Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 1 (concluded)

Sep. 1, 2018

Prepaid Rent

2,400

Cash

2,400

(Pay cash for one-year rental policy)

Sep. 21, 2018

Cash

Service Revenue (Clinic)

(Receive cash for rock climbing clinic)

Oct. 17, 2018

Cash

Service Revenue (Clinic)

(Receive cash for orienteering clinic)

Dec. 8, 2018

Miscellaneous Expense

1,200

Cash

1,200

(Pay cash for race permit)

Dec. 12, 2018

Supplies (Racing)

2,800

Accounts Payable

2,800

Dec. 15, 2018

Cash

(Receive cash for adventure race)

Dec. 16, 2018

Salaries Expense

2,000

(Pay cash for salary)

Dec. 31, 2018

Dividend

4,000

(Pay cash for dividend)

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 2

Dec. 31, 2018

Debit

Credit

Depreciation Expense

8,000

Accumulated Depreciation

8,000

(Adjust accumulated depreciation)

Dec. 31, 2018

Insurance Expense

2,400

Prepaid Insurance

2,400

(Adjust prepaid insurance)

Dec. 31, 2018

Rent Expense

Prepaid Rent

(Adjust prepaid rent)

Dec. 31, 2018

Supplies (Office)

1,500

(Adjust office supplies)

Dec. 31, 2018

Interest Expense

Interest Payable

(Adjust interest payable)

Supplies Expense (Racing)

Supplies (Racing)

