CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Prob. 17–4B (FIN MAN); Prob. 3–4B (MAN) (Continued)

2.

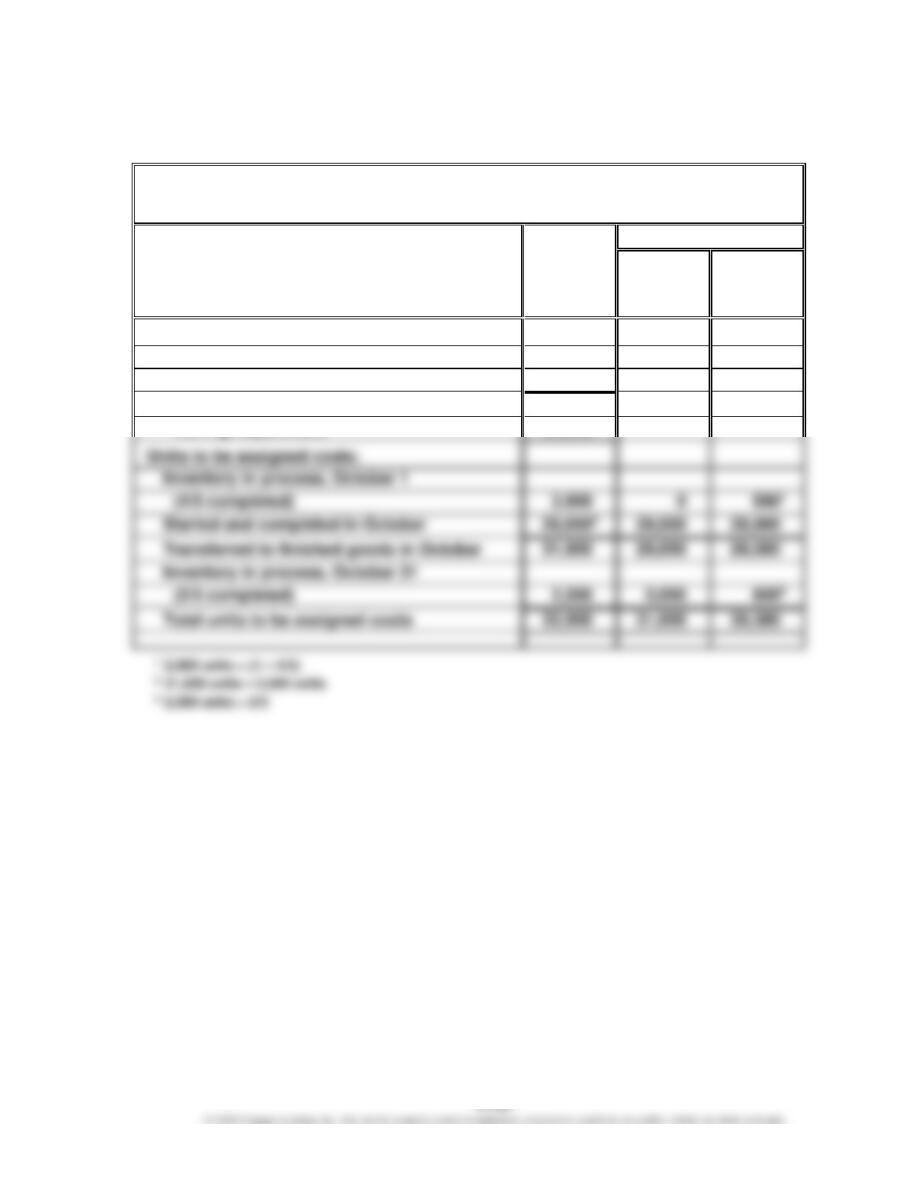

Pittsburgh Aluminum Company

Cost of Production Report—Rolling Department

For the Month Ended October 31

UNITS

Whole

Units

Equivalent Units

Direct

Materials

(a)

Conversion

(a)

Units charged to production:

Inventory in process, October 1

2,900

Received from Smelting Department

31,000

Total units accounted for by the

Units to be assigned costs:

Inventory in process, October 1

Transferred to finished goods in October

31,900

29,000

29,580

Inventory in process, October 31

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Prob. 17–4B (FIN MAN); Prob. 3–4B (MAN) (Concluded)

