CHAPTER 3

SOLUTIONS TO EXERCISES—SET B

EXERCISE 3-1B

(a) April 30 Work in Process—Cooking …………………. 27,000

Work in Process—Canning …………………. 10,000

Raw Materials Inventory……………….. 37,000

30 Work in Process—Cooking …………………. 9,000

EXERCISE 3-2B

(a) Work in process, May 1 500

Started into production 1,350

Total units to be accounted for 1,850

Less: Transferred out 1,350

Work in process, May 31 500

(b)

Equivalent Units

Materials

Conversion Costs

EXERCISE 3-2B (Continued)

(c) $7,905 ÷ 1,550 = $5.10

(d) Transferred out (1,350 X $11.22) $15,147

EXERCISE 3-3B

1. Raw Materials Inventory …………………………………… 64,300

Accounts Payable …………………………………….. 64,300

2. Factory Labor ………………………………………………….. 48,500

4. Work in Process—Cutting ………………………………… 16,400

Work in Process—Assembly ……………………………. 9,900

Raw Materials Inventory ……………………………. 26,300

7. Work in Process—Assembly ……………………………. 68,300

Work in Process—Cutting …………………………. 68,300

8. Finished Goods Inventory ………………………………… 136,000

Work in Process—Assembly ……………………… 136,000

(a)

January

May

Units to be accounted for

Beginning work in process

Started into production

0

12,000

0

21,000

(b)

(1)

Materials

(2)

Conversion Costs

11,500 (10,000 + 1,500)

January

12,000 ( 9,000 + 3,000)

10,800 ( 9,000 + 1,800)

EXERCISE 3-5B

(a)

Materials

Conversion Costs

Units transferred out

12,000

12,000

Total units

EXERCISE 3-6B

JOSE FURNITURE COMPANY

Sanding Department

Production Cost Report

For the Month Ended March 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, March 1

Started into production

Total units

Units accounted for

0

15,000

15,000

Costs

Materials

Conversion

Costs

Total

Work in process, March 1

Started into production

Total costs

Unit costs

Cost Reconciliation Schedule

Total costs

Costs accounted for

Transferred out (11,000 X $10.35)

Work in process, March 31

$113,850

Transferred out

Work in process, March 31

(4,000 X 30%)

Total units

EXERCISE 3-7B

(a)

Materials

Conversion

Costs

Units transferred out

Work in process, April 30

18,000

18,000

(b)

Materials

Conversion

Costs

Total

Costs in April

$808,000(1)

$385,700(2)

$1,193,700

(c)

Transferred out (18,000 X $60.70)

Work in process

$1,092,600

EXERCISE 3-8B

(a) Materials: 32,000 + 8,000 = 40,000

2,000 X 100%

EXERCISE 3-9B

(a) Materials: 55,000(1) + 30,000 = 85,000

(b) Materials: $136,000/85,000 = $1.60

(c) Units transferred out: 55,000 X $5.77 = $317,350

Units in ending work in process:

EXERCISE 3-10B

(a)

Physical

Units

Work in process, September 30

Work in process, September 1

Units started into production

2,800

12,000

Equivalent Units

Materials

Conversion Costs

Units transferred out

11,800

11,800

EXERCISE 3-10B (Continued)

(b)

Materials

Work in process, September 1

Direct materials

Costs added to production

$ 32,000

Conversion Costs

during September

Work in process, September 1

Conversion costs

$ 29,100

(c) Costs accounted for

Transferred out (11,800 X $43.05) ……………. $507,990

Work in process, September 30

Total materials cost

EXERCISE 3-11B

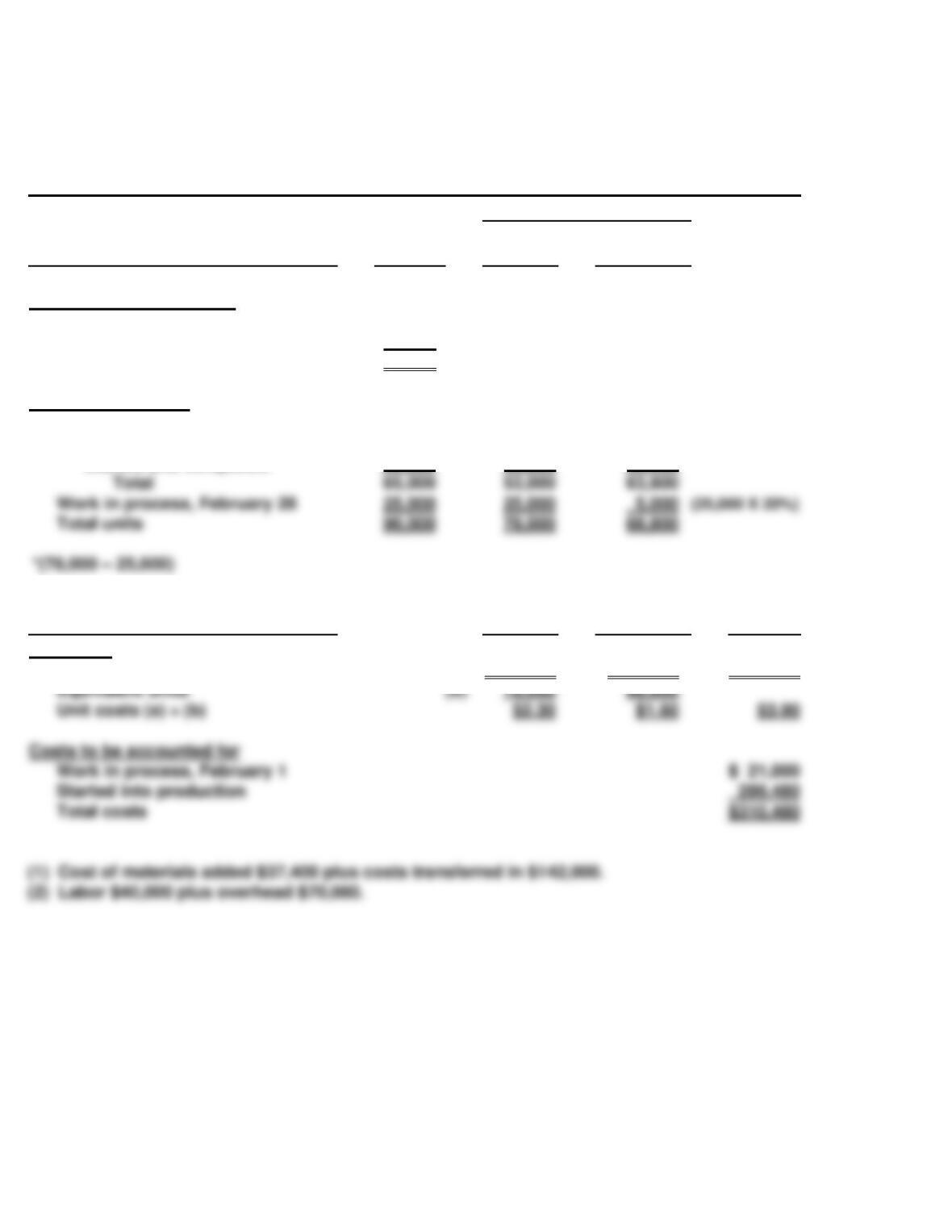

HANSON MANUFACTURING COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, February 1

Started into production

Total units

Units accounted for

27,000

60,000

87,000

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Work in process, February 1

Started into production

Total costs

$ 40,175

254,773

$294,948

Cost Reconciliation Schedule (Step 4)

Conversion costs (6,600 X $1.68)

Total costs

$294,948

Costs accounted for

Transferred out (54,000 X $3.90)

$210,600

Transferred out

Work in process, February 28

Total units

EXERCISE 3-12B

(a)

Containers in transit, April 1

0

Containers loaded

800

Equivalent Units

(b)

Physical

Units

Direct

Materials

Conversion

Costs

Containers off-loaded

350

350

350

Containers in transit, April 30

450

180*

135**

Total equivalent units

EXERCISE 3-13B

(a)

Materials

Conversion

Costs

Applications transferred out

800

800

Work in process, September 30

300*

180**

Equivalent units

1,100

980

(b)

Materials: $6,270 ÷ 1,100 = $5.70

Conversion costs: $22,540* ÷ 980 = $23

Costs accounted for:

Transferred out (800 X $28.70) …………………..

