CHAPTER 3 The Adjusting Process

Prob. 3-5A (Concluded)

2.

Debit Credit

Balances Balances

Cash 6,820

Accounts Receivable 44,080

Prepaid Insurance 550

Unearned Rent 2,050

Salaries and Wages Payable 2,550

Suzanne Emerson, Capital 338,000

Suzanne Emerson, Drawing 14,000

Fees Earned 304,460

Rent Revenue 4,090

Salaries and Wages Expense 178,500

Utilities Expense 38,560

849,750 849,750

October 31, 20Y6

Emerson Company

Adjusted Trial Balance

CHAPTER 3 The Adjusting Process

Prob. 3-6A

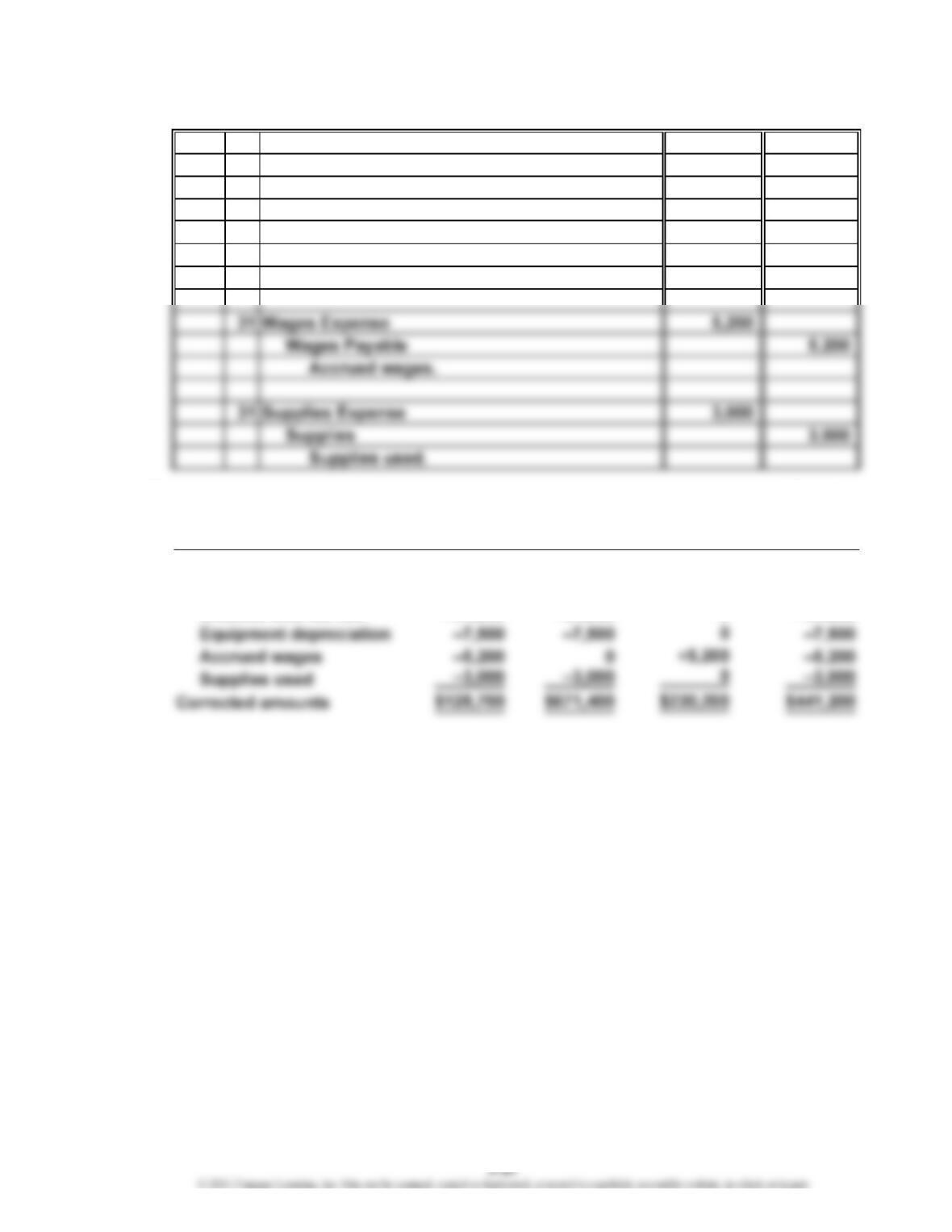

1. Apr. 30 Supplies Expense

Supplies 2,750

Supplies used.

30 Wages Expense

Wages Payable 1,400

Accrued wages.

2. Total

Net Total Owner’s

Income Assets = + Equity

Reported amounts $120,000 $750,000 $450,000

Corrections:

Supplies used –2,750 –2,750 –2,750

Unbilled fees earned +23,700 +23,700 +23,700

1,400

2,750

Total

Liabilities

$300,000

0

0

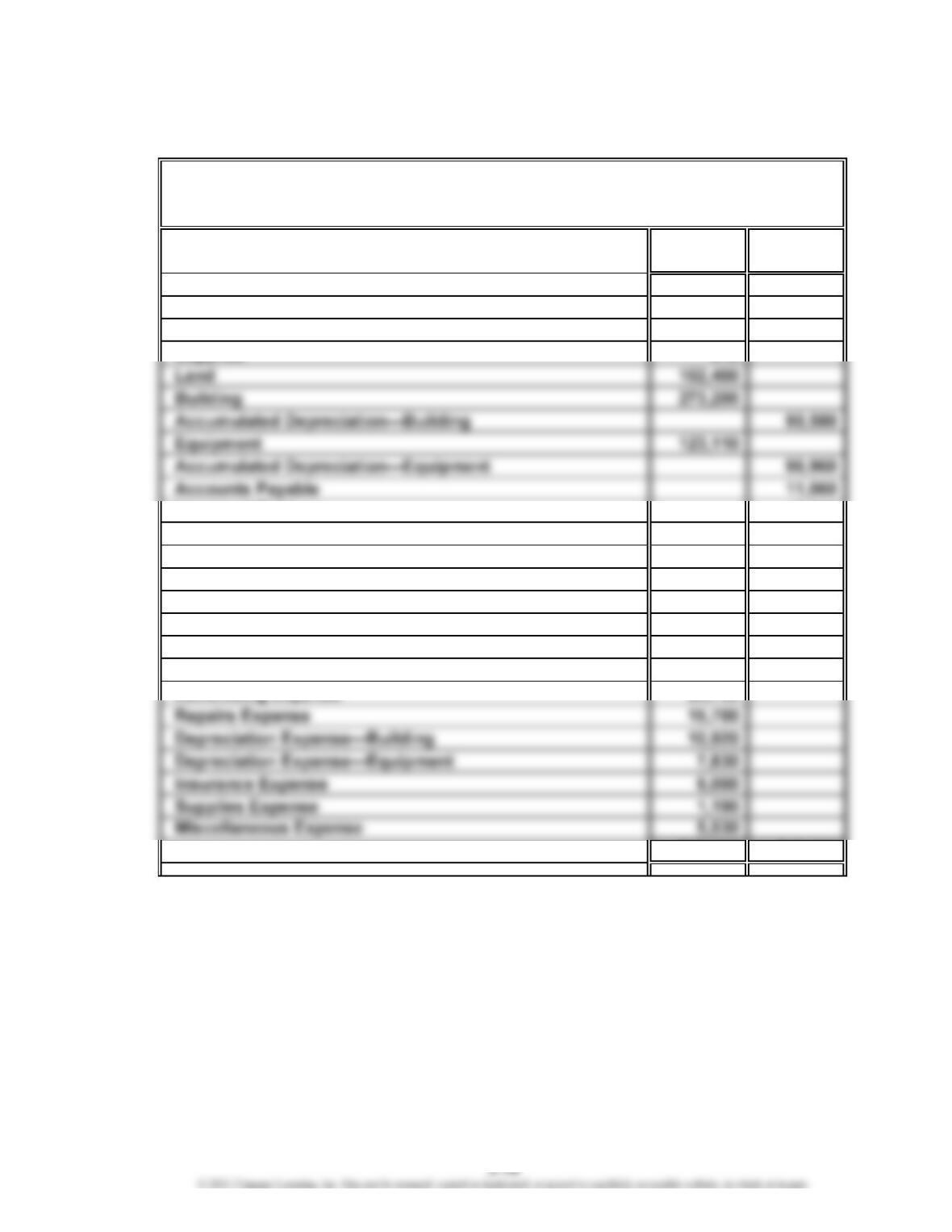

CHAPTER 3 The Adjusting Process

Prob. 3-1B

1. May 31 Accounts Receivable 19,750

Fees Earned 19,750

Accrued fees earned.

