Primary financial statements Purpose is to report

TRANSACTIONS AND EVENTS

Practice of bookkeeping

ACCOUNTING RECORDS

Rules of measurement and disclosure

FINANCIAL STATEMENTS

Financial Accounting

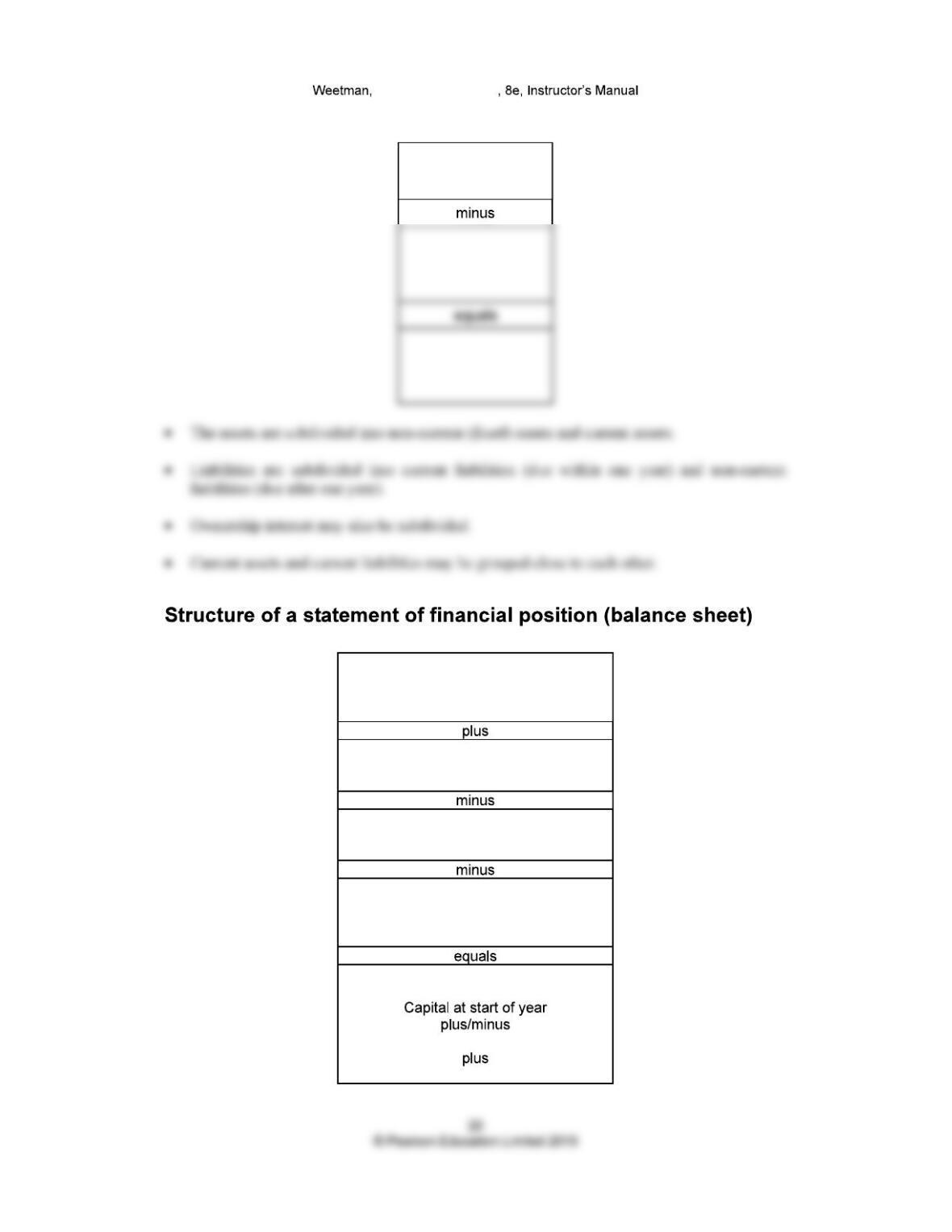

Horizontally, it is as follows:

The following list of assets and liabilities of P. Masons legal practice was prepared from the

