3–1

Chapter 3

Fundamentals of Cost-Volume-Profit Analysis

Learning Objectives

1. Use cost-volume-profit (CVP) analysis to analyze decisions.

2. Understand the effect of cost structure on decisions.

3. Use Microsoft Excel to perform CVP analysis.

4. Incorporate taxes, multiple products, and alternative cost structures into the CVP analysis.

5. Understand the assumptions and limitations of CVP analysis.

3–2

Chapter Overview

I. COST-VOLUME-PROFIT ANALYSIS

• Profit Equation

• CVP Example

o Finding Break-Even and Target Volumes

▪ Break-Even Volume in Units

▪ Break-Even Volume in Sales Dollars

▪ Target Volume in Units

▪ Target Volume in Sales Dollars

• Graphic Presentation

• Profit-Volume Model

• Use of CVP to Analyze the effect of Different Cost Structures

• Margin of Safety

II. CVP ANALYSIS WITH SPREADSHEETS

III. EXTENSIONS OF THE CVP MODEL

• Income Taxes

• Multiproduct CVP Analysis

IV. ASSUMPTIONS AND LIMITATIONS OF CVP ANALYSIS

3–3

Chapter Outline

LO 3-1 Use cost-volume-profit (CVP) analysis to analyze decisions.

COST-VOLUME-PROFIT ANALYSIS

• Cost-Volume-Profit (CVP) Analysis

o Cost-volume-profit (CVP) analysis is a study of the relations among revenues, costs, and

volume and their effect on profit.

o Managers make decisions on volume, pricing, or incurring a cost that will impact profit.

(See Business Application box “Cost-Volume-Profit Analysis and On-Demand Services.”)

• Profit equation

o Profit equation equals total revenues less total costs.

▪ Operating profit (also referred to as profit) = Total revenues – Total costs

Profit = TR – TC

o Contribution margin is the amount that units sold contribute toward (1) covering fixed

costs and (2) providing operating profits

▪ Unit contribution margin

• The difference between sales price and variable cost per unit

• Unit contribution margin = Price – Variable cost per unit = P – V

▪ Total contribution margin

• The difference between total revenues and total variable cost

• Total contribution margin

= (Price – Variable cost per unit) x Units of output = (P – V)X

3–4

▪ Alternatively, in CVP income statement format,

Total

Unit

Percentage

Sales revenue

PX

P

100%

– Variable costs

VX

V

V ÷ P

= Contribution margin

(P – V)X

P – V

(P – V) ÷ P

– Fixed costs

F

= Profit

(P – V)X – F

Contribution margin ratio

o Financial accounting classifies costs as either manufacturing or administrative; for

decision making, for decision making, costs are classified as fixed or variable.

▪ V represents the sum of variable manufacturing cost per unit and variable marketing

and administrative cost per unit

• CVP Example

o Exhibit 3.1 illustrates a contribution margin income statement; profit equals contribution

less fixed costs.

o Finding Break-Even and Target Volumes

▪ Break-even point is the volume level at which profits equal zero; if the company

3–5

▪ Target volume is the level at which profits equal a target profit.

▪ Exhibit 3.2 summarizes the break-even and target volume formulas.

See Demonstration Problem 1

• Graphic Presentation

o Exhibit 3.3 plots total revenues against total costs at various activity levels (volumes).

▪ The total revenue line (TR) starts at the origin (0, 0) with slope P, the price per unit.

