1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and

expenses are reported in the period in which cash is paid.

b. Under accrual-basis accounting, revenues are reported in the period in which they are earned

and expenses are reported in the same period as the revenues to which they relate.

5. Four different categories of adjusting entries include prepaid expenses (deferred expenses), unearned

revenues (deferred revenues), accrued expenses (accrued liabilities), and accrued revenues (accrued

assets).

6. Statement (a): Increases the balance of a revenue account.

7. Statement (b): Increases the balance of an expense account.

8. Yes, because every adjusting entry affects expenses or revenues.

9. a. The rights acquired represent an asset.

b. The justification for debiting Rent Expense is that when the ledger is summarized in a trial

b

alance at the end of the month and statements are prepared, the rent will have become an

expense. Hence, no adjusting entry will be necessary.

b

CHAPTER 3

THE ADJUSTING PROCESS

DISCUSSION QUESTIONS

CHAPTER 3 The Adjusting Process

PE 3-1A

a. No c. Yes e. No

b. No d. No f. Yes

PE 3-1B

PE 3-2A

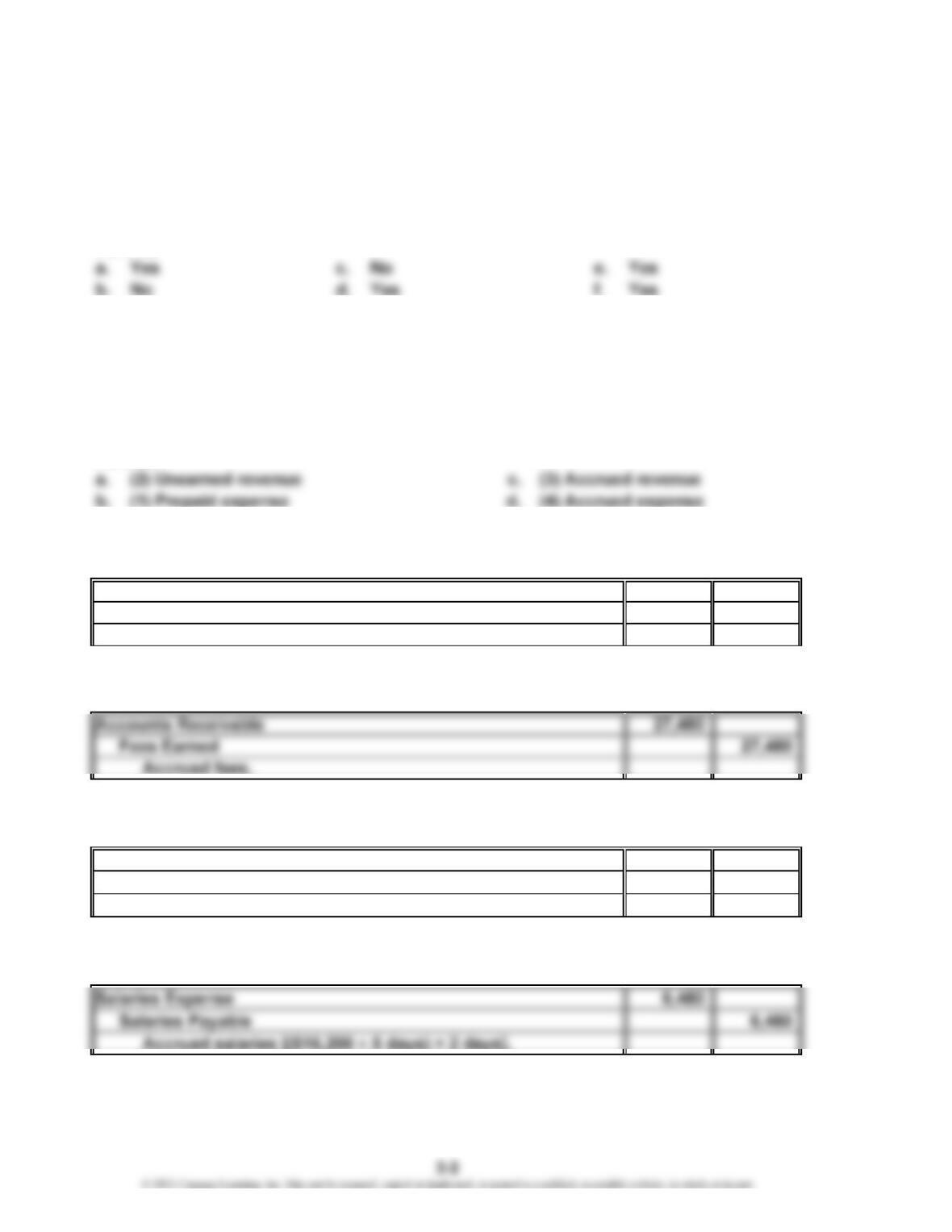

a. (2) Unearned revenue c. (4) Accrued expense

b. (3) Accrued revenue d. (1) Prepaid expense

PE 3-2B

PE 3-3A

Accounts Receivable 18,540

Fees Earned 18,540

Accrued fees.

PE 3-3B

PE 3-4A

Salaries Expense 22,200

Salaries Payable 22,200

Accrued salaries [($33,300 ÷ 6 days) × 4 days].