$22,960

Work in process, September 30

Materials (300 X $5.70) ………………………..

Conversion costs (180 X $23) ………………

Total costs ……………………………………………….

Total containers

Containers off-loaded

350

Containers in transit, April 30

Total containers

800

*EXERCISE 3-14B

Equivalent Units

(a)

Physical

Units

Materials

Conversion

Costs

Applications completed:

Work in process, September 1

100

0

50

(b)

Materials: $5,270 ÷ 1,000 = $5.27

Conversion costs: $18,540* ÷ 930 = $19.94

*($12,000 + $6,540)

Costs accounted for:

Applications completed:

5,170

Total costs …………………………………………..

$6,540 = $28,810

Started and completed

700

Work in process, September 30

300

Total units

1,100

1,000

*EXERCISE 3-15B

(a) (1) Materials:

Production Data

Physical

Units

Materials Added

This Period

Equivalent

Units

Work in process, August 1

Started and completed

0

8,000

%100

100%

0

8,000

(2) Conversion Costs:

Production Data

Physical

Units

%

Equivalent

Units

Work in process, August 31

Total

Work in process, August 1

Started and completed

0

8,000

0

100

0

8,000

(b) Unit costs are:

Materials $45,000 ÷ 10,000 = $4.50

Work in process, August 31

Total

*EXERCISE 3-16B

(a)

(1)

Materials

Physical

Units

Materials Added

This Period

Equivalent

Units

Work in process,

Q

(2)

Conversion Costs

Physical

Units

Work Added

This Period

Equivalent

Units

Work in process,

September 1

Started and completed

1,000

8,000

80%

100%

800

8,000

(b) Materials $ 63,000 ÷ 9,000 = $ 7.00

Conversion costs $139,840 ÷ 9,200 = 15.20

$22.20

(c)

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

Started and completed

Total costs transferred out

Total costs

Work in process, 9/1

Conversion costs

0

800

$ 0

$15.20

$16,000

12,160

$ 28,160

September 1

Total

1,000

*EXERCISE 3-17B

(a) Work in process, March 1 800

Started into production 1,200

Total units to be accounted for 2,000

(b) Materials:

Production Data

Physical

Units

Materials Added

This Period

Equivalent

Units

Work in process, March 31

Total

1,200

Work in process, March 1

Started and completed

800

500

%100

100%

0

500

(c) Conversion costs:

Production Data

Physical

Units

Work Added

This Period

Equivalent

Units

Work in process, March 31

Total

1,340

Work in process, March 1

Started and completed

800

500

70%

100%

560

500

(d) In process, March 1 …………………………………………………. $3,000

Conversion costs (560 X $2.40) ………………………………… 1,344

(f) Materials (700 X $6.00) …………………………………………….. $4,200

*EXERCISE 3-18B

HOLSUM MANUFACTURING COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, February 1

Started into production

Total units

Units accounted for

Completed and transferred out

12,000

78,000

90,000

Work in process, February 1

Started and completed

12,000

53,000*

0

53,000

10,800

53,000

(12,000 X 90%)

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Work in process, February 1

Started into production

Total costs

$ 21,000

289,480

Unit costs (Step 3)

Costs in February

(a)

$179,400

(1)

$110,080

(2)

$289,480

Total

Work in process, February 28

Total units

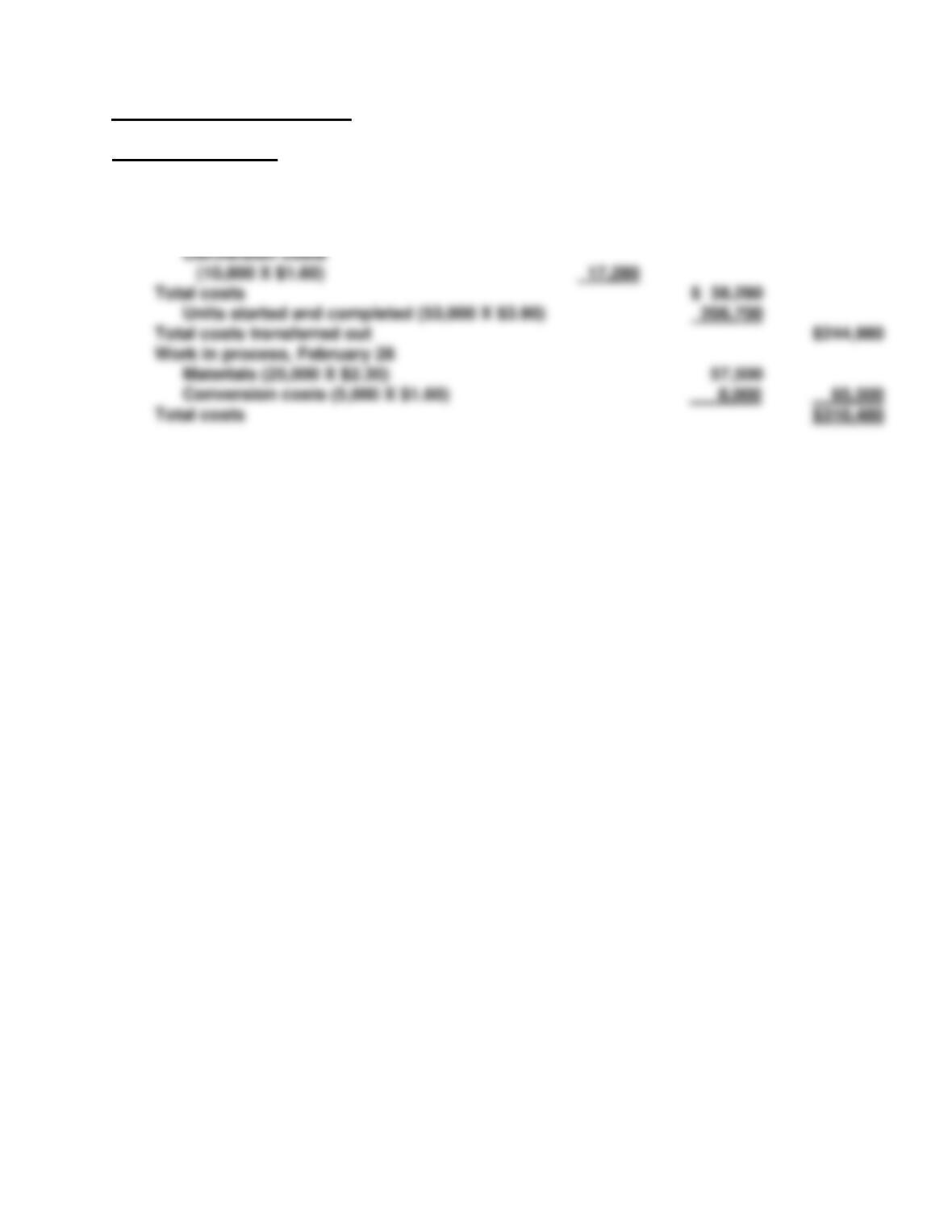

*EXERCISE 3-18B (Continued)