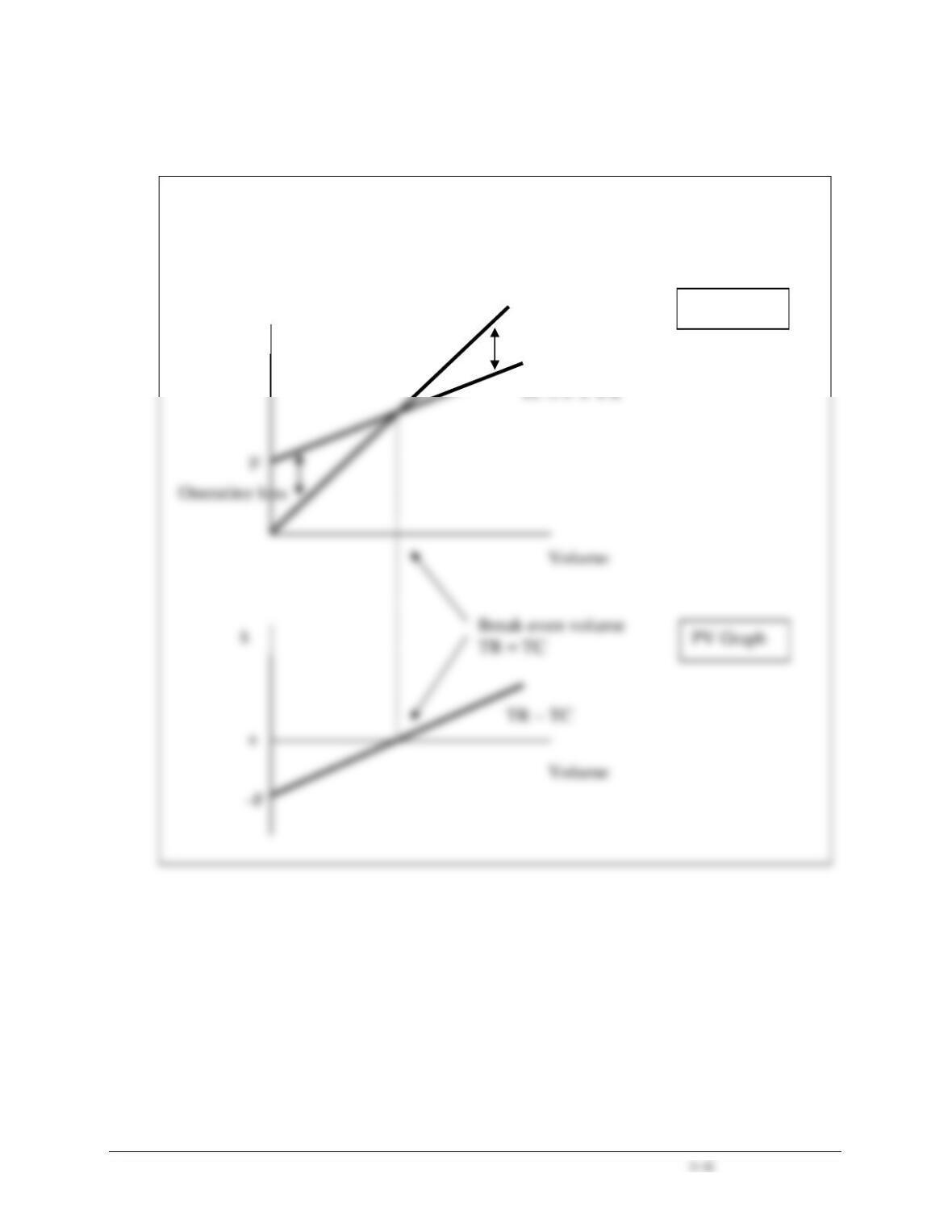

• Profit-Volume Model

o Profit-volume analysis is a version of cost-volume-profit analysis using a single profit

line.

o A Profit-Volume graph collapses the cost and revenue lines into a single profit line in the

profit-volume graph.

o Exhibit 3.4 (shown in a more generic form below) is a comparison of a CVP graph and a

Profit-Volume graph using the same background information.

Volume

Volume

–F

TC = F + VX

Operating loss

TR – TC

Comparison of CVP Graph and PV Graph

$

TR = PX

Operating profit

CVP Graph

3–7

LO 3-2 Understand the effect of cost structure on decisions.