2,600

Income Tax Expense

Income Tax Payable

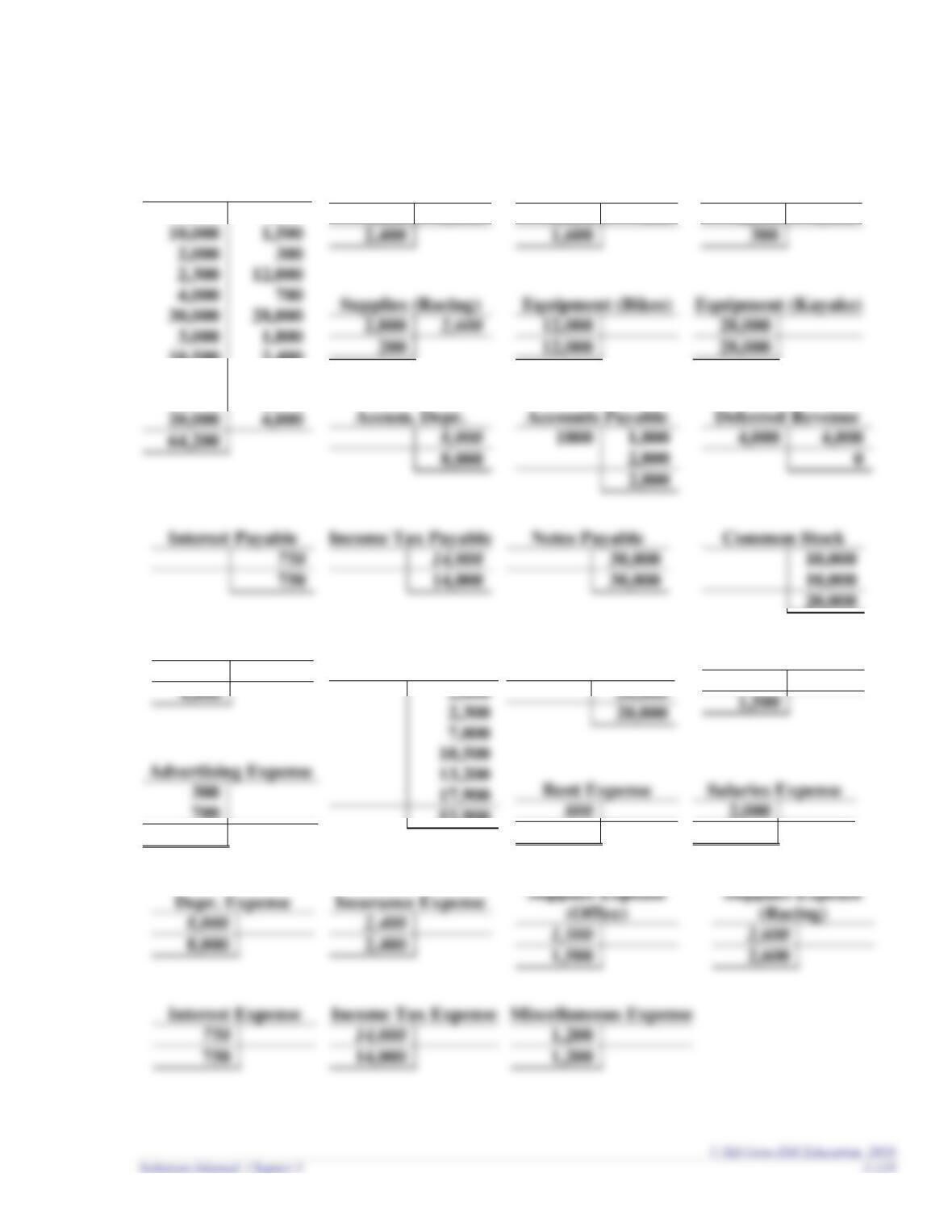

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 3 (Note: adjusting entries in italics)

8,000

2,400

1,500

Interest Expense

750

14,000

2,600

Prepaid Insurance

4,800

2,400

2,400

1,600

2,800

2,600

200

300

4,000

8,000

Legal Fees Expense

1,500

1,500

4,000

Salaries Expense

2,000

700

1,000

Prepaid Rent

2,400

800

Service Revenue

(Racing)

Dividends

4,000

2,000

Supplies (Office)

1,800

1,500

800

Service Revenue

(Clinic)

52,900

Cash

10,000

10,500

13,200

17,900

4,800

2,400

1,200

2,000

Additional Perspective 3-1 (continued)

Requirement 4

Great Adventures, Inc.

Adjusted Trial Balance

December 31, 2018

Accounts

Debit

Credit

Cash

$ 64,200

Prepaid Insurance

2,400

Prepaid Rent

Supplies (Office)

Supplies (Racing)

Equipment (Bikes)

12,000

Equipment (Kayaks)

28,000

Accumulated Depreciation

$ 8,000

Accounts Payable

2,800

Income Tax Payable

14,000

Interest Payable

750

Notes Payable

30,000

Common Stock

20,000

Dividends

4,000

Service Revenue (Clinic)

52,900

Service Revenue (Racing)

20,000

Advertising Expense

Depreciation Expense

Income Tax Expense

Insurance Expense

Interest Expense

Legal Fees Expense

Miscellaneous Expense

Rent Expense

Salaries Expense

Supplies Expense (Office)

Supplies Expense (Racing)

$148,450

$148,450

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 5

Great Adventures, Inc.

Income Statement

For the period ended December 31, 2018

Revenues:

Service revenue (clinic)

$52,900

Expenses:

Advertising expense

1,000

Depreciation expense

8,000

Income tax expense

14,000

Insurance expense

2,400

Interest expense

Legal fees expense

1,500

Miscellaneous expense

1,200

Rent expense

Salaries expense

2,000

Supplies expense (office)

1,500

Supplies expense (racing)

2,600

Net income

Great Adventures, Inc.

Statement of Stockholders’ Equity

For the period ended December 31, 2018

Common

Stock

Retained

Earnings

Total

Stockholders’

Equity

Balance at July 1

$ 0

$ 0

$ 0

Issuance of common stock

20,000

20,000

Add: Net income for 2018

37,150

37,150

Less: Dividends

Balance at December 31

$20,000

$33,150

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 5 (concluded)

Great Adventures, Inc.

Balance Sheet

December 31, 2018

Assets

Liabilities

Current assets:

Current liabilities:

Cash

$ 64,200

Accounts payable

$ 2,800

Prepaid insurance

Interest payable

Prepaid rent

Income tax payable

Supplies (office)

Supplies (racing)

Notes payable

30,000

68,700

Long-term assets:

Stockholders’ Equity

Equipment (bikes)

12,000

Common stock

20,000

Equipment (kayaks)

28,000

Retained earnings

33,150

Accumulated depr.

