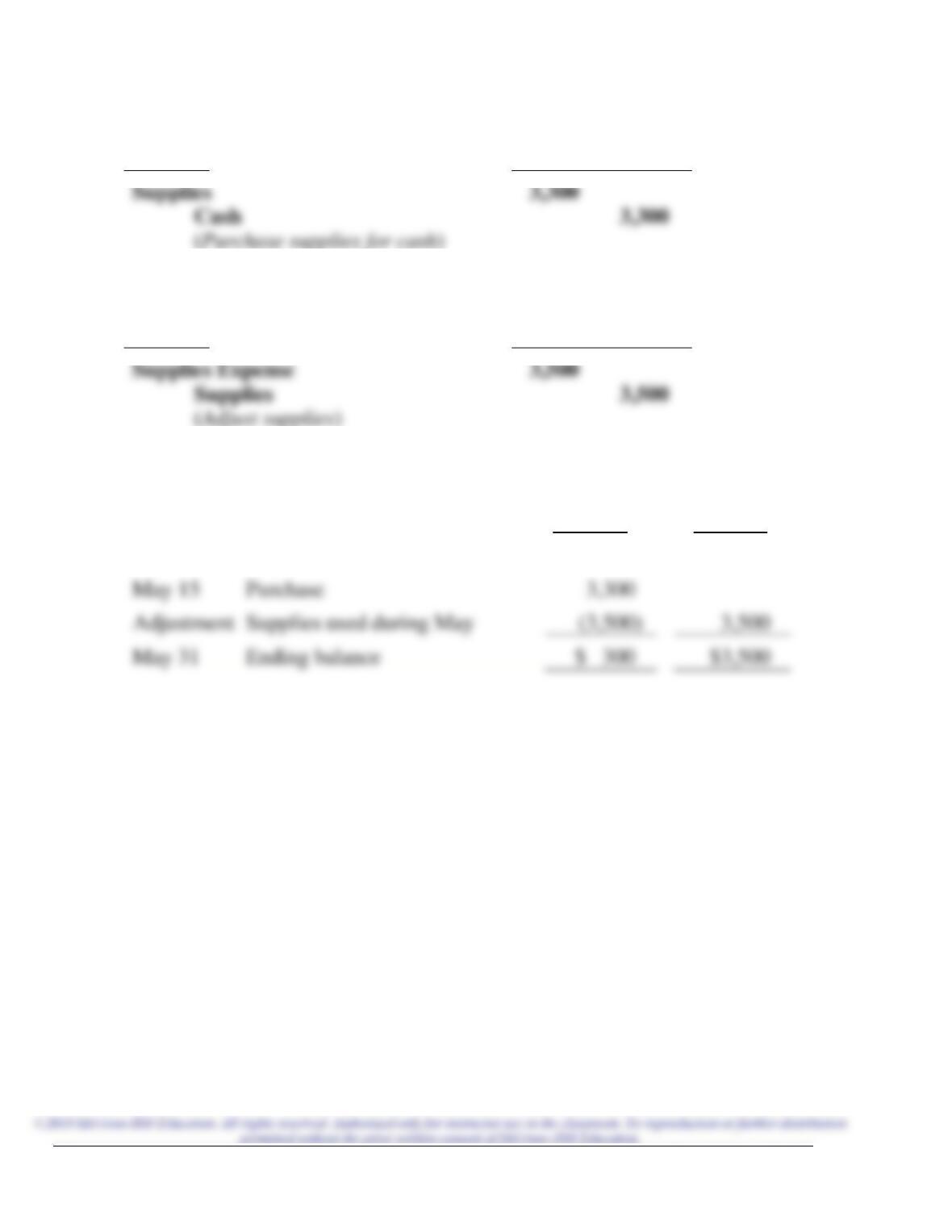

Brief Exercise 3-6 (LO 3-3)

(1)

May 15

Debit

Credit

(2)

May 31

Debit

Credit

(3)

Supplies

Supplies

Expense

May 1

Beginning balance

$ 500

$ 0

May 15

Purchase

Adjustment

Supplies used during May

May 31

Ending balance

Chapter 3 – The Accounting Cycle: End of the Period

Brief Exercise 3-7 (LO 3-3)

(1)

Oct. 1

Debit

Credit

(2)

Dec. 31

Debit

Credit

(3)