Cost Reconciliation Schedule

Costs accounted for (Step 4)

Transferred out

Work in process, February 1

Costs to complete beginning

work in process

$21,000

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 3-1C

(a)

Physical units

Units to be accounted for

Work in process, January 1

Started into production

0

50,000

(b)

Equivalent units

Materials

Conversion Costs

Total equivalent units

Units transferred out

40,000

40,000

(c)

Unit Costs

Materials

$11.10 ($555,000 ÷ 50,000)

(d) Costs accounted for

Transferred out (40,000 X $16.35) …………….. $654,000

Work in process, January 31

Total units

PROBLEM 3-1C (Continued)

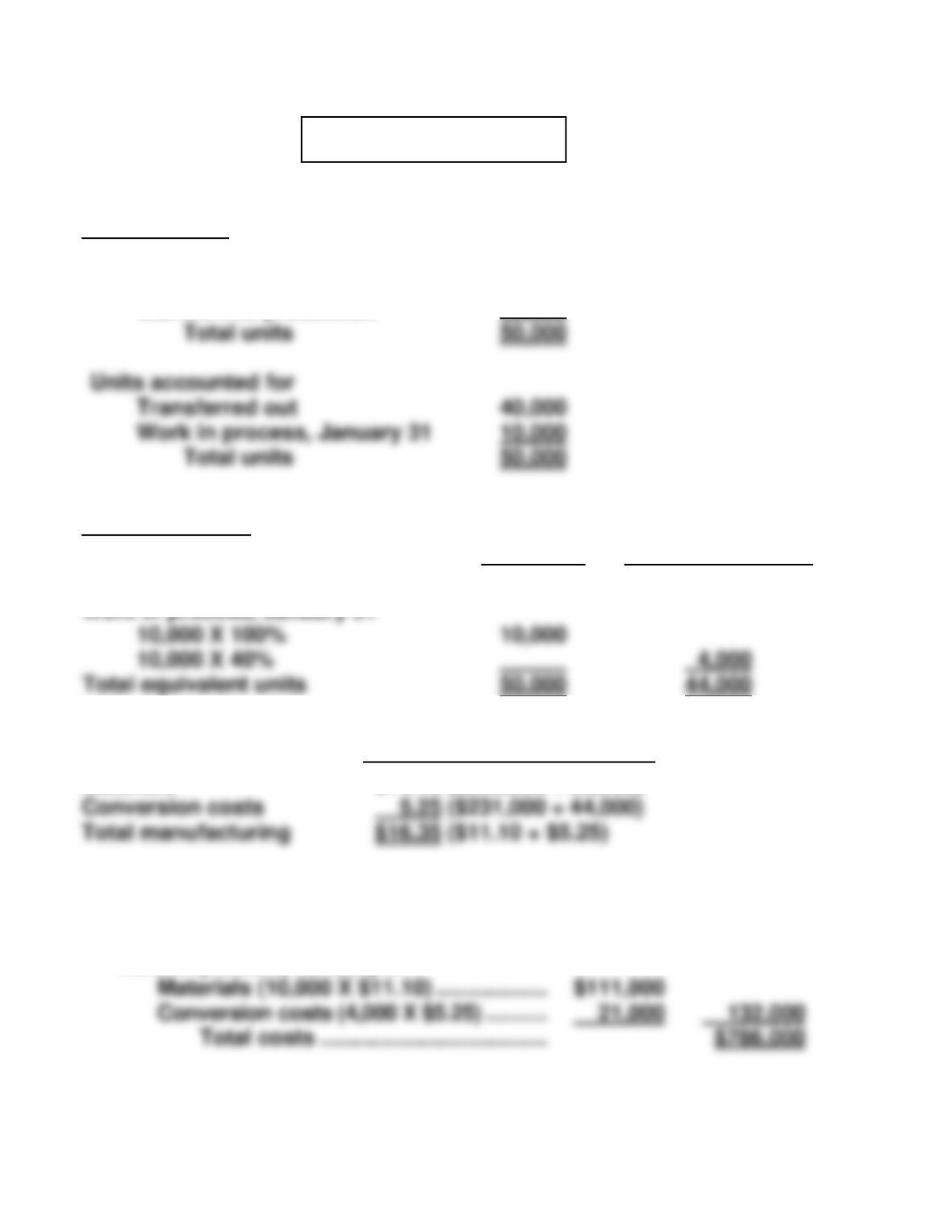

(e) COMPLETE CORPORATION

Molding Department

Production Cost Report

For the Month Ended January 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, January 1

Started into production

Total units

0

50,000

50,000

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Costs in January

(a)

$555,000

$231,000

$786,000

Cost Reconciliation Schedule (Step 4)

Conversion costs (4,000 X $5.25)

Total costs

132,000

Costs accounted for

Transferred out (40,000 X $16.35)

$654,000

Transferred out

Work in process, January 31

Total units

PROBLEM 3-2C

(a) (1) Physical units

R12

Refrigerators

F24

Freezers

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

22,000

22,000

0

20,000

20,000

(2) Equivalent units

R12 Refrigerators

Materials

Conversion

Costs

Units transferred out

Work in process, June 30

14,000

14,000

F24 Freezers

Materials

Conversion

Costs

Units transferred out

Work in process, June 30

18,000

18,000

PROBLEM 3-2C (Continued)

(3) Unit costs

R12

Refrigerators

F24

Freezers

Materials ($836,000 ÷ 22,000)

($720,000 ÷ 20,000)

$38

$36

(4) R12 Refrigerators

Costs accounted for

Transferred out (14,000 X $72) ………….. $1,008,000

Work in process

F24 Freezers

Costs accounted for

Transferred out (18,000 X $63) ………….. $1,134,000

Work in process

PROBLEM 3-2C (Continued)