Financial Accounting

List of assets and liabilities at 30 September Year 5: P. Mason s legal practice

Statement of financial position (balance sheet) at 30 September Year 5

Financial Accounting

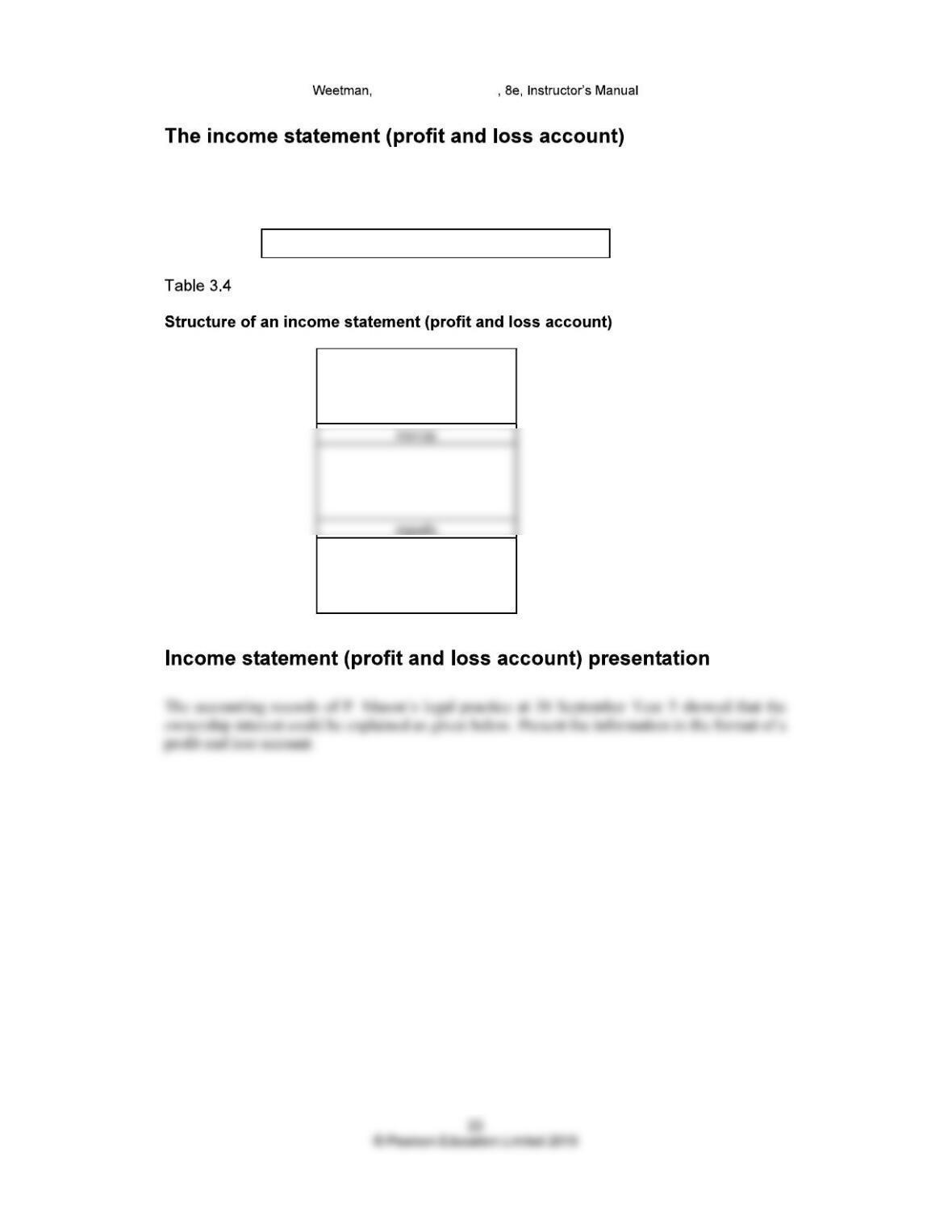

The income statement (profit and loss account) reflects that part of the accounting equation that

defines profit.

Profit equals revenue minus expenses

Financial Accounting

The accounting records of P. Mason s legal practice

at 30 September Year 5 showed that the ownership

interest could be explained as follows

(using brackets to show negative items):

P. Masons legal practice

Income statement (profit and loss account) for the

month of September

Increases in claim

Financial Accounting

Liquidity is measured by the cash and near-cash assets and the change in those assets; hence, a

financial statement that explains cash flows should be of general interest to user groups.

Cash flow equals cash inflows to the enterprise minus cash outflows from the enterprise.

The statement of cash flows will appear in a vertical form:

Financial Accounting

Structure of a statement of cash flows

Operating activities

minus

plus

Investing activities

minus

plus

Financial Accounting

P. Mason legal practice

Statement of cash flows for the month of September Year 5

Year 5

Cash received

Financial Accounting

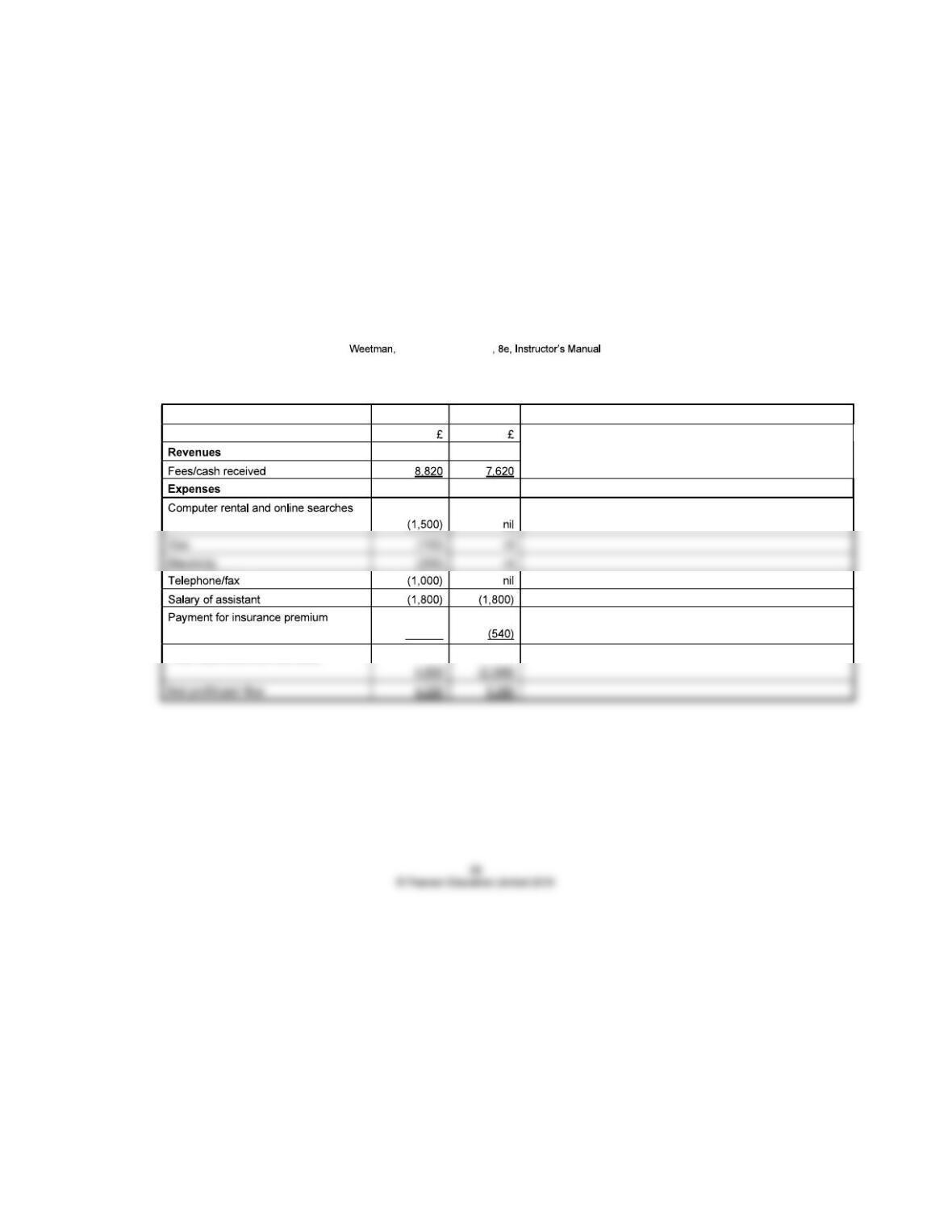

P. Masons legal practice

Profit Cash flow EXPLANATION

Total expenses/total cash paid

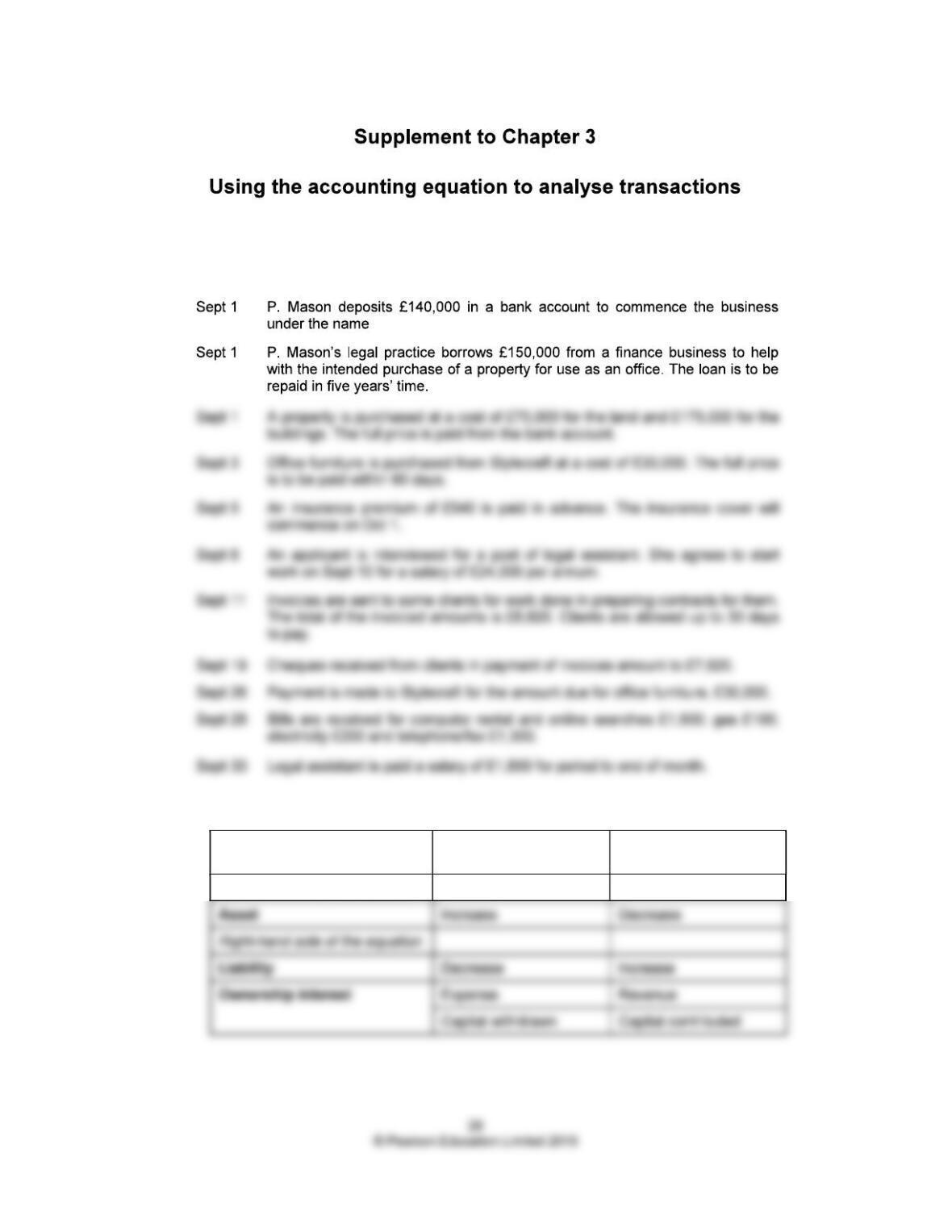

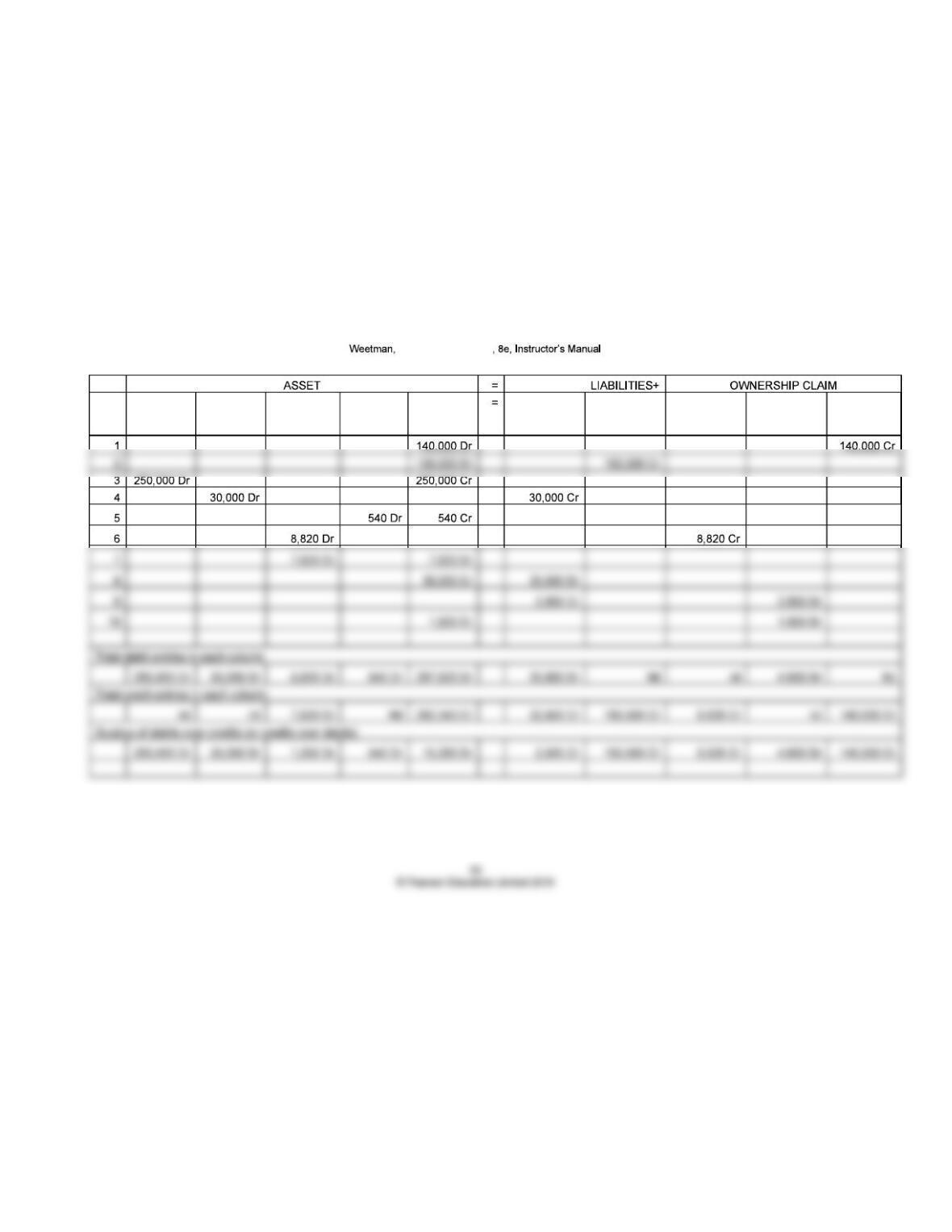

The list of transactions is as follows:

P Masons legal practice.

