P3–2

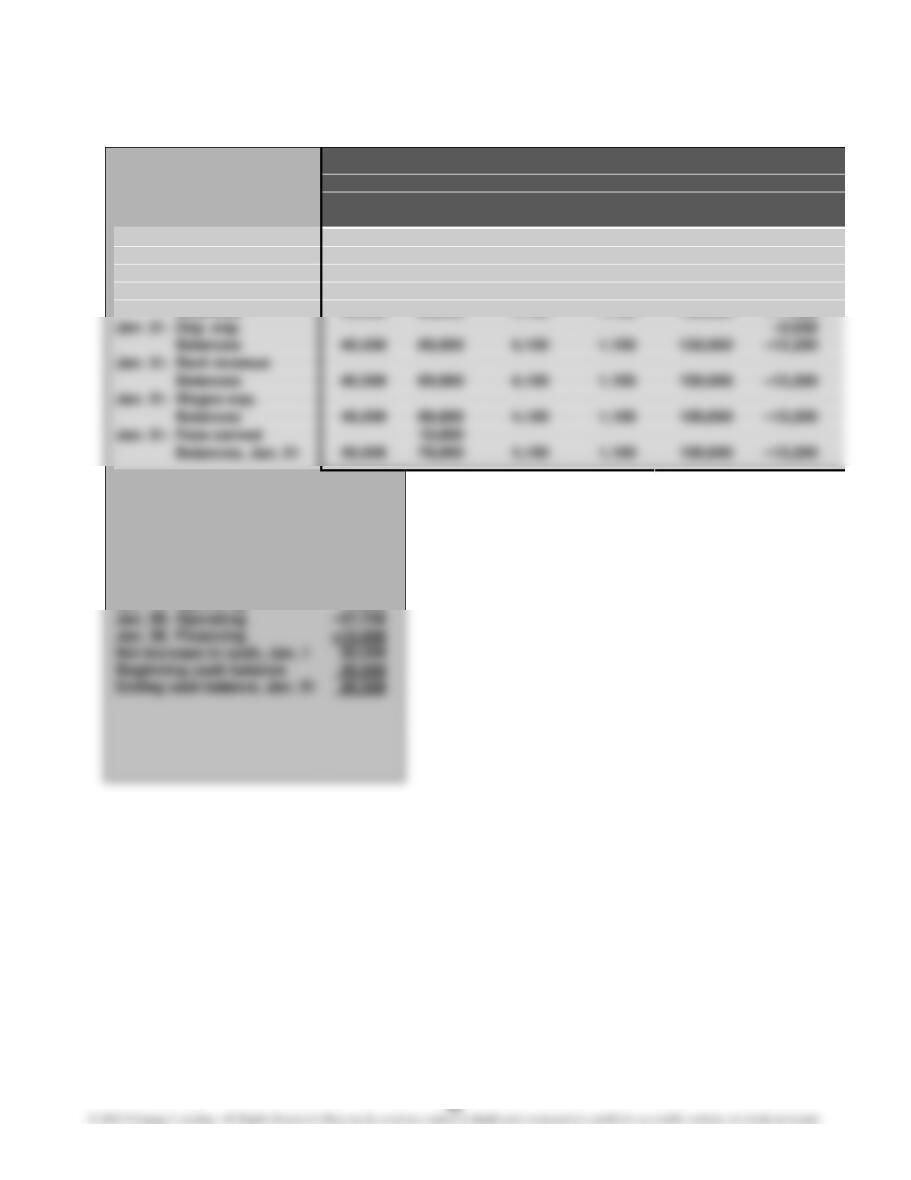

Statement of

Balance

Cash Flows

Assets

Accts.

Prepaid

Acc.

Cash

+

Rec.

+

Insurance

+

Supplies

+

Building

–

Depr.

+

Balances

40,500

69,000

4,900

2,800

150,000

–11,200

Jan. 31.

Insurance exp.

