3-21

PROBLEM 3-43 (35 MINUTES)

1. Predetermined overhead rate = budgeted overhead ÷ budgeted direct-labor cost

4. Since there is no work in process at year-end, all amounts in the Work-in-Process

account must be transferred to Finished-Goods Inventory. Thus:

5. BBBC’s applied overhead totals 130% of direct-labor cost, or $2,827,500 ($2,175,000 x

130%). Actual overhead was $2,777,000, itemized as follows, resulting in overapplied

overhead of $50,500.

Indirect materials used …………………………………….

$ 32,500

Indirect labor …………………………………………………..

1,430,000

Factory depreciation ………………………………………..

870,000

Factory insurance ……………………………………………

29,500

Factory utilities ……………………………………………….

415,000

$2,777,000

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-22

PROBLEM 3-43 (CONTINUED)

6. The company’s cost of goods sold totals $7,654,650:

Finished-goods inventory, Jan. 1…………….

$ 0

7. No, selling and administrative expenses are operating expenses of the firm and are

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-23

PROBLEM 3-44 (45 MINUTES)

NOTE: The 12/31/x4 balances for cash and accounts receivable, although given in the

problem, are irrelevant to the solution.

1.

MISTER MUNCHIE, INC.

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE YEAR ENDED DECEMBER 31, 20X4

Direct material:

Raw-material inventory, 12/31/x3 ………………………………………

$ 30,300

Add: Purchases of raw material ………………………………………..

Raw material available for use ………………………………………….

$147,300

Deduct: Raw-material inventory, 12/31/x4 ………………………….

Raw material used ……………………………………………………….

$114,300

Direct labor ……………………………………………………………………………

Manufacturing overhead:

Indirect material ………………………………………………………………

$ 14,700

Indirect labor …………………………………………………………………..

87,000

Depreciation on factory building ………………………………………

11,400

Depreciation on factory equipment …………………………..………

Utilities ……………………………………………………………………………

18,000

Property taxes …………………………………………………………………

7,200

Insurance ………………………………………………………………………..

10,800

Rental of warehouse space† ……………………………………………..

Total actual manufacturing overhead …………………………..

$164,700

Add: Overapplied overhead* …………………………………………

Overhead applied to work in process …………………………..

Total manufacturing costs ……………………………………………………..

$525,300

Add: Work-in-process inventory, 12/31/x3 …………………………..

Subtotal …………………………………………………………………………………

$549,600

Deduct: Work-in-process inventory, 12/31/x4 …………………………..

Cost of goods manufactured …………………………………………………..

$524,700

*The Schedule of Cost of Goods Manufactured lists the manufacturing costs applied to work

3-24

PROBLEM 3-44 (CONTINUED)

2.

MISTER MUNCHIE, INC.

SCHEDULE OF COST OF GOODS SOLD

FOR THE YEAR ENDED DECEMBER 31, 20X4

Finished-goods inventory, 12/31/x3 ………………………………………………………….

$ 42,000

Add: Cost of goods manufactured* ………………………………………………………….

Cost of goods available for sale …………………………..………………………………….

Deduct: Finished-goods inventory, 12/31/x4 …………………………………………….

Cost of goods sold ………………………………………………………………………………….

Deduct: Overapplied overhead† ……………………………………………………………….

Cost of goods sold (adjusted for overapplied overhead) …………………………..

3.

MISTER MUNCHIE, INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20X4

Sales revenue ……………………………………………………..

$617,400

Less: Cost of goods sold …………………………………….

511,200

Gross margin ………………………………………………………

$106,200

Selling and administrative expenses:

Salaries ………………………………………………………..

Utilities …………………………………………………………

Depreciation …………………………………………………

Rental of office space ……………………………………

Other expenses …………………………………………….

Total ……………………………………………………………..

Income before taxes …………………………………………….

Income tax expense …………………………………………….

Net income ………………………………………………………….

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-25

PROBLEM 3-45 (25 MINUTES)