PE 3-4B

PRACTICE EXERCISES

CHAPTER 3 The Adjusting Process

PE 3-5A

PE 3-5B

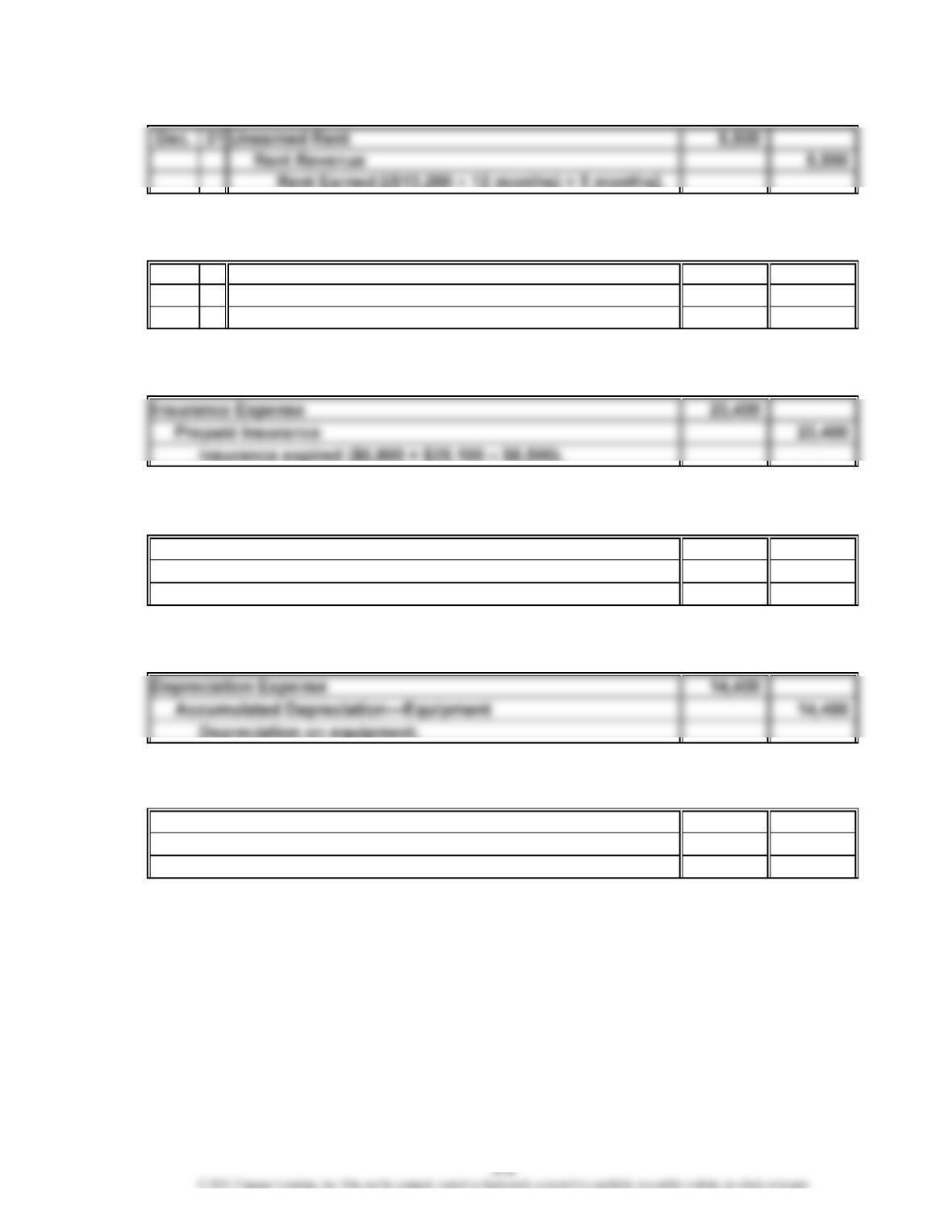

Dec. 31 Unearned Fees 96,050

Fees Earned 96,050

Fees Earned ($316,290 – $220,240).

PE 3-6A

PE 3-6B

Supplies Expense 8,285

Supplies 8,285

Supplies used ($4,085 + $7,810 – $3,610).

PE 3-7A

PE 3-7B

Depreciation Expense 8,120

Accumulated Depreciation—Building 8,120

Depreciation on building.