31 Unearned Rent 3,000

Rent Revenue 3,000

Rent earned ($9,000 ÷ 3 months).

31 Depreciation Expense 3,200

Accumulated Depreciation—Equipment 3,200

Depreciation expense.

CHAPTER 3 The Adjusting Process

Prob. 3-2B

1. Nov. 30 Supplies Expense 2,620

Supplies 2,620

Supplies used ($3,170 – $550).

30 Wages Expense 2,000

Wages Payable 2,000

Accrued wages.

Accrued fees.

2. Fees Earned would be understated by $6,000, Depreciation Expense would

be understated by $1,675, and net income would be understated by $4,325

($6,000 – $1,675).

4. There is no effect on “Net increase or decrease in cash” on the statement of

of cash flows because adjusting entries do not affect cash.

CHAPTER 3 The Adjusting Process

Prob. 3-3B

1. 20Y4

Apr. 30 Supplies Expense 5,820

Supplies 5,820

Supplies used ($7,200 – $1,380).

30 Wages Expense 2,475

Wages Payable 2,475

Accrued wages.

30 Unearned Fees 14,140

Fees Earned 14,140

Fees earned.

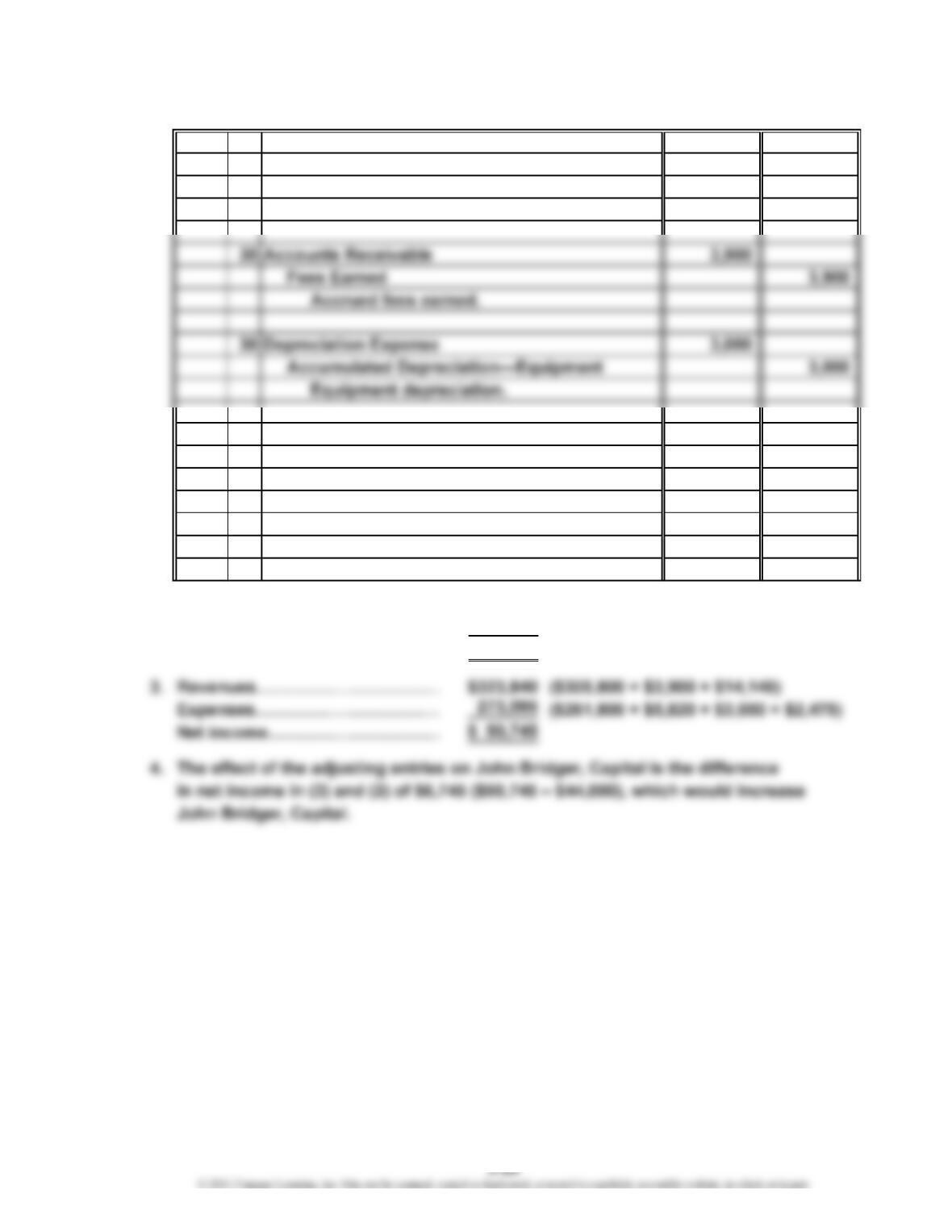

2. Revenues…………………………… $305,800

Expenses…………………………… 261,800 ($157,800 + $55,000 + $42,000 + $7,000)

Net income…………………………

…

$ 44,000

…

CHAPTER 3 The Adjusting Process

Prob. 3-4B

20Y5

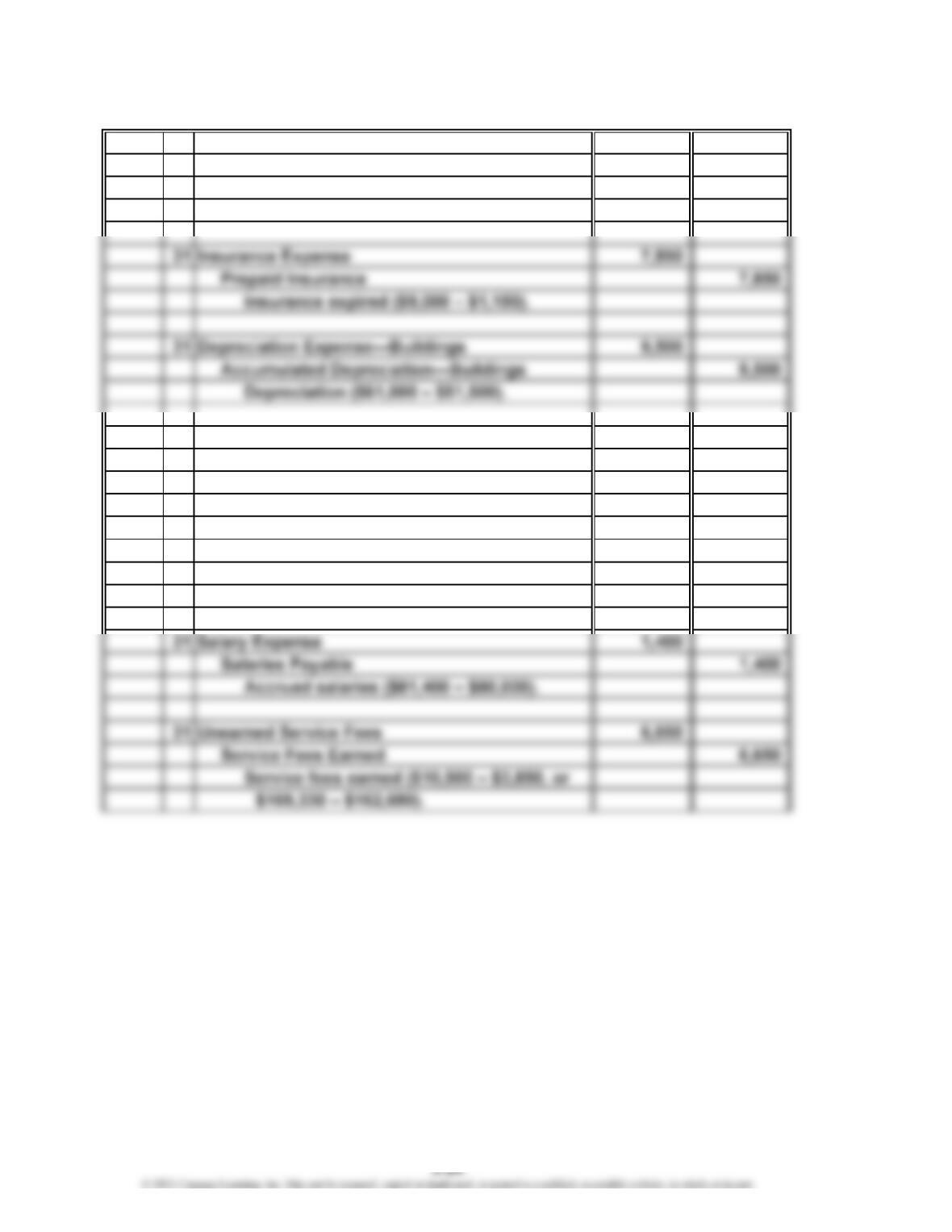

Mar. 31 Supplies Expense 4,025

Supplies 4,025

Supplies used ($6,200 – $2,175).

