3-41 Ch. 3—Problems

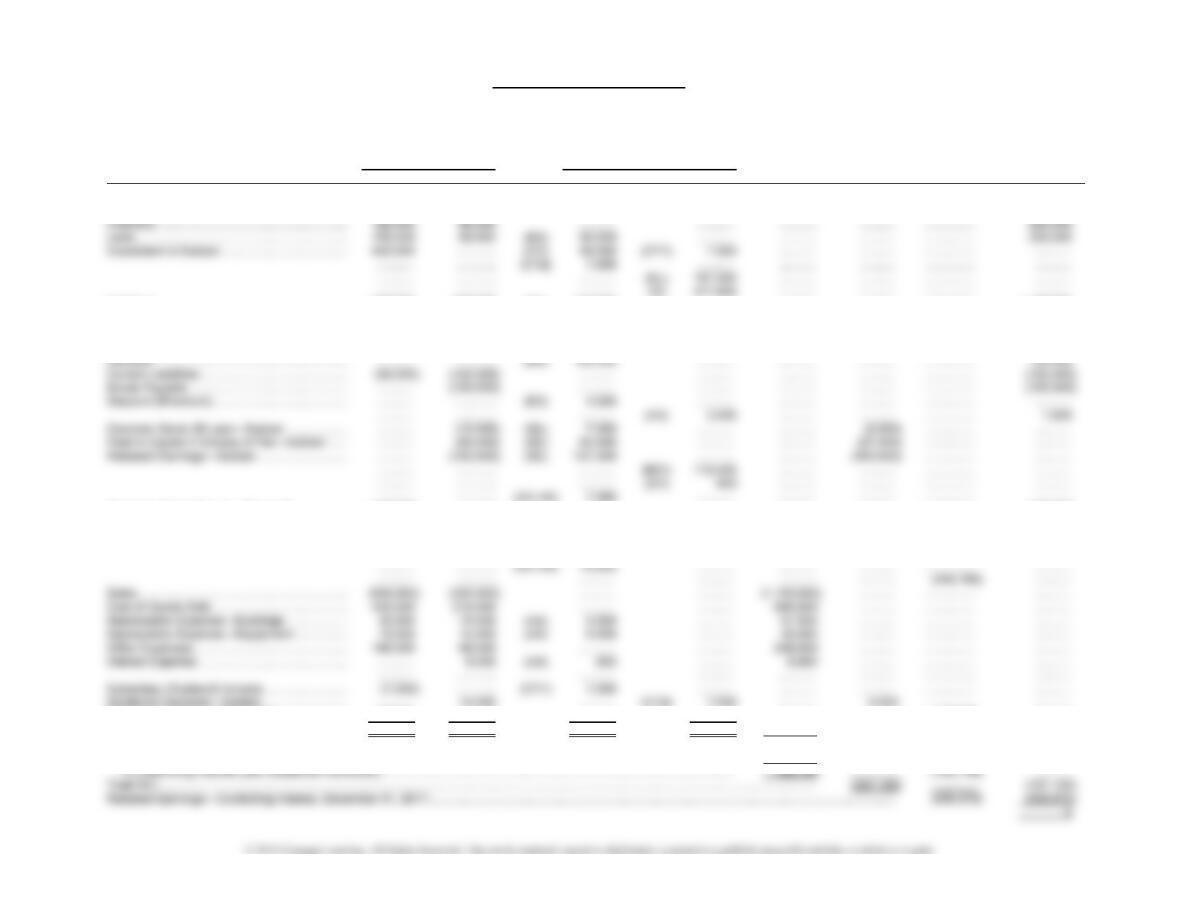

Problem 3-8, Continued

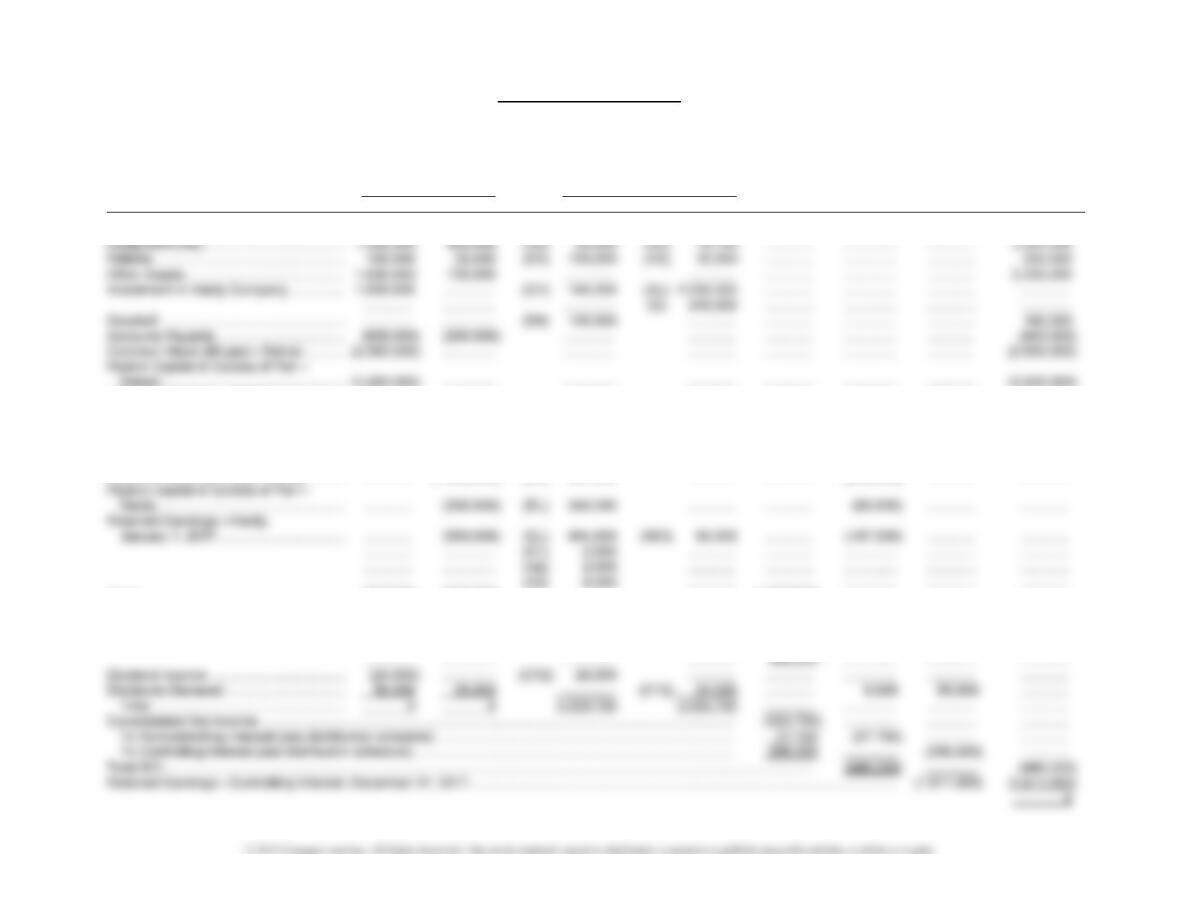

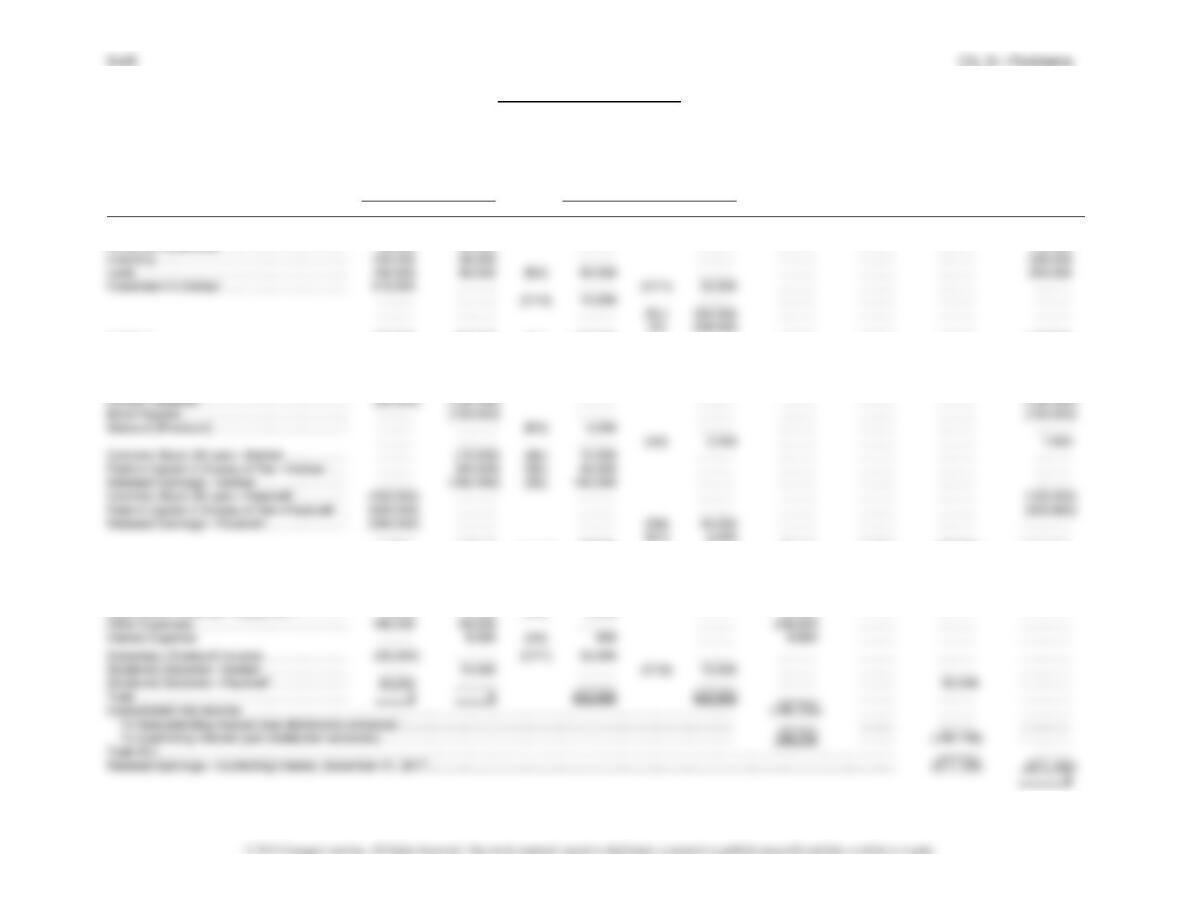

(2) Detner International and Subsidiary Hardy Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Detner Hardy Dr. Cr. Statement NCI Earnings Sheet

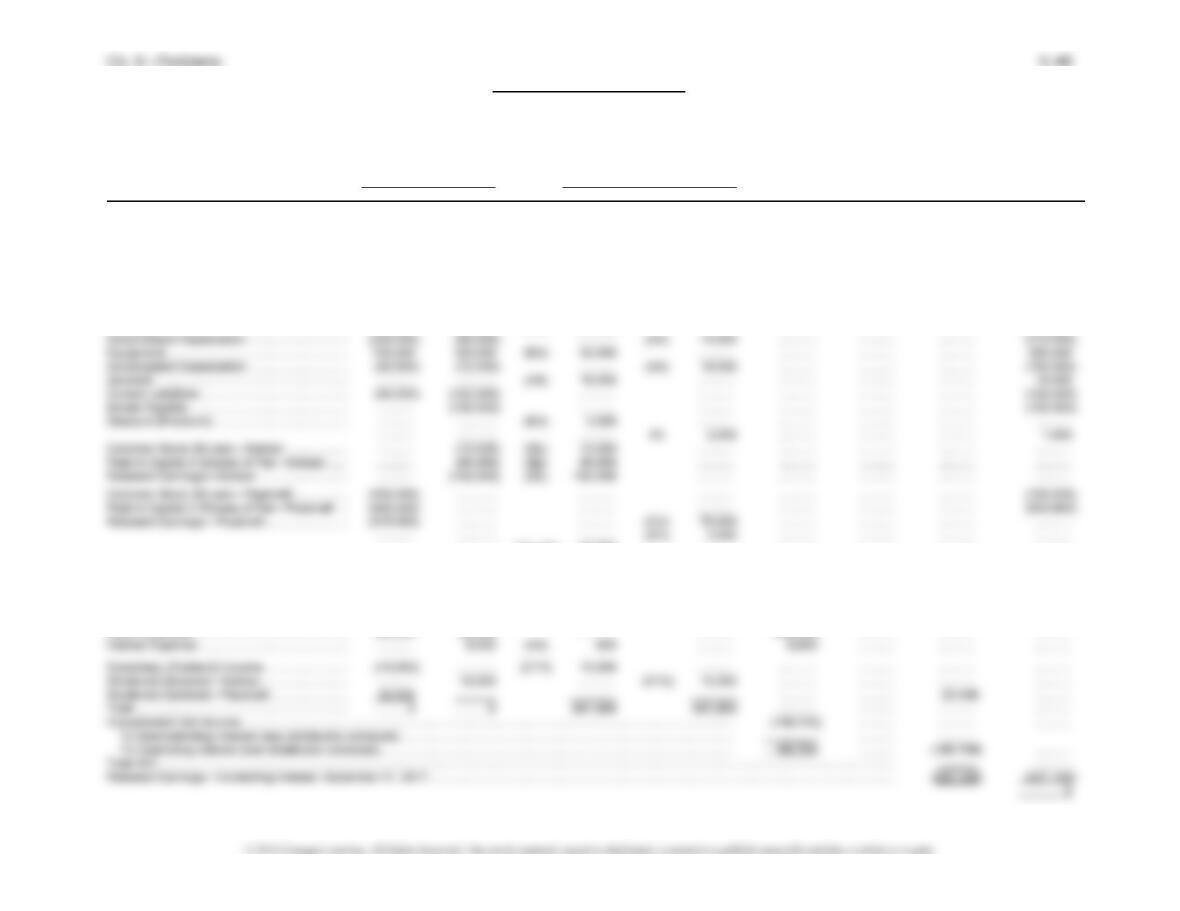