CHAPTER 3 The Adjusting Process

PE 3-8A

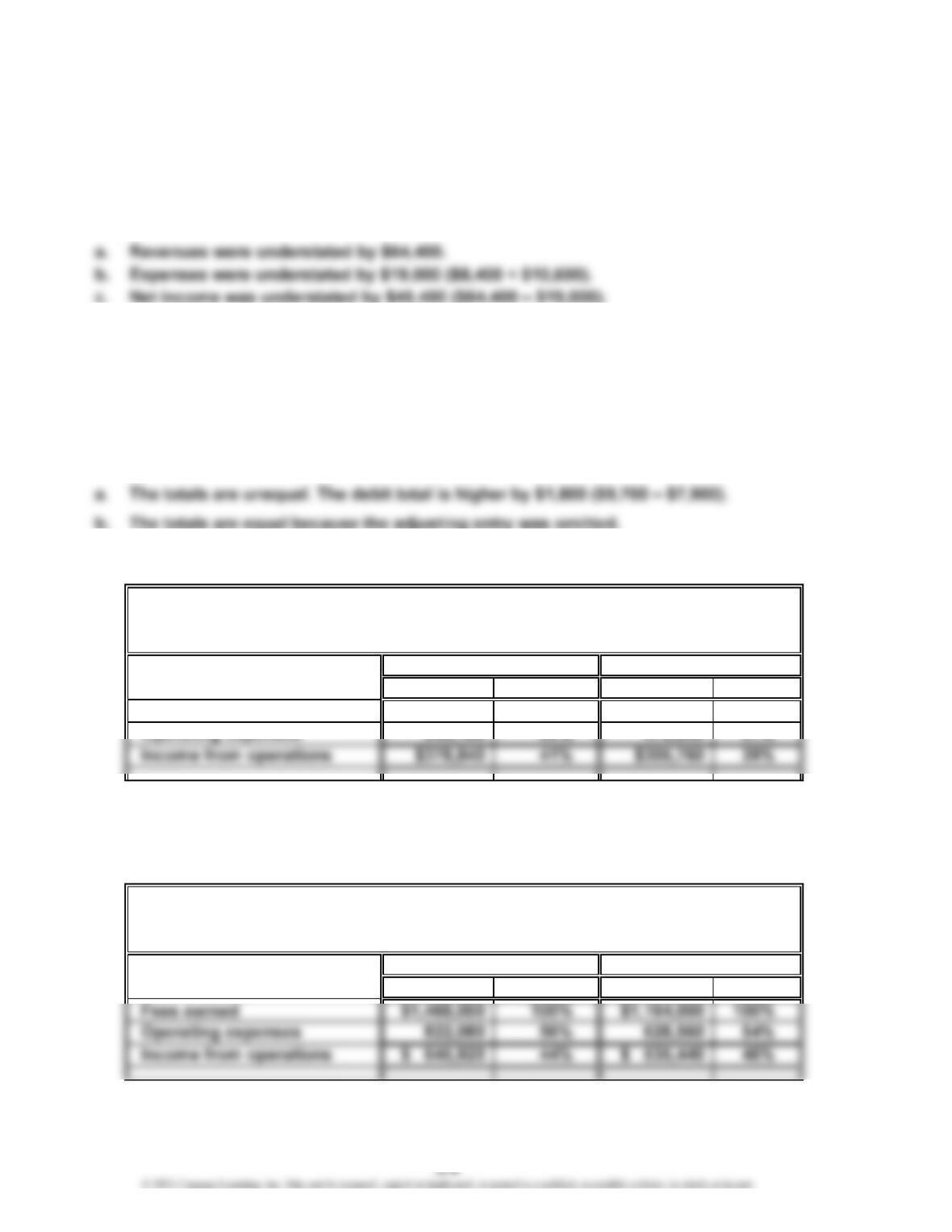

a. Revenues were understated by $8,000.

b. Expenses were understated by $12,600 ($1,700 + $10,900).

c. Net income was overstated by $4,600 ($12,600 – $8,000).

PE 3-8B

PE 3-9A

a. The totals are equal even though the credit should have been to Wages

Payable instead of Accounts Payable.

b. The totals are unequal. The credit total is higher by $72 ($1,591 – $1,519).

PE 3-9B

PE 3-10A

a.

Amount Percent Amount Percent

Fees earned $924,000 100% $784,000 100%

b. A favorable change of decreasing operating expenses and increasing income from

operations as percentages of revenue is indicated.

PE 3-10B

a.

Amount Percent Amount Percent

b. An unfavorable change of increasing operating expenses and decreasing income

from operations as percentages of revenue is indicated.

Income Statements

For the Years Ended December 31

20Y5 20Y4

Versatile Company

Upward Company

Income Statements

For the Years Ended December 31

20Y5 20Y4

CHAPTER 3 The Adjusting Process

Ex. 3-1

1. Accrued expense (b) 5. Unearned revenue (c)

2. Unearned revenue (c) 6. Prepaid expense (d)

Ex. 3-2

Accounts Receivable…………………… Normally requires adjustment (AR).

Cash………………………………………

…

Does not normally require adjustment.

Harriet Kasun, Capital…………………

…

Does not normally require adjustment.

Interest Expense………………………… Normally requires adjustment (AE).

Interest Receivable……………………… Normally requires adjustment (AR).