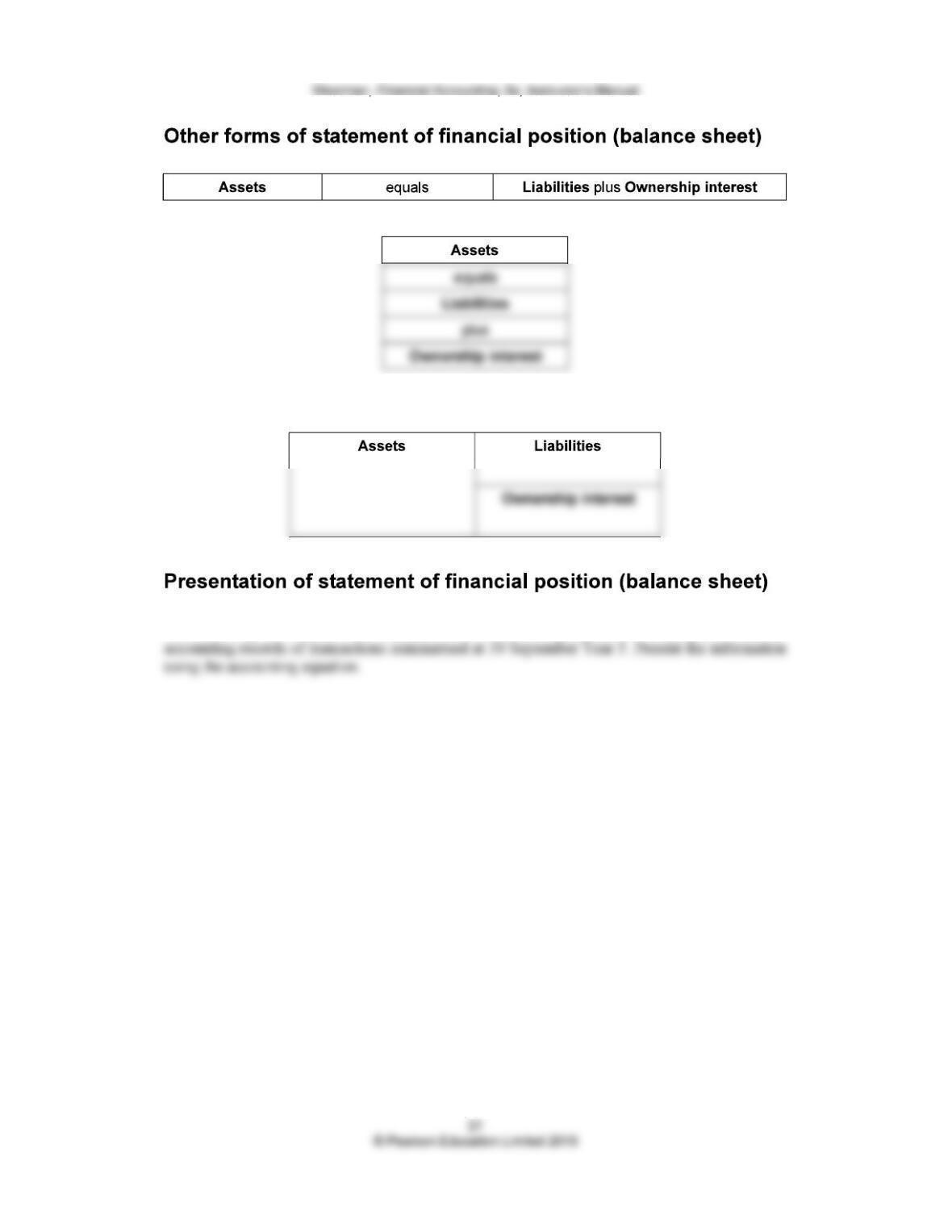

Assets equal to Liabilities plus Ownership interest

Debit entries in a

ledger account

Credit entries in a

ledger account

Left-hand side of the equation