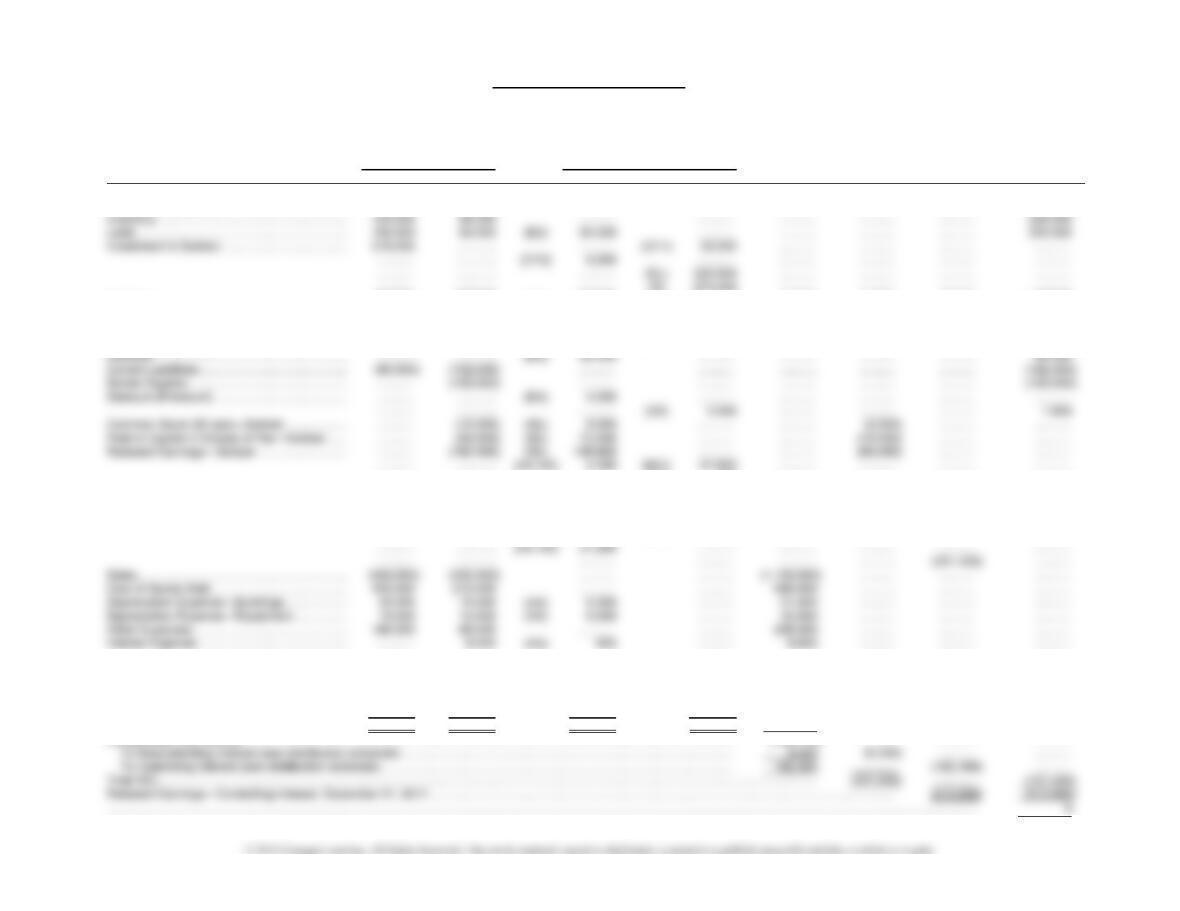

Current Assets ………………………………… 632,000 505,000 ………….. …………. …………. …..……… …………. 1,137,000

Detner …………………………………………. (1,200,000) ………….. ………….. …………. ….……… ………….. …………. (1,200,000)

Retained Earnings—Detner,

January 1, 2017 ……………………………. (1,255,000) ………….. (D1) 8,000 (CV) 144,000 …………. …..……… …………. ………….