–800

Balances

40,500

69,000

4,100

2,800

150,000

–11,200

Jan. 31.

Supplies exp.

–1,700

Balances

40,500

69,000

4,100

1,100

150,000

–11,200

Jan. 31.

Dep. exp.

Balances

40,500

69,000

4,100

1,100

150,000

–13,200

Jan. 31.

Rent revenue

Balances

40,500

69,000

4,100

1,100

–13,200

Jan. 31.

Wages exp.

Balances

40,500

69,000

4,100

1,100

–13,200

Jan. 31.

Fees earned

10,000

Balances, Jan. 31

40,500

79,000

4,100

1,100

–13,200

Statement of Cash Flows

Jan. 1.

Operating

15,000

Jan. 1.

Operating

–4,200

Jan. 9.

Operating

27,500

Jan. 11.

Operating

–3,000

Jan. 18.

Financing

25,000

Jan. 25.

Operating

12,900

Jan. 30.

Operating

Jan. 30.

Financing

Net increase in cash, Jan. 1

20,500

20,000

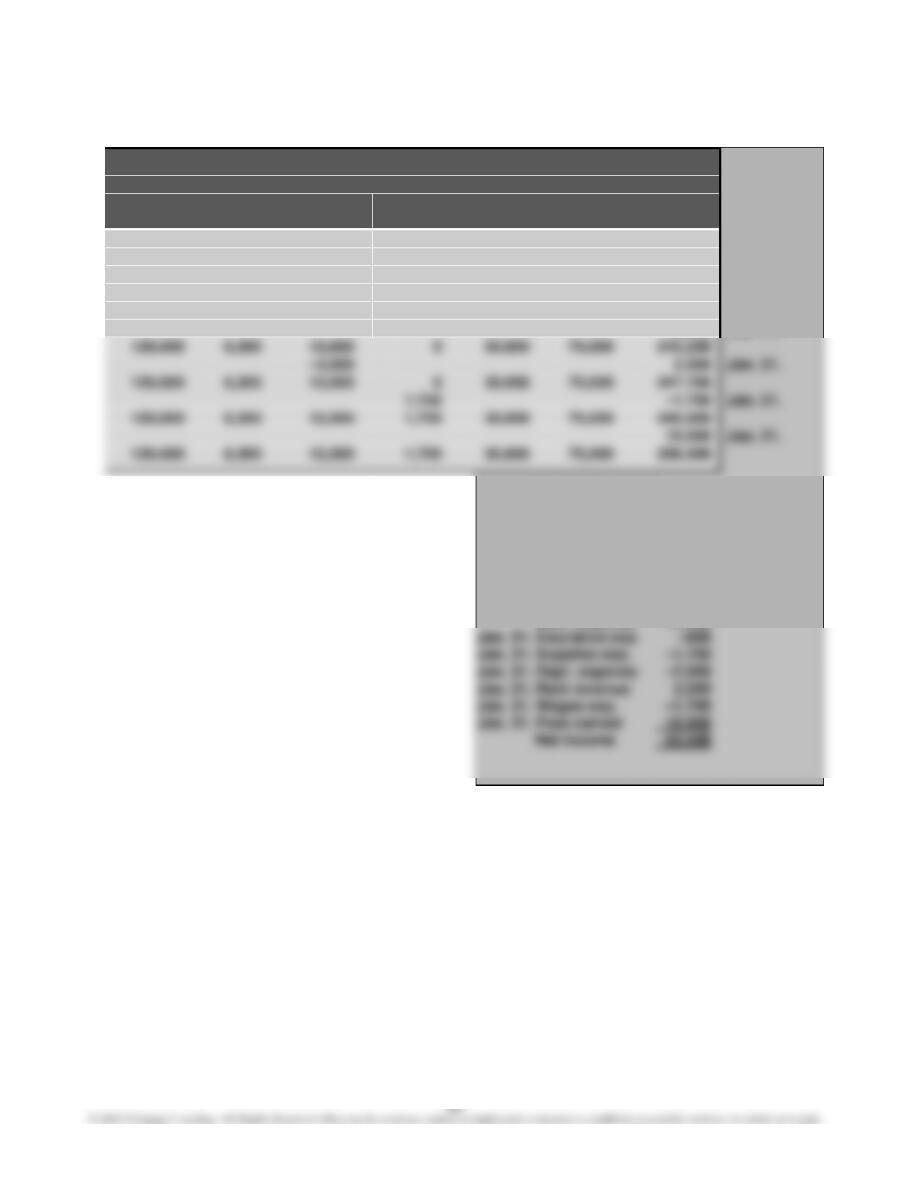

P3–2, Concluded

Sheet

Income

=

Liabilities

+

Stockholders’ Equity

Statement

Accts.

Unearned

Wages

Notes

Capital

Retained

+

Land

=

Payable

+

Revenue

+

Payable

+

Payable

+

Stock

+

Earnings

120,000

6,300

15,000

0

30,000

75,000

249,700

–800

Jan. 31.

120,000

6,300

15,000

0

30,000

75,000

248,900

–1,700

Jan. 31.

120,000

6,300

15,000

0

30,000

75,000

247,200

–2,000

Jan. 31.

120,000

6,300

15,000

0

30,000

75,000

245,200

2,500

Jan. 31.

120,000

6,300

12,500

0

30,000