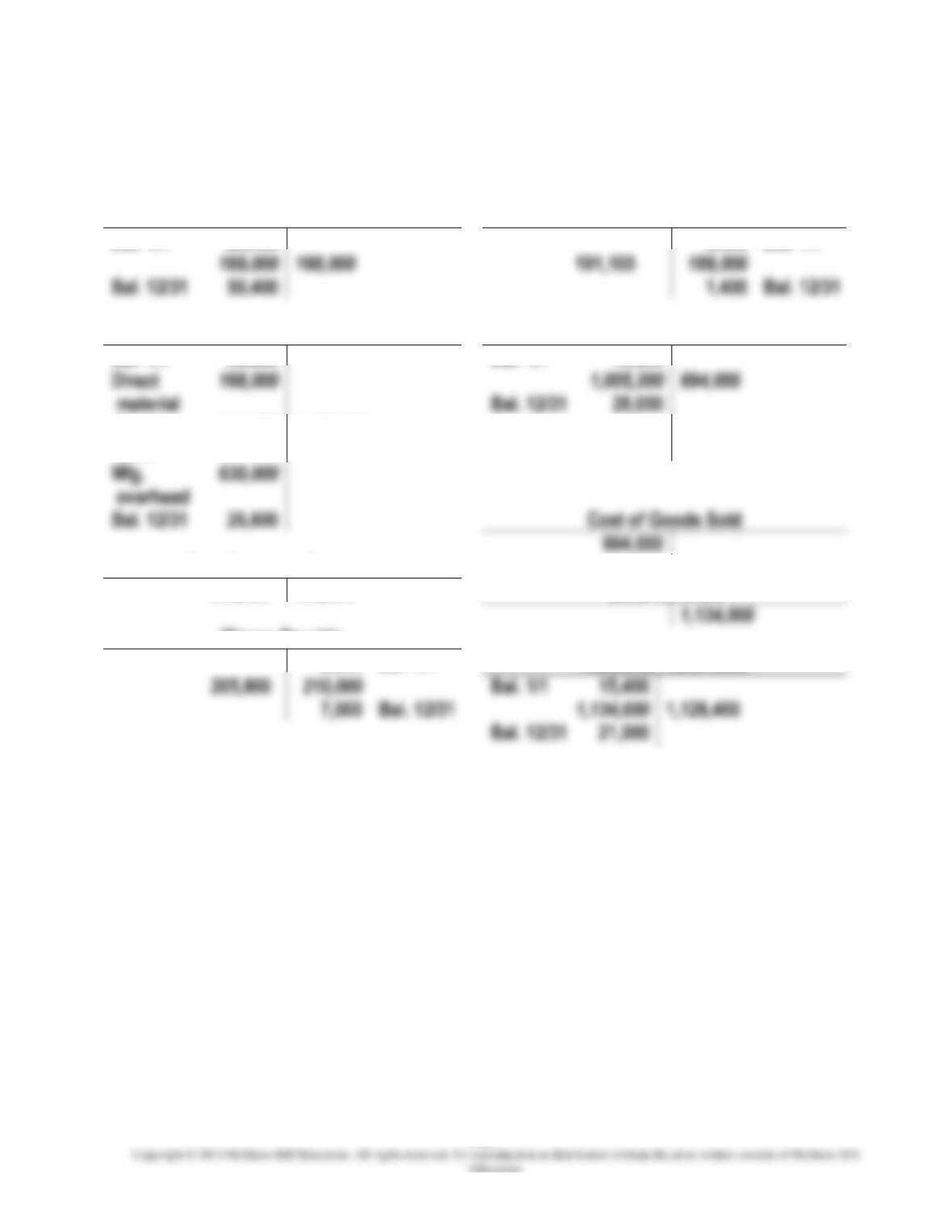

The completed T-accounts are shown below. (Missing amounts in problem are italicized.)

Raw-Material Inventory

Accounts Payable

Bal. 1/1

29,400

3,500

Bal. 1/1

168,000

191,100

Bal. 12/31

50,400

Bal. 12/31

Work-in-Process Inventory

Finished-Goods Inventory

Bal. 1/1

23,800

Bal. 1/1

16,800

Direct

labor

210,000

1,005,200

Bal. 12/31

26,600

Manufacturing Overhead

633,500

630,000

Sales Revenue

1,134,000

Wages Payable

2,800

Bal. 1/1

Accounts Receivable

205,800

Bal. 1/1

15,400

7,000

Bal. 12/31

1,134,000

1,128,400

3-26

PROBLEM 3-46 (35 MINUTES)

2. (a) Work-in-Process Inventory ………………………………………….. 160,000*

Raw-Material Inventory ……………………………………… 160,000

(b) Manufacturing Overhead ……………………………………………… 477,000

(d) Finished-Goods Inventory …………………………………………… 630,500*

(e) Accounts Receivable …………………………………………………… 293,900*

3. Job no. 103 and no. 104 are in production as of March 31:

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-27

PROBLEM 3-46 (CONTINUED)

PROBLEM 3-47 (30 MINUTES)

NOTE: Actual selling and administrative expense, although given in the exercise, is irrelevant

to the solution.

