CHAPTER 3

ACCRUAL ACCOUNTING CONCEPTS

CLASS DISCUSSION QUESTIONS

1. AT&T and Microsoft use the accrual

basis of accounting. Generally accepted

accounting principles (GAAP) require all but

very small businesses to use the accrual

basis of accounting. This is because the ac-

2. a. Under the cash basis of accounting,

revenues are reported in the period in

which cash is received, and expenses

are reported in the period in which cash

is paid.

b. Under the accrual basis of accounting,

revenues are reported in the period in

5. Accrual basis only: c, f

Cash or accrual basis: a, b, d, e

6. Yes. Land needs no adjustment at the end

of the period.

7. No. Supplies before adjustments normally

represents the cost of the supplies at the

beginning of the period plus the cost of the

supplies purchased during the period. Some

of the supplies have been used; therefore,

an adjustment is necessary for the supplies

used before the amount for the balance

sheet is determined.

10. Statement (b): Increases the balance of an

expense account (accrued expense).

11. Statement (a): Increases the balance of a

revenue account (accrued revenue).

pired cost for the period. The reduction

in the fixed asset account is recorded by

increasing Accumulated Depreciation

rather than decreasing the fixed asset

account. The use of the contra asset ac-

count facilitates the presentation of orig-

inal cost and accumulated depreciation

for tax and other purposes.

in time.

c. Depreciation Expense appears in the

income statement; Accumulated Depre-

ciation appears in the balance sheet.

Note: Depreciation may also appear on

the statement of cash flows when the

indirect method is used. The indirect

method of preparing the statement of

cash flows is discussed in Chapter 4.

14. a. Current assets are composed of cash

and other assets that may reasonably be

expected to be realized in cash or sold

EXERCISES

E3–1

Statement of

Balance Sheet

Income

Cash Flows

Assets

=

Liabilities

+

Stockholders’ Equity

Statement

Prepaid

Accounts

Capital

Retained

Cash

+

Supplies

+

Ins.

=

Payable

+

Stock

+

Earnings

a.

Investment

25,000

25,000

b.

Paid insurance

–4,200

4,200

Balances

20,800

4,200

25,000

c.

Purchased supplies

1,200

1,200

Balances

20,800

1,200

4,200

1,200

25,000

d.

Fees earned

36,500

36,500

d.

Balances

57,300

1,200

4,200

1,200

25,000

36,500

e.

Paid expenses

–16,100

e.

Balances

41,200

1,200

4,200

1,200

25,000

20,400

Paid dividends

–7,500

Balances

33,700

1,200

4,200

1,200

25,000

a.

Financing

25,000

Fees earned

b.

Operating

–4,200

Wages exp.

–12,000

d.

36,500

Rent exp.

e.

Operating

Utilities exp.

Financing

–7,500

Misc. exp.