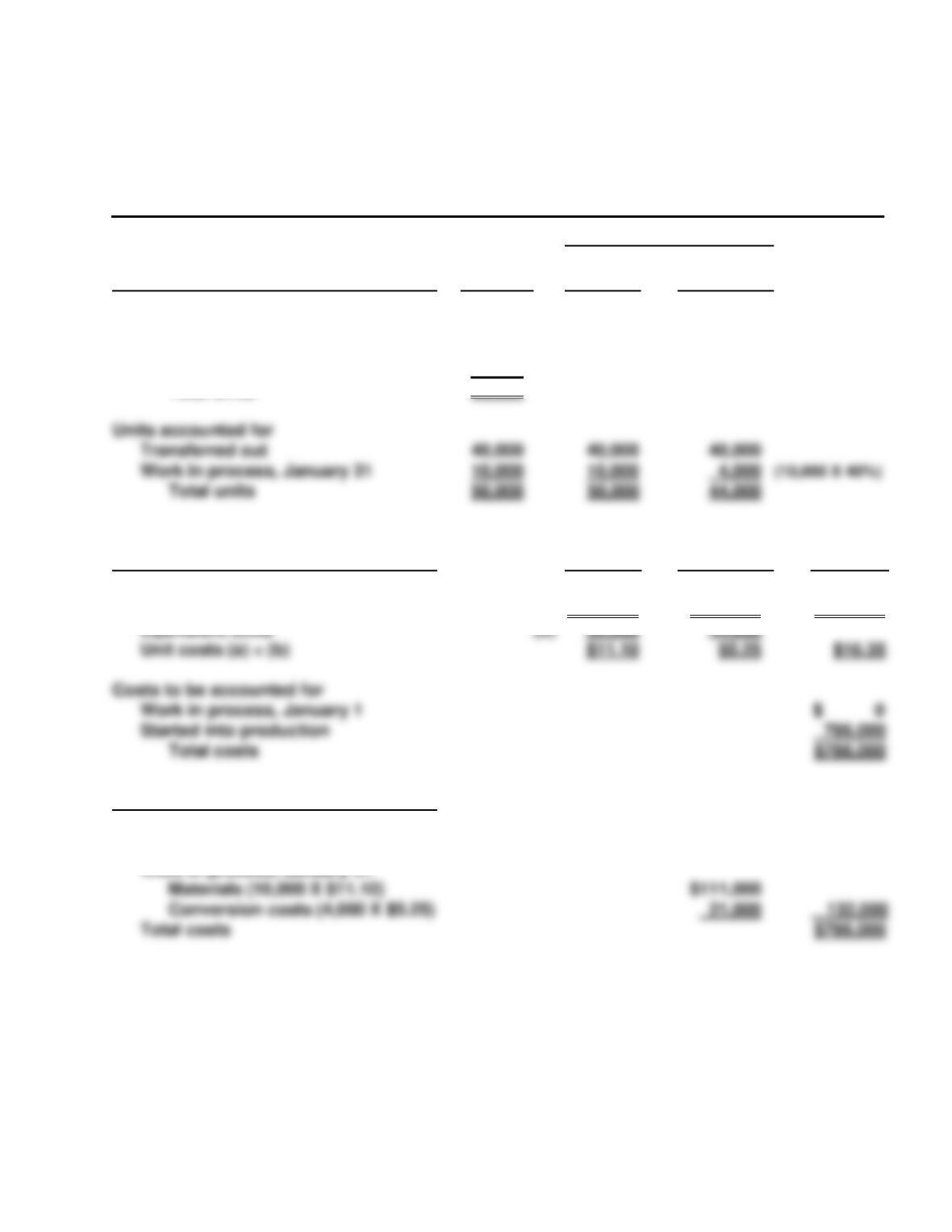

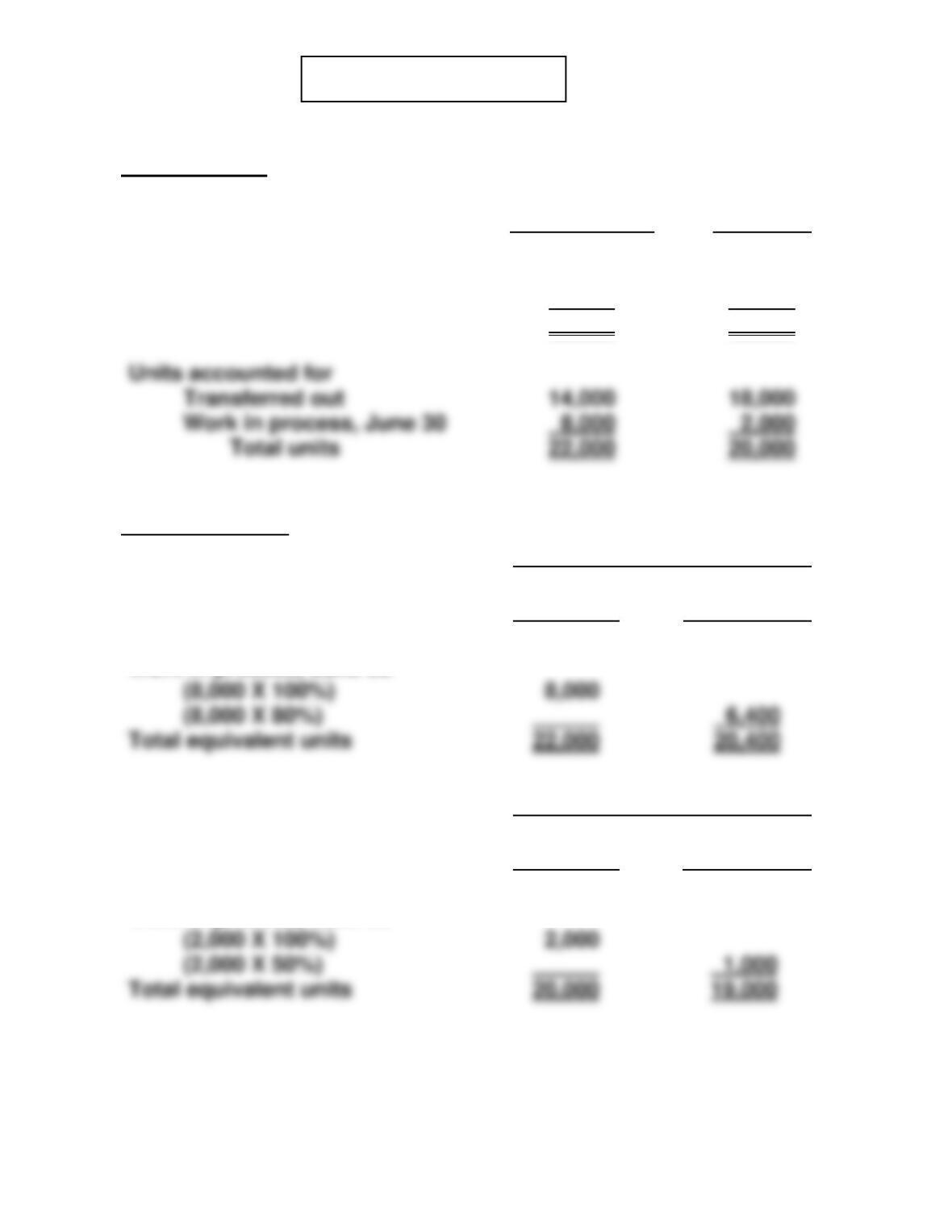

(b) SUNNYLAND CORPORATION

Stamping Department—Plant A

Production Cost Report

For the Month Ended June 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

22,000

22,000

Costs

Materials

Conversion

Costs

Total

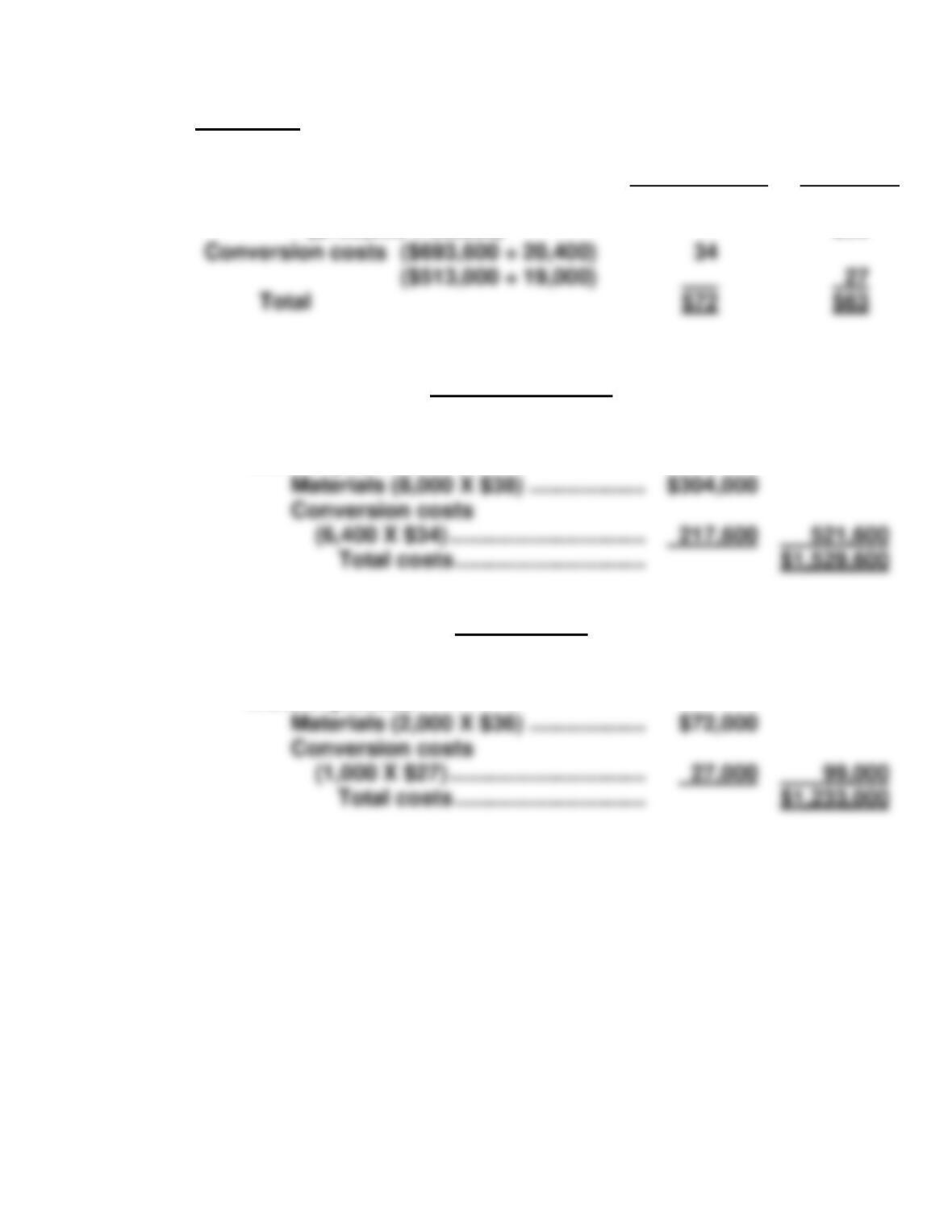

Work in process, June 1

Total costs

Unit costs (Step 3)

Costs in June

Equivalent units

(a)

(b)

$836,000

22,000

$693,600

20,400

$1,529,600

Cost Reconciliation Schedule (Step 4)

Conversion costs (6,400 X $34)

Total costs

Costs accounted for

Transferred out (14,000 X $72)

$1,008,000

Transferred out

Work in process, June 30

Total units

PROBLEM 3-3C

1. Raw Materials Inventory …………………………………….. 28,000

Accounts Payable ……………………………………….. 28,000

2. Work in Process—Blending ……………………………….. 18,390

Work in Process—Packaging ……………………………… 9,410

