3-41

PROBLEM 3-56 (25 MINUTES)

1.

Quarter

Predetermined

Overhead Rate

Calculations

2.

February

May

Direct material………………………………………

$600

$600

Direct labor ………………………………………….

Manufacturing overhead:

3.

February

May

Total cost …………………………………………….

$1,100

$1,140

Markup (10%) ……………………………………….

110

4.

hours labor–direct budgeted annual

overhead ingmanufactur budgeted annual

rate nedPredetermi =

5.

February

May

Direct material………………………………………..

$ 600.00

$ 600.00

Direct labor ……………………………………………

PROBLEM 3-56 (CONTINUED)

6.

Total cost ………………………………………………

$1,117.80

Markup (10%) …………………………………………

$1,229.58

3-43

PROBLEM 3-57 (55 MINUTES)

The answers to the questions are as follows:

1.

$648,000

6.

$180,000

2.

$57,000

7.

$450,000

3.

$210,000

8.

$120,000

4.

$114,000

9.

$45,000

5.

$240,000

Zero

The completed T accounts, along with supporting calculations, follow.

Raw-Material Inventory

Accounts Payable

Bal. 8/31

45,000

36,000

Bal. 8/31

210,000

120,000

243,000

210,000

Bal. 9/30

135,000

3,000

Bal. 9/30

Work-in-Process Inventory

Finished-Goods Inventory

Bal. 8/31

24,000

Bal. 8/31

105,000

Direct

450,000

450,000

540,000

material

Bal. 9/30

15,000

Direct

labor

Overhead

540,000

Bal. 9/30

Manufacturing Overhead

Sales Revenue

180,000

180,000

648,000

Wages Payable

Accounts Receivable

3,000

Bal. 8/31

Bal. 8/31

24,000

238,500

240,000

648,000

615,000

Bal. 9/30

Bal. 9/30

57,000

Supporting Calculations:

3-44

PROBLEM 3-57 (CONTINUED)

2.

Ending balance in accounts receivable

=

=

$24,000 + $648,000 – $615,000

=

$57,000

beginning balance + sales revenue

3.

Purchases of raw material

=

addition to accounts payable

Addition to accounts payable

=

ending balance + payments

=

$3,000 + $243,000 – $36,000

=

$210,000

4.

September 30 balance in

work-in-process inventory

=

direct

material

+

direct

labor

+

manufacturing

overhead

=

$61,500 + (1,500)($20) + (1,500)($15*)

*Predetermined overhead rate

=

†

hours labor–direct budgeted

overhead budgeted

=

$15 per direct-labor hour

5.

Addition to work in process

for direct labor

=

September credit to

wages payable

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-45

PROBLEM 3-57 (CONTINUED)

6.

September applied overhead

=

direct labor hours predetermined overhead rate

7.

Cost of goods completed

during September

=

beginning

balance in

work in

process

+

additions

during

September

–

ending balance in

work in process

=

$24,000 + ($120,000 + $240,000 + $180,000) – $114,000

=

$450,000

9.

August 31 balance in

raw-material inventory

=

=

$135,000 + $120,000 – $210,000

=

$45,000

September 30

balance in raw-

+

direct

material

–

purchases

10.

Overapplied or underapplied overhead = actual overhead – applied overhead

= $180,000 – $180,000 = 0

3-46

PROBLEM 3-58 (75 MINUTES)

1.

hours labor–direct budgeted

overhead ingmanufactur budgeted

rate overhead nedPredetermi

=

2.

Journal entries:

(a)

Raw-Material Inventory ………………………………..

6,000

Accounts Payable ………………………………

6,000

(b)

Raw-Material Inventory ………………………………..

5,200

Accounts Payable ………………………………

5,200

(c)

Work-in-Process Inventory …………………………..

Raw-Material Inventory ……………………….

11,330

Manufacturing Overhead** …………………………...

Manufacturing-Supplies Inventory ……….