Financial Accounting

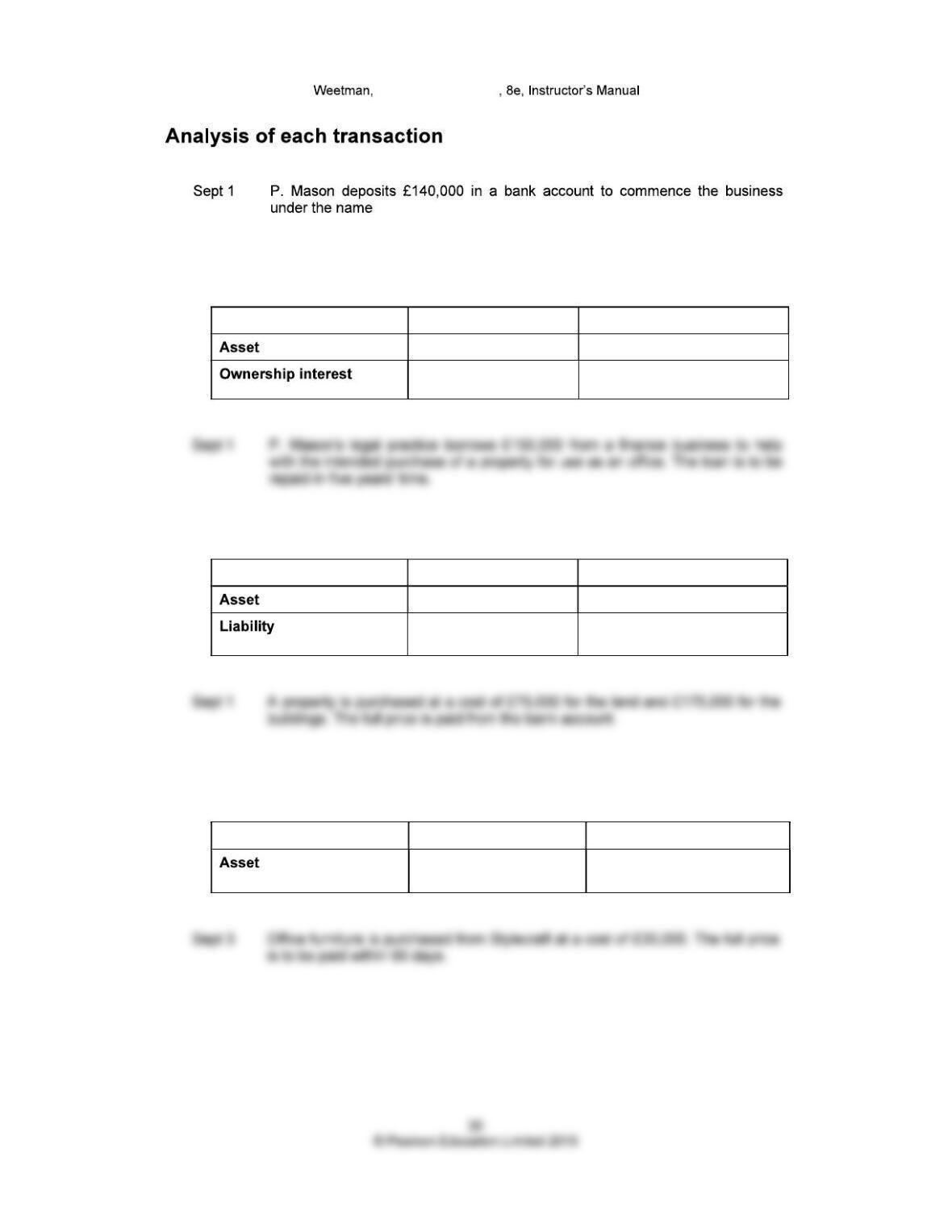

P. Masons legal practice.

The business acquires an asset (cash in the bank) and an ownership interest is created

through contribution of capital.

