3-61 Ch. 3—Problems

Problem 3-14, Concluded

Eliminations and Adjustments:

PROBLEM 3-15

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ……………………………………. $800,000 $800,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary ………….. $800,000 $800,000 N/A

Less book value of interest acquired:

Common stock ($1 par) ……… $100,000

Paid-in capital in excess of par 200,000

Problem 3-15, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($65,000 fair –

$60,000 book value) ………….. $ 5,000 debit D1

Land ($100,000 fair –

$50,000 book value) ………….. 50,000 debit D2

Mortgage payable ($205,000

fair – $200,000 book value) … (5,000) credit D3 5 $(1,000)

(2) Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory ……………………. 1 $ 5,000 $ — $ 5,000 $ 5,000 (D1)

Subject to amortization:

Mortgage payable ……….. 5 $ (1,000) $ (1,000) $(1,000) $ (2,000) (A3)

Subsidiary Fast Air Company Income Distribution

Current-year amortizations ………… $9,500 Internally generated net

income …………………………… $67,500

Parent Fast Cool Company Income Distribution

Internally generated net

3-63 Ch. 3—Problems

Problem 3-15, Continued

Fast Cool Company and Subsidiary Fast Air Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Fast Cool Fast Air Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………….. 396,000 99,000 ………… ………… ….…….. ………… ………… 495,000

Buildings …………………………………………………….. 1,200,000 400,000 (D4) 150,000 ………… ………… ………… ………… 1,750,000

Accumulated Depreciation …………………………….. (200,000) (85,000) ………… (A4 15,000 ………… ………… ………… (300,000)

Equipment ………………………………………………….. 140,000 150,000 ………… (D5) 20,000 ………… ………… ………… 270,000

Accumulated Depreciation …………………………….. (80,000) (78,000) (A5) 8,000 ………… ………… ………… ………… (150,000)

Patent ………………………………………………………… ………… 24,000 (D6) 10,000 (A6) 4,000 …….….. ………… ………… 30,000

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

Common Stock ($1 par)—Fast Cool ………………. (100,000) ………… ………… ………… ………… .……….. ………… (100,000)

Paid-In Capital in Excess of Par—Fast Cool ……. (1,500,000) ………… ………… ………… ………… ………… ………… (1,500,000)

Retained Earnings—Fast Cool ………………………. (680,500) ………… ………… ………… ………... ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

Subsidiary (Dividend) Income ………………………… (67,500) ………… (CY1) 67,500 ………… ………… ………… ………… …………

Dividends Declared—Fast Air ……………………….. ………… 10,000 ………… (CY2) 10,000 ………… ..………. ………… …………