Ex. 3-3

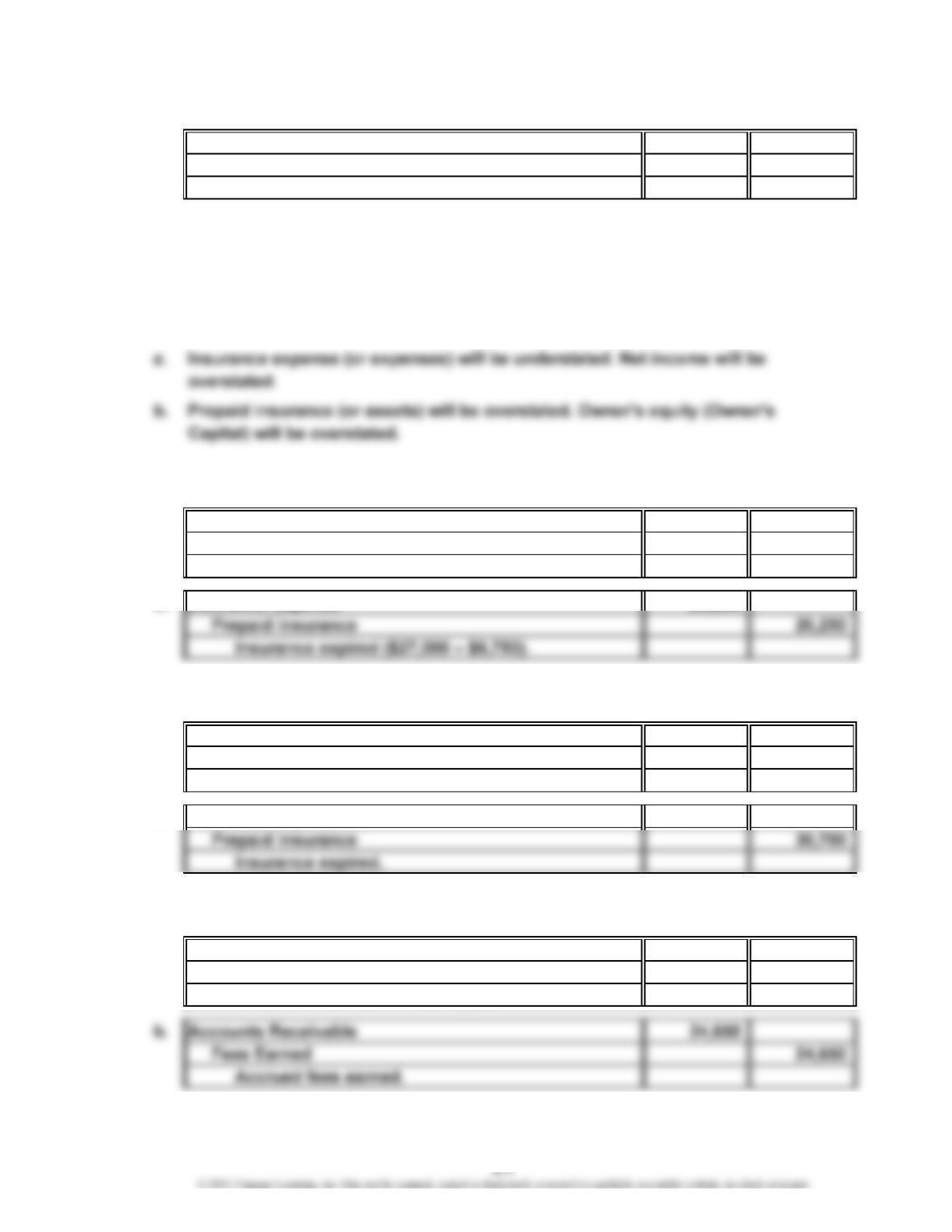

a. Accounts Receivable 59,500

Ex. 3-4

a. Fees earned (or revenues) will be understated. Net income will be understated.

b. Accounts receivable (or assets) will be understated. Owner’s equity (owner’s

capital account) will be understated.

EXERCISES

Account Answer

CHAPTER 3 The Adjusting Process

Ex. 3-5

a. Salaries Expense 8,880

Salaries Payable 8,880

Accrued salaries [($14,800 ÷ 5 days) × 3 days].

b. Salaries Expense 11,840

Ex. 3-6

$66,075 ($73,250 – $7,175)

Ex. 3-7

a. Salary expense (or expenses) will be understated. Net income will be overstated.

b. Salaries payable (or liabilities) will be understated. Owner’s equity (owner’s

capital account) will be overstated.

Ex. 3-8

a. Salary expense (or expenses) will be overstated because two days of salaries

that should have been included as October expenses are being recorded in

November. Net income will be understated.

Ex. 3-9

Unearned Fees 18,480

Fees Earned 18,480

($23,100 – $4,620).

CHAPTER 3 The Adjusting Process

Ex. 3-11

Supplies Expense 8,740

Supplies 8,740

Supplies used ($10,680 – $1,940).

Ex. 3-12

$9,110 ($1,310 + $7,800)

Ex. 3-13

Ex. 3-14

a. Insurance Expense 20,250

Prepaid Insurance 20,250

Insurance expired.

Ex. 3-15

a. Insurance Expense 30,700

Prepaid Insurance 30,700

Insurance expired ($3,000 + $32,500 – $4,800).

b. Insurance Expense 30,700

Ex. 3-16

a. Unearned Fees 39,750

Fees Earned 39,750

Unearned fees earned during year.

CHAPTER 3 The Adjusting Process

Ex. 3-17

a. Dec. 31 Taxes Expense 12,320

Prepaid Taxes 12,320

Prepaid taxes expired

[($18,480 ÷ 12 months) × 8 months].

b. $57,320 ($12,320 + $45,000)

Ex. 3-18

Depreciation Expense 8,200

Accumulated Depreciation—Equipment 8,200

Depreciation on equipment.

Ex. 3-19

Ex. 3-20

a. $29,460 million ($58,683 – $29,223)

b. No. Depreciation is an allocation method, not a valuation method. That is,

depreciation allocates the cost of a fixed asset over its useful life. Depreciation

does not attempt to measure market values, which may vary significantly from

year to year.

Ex. 3-21

CHAPTER 3 The Adjusting Process

Ex. 3-23

Over- Under- Over- Under-

stated stated stated stated

1. Revenue for the year would be $ 0 $34,900 $ 0 $ 0

2. Expenses for the year would be 0 0 0 12,770

Ex. 3-24

$218,530 ($196,400 + $34,900 – $12,770)

Ex. 3-25

a. Dec. 31 Depreciation Expense 13,900

Accumulated Depreciation—Equipment 13,900

Depreciation on equipment.

Error (b)Error (a)

CHAPTER 3 The Adjusting Process

Ex. 3-26

1. Accounts Receivable 6

Fees Earned 6

Accrued fees earned.

3. Insurance Expense 12

Prepaid Insurance 12

Insurance expired.

5. Wages Expense 2

Wages Payable 2

Accrued wages.

CHAPTER 3 The Adjusting Process

Ex. 3-27

1. The accountant debited Accounts Receivable for $5,000 but did not credit

Laundry Revenue. This adjusting entry represents accrued laundry revenue.

4. The accountant credited Laundry Equipment for the depreciation expense of

$13,000 instead of crediting the accumulated depreciation account.

The corrected adjusted trial balance is shown below.