Raw Materials Inventory ………………………………. 27,800

5. Manufacturing Overhead ……………………………………. 41,500

Accounts Payable ……………………………………….. 41,500

6. Work in Process—Blending (1,800 X $20) ……………. 36,000

Work in Process—Packaging (600 X $20) ……………. 12,000

Manufacturing Overhead……………………………… 48,000

PROBLEM 3-4C

(a)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, October 1

Started into production

30,000

375,000

(b)

Total costs

Costs accounted for

Transferred out (365,000 X $3.80)

Work in process, October 31

$1,387,000

Total units

40,000

PROBLEM 3-4C (Continued)

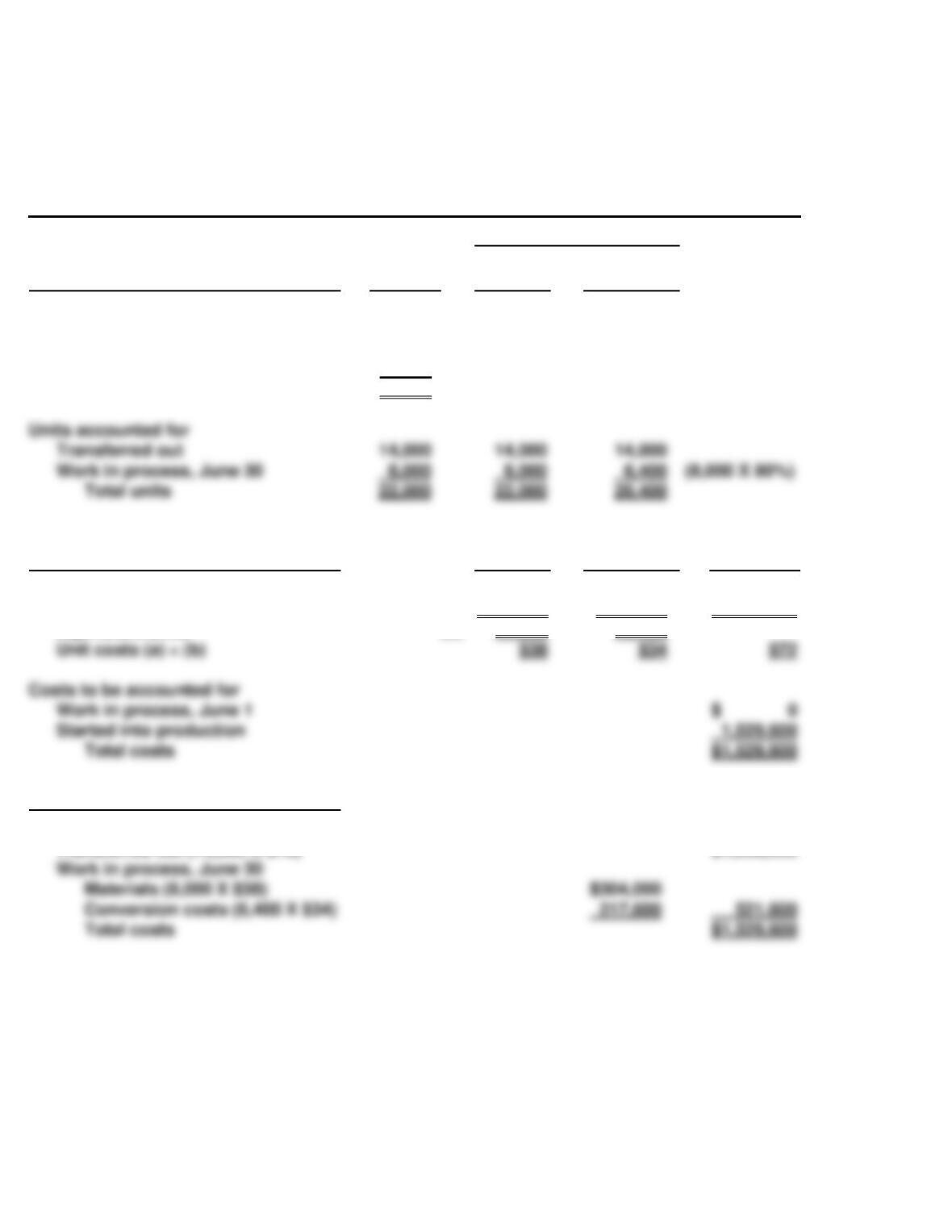

(c) SIENNA COMPANY

Assembly Department

Production Cost Report

For the Month Ended October 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, October 1

Started into production

Total units

30,000

375,000

405,000

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Costs in October

Equivalent units

(a)