1. Machining Dept. overhead rate = budgeted overhead ÷ budgeted machine hours

2. The ending work-in-process inventory is carried at a cost of $76,765, computed as

follows:

Machining Department:

$12,250

1,800

$ 28,000

Assembly Department:

$ 3,350

48,765

$ 76,765

3. Actual overhead in the Machining Department amounted to $2,130,000, whereas

4. Actual overhead in the Assembly Department amounted to $1,525,000, whereas

5. The company’s manufacturing overhead was overapplied by $59,500 ($64,500 –

3-28

PROBLEM 3-47 (CONTINUED)

7. The firm’s selection of cost drivers (or application bases) seems appropriate. There

PROBLEM 3-48 (30 MINUTES)

1. Traceable costs total $3,750,000, computed as follows:

Total Cost

Percent

Traceable

Traceable

Cost

Professional staff salaries………

$3,750,000

80%

$3,000,000

Administrative support staff……

450,000

60

270,000

75,000

90

67,500

375,000

90

337,500

Other operating costs……………

150,000

50

75,000

$4,800,000

$3,750,000

2. Predetermined overhead rate = budgeted overhead ÷ traceable costs

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

PROBLEM 3-48 (CONTINUED)

4. The total cost of the Davis Manufacturing project is $96,000, and the billing is

$115,200, as follows:

Professional staff salaries… ………

$61,500

3,900

750

6,750

Other operating costs……………….

2,100

$75,000

$96,000

6. Professional staff members are compensated for attending training sessions and firm-

3-30

PROBLEM 3-49 (45 MINUTES)

1.

SUPERIOR METALS

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE YEAR ENDED DECEMBER 31, 20X4

Direct material:

Raw material inventory, 12/31/x3 ……………………

$ 66,750

Add: Purchases of raw material ………………………

Raw material available for use ………………………..

Deduct: Raw-material inventory, 12/31/x4 ………..

Raw material used ………………………………………….

Direct labor ………………………………………………………….

Manufacturing overhead:

Indirect material ……………………………………………..

$ 33,750

Indirect labor …………………………………………………

112,500

Depreciation on factory building……………………..

Depreciation on factory equipment …………………

Utilities ………………………………………………………….

Property taxes ……………………………………………….

Insurance ………………………………………………………

Total actual manufacturing overhead …………

Deduct: Underapplied overhead* ……………….

Overhead applied to work in process ………………

433,125

Total manufacturing costs ……………………………………

Add: Work-in-process inventory, 12/31/x3 ……………..

Subtotal ……………………………………………………………….

Deduct: Work-in-process inventory, 12/31/x4 …………

Cost of goods manufactured …………………………………

*The Schedule of Cost of Goods Manufactured lists the manufacturing costs applied to work

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-31

PROBLEM 3-49 (CONTINUED)

2.

SUPERIOR METALS

SCHEDULE OF COST OF GOODS SOLD

FOR THE YEAR ENDED DECEMBER 31, 20X4

Finished-goods inventory, 12/31/x3 ……………………………………………….

$ 26,250

Add: cost of goods manufactured …………………………………………………

1,329,375

Cost of goods available for sale …………………………..……………………….

Deduct: Finished-goods inventory, 12/31/x4 ………………………………….

Cost of goods sold ……………………………………………………………………….

Add: Underapplied overhead* ……………………………………………………….

Cost of goods sold (adjusted for underapplied overhead) ………………

3.

SUPERIOR METALS

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20X4

Sales revenue ………………………………………………………………………………

$1,578,750

Less: Cost of goods sold ………………………………………………………………

1,327,500

Gross margin ……………………………………………………………………………….

Selling and administrative expenses ……………………………………………..

Income before taxes ……………………………………………………………………..

Income tax expense ……………………………………………………………………..

Net income …………………………………………………………………………………..

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-32

PROBLEM 3-50 (15 MINUTES)

1. $30,000. Since there was no work-in-process inventory at the beginning of 20×4, all of the

4. Only the $22,500 of equipment depreciation would have been included in

3-33

PROBLEM 3-51 (25 MINUTES)

1.

hours machine budgeted

overhead ingmanufactur budgeted

rate overhead nedPredetermi

=

2.

Journal entries:

(a)

Raw-Material Inventory ………………………………..

8,240

Accounts Payable ………………………………

8,240

(b)

Raw-Material Inventory ……………………….

(c)

Manufacturing Overhead ……………………………..

Manufacturing-Supplies Inventory ……….

(d)

Manufacturing Overhead ……………………………..

Cash ………………………………………………….

(e)

Wages Payable …………………………………..

Selling and Administrative Expense ……………..

2,100

Prepaid Insurance ………………………………

(g)

Raw-Material Inventory ………………………………..

2,800

Accounts Payable ………………………………

2,800

(h)

Accounts Payable ………………………………………..

1,850

Cash ………………………………………………….

1,850

3-34

PROBLEM 3-51 (CONTINUED)

(i)

Manufacturing Overhead ……………………………..

