EXERCISE 3-8

1. Jan. 31 Accounts Receivable …………………………….. 875

Service Revenue …………………………….. 875

EXERCISE 3-9

1. Oct. 31 Supplies Expense ………………………………….. 2,000

Supplies ($2,500 – $500) ………………….. 2,000

2. 31 Insurance Expense ………………………………… 120

Prepaid Insurance …………………………... 120

EXERCISE 3-9 (Continued)

6. Oct. 31 Interest Expense ………………………………. 95

Interest Payable…………………………. 95

EXERCISE 3-10

MONTEE CO.

Income Statement

For the Month Ended July 31, 2017

Revenues

Service revenue ($5,500 + $650) ……………………….. $6,150

EXERCISE 3-11

Answer Computation

(a) Supplies balance = $800 Supplies expense $ 950

Add: Supplies (1/31) 850

Less: Supplies purchased (1,000)

Supplies (1/1) $ 800

EXERCISE 3-11 (Continued)

(c) Salaries and wages

payable = $1,820 Cash paid $3,800

Salaries and wages

payable (1/31/17) 920

EXERCISE 3-12

(a) July 10 Supplies ……………………………………………….. 650

Cash …………………………..………………….. 650

14 Cash …………………………………………………….. 2,000

Service Revenue …………………………….. 2,000

(b) July 31 Supplies Expense ………………………………….. 800

Supplies …………………………..…………….. 800

31 Accounts Receivable …………………………….. 500

Service Revenue …………………………….. 500

EXERCISE 3-13

Aug. 31 Accounts Receivable ………………………………. 2,600

Service Revenue ……………………………… 2,600

31 Supplies Expense …………………………………… 1,400

Supplies ………………………………………….. 1,400

31 Insurance Expense …………………………………. 1,500

Prepaid Insurance ……………………………. 1,500

EXERCISE 3-14

TURNQUIST COMPANY

Income Statement

For the Year Ended August 31, 2017

Revenues

Service revenue ………………………………………………. $36,600

Rent revenue …………………………………………………… 12,100

Total revenues ………………………………………….. $48,700

Expenses

EXERCISE 3-14 (Continued)