**Valve lubricant is an indirect material, so it is considered an overhead cost.

(d)

Work-in-Process Inventory …………………………..

36,000

Manufacturing Overhead ……………………………..

14,100

Wages Payable …………………………………..

50,100

Work-in-Process Inventory …………………………..

Manufacturing Overhead …………………….

39,600

(e)

Manufacturing Overhead ……………………………..

13,000

Accumulated Depreciation: Building and

Equipment ……………………………………….

13,000

Manufacturing Overhead ……………………………..

1,340

3-47

PROBLEM 3-58 (CONTINUED)

(g)

Manufacturing Overhead ……………………………..

2,400

Accounts Payable ………………………………

2,400

(h)

Manufacturing Overhead ……………………………..

2,370

Cash ………………………………………………….

2,370

(i)

Manufacturing Overhead ……………………………..

2,900

Prepaid Insurance ………………………………

2,900

(j)

Selling and Administrative Expenses ……………

7,500

Cash ………………………………………………….

7,500

(k)

Selling and Administrative Expenses ……………

4,500

Accumulated Depreciation: Buildings and

Equipment ……………………………………….

4,500

(l)

Selling and Administrative Expenses ……………

1,150

Cash ………………………………………………….

1,150

Finished-Goods Inventory ………………………….

37,130*

Work-in-Process Inventory ………………..

*Cost of Job T79:

Direct material (260 $5.50) …………….

$ 1,430

Manufacturing overhead (850 $22) ..

Total cost ……………………………………….

(n)

Accounts Receivable …………………………………

27,360*

Sales Revenue …………………………..………

Cost of Goods Sold ……………………………………

Finished-Goods Inventory ………………….

**18,565 = $37,130

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-48

PROBLEM 3-58 (CONTINUED)

3.