–1,100

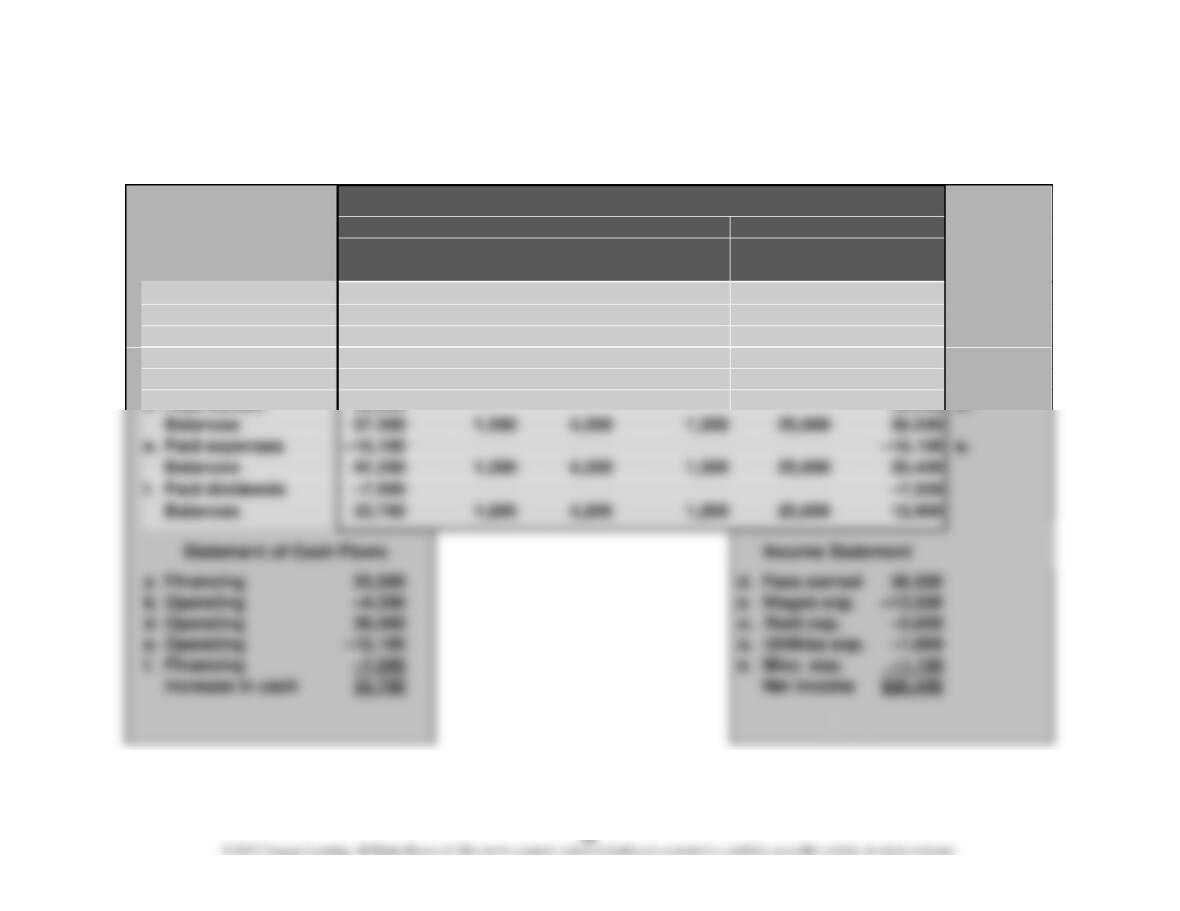

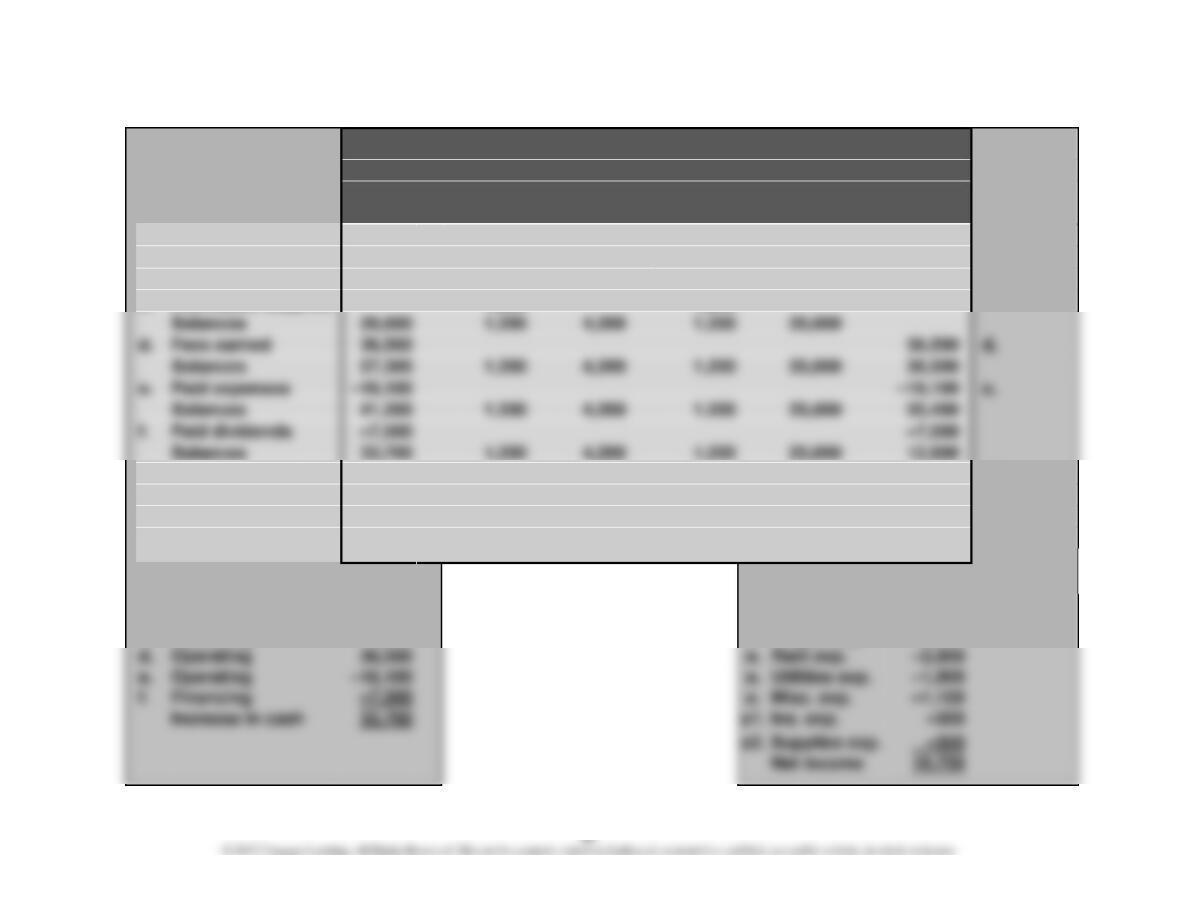

E3–2

Statement of

Balance Sheet

Income

Cash Flows

Assets

=

Liabilities

+

Stockholders’ Equity

Statement

Prepaid

Accounts

Capital

Retained

Cash

+

Supplies

+

Ins.

=

Payable

+

Stock

+

Earnings

a.

Investment

25,000

25,000

b.

Paid insurance

–4,200

4,200

Balances

20,800

4,200

25,000

c.

Purchased supplies

1,200

1,200

Balances

1,200

4,200

1,200

25,000

d.

Fees earned

36,500

36,500

d.

Balances

57,300

1,200

4,200

1,200

25,000

36,500

e.

Paid expenses

–16,100

e.

Balances

41,200

1,200

4,200

1,200

25,000

20,400

Paid dividends

–7,500

–7,500

Balances

33,700

1,200

4,200

1,200

25,000

12,900

a1.

Insurance expense

–350

–350

a1.

Balances

33,700

1,200

3,850

1,200

25,000

12,550

a2.

Supplies expense

–300

–300

a2.

Balances, Feb. 28

33,700

900

3,850

1,200

25,000

12,250

Statement of Cash Flows

Income Statement

a.

Financing

25,000

d.

Fees earned

36,500

b.

Operating

–4,200

e.

Wages exp.

–12,000

d.

Operating

36,500

e.

Rent exp.

–2,000

e.

Operating

e.

Utilities exp.

–1,000

Financing

e.

Misc. exp.

–1,100

Supplies exp.