31 Depreciation Expense—Trucks 5,000

Accumulated Depreciation—Trucks 5,000

Depreciation ($17,000 – $12,000).

31 Utilities Expense 1,830

Accounts Payable 1,830

Accrued utilities expense

($8,750 – $6,920, or $8,030 – $6,200).

CHAPTER 3 The Adjusting Process

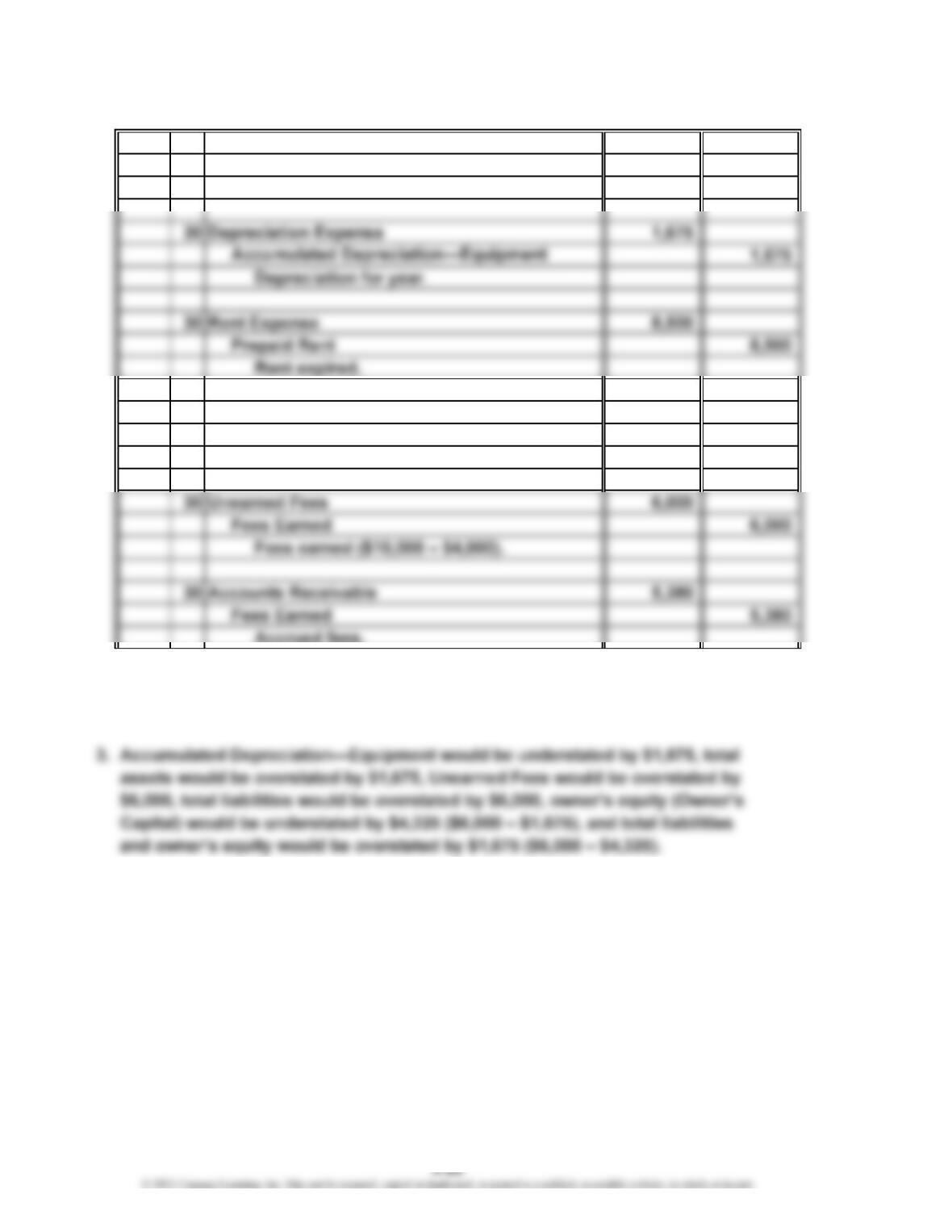

Prob. 3-5B

1. 20Y6

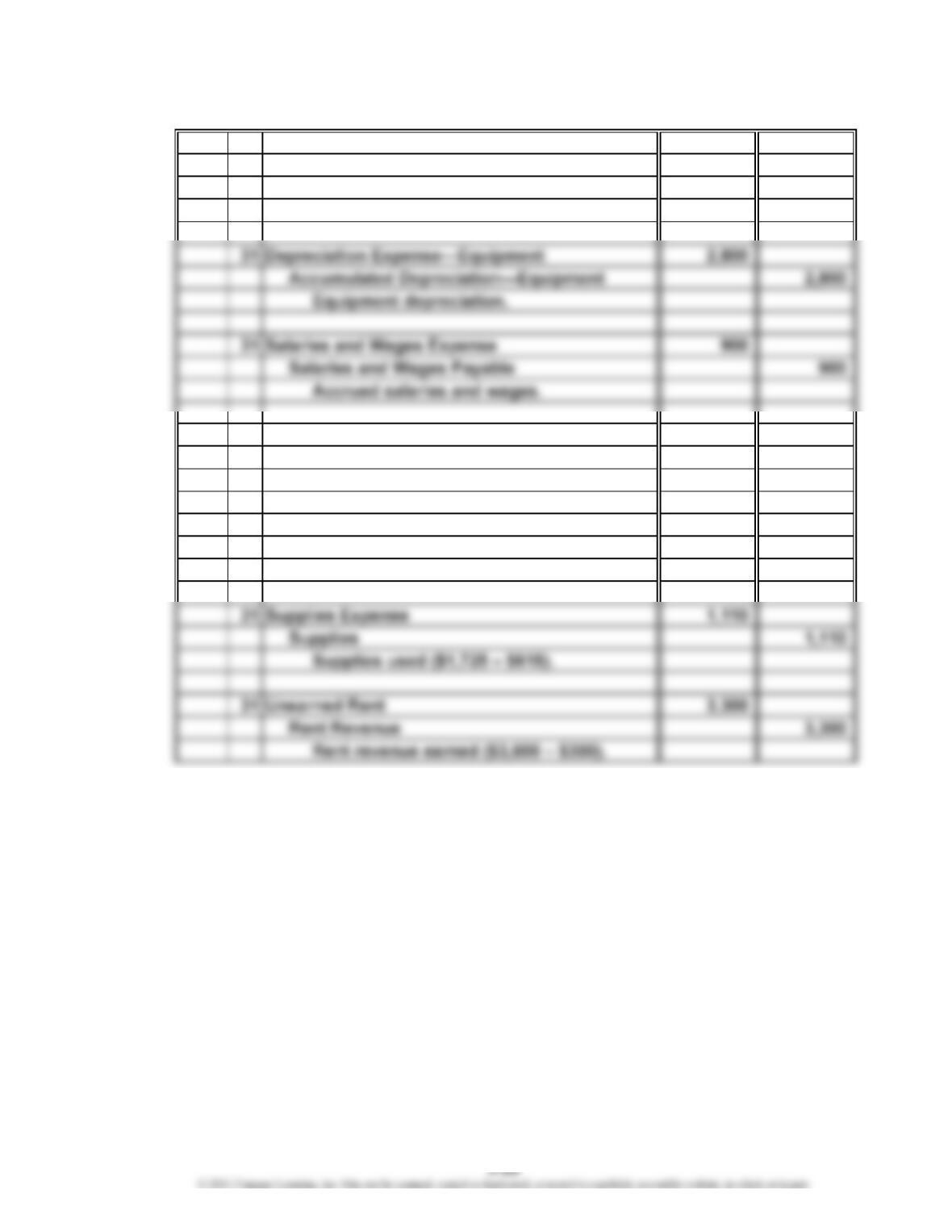

July 31 Depreciation Expense—Building 6,400

Accumulated Depreciation—Building 6,400

Building depreciation.

31 Insurance Expense 4,500

Prepaid Insurance 4,500

Insurance expired ($6,000 – $1,500).

31 Accounts Receivable 10,200

Fees Earned 10,200

Accrued fees earned.