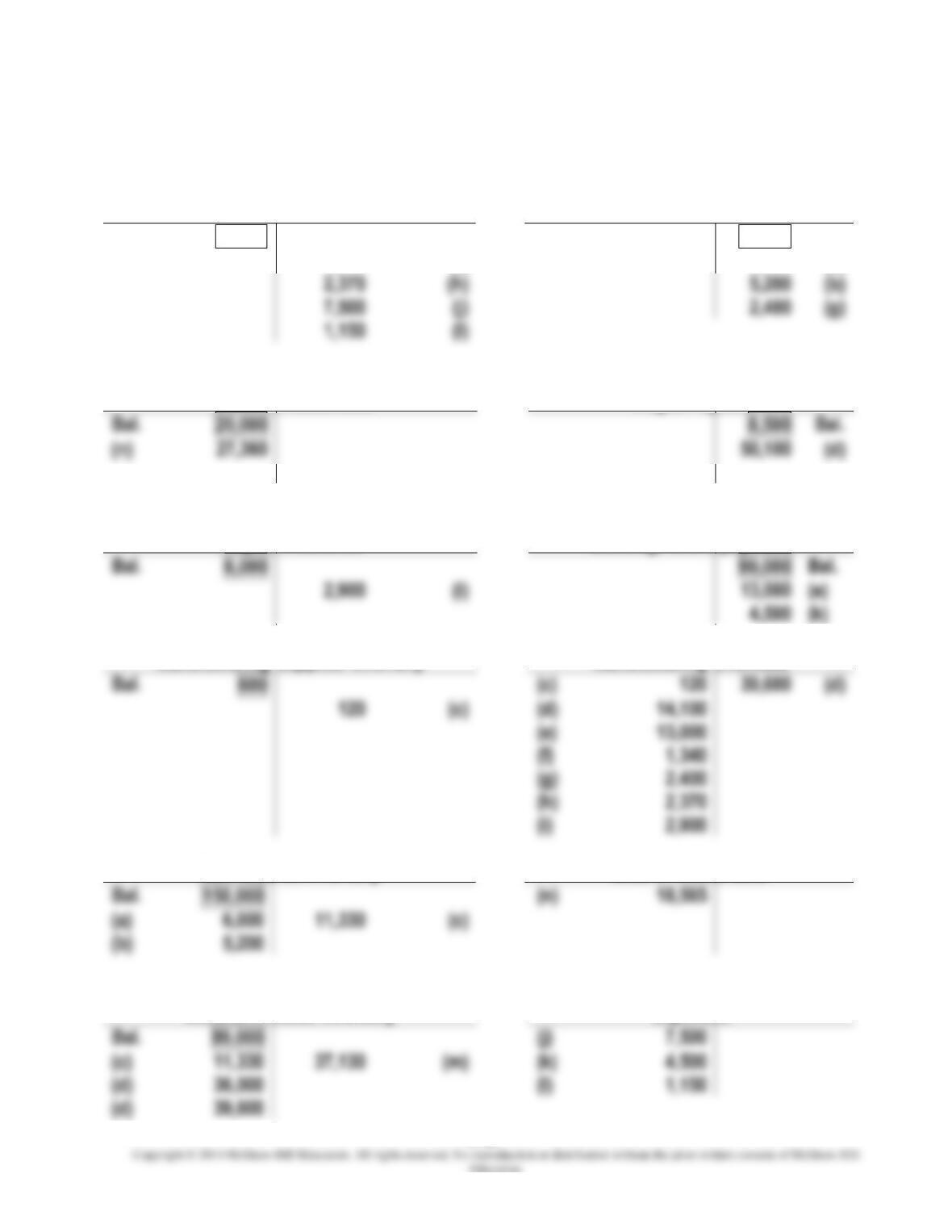

T-accounts and posting of journal entries:

Cash

Accounts Payable

Bal

11,000

14,500

Bal

1,340

(f)

6,000

(a)

2,370

5,200

(b)

7,500

2,400

(g)

1,150

Accounts Receivable

Wages Payable

20,000

(n)

50,100

(d)

Accumulated Depreciation:

Prepaid Insurance

Buildings and Equipment

Bal.

99,000

Bal.

13,000

(e)

4,500

(k)

Manufacturing-Supplies Inventory

Manufacturing Overhead

(d)

14,100

(e)

13,000

1,340

(g)

2,400

(h)

2,370

(i)

2,900

Raw-Material Inventory

Cost of Goods Sold

Bal.

(n)

(a)

(b)

Selling and Administrative

Work-in-Process Inventory

Expenses

(c)

(k)

4,500

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

PROBLEM 3-58 (CONTINUED)

Finished-Goods Inventory

Sales Revenue

4.

(a)

Calculation of actual overhead:

Indirect material (valve lubricant) …………………………………….

$ 120

Indirect labor ………………………………………………………………….

Depreciation: factory building and equipment ………………….

Rent: warehouse …………………………………………………………….

Utilities …………………………………………………………………………..

Property taxes ………………………………………………………………..

Insurance ……………………………………………………………………….

Total actual overhead ……………………………………………………..

(b)

Overapplied overhead

=

−

overhead

ingmanufactur applied

overhead

ingmanufactur actual

=

$36,230 – $39,600*

=

$3,370 overapplied

(c)

Manufacturing Overhead …………………………………………………

Cost of Goods Sold ……………………………………………….

PROBLEM 3-58 (CONTINUED)

5.

BANDWAY COMPANY

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE MONTH OF OCTOBER

Direct material:

Raw-material inventory, October 1 …………………….

$150,000

Add: October purchases of raw material ……………

Raw material available for use …………………………..

$161,200

Deduct: Raw-material inventory, October 31 ………

Raw material used …………………………………………….

Direct labor …………………………………………………………….

Manufacturing overhead:

Indirect material ………………………………………………..

$ 120

Indirect labor ……………………………………………………

Depreciation on factory building and equipment ..

Utilities …………………………………………………………….