Debit Credit

Balances Balances

Cash 7,500

Accounts Receivable 23,250

Accounts Payable 9,600

Wages Payable 1,000

Eva Baldwin, Capital 110,300

Eva Baldwin, Drawing 28,775

Laundry Revenue 187,100

Miscellaneous Expense 3,250

369,000 369,000

May 31, 20Y3

Eva’s Laundry

Adjusted Trial Balance

CHAPTER 3 The Adjusting Process

Ex. 3-28

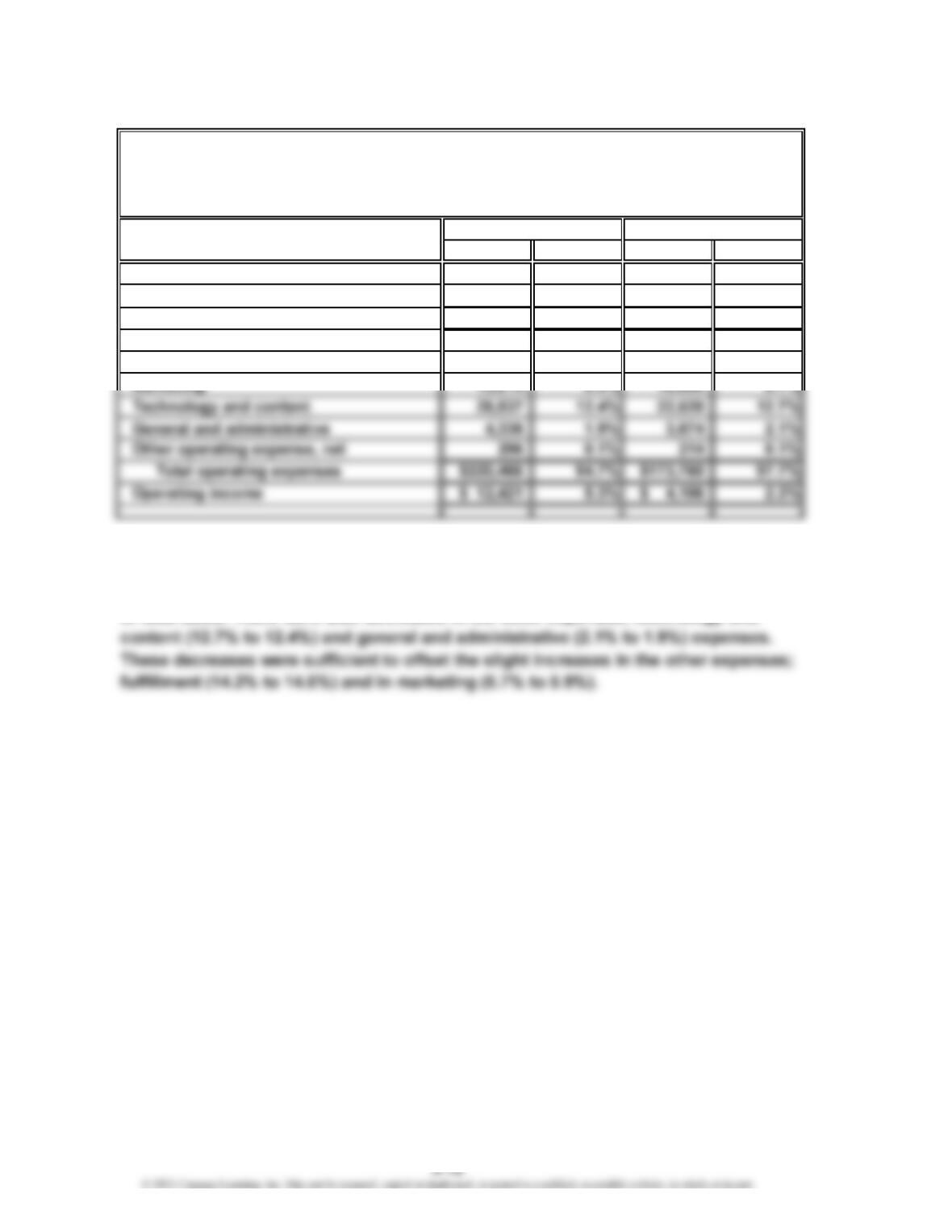

a.

Amount Percent Amount Percent

Product sales $141,915 60.9% $118,573 66.7%

Service sales 90,972 39.1% 59,293 33.3%

Total sales $232,887 100.0% $177,866 100.0%

Cost of sales $139,156 59.8% $111,934 62.9%

Fulfillment 34,027 14.6% 25,249 14.2%

b. The vertical analysis indicates that operating income increased from 2.3% to 5.3%

of total sales between the two years. Total expenses decreased from 97.7% to 94.7%

of total sales. There was a sizable decrease in the cost of sales from 62.9% to 59.8%

Amazon.com, Inc.

Operating Income Statements

For the Years Ended December 31

Year 2 Year 1

(in millions)