…………. ………….. (A2) 10,000 …………. …………. ………….. …………. ………….

…………. ………….. (A3) 16,000 …………. …………. ………….. …………. ………….

…………. ………….. ………….. …………. …………. ………….. (1,365,000) ………….

Common Stock ($10 par)—Hardy ………. …………. (1,000,000) (EL) 800,000 …………. …………. (200,000) .………… ………….

Sales ……………………………………………… (905,000) (425,000) ………….. …………. (1,330,000) ………….. …………. ………….

Cost of Goods Sold ………………………….. 470,000 170,000 ………….. …………. 640,000 ………….. …………. ………….

Other Expenses ………………………………. 250,000 100,000 (A2) 6,250 …………. …………. ………….. …………. ………….

…………. ………….. (A3) 10,000 …………. …………. ………….. …………. ………….

Problem 3-8, Concluded

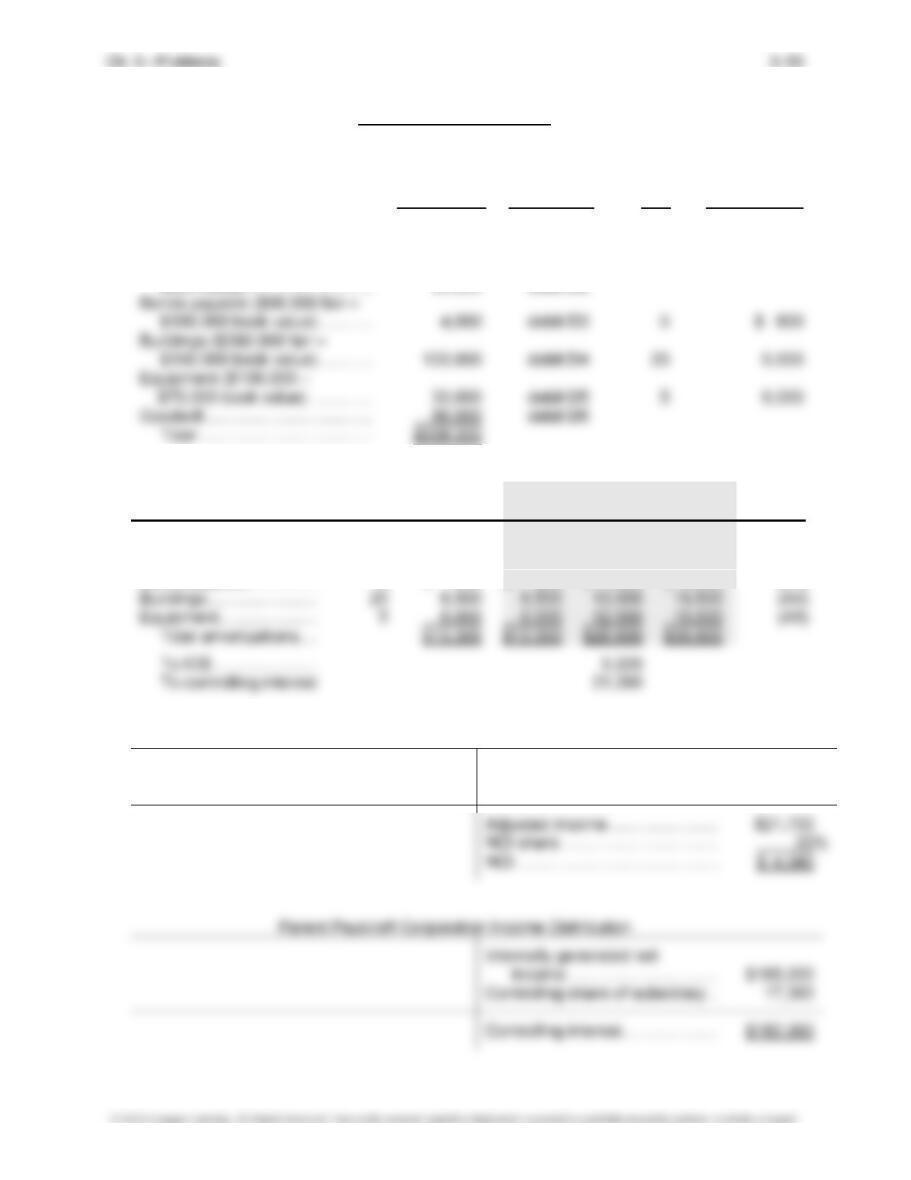

Eliminations and Adjustments:

(CV) Convert from cost to the equity method as of January 1, 2017. ($580,000

January 1, 2017 – $400,000 January 1, 2015 = $180,000 × 80% = $144,000.)

(D)/(NCI) Distribute the excess cost and adjust NCI as given by the determination and dis-

tribution of excess schedule:

(D1) Distribute inventory adjustment for units sold in prior years to retained earnings,

80% controlling.

(D3) Increase patents by $100,000.

(A1) No amortizations necessary.

(A3) Record $10,000 annual increase in patents depreciation for the current and past

two years.

