41

chapter

3

The Adjusting Process

______________________________________________

OPENING COMMENTS

Chapter 3 introduces students to the adjusting process. The beginning of the chapter briefly describes the

cash basis of accounting and includes examples of businesses that use it. The focus of the text is on the

accrual basis accounting. The basic idea of the matching concept was presented in Chapter 1, where

expenses incurred were matched against revenues. Now in Chapter 3, matching is introduced formally

After studying the chapter, your students should be able to:

2. Journalize entries for accounts requiring adjustment.

4. Prepare an adjusted trial balance.

5. Describe and illustrate the use of vertical analysis in evaluating a company’s performance and

financial condition.

KEY TERMS

accounting period concept

accrual basis of accounting

42 Chapter 3 The Adjusting Process

accrued expenses

accrued revenues

Accumulated Depreciation

adjusted trial balance

adjusting entries

adjusting process

book value of the asset (or net book value)

cash basis of accounting

STUDENT FAQS

• Why can’t we just do cash basis accounting?

• Why is unearned revenue a liability instead of a revenue account?

• Adjusting entries give me a headache. Can we just skip them?

• Why are adjusting entries done at the end of the accounting period instead of at the beginning?

• Expired and unexpired give me problems. Is there an easy way to understand them?

• Why is matching revenues and expenses so important?

• How can an expense item temporarily be treated as an asset? I thought an asset was something of

value or worth, not a cost of doing business.

• How can revenue temporarily be treated as a liability? I thought revenue was a good thing, not a debt

or obligation.

• Why can’t you debit depreciation expense and credit equipment? No other adjusting entry uses a

contra account.

Chapter 3 The Adjusting Process 43

• If you are going to deduct the contra account (accumulated depreciation) from the equipment account,

why not show equipment at the net value to start with?

• Now that I know about vertical analysis, what are some examples of when it’s better or more

informative to use one instead of the other or both?

OBJECTIVE 1

Describe the nature of the adjusting process.

SYNOPSIS

Accountants use generally accepted accounting principles called GAAP. The accounting period concept

requires that revenues and expenses be recorded in the proper period. The revenue recognition concept

and the matching concept require that revenue be reported when it is earned and related expenses be

reported in the same time period. Some businesses use the cash basis of accounting; in this method,

revenue is recorded when cash is received and expenses are recorded when the cash is paid. Small service

businesses that have few receivables and payables may use the cash basis.

At the end of the accounting period, a few accounts require updating. Expenses not recorded daily,

revenues and expenses incurred as time passes, and revenues and expenses that are unrecorded are all

accounts that need adjusted. These transactions are recorded at the end of the period prior to the financial

statements being prepared and are called adjusting entries. Prepaid expenses, accrued expenses, unearned

revenues, and accrued revenues are examples of accounts that require adjusting.

Key Terms and Definitions

• Accounting Period Concept – The accounting concept that assumes that the economic life of the

business can be divided into time periods.

• Accrual Basis of Accounting – Under this basis of accounting, all revenues are recognized when

services have been performed or products have been delivered to customers and expenses are reported in

the period in they are incurred.

• Accrued Expenses – Expenses that have been incurred but not recorded in the accounts.

• Accrued Revenues – Revenues that have been earned but not recorded in the accounts.

44 Chapter 3 The Adjusting Process

• Adjusting Entries – The journal entries that bring the accounts up to date at the end of the

accounting period.

• Adjusting Process – An analysis and updating of the accounts when financial statements are

prepared.

• Cash Basis of Accounting – Under this basis of accounting, revenues and expenses are reported

in the income statement in the period in which cash is received or paid.

Relevant Example Exercises and Exhibits

• Example Exercise 3-1 Accounts Requiring Adjustment

• Example Exercise 3-2 Type of Adjustment

• Exhibit 1 – Prepaid Expenses

• Exhibit 2 – Unearned Revenues

• Exhibit 3 – Accrued Revenues

• Exhibit 4 – Accrued Expenses

SUGGESTED APPROACH

Under this objective, you will need to revisit the matching concept from Chapter 1. Emphasize again that

the matching concept is necessary in order to match revenues and expenses in the proper accounting

period. If the concept is violated, the financial statements for the period will not be accurate. The

adjusting process discussed in this chapter is critical to conforming to the matching concept.