Property taxes ………………………………………………….

Insurance …………………………………………………………

Total actual manufacturing overhead ……………

Add: overapplied overhead ………………………….

Overhead applied to work in process …………………

39,600

Total manufacturing costs ……………………………………….

$ 86,930

Add: Work-in-process inventory, October 1 ………………

89,000

Subtotal ………………………………………………………………….

Deduct: Work-in-process inventory, October 31 ……….

Cost of goods manufactured ……………………………………

$ 37,130†

3-51

PROBLEM 3-58 (CONTINUED)

6.

BANDWAY COMPANY

SCHEDULE OF COST OF GOODS SOLD

FOR THE MONTH OF OCTOBER

Finished-goods inventory, October 1 ………………………………………………

$223,000

Add: Cost of goods manufactured …………………………………………………..

37,130

Cost of goods available for sale ………………………………………………………

$260,130

Deduct: Finished-goods inventory, October 31 ………………………………..

Cost of goods sold …………………………………………………………………………

Deduct: Overapplied overhead* ………………………………………………………

Cost of goods sold (adjusted for overapplied overhead) …………………..

7.

BANDWAY COMPANY

INCOME STATEMENT

FOR THE MONTH OF OCTOBER

Sales revenue ………………………………………………………………………………..

$27,360

Less: Cost of goods sold ……………………………………………………………….

Gross margin …………………………………………………………………………………

$12,165

Selling and administrative expenses …………………………..…………………..

