CHAPTER 3

UNDERSTANDING THE ISSUES

1. (a) Subsidiary Income = $40,000.

Investment in Subsidiary ($500,000 +

Investment in Subsidiary ($500,000 +

$33,000 – $5,000) = $528,000.

(c) Subsidiary Income = $0.

2. Date alignment means adjusting the in-

vestment account to reflect the same date

as the subsidiary equity accounts so that

their balances reflect the same point in

time.

(a) Simple equity method—The subsidi–

ary’s equity accounts reflect beginning–

of-year balances, yet the investment

account reflects an end-of-year bal-

ance. During the consolidation process,

(b) Sophisticated equity method—The

subsidiary’s equity accounts reflect

beginning-of-year balances, yet the in-

vestment account reflects an end-of-

year balance. During the consolidation

(c) Cost method—The subsidiary’s equity

accounts reflect beginning-of-year

balances, yet the investment account

reflects the balance on the date of

3. The noncontrolling share of consolidated

net income is the outside ownership share

of the subsidiary’s internally generated in-

come as adjusted for amortizations created

by fair value adjustments on the acquisition

date. The NCI share of consolidated net in-

4. The $80,000 excess attributed to the con-

trolling interest means that the patent is ad-

(a) Parent net income for 2015 . $140,000

Subsidiary net income in

2015 ($60,000 × ½ year) .. 30,000

Amortization of excess for

2015 ($100,000 ÷ 10 ×

½ year) ………………………… (5,000)

Consolidated net income ….. $165,000

(b) NCI share of net income = 1/2 ×

($60,000 – $10,000) × 20% = $5,000.

5. In 2015, consolidated net income would be

by $12,000 [($160,000 – $100,000) ÷ 5

years]. In 2016, consolidated net income

would be reduced by $12,000 as a result of

the equipment. The equipment would in-

crease depreciation expense by $12,000

[($160,000 – $100,000) ÷ 5 years].

generated income. The NCI is shown, in

total, as a subdivision of equity on the con-

solidated balance sheet.

7. Consolidated net income could exceed the

The amortization of this markdown would

decrease expense; therefore, consolidated

net income is increased.

Ch. 3—Exercises 3–2

EXERCISES

EXERCISE 3-1

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $525,000* $420,000 $105,000

Less book value of interest acquired:

Common stock ($5 par) …………… $ 50,000

Paid-in capital in excess of par … 100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Equipment ………………………………….. $ 40,000 debit D1 5 $8,000

(a) Event Simple Equity Method

2015

Subsidiary income of Investment in Huron Company ………. 40,000

$50,000 reported to parent Subsidiary Income ………………….. 40,000

Dividends of $10,000 paid Cash ………………………………………….. 8,000

3-3 Ch. 3—Exercises

Exercise 3-1, Concluded

(b) Event Sophisticated Equity Method

2015

Subsidiary income of Investment in Huron Company ………. 33,600

($50,000 – $8,000 Subsidiary Income ………………….. 33,600

amortization) × 80%

reported to parent

(c)

Event Cost Method

2015

Subsidiary income of No entry

$50,000 reported to parent

Dividends of $10,000 paid Cash ………………………………………….. 8,000

by Huron Dividend Income ……………………. 8,000

EXERCISE 3-2

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (75%) (25%)

Fair value of subsidiary ………………… $616,667* $462,500 $154,167

Less book value of interest acquired:

Common stock ($5 par) …………… $ 50,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($50,000 fair – $40,000

book value)……………………………. $ 10,000 debit D1

Buildings and equipment

(a) Simple equity ……………………………………………………………………………. $462,500

+ (75% × Increase in Retained Earnings of $78,000*) ……………………. 58,500**

Balance ……………………………………………………………………………………. $521,000

(b) Sophisticated equity…………………………………………………………………… $462,500

+ (75% × Increase in Retained Earnings of $78,000*) ……………………. 58,500**

– 2014 Amortization of Excess

75% × ($10,000 Inventory + $5,000 Buildings and Equipment +

EXERCISE 3-3

(1) Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $375,000* $300,000 $ 75,000

Less book value of interest acquired:

Common stock ($10 par) …….. $100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Fixed assets…………………………. $ 50,000 debit D1 10 $5,000

(2) (CY1) Subsidiary Income …………………………………………………………. 20,000

Investment in Sargent Company ………………………………… 20,000

To eliminate parent’s share of subsidiary earnings

for the current year.