CHAPTER 3 The Adjusting Process

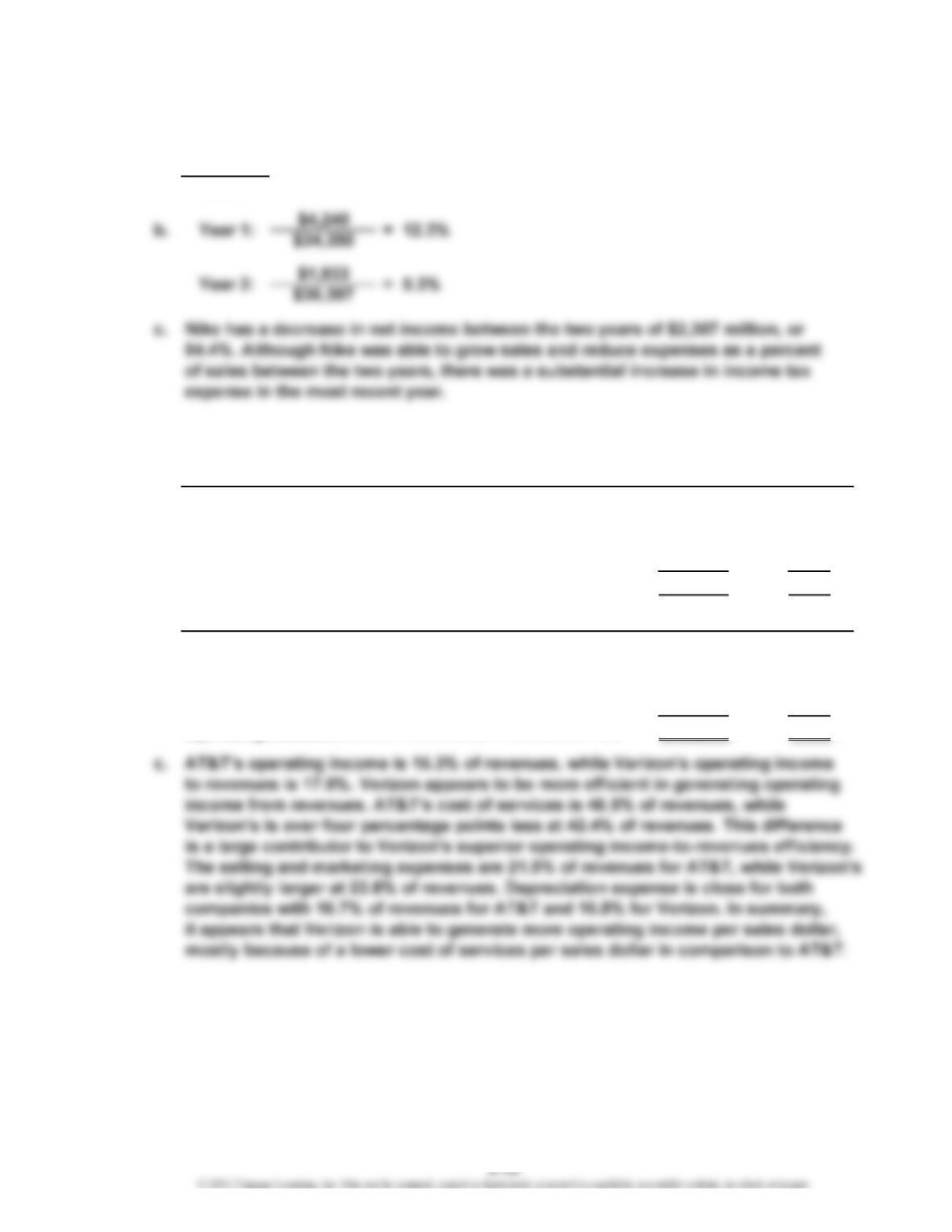

Ex. 3-29

a. Net income: $1,933 – $4,240 = –$2,307 million

($2,307)

$4,240

Ex. 3-30

a.

Revenues………………………………………………………

…

$170,756 100.0%

Cost of services (expense)…………………………………

…

(79,419) (46.5)%

Selling and marketing expense……………………………

…

(36,765) (21.5)%

Depreciation and other expenses…………………………

…

(28,476) (16.7)%

Operating income……………………………………………

…

$ 26,096 15.3%

b.

Revenues………………………………………………………

…

$130,863 100.0%

Cost of services (expense)…………………………………

…

(55,508) (42.4)%

Selling and marketing expense……………………………

…

(31,083) (23.8)%

Depreciation and other expenses…………………………

…

(21,994) (16.8)%

Operating income……………………………………………

…

$ 22,278 17.0%

= –54.4%

AT&T

Verizon

CHAPTER 3 The Adjusting Process

Prob. 3-1A

1. Dec. 31 Supplies Expense 1,265

Supplies 1,265

Supplies used ($1,585 – $320).

31 Accounts Receivable 21,610

Fees Earned 21,610

Accrued fees earned.

31 Depreciation Expense 3,340

Accumulated Depreciation—Office Equipment 3,340

Depreciation expense.

PROBLEMS

CHAPTER 3 The Adjusting Process

Prob. 3-2A

1. July 31 Accounts Receivable 11,150

Fees Earned 11,150

Accrued fees earned.

31 Depreciation Expense 8,950

Accumulated Depreciation—Equipment 8,950

Equipment depreciation.