–300

E3–3

THE HERBAL SHOPPE

Income Statement

For the Month Ended February 28, 20Y4

Fees earned ……………………………………………………………….. $36,500

Operating expenses:

Wages expense ……………………………………………………… $12,000

Rent expense…………………………………………………………. 2,000

THE HERBAL SHOPPE

Retained Earnings Statement

For the Month Ended February 28, 20Y4

Net income …………………………………………………………………. $19,750

E3–3, Concluded

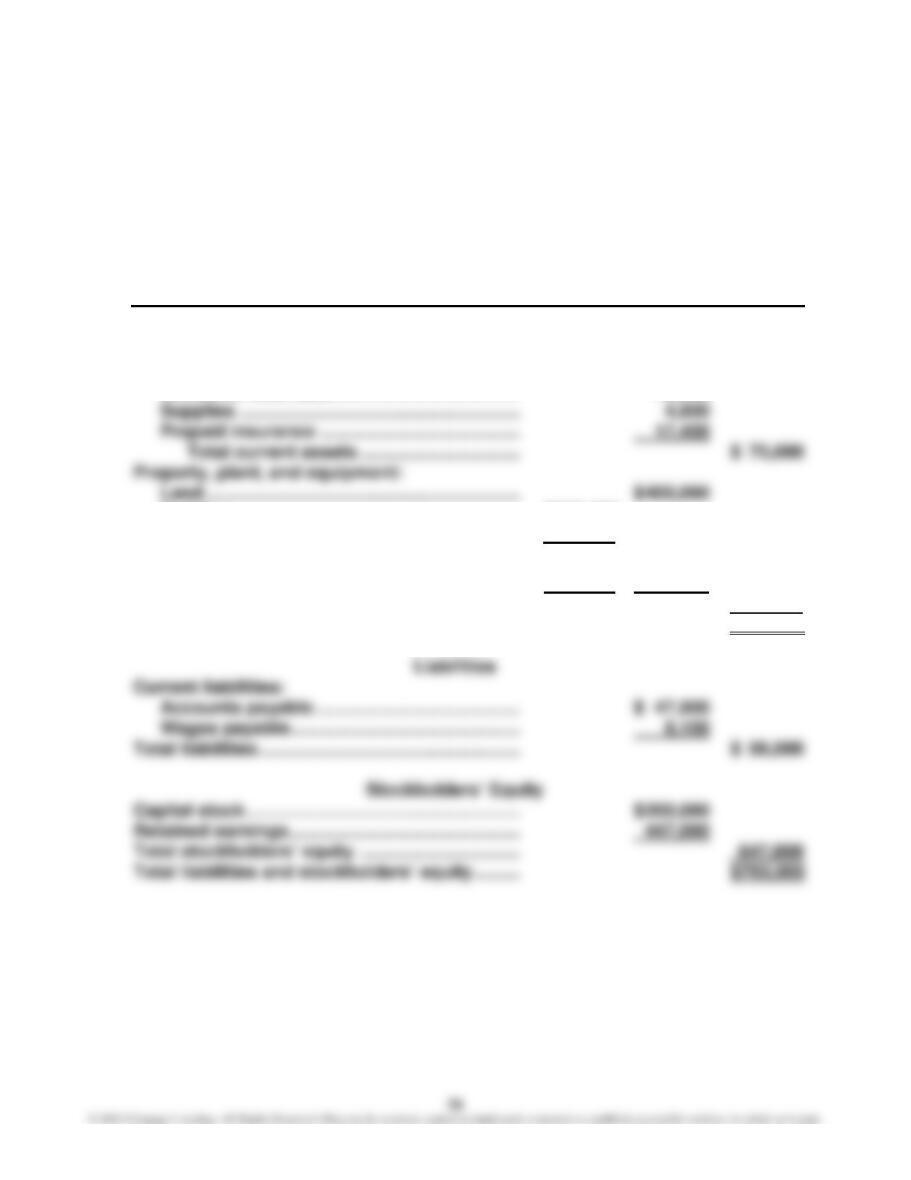

THE HERBAL SHOPPE

Balance Sheet

February 28, 20Y4

Assets

Cash ………………………………………………………………………….. $33,700

Supplies …………………………………………………………………….. 900

Prepaid insurance ………………………………………………………. 3,850

Total assets …………………………………………………………… $38,450

THE HERBAL SHOPPE

Statement of Cash Flows

For the Month Ended February 28, 20Y4

Cash flows from operating activities:

Cash received from customers……………………………….. $ 36,500

Cash paid for expenses ………………………………………….. (20,300)*

E3–4

Net income …………………………………………………………………. $19,750

Add increase in accounts payable. ………………………………. 1,200

Deduct:

E3–5

a. Transaction:

(a) Issued capital stock in exchange for cash, $50,000

(b) Purchased supplies on account, $1,500

(c) Paid cash to creditors for amounts owed, $1,000

E3–6

1. (b) Deferred revenue (unearned revenue)

2. (a) Deferred expense (prepaid expense)

3. (b) Deferred revenue (unearned revenue)

4. (d) Accrued revenue (accrued asset)

E3–7

Account Answer

Accounts Receivable ……………………… Normally requires adjustment (AR).

Accumulated Depreciation ……………… Normally requires adjustment (DE).

Capital Stock …………………………………. Does not normally require adjustment.

Dividends ………………………………………. Does not normally require adjustment.

E3–8

a. $2,250 ($4,000 – $1,750)

b. $4,200 ($1,100 + $3,100)

E3–9

a. Insurance Expense, increase, $10,500 ($14,400 + $9,600 – $13,500)

E3–10

E3–11

a. Unearned Revenue, decrease, $6,000 million

Revenue, increase, $6,000 million

E3–12

a. Rent revenue (or revenues) will be understated by $36,750. Net income will be

E3–13

a. Salary Expense, increase, $4,740 [($7,900/5 days) × 3 days]

E3–14

$813,100 ($825,000 – $11,900)

E3–15

a. Salary expense (or expenses) will be understated by $6,750. Net income will

be overstated by $6,750.

E3–16

a. Salary expense (or expenses) will be overstated by $6,750. Net income will be

understated by $6,750.

E3–17

a. $598,000,000

E3–18

Error (a) Error (b)

Over- Under- Over- Under-

stated stated stated stated

1. Revenue for the year would be ………….. $ 0 $175,000 $ 0 $ 0

2. Expenses for the year would be ………… 0 0 0 12,300

E3–19

$2,387,300 ($2,224,600 + $175,000 – $12,300)

E3–20

a. Accounts Receivable, increase, $47,700

E3–21

a. Unearned Fees, decrease, $50,000

Fees Earned, increase, $50,000

E3–22

a. Fees earned (or revenues) will be understated by $13,400. Net income will be

E3–23

a. Depreciation Expense, increase, $133,000

Accumulated Depreciation, increase, $133,000

b. (1) Depreciation expense would be understated by $133,000. Net income

E3–24

Adjustment Account Increase or Decrease Amount

1. Accounts Receivable Increase $11,250

Fees Earned Increase 11,250

2. Supplies Expense Increase 1,350

Supplies Decrease 1,350

3. Insurance Expense Increase 1,800

Prepaid Insurance Decrease 1,800

E3–25

a. $622,655 ($2,983,797 – $2,361,142)

E3–26

a. Current asset: 1, 3, 5, 6

E3–27

Since current liabilities are usually due within one year, $96,000 ($8,000 × 12

months) would be reported as a current liability on the balance sheet. The re-

E3–28

POUNDS-AWAY SERVICES CO.

Balance Sheet

November 30, 20Y9

Assets

Current assets:

Cash ……………………………………………………….…. $ 87,600

Accounts receivable …………………………………… 129,000

Supplies …………………………………………………….. 48,000

Liabilities

Current liabilities:

Accounts payable ………………………………………. $135,600

Salaries payable …………………………………………. 26,400

Unearned fees ……………………………………………. 18,000

Total liabilities ………………………………………………… $ 180,000

Stockholders’ Equity

Capital stock …………………………………………………… $150,000

E3–29

LA-Z-BOY INC.