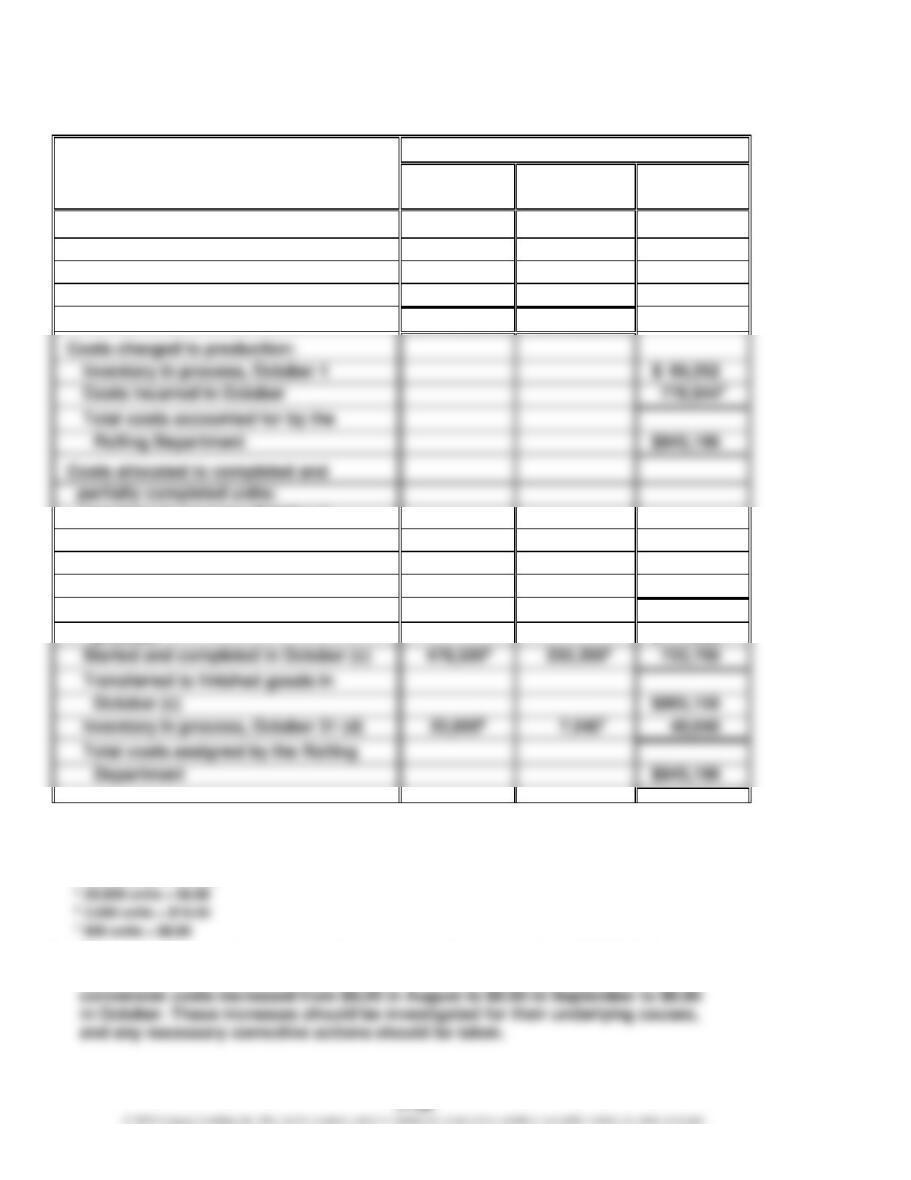

COSTS

Costs

Direct

Materials

Conversion

Total

Cost per equivalent unit:

Total costs for October in Rolling

Department

$511,500

$267,3441

Total equivalent units

÷ 31,000

÷ 30,380

Cost per equivalent unit (b)

$ 16.50

$ 8.80

Inventory in process, October 1

$ 66,352

Costs incurred in October

Total costs accounted for by the

Rolling Department

Costs allocated to completed and

Inventory in process, October 1

balance (c)

$ 66,352

To complete inventory in process,

October 1 (c)

$ 0

$ 5,1043

5,104

Cost of completed October 1 work in

Started and completed in October (c)

Transferred to finished goods in

October (c)

Inventory in process, October 31 (d)