(b)

$1,093,500

405,000

$419,100

381,000

$1,512,600

Cost Reconciliation Schedule (Step 4)

Conversion costs (16,000 X $1.10)

Total costs

Costs accounted for

Transferred out (365,000 X $3.80)

Work in process, October 31

$1,387,000

Transferred out

Work in process, October 31

40,000

40,000

Total units

PROBLEM 3-5C

(a)

(1)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, May 1

Started into production

2,000

2,500

(2)

Materials cost

Conversion costs

Beginning work in

process

Added during month

$18,000

90,000

Beginning work in

process

Added during month

$22,000

110,300

($46,000 + $64,300)

(3)

Costs accounted for

Transferred out (2,700 X $66)

Work in process, May 31

$178,200

PROBLEM 3-5C (Continued)

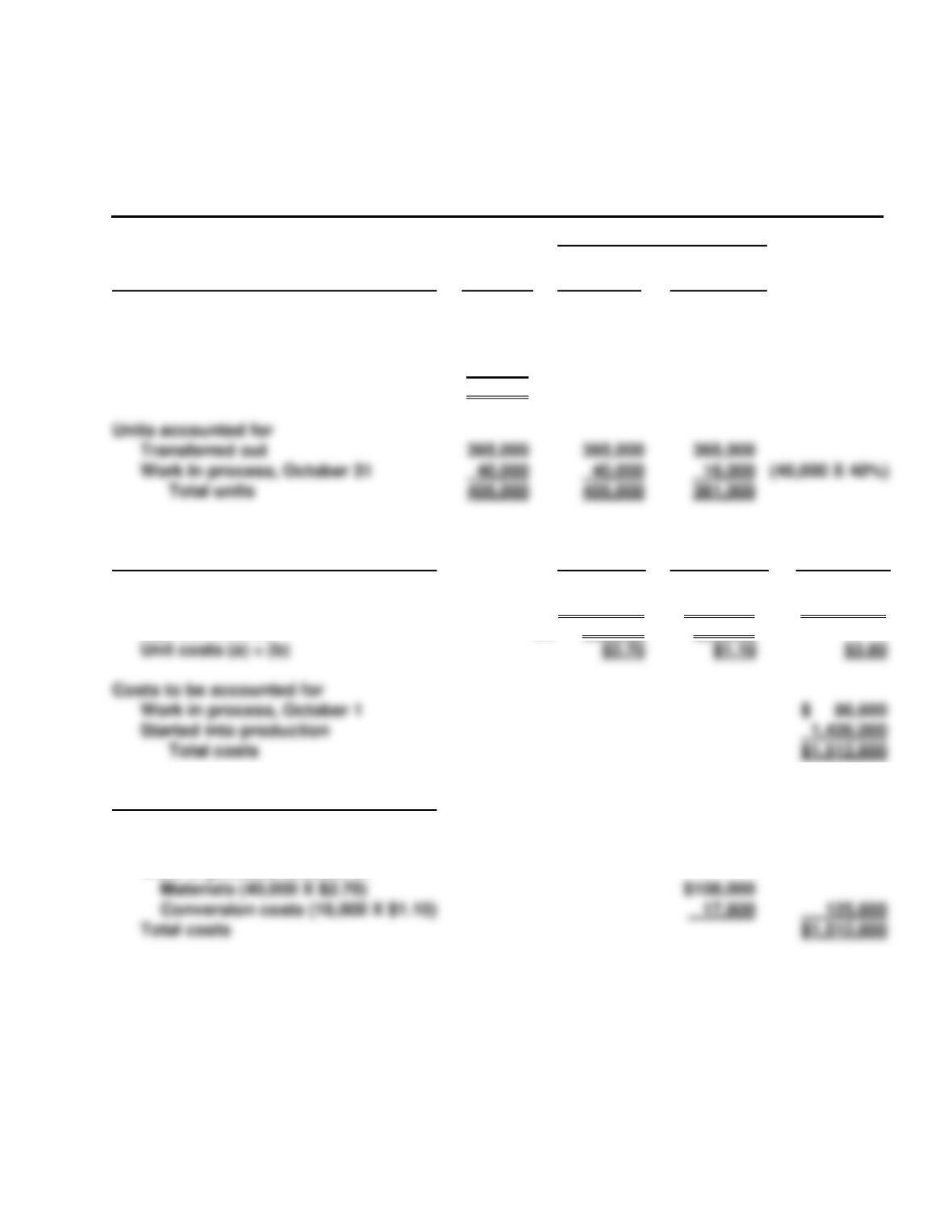

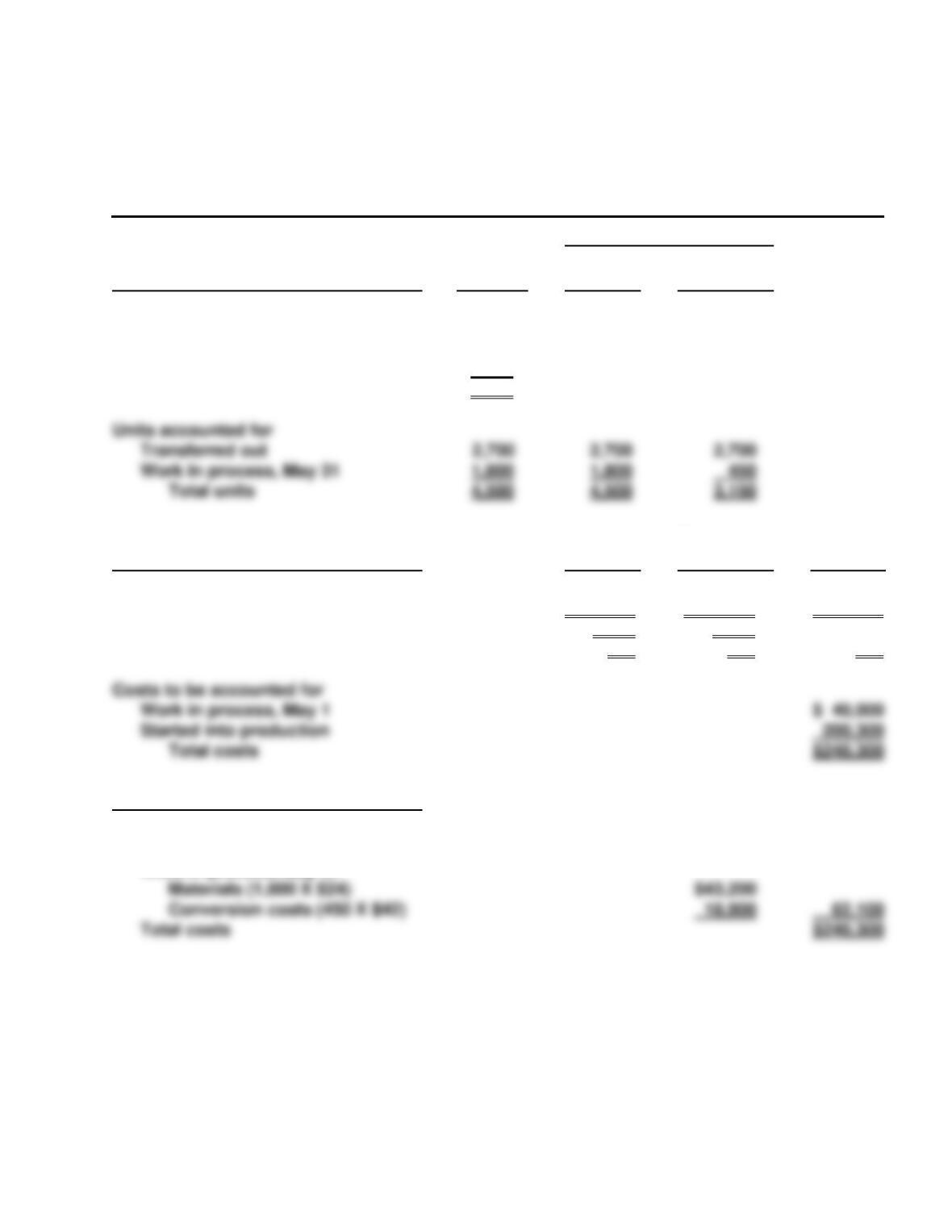

(b) MAUEVE COMPANY

Bicycle Department

Production Cost Report

For the Month Ended May 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, May 1

