Case 03-62 Student Name:

Class:

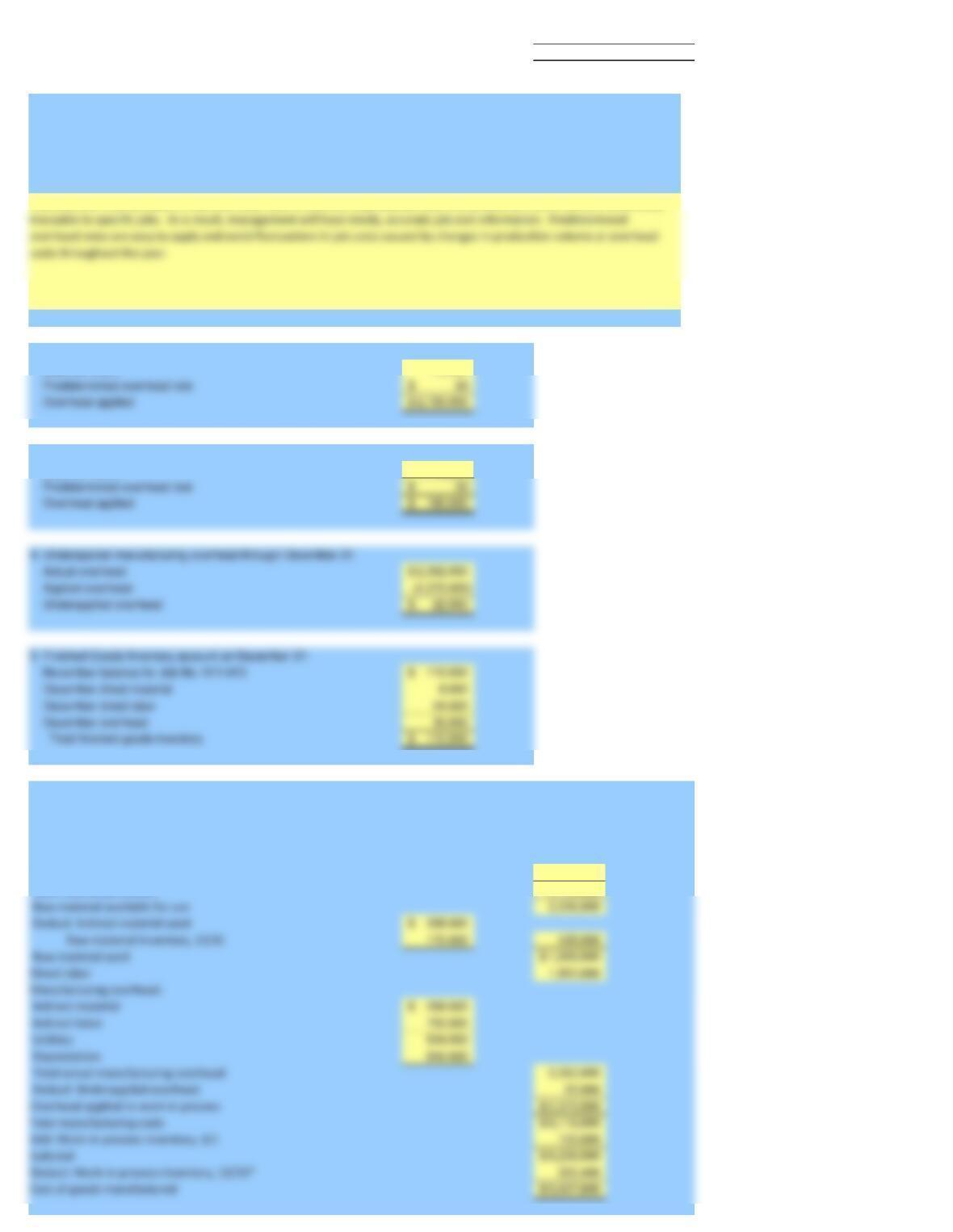

Opticom, Inc.

Requirements 1 – 6

1. Explain why manufacturers use a predetermined overhead rate to

apply manufacturing overhead to their jobs.

2. Manufacturing overhead applied through November 30:

Machine hours

*

Predetermined overhead rate

*

Overhead applied

*

3. Manufacturing overhead applied in December:

Machine hours

*

Predetermined overhead rate

*

Overhead applied

*

4. Underapplied manufacturing overhead through December 31:

Actual overhead

*

Applied overhead

*

Underapplied overhead

*

5. Finished-Goods Inventory account on December 31:

November balance for Job No. N11-013

*

December direct material

*

December direct labor

*

December overhead

*

Total finished-goods inventory

*

Direct material:

Raw-material inventory, 1/1 *

Raw material purchases *

Raw material available for use *

Deduct: Indirect material used *

Raw-material inventory, 12/31 * *

For the Year Ended December 31

Opticom, Inc.