CHAPTER 3 The Adjusting Process

Prob. 3-5B (Concluded)

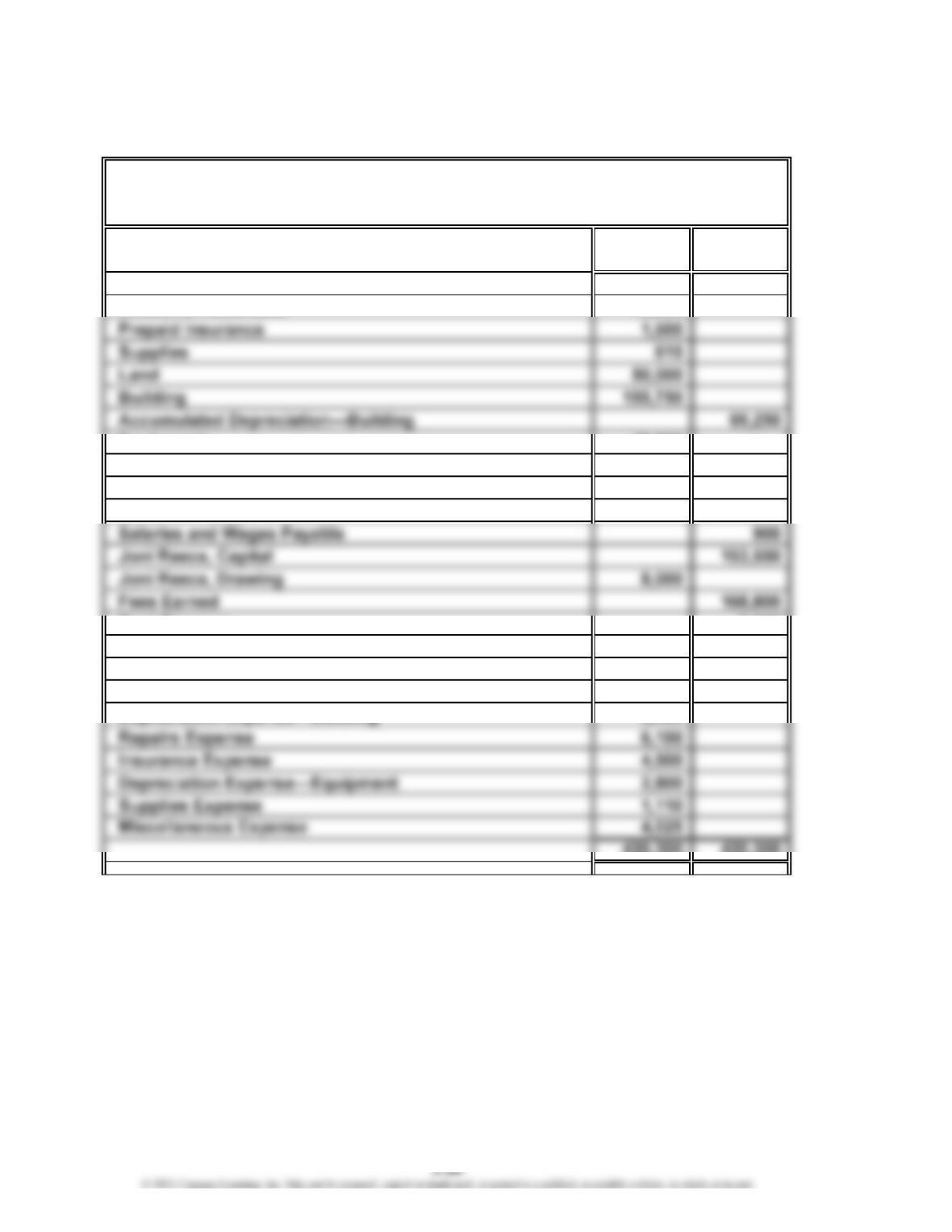

2.

Debit Credit

Balances Balances

Cash 10,200

Accounts Receivable 44,950

Equipment 45,000

Accumulated Depreciation—Equipment 20,450

Accounts Payable 3,750

Unearned Rent 300

Rent Revenue 3,300

Salaries and Wages Expense 57,750

Utilities Expense 14,100

Advertising Expense 7,500

420,300 420,300

July 31, 20Y6

Reece Financial Services Co.