75,000

247,700

1,700

–1,700

Jan. 31.

120,000

6,300

12,500

1,700

30,000

75,000

246,000

10,000

Jan. 31.

120,000

6,300

12,500

1,700

30,000

75,000

256,000

Income Statement

Jan. 20. Fees earned

62,000

Jan. 25. Fees earned

12,900

Jan. 30. Wages exp.

–24,000

Utilities exp.

–6,000

Rent expense

–5,000

Interest exp.

–200

Misc. expense

–2,500

Jan. 31. Insurance exp.

–800

Jan. 31. Supplies exp.

–1,700

Jan. 31. Depr. expense

–2,000

Jan. 31. Rent revenue

Jan. 31. Wages exp.

–1,700

Jan. 31. Fees earned

10,000

P3–3

OASIS HEALTH CARE, INC.

Income Statement

For the Month Ended January 31, 20Y5

Fees earned …………………………………………………………… $84,900

Operating expenses:

Wages expense …………………………………………………. $25,700

Utilities expense ……………………………………………….. 6,000

Rent expense ……………………………………………………. 5,000

Depreciation expense ……………………………………….. 2,000

OASIS HEALTH CARE, INC.

Retained Earnings Statement

For the Month Ended January 31, 20Y5

Retained earnings, January 1, 20Y5 ………………………… $227,500

P3–3, Concluded

OASIS HEALTH CARE, INC.

Balance Sheet

January 31, 20Y5

Assets

Current assets:

Cash ……………………………………………………… $ 40,500

Accounts receivable ………………………………. 79,000

Prepaid insurance …………………………………. 4,100

Supplies ……………………………………………….. 1,100

Liabilities

Current liabilities:

Accounts payable ………………………………….. $ 6,300

Unearned rent ……………………………………….. 12,500

Wages payable ………………………………………. 1,700

Total current liabilities ………………………. $ 20,500

P3–4

1. OASIS HEALTH CARE, INC.

Statement of Cash Flows

For the Month Ended January 31, 20Y5

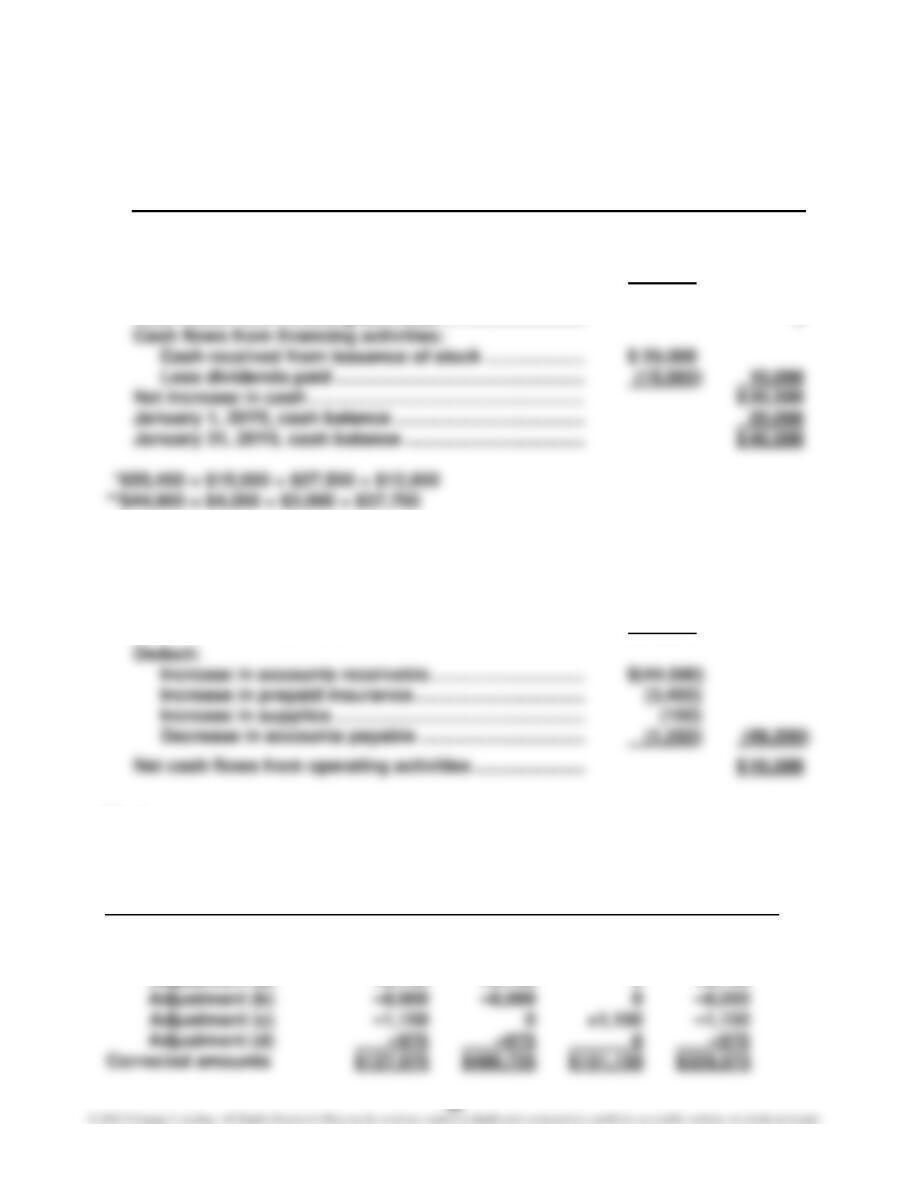

Cash flows from operating activities:

Cash received from customers ………………………….. $ 55,400*

Deduct cash payments for expenses …………………. (44,900)**

Net cash flows from operating activities …………………. $ 10,500

Cash flows from investing activities ……………………….. 0

2. Net income ……………………………………………………………. $ 43,500

Add:

Depreciation expense ……………………………………….. $ 2,000

Increase in unearned revenue ……………………………. 12,500

Increase in wages payable ………………………………… 1,700 16,200

P3–5

Total

Net Total Total Stockholders’

Income Assets Liabilities Equity

Reported amounts $127,500 $480,000 $150,000 $330,000

Corrections:

Adjustment (a) +9,700 +9,700 0 +9,700

1.