(CY2) Investment in Sargent Company ($5,000 × 80%) ………………. 4,000

Dividends Declared ………………………………………………….. 4,000

To eliminate parent’s share of dividends for the

current year.

(EL) Common Stock—Sargent ($100,000 × 80%) …………………….. 80,000

Retained Earnings—Sargent ($150,000 × 80%) ………………… 120,000

Exercise 3–3, Continued

(3) Parker Company and Sargent Company

Consolidated Income Statement

For Year Ended December 31, 2015

Sales …………………………………………………………………………………………………. $250,000

Subsidiary Sargent Company Income Distribution

Depreciation adjustment ……. $5,000 Internally generated net

income …………………………… $25,000

Adjusted income …………………… $20,000

NCI share …………………………….. × 20%

NCI ……………………………………… $ 4,000

(4) Parker Company and Subsidiary Sargent Company

Consolidated Statement of Retained Earnings

For the Year Ended December 31, 2015

Noncontrolling Controlling

Interest

Retained Earnings

Retained earnings, January 1, 2015 …………….. $30,000 $200,000

3-7 Ch. 3—Exercises

Exercise 3–3, Concluded

(5) Parker Company and Sargent Company

Consolidated Balance Sheet

December 31, 2015

Assets

Current assets ……………………………………………………………….. $140,000

Depreciable fixed assets ………………………………………………….. $650,000a

Less accumulated depreciation ………………………………………… 131,000b 519,000

Liabilities and Stockholders’ Equity

Current liabilities …………………………………………………………….. $100,000

Stockholders’ equity:

Controlling interest:

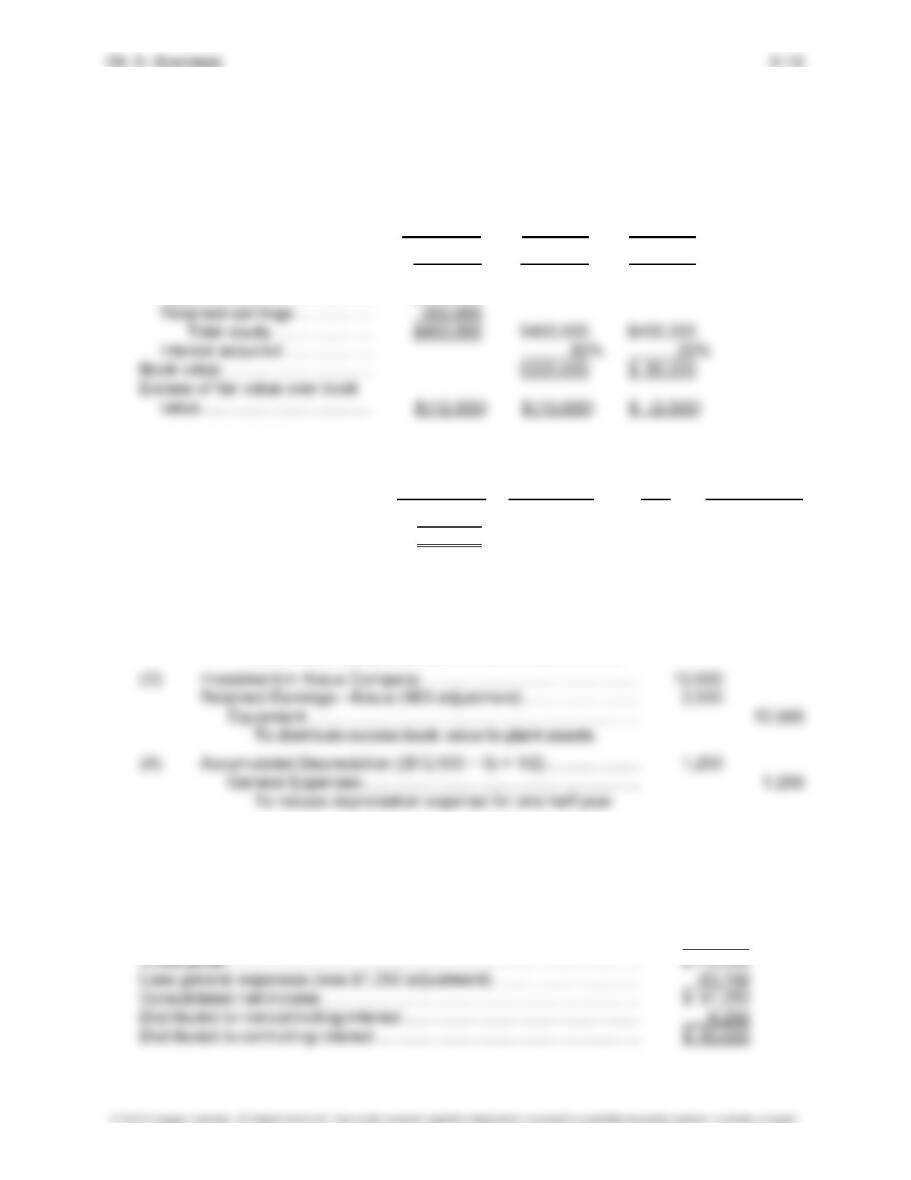

EXERCISE 3-4

(1) (CY1) Subsidiary Income …………………………………………………………. 12,000

Investment in Sargent Company ………………………………… 12,000

To eliminate parent’s share of subsidiary earnings

for the current year.

(CY2) Investment in Sargent Company ……………………………………… 8,000

Exercise 3–4, Concluded

(A) Depreciation Expense ……………………………………………………. 5,000

Retained Earnings—Parker (80% × $5,000) ……………………… 4,000

(2) Parker Company and Sargent Company

Consolidated Income Statement

For Year Ended December 31, 2016

Sales …………………………………………………………………………………………………. $300,000

Less expenses (add $5,000 adjustment) ………………………………………………… 250,000

Subsidiary Sargent Company Income Distribution

Depreciation adjustment …… (A) 5,000 Internally generated net

income ………………………………. $15,000

Adjusted income ………………………. $10,000

Parent Parker Company Income Distribution

Internally generated net

income ………………………………. $40,000

EXERCISE 3-5

(1) Same as Exercise 3, part (1).

(2) (CY1) Subsidiary Income $20,000 – $4,000 amortization) ……………. 16,000

Investment in Sargent Company ………………………………… 16,000

(CY2) Investment in Sargent Company ……………………………………… 4,000

(3) Same as Exercise 3, part (3).

(5) Same as Exercise 3, part (5).

EXERCISE 3-6

(1) (CY1) Subsidiary Income …………………………………………………………. 8,000

Investment in Sargent Company ………………………………… 8,000

(CY2) Investment in Sargent Company ……………………………………… 8,000

Dividends Declared ………………………………………………….. 8,000

(A) Depreciation Expense ……………………………………………………. 5,000

Accumulated Depreciation …………………………………………. 5,000

Ch. 3—Exercises 3–10

EXERCISE 3-7

(1) Same as Exercise 3, part (1).

(2) (CY2) Dividend Income ……………………………………………………………. 4,000

Dividends Declared ………………………………………………….. 4,000

To eliminate parent’s share of subsidiary dividends

for the current year.

(EL) Common Stock—Sargent ……………………………………………….. 80,000

Retained Earnings—Sargent …………………………………………… 120,000

year Sargent equity balances.

(D) Depreciable Fixed Assets ……………………………………………….. 50,000

Goodwill ……………………………………………………………………….. 75,000

Investment in Sargent Company ………………………………… 100,000

(A) Depreciation Expense ……………………………………………………. 5,000

Accumulated Depreciation …………………………………………. 5,000

To amortize excess for the current year.

(4) Same as Exercise 3, part (4).

3-11 Ch. 3—Exercises

EXERCISE 3-8

(1) (CV) Investment in Sargent Company ……………………………………… 16,000

Retained Earnings—Parker ……………………………………….. 16,000

Convert from cost to equity method by adding to

investment account parent’s share of subsidiary

equity increase. [80% × ($170,000 – $150,000)]

(CY2) Dividend Income ……………………………………………………………. 8,000

Dividends Declared ………………………………………………….. 8,000

To eliminate parent’s share of subsidiary dividends

for the current year.

(EL) Common Stock—Sargent ……………………………………………….. 80,000

Retained Earnings—Sargent …………………………………………… 136,000

(D) Depreciable Fixed Assets ……………………………………………….. 50,000

Goodwill ……………………………………………………………………….. 75,000

Investment in Sargent Company ………………………………… 100,000

(A) Depreciation Expense ……………………………………………………. 5,000

Retained Earnings—Parker (80% × $5,000) ……………………… 4,000

(2) Same as Exercise 4, part (2).