Income (loss) …………………………………………………………………………………

3-52

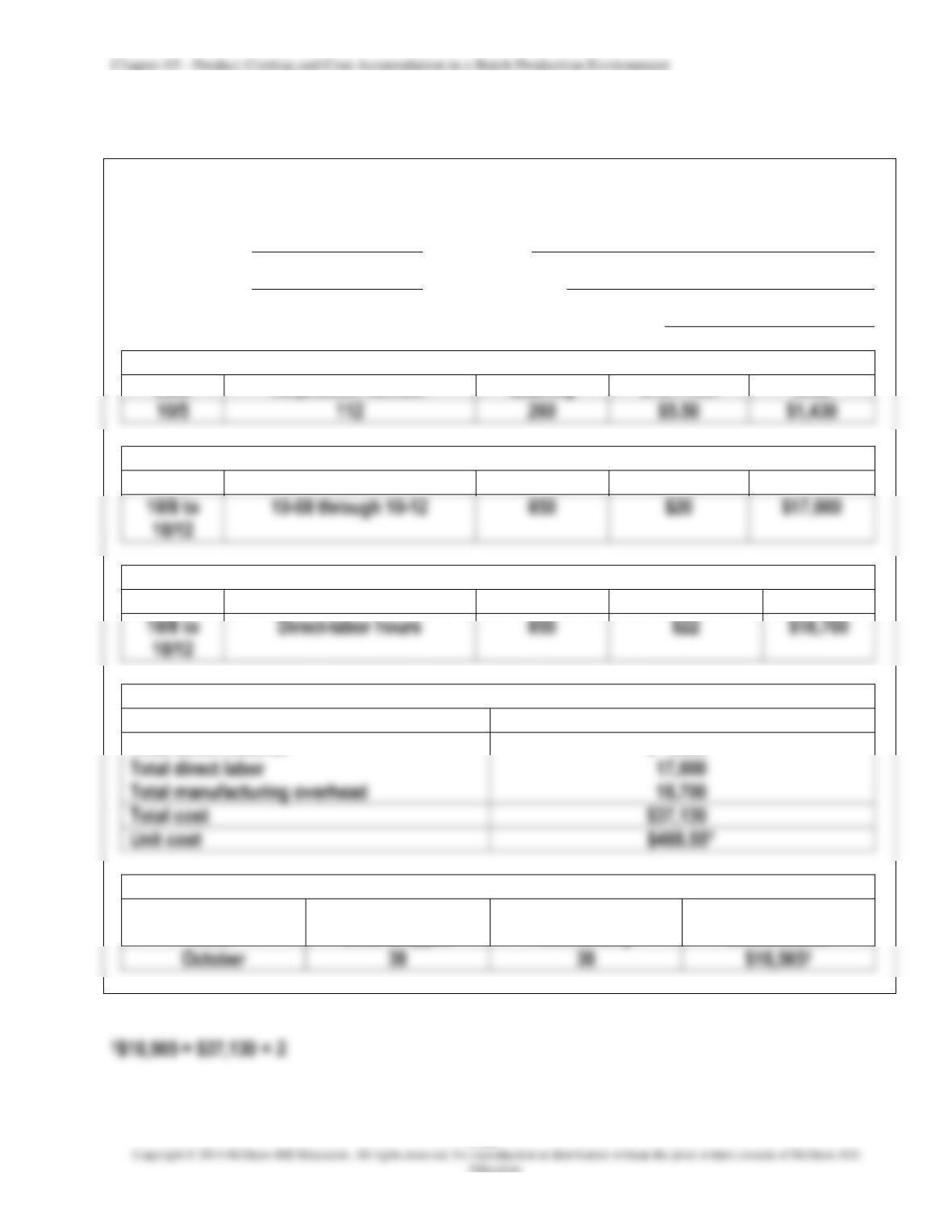

PROBLEM 3-59 (20 MINUTES)

JOB-COST RECORD

Job Number

T79

Description

Trombones

Date Started

October 5

Date Completed

October 20

Number of Units Completed

76

Direct Material

Date

Requisition Number

Quantity

Unit Price

Cost

$1,430

Direct Labor

Date

Time Card Number

Hours

Rate

Cost

Manufacturing Overhead

Date

Cost Driver (Activity Base)

Quantity

Application Rate

Cost

Cost Summary

Cost Item

Amount

Total cost

$37,130

Unit cost

$488.55*

Total direct material

$ 1,430

Shipping Summary

Date

Units Shipped

Units Remaining

In Inventory

Cost Balance

*Rounded

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-53

PROBLEM 3-60 (50 MINUTES)

1.

Schedule of budgeted overhead costs:

Department A

Department B

Variable overhead

A 21,000 $17 ………………………………………………

$357,000

Fixed overhead …………………………………………………….

Total overhead ……………………………………………………..

Grand total of budgeted overhead (A + B):

hours labor–direct budgeted total

rate overhead budgeted total

rate overhead nedPredetermi

=

2.

Product prices:

Basic

System

Advanced

System

Total cost ……………………………………………………………

$1,190

$1,640

Markup, 10% of cost …………………………………………….

3.

Departmental overhead rates:

Department A

Department B

Budgeted overhead

(from requirement 1) ………………………………………..

$567,000

$315,000

Budgeted direct-labor hours ………………………………..

Predetermined overhead rates ……………………………..

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-54

PROBLEM 3-60 (CONTINUED)

4.

Revised product costs:

Basic

Advanced

System

System

Direct material …………………………………………………….

$ 450

$ 900

Direct labor …………………………………………………………

Manufacturing overhead:

Department A:

Department B:

5.

Revised product prices:

Basic

Advanced

System

System

Total cost ……………………………………………………………

Markup, 10% of cost …………………………………………….

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-55

PROBLEM 3-60 (CONTINUED)

6.

COLORTECH CORPORATION

Memorandum

Date:

Today

To:

President, ColorTech Corporation

From:

I. M. Student

Subject:

Departmental overhead rates

Until now the company has used a single, plantwide overhead rate in computing product

costs. This approach resulted in a product cost of $1,190 for the basic system and a cost of

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-56

SOLUTIONS TO CASES

CASE 3-61 (45 MINUTES)

1.

A job order costing system is appropriate in any environment where costs can be

readily identified with specific products, batches, contracts, or projects.