Adjusted Trial Balance

CHAPTER 3 The Adjusting Process

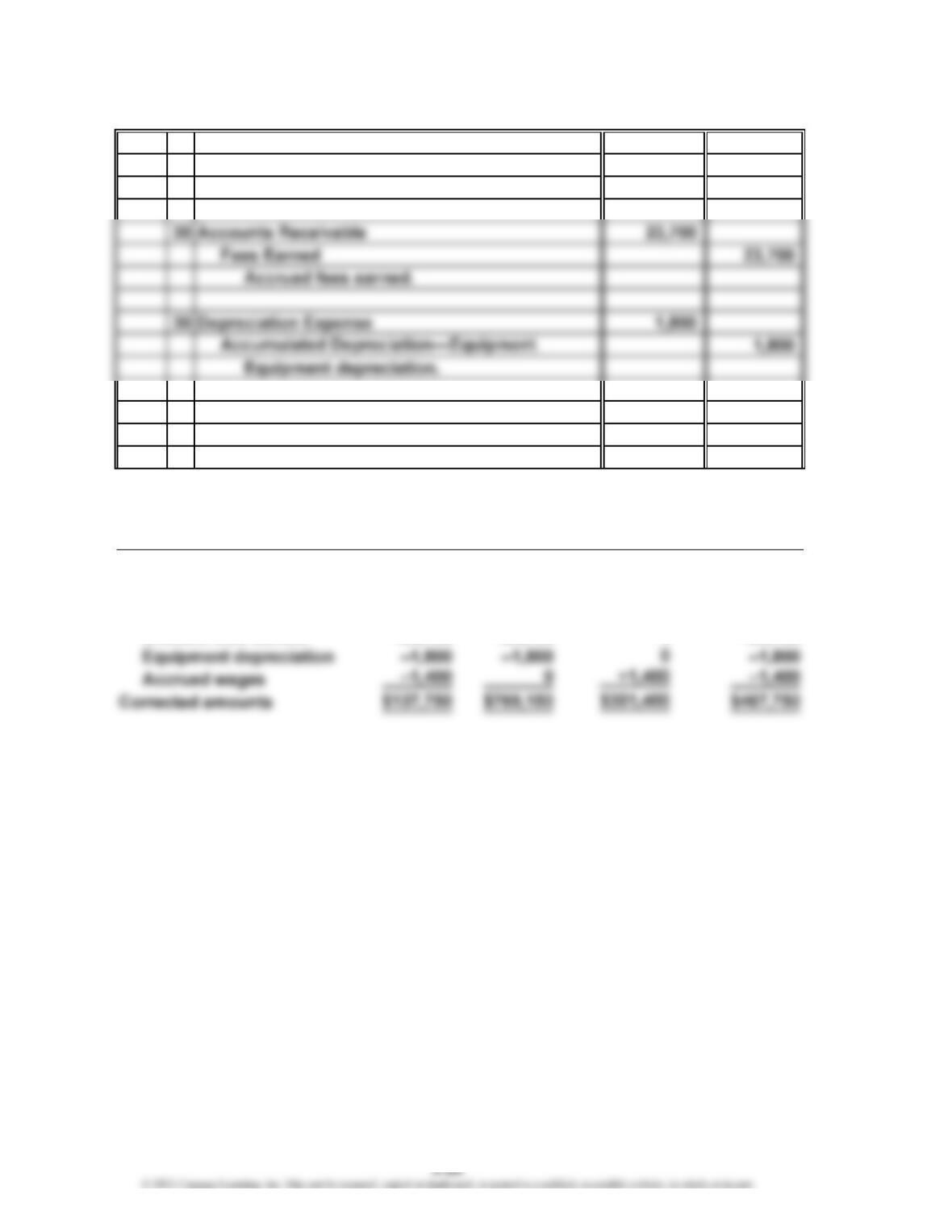

Prob. 3-6B

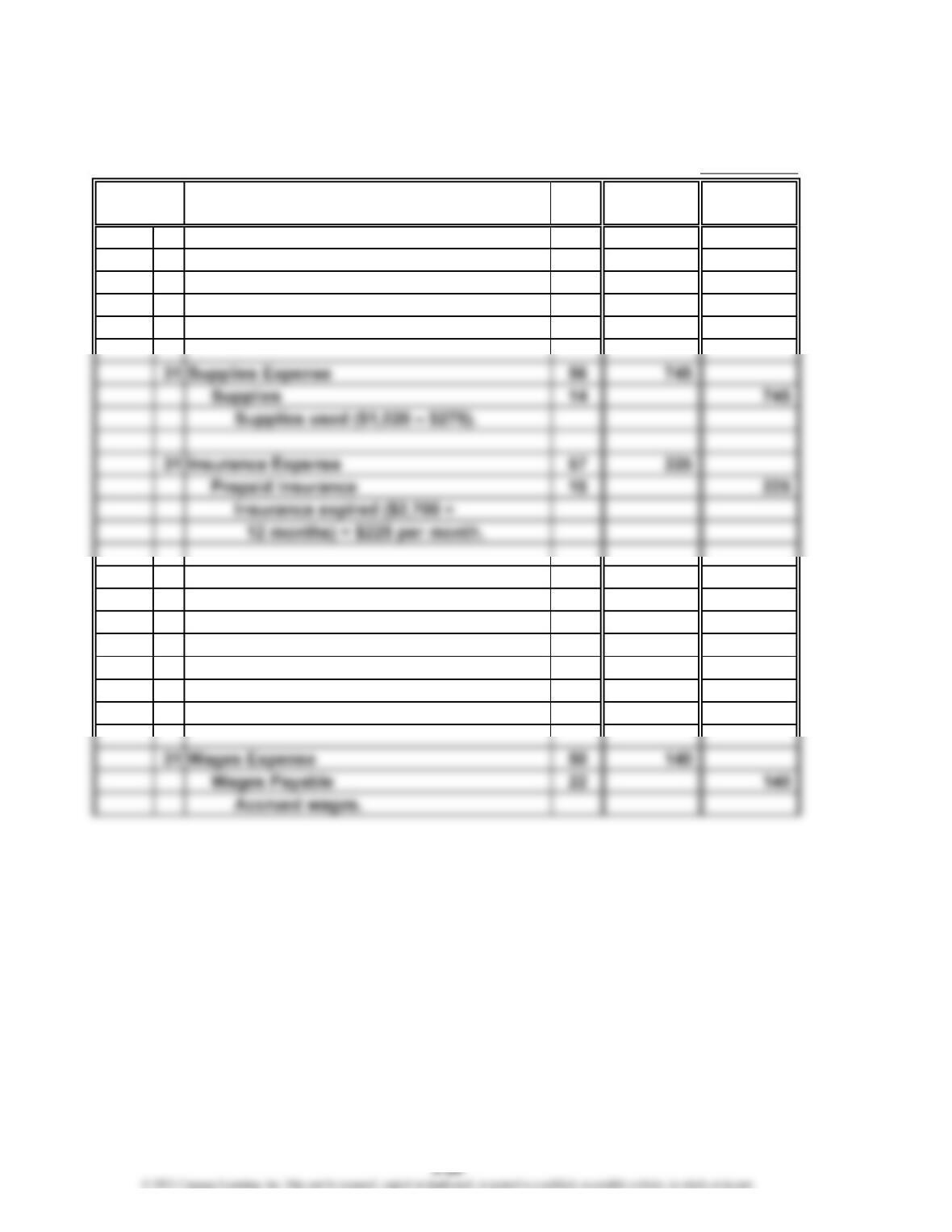

1. Aug. 31 Accounts Receivable

Fees Earned 31,900

Accrued fees earned.

31 Depreciation Expense

Accumulated Depreciation—Equipment 7,500

Equipment depreciation.

2. Total

Net Total Owner’s

Income Assets = + Equity

Reported amounts $112,500 $650,000 $425,000

Corrections:

Unbilled fees earned +31,900 +31,900 +31,900

0

Total

Liabilities

$225,000

31,900

7,500

CHAPTER 3 The Adjusting Process

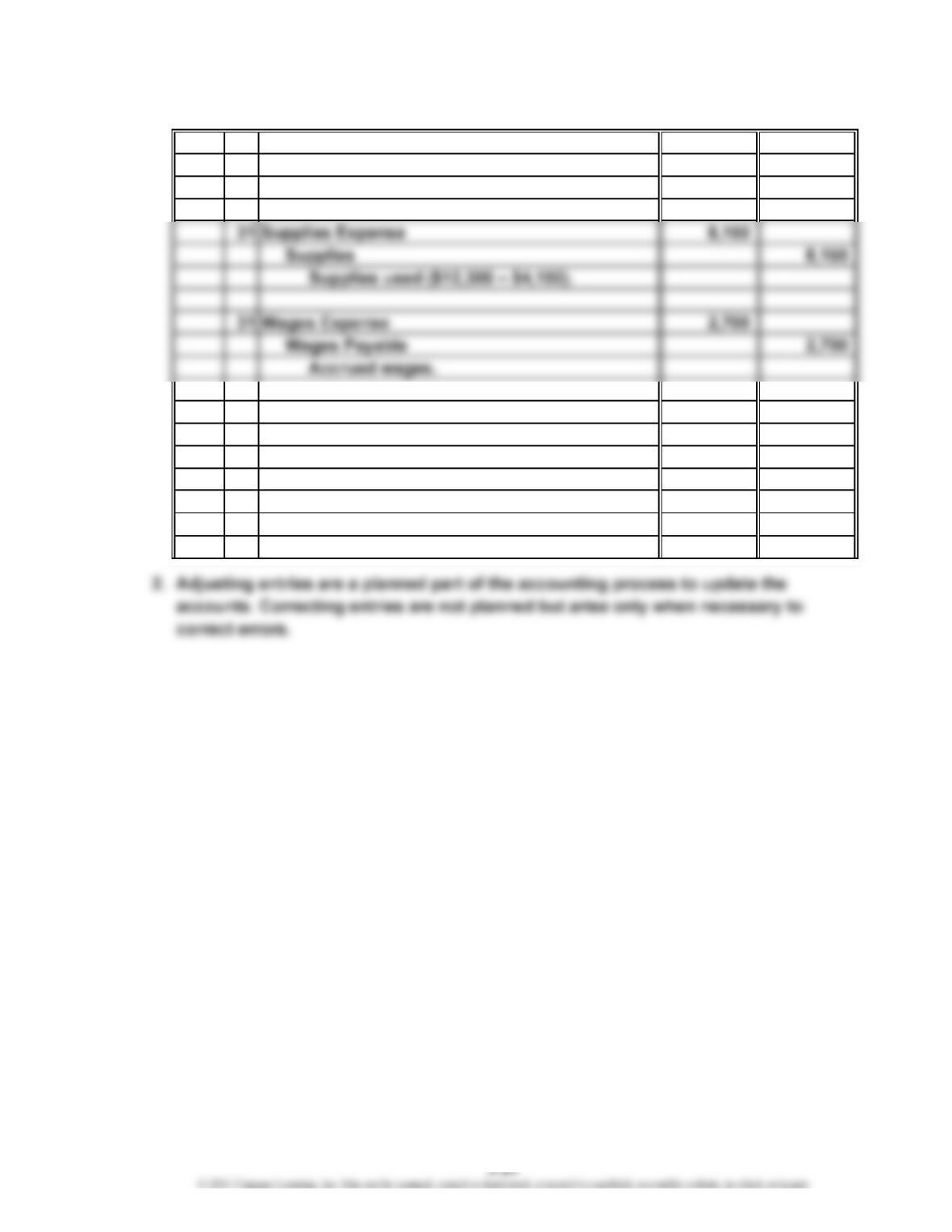

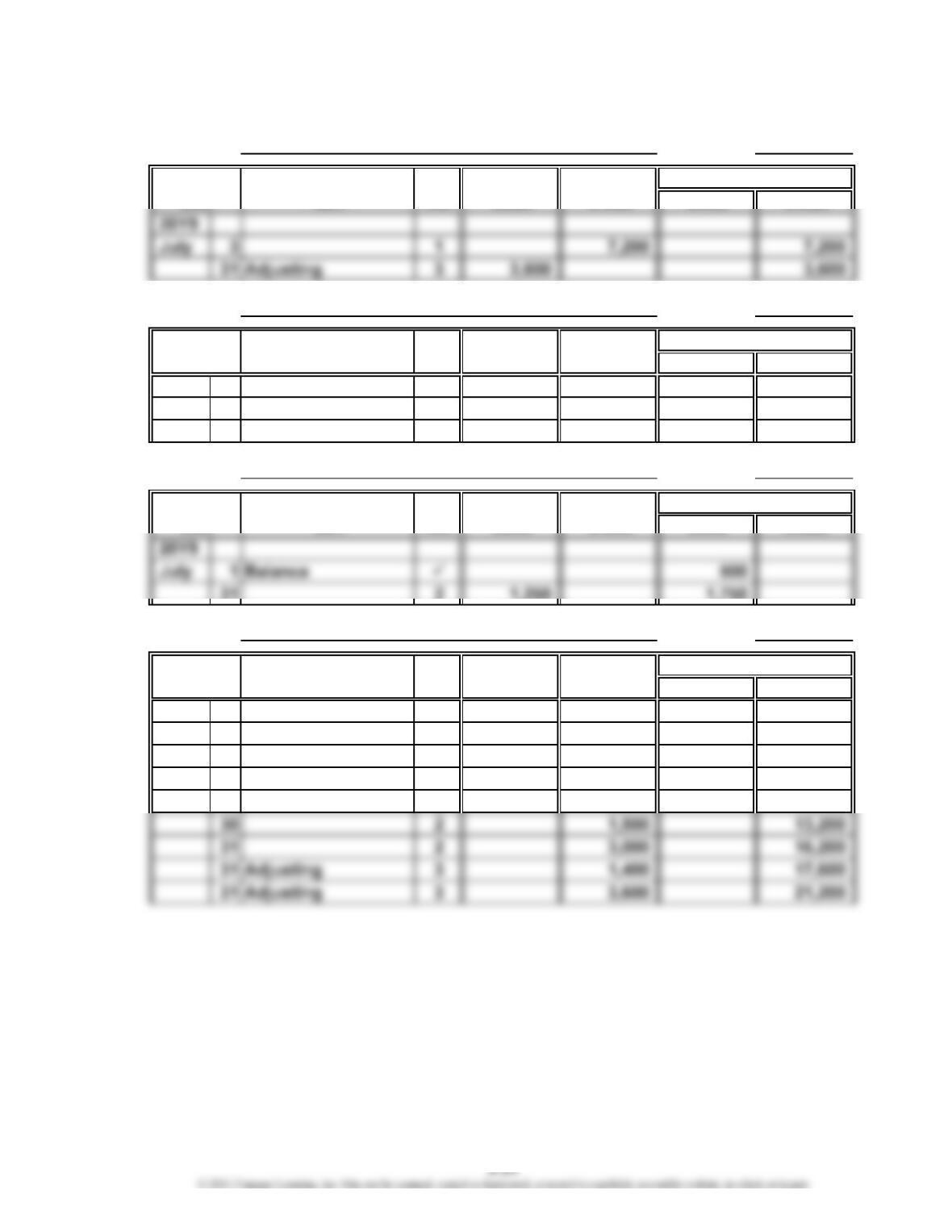

1.

Page 3

Post.

Ref. Debit Credit

20Y9

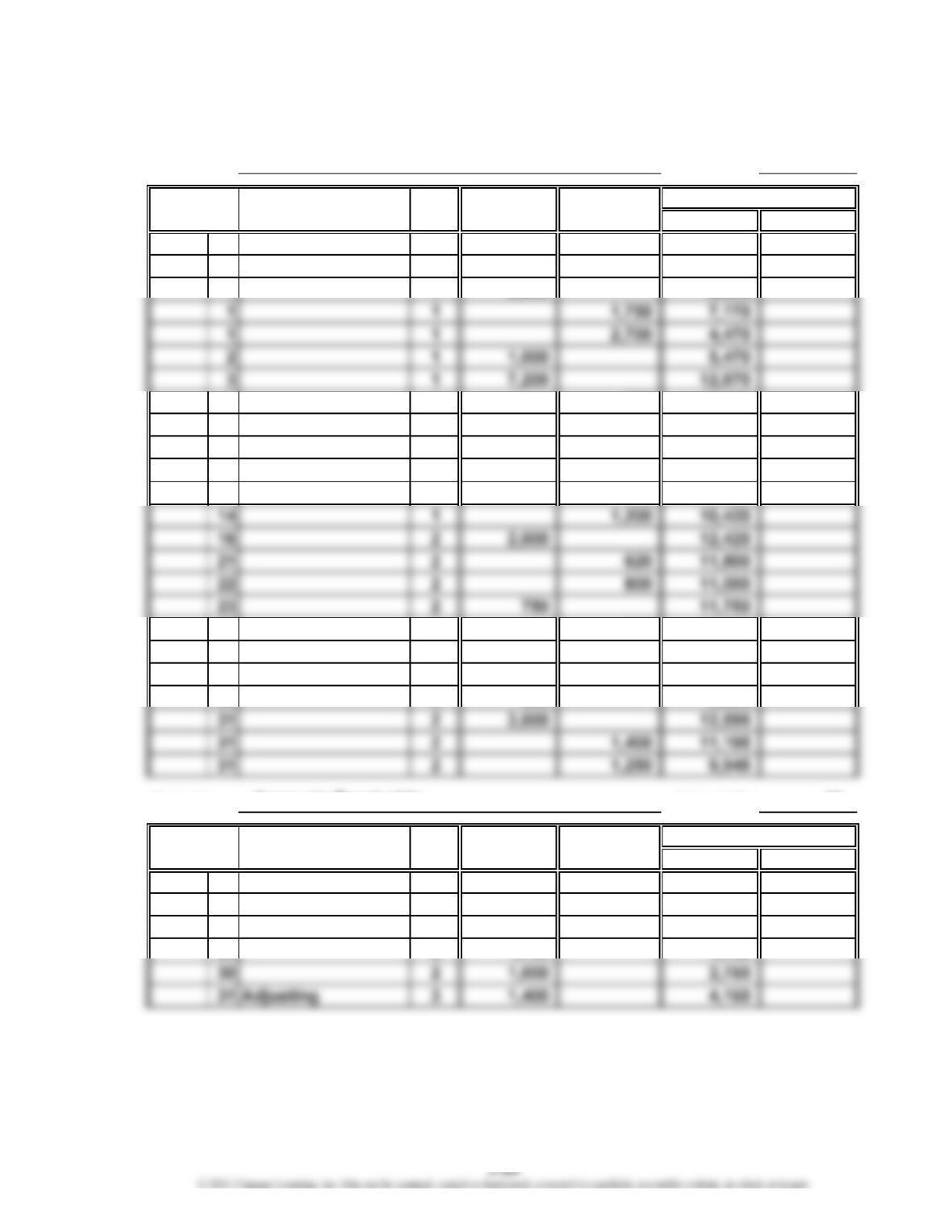

July 31 Accounts Receivable 12 1,400

Fees Earned 41 1,400

Accrued fees earned (115 hrs. –

80 hrs.) × $40 = $1,400.

31 Depreciation Expense 58 50

Accum. Depr.—Office Equipment 18 50

Office equipment depreciation.

31 Unearned Revenue 23 3,600

Fees Earned 41 3,600

Fees earned ($7,200 ÷ 2 months).

CONTINUING PROBLEM

Date

JOURNAL

Adjusting Entries

Description

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

2.

Account No. 11

Post.