Balance Sheet

April 30, 20Y8

(in thousands)

Assets

Current assets:

Cash ……………………………………………………….…………….. $115,262

Accounts receivable ………………………………………………. 161,299

Inventories …………………………………………………………….. 138,444

Other current assets ………………………………………………. 17,218

Liabilities

Current liabilities:

Accounts payable ………………………………………………….. $ 49,537

Accrued expenses …………………………………………………. 77,447

Debt due within one year ……………………………………….. 5,120

Total current liabilities ………………………………………. $132,104

Stockholders’ Equity

Capital stock ………………………………………………………………. $256,322

Retained earnings ………………………………………………………. 107,818

E3–30

1. The date of the statement should be “May 31, 20Y5” and not “For the Year

Ended May 31, 20Y5.”

2. Accounts payable should be a current liability.

3. Land should be classified as property, plant, and equipment.

4. “Accumulated depreciation” should be deducted from the related fixed asset.

E3–30, Concluded

A corrected balance sheet would be as follows:

ATLAS SERVICES CO.

Balance Sheet

May 31, 20Y5

Assets

Current assets:

Cash ……………………………………………………… $ 12,000

Accounts receivable ………………………………. 40,800

Building ………………………………………………… $225,000

Less accumulated depreciation …………. 54,600 170,400

Equipment …………………………………………….. $ 90,000

Less accumulated depreciation …………. 32,400 57,600

Total property, plant, and equipment 628,000

Total assets ……………………………………………….. $703,000

PROBLEMS

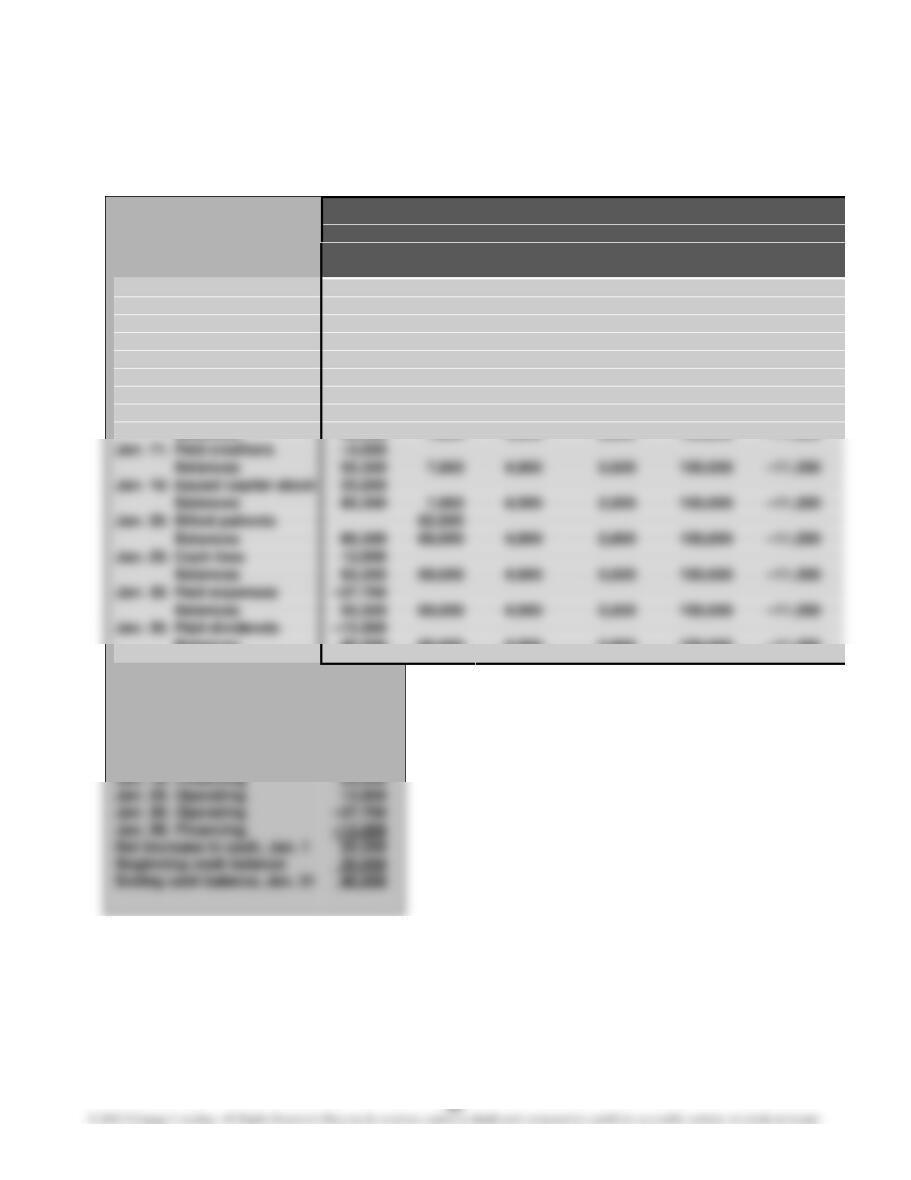

P3–1

Statement of

Balance

Cash Flows

Assets

Accts.

Prepaid

Acc.

Cash

+

Rec.

+

Insurance

+

Supplies

+

Building

–

Depr.

+

Balances, Jan. 1

20,000

34,500

700

1,000

150,000

–11,200

Jan. 1.

Received rent rev.

15,000

Balances

35,000

34,500

700

1,000

150,000

–11,200

Jan. 1.

Paid ins.

–4,200

4,200

Balances

30,800

34,500

4,900

1,000

150,000

–11,200

Jan. 6.

Purchased supplies

1,800