Total costs assigned by the Rolling

1 $162,850 + $104,494

2 $511,500 + $162,850 + $104,494

3 580 units × $8.80

4 29,000 units × $16.50

3. The cost per equivalent unit for direct materials increased from $15.50 in August

to $16.00 in September to $16.50 in October. The cost per equivalent unit for

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

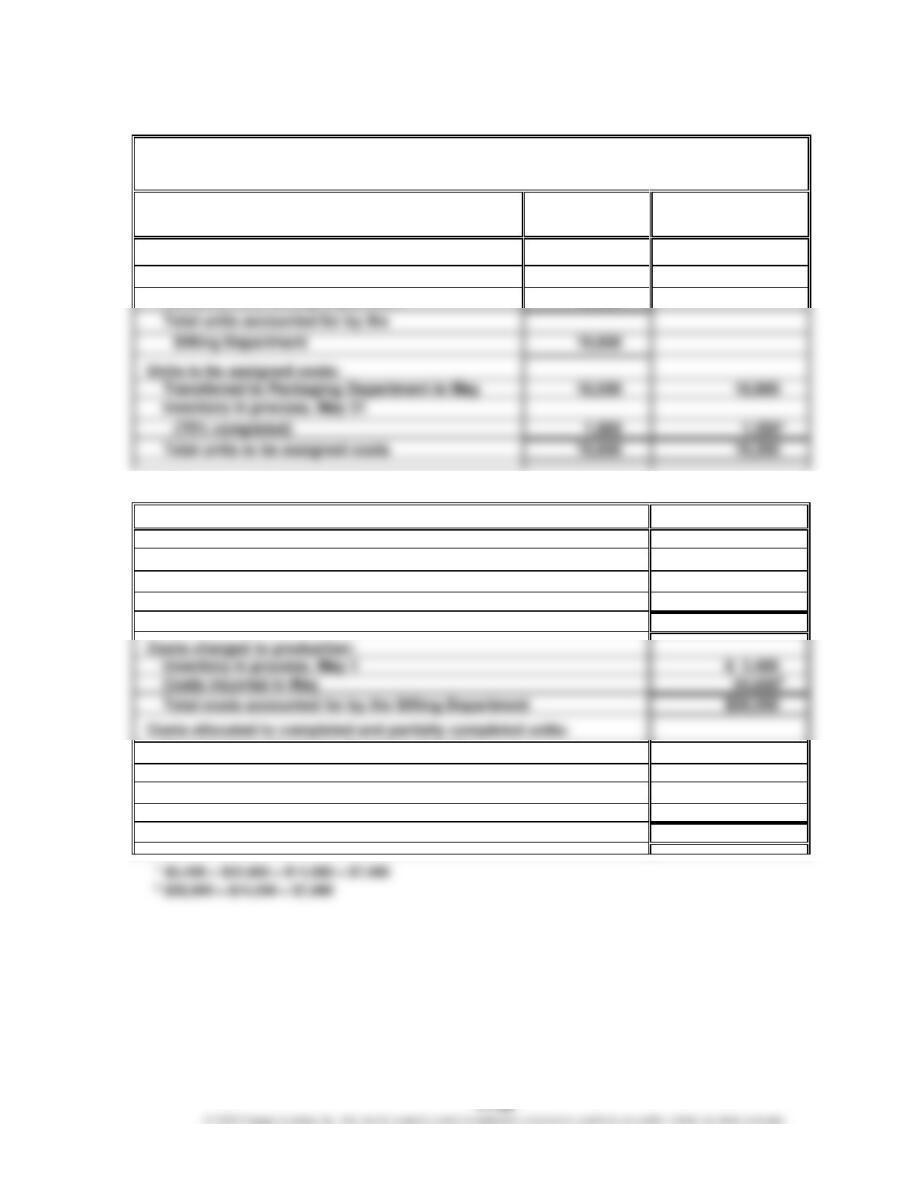

Appendix Prob. 17–5B (FIN MAN); Appendix Prob. 3–5B (MAN)

Blue Ribbon Flour Company

Cost of Production Report—Sifting Department

For the Month Ended May 31

UNITS

Whole

Units

Equivalent Units

of Production

Units charged to production:

Inventory in process, May 1

1,500

Received from Milling Department

18,300

Total units accounted for by the

19,800

Units to be assigned costs:

Transferred to Packaging Department in May

Inventory in process, May 31

(75% completed)

Total units to be assigned costs

*75% units × 1,800 units

COSTS

Costs

Cost per equivalent unit:

Total costs for May in Sifting Department

$58,0501

Total equivalent units

÷19,350

Cost per equivalent unit

$ 3.00

Inventory in process, May 1

Costs incurred in May

Total costs accounted for by the Sifting Department

$58,050

Transferred to Packaging Department in May

(18,000 units × $3.00)

$54,000

Inventory in process, May 31

(1,800 units × 75% × $3.00)

4,050

Total costs assigned by the Sifting Department

$58,050

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

MAKE A DECISION

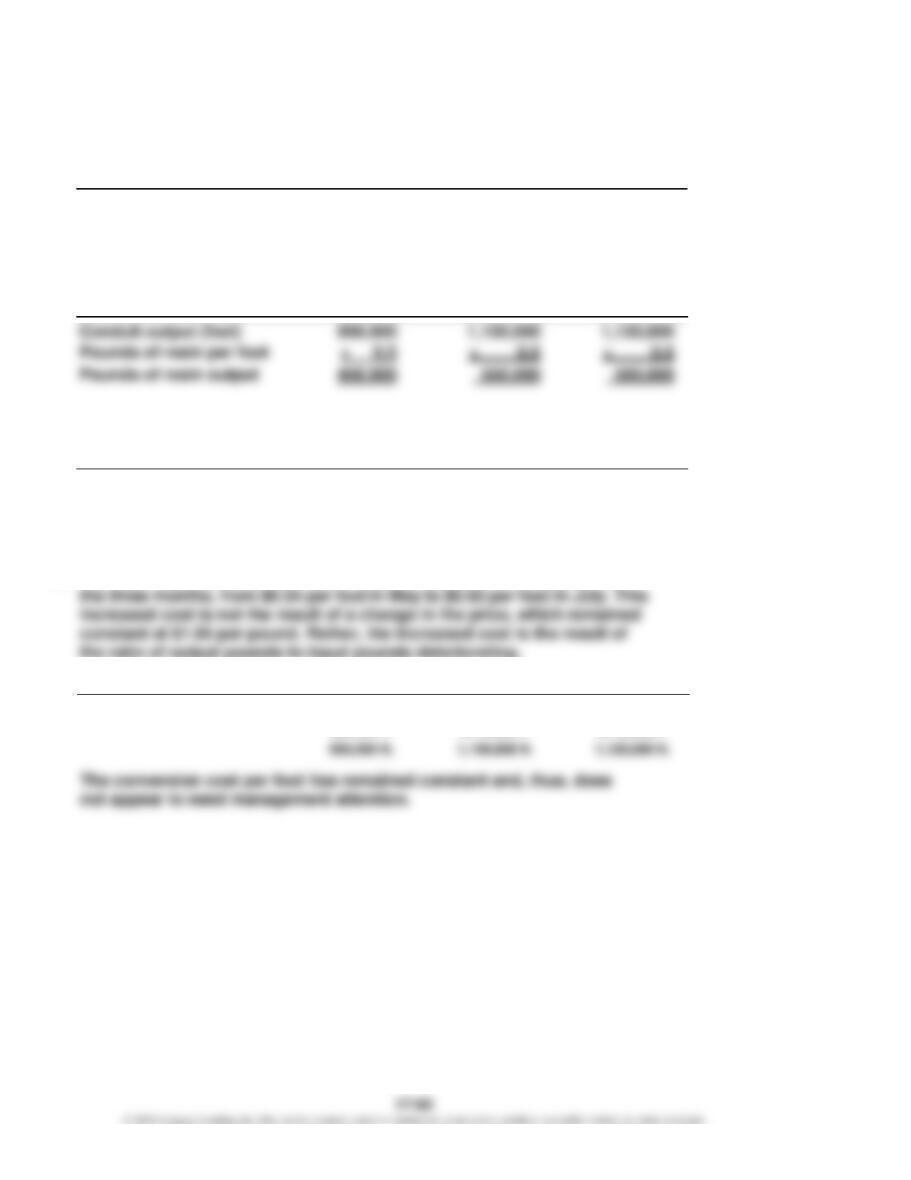

MAD 17–1 (FIN MAN); MAD 3–1 (MAN)

a.