Item Ref. Debit Debit Credit

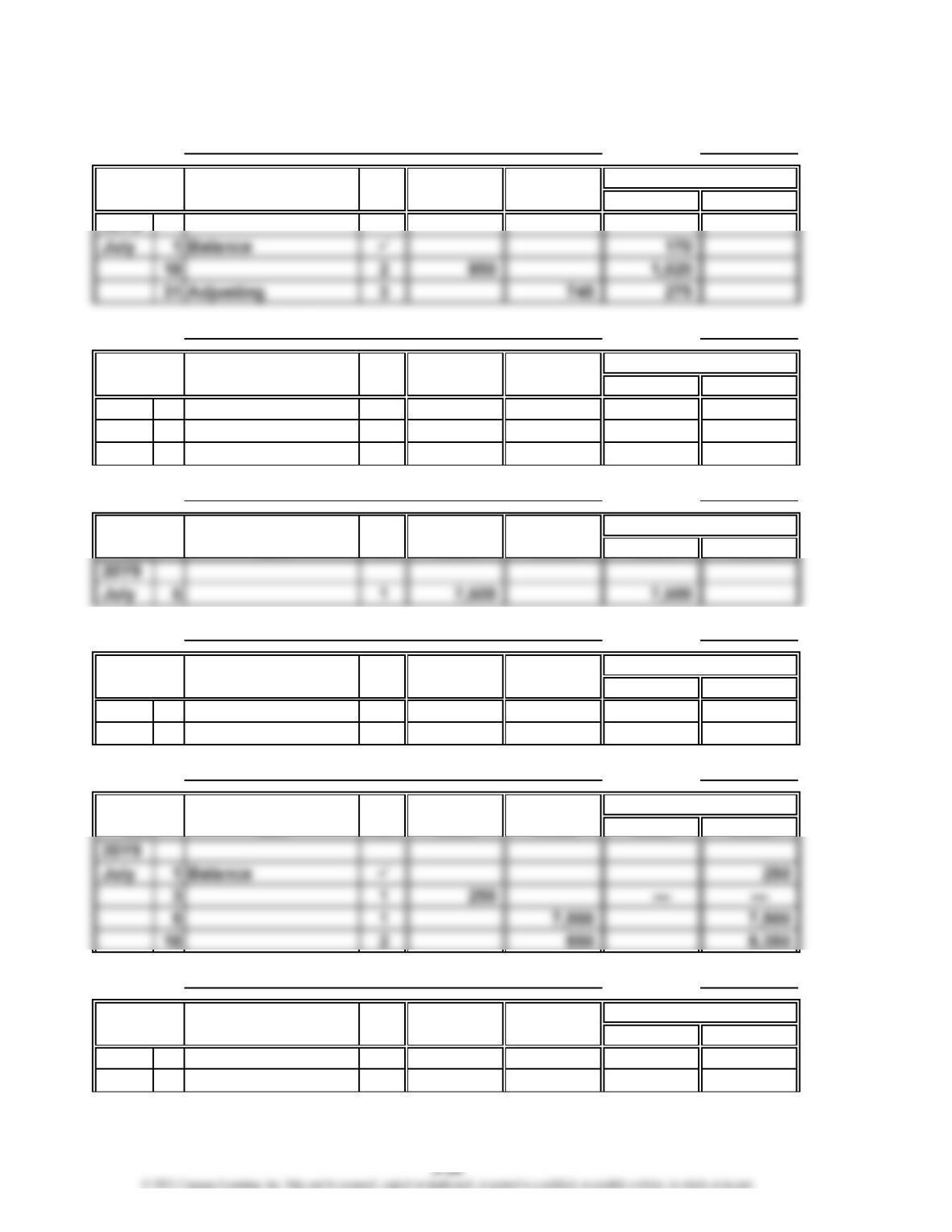

20Y9

July 1 Balance 3,920

3 1 12,420

4 1 11,520

8 1 11,320

11 1 1,000 12,320

13 1 11,620

27 2 10,835

28 2 9,635

29 2 9,095

Account No. 12

Post.

Item Ref. Debit Debit Credit

20Y9

July 1 Balance 1,000

21 ——

1,000

Balance

1,200

540

Date Credit

700

Account: Accounts Receivable

915

250

900

200

Account: Cash

Balance

CreditDate

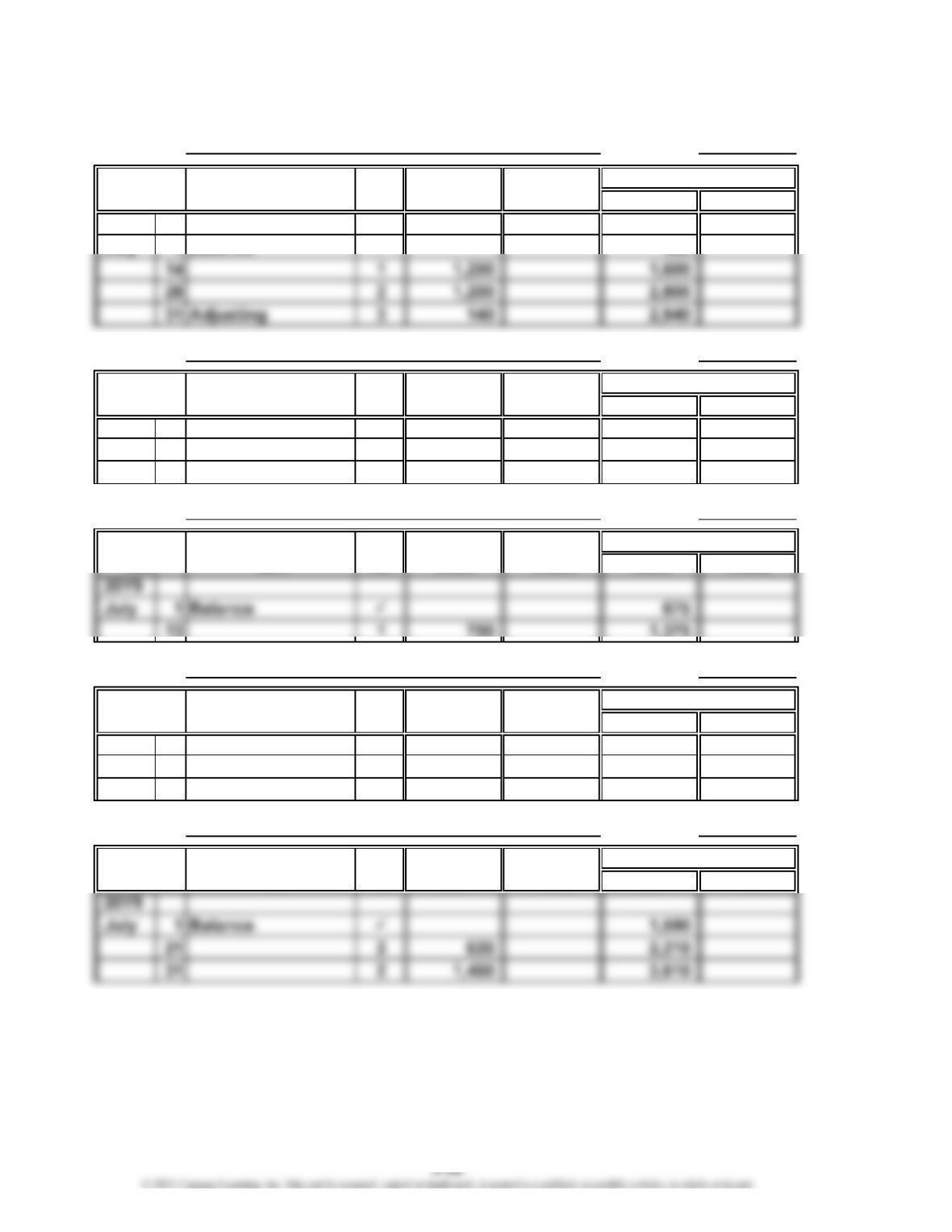

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 14

Post.

Item Ref. Debit Credit Debit Credit

Account No. 15

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 1 2,700 2,700

31 Adjusting 3 225 2,475

Account No. 17

Post.

Item Ref. Debit Credit Debit Credit

Account No. 18

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 31 Adjusting 3 50 50

Account No. 21

Post.

Item Ref. Debit Credit Debit Credit

Account No. 22

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 31 Adjusting 3 140 140

Account: Supplies

Account: Prepaid Insurance

Date

Balance

Account: Accounts Payable

Date

Balance

Account: Wages Payable

Date

Balance

Date

Balance

Balance

Balance

Date

Account: Office Equipment

Date

Account: Accumulated Depreciation—Office Equipment

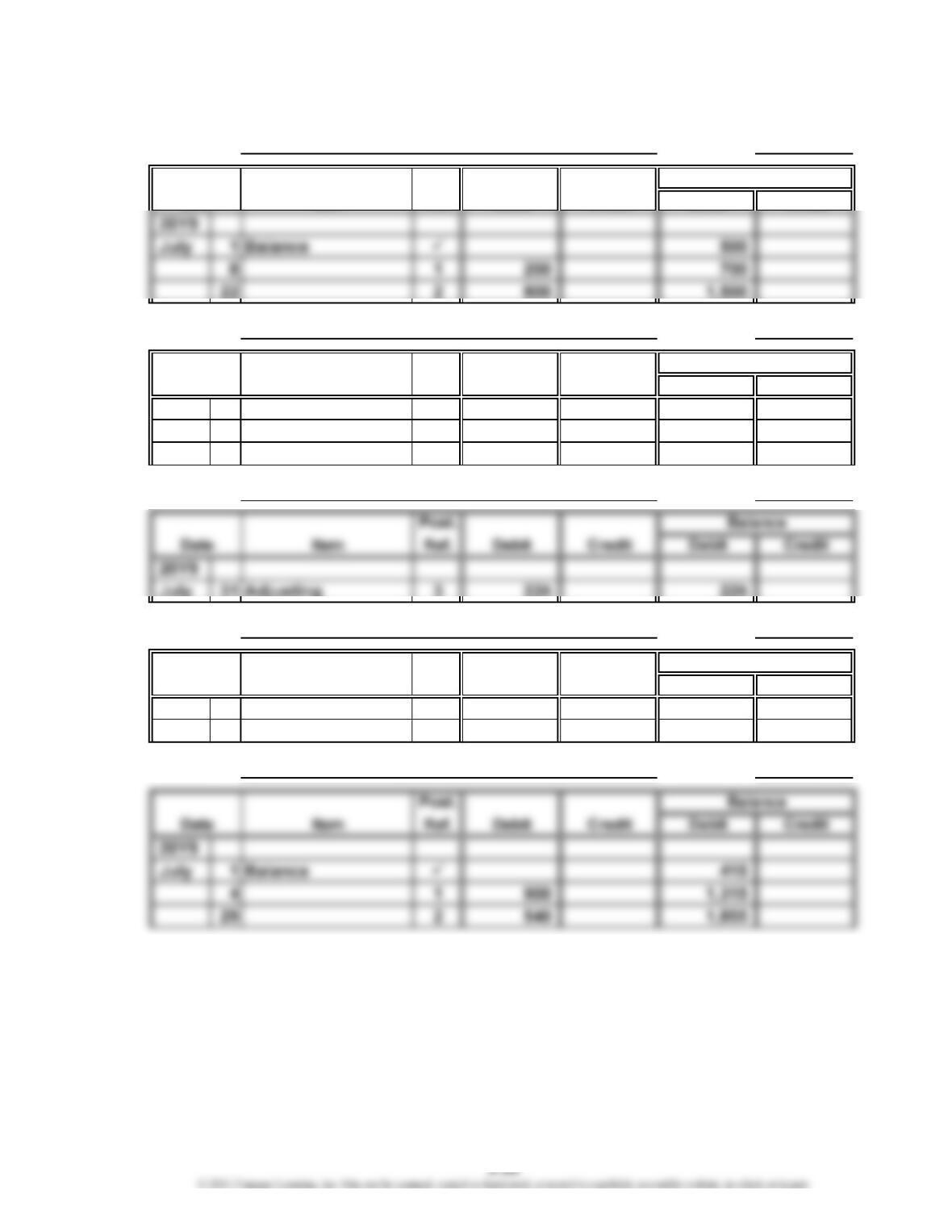

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 23

Post.