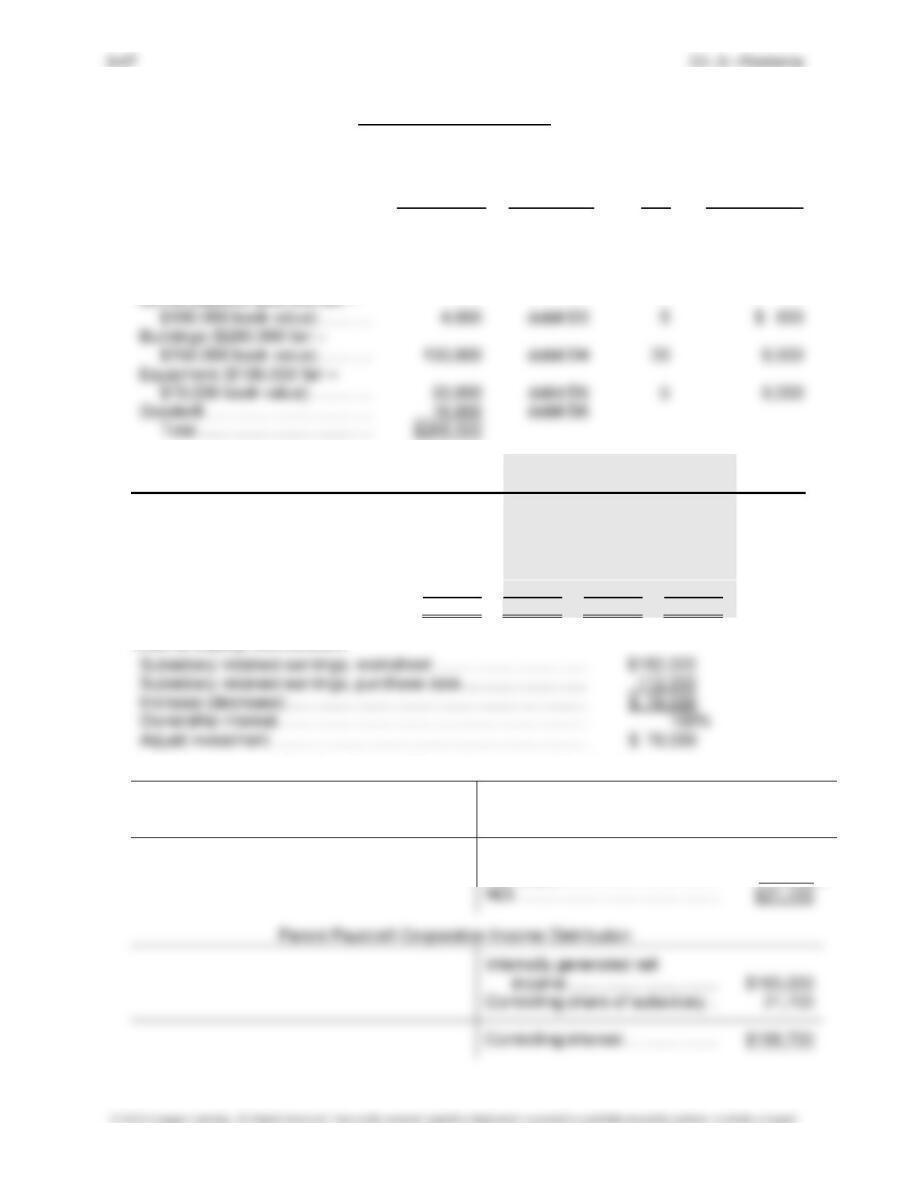

Subsidiary Hardy Company Income Distribution

Equipment depreciation ……. (A2) $ 6,250 Internally generated net

Patent depreciation ………….. (A3) 10,000 income ………………………… $155,000

Adjusted income ………………… $138,750

Parent Detner International Income Distribution

Internally generated net

income ………………………… $185,000

3-43 Ch. 3—Problems

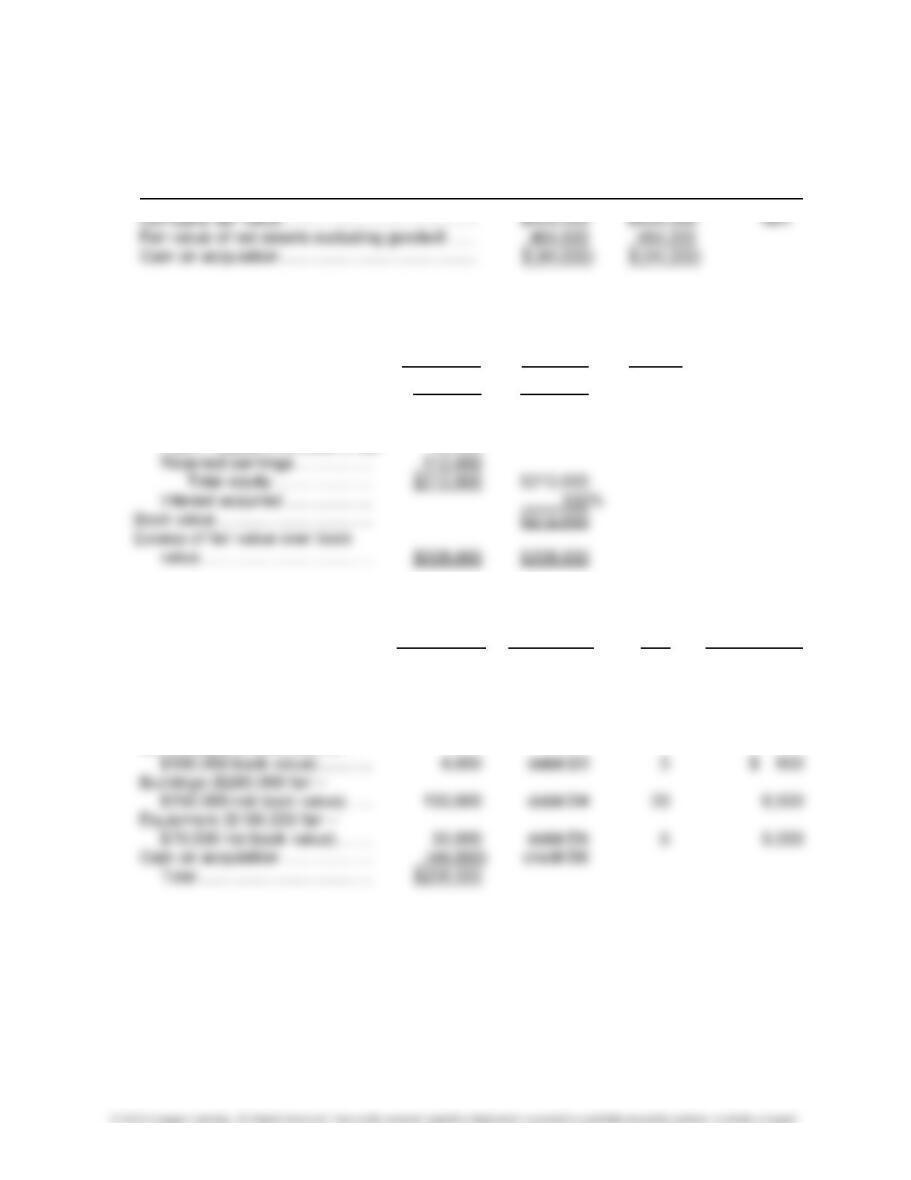

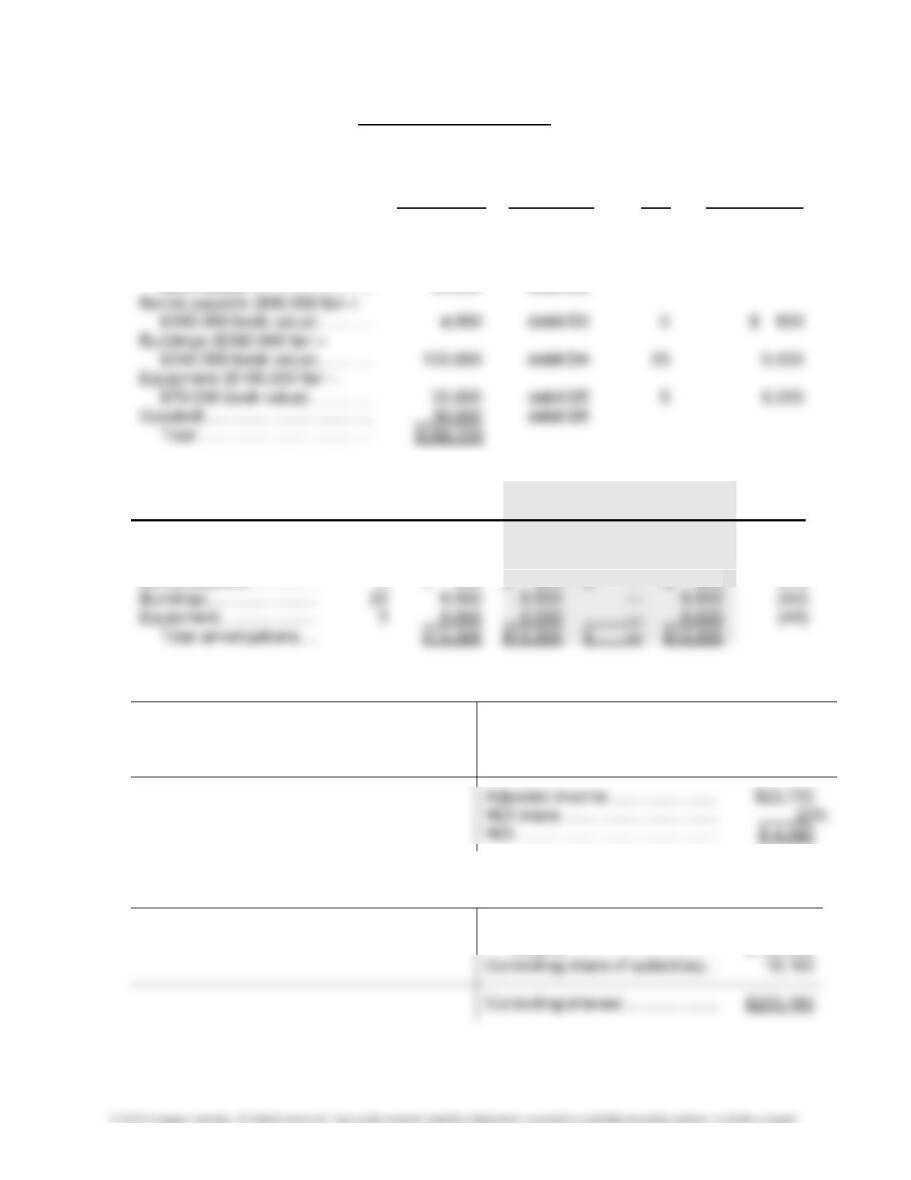

PROBLEM 3-9

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Price paid for investment …………. $420,000 $420,000 N/A

Less book value of interest acquired:

Common stock …………………. $ 10,000

Paid-in capital in excess of par 90,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($38,000 fair – $40,000

book value) ………………………. $ (2,000) credit D1

Land ($150,000 fair – $60,000

book value) ………………………. 90,000 debit D2

Bonds payable ($96,000 fair –

Ch. 3—Problems 3–44

Problem 3-9, Continued

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ (2,000) $ — $ (2,000) $ (2,000) (D1)

Subject to amortization:

Bonds payable …………… 5 $ 800 $ 800 $ 1,600 $ 2,400 (A3)

Subsidiary Switzer Corporation Income Distribution

Current-year amortizations ………… $13,300 Internally generated net

income …………………………… $35,000

Adjusted income …………………… $21,700

Problem 3-9, Continued

Paulcraft Corporation and Subsidiary Switzer Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulcraft Switzer Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 160,000 110,000 ……….. ……….. ……….. ……….. ……….. 270,000

Accounts Receivable ……………………………….. 90,000 55,000 ……….. ……….. ……….. ……..… ……….. 145,000