To check your students’ understanding of these concepts, pose the following questions:

If rent for May is paid on June 1, in which month will it be reported as an expense under

(a) the cash basis and (b) the accrual basis? Answer: (a) June, (b) May.

GROUP LEARNING ACTIVITY—Introduction to the Matching Concept

TM 3-1 provides financial information about an individual filling out a loan application. The loan

application asks for total monthly expenses. The person applying for the loan has a few expenses that are

Chapter 3 The Adjusting Process 45

paid annually or semiannually. Therefore, your students must “match” expenses to the time period

requested by the loan application: one month. The expenses paid annually and semiannually must be

divided into monthly amounts to properly determine the applicant’s total monthly expenses.

The solution to this exercise is provided in TM 3-2.

LECTURE AID—Matching Concept

Remind your students that, similar to personal expenses, not all business expenses are paid monthly. If a

business wants to know its true expenses for the month, it must consider all expenses incurred, not just

the expenses paid that month.

Likewise, payment for services provided to customers is not always received in the same month that the

service is completed. If a business wants to know how much revenue it has earned, it must determine the

value of services provided, not just the cash received in payment for services rendered.

GROUP LEARNING ACTIVITY—Reviewing the Matching Concept

TM 3-3 asks students to apply the matching concept by determining the profit on a stone patio laid by

Artisan Stone and Brick. TM 3-4 provides the solution to this exercise.

LECTURE AID—Accruals and Deferrals

Deferrals adjust accounts that are already a part of a company’s accounting records.

46 Chapter 3 The Adjusting Process

Deferred expenses occur when an asset that will be used up or will expire is purchased. As this asset is

used, its cost must be recorded as an expense. Therefore, you defer recording the cost of the asset as an

expense until it is used. An example of a deferred expense for a student is tuition paid at the beginning of

each term. Business examples of deferred expenses include the following:

1. Supplies—These are recorded as an asset when they are purchased. As the supplies are used, an

adjusting entry is made to transfer the cost of the supplies to an expense account.

2. Prepaid insurance—When an insurance policy is paid in advance of the period covered, its cost is

recorded as an asset. An adjusting entry must be made to transfer the cost of the insurance policy to

an expense account as the policy expires.

Revenues are deferred when cash is received from a customer before a business completes its service for

the customer or delivers its product. When cash is received under these circumstances, it cannot be

recorded as revenue, since it has not been earned. Instead, it is recorded as a liability, reflecting the

1. Accrued expenses—salaries/wages owed to employees at the end of an accounting period that have

not been paid; interest owed on loans that have not been paid.

TM 3-5 provides a summary of deferrals and accruals. This TM can be used as a handout for students to

review these concepts.

Chapter 3 The Adjusting Process 47

OBJECTIVE 2

Journalize entries for accounts requiring adjustment.

SYNOPSIS

The previous objective showed the overall nature and process of adjusting. This objective shows the

journal entries and how they affect the trial balance. Starting with the unadjusted trial balance for

NetSolutions, this objective shows the how the adjustments change the balances of the accounts while

keeping the debits and credits in the new adjusted trial balance equal. Using supplies and prepaid

insurance as examples of prepaid expenses, this objective demonstrates how to calculate how much of

these assets have been used up and how to journalize this transaction. Without these adjustments,

expenses would be understated. Unearned revenue accounts must be adjusted to account for revenue that

has been earned in this period. Accrued revenues and expenses must also be recorded to update these

accounts. The last type of account to be adjusted is depreciation expense. This involves the use of fixed or

Key Terms and Definitions

• Accumulated Depreciation – The contra asset account credited when recording the depreciation

of a fixed asset.

• Book Value of the Asset (or Net Book Value) – The difference between the cost of a fixed asset

and its accumulated depreciation.

• Contra Accounts (or Contra Asset Accounts) – An account offset against another account.

• Depreciate – To lose usefulness as all fixed assets except land do.