Account No. 31

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 4,000

1 1 5,000 9,000

Account No. 32

Post.

31 2 1,250 1,750

Account No. 41

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 6,200

11 1 1,000 7,200

16 2 2,000 9,200

23 2 2,500 11,700

Balance

Date

Account: Fees Earned

Balance

Balance

Date

Account:

Account: Unearned Revenue

Account: Peyton Smith, Capital

Balance

Peyton Smith, Drawing

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 50

Post.

Item Ref. Debit Credit Debit Credit

20Y9

Account No. 51

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 800

1 1 1,750 2,550

Account No. 52

Post.

13 1 700 1,375

Account No. 53

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 300

27 2 915 1,215

Account No. 54

Post.

Item Ref. Debit Credit Debit Credit

Date

Balance

Account: Wages Expense

Music Expense

Account: Office Rent Expense

Account: Equipment Rent Expense

Date

Balance

Date

Balance

Balance

Balance

Account: Utilities Expense

Date

Account:

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 55

Post.

Item Ref. Debit Credit Debit Credit

Account No. 56

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 180

31 Adjusting 3 745 925

Account No. 57

July 31 Adjusting 3 225 225

Account No. 58

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 31 Adjusting 3 50 50

Account No. 59

Balance

Account: Advertising Expense

Date

Balance

Account: Supplies Expense

Date

Balance

Date

Account: Miscellaneous Expense

Account: Insurance Expense

Account: Depreciation Expense

CHAPTER 3 The Adjusting Process

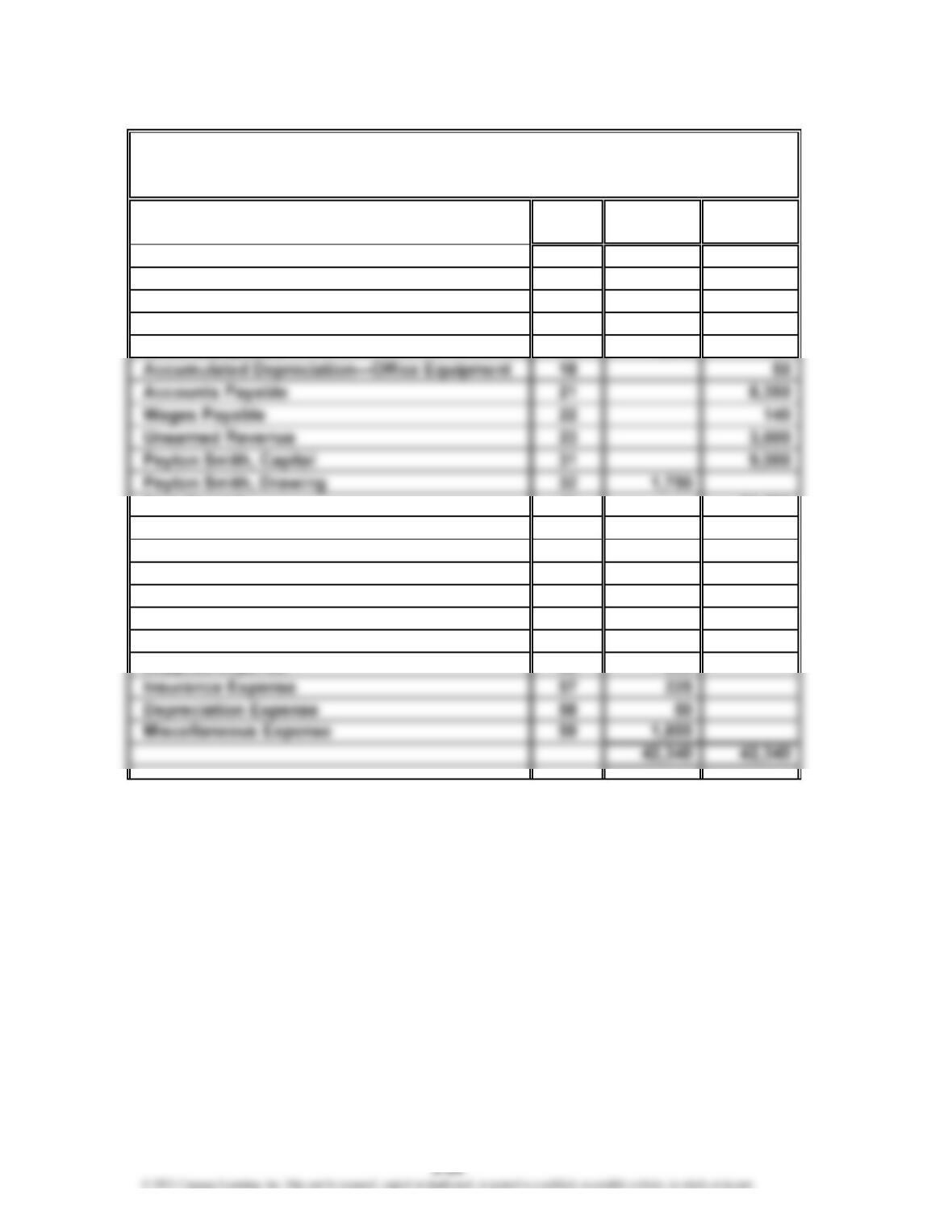

Continuing Problem (Concluded)

3.

Account Debit Credit

No. Balances Balances

Cash 11 9,945

Accounts Receivable 12 4,150

Supplies 14 275

Prepaid Insurance 15 2,475

Office Equipment 17 7,500

Fees Earned 41 21,200

Wages Expense 50 2,940

Office Rent Expense 51 2,550

Equipment Rent Expense 52 1,375

Utilities Expense 53 1,215

Music Expense 54 3,610

Advertising Expense 55 1,500

PS Music

Adjusted Trial Balance

July 31, 20Y9

CHAPTER 3 The Adjusting Process

CP 3-1

1. No. The accrual basis of accounting requires that revenues be reported in the

period in which they are earned. When revenue is reported before it is earned, the

revenues do not accurately reflect the revenues for the period. By knowingly

CP 3-2

It is acceptable for Daryl to prepare the financial statements for Squid Realty Co. on

an accrual basis. The revision of the financial statements to include the accrual of

the $30,000 commission as of December 28, 20Y7, would not be appropriate. Most

real estate contracts include contingencies that can void the contract. Such

contingencies include obtaining a loan, appraisals, environmental studies, and

CP 3-3

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31, 2018,

follows:

1. Athletic footwear, apparel, and equipment

2. 3

3. $1,933 million in 2018; $4,240 million in 2017; $3,760 million in 2016

4. $36,397 million in 2018; $34,350 million in 2017; $32,376 million in 2016

CASES & PROJECTS

CHAPTER 3 The Adjusting Process

CP 3-4

To: My Instructor

From: Ima Student

Re: Revenue Recognition of Ticket Sales at Delta Air Lines

Customers of Delta Air Lines typically purchase tickets for air travel several weeks prior

to their scheduled flight and pay for their tickets using a credit card such as VISA or

American Express. While the credit card company will remit payment to Delta shortly

after the ticket is purchased, Delta will not record revenue from the ticket until after

CP 3-5

a. There are several indications that adjusting entries were not recorded before

the financial statements were prepared, including:

1. All expenses on the income statement are identified as “paid” items and

not as “expenses.”

b. Likely accounts requiring adjustment include:

1. Accumulated Depreciation—Truck for depreciation expense.

2. Supplies (paid) Expense for supplies on hand.