TURNQUIST COMPANY

Owner’s Equity Statement

For the Year Ended August 31, 2017

Owner’s capital, September 1, 2016 ……………………………………….. $15,600

TURNQUIST COMPANY

Balance Sheet

August 31, 2017

Assets

Cash ……………………………………………………………………… $10,400

Accounts receivable ………………………………………………. 11,400

Liabilities and Owner’s Equity

Liabilities

Accounts payable ………………………………………………………….. $ 5,800

Salaries and wages payable …………………………………………… 1,100

EXERCISE 3-15

(a) 1. Cash …………………………………………………………. 8,000

Accounts Receivable ………………………….. 8,000

2. Unearned Service Revenue ………………………… 25,000

Service Revenue …………………………………. 25,000

4. Accounts Receivable …………………………………. 115,000

Service Revenue

($161,000 – $25,000 – $21,000) ………….. 115,000

5. Cash …………………………………………………………. 99,000

*EXERCISE 3-16

1. Prepaid Insurance ………………………………………….. 1,125

Insurance Expense

($2,700 X 5/12) …………………………..………….. 1,125

*EXERCISE 3-17

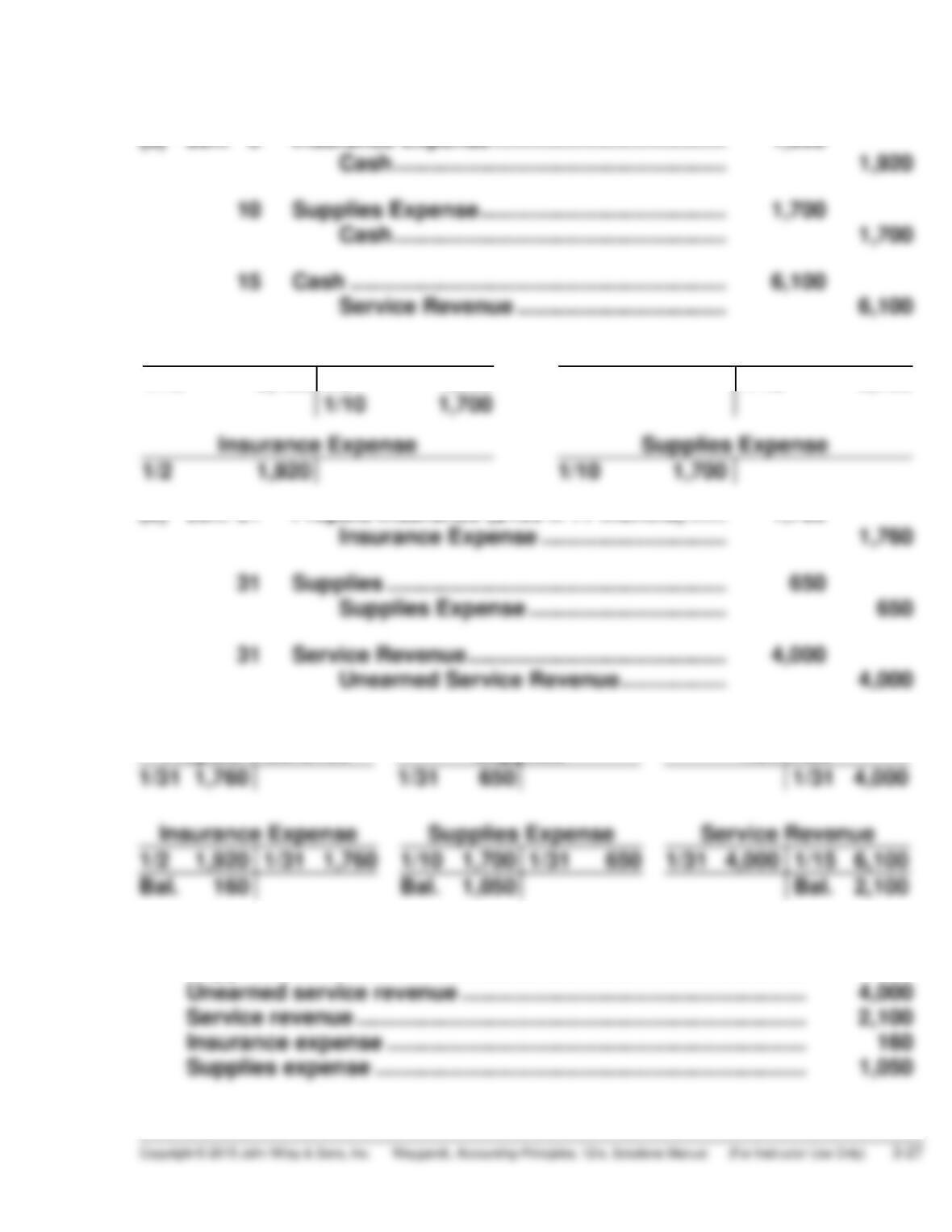

(a) Jan. 2 Insurance Expense ……………………………….. 1,920

Cash …………………………..…………………. 1,920

Cash

Service Revenue

1/15 6,100

1/2 1,920

1/10 1,700

1/15 6,100

Insurance Expense

Supplies Expense

1/2 1,920

1/10 1,700

(b) Jan. 31 Prepaid Insurance ($160 X 11 months) …… 1,760

Prepaid Insurance

Supplies

Unearned Service

Revenue

1/31 1,760

1/31 650

1/31 4,000

1/2 1,920

1/31 1,760

1/10 1,700

1/31 650

1/31 4,000

1/15 6,100

Bal. 160

Bal. 1,050

Bal. 2,100

(c) Prepaid insurance ……………………………………………………………. $1,760

Supplies …………………………………………………………………………. 650

*EXERCISE 3-18

(a) 2 Going concern assumption

(b) 6 Economic entity assumption

*EXERCISE 3-19

(a) This is a violation of the historical cost principle. The inventory was

written up to its fair value when it should have remained at cost.

(b) This is a violation of the economic entity assumption. The treatment of

the transaction treats Austin Weber and Weber Co. as one entity when

they are two separate entities. Salaries and Wages Expense should

have been debited for the purchase of the truck.

*EXERCISE 3-20

1. Comparability

2. Going concern assumption

3. Materiality

*EXERCISE 3-21

(a) The primary objective of financial reporting is to provide financial

information that is useful to investors and creditors for making

decisions about providing capital. Since Speyeware’s shares appear to

be actively traded, investors must be capable of using the information

made available by Speyeware to make decisions about the company.