Statement of

Balance Sheet

Income

Cash Flows

Assets

=

Liabilities

+

Stockholders’ Equity

Statement

Laundry

Prepaid

Laundry

Acc.

Accts.

Wages

Capital

Retained

Cash

+

Supplies

+

Ins.

+

Equip.

–

Depr.

=

Payable

+

Payable

+

Stock

+

Earnings

Balances, Dec. 31, 2013

53,000

9,000

6,000

250,000

–65,000

7,000

0

50,000

196,000

Dec. 31. (a)

2,150

–2,150

(a)

Dec. 31. (b)

–12,500

–12,500

(b)

Dec. 31. (c)

–7,500

–7,500

(c)

Dec. 31. (d)

–4,600

–4,600

(d)

Balances, Dec. 31, 2013

53,000

1,500

1,400

250,000

–77,500

7,000

2,150

50,000

169,250

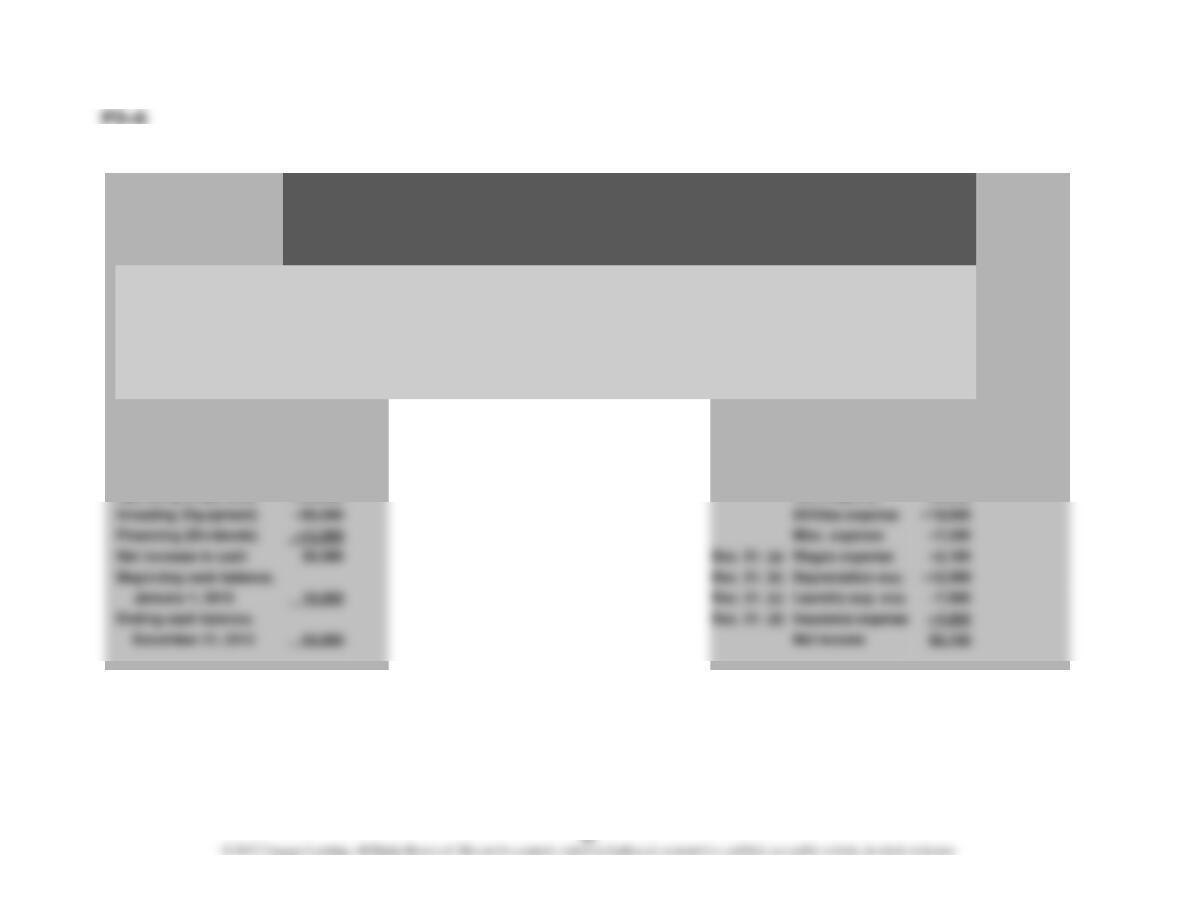

Statement of Cash Flows

Income Statement

Operating (Revenues)