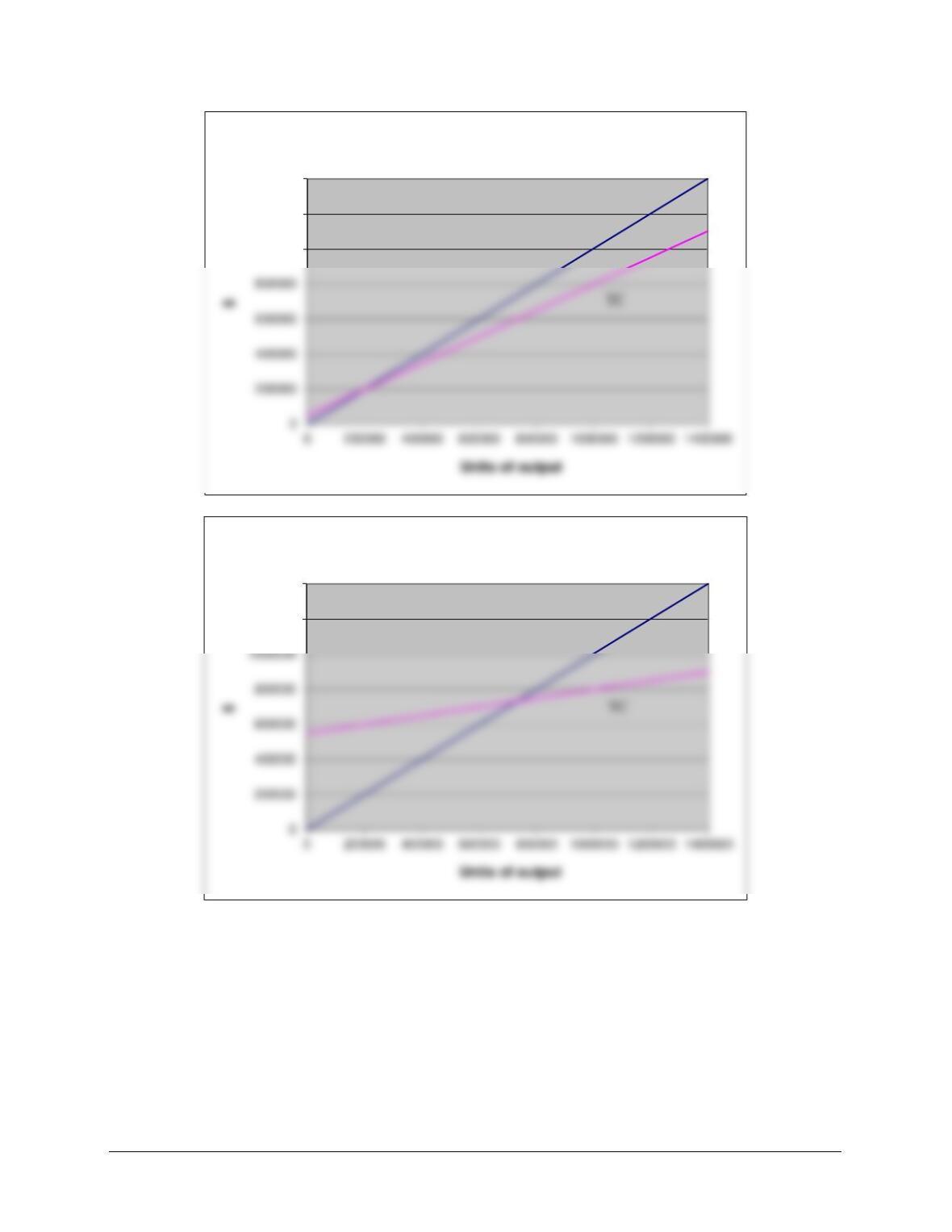

• Use of CVP to Analyze the effect of Different Cost Structures

o An organization’s cost structure is the proportion of fixed and variable costs to total

costs; it has a significant effect on the sensitivity of its profits to changes in volume.

o Operating leverage describes the extent to which an organization’s cost structure is

made up of fixed costs.

▪ Operating leverage is high in firms with a high proportion of fixed costs and a low

proportion of variable costs and results in a high contribution margin per unit.

• The higher the firm’s fixed costs, the higher its break-even point.

▪ Profit increase (decrease) as a result of improved (declining) sales can be calculated

as the product of operating leverage and sales increase (decrease) in percentage. (See

Business Application box “Effect of Cost Structure on Operating and Investing

Decisions.”)

▪ Exhibit 3.5 compares the cost structure of two companies.