May

June

July

Resin cost per foot

$0.54

$0.57

$0.60

$483,000 ÷

$630,000 ÷

$672,000 ÷

900,000 ft.

1,100,000 ft.

1,120,000 ft.

b.

Pounds of resin:

May

June

July

Conduit output (feet)

Ratio of output pounds to input pounds:

May

June

July

Resin output pounds

divided by input pounds

97.8%

91.7%

87.5%

450,000 ÷

550,000 ÷

560,000 ÷

460,000

600,000

640,000

c. The resin materials cost per foot of finished product is increasing over

the ratio of output pounds to input pounds deteriorating.

d.

May

June

July

Conversion cost per foot

$0.10

$0.10

$0.10

$110,000 ÷

$112,000 ÷

1,100,000 ft.

1,120,000 ft.

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

MAD 17–2 (FIN MAN); MAD 3–2 (MAN)

Memo

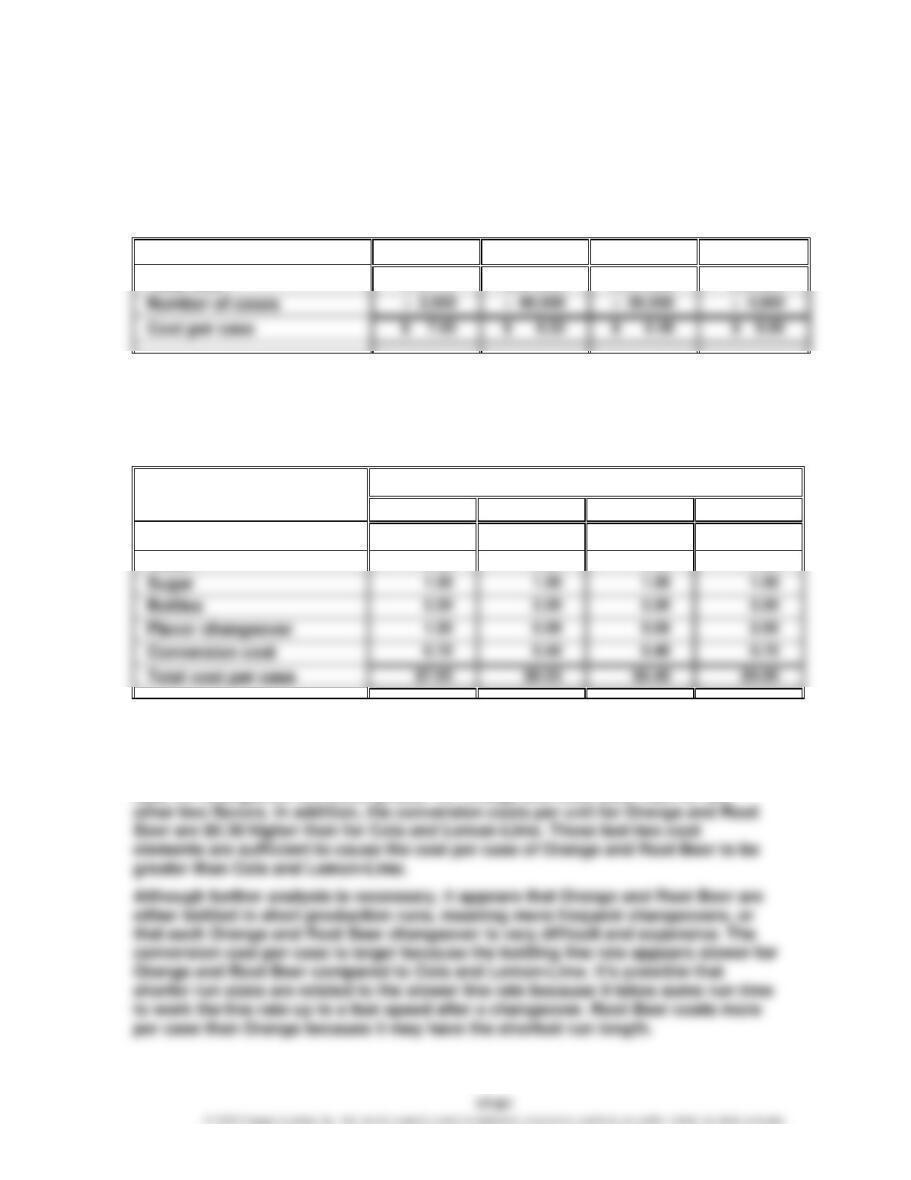

To: Production Manager

The cost of production report is used to identify the cost per case for each of the four

flavors as follows:

Orange

Cola

Lemon-Lime

Root Beer

$19,125

$391,800

$324,000

$36,000

As can be seen, the cost per case of Root Beer is significantly above the cost per

case of the other three flavors. A more detailed analysis is necessary to

understand the causes of this difference. The individual cost elements that

determine the total cost can be divided by the number of cases. This analysis

follows:

Cost per Case by Cost Element

Orange

Cola

Lemon-Lime

Root Beer

Concentrate

$1.85

$2.15

$2.10

$1.90

Water

0.70

0.40

0.40

0.70

0.50

0.50

0.50

0.50

This table indicates that the concentrate per case is actually less for Orange and