Transaction number: 1 Debit Credit

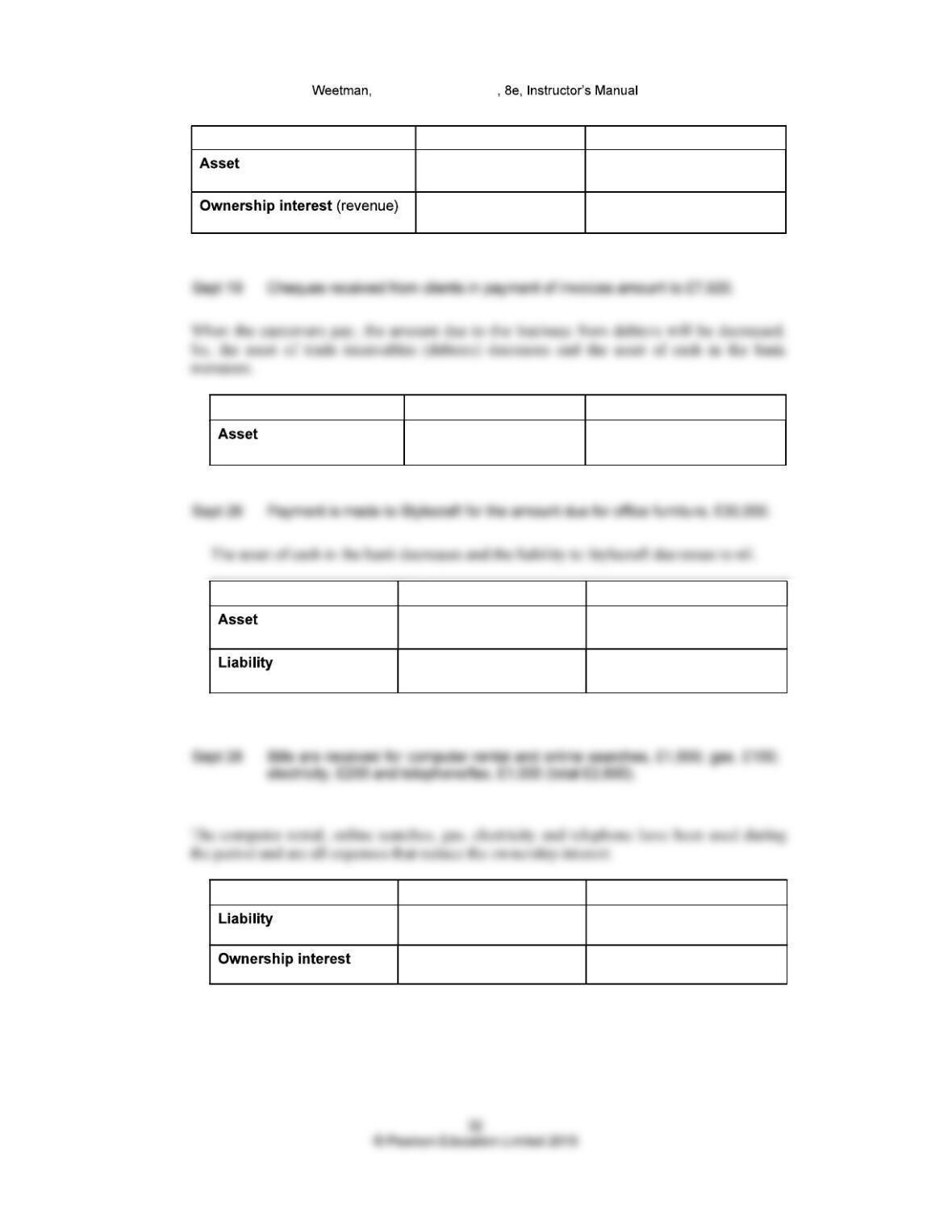

The business acquires an asset of cash and a long-term liability is created.

Transaction number: 2 Debit Credit

The business acquires an asset of land and buildings (£250,000 in total) and the asset of

cash in the bank is reduced.

Transaction number: 3

The business acquires an asset of furniture and also acquires a liability to pay the supplier,

Stylecraft. The liability is called a trade payable (creditor).

Financial Accounting

Transaction number: 4 Debit Credit

The business acquires an asset of prepaid insurance (the benefit of cover exists in the future)

and the asset of cash at bank is reduced.