3–8

1000000

1200000

1400000

LO-LEV

1200000

1400000

HI-LEV

TR

TR

TC

3–9

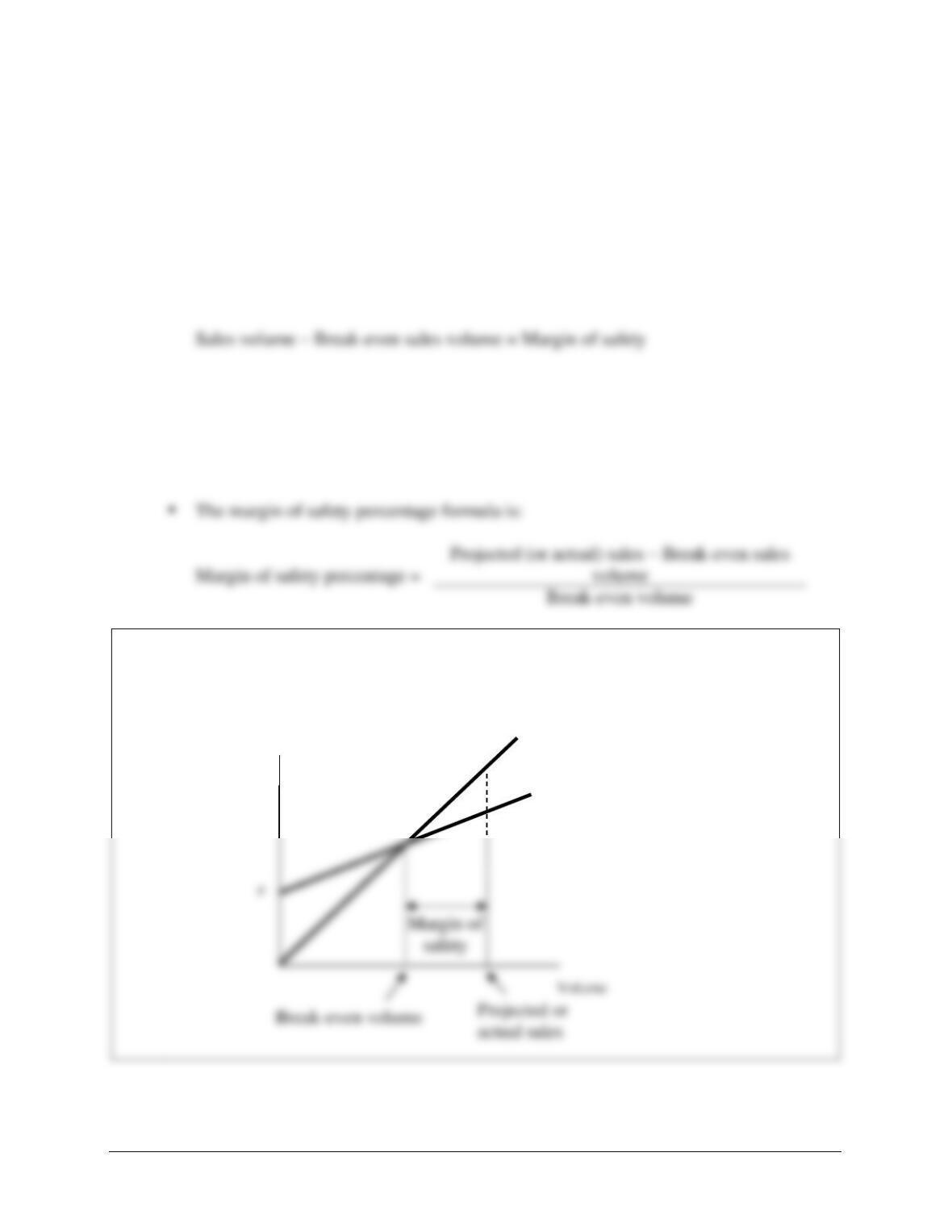

• Margin of Safety

o Margin of safety is the excess of projected (or actual) sales over the break-even sales

level.

▪ The margin of safety indicates the risk of losing money that a company faces; that is,

the amount by which sales can fall before the company is in the loss area.

▪ The margin of safety formula is:

o The margin of safety percentage is the excess of projected (or actual) sales over the

break-even sales volume expressed as a percentage of the break-even volume.

▪ The margin of safety percentage indicates the percentage decline in sales volume

before the company finds itself operating at a loss.