Root Beer than for Cola and Lemon-Lime. This is because the concentrate

supplier charges a higher price for the more popular flavors. The costs per case

for water, sugar, and bottles are the same for each flavor. However, the costs per

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

MAD 17–3 (FIN MAN); MAD 3–3 (MAN)

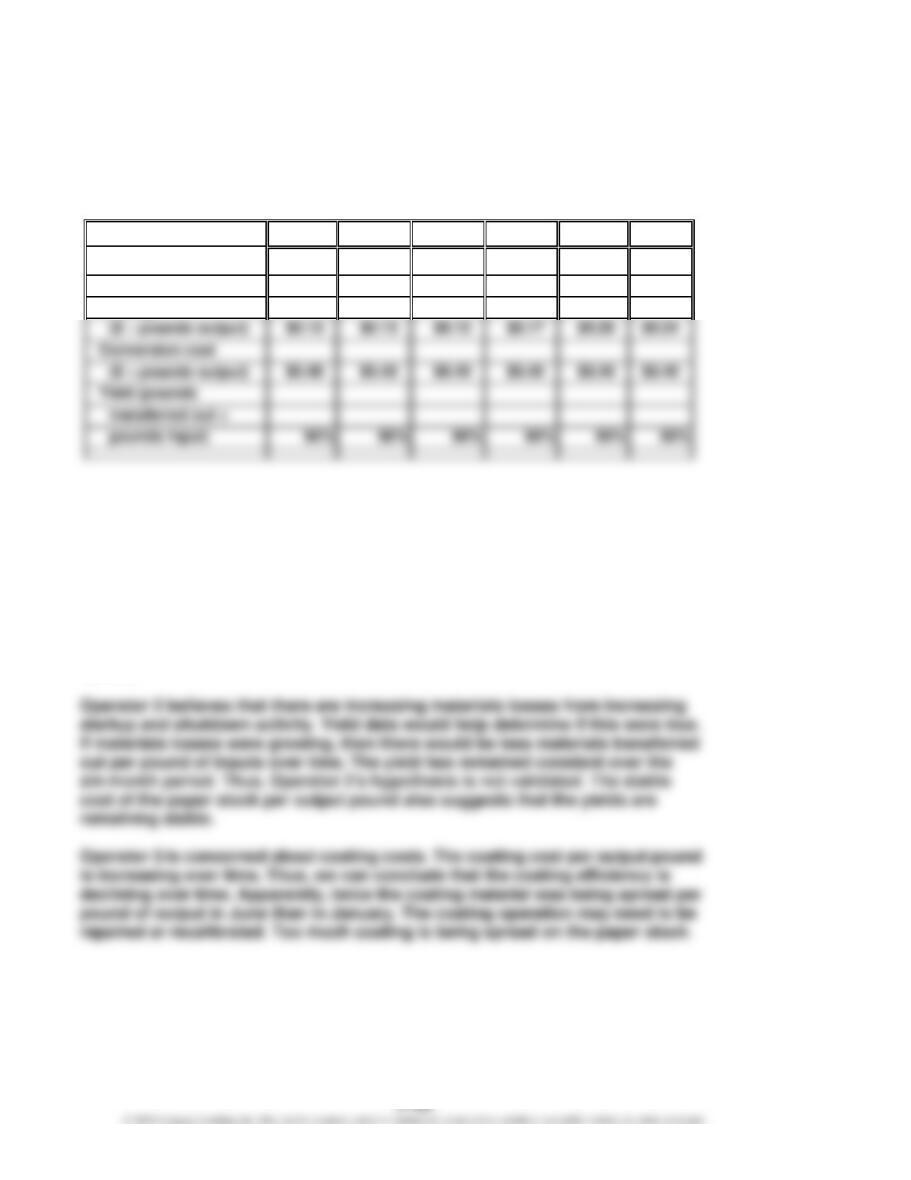

The solution to this exercise is to determine if the cost per pound trends in paper

stock, conversion, and coating costs are remaining stable over time. The following

table can be developed from the data:

a.

January

February

March

April

May

June

Paper stock

($ ÷ pounds output)

$0.70

$0.70

$0.70

$0.70

$0.70

$0.70

Coating

($ ÷ pounds output)

$0.12

$0.13

$0.15

$0.17

$0.20

$0.24

($ ÷ pounds output)

$0.40

$0.40

$0.40

$0.40

$0.40

$0.40

transferred out ÷

The cost per pound information is determined by dividing the costs by the

pounds transferred out. The yield is determined by dividing the pounds

transferred out by the pounds input.

b. Operator 1 believes that energy consumption is becoming less efficient. The

energy cost is part of the conversion cost. The conversion cost per output

pound has remained constant for the six months. If the energy efficiency were

declining, it would take more energy per pound of output over time. Thus, we

would expect to see the conversion rate per pound increasing if Operator 1 were

correct.