Prepaid

Rent

Rent

Expense

Jan. 1

Beginning balance

$ 0

$ 0

Oct. 1

Payment

Dec. 31

Ending balance

Chapter 3 – The Accounting Cycle: End of the Period

3-10 Financial Accounting, 5e

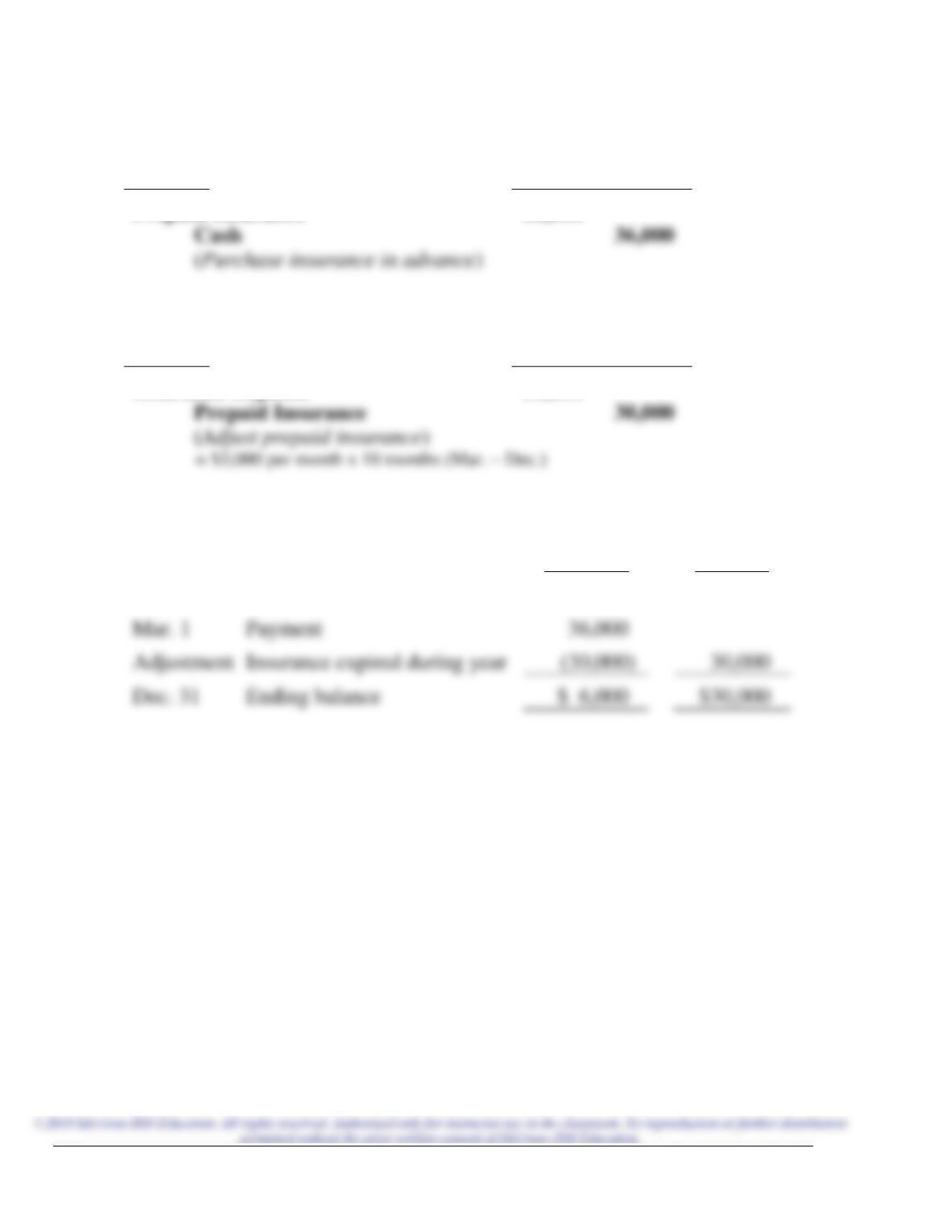

Brief Exercise 3-8 (LO 3-3)

(1)

Mar. 1

Debit

Credit

Prepaid Insurance

36,000

(2)

Dec. 31

Debit

Credit

Insurance Expense

30,000

(3)