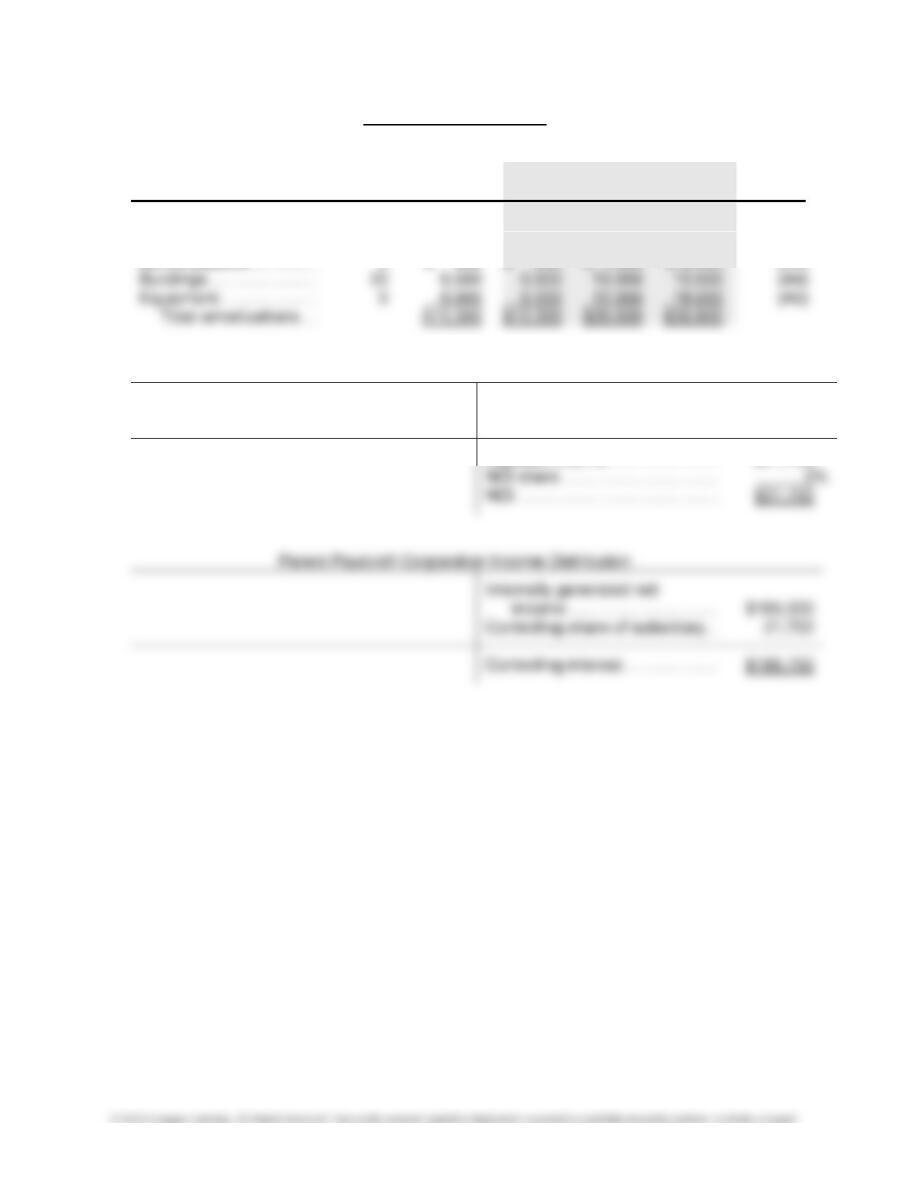

Buildings ………………………………………………… 800,000 250,000 (D4) 130,000 ……….. ……….. ……….. ……….. 1,180,000

Accumulated Depreciation ………………………… (220,000) (80,000) ……….. (A4) 19,500 ……….. ……….. ……….. (319,500)

Equipment ………………………………………………. 150,000 100,000 (D5) 30,000 ……….. ……….. ..……… ……….. 280,000

Accumulated Depreciation ………………………… (90,000) (72,000) ……….. (A5) 18,000 ……….. ……….. ……….. (180,000)

……….. ………… (A3–A5) 26,600 ……….. ……….. ……….. (404,400) ……………

Sales ……………………………………………………… (800,000) (350,000) ……….. ……….. (1,150,000) ……….. ……….. ……………

Cost of Goods Sold ………………………………….. 450,000 210,000 ……….. ……….. 660,000 ……….. ……….. ……………

Depreciation Expense—Building ……………….. 30,000 15,000 (A4) 6,500 ……….. 51,500 ……….. ……….. ……………

Depreciation Expense—Equipment ……………. 15,000 14,000 (A5) 6,000 ……….. 35,000 ……….. ……….. ..………….

Problem 3-9, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

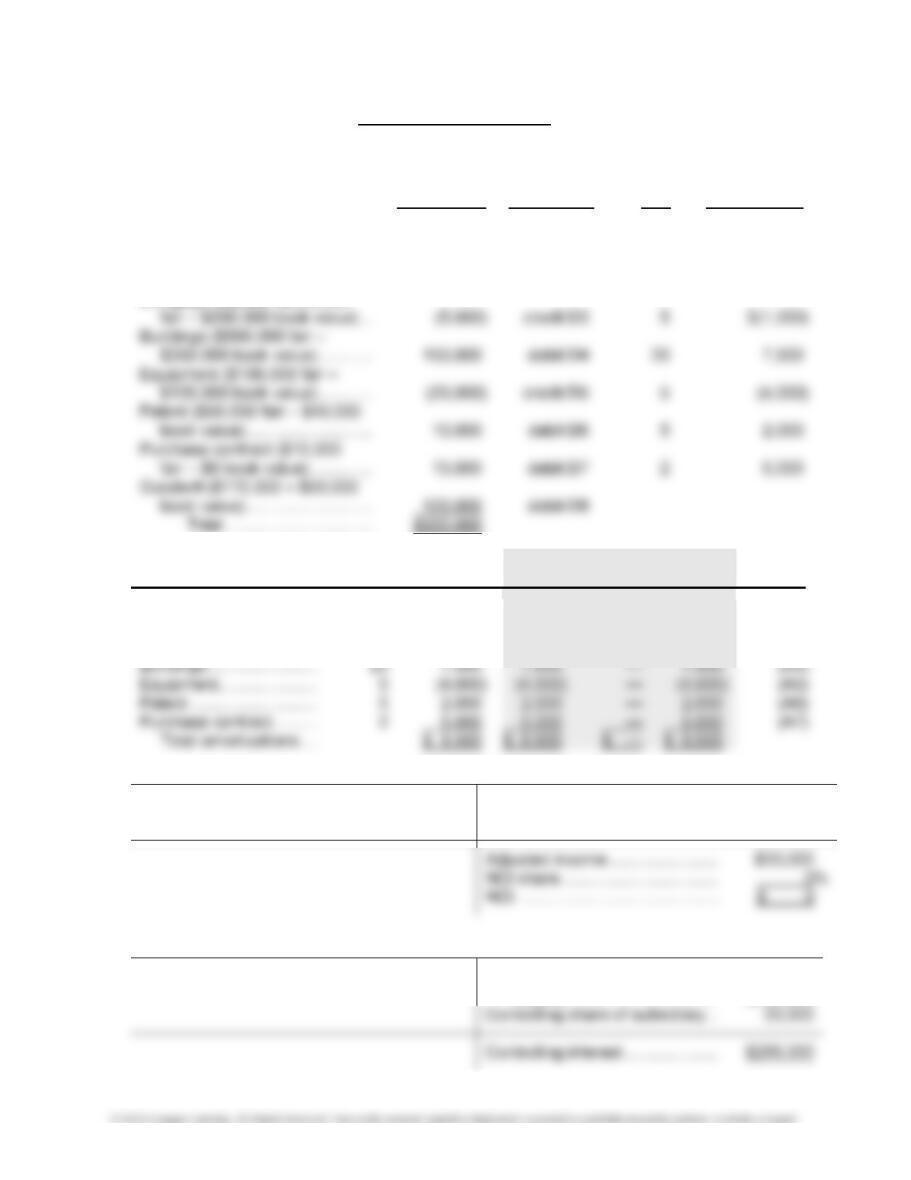

PROBLEM 3-10

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ……………………………………. $480,000 $480,000 N/A

Determination and Distribution of Excess Schedule

Company Parent

Implied Price NCI

Fair Value (100%)(0%) Value

Fair value of subsidiary …………………. $480,000 $480,000 N/A

Less book value of interest acquired:

Common stock ($1 par) ………. $ 10,000

Paid-in capital in excess of par 90,000

Problem 3-10, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($38,000 fair – $40,000

book value) ………………………. $ (2,000) credit D1

Land ($150,000 fair – $60,000

book value) ………………………. 90,000 debit D2

(2) Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ (2,000) $ — $ (2,000) $ (2,000) (D1)

Subject to amortization:

Bonds payable …………… 5 $ 800 $ 800 $ 1,600 $ 2,400 (A3)

Buildings …………………… 20 6,500 6,500 13,000 19,500 (A4)

Equipment…………………. 5 6,000 6,000 12,000 18,000 (A5)

Total amortizations …. $13,300 $13,300 $26,600 $39,900

Cost-to-Equity Conversion:

Subsidiary Switzer Corporation Income Distribution

Current-year amortizations ………… $13,300 Internally generated net

income …………………………… $35,000

Adjusted income …………………… $21,700

NCI share …………………………….. 0%

Problem 3-10, Continued

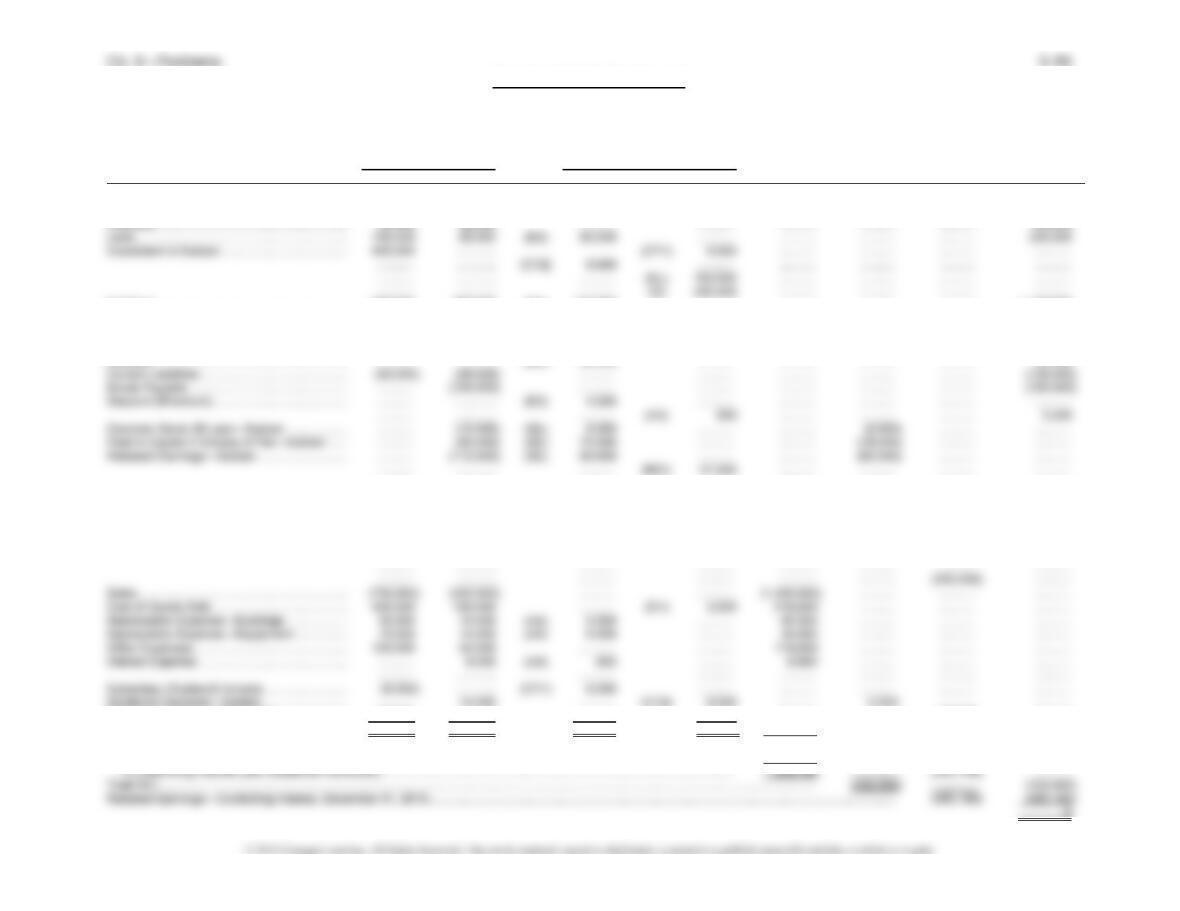

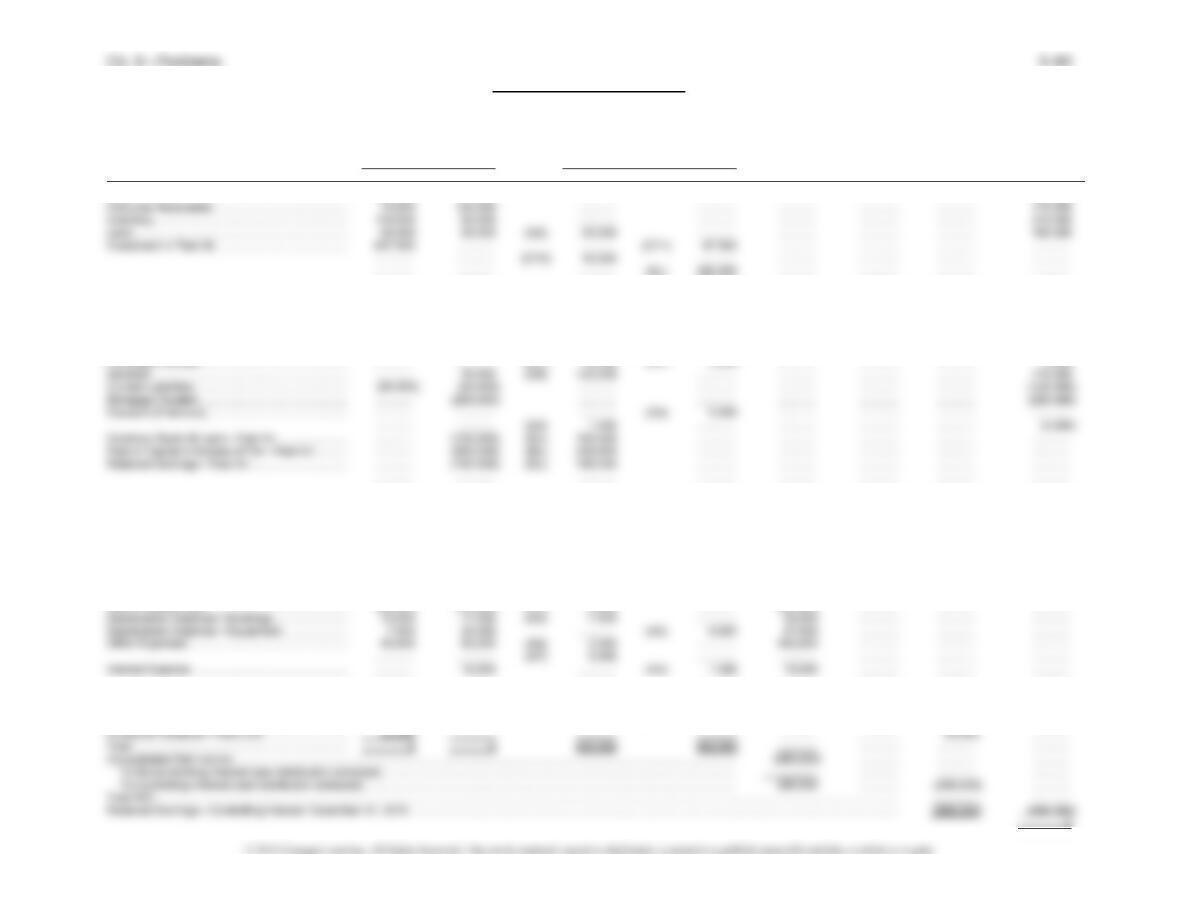

Paulcraft Corporation and Subsidiary Switzer Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulcraft Switzer Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 100,000 110,000 ……….. ……….. ……….. ……….. ……….. 210,000

Accounts Receivable ……………………………….. 90,000 55,000 ……….. ……….. ……….. ……..… ……….. 145,000

Inventory ………………………………………………… 120,000 86,000 ……….. ……….. ……….. ……….. ……….. 206,000

Land ………………………………………………………. 100,000 60,000 (D2) 90,000 ……….. ……….. ……….. ……….. 250,000

Investment in Switzer ……………………………….. 480,000 ………… (CV) 70,000 (CY1) 10,000 ……….. ……….. ……….. ……………

……….. ………… (CY2) 10,000 ……….. ……….. ……….. ……….. ……………

……….. ………… ……….. (EL) 282,000 ……….. ……….. ……….. ……………

……….. ………… ……….. (D) 268,000 ……….. ……….. ……….. ……………

Buildings ………………………………………………… 800,000 250,000 (D4) 130,000 ……….. ……….. ……….. ……….. 1,180,000

……….. ………… (A3–A5) 26,600 ……….. ……….. ……….. ……….. ………..

……….. ………… ……….. ……….. ……….. ……….. (360,400) ………..

Sales …………………………………………………….. (800,000) (350,000) ……….. ……….. (1,150,000) ……….. ……….. ………..

Cost of Goods Sold ………………………………….. 450,000 210,000 ……….. ……….. 660,000 ……….. ……….. ………..

Depreciation Expense—Buildings ………………. 30,000 15,000 (A4) 6,500 ……….. 51,500 ……….. ……….. ………..

Depreciation Expense—Equipment ……………. 15,000 14,000 (A5) 6,000 ……….. 35,000 ……….. ……….. ..………

Other Expenses ………………………………………. 140,000 68,000 ……….. ……….. 208,000 ……….. ……….. ………..

3-49 Ch. 3—Problems

Problem 3-10, Concluded

Eliminations and Adjustments:

(CV) Conversion to equity.