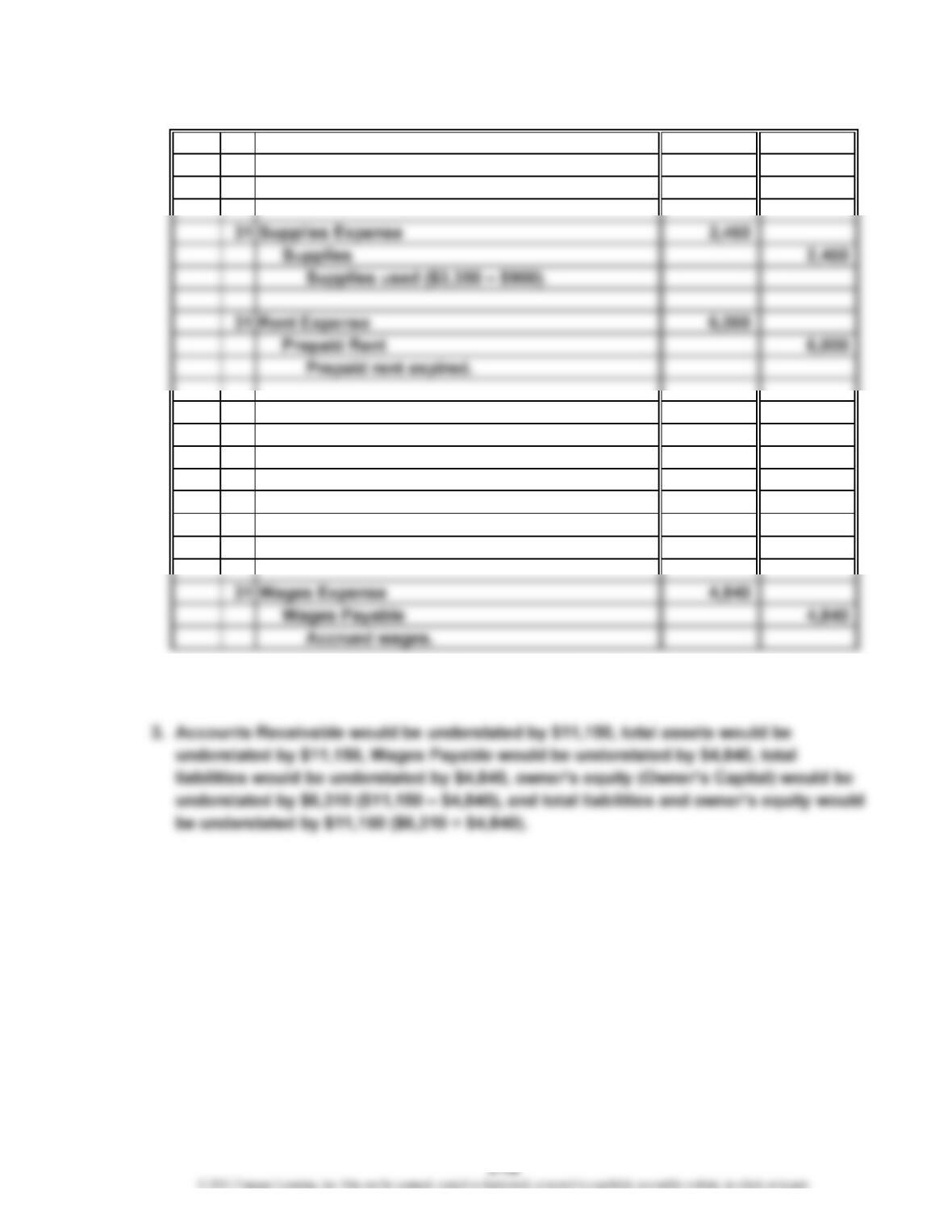

31 Unearned Fees 10,000

Fees Earned 10,000

Fees earned ($12,000 – $2,000).

2. Fees Earned would be understated by $11,150, Wages Expense would be understated

by $4,840, and net income would be understated by $6,310 ($11,150 – $4,840).

4. There is no effect on “Net increase or decrease in cash” on the statement of cash

flows because adjusting entries do not affect cash.

CHAPTER 3 The Adjusting Process

Prob. 3-3A

1. 20Y4

June 30 Accounts Receivable 7,380

Fees Earned 7,380

Accrued fees earned.

30 Unearned Fees 16,500

Fees Earned 16,500

Fees earned.

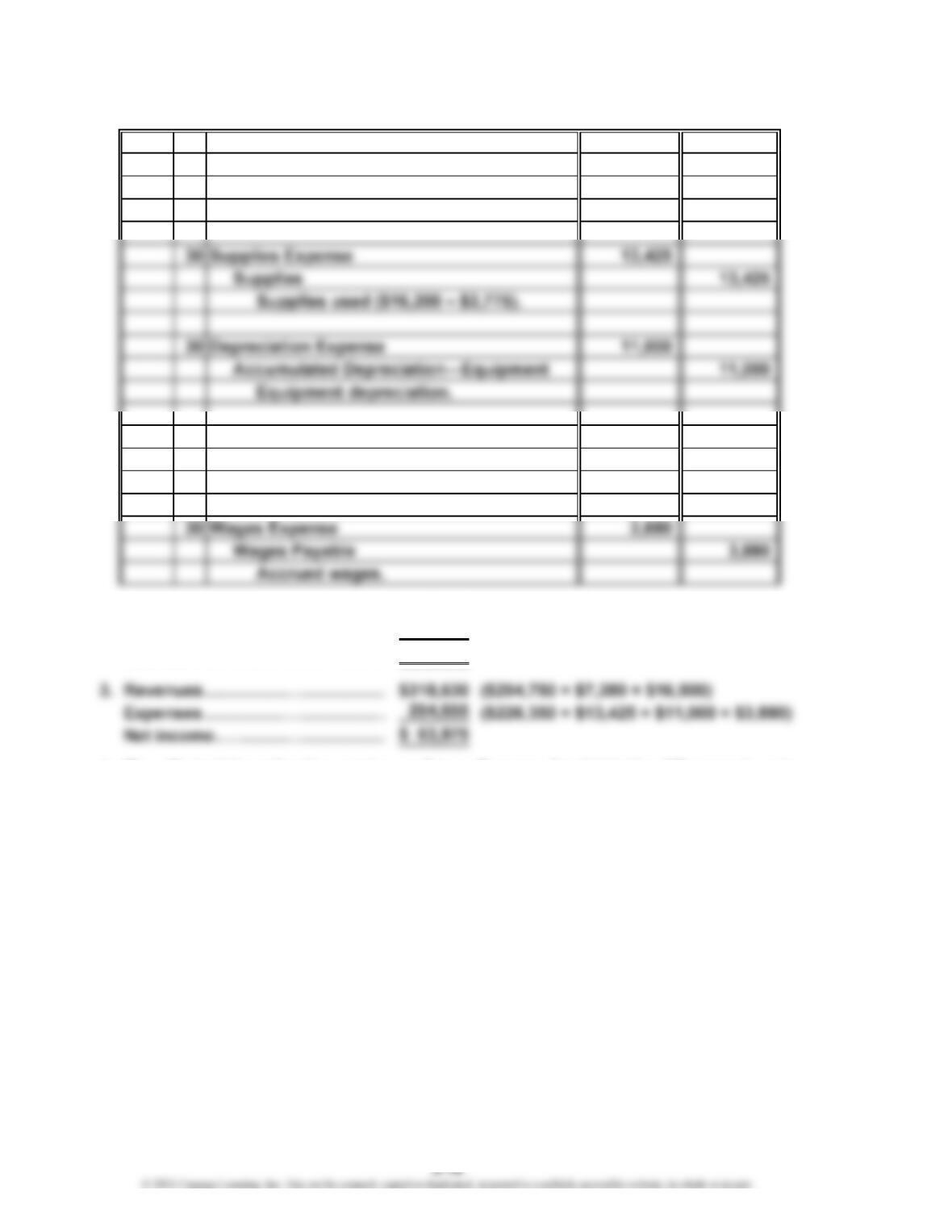

2. Revenues…………………………

…

$294,750

Expenses…………………………

…

226,350 ($94,500 + $72,000 + $51,750 + $8,100)