Margin of safety is presented below.

$

TR = PX

TC = F + VX

3–10

LO 3-3 Use Microsoft Excel to perform CVP analysis.

CVP ANALYSIS WITH SPREADSHEETS

• Spreadsheet programs such as Microsoft Excel® are ideally suited to doing CVP routinely.

o Exhibit 3.6 illustrates a screenshot of a spreadsheet program for CVP Analysis.

LO 3-4 Incorporate taxes, multiple products, and alternative cost structures

into the CVP analysis.

EXTENSIONS OF THE CVP MODEL

• Income Taxes

o Assuming that operating profits before taxes and taxable income are the same, income

taxes may be incorporated into the basic model as follows (where t is the tax rate):

See Demonstration Problem 2

• Multiproduct CVP Analysis

o Without some assumptions, there is an infinite number of combinations of services or

products that would achieve a given level of profit.

o Fixed Product Mix

▪ Using the fixed product mix method, managers define a package or bundle of

products in the typical product mix and then compute the break-even or target volume

for the package.

o Weighted-Average Contribution Margin

▪ Assuming a constant product mix, the second method calculates a weighted-average

contribution margin per unit for all of the products considered.

▪ The break-even formula determines the required total number of units for all products

involved.

See Demonstration Problem 3

• Alternative Cost Structures

o When more complicated cost structures are considered, the basic setup developed so far

must be adapted to deliver relevant information for decision making.

▪ Consider the fixed cost that follows a step-cost pattern over the relevant range as

3–12

LO 3-5 Understand the assumptions and limitations of CVP analysis.

ASSUMPTIONS AND LIMITATIONS OF CVP ANALYSIS

• CVP analysis relies on certain assumptions that may limit the applicability of the results for

decision making.

o The limitations are due to the assumptions made; they are not inherent to the method of

CVP analysis itself.

3–13

Matching

A.

Break-even point

G.

Operating leverage

B.

Contribution margin ratio

H.

Profit equation

C.

Cost structure

I.

Profit-volume analysis

D.

Cost-volume-profit analysis

J.

Total contribution margin

E.

Margin of safety

K.

Unit contribution margin

F.

Margin of safety percentage

_____ 1. Operating profit equals total revenues less total costs.

_____ 2. Volume level at which profits equal zero.

_____ 3. Extent to which an organization’s cost structure is made up of fixed costs.

_____ 4. Version of the cost-volume-profit analysis using a single profit line.

_____ 5. The proportion of fixed and variable costs to total costs of an organization.

_____ 6. Contribution margin expressed as a percentage of sales revenue.

_____ 7. Difference between revenues and total variable costs.

_____ 8. Difference between revenues per unit (price) and variable costs per unit.

_____ 9. Study of the relations among revenues, costs, and volume and their effect on profit.

_____ 10. The excess of projected or actual sales over the break-even volume.

_____ 11. The excess of projected or actual sales over the breakeven volume expressed as a

percentage of the breakeven volume.

3–14

Matching Answers

1. H

Multiple Choice

Use the following information to answer questions 1 through 4:

Company A currently sells a product for $2 each. Fixed cost and unit variable cost are $12,000

and $0.80, respectively.

1. What is the break-even point in units and in sales dollars, respectively?

a. 10,000 units and $20,000

b. 12,000 units and $24,000

c. 10,000 units and $15,000

d. 20,000 units and $20,000

2. What is the contribution margin ratio?

a. 20%

b. 30%

c. 40%

d. 60%

3. To reach a target profit of $33,000, how many units of output should be sold?

a. 22,500 units

b. 31,750 units

c. 37,500 units

d. 42,000 units

4. If variable cost per unit is increased by 15%, fixed cost is increased to $15,120, and the unit

price remains the same, what is the new break-even point in sales dollars?

a. $22,000

b. $24,000

c. $26,000

d. $28,000

5. Relative to companies with low operating leverage, a company with high operating leverage:

a. Is more sensitive to economic fluctuations.

b. Has a high proportion of variable costs.

c. Experiences a smaller break-even volume.

d. Has a low contribution margin per unit.

6. The excess of actual or projected sales over the break-even sales is known as:

a. Contribution margin.

b. Margin of safety.

c. Gross margin.

d. Target profit.