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

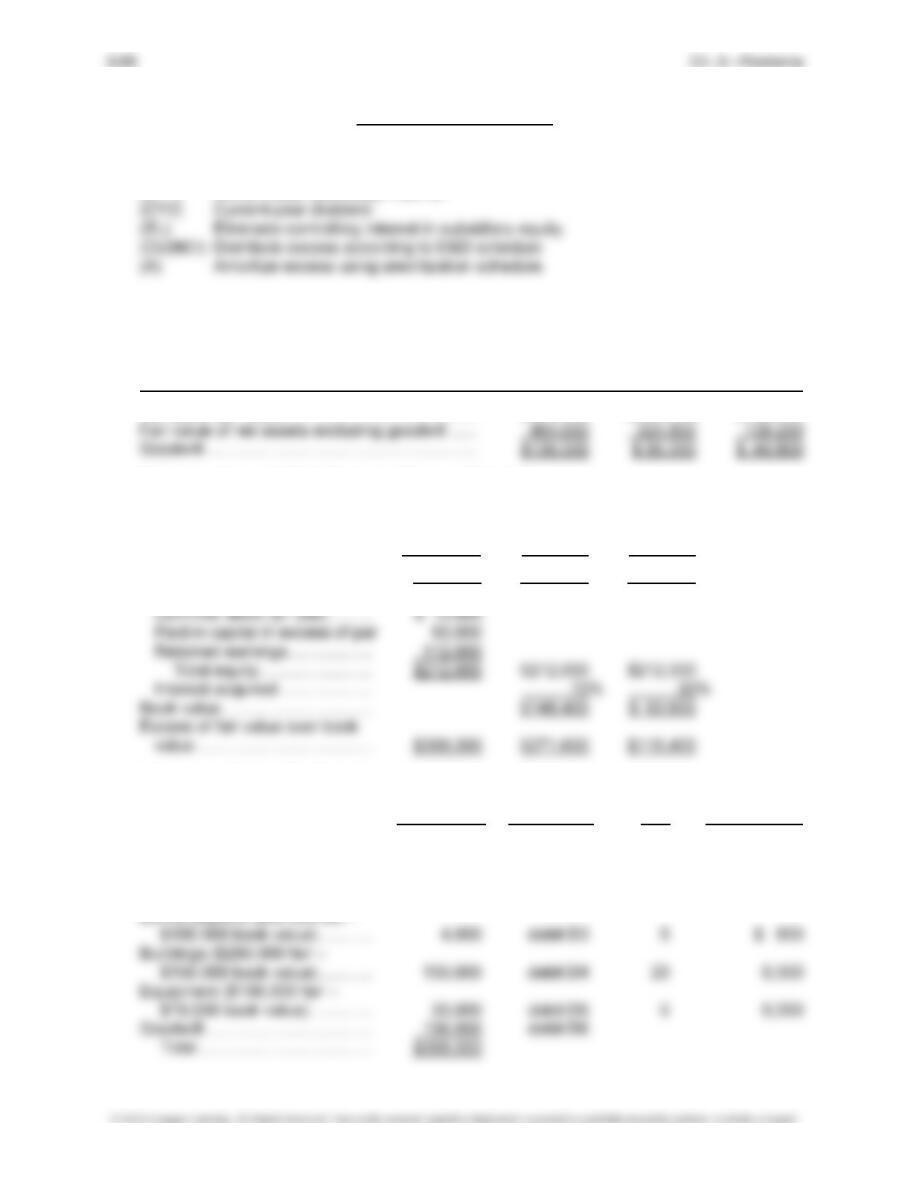

PROBLEM 3-11

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ……………………………………. $550,000 $440,000 $110,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $550,000 $440,000 $110,000

Less book value of interest acquired:

Common stock ($1 par) ………. $ 10,000

Problem 3-11, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($38,000 fair –

$40,000 book value) ………….. $ (2,000) credit D1 1

Land ($150,000 fair – $ 60,000

book value) ………………………. 90,000 debit D2

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ (2,000) $ — $ (2,000) $ (2,000) (D1)

Subject to amortization:

Bonds payable …………… 5 $ 800 $ 800 $ 1,600 $ 2,400 (A3)

Subsidiary Switzer Corporation Income Distribution

Current-year amortizations ………… $13,300 Internally generated net

income …………………………… $35,000

3-51 Ch. 3—Problems

Problem 3-11, Continued

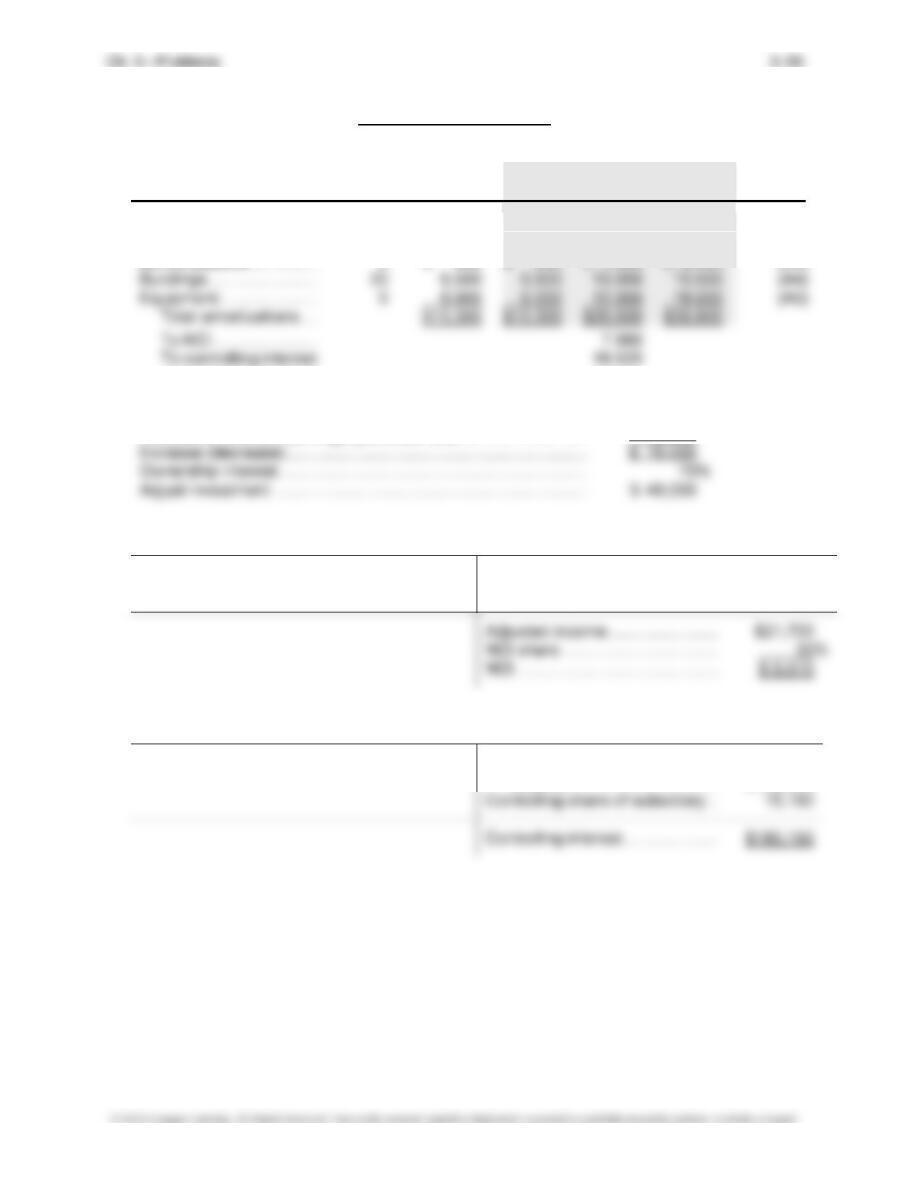

Paulcraft Corporation and Subsidiary Switzer Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulcraft Switzer Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 138,000 110,000 ……….. ……….. ……….. ……….. ……….. 248,000

Accounts Receivable ……………………………….. 90,000 55,000 ……….. ……….. ……….. ……..… ……….. 145,000

……….. ………… ……….. (D) 270,400 ……….. ……….. ……….. ………..

Buildings ………………………………………………… 800,000 250,000 (D4) 130,000 ……….. ……….. ……….. ……….. 1,180,000

Accumulated Depreciation ………………………… (220,000) (80,000) ……….. (A4) 19,500 ……….. ……….. ……….. (319,500)

Equipment ………………………………………………. 150,000 100,000 (D5) 30,000 ……….. ……….. ..……… ……….. 280,000

Accumulated Depreciation ………………………… (90,000) (72,000) ……….. (A5) 18,000 ……….. ……….. ……….. (180,000)

……….. ………… ……….. (D1) 400 ……….. ……….. ……….. ………..

Common Stock ($1 par)—Paulcraft ……………. (100,000) ………… ……….. ……….. ……….. ……..… ……….. (100,000)

Paid-In Capital in Excess of Par—Paulcraft …. (900,000) ………… ……….. ……….. ……….. ……….. ……….. (900,000)

Retained Earnings—Paulcraft ……………………. (371,000) ………… ……….. ……….. ……….. ……….. ……….. ………..

……….. ………… ……….. (D1) 1,600 ……….. ……….. ……….. ………..

……….. ………… ……….. ……….. ……….. ……….. ……….. ………..

……….. ………… ……….. ……….. ……….. ……….. ……….. ………..

Subsidiary (Dividend) Income ……………………. (28,000) ………… (CY1) 28,000 ……….. ……….. …..…… ……….. ………..