Prepaid

Insurance

Insurance

Expense

Jan. 1

Beginning balance

$ 0

$ 0

Mar. 1

Payment

Dec. 31

Ending balance

$ 6,000

$30,000

Chapter 3 – The Accounting Cycle: End of the Period

Brief Exercise 3-9 (LO 3-3)

(1)

Apr. 1

Debit

Credit

(2)

Dec. 31

Debit

Credit

(3)

Accumulated

Depreciation

Depreciation

Expense

Jan. 1

Beginning balance

$ 0

$ 0

Adjustment

Depreciation during year

Dec. 31

Ending balance

Chapter 3 – The Accounting Cycle: End of the Period

3-12 Financial Accounting, 5e

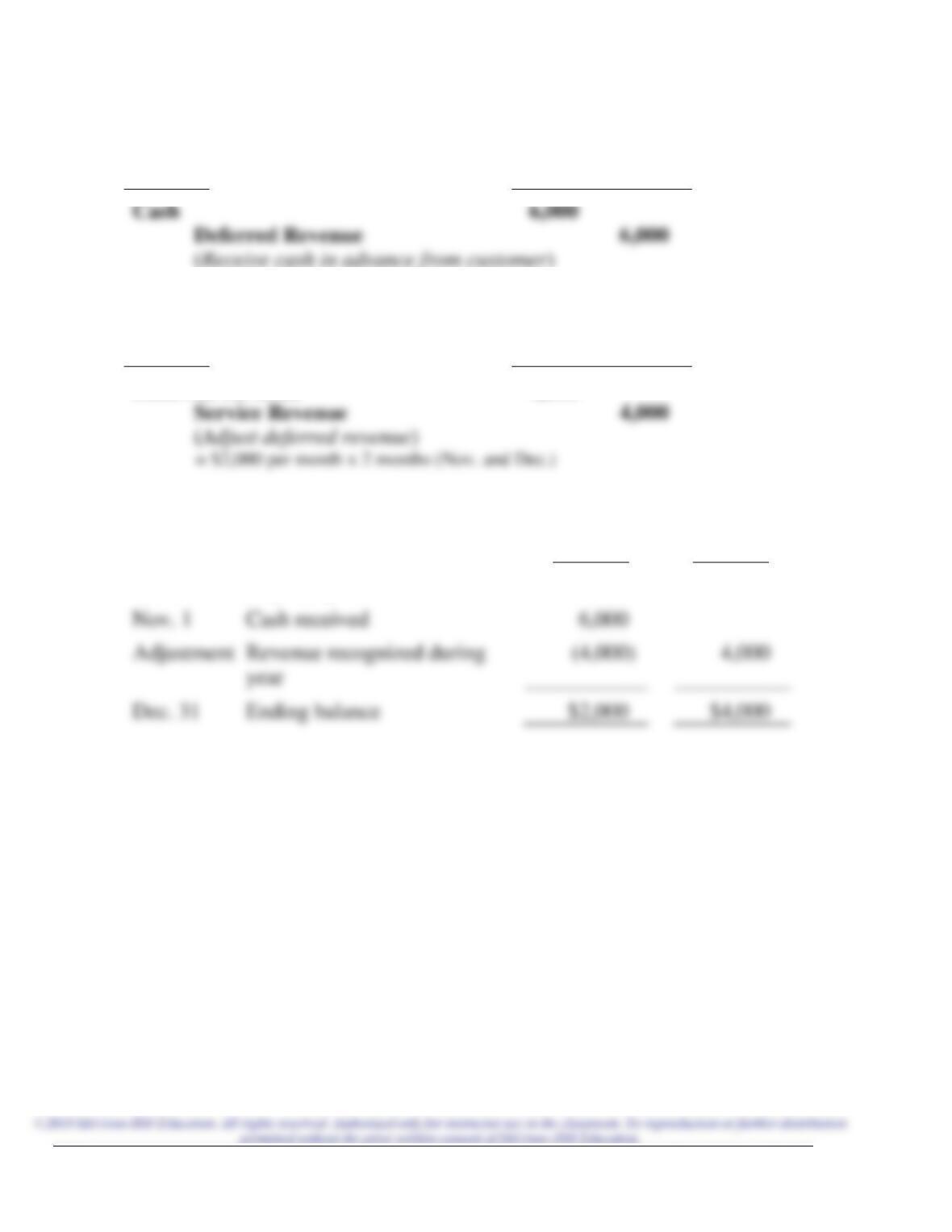

Brief Exercise 3-10 (LO 3-3)