19,000

Wages Payable …………………………………..

19,000

(j)

Manufacturing Overhead ……………………………..

Accumulated Depreciation: Equipment ..

(k)

Finished-Goods Inventory …………………………...

(l)

Manufacturing Overhead…………………….

Accounts Receivable …………………………………..

Sales Revenue …………………………………..

Cost of Goods Sold ……………………………………..

Finished-Goods Inventory ………………….

PROBLEM 3-52 (40 MINUTES)

1. In accordance with the Standards of Ethical Conduct for Management Accountants,

the appropriateness of Joey Dulwich’s three alternative courses of action is described

as follows:

• Follow Brown’s directive and do nothing further. This action is inappropriate as

3-35

PROBLEM 3-52 (CONTINUED)

2. The next step that Dulwich should take in resolving this conflict is to inform Brown

that he is planning to discuss the conflict with the next higher managerial level.

Dulwich should pursue discussions with successively higher levels of management,

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-36

PROBLEM 3-53 (30 MINUTES)

1.

MARVELOUS MARSHMALLOW COMPANY

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE MONTH OF JANUARY

Direct material:

Raw-material inventory, January 1 ……………………..

$ 34,000

Add: January purchases of raw material …………….

Raw material available for use …………………………...

Deduct: Raw-material inventory, January 31 ……….

Raw materials used …………………………………………..

Direct labor ……………………………………………………………

Manufacturing overhead applied (50% of direct labor)

Total manufacturing costs ……………………………………..

Add: Work-in-process inventory, January 1 …………….

Subtotal …………………………………………………………………

Deduct: Work-in-process inventory,

Cost of goods manufactured …………………………………..

*Work upward from the bottom of the statement, using the information available. Direct labor

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-37

PROBLEM 3-53 (CONTINUED)

2.

MARVELOUS MARSHMALLOW COMPANY

SCHEDULE OF PRIME COSTS

FOR THE MONTH OF JANUARY

Raw material:

Beginning inventory ………………………………………………………….

$ 34,000

Add: Purchases ………………………………………………………………..

Raw material available for use ……………………………………………

Deduct: Ending inventory ………………………………………………….

Raw material used …………………………………………………………………….

Direct labor ………………………………………………………………………………

Total prime costs ………………………………………………………………………

3.

MARVELOUS MARSHMALLOW COMPANY

SCHEDULE OF CONVERSION COSTS

FOR THE MONTH OF JANUARY

Direct labor ………………………………………………………………………………..

Manufacturing overhead applied (50% of direct labor) ………………….

Total conversion cost …………………………………………………………………

PROBLEM 3-54 (30 MINUTES)

1.

hours machine budgeted

overhead ingmanufactur budgeted

rate overhead nedPredetermi

=

2.

Calculation of applied manufacturing overhead:

3.

actual overhead – applied overhead

$38,000 – $36,000

4.

Cost of Goods Sold …………………………………………………..

3-38

PROBLEM 3-54 (CONTINUED)

5.

(a)

Calculation of proration amounts:

Account

Explanation

Amount*

Percentage

Calculation

of Percentage

Work in Process

Job B19 only

$10,800

30%

10,800

36,000

Finished Goods

50%

18,000

36,000

Cost of Goods

Sold

Job M07 only

36,000

*Machine hours used on job predetermined overhead rate.

Account

Underapplied

Overhead

Percentage

Amount Added

to Account

Work in Process

$2,000

30%

$ 600

(b)

Journal entry:

Work-in-Process Inventory …………………………………………..

600

Finished-Goods Inventory ……………………………………………

Cost of Goods Sold ……………………………………………………..

400

Manufacturing Overhead …………………………………….

3-39

PROBLEM 3-55 (45 MINUTES)

1.

Predetermined overhead rate:

*$575,000 = $345,000 + $230,000

2.

Cost of Job 57:

Cost in beginning work-in-process inventory ………………………………

$108,000

Direct material……………………………………………………………………………

Applied manufacturing overhead

Total cost ………………………………………………………………………………….

3.

Manufacturing overhead applied to Job 59:

=

=

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-40

PROBLEM 3-55 (CONTINUED)

4.

Total manufacturing overhead applied during November:

5.

Actual manufacturing overhead incurred during November:

Indirect material (supplies) ………………………………………………………………

$24,000

Indirect-labor wages ……………………………………………………………………….

Supervisory salaries ……………………………………………………………………….

Building occupancy costs, factory facilities ……………………………………..

Production equipment costs ……………………………………………………………

Total ………………………………………………………………………………………………

$95,000

6.

Underapplied overhead for November:

Actual manufacturing overhead – applied manufacturing overhead

=

=