3–16

7. A company produces key chains. The data include price $1, unit variable cost $0.40, monthly

fixed cost $3,000 and tax rate 30%. The owner wants to earn an after-tax profit of $10,500

per month. How many key chains must be produced and sold to meet that goal?

a. 24,000

b. 30,000

c. 32,000

d. 36,000

8. When more than one product is involved:

a. The CVP method reaches its limit.

b. No particular assumption is needed to calculate the break-even volume.

c. A fixed product mix will produce a unique break-even solution.

d. Weighted-average product mix method can be used.

9. A start-up company manufactures two products: X is sold for $5 with variable cost of $3

each; Y is sold for $8 with variable cost of $4 each. An annual fixed cost of $10,000 is

projected. The marketing department estimates a 3:1 ratio between X and Y. How many units

of X must be sold to break even for the first year of operation?

a. 3,000

b. 3,600

c. 1,000

d. 1,500

10. CVP analysis:

a. Requires certain assumptions to be made.

b. Is inherently limited by its applicability.

c. Usually assumes unit variable cost to be constantly changing.

d. Does not allow for alternative assumptions.

11. In October, Fashionable Clothing manufactured 2,000 items with the following financial

statement amounts: direct materials $12,000, sales $48,000, direct labor $16,000,

depreciation $3,600, rent $1,500, and variable overhead $9,000. What is contribution margin

per unit?

a. $5.50

b. $2.95

c. $3.40

d. $4.10

12. Which of the following statements regarding margin of safety is correct?

a. The margin of safety indicates the risk of losing money.

b. The break-even sales volume is not considered.

c. Margin of safety is expressed in sales dollars only.

d. The higher the fixed costs, the lower the margin of safety.

3–17

Multiple Choice Answers

2. d (LO1)

3–18

3–19

Demonstration Problem 1

The Power Tool Division of ABC Hardware sells one product, Jig Saw, and has the following

data for the second quarter:

Units of output

1,200 units

Price per unit

$ 150

Variable cost per unit

90

Total fixed costs

48,000

Required:

Determine the following:

1. Quarterly operating profit when 1,200 units are sold.

2. Break-even volume in units.

3. Contribution margin ratio.

4. Break-even volume in sales dollars.

5. Sales dollars and units needed to generate an operating profit of $57,000.

6. Number of units sold that would produce an operating profit of 15% of sales dollars.

Demonstration Problem 1 – Solution

CM = Contribution margin

Part 1

Part 6

Let X = Number of units sold that would produce an operating profit of 15% of sales dollars

3–21

Demonstration Problem 2

(Same background information as in Demonstration Problem 1.)

The Power Tool Division of ABC Hardware sells one product, Jig Saw, and has the following

data for the second quarter:

Units of output

1,200 units

Price per unit

$ 150

Variable cost per unit

90

Total fixed costs

48,000

Required:

Assume that the Power Tool Division of ABC Hardware now faces a tax rate of 30 percent.

Determine the number of Jig Saws required to generate the after-tax operating profit of $16,800.

3–22

Demonstration Problem 2 – Solution

CM = Contribution margin

3–23

Demonstration Problem 3

(Same background information as in Demonstration Problem 1.)

The Power Tool Division of ABC Hardware sells one product, Jig Saw, and has the following

data for the second quarter:

Units of output

1,200 units

Price per unit

$150

Variable cost per unit

90

Total fixed costs

48,000

Required:

Assume that the Power Tool Division introduces a second product, Circular Saw, with a unit

price of $200 and a unit variable cost of $120. The total fixed cost is increased to $68,000. The

manager of ABC Hardware estimates that Jig Saws and Circular Saws will sell in a 3:2 ratio.

Calculate the break-even volume in units using:

1. Fixed product mix method

2. Weighted-average contribution margin method

Demonstration Problem 3 – Solution

CM = Contribution margin

Part 1

According to the product mix, out of every 5 units sold, three will be Jig Saws and two will be

Circular Saws. Let X represent the number of such 5-unit packages to break even.

Part 2

The produce mix consists of 60 % (or 3 ÷ 5) Jig Saws and 40% (or 2 ÷ 5) Circular Saws.