*EXERCISE 3-22

(a) Accounting information is the compilation and presentation of

financial information for a company. It provides information in the form

of financial statements and additional disclosures that is useful for

decision making.

(b) Gina is correct in her understanding that the low success rate for new

biotech products will be a cause of concern for investors. Her

suggestion that detailed scientific findings be reported to prospective

investors might offset some of their concerns but it probably won’t

conform to the qualitative characteristics of accounting information.

SOLUTIONS TO PROBLEMS

PROBLEM 3-1A

(a)

J4

Date

Account Titles

Ref.

Debit

Credit

2017

May 31

Supplies Expense …………………………..

Supplies ………………………………..

631

126

900

900

31

Insurance Expense …………………………

722

150

31

Unearned Service Revenue …………….

Service Revenue

($2,000 – $400) ……………………

209

400

1,600

1,600

31

Depreciation Expense …………………….

Accumulated Depreciation—

Equipment ………………………….

717

150

190

190

31

Accounts Receivable ……………………..

Service Revenue …………………….

112

400

1,700

1,700

(b)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

Balance

4,500

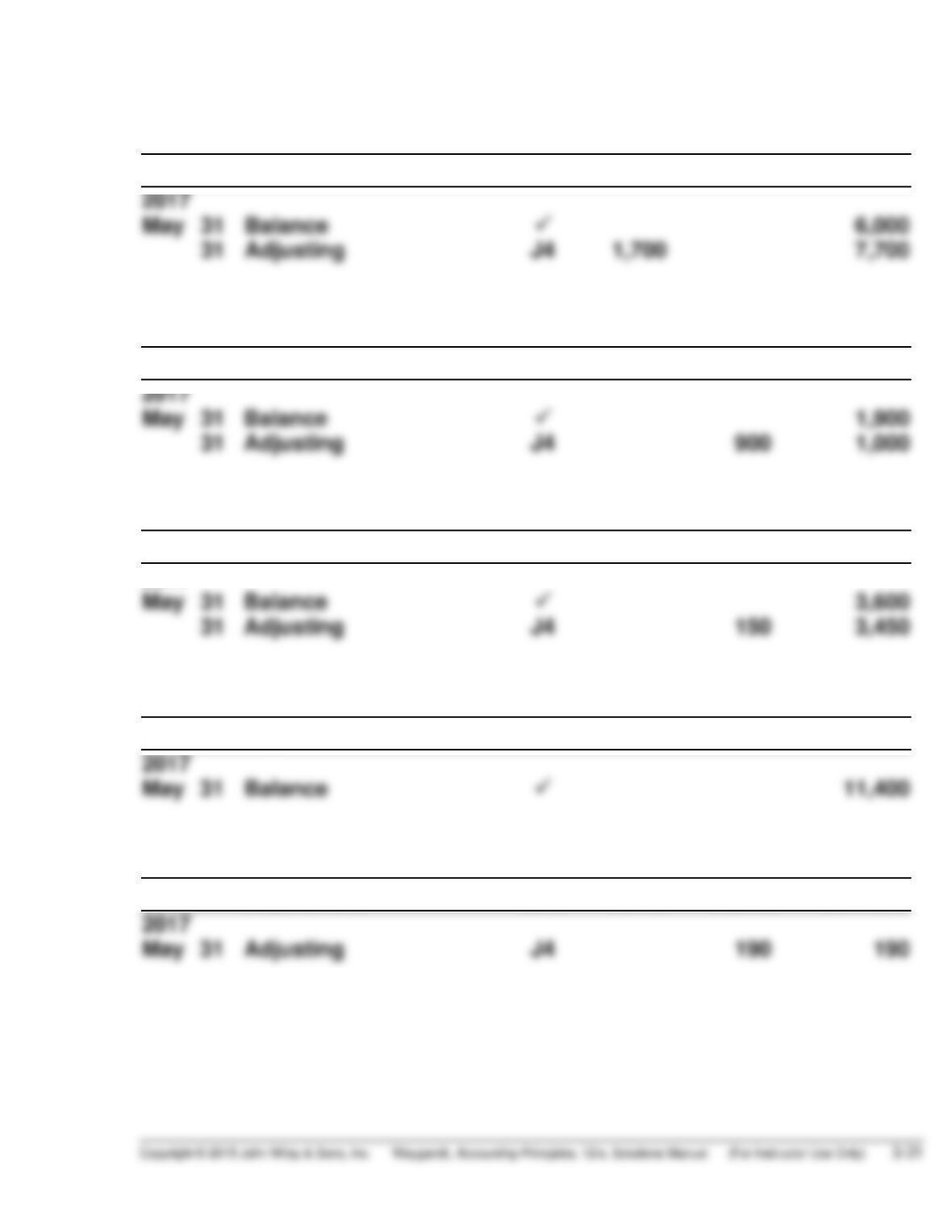

PROBLEM 3-1A (Continued)

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

Balance

6,000

Supplies No. 126

Date

Explanation

Ref.

Debit

Credit

Balance

2017

Prepaid Insurance No. 130

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

31

Balance

Adjusting

J4

150

3,600

3,450

Equipment No. 149

Date

Explanation

Ref.

Debit

Credit

Balance

Accumulated Depreciation—Equipment No. 150

Date

Explanation

Ref.