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

MAD 17–4 (FIN MAN); MAD 3–4 (MAN)

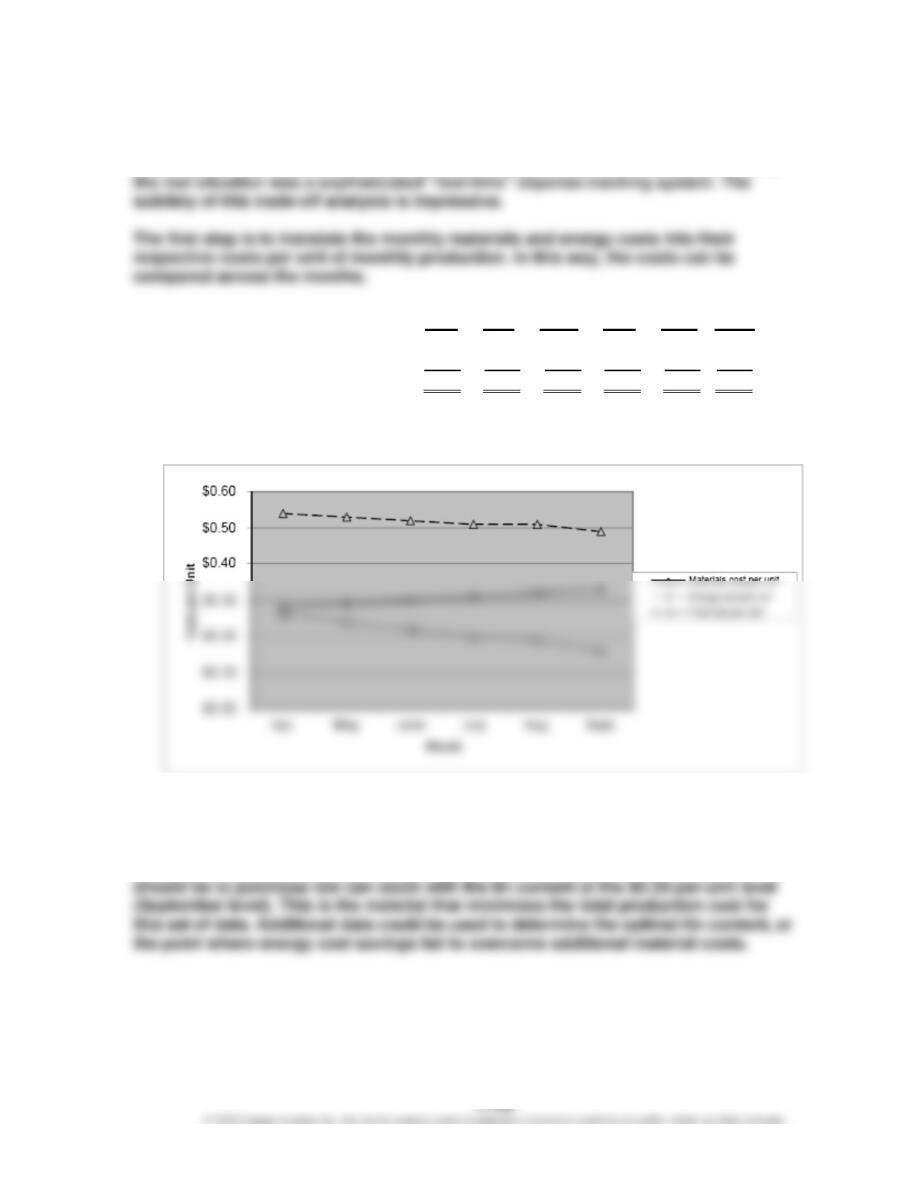

This case is abstracted from a real situation, where higher raw materials costs due

to tin content were more than offset by lower energy costs. The cost system used in

Apr.

May

June

July

Aug.

Sept.

Materials cost per unit ……………..

$0.28

$0.29

$0.30

$0.31

$0.32

$0.33

Energy cost per unit ………………..

0.26

0.24

0.22

0.20

0.19

0.16

Total cost per unit …………………..

$0.54

$0.53

$0.52

$0.51

$0.51

$0.49

The graph below shows the total unit cost data for each month.

The graph reveals that the tin content and energy costs are inversely related. That is,

as the materials cost increased due to higher tin content, the energy costs dropped

by more. In fact, the total cost line shows that the energy savings exceeds the

additional materials cost, due to higher tin content. Thus, the recommendation

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

TAKE IT FURTHER

TIF 17–1 (FIN MAN); TIF 3–1 (MAN)

1. This case comes from a real story. In the real story, the first reduction in chips had no

impact on market demand. The manager was promoted, and the next manager

2. There are several options that you, as the controller, have:

a. Do nothing. This is a safe strategy. It would be highly unlikely that failing to reveal

this information to anybody would ever be discovered or “pinned” on you.

Unfortunately, this is one of those situations where silence has very little penalty,

yet speaking up entails some risk. However, silence may not be the best option.

Silence may allow the product quality erosion to continue, which could be harmful

with Brandon.

c. Talk to the vice president. You could also go right over Brandon’s head to the vice

president. This strategy might label you as “not a team player,” so some caution is

in order here. You might get Brandon in trouble, or you may get yourself in some

trouble. This is probably not the best first move. It is within Brandon’s authority to

make the chip decision, so you are, in a sense, second- guessing Brandon when

you go to the vice president. You could be accused of being out of your expertise.

After all, what do you know about chips and the marketplace?