(1)

Nov. 1

Debit

Credit

(2)

Dec. 31

Debit

Credit

Deferred Revenue

4,000

(3)

Deferred

Revenue

Service

Revenue

Jan. 1

Beginning balance

$ 0

$ 0

Nov. 1

Cash received

year

Dec. 31

Ending balance

$4,000

Chapter 3 – The Accounting Cycle: End of the Period

Brief Exercise 3-11 (LO 3-3)

(1)

Dec. 31, 2021

Debit

Credit

Salaries Expense

1,200

(2)

Salaries

Payable

Jan. 1, 2021

Beginning balance

$ 0

Adjustment

Salaries incurred but not paid

Dec. 31, 2021

Ending balance

Chapter 3 – The Accounting Cycle: End of the Period

3-14 Financial Accounting, 5e

Brief Exercise 3-12 (LO 3-3)

(1)

Jul. 1, 2021

Debit

Credit

Cash

(2)

Dec. 31, 2021

Debit

Credit

Interest Expense

900

(3)

Interest

Payable

Interest

Expense

Jan. 1, 2021

Beginning balance

$ 0

$ 0

Adjustment

Interest incurred but not paid

Dec. 31, 2021

Ending balance

Brief Exercise 3-13 (LO 3-3)

(1)

Jul. 1, 2021

Debit

Credit

(2)

Dec. 31, 2021

Debit

Credit

Interest Receivable

900

Chapter 3 – The Accounting Cycle: End of the Period

(3)

Interest

Receivable

Interest

Revenue

Jan. 1, 2021

Beginning balance

$ 0

$ 0

Adjustment

Interest earned but not received

Dec. 31, 2021

Ending balance

Chapter 3 – The Accounting Cycle: End of the Period

3-16 Financial Accounting, 5e

Brief Exercise 3-14 (LO 3-5)

Account

Financial Statement

1.

Accounts Receivable

Balance Sheet

2.

Deferred Revenue

Balance Sheet

4.

Salaries Payable

Balance Sheet

5.

Depreciation Expense

6.

Service Revenue

Brief Exercise 3-15 (LO 3-5)

1.

(b)

3.

Chapter 3 – The Accounting Cycle: End of the Period

Brief Exercise 3-16 (LO 3-5)

Beavers Corporation

Income Statement

For the year ended December 31, 2021

Service revenue

$275,000

Expenses:

Net income

Brief Exercise 3-17 (LO 3-5)

Spiders Corporation

Statement of Stockholders’ Equity

For the year ended December 31, 2021

Common

Stock

Retained

Earnings

Total

Stockholders’

Equity

Balance at January 1

$30,000

$ 8,000

$38,000

Issuance of common stock

Less: Dividends

Balance at December 31

$30,000

$40,000

3-18 Financial Accounting, 5e

Blue Devils Corporation

Balance Sheet

December 31, 2021

Assets

Liabilities

Current assets:

Current liabilities:

Cash

$ 5,000

Accounts payable

$ 26,000

Supplies

Long-term assets:

Common stock

Equipment

Retained earnings

Accumulated depr.

$108,000

Total assets

*

Assets

=

Liabilities

+

Stockholders’ equity

$108,000

=

+

$108,000

$6,000

Chapter 3 – The Accounting Cycle: End of the Period

Brief Exercise 3-19 (LO 3-6)

December 31

Debit

Credit

Service Revenue

900,000

Retained Earnings

900,000

(Close revenue accounts)

Retained Earnings

625,000

Rent Expense

(Close expense accounts)

Retained Earnings

Dividends

(Close dividends account)

Brief Exercise 3-20 (LO 3-7)

Hilltoppers Corporation

Post-Closing Trial Balance

Accounts

Debit

Credit

Cash

$ 5,000

Equipment

Accounts Payable

Common Stock

Retained Earnings

* Retained Earnings

(before closing)

+

Revenues

−

Expenses

−

Dividends

=

Retained

Earnings

Chapter 3 – The Accounting Cycle: End of the Period

3-20 Financial Accounting, 5e

EXERCISES

Exercise 3-1 (LO 3-1)

1.

August 16.

2.

January 27.

3.

April 2.

Exercise 3-2 (LO 3-1)

1.

August 16.

2.

January 27.

4.

February 4.

Exercise 3-3 (LO 3-2)

1.

June 12.

3.

April 2.