Debit

Credit

Balance

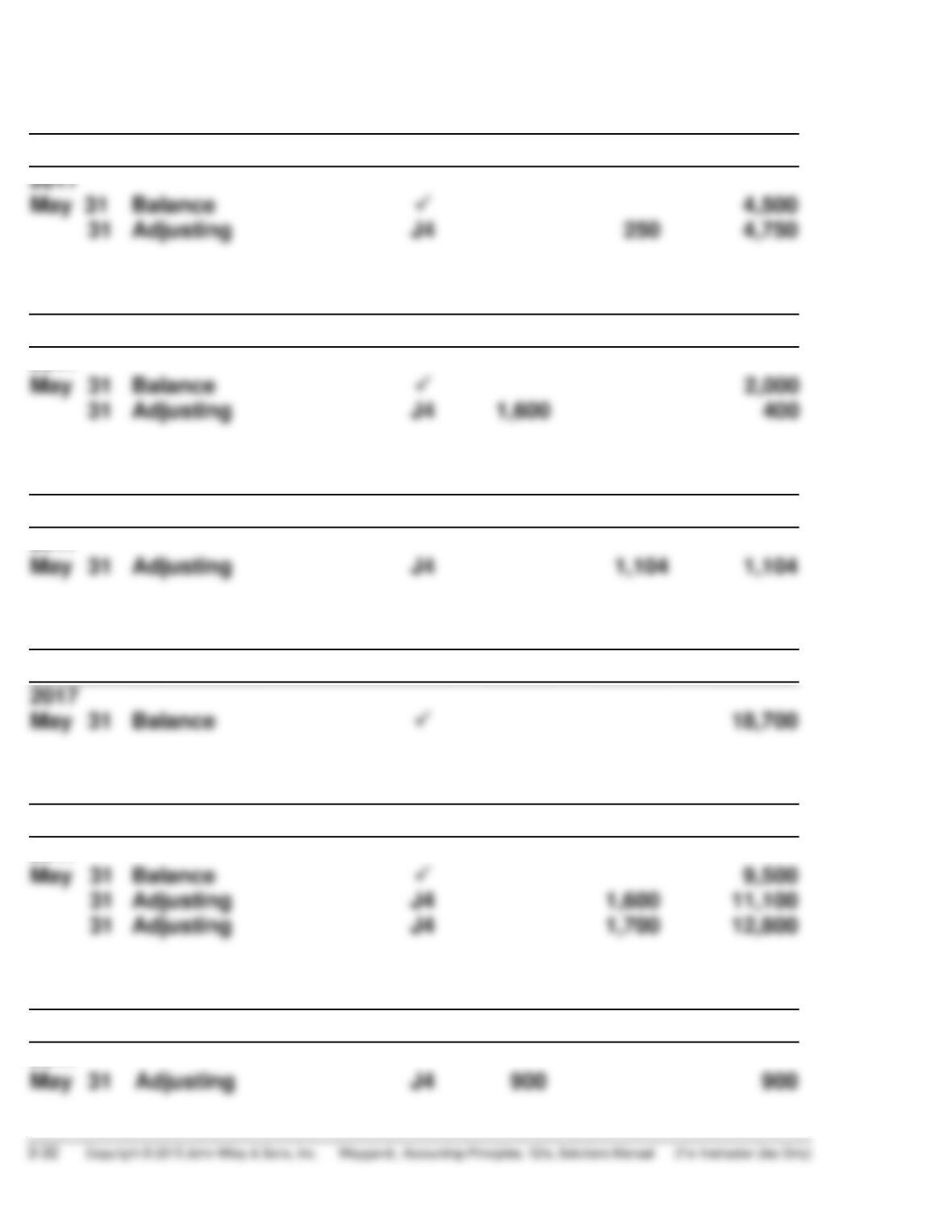

PROBLEM 3-1A (Continued)

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

31

Balance

Adjusting

J4

250

4,500

4,750

Unearned Service Revenue No. 209

Date

Explanation

Ref.

Debit

Credit

Balance

2017

Salaries and Wages Payable No. 212

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

Adjusting

J4

1,104

1,104

Owner’s Capital No. 301

Date

Explanation

Ref.

Debit

Credit

Balance

Service Revenue No. 400

Date

Explanation

Ref.