53,150

Total assets

$100,700

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

Requirement 6

Dec. 31, 2018

Debit

Credit

Service Revenue (Clinic)

52,900

Service Revenue (Racing)

20,000

Dec. 31, 2018

Retained Earnings

35,750

Advertising Expense

1,000

Depreciation Expense

8,000

Income Tax Expense

14,000

Insurance Expense

2,400

Interest Expense

Legal Fees Expense

1,500

Miscellaneous Expense

1,200

Rent Expense

Salaries Expense

2,000

Supplies Expense (Office)

1,500

Supplies Expense (Racing)

2,600

Dec. 31, 2018

Retained Earnings

4,000

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (continued)

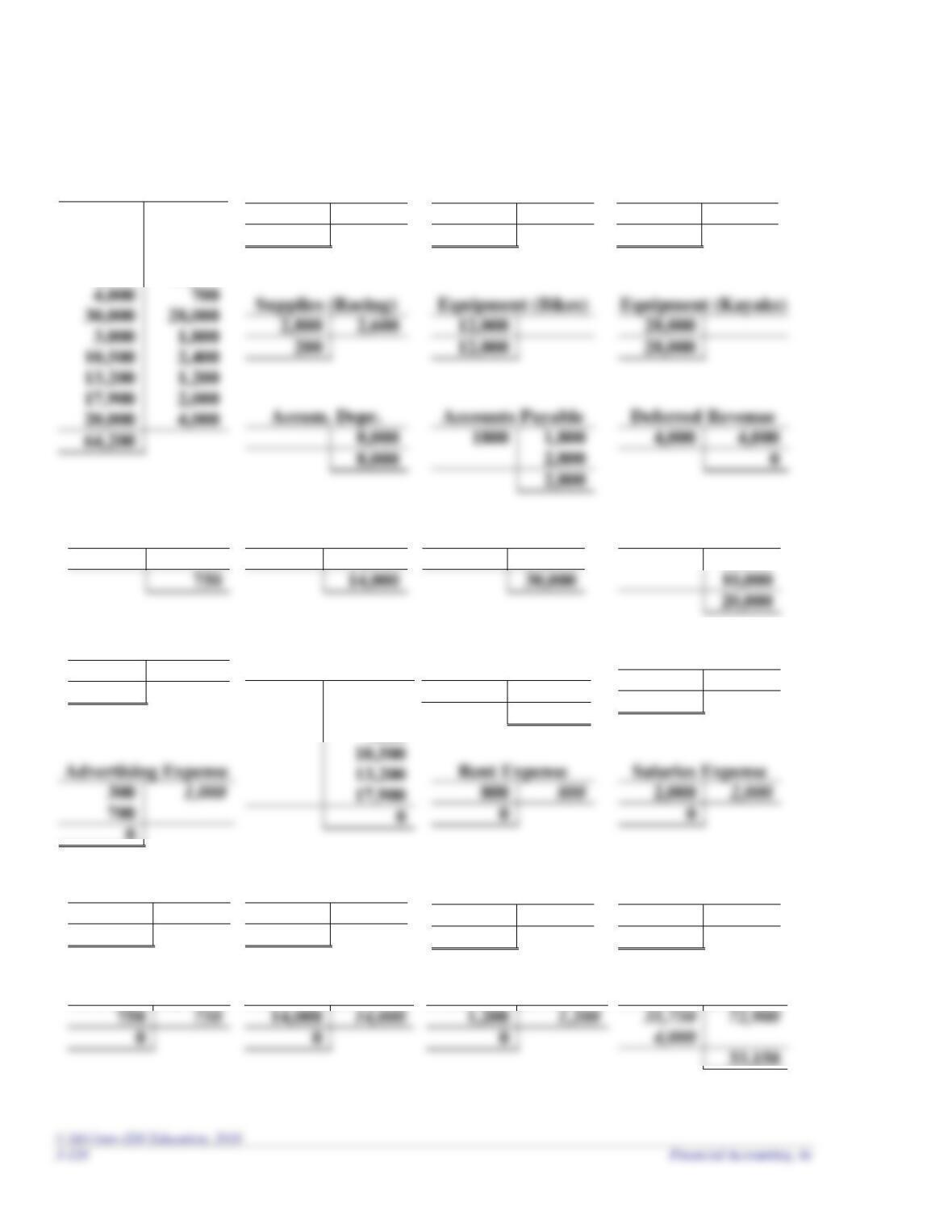

Requirement 7 (Note: closing entries in italics)

Prepaid Insurance

4,800

2,400

2,400

Equipment (Bikes)

12,000

12,000

2,800

4,000

0

Equipment (Kayaks)

28,000

28,000

2,800

2,600

200

Accum. Depr.