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

TIF 17–2 (FIN MAN); TIF 3–2 (MAN)

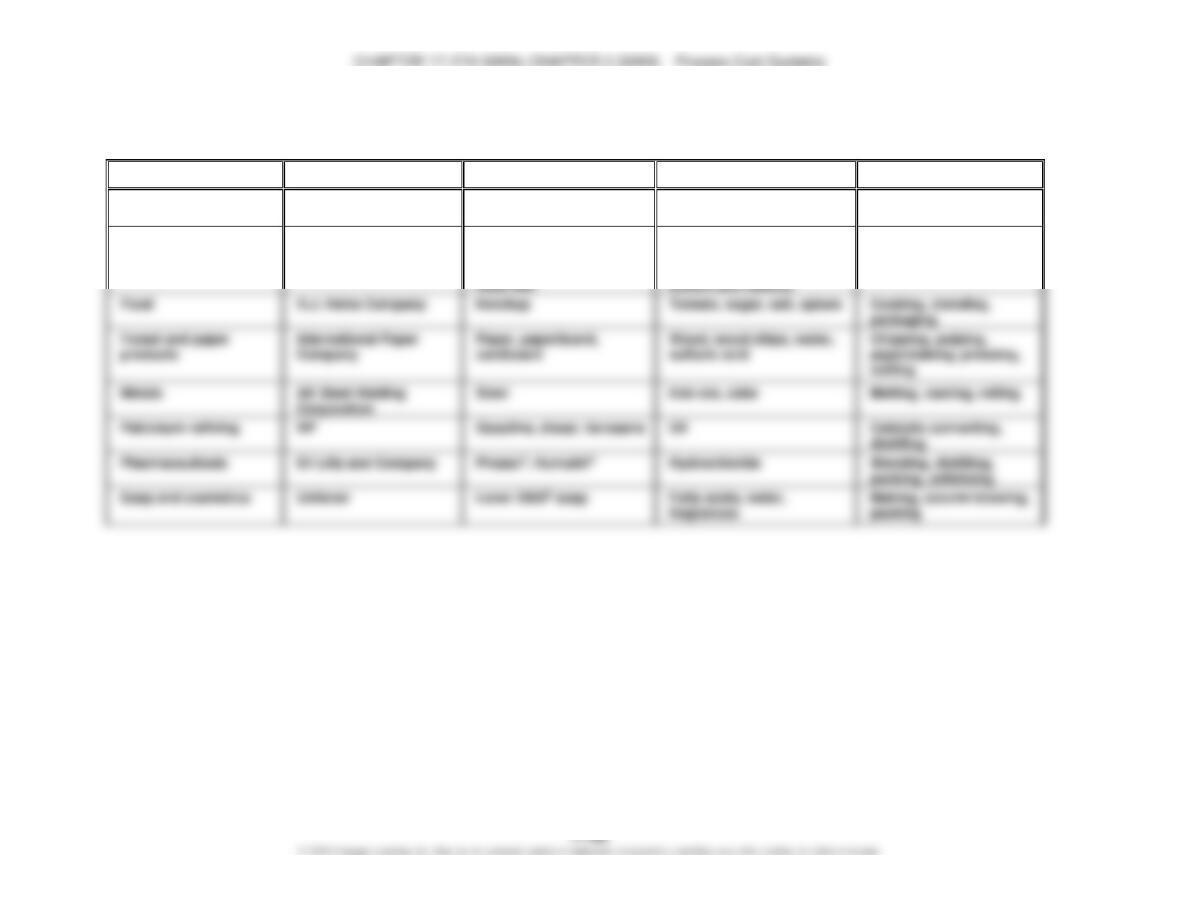

This activity can be accomplished with multiple groups assigned to one or more of the

industry categories. Assign at least one group to each industry category. (Some are

TIF 17–2 (FIN MAN); TIF 3–2 (MAN) (Concluded)

Industry Category

Example Company

Products

Materials

Processes

Beverages

PepsiCo, Inc.

Pepsi, Diet Pepsi

Sugar, carbonated water,

concentrate

Mixing, bottling

Chemicals

E. I. du Pont de Nemours

and Company

Stain master®, Kevlar®,

Lycra®, Teflon®,

refrigerants, electronic

materials

Petroleum refining

Gasoline, diesel, kerosene

Oil

Catalytic converting,

distilling

Petroleum and

petroleum-based

intermediates

Reaction, blending,

distilling, extruding

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

TIF 17–3 (FIN MAN); TIF 3–3 (MAN)

Memo

To: Jamarcus Bradshaw

From: Ima Student

Re: Analysis of August Increase in Unit Cost for Papermaking Department

The increase in the unit costs from July to August occurred for both the materials (pulp

and chemicals) and conversion costs in the Papermaking Department, as indicated in the

table below.

Materials cost per ton …………………………………………

Conversion cost per ton ……………………………………..

Fortunately, we run both colors on paper machine No. 1. Thus, we can separate the analysis

between these two possible explanations. I have provided the following cost- per-ton data

for the two paper machines and the two product colors:

Paper machine analysis:

Materials

Cost per Ton

Conversion

Cost per Ton

Total

Paper machine No. 1 ………………………….

$290.54

$143.04

$433.58

Paper machine No. 2 ………………………….

Difference ………………………………………….

Cost per Ton

Green ………………………………………………..

$269.15

TIF 17–3 (FIN MAN); TIF 3–3 (MAN) (Continued)

