SOLUTION

Chapter 3 Waterways Continuing Problem

(a) Production Report—Weighted-Average

Method

WATERWAYS CORPORATION

Molding Department Production Report

For the month of January, 2017

Equivalent Units

Physical

Units

Materials

Conversion

Quantities

Units to be accounted for:

Work in process, Jan 1 (80% materials, 30% conversion) ……………

22,000

Started into production ……………………………………………………………

60,000

Total units ……………………………………………………………………………….

82,000

Units accounted for:

Costs

Unit costs

Materials

Conversion

Costs

Total

Costs in January* …………………………………………………………………..

(a)

$433,300

$434,880

$868,180

Equivalent units ……………………………………………………………………..

(b)

Unit costs [(a)/(b)] ………………………………………………………………….

Costs to be accounted for

Work in process, January 1 ………………………………………………………

$253,194

Started into production …………………………………………………………….

Total costs ……………………………………………………………………………

$868,180

Conversion costs—$67,564 + $17,270 + $289,468 + $60,578

Cost Reconciliation Schedule

Costs accounted for

Transferred out (58,000 X $13.39) ……………………………………………

$776,620

Work in process, Jan 31

Materials (12,000 X $6.19) ……………………………………………………..

Conversion (2,400 X $7.20) ……………………………………………………

Total costs

$868,180

Transferred out ………………………………………………………………………

58,000

Work in process, Jan 31 (50% materials, 10% conversion) …………..

24,000

Total units ……………………………………………………………………………….

82,000

*(b) Equivalent Units—FIFO Method

Equivalent Units

Physical

Units

Materials

Conversion

Units accounted for

Completed and transferred out

Work in process, January 1 (20% materials, 70% conversion) …….

22,000

4,400

15,400

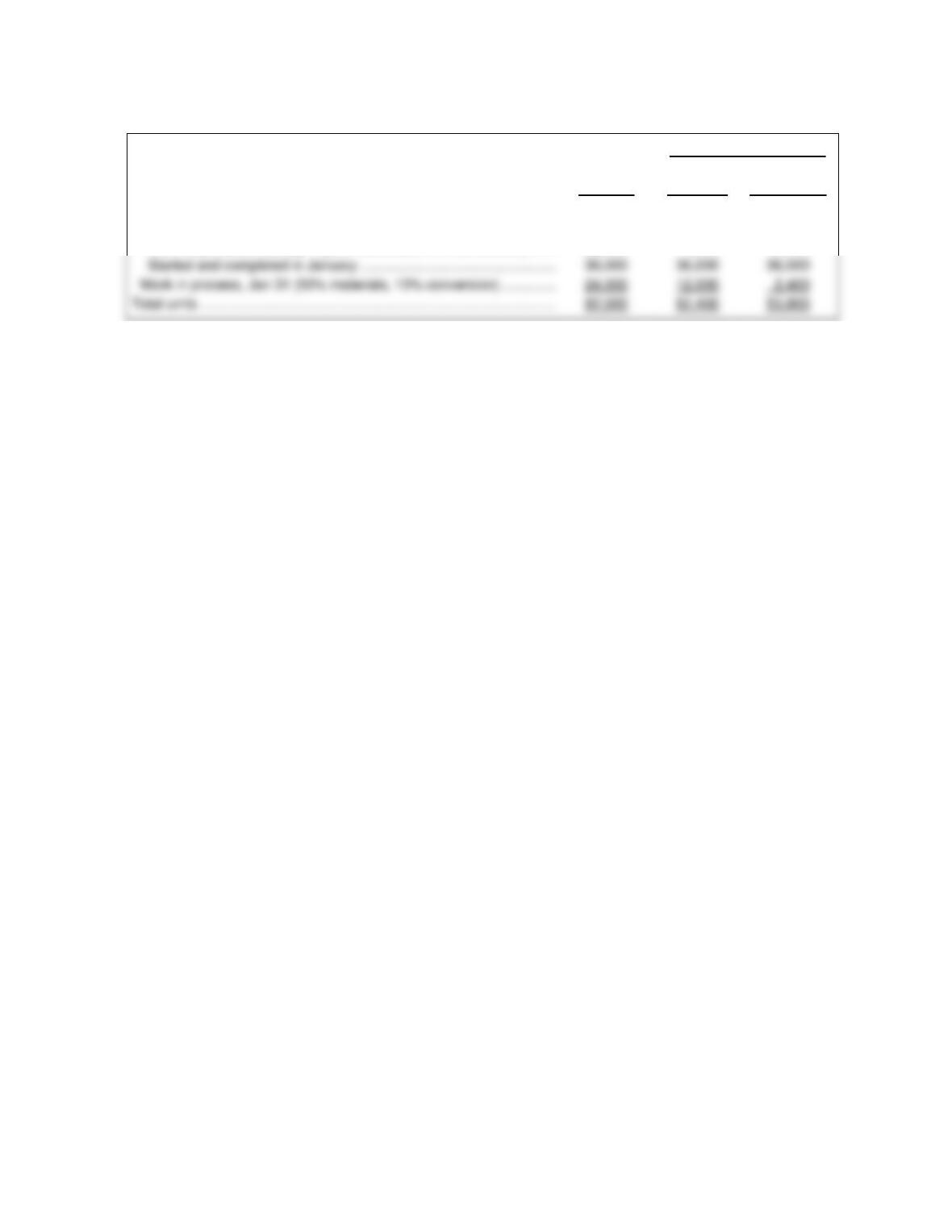

Started and completed in January …………………………………………..

36,000

36,000

Work in process, Jan 31 (50% materials, 10% conversion) …………..

24,000