8,000

8,000

64,200

Common Stock

20,000

30,000

750

14,000

10,000

Legal Fees Expense

1,500

1,500

0

Advertising Expense

Salaries Expense

2,000

2,000

0

Rent Expense

800

0

0

Notes Payable

30,000

Prepaid Rent

2,400

800

1,600

Service Revenue

(Racing)

20,000

20,000

0

Dividends

4,000

4,000

0

Supplies (Office)

1,800

1,500

300

Interest Payable

750

Depr. Expense

8,000

8,000

0

Insurance Expense

2,400

2,400

0

Supplies Expense

(Office)

1,500

1,500

0

Supplies Expense

(Racing)

2,600

2,600

0

Interest Expense

750

0

14,000

0

33,150

1,200

Income Tax Payable

14,000

Income Tax Expense

Service Revenue

(Clinic)

52,900

2,000

2,300

7,000

Retained Earnings

Miscellaneous Expense

Cash

10,000

10,000

2,000

2,300

4,800

1,500

300

12,000

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-1 (concluded)

Requirement 8

Great Adventures, Inc.

Post-closing Trial Balance

December 31, 2018

Accounts

Debit

Credit

Cash

$ 64,200

Prepaid Insurance

2,400

Prepaid Rent

Supplies (Office)

Supplies (Racing)

Equipment (Bikes)

12,000

Equipment (Kayaks)

28,000

Accumulated Depreciation

$ 8,000

Accounts Payable

2,800

Income Tax Payable

14,000

Interest Payable

750

Notes Payable

30,000

Common Stock

Retained Earnings

33,150

$108,700

$108,700

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-2

Requirement 1

Current assets equal $890,513 thousand. Current assets include cash and cash

equivalents, short-term investments, merchandise inventory, accounts receivable,

Requirement 2

Current liabilities equal $459,093 thousand. Current liabilities include accounts

payable, accrued compensation and payroll taxes, accrued rent, accrued income and

Requirement 3

Requirement 4

Requirement 6

The change in retained earnings typically represents net income for the year less

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-3

Requirement 1

Current assets equal $324,589 thousand. Current assets include cash and cash

Requirement 2

Current liabilities equal $122,271 thousand. Current liabilities include accounts

Requirement 3

Requirement 4

Requirement 6

The change in retained earnings represents net income for the year less dividends. If

the change in retained earnings is -$14,040 thousand and net income equals $162,564

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-4

Requirement 1

For American Eagle, the ratio of current assets to total assets is 0.52 (= $890,513 /

$1,696,908). For Buckle, the ratio of current assets to total assets is 0.60 (= $324,589 /

Requirement 2

For American Eagle, the ratio of current liabilities to total liabilities is 0.82 (=

$459,093 / $557,162). For Buckle, the ratio of current liabilities to total liabilities is

Requirement 3

For American Eagle, the dividend payout ratio is 1.24 (= $99,585 / $80,322). For

Buckle, the dividend payout ratio is 1.09 (= $176,604 / $162,564). A higher ratio

indicates that a higher portion of the company’s net income is paid in dividends. More

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-5

What is the issue?

By reporting the $80,000 as Service Revenue instead of Deferred Revenue, before-tax

profit will increase from $280,000 to $360,000. This adjustment would make it appear

Who are the parties affected?

As the assistant controller (accountant), you should understand that your

What factors should you consider in making your decision?

Because you are new to the position, you might not be sure that it’s right for you to

question any decision of the company’s president. You have just been assigned and

don’t want to lose your job. If you do make the adjustment, then the company’s

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-6

(Note to instructor: Answers are based on McDonald’s December 2014 annual report,

and dollar amounts are in millions.)

Requirement 1

Requirement 2

Requirement 3

Current assets include cash and equivalents, accounts and notes receivable,

Requirement 4

Current liabilities include accounts payable, income taxes, other taxes, accrued

Requirement 5

Chapter 3 – The Accounting Cycle: End of the Period

Additional Perspective 3-7

Requirement 1

Prepaid revenues occur when cash is received before the related revenues are reported.

Prepaid expenses occur when cash (or an obligation to pay cash) is paid before the

related expenses and liabilities are reported.

Requirement 2

The adjusting entry for prepaid expenses includes a debit to an expense and a credit to

an asset. The adjusting entry for Deferred revenue includes a debit to Deferred

Requirement 3

The adjusting entry for accrued expenses includes a debit to an expense and a credit to

a liability. The adjusting entry for accrued revenues includes a debit to an asset and a