Balances

30,800

34,500

4,900

2,800

150,000

–11,200

Jan. 9.

Collected cash

27,500

–27,500

Balances

58,300

7,000

4,900

2,800

150,000

–11,200

Jan. 11.

Paid creditors

–3,000

Balances

55,300

7,000

4,900

2,800

150,000

–11,200

Jan. 18.

Issued capital stock

25,000

Balances

80,300

7,000

4,900

2,800

150,000

–11,200

Jan. 20.

Billed patients

62,000

Balances

80,300

69,000

4,900

2,800

150,000

–11,200

Jan. 25.

Cash fees

12,900

Balances

93,200

69,000

4,900

2,800

150,000

–11,200

Jan. 30.

Paid expenses

Balances

55,500

69,000

4,900

2,800

150,000

–11,200

Jan. 30.

Paid dividends

Balances

40,500

69,000

4,900

2,800

150,000

–11,200

Statement of Cash Flows

Jan. 1.

Operating

15,000

Jan. 1.

Operating

–4,200

Jan. 9.

Operating

27,500

Jan. 11.

Operating

–3,000

Jan. 18.

Financing

Jan. 25.

Operating

Jan. 30.

Operating

Jan. 30.

Financing

Net increase in cash, Jan. 1

20,000

Ending cash balance, Jan. 31

40,500

P3–1, Concluded

Sheet

Income

=

Liabilities

+

Stockholders’ Equity

Statement

Accts.

Unearned

Wages

Notes

Capital

Retained

+

Land

=

Payable

+

Revenue

+

Payable

+

Payable

+

Stock

+

Earnings

120,000

7,500

0

0

30,000

50,000

227,500

15,000

120,000

7,500

15,000

0

30,000

50,000

227,500

120,000

7,500

15,000

0

30,000

50,000

227,500

1,800

120,000

9,300

15,000

0

30,000

50,000

227,500

120,000

9,300

15,000

0

30,000

50,000

227,500

120,000

6,300

15,000

0

30,000

50,000

227,500

120,000

6,300

15,000

0

30,000

227,500

Jan. 20.

120,000

6,300

15,000

0

30,000

289,500

12,900

Jan. 25.

120,000

6,300

15,000

0

30,000

302,400

–37,700

Jan. 30.

–15,000

120,000

6,300

15,000

0

30,000

249,700

Income Statement

Jan. 20. Fees earned

62,000

Jan. 25. Fees earned

12,900

Jan. 30. Wages exp.

–24,000

–6,000

–5,000

–2,500