275,000

Laundry revenue

275,000

Financing (Capital Stock)

25,000

Wages expense

–110,000

Operating (Expenses)

–200,000

Rent expense

–30,000

Investing (Equipment)

Utilities expense

–18,000

Financing (Dividends)

–15,000

Misc. expense

Net increase in cash

35,000

Dec. 31. (a)

Wages expense

Beginning cash balance,

Dec. 31. (b)

Depreciation exp.

January 1, 2013

18,000

Dec. 31. (c)

Laundry sup. exp.

Ending cash balance,

Dec. 31. (d)

Insurance expense

P3–6, Continued

2. MS. ELLEN’S LAUNDRY INC.

Income Statement

For the Year Ended December 31, 20Y8

Laundry revenue ……………………………………………………. $275,000

Operating expenses:

Wages expense …………………………………………………. $112,150

Rent expense ……………………………………………………. 30,000

MS. ELLEN’S LAUNDRY INC.

Retained Earnings Statement

For the Year Ended December 31, 20Y8

Retained earnings, January 1, 20Y8 ………………………… $101,500

Net income for the year ………………………………………….. $82,750

P3–6, Continued

3. MS. ELLEN’S LAUNDRY INC.

Balance Sheet

December 31, 20Y8

Assets

Current assets:

Cash …………………………………………………………………. $ 53,000

Laundry supplies ………………………………………………. 1,500

Prepaid insurance …………………………………………….. 1,400

Liabilities

Current liabilities:

Accounts payable ……………………………………………… $ 7,000

Wages payable ………………………………………………….. 2,150

Total liabilities ……………………………………………………….. $ 9,150

P3–6, Concluded

4. MS. ELLEN’S LAUNDRY INC.

Statement of Cash Flows

For the Year Ended December 31, 20Y8

Cash flows from operating activities:

Cash received from customers ………………………….. $ 275,000

Cash paid for expenses …………………………………….. (200,000)

Net cash flows from operating activities …………………. $ 75,000

Cash flows used for investing activities:

Cash paid for equipment……………………………………. (50,000)

FINANCIAL ANALYSIS

FA3–1

1. Year 2: $363 ($1,997 – $1,634)

Year 1: $407 ($2,155 – $1,748)

2. Year 2: 1.2 ($1,997 ÷ $1,634)

4. GameStop’s working capital has declined $44 million in Year 2 from $407 mil-

5. GameStop is experiencing competitive pressures from the availability of in-

expensive games that can be downloaded from various online sources for

FA3–2

1. Year 2: $2,181 ($4,309 – $2,128)

Year 1: $1,831 ($3,926 – $2,095)

2. Year 2: 2.0 ($4,309 ÷ $2,128)

Year 1: 1.9 ($3,926 ÷ $2,095)

FA3–3

1. Year 2: $882 ($1,287 – $405)

Year 1: $786 ($1,174 – $388)

2. Year 2: 3.2 ($1,287 ÷ $405)

4. American Eagle Outfitters’ liquidity position stayed approximately the same

from Year 1 to Year 2. Working capital increased by $96 million while the cur-

FA3–4

Working capital, the current ratio, and the quick ratio for Year 2 (from FA3–2 and

FA3–3) are summarized below.