2.

The only job remaining in KidCo’s Work–in-Process Inventory on December 31 is

DRS114. The dollar value of DRS114 is calculated as follows:

DRS114 balance, 11/30 ……………………………………………….

$250,000

December additions:

Direct material used ……………………………………………

$124,000

Purchased parts …………………………………………………

Direct labor ………………………………………………………..

$807,750

3.

The dollar value of the playpens remaining in KidCo’s finished-goods inventory on

December 31 is $455,600, calculated as follows:

Playpen Units

Finished-goods inventory, 11/30 …………………………………………………..

19,400

Units completed in December ……………………………………………………….

15,000

Units available for sale …………………………………………………………………

34,400

Units shipped in December …………………………………………………………..

21,000

3-57

CASE 3-61 (CONTINUED)

Since KidCo uses the FIFO inventory method, all units remaining in finished- goods

Unit cost of playpens completed in December:

Work in process inventory, 11/30 ………………………………

$420,000

December additions:

Direct material used ……………………………………………..

Purchased parts …………………………………………………..

Direct labor ………………………………………………………….

Total cost …………………………………………………………………

$510,000

=

$34 per unit

=

$455,600

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-58

CASE 3-62 (50 MINUTES)

1.

Manufacturers use predetermined overhead rates to allocate to production jobs the

2.

The manufacturing overhead applied through November 30 is calculated as follows:

3.

The manufacturing overhead applied in December is calculated as follows:

4.

Underapplied manufacturing overhead through December 31 is calculated as follows:

Actual overhead ($2,200,000 + $192,000) …………………………………………….

Applied overhead ($2,190,000 + $180,000) …………………………..……………..

Underapplied overhead ……………………………………………………………………..

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-59

CASE 3-62 (CONTINUED)

5.

The balance in the Finished-Goods Inventory account on December 31 is comprised

only of Job No. N11-013 and is calculated as follows:

November 30 balance for Job No. N11-013 ……………………………………….

December direct material …………………………………………………………………

December direct labor ……………………………………………………………………..

Total finished-goods inventory ………………………………………………….

6.

Opticom’s Schedule of Cost of Goods Manufactured for the year just completed is

constructed as follows:

OPTICOM, INC.

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE YEAR ENDED DECEMBER 31

Direct material:

Raw-material inventory, 1/1 …………………………………….

$ 210,000

Raw-material purchases ($1,930,000 + $196,000) ……..

Raw material available for use ………………………………..

Deduct: Indirect material used ($250,000 + $18,000) ..

Raw-material inventory 12/31 …………………….

Raw material used ………………………………………………….

Direct labor ($1,690,000 + $160,000) …………………………...

Manufacturing overhead:

Indirect material ($250,000 + $18,000) ……………………..

Indirect labor ($690,000 + $60,000) ………………………….

Utilities ($490,000 + $44,000) …………………………………..

Depreciation ($770,000 + $70,000) …………………………..

Total actual manufacturing overhead ………………………

Deduct: Underapplied overhead ……………………………..

Overhead applied to work in process ………………………….

Total manufacturing costs …………………………………………

Add: Work-in-process inventory, 1/1 …………………………..

Subtotal …………………………………………………………………….

Deduct: Work-in-process inventory, 12/31* …………………

Cost of goods manufactured ………………………………………

Chapter 03 – Product Costing and Cost Accumulation in a Batch Production Environment

3-60

CASE 3-62 (CONTINUED)

*Supporting calculations for work in process 12/31:

D12-002

D12-003

Total

Direct material ………………..

$ 75,800

$ 52,000

$127,800

Direct labor …………………….

Applied overhead:

FOCUS ON ETHICS (See page 107 in the text.)

Did Boeing exploit accounting rules to conceal cost overruns and production snafus?

According to the circumstances alleged in the Business Week article cited in the text

(page 107), Boeing did not handle its cost overruns, production problems, and the merger