Debit

Credit

Balance

J4

2017

May 31

Balance

9,500

Supplies Expense No. 631

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

Adjusting

J4

900

900

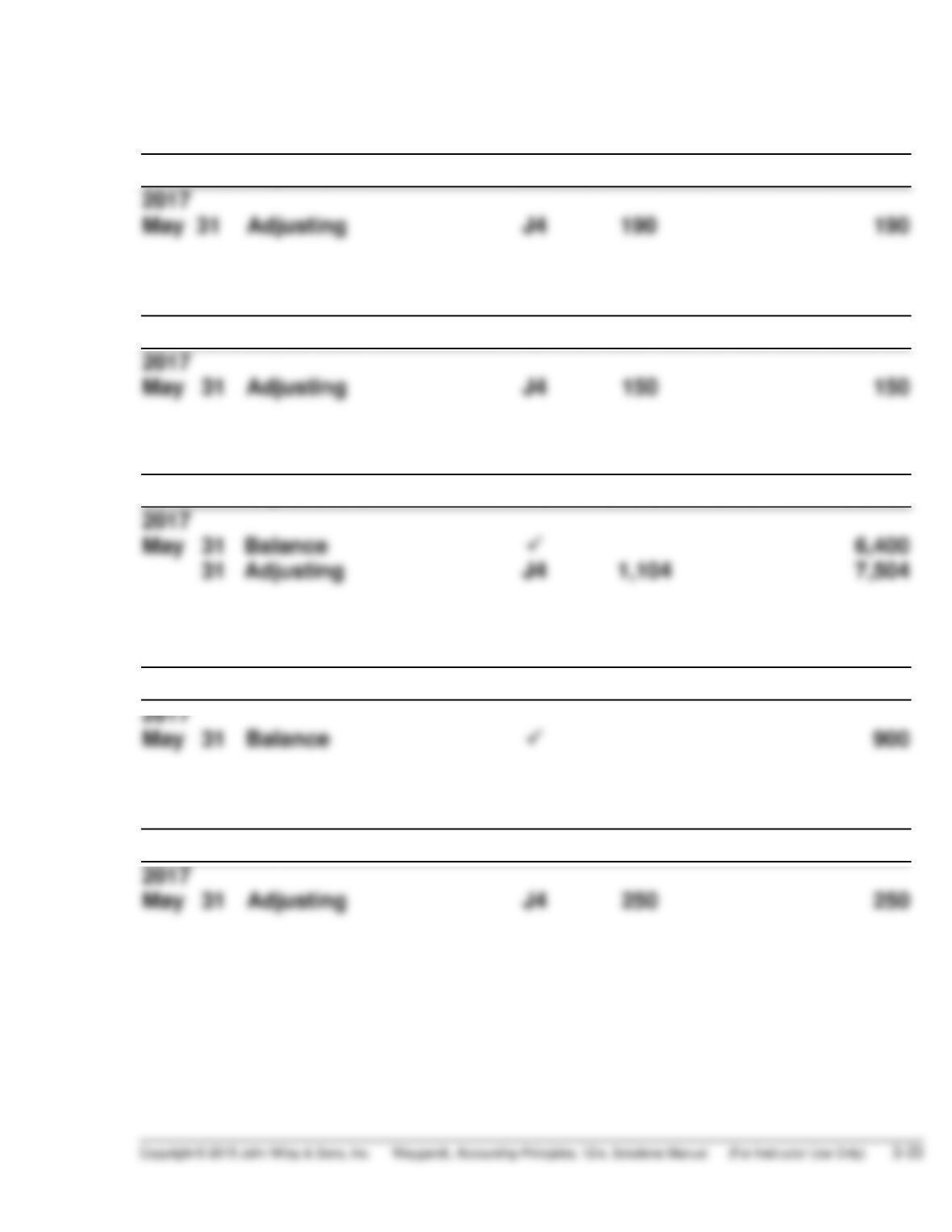

PROBLEM 3-1A (Continued)

Depreciation Expense No. 717

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

Insurance Expense No. 722

Date

Explanation

Ref.

Debit

Credit

Balance

Salaries and Wages Expense 726

Date

Explanation

Ref.

Debit

Credit

Balance

Rent Expense No. 729

Date

Explanation

Ref.

Debit

Credit

Balance

2017

May 31

Balance

900

Utilities Expense No. 732

Date

Explanation

Ref.

Debit

Credit

Balance

2017

PROBLEM 3-1A (Continued)

(c) KRAUSE CONSULTING

Adjusted Trial Balance

May 31, 2017

Debit

Credit

Cash ……………………………………………………….….

Accounts Receivable …………………………………..

Salaries and Wages Payable…………………………

Owner’s Capital …………………………………………..

Service Revenue ………………………………………….

Salaries and Wages Expense ……………………….

Rent Expense ………………………………………………

Depreciation Expense ………………………………….

$ 4,500

7,700

7,504

900

190

1,104

18,700

12,800

PROBLEM 3-2A

(a)

J1

Date

Account Titles

Ref.