EXERCISE 3-9

Amortization Schedule

Annual

Account Adjustments Life Amount 2015 2016 2017 2018

Inventory …………………………………. 1 $ 6,250 $ 6,250

Amortization:

Investments ………………………… 3 5,000 5,000 $ 5,000 $ 5,000 $ 0

Buildings (net) …………………….. 20 12,500 12,500 12,500 12,500 12,500

Equipment (net) …………………… 5 34,500 34,500 34,500 34,500 34,500

EXERCISE 3-10

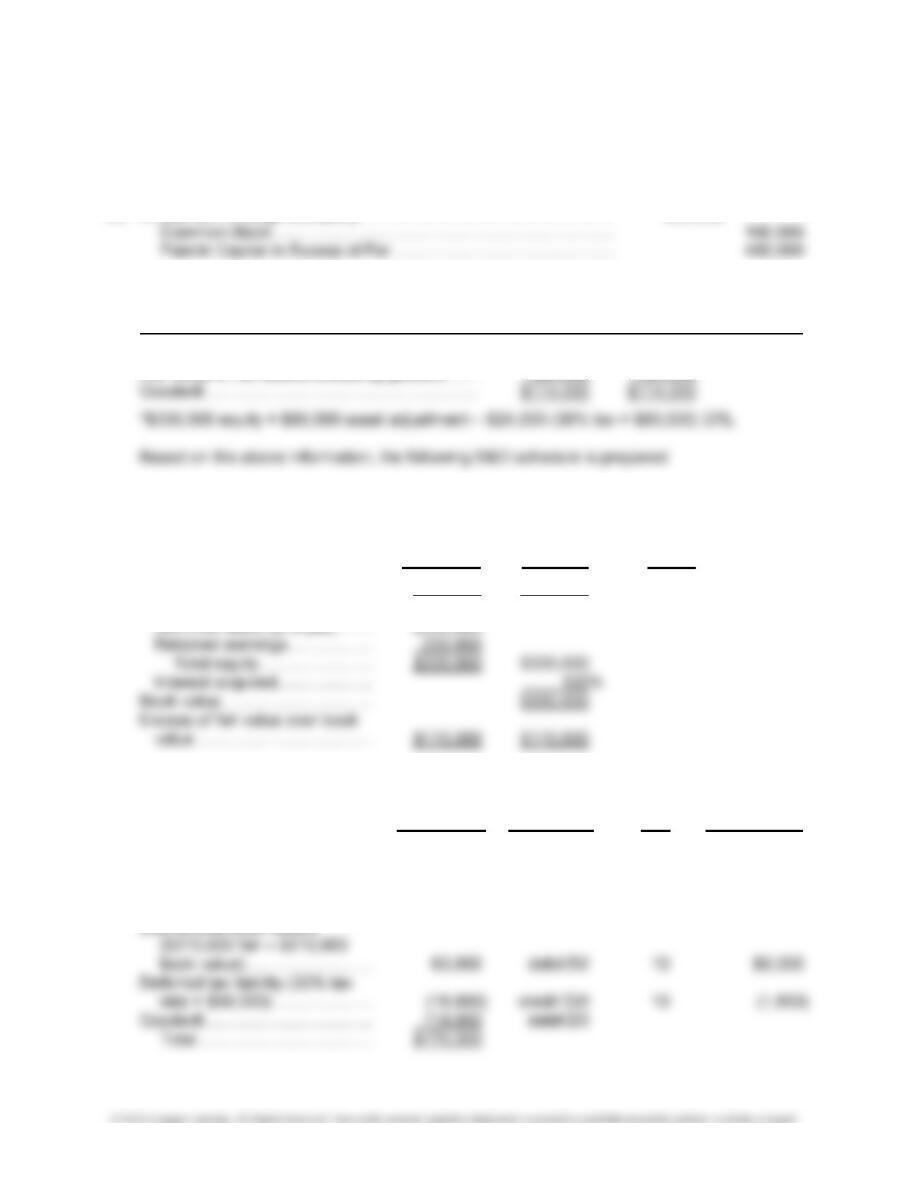

(1) Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $387,500 $310,000 $ 77,500

Less book value of interest acquired:

Common stock …………………. $100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Fixed assets ………………………….. $(12,500) credit D 5 $(2,500)

Total ……………………………….. $(12,500)

(2) (EL) Common Stock—Kraus ………………………………………………….. 80,000

Retained Earnings—Kraus ……………………………………………… 240,000

Investment in Kraus Company …………………………………… 320,000

To eliminate pro rata share of the beginning-of-

year Kraus equity balances and purchased income.