Started into production

Total units

2,000

2,500

4,500

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Costs in May

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$108,000

4,500

$24

$132,300

3,150

$42

$240,300

$66

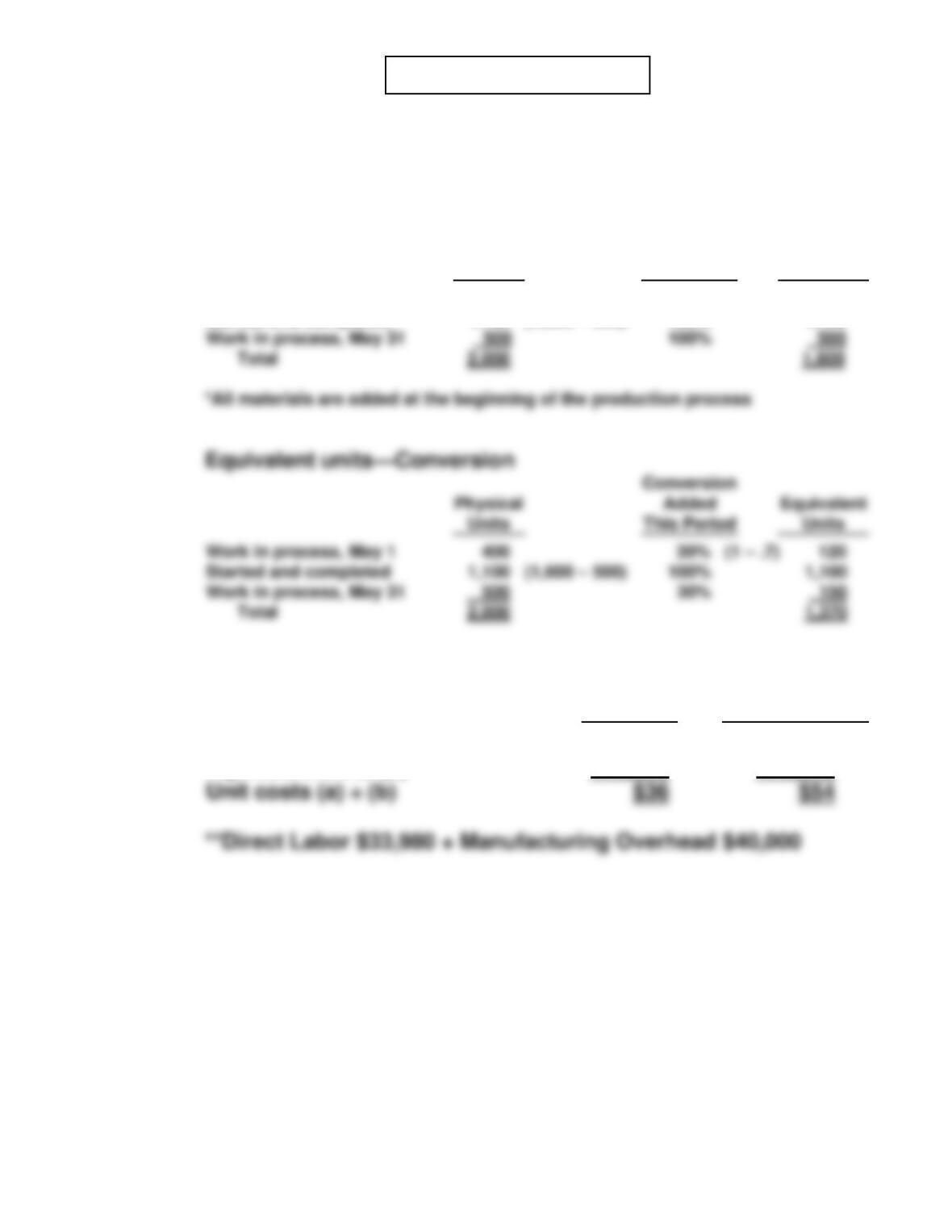

Cost Reconciliation Schedule (Step 4)

Conversion costs (450 X $42)

Total costs

Costs accounted for

Transferred out (2,700 X $66)

Work in process, May 31

178,200

Transferred out

2,700

Work in process, May 31

Total units

4,500

4,500

PROBLEM 3-6C

(a) Computation of equivalent units:

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units accounted for

Transferred out

Work in process, March 31

100,000

100,000

100,000

Computation of March unit costs

Materials: $212,800 ÷ 112,000 equivalent units = $1.90

(b) Cost Reconciliation Schedule

Costs accounted for

Transferred out (100,000 X $2.95) ……………. $295,000

Work in process, March 31

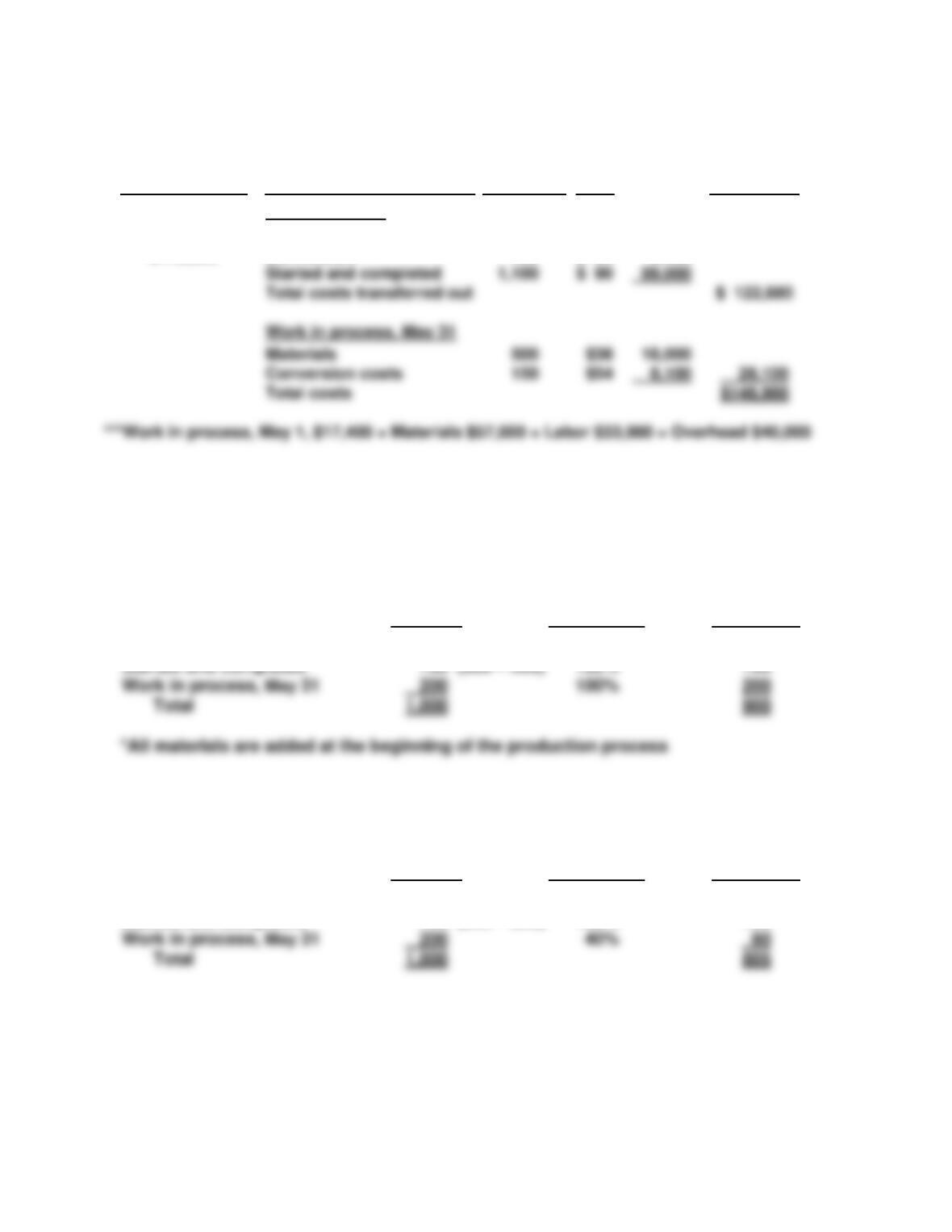

*PROBLEM 3-7C

(a) Standard Bicycles

(1) Equivalent units—Materials

Physical

Units

Materials

Added

This Period

Equivalent

Units

Work in process, May 1

Started and completed

400

1,100

(1,600 – 500)

* 0%*

100%

0

1,100

(2) Unit costs

Materials

Conversion

Costs in May (a)

Equivalent units (b)

$57,600

1,600

**$73,980**

1,370

Work in process, May 31

Total

Units

Conversion

This Period

Units

Work in process, May 1

400

Started and completed

Total

(1,600 – 500)

100%

*PROBLEM 3-7C (Continued)

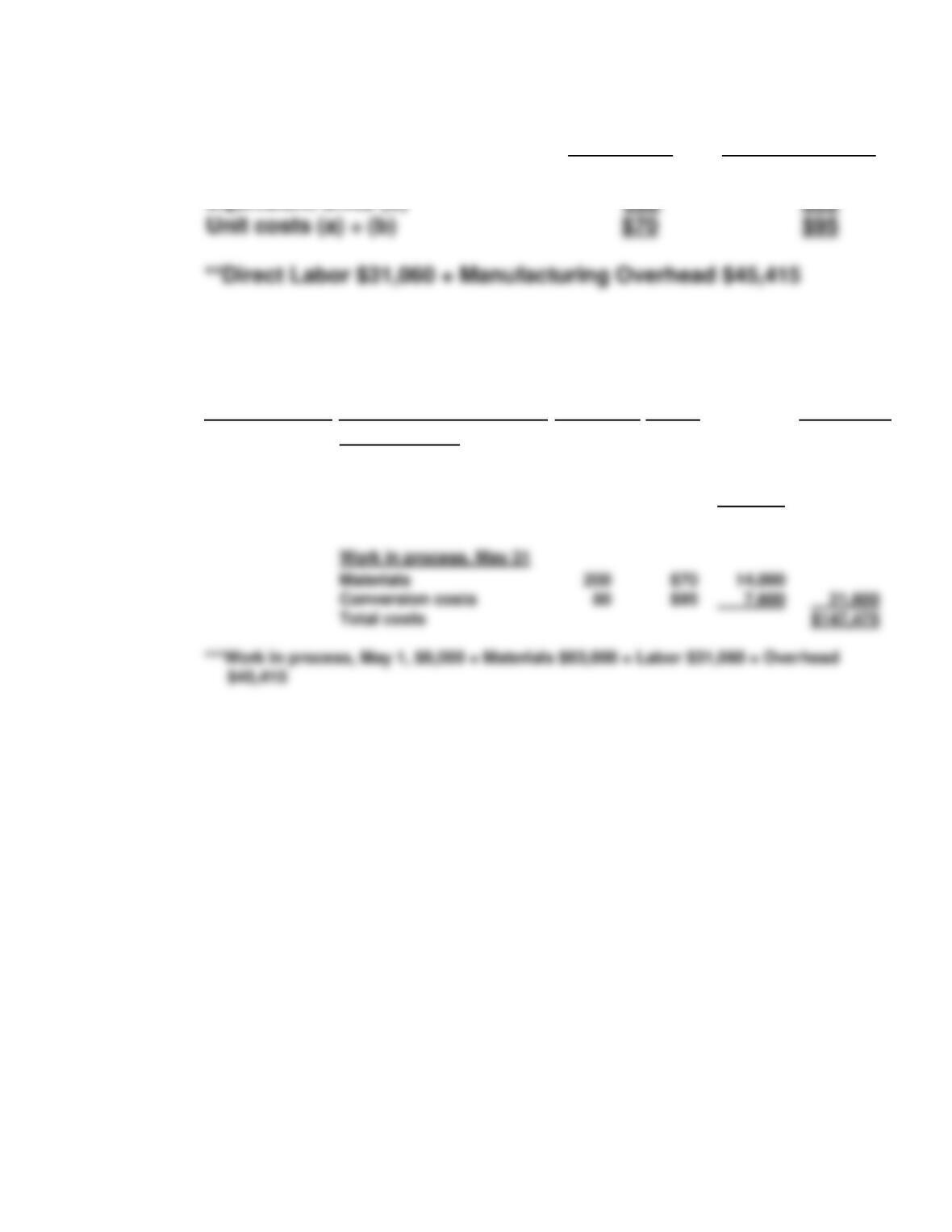

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

***$148,980***

Work in process, May 1

Conversion

120

$ 54

$17,400

6,480

Premium Bicycles

(1) Equivalent units—Materials

Physical

Units

Materials

Added

This Period

Equivalent

Units

Work in process, May 1

100

* 0%*

0

Started and completed

Work in process, May 31

Total

1,000

900

Equivalent units—Conversion

Physical

Units

Conversion

Added

This Period

Equivalent

Units

Work in process, May 1

100

25% (1 – .75) 25

Started and completed

700 (900 – 200)

100%

700

Work in process, May 31

Total

1,000

Total costs transferred out

Work in process, May 31

Total costs

*PROBLEM 3-7C (Continued)

(2) Unit costs

Materials

Conversion

Costs in May (a)

Equivalent units (b)

$63,000

900

**$76,475**

805

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

***$147,475***

Work in process, May 1

Conversion

Started and completed

Total costs transferred out

25

700

$ 95

$165

$ 8,000

2,375

115,500

$125,875

Total costs

$147,475

Unit costs (a) ÷ (b)

$70

*PROBLEM 3-7C (Continued)

(b) BRACK COMPANY

Production Cost Report—Standard Bicycles

For the Month Ended May 31

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, May 1

Started into production

Total units

400

1,600

2,000

Costs

Materials

Conversion

Costs

Unit costs (Step 3)

Costs in March (a)

Equivalent units (b)

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out

Work in process, May 1

Conversion costs (120 X $54)

Started and completed (1,100 X $90)

$57,600

1,600

$17,400

6,480

99,000

$ 73,980

1,370

Work In process, May 31

Total units