Debit

Credit

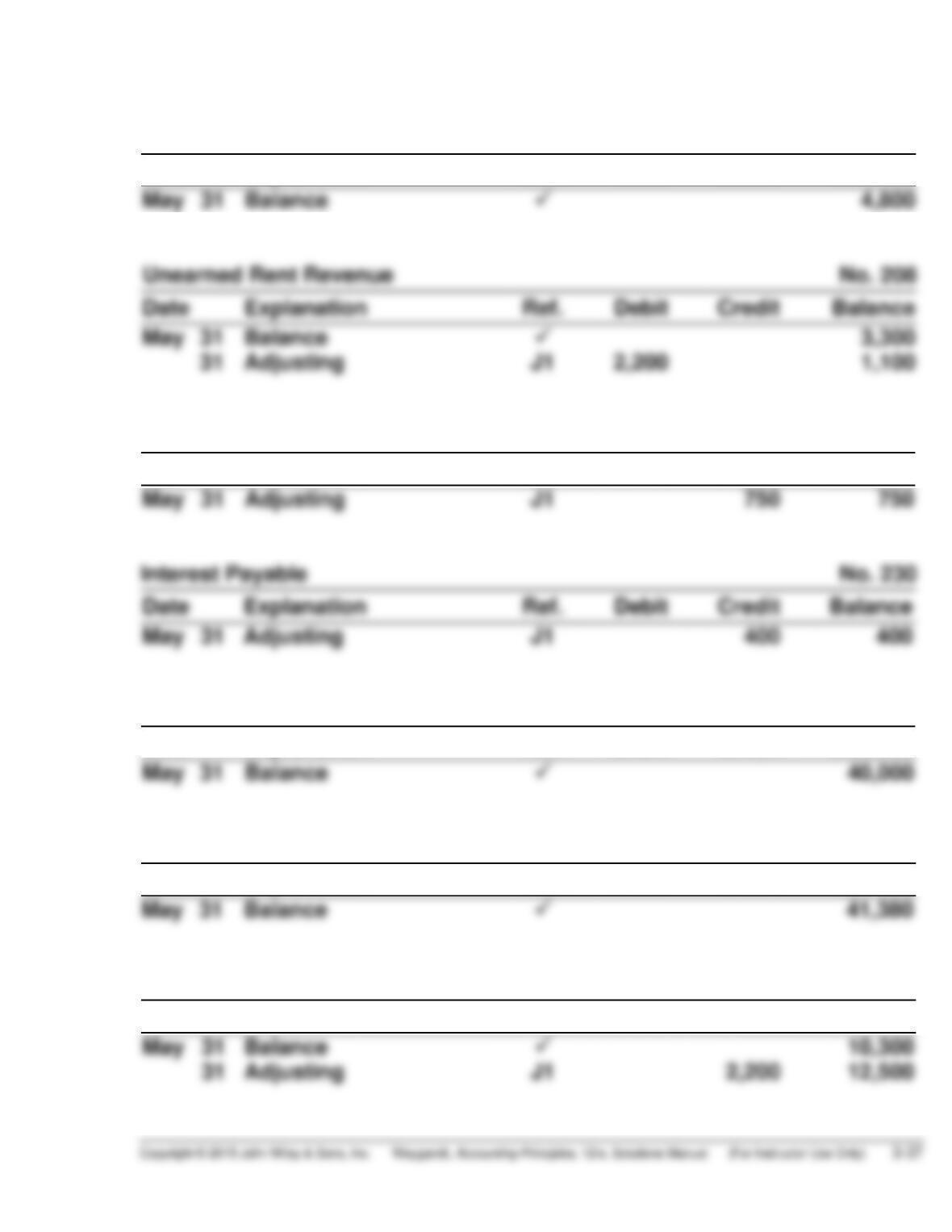

May 31

Insurance Expense…………………………

Prepaid Insurance

($2,400 X 1/12)…………………….

722

130

200

200

31

Interest Expense …………………………...

Interest Payable

[($40,000 X 12%) X 1/12] ………..

718

230

400

400

31

(2/3 X $3,300) …………………….

429

Unearned Rent Revenue …………………

208

2,200

(b)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

3,500

PROBLEM 3-2A (Continued)

Supplies No. 126

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

31

Balance

Adjusting

J1

1,330

2,080

750

Date

Explanation

Ref.

Debit

Credit

Balance

Land No. 140

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

12,000

Buildings No. 141

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

60,000

Date

Ref.

Debit

Credit

Balance

May 31

Equipment No. 149

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

15,000

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Adjusting

125

PROBLEM 3-2A (Continued)

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

4,800

Salaries and Wages Payable No. 212

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Adjusting

J1

750

750

May 31

Mortgage Payable No. 275

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

40,000

Owner’s Capital No. 301

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

41,380

12,500

PROBLEM 3-2A (Continued)

Advertising Expense No. 610

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Balance

600

Date

Ref.

Debit