Dividends Declared—Switzer ……………………. ……….. 10,000 ……….. (CY2) 8,000 ……….. 2,000 ….……. ………..

Dividends Declared—Paulcraft ………………….. 20,000 ………… ……….. ……….. ……….. ……….. 20,000 ………..

Total ………………………………………………………. 0 0 641,500 641,500 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (186,700) ……….. ……….. ………..

Problem 3-11, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

PROBLEM 3-12

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ……………………………………. $500,000 $400,000 $100,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $500,000 $400,000 $100,000

Less book value of interest acquired:

Common stock ($1 par) ………. $ 10,000

Paid-in capital in excess of par 90,000

3-53 Ch. 3—Problems

Problem 3-12, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($38,000 fair –

$40,000 book value) ………….. $ (2,000) credit D1 1

Land ($150,000 fair – $60,000

book value) ………………………. 90,000 debit D2

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ (2,000) $ (2,000) $ — $(2,000) (D1)

Subject to amortization:

Bonds payable …………… 5 $ 800 $ 800 $ — $ 800 (A3)

Subsidiary Switzer Corporation Income Distribution

Current-year amortizations ………… $13,300 Internally generated net

income …………………………… $34,000

Inventory adjustment …………….. 2,000

Parent Paulcraft Corporation Income Distribution

Internally generated net

income …………………………… $185,000

Problem 3-12, Continued

Paulcraft Corporation and Subsidiary Switzer Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulcraft Switzer Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 178,000 81,000 ……….. ……….. ……….. ……….. ……….. 259,000

Accounts Receivable ……………………………….. 80,000 35,000 ……….. ……….. ……….. ……..… ……….. 115,000

Buildings ………………………………………………… 800,000 200,000 (D4) 130,000 ……….. ……….. ……….. ……….. 1,130,000

Accumulated Depreciation ………………………… (200,000) (60,000) ……….. (A4) 6,500 ……….. ……….. ……….. (266,500)

Equipment ………………………………………………. 150,000 100,000 (D5) 30,000 ……….. ……….. ..……… ……….. 280,000

Accumulated Depreciation ………………………… (75,000) (44,000) ……….. (A5) 6,000 ……….. ……….. ……….. (125,000)

Goodwill …………………………………………………. ……….. ………… (D6) 36,000 ……….. ..……… ……….. ……….. 36,000

……….. ………… ……….. ……….. ……….. ……….. ……….. ………..

……….. ………… ……….. ……….. ……….. ……….. ……….. ………..

Common Stock ($1 par)—Paulcraft ……………. (100,000) ………… ……….. ……….. ……….. ……..… ……….. (100,000)

Paid-In Capital in Excess of Par—Paulcraft …. (900,000) ………… ……….. ……….. ……….. ……….. ……….. (900,000)

Retained Earnings—Paulcraft ……………………. (300,000) ………… ……….. ……….. ……….. ..……… ………..

……….. ………… ……….. ……….. ……….. ……….. ……….. ………..

Dividends Declared—Paulcraft ………………….. 20,000 ………… ……….. ……… ……….. ……….. 20,000 ………..

Total ………………………………………………………. 0 0 488,900 488,900 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (207,700) ……….. ……….. ………..

To Noncontrolling Interest (see distribution schedule) ……………………………………………………………..………………………… 4,540 (4,540) ……….. ………..

Problem 3-12, Concluded

Eliminations and Adjustments:

(CV) Conversion to equity

(CY1) Current-year subsidiary income.

PROBLEM 3-13

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (70%) (30%)

Company fair value ……………………………………. $600,000 $420,000 $180,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (70%) (30%)

Fair value of subsidiary ………….. $600,000 $420,000 $180,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($38,000 fair –

$40,000 book value) ………….. $ (2,000) credit D1 1

Land ($150,000 fair – $60,000

book value) ………………………. 90,000 debit D2

Problem 3-13, Continued

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ (2,000) $ — $ (2,000) $ (2,000) (D1)

Subject to amortization:

Bonds payable …………… 5 $ 800 $ 800 $ 1,600 $ 2,400 (A3)

Cost-to-Equity Conversion:

Subsidiary retained earnings, worksheet ……………………………. $182,000

Subsidiary retained earnings, purchase date ……………………… 112,000

Subsidiary Switzer Corporation Income Distribution

Current-year amortizations ………… $13,300 Internally generated net

income …………………………… $35,000

Parent Paulcraft Corporation Income Distribution

Internally generated net

income …………………………… $165,000

3-57 Ch. 3—Problems

Problem 3-13, Continued

Paulcraft Corporation and Subsidiary Switzer Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulcraft Switzer Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 157,000 110,000 ……….. ……….. ……….. ……….. …………… 267,000

Accounts Receivable ……………………………….. 90,000 55,000 ……….. ……….. ……….. ……..… …………… 145,000

Buildings ………………………………………………… 800,000 250,000 (D4) 130,000 ……….. ……….. ……….. …………… 1,180,000

Accumulated Depreciation ………………………… (220,000) (80,000) ……….. (A4) 19,500 ……….. ……….. …………… (319,500)

Equipment ………………………………………………. 150,000 100,000 (D5) 30,000 ……….. ……….. ..……… …………… 280,000

Accumulated Depreciation ………………………… (90,000) (72,000) ……….. (A5) 18,000 ……….. ……….. …………… (180,000)

Common Stock ($1 par)—Paulcraft ……………. (100,000) ………… ……….. ……….. ……….. ……..… …………… (100,000)

Paid-In Capital in Excess of Par—Paulcraft …. (900,000) ………… ……….. ……….. ……….. ……….. …………… (900,000)

Retained Earnings—Paulcraft ……………………. (315,000) ………… ……….. (CV) 49,000 ……….. ……….. …………… ………..

……….. ………… ……….. (D1) 1,400 ……….. ……….. …………… ………..

Dividends Declared—Paulcraft ………………….. 20,000 ………… ……….. ……….. ……….. ……….. 20,000 ………..

Total ………………………………………………………. 0 0 690,300 690,300 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (186,700) ……….. ……….. ………..

To Noncontrolling Interest (see distribution schedule) ……………………………………………………………..………………………… 6,510 (6,510) ……….. ………..

Problem 3-13, Concluded

Eliminations and Adjustments:

(CV) Conversion to equity.

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

PROBLEM 3-14

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ……………………………………. $800,000 $800,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary ………….. $800,000 $800,000 N/A

Less book value of interest acquired:

Common stock ($1 par) ………. $100,000

Paid-in capital in excess of par 200,000

3-59 Ch. 3—Problems

Problem 3-14, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($65,000 fair –

$60,000 book value) ………….. $ 5,000 debit D1

Land ($100,000 fair – $50,000

book value) ………………………. 50,000 debit D2

Mortgage payable ($205,000

(2) Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ 5,000 $ 5,000 $ — $ 5,000 (D1)

Subject to amortization:

Mortgage payable ………. 5 $ (1,000) $ (1,000) $ — $ (1,000) (A3)

Subsidiary Fast Air Company Income Distribution

Inventory adjustment ………………… $5,000 Internally generated net

Current-year amortizations ………… 9,500 income …………………………… $47,500

Parent Fast Cool Company Income Distribution

Internally generated net

income …………………………… $253,000

Problem 3-14, Continued

Fast Cool Company and Subsidiary Fast Air Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Fast Cool Fast Air Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………….. 147,000 37,000 ………… ………… ….…….. ………… ………… 184,000

………… ………… ………… (D) 320,000 ………… ………… ………… …………

Buildings …………………………………………………….. 1,200,000 400,000 (D4) 150,000 ………… ………… ………… ………… 1,750,000

Accumulated Depreciation …………………………….. (176,000) (67,500) ………… (A4) 7,500 ………… ………… ………… (251,000)

Equipment ………………………………………………….. 140,000 150,000 ………… (D5) 20,000 ………... ………… ………… 270,000

Accumulated Depreciation …………………………….. (68,000) (54,000) (A5) 4,000 ………… ………… ………… ………… (118,000)

Patent ………………………………………………………… ………… 32,000 (D6) 10,000 (A6) 2,000 …….….. ………… ………… 40,000

Purchase Contract ……………………………………….. ………… ………… (D7) 10,000 (A7) 5,000 …….….. ………… ………… 5,000

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

Common Stock ($1 par)—Fast Cool ………………. (100,000) ………… ………… ………… ………… .……….. ………… (100,000)

Paid-In Capital in Excess of Par—Fast Cool ……. (1,500,000) ………… ………… ………… ………… ………… ………… (1,500,000)

Retained Earnings—Fast Cool ………………………. (400,000) ………… ………… ………… ………... ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… (400,000) …………

Sales …………………………………………………………. (700,000) (400,000) ………… ………… (1,100,000) ………… ………… …………

Cost of Goods Sold ……………………………………… 380,000 210,000 (D1) 5,000 ………… 595,000 ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

Subsidiary (Dividend) Income ………………………… (47,500) ………… (CY1) 47,500 ………… ………… ………… ………… …………

Dividends Declared—Fast Air ……………………….. ………… 10,000 ………… (CY2) 10,000 ………… ..………. ………… …………