(3) Neiman Company and Subsidiary Kraus Company

Consolidated Income Statement

For Year Ended December 31, 2016

Sales ……………………………………………………………………………………….. $400,000

Less cost of goods sold ……………………………………………………………… 225,000

3-13 Ch. 3—Exercises

Exercise 3-10, Concluded

Subsidiary Kraus Company Income Distribution

Internally generated net

income ……………………………… $30,000

Adjustment of depreciation ……….. 1,250

Parent Neiman Company Income Distribution

Internally generated net

income ……………………………… $60,000

EXERCISE 3-11

Calculation of book value of Subsidiary:

Fair value at purchase …………………………………………………………………………… $1,062,500

Add $200,000 increase in Barker retained earnings ………………………………….. 200,000

Deduct amortization of excess (5 years × $10,000 per year) ………………………. (50,000)

Book value balance ……………………………………………………………………………….. $1,212,500

Ch. 3—Exercises 3–14

APPENDIX EXERCISES

EXERCISE 3B-1

(1) Investment in Largo Company ……………………………………………….. 500,000

(2) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ……………………………………. $500,000 $500,000 N/A

Fair value of net assets excluding goodwill …… 386,000 386,000*

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary ………….. $500,000 $500,000 N/A

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($120,000 fair –

$100,000 book value) ………… $ 20,000 debit D1 1

Deferred tax liability (30% tax

rate × $20,000) …………………. (6,000) credit D1t 1

Depreciable fixed assets

3-15 Ch. 3—Exercises

Exercise 3B-1, Concluded

(3) Elimination Entries:

Common Stock ……………………………………………………………………. 100,000

Retained Earnings ……………………………………………………………….. 230,000

Investment in Largo Company …………………………………………… 330,000

EXERCISE 3B-2

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (90%) (10%)

Company fair value ……………………………………. $520,000 $468,000 $52,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………….. $520,000 $468,000 $ 52,000

Less book value of interest acquired:

Common stock ($5 par) ………. $100,000

Exercise 3B-2, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ……………………………… $ 20,000 debit D1 1

Deferred tax liability (30% tax

rate × $20,000) …………………. (6,000) credit D1t 1

(2) Lucy Company and Subsidiary Diamond Company

Consolidated Income Statement

For Year Ended December 31, 2015

Sales …………………………………………………………………………….. $550,000

Less cost of goods sold (add $20,000 adjustment) ……………… 310,000

Gross profit ……………………………………………………………………. $240,000

Less expenses:

Exercise 3B-2, Concluded

Subsidiary Diamond Company Income Distribution

Inventory consumption…………. $20,000 Internally generated

Building depreciation …………… 5,000 income before tax …………… $20,000

Adjusted income before tax …… $ (5,000)

Parent Lucy Company Income Distribution

Internally generated

income before tax ……………….. $ 90,000

Adjusted income ………………………. $ 90,000

EXERCISE 3B-3

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ………………………………………….. $700,000 $700,000 N/A

Fair value of net assets excluding goodwill ………….. 445,000* 455,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary ………………… $700,000 $700,000 N/A

Less book value of interest acquired:

Common stock ($5 par) …………… $250,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings and equipment ………………. $ 50,000 debit D1 10 $5,000

Deferred tax liability (30% tax

rate × $50,000) ………………………. (15,000) credit D1t 10 (1,500)

3-19 Ch. 3—Problems

PROBLEMS

PROBLEM 3-1

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ……………………………………. $950,000 $800,000 $150,000*

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $9500,000 $800,000 $150,000

Less book value of interest acquired:

Common stock ($10 par) …….. $100,000

Paid-in capital in excess of par 200,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Land ($180,000 book –

$120,000 fair value) ………….. $ 60,000 debit D1

Building ($450,000 book –

Ch. 3—Problems 3-20

Problem 3-1, Continued

(2) Investment Entries:

Simple Equity Method

Sophisticated Equity Method Cost Method

Investment Entries

2015

Subsidiary reports Investment in Investment in No entry

income of $60,000. Solvo Company ……… 48,000 Solvo Company …………. 44,000

Subsidiary Income Subsidiary Income

(80% × reported) …. 48,000 [80% × (reported –