Credit

Balance

Supplies Expense No. 631

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Adjusting

J1

1,330

1,330

Interest Expense No. 718

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

Adjusting

J1

400

400

Date

Explanation

Ref.

Debit

Credit

Balance

Salaries and Wages Expense No. 726

Date

Explanation

Ref.

Debit

Credit

Balance

May 31

31

Balance

Adjusting

J1

750

3,300

4,050

Date

Ref.

Credit

PROBLEM 3-2A (Continued)

(c) MAC’S MOTEL

Adjusted Trial Balance

May 31, 2017

Debit

Credit

Cash …………………………………………………………..

Supplies ……………………………………………………..

Accumulated Depreciation—Equipment ……….

Accounts Payable ……………………………………….

Unearned Rent Revenue ………………………………

Salaries and Wages Payable ………………………..

Interest Payable …………………………………………..

Mortgage Payable ………………………………………..

Owner’s Capital …………………………………………..

Rent Revenue ……………………………………………..

Advertising Expense ……………………………………

Depreciation Expense ………………………………….

Supplies Expense ………………………………………..

$ 3,500

750

600

375

1,330

125

4,800

1,100

750

400

40,000

41,380

12,500

PROBLEM 3-2A (Continued)

(d) MAC’S MOTEL

Income Statement

For the Month Ended May 31, 2017

Revenues

Rent revenue ………………………………………….. $12,500

Expenses

Salaries and wages expense ……………………. $4,050

Supplies expense ……………………………………. 1,330

MAC’S MOTEL

Owner’s Equity Statement

For the Month Ended May 31, 2017

Owner’s capital, May 1 …………………………………………………… $ 0

Investment by owner ……………………………………………………… 41,380