American Eagle

The Gap Outfitters

Working capital (in millions) …………… $2,181 $882

Current ratio ………………………………….. 2.0 3.2

Quick ratio …………………………………….. 1.0 2.1

FA3–5

1. This item is intended to encourage students to think about different types of

businesses and their operations. It then requires the student to think about

how business operations might affect the current ratio.

2. This item is intended to encourage students to think about different types of

3. Walmart:

Current ratio: 0.9 ($54,975 ÷ $62,300)

Quick ratio: 0.2 ($12,487 ÷ $62,300)

4. Walmart has significantly lower current and quick ratios than does Google.

Walmart’s current and quick ratios are 0.9 and 0.2 compared to Google’s 3.7

and 3.1. These differences can be partially explained by the nature of the op-

erations of the two companies. As a large retailer, Walmart has a significant

amount of merchandise inventory (over $40 billion) included in its current as-

sets. In contrast, Google has no inventory. In addition, because of its large

CASES

Case 3–1

Revenue is normally recorded when the services are provided or when the goods

are delivered (title passes) to the buyer. By waiting until after the services are

provided, the expenses of providing the services can be more accurately

measured and matched against the related revenues. Also, at this point, the pro-

vider of the services has a right to demand payment for the services if payment

hasn’t already been received.

Note to Instructors: You might point out to students the following points related

to the discussion of the adjusting process in this chapter.

(1) The receipt of revenue from customers in advance of a flight represents un-

earned revenues to the airline. For example, the purchase of discount tickets,

which often requires prepayment months in advance of the actual flight, is

unearned revenue to the airline.

(2) At the end of the airline’s accounting period, it would have adjustments relat-

ed to items such as the following:

• Accrued wages for employees

Case 3–2

1. There are several indications that adjustments were not recorded before the

financial statements were prepared, including:

a. All expenses on the income statement are identified as “paid” items and

not as “expenses.”

2. Likely accounts requiring adjustment include:

a. Truck (for depreciation)

Case 3–3

1. The answers will vary among the student groups. The objective of this case is

to generate student interest and discussion of business emphases.

The advantages of the do-it-yourself emphasis are as follows:

a. It requires less capital equipment and training of employees. For example,

expensive automotive diagnostic equipment will not have to be pur-

The advantages of the do-it-for-me emphasis are as follows:

a. Demographically, the population of the United States is aging. In the fu-

ture, such demographics mean that more customers will be less willing to

fix their own cars. That is, they would rather pay someone to fix their cars

for them.

2. Examples of do-it-yourself include AutoZone, Pep Boys, and Napa Auto Parts

in the automotive industry. In the home improvement industry, examples in-

clude Home Depot and Lowe’s.

Case 3–4

1. CVS:

Operating income ………………………………………………………… $3,461

Add: Increase in accounts payable ($7,663 – $7,096) …….. $ 567

Deduct: Increase in accounts receivable ($6,550 – $5,436) (1,114) (547)

Adjusted cash basis operating income ………………………… $2,914

2. CVS: $547 ($3,461 – $2,914)

Walgreens: $337 ($2,127 – $1,790)

3. CVS: 15.8% ($547 ÷ $3,461)

Walgreens: 15.8% ($337 ÷ $2,127)

5. Most analysts focus on operating income rather than net income in assessing

the long-term profitability of a company. This is because operating income

Case 3–5

1. Company A is Amazon.com

2. Amazon.com (Company A) has experienced rapidly growing revenues since

its inception. In Year 3 Amazon reported revenues of $48,077 million, which is

a $13,873 million ($48,077 – $34,204) increase from Year 2. At the same time,

Amazon’s net cash flows from operations and total assets have increased.

Amazon’s investment in its future operations decreased in Year 3 by $1,430

(21.8 cents per revenue dollar). Coke obviously has higher operating margins

than does Kroger. This is what we would expect because of Coke’s brand

name and acceptance of its core products. Like Coke, Kroger has positive net

cash flows from operating activities and continues to invest cash in its busi-

ness.