• Depreciation – The systematic periodic transfer of the cost of a fixed asset to an expense account

during its expected useful life.

Relevant Example Exercises and Exhibits

• Example Exercise 3-3 Adjustment for Prepaid Expense

• Example Exercise 3-4 Adjustment for Unearned Revenue

• Example Exercise 3-5 Adjustment for Accrued Revenues

• Example Exercise 3-6 Adjustment for Accrued Expense

48 Chapter 3 The Adjusting Process

• Example Exercise 3-7 Adjustment for Depreciation

• Exhibit 5 – Unadjusted Trial Balance for NetSolutions

• Exhibit 6 – Expanded Chart of Accounts for NetSolutions

• Exhibit 7 – Accrued Wages

SUGGESTED APPROACH

Adjusting entries can be effectively presented to your class by working through an example of each

adjusting entry covered in the text. Or, you may choose to work a problem opposite an assigned

DEMONSTRATION PROBLEM—Adjusting Entry for Prepaid Insurance

An example of an expense that is typically paid in advance is insurance. Insurance policies are paid at the

beginning of a policy period. This outlay of cash is recorded in Prepaid Insurance—an asset account. The

portion of the insurance coverage that has expired by the end of the accounting period must be transferred

Graphically, this can be illustrated as follows:

New Data

Asset: Prepaid Expense: Insurance

Insurance Amount of Insurance Expense

Coverage Expired

For example, on December 1, Atherton Plumbing purchased a six-month insurance policy for $600. As of

December 31, one month (or $100) of that coverage had expired.

Original Prepaid Insurance……… 600

Chapter 3 The Adjusting Process 49

The T accounts follow:

Prepaid Insurance Insurance Expense

12/1 600

Adj. 100 Adj. 100

DEMONSTRATION PROBLEM—Adjusting Entry for Supplies

Another asset that must be adjusted at the end of the accounting period is the supplies account. All

supplies are recorded in the supplies account as they are purchased. By the end of the accounting period,

some of the supplies will have been used. The supplies used must be taken out of the supplies account and

transferred to an expense account.

Graphically, this can be illustrated as follows:

New Data

Asset: Supplies Expense: Supplies

Amount of Supplies Expense

That Have Been Used

For example, on December 5, Atherton Plumbing purchased $250 in supplies. As of December 31, only

$50 worth of those supplies was left.

Original Supplies………….…. 250

Entry: Cash………………… 250

The T accounts follow:

Supplies Supplies Expense

12/5 250 Adj. 200 Adj. 200

Bal. 50

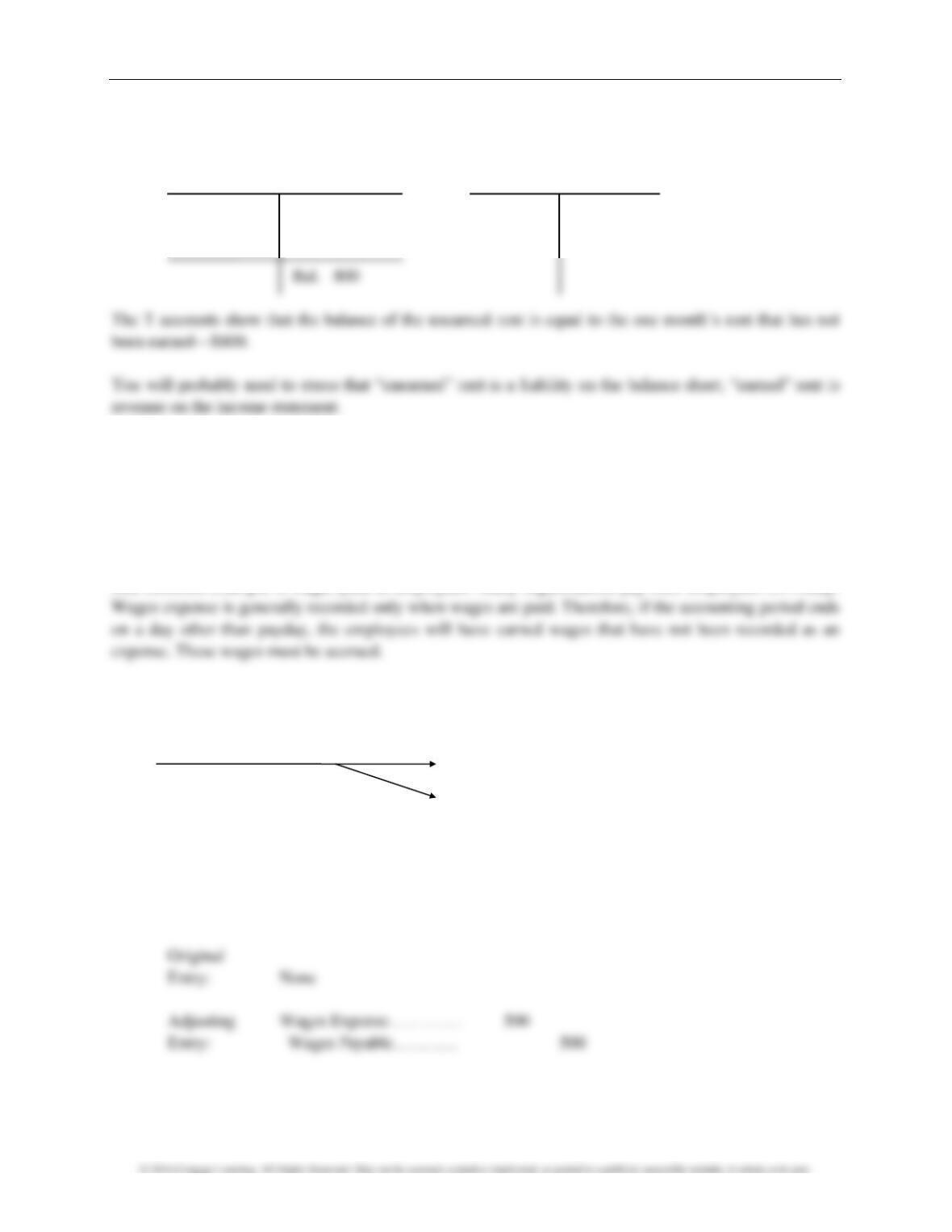

The T accounts show that the balance of the supplies account is $50—the amount of supplies left.

50 Chapter 3 The Adjusting Process

To illustrate why businesses typically count the amount of supplies left at the end of the month and use

that information to determine the cost of supplies used, ask your students the following question:

What is the easiest way to determine how many miles you have driven your car this

month? Answer: Record the beginning and ending odometer readings. This is easier than

DEMONSTRATION PROBLEM—Adjusting Entry for Unearned Revenue

If payment for goods or services is received before the goods are delivered or the service is performed, it

cannot be recognized as revenue. Revenue can be recorded only after it is earned. Therefore, when

payment is received in advance, it is recorded in an unearned revenue account. This is a liability account.

Graphically, this can be illustrated as follows:

New Data

Liability: Unearned Revenue: Fees Earned

Revenue Amount of Revenue (or other revenue

That Has Been Earned earned account

as appropriate)

For example, on November 2, Huber Rental Properties received three months’ rent, totaling $2,400, in

advance for one of its commercial properties. As of December 31, two months’ worth of this rent had

been earned.

Original Cash……………………. 2,400

Entry: Unearned Rent……….. 2,400

Chapter 3 The Adjusting Process 51

The T accounts follow:

Unearned Rent Rent Revenue

Adj. 1,600 11/2 2,400 Adj. 1,600

DEMONSTRATION PROBLEM—Adjusting Entry for Accrued Expenses

Any expenses that a business has incurred must be recorded before preparing financial statements in order

to get a true measure of profitability. The act of recording expenses that have not been paid is called

accruing expenses.

One common example is wages paid to employees. Many organizations pay their employees on Friday.

Graphically, this can be illustrated as follows:

New Data

Expense: Wages Expense

Amount of Wages

That Employees Have Liability: Wages Payable

Earned

For example, assume that December 31 is a Wednesday. On that date, Huber Rental Properties owes $500

in wages to employees. These wages will be paid on Friday, the usual payday.