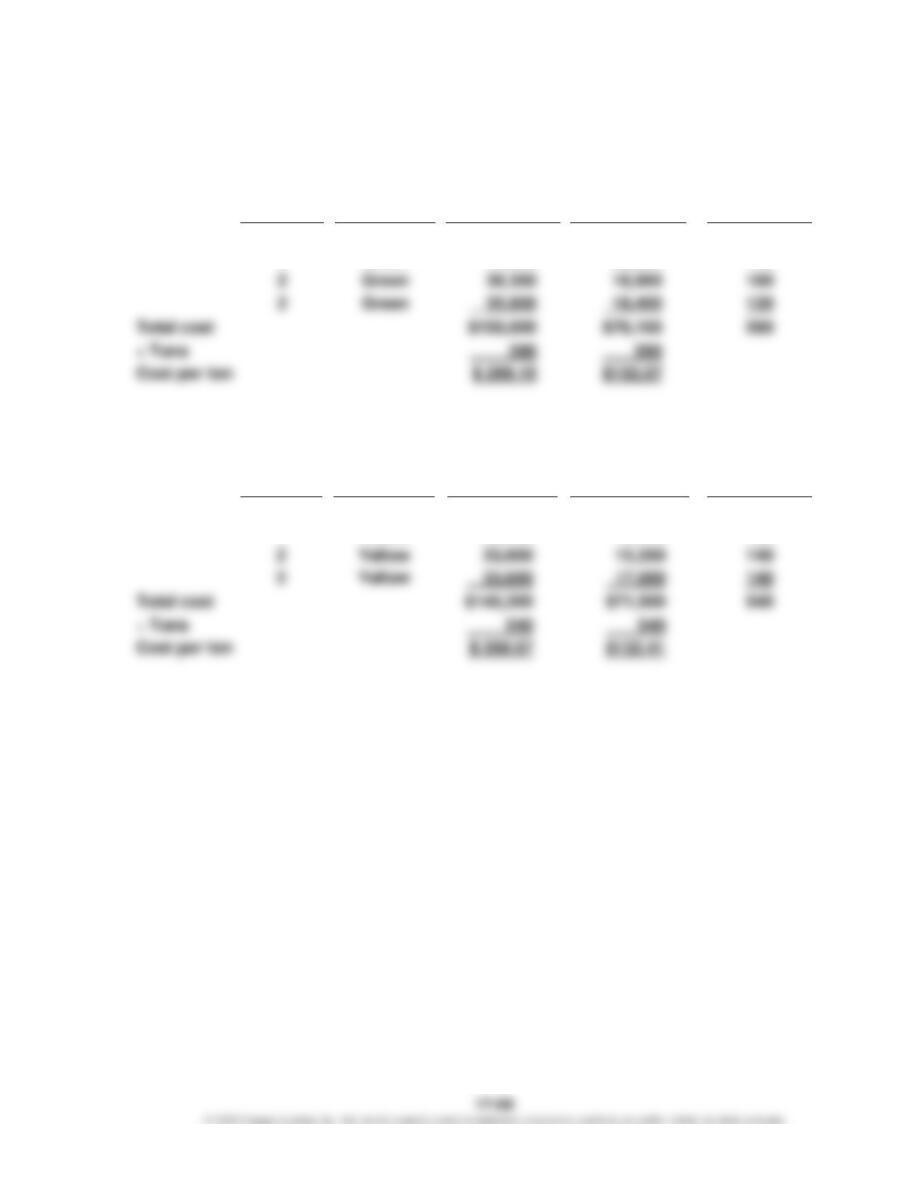

The results are clear. Paper machine No. 1 had a much higher materials and conversion

cost per ton in August. Apparently, the paper machine is overapplying pulp. This is

Supporting calculations:

Machine No. 1:

Materials

Conversion

Machine

Color

Cost

Cost

Tons

1

Green

$ 40,300

$18,300

150

1

Yellow

41,700

21,200

140

1

Yellow

120

560

Machine No. 2:

Machine

Color

Materials

Cost

Conversion

Cost

Tons

2

Yellow

15,200

2

Green

$ 38,300

$18,900

160

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

TIF 17–3 (FIN MAN); TIF 3–3 (MAN) (Concluded)

Green Paper Color:

Materials

Conversion

Machine

Color

Cost

Cost

Tons

1

Green

$ 40,300

$18,300

150

590

1

Green

44,600

22,500

150

Yellow Paper Color:

Materials

Conversion

Machine

Color

Cost

Cost

Tons

1

Yellow

$ 41,700

$21,200

140

1

Yellow

36,100

18,100

120

TIF 17–4 (FIN MAN); TIF 3–4 (MAN)

a. This accounting procedure has the effect of rewarding the production of broke.

b. The accounting for broke that is typical in the industry fails to account for the

total impact of broke. It is true that the use of recycled materials may reduce the

direct materials cost to the operation. However, such a view is very limited. For

example, the production of broke has a cost. Machine capacity was used to

is not captured by most accounting systems in the accounting for broke.

There are other hidden costs. Broke production makes the total amount

produced difficult to predict. As a result of this source of variation (broke),

production schedules are difficult to maintain. For example, if a particular

production run has a high amount of broke, then the scheduled run will need to

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1.

d.

Krause’s equivalent units for conversion costs are 92 units, computed as

follows:

Beginning work in process (20 units × 40%) ………………………………

8

units

Units started and completed (100 units – 20 units) ……………………..

80

Ending work in process (10 units × 40%) …………………………………..

4

Total …………………………………………………………………………………..

92

units

2.

a.

Jones’s equivalent units for conversion costs is 87,300 units, computed as

follows:

Beginning inventory [10,000 units × (100% – 75%)] …………………….

2,500

units

Started and completed in August (90,000 units – 10,000 units) ……

80,000

Total …………………………………………………………………………………..

87,300

units

3.

c.

Kimbeth’s equivalent units for conversion costs is 98,400 units, computed as

follows:

Beginning inventory [16,000 units × (100% – 20%)] …………………….

12,800

units

Started and completed in May (100,000 units – 24,000 units) ………

76,000

Ending inventory (24,000 units × 40%) ……………………………………….

9,600

Total …………………………………………………………………………………..

98,400

units

4.

c.

Equivalent units for the period are 24,500 units, computed as follows:

Started and completed during period

15,000

Total …………………………………………………………………………………..

24,500

units

Beginning inventory [5,000 units × (100% – 30%)] ………………………

3,500

units