Schedule of Cost of Goods Manufactured

Raw material used *

Direct labor *

Manufacturing overhead:

Indirect material *

Indirect labor *

Utilities *

Depreciation *

Total actual manufacturing overhead *

Deduct: Underapplied overhead *

Overhead applied to work in process *

Total manufacturing costs *

Add: Work-in-process inventory, 1/1 *

Subtotal *

Deduct: Work-in-process inventory, 12/31* *

Cost of goods manufactured *

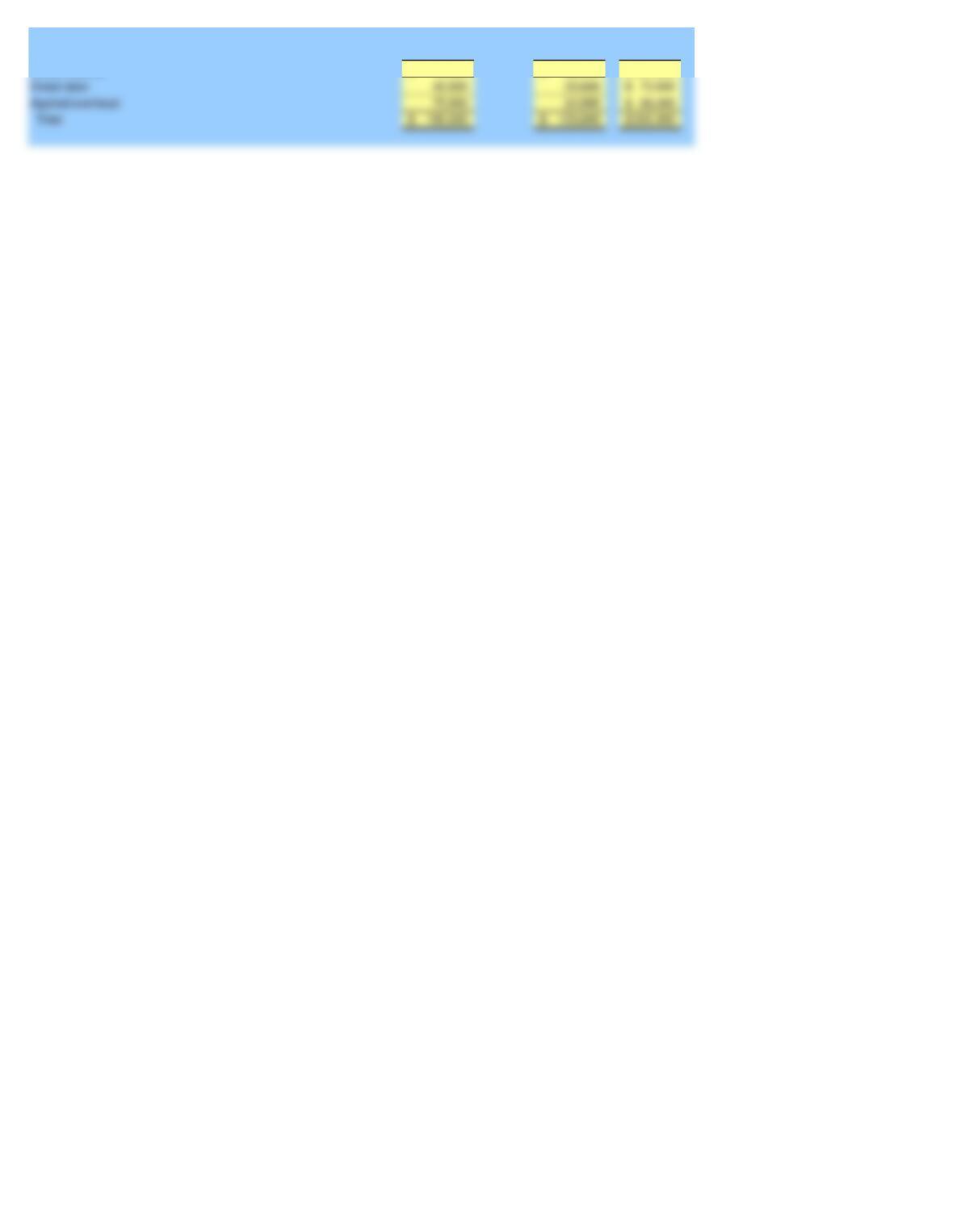

*Supporting calculations for work-in-process, 12/31

D12-002 D12-003 Total

Direct material

* * *

Direct labor

* * *

Applied overhead

* * *

Total

* * *

1

Case 03-62 Student Name:

Class:

Opticom Inc., Inc.

Requirements 1 – 6

1. Explain why manufacturers use a predetermined overhead rate to

apply manufacturing overhead to their jobs.

2. Manufacturing overhead applied through November 30:

Machine hours 73,000

3. Manufacturing overhead applied in December:

Machine hours 6,000

Direct material:

Raw-material inventory, 1/1 210,000$

Raw material purchases 2,126,000

Raw material available for use 2,336,000

Deduct: Indirect material used 268,000$

Raw material used 1,898,000$

Direct labor 1,850,000

Manufacturing overhead:

Indirect material 268,000$

Indirect labor 750,000

Utilities 534,000

Depreciation 840,000

Total actual manufacturing overhead 2,392,000

Deduct: Underapplied overhead 22,000

Overhead applied to work in process 2,370,000$

For the Year Ended December 31

Instructor

McGraw-Hill/Irwin

Manufacturers use predetermined overhead rates to allocate to production jobs the production costs that are not directly

Opticom, Inc.

Schedule of Cost of Goods Manufactured

*Supporting calculations for work-in-process, 12/31

D12-002 D12-003 Total

Direct material 75,800$ 52,000$ 127,800$