Net income…………………………

…

$ 68,400

…

…

…

4. The effect of the adjusting entries on Nancy Townes, Capital is the difference in net

income in (2) and (3) of $4,425 ($68,400 – $63,975). The adjusting entries reduced

net income by $4,425.

CHAPTER 3 The Adjusting Process

Prob. 3-4A

20Y5

Nov. 30 Supplies Expense 8,850

Supplies 8,850

Supplies used ($11,250 – $2,400).

30 Depreciation Expense—Automobiles 7,300

Accumulated Depreciation—Automobiles 7,300

Automobile depreciation

($62,050 – $54,750).

30 Unearned Service Fees 9,000

Service Fees Earned 9,000

Service fees earned ($18,000 – $9,000, or

$742,800 – $733,800).

1. 20Y6

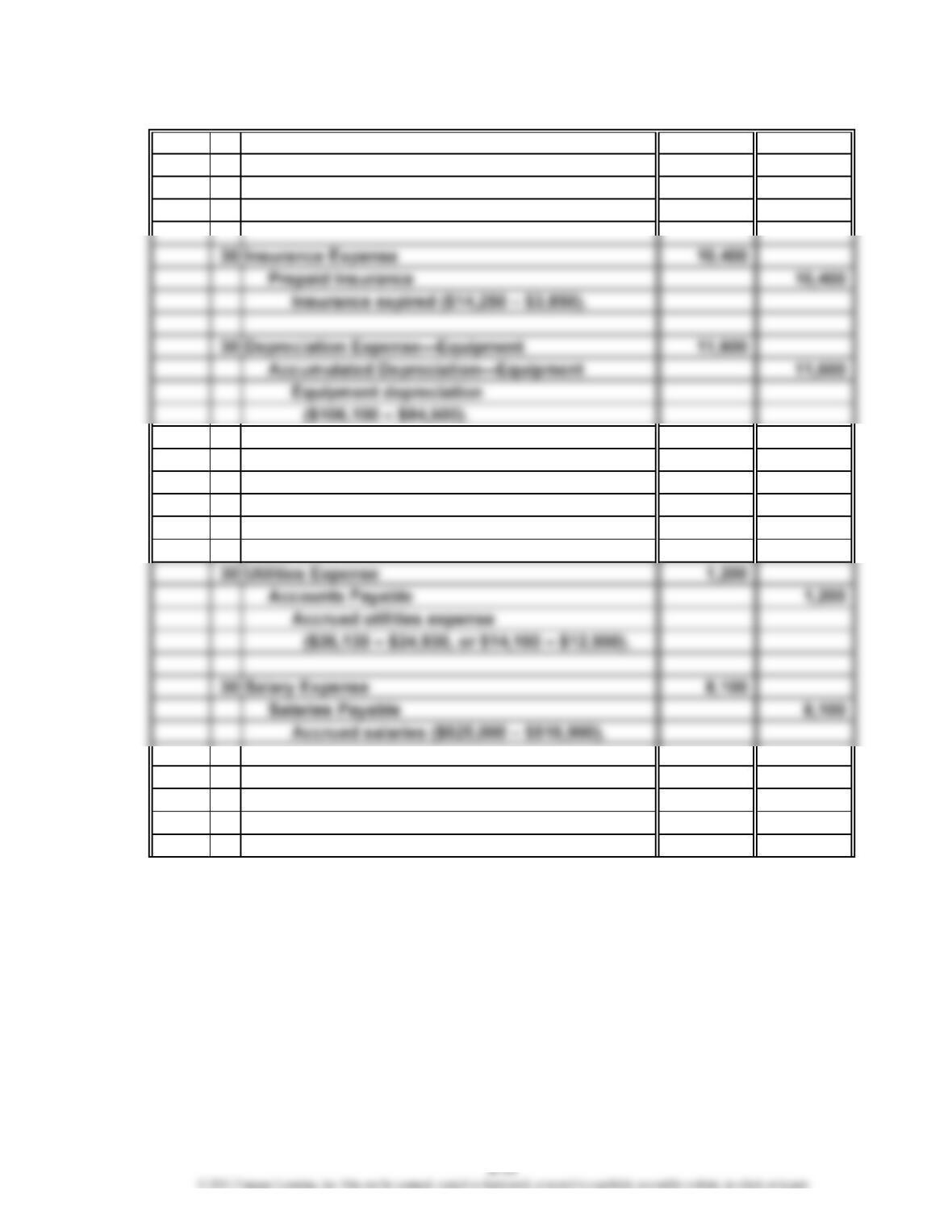

Oct. 31 Insurance Expense 6,000

Prepaid Insurance 6,000

Insurance expired ($6,550 – $550).

31 Depreciation Expense—Equipment 7,830

Accumulated Depreciation—Equipment 7,830

Equipment depreciation.

31 Unearned Rent 4,090

Rent Revenue 4,090

Rent revenue earned ($6,140 – $2,050).