Transaction number: 5 Debit Credit

The successful outcome of the interview is an event and there is an expected future benefit

from employing the new legal assistant. The employee will be controlled by the

organisation through a contract of employment. The organisation has a commitment to pay

her the agreed salary. It could be argued that the offer of employment, and acceptance of

Financial Accounting

Transaction number: 6 Debit Credit

Transaction number: 7 Debit Credit

Transaction number: 8 Debit Credit

Transaction number: 9 Debit Credit

Financial Accounting

The asset of cash at bank decreases and the salary paid to the legal assistant is an expense of the

month.

Transaction number: 10 Debit Credit

One line for each transaction.

Financial Accounting

No Land and

buildings

Office

furniture

Trade

receivables

Pre-

payments

Cash at

bank

= Trade

payables

Bank loan Revenue Expenses Owners

capital

contributed

Financial Accounting

No Land and

buildings

Office

furniture

Trade

receivables

Pre-

payments

Cash at

bank

Trade

payables

Bank loan Revenue Expenses Owners

capital

contributed

Financial Accounting

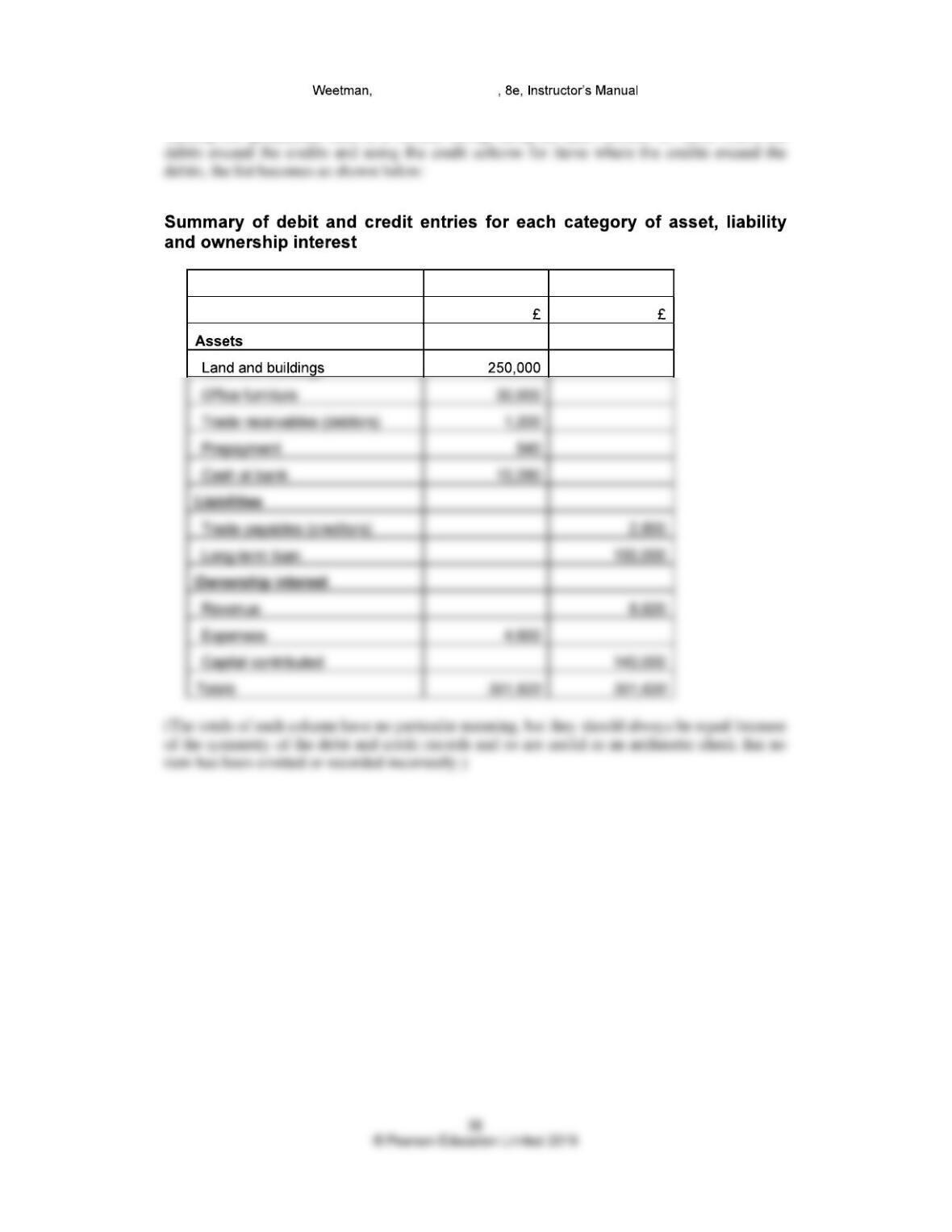

Turning the spreadsheet back to a vertical listing, using the debit column for items where the

Debit Credit