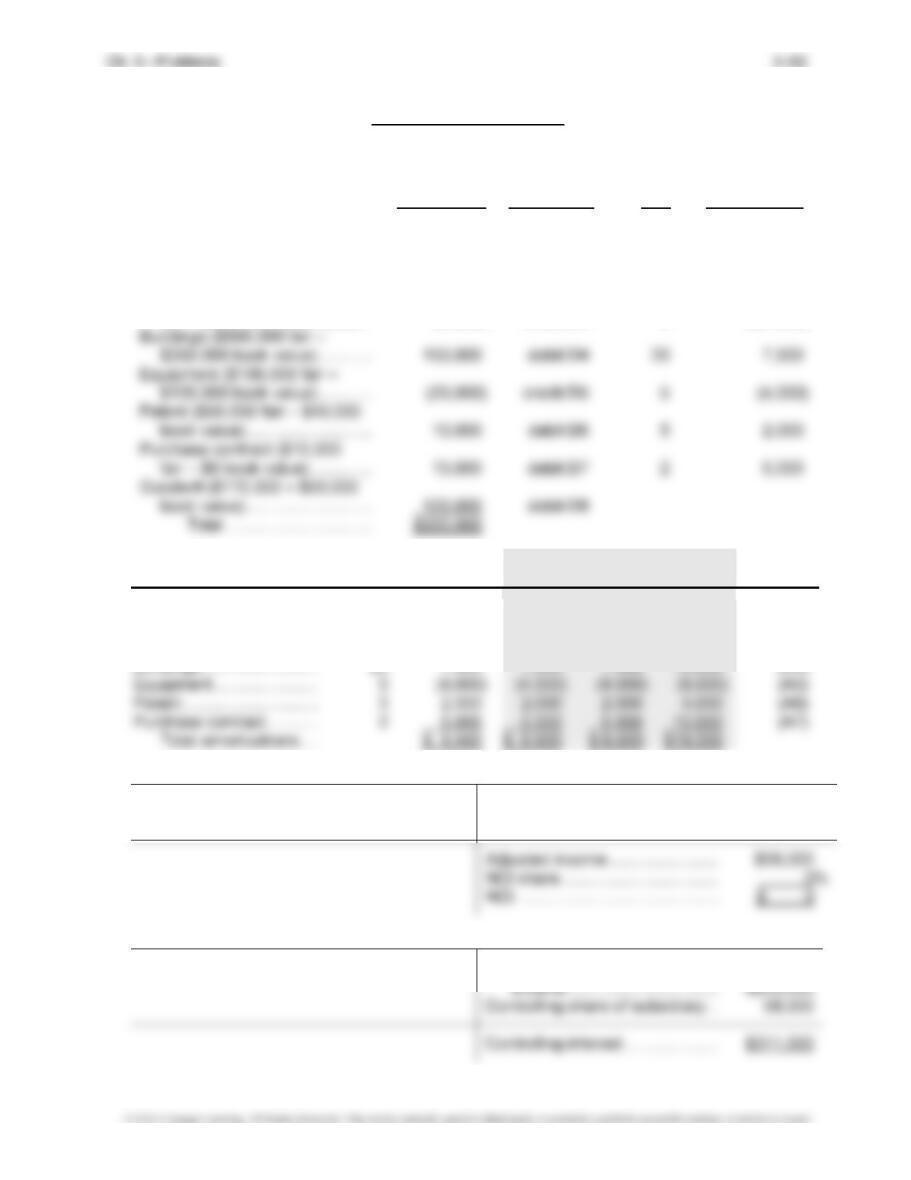

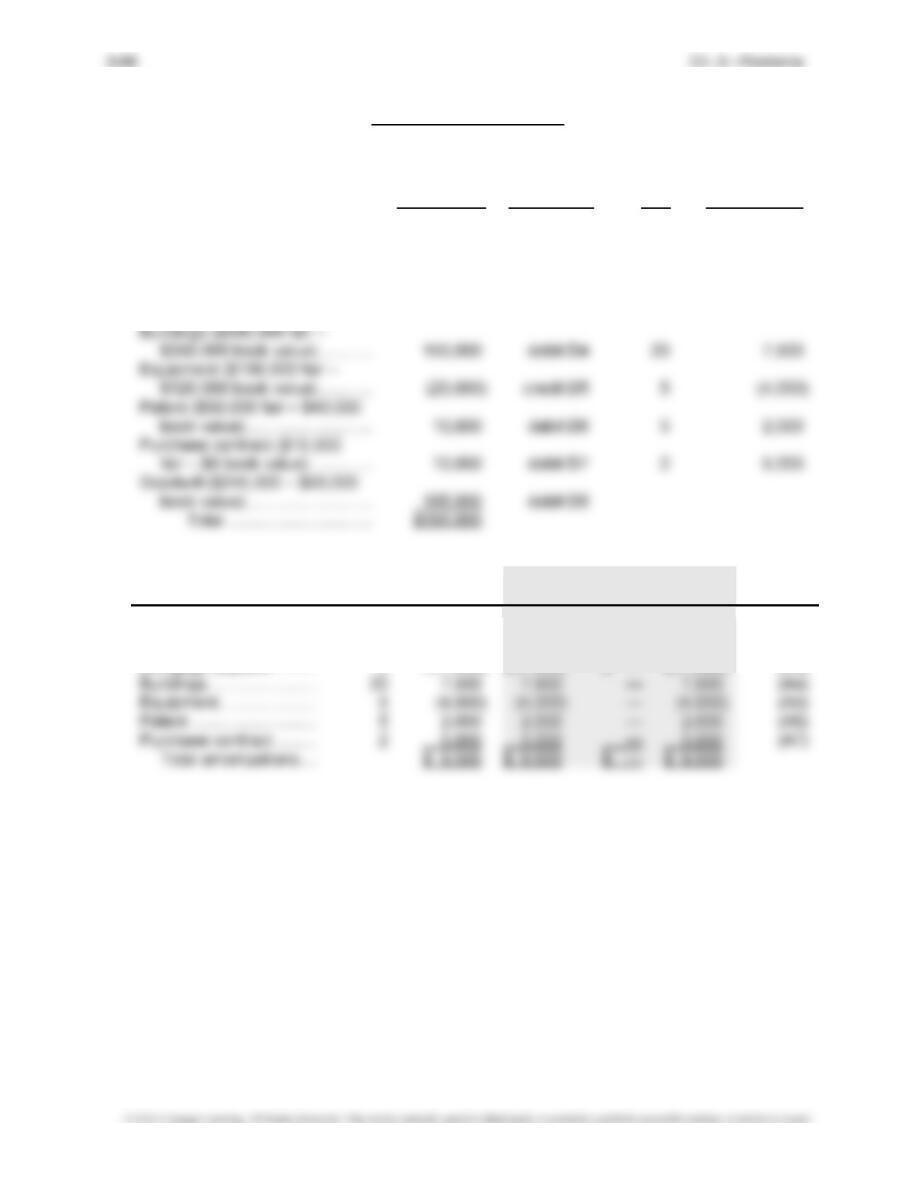

Problem 3-15, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

PROBLEM 3-16

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ……………………………………. $500,000 $500,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Price paid for investment ……….. $500,000 $500,000 N/A

Less book value of interest acquired:

Common stock ($1 par) ………. $100,000

3-65 Ch. 3—Problems

Problem 3-16, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($65,000 fair –

$60,000 book value) ………….. $ 5,000 debit D1

Land ($100,000 fair – $50,000

book value) ………………………. 50,000 debit D2

Mortgage payable ($205,000

fair – $200,000 book value) … (5,000) credit D3 5 $(1,000)

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ 5,000 $ — $ 5,000 $ 5,000 (D1)

Subject to amortization:

Mortgage payable ………. 5 $ (1,000) $ (1,000) $(1,000) $ (2,000) (A3)

Buildings …………………… 20 7,500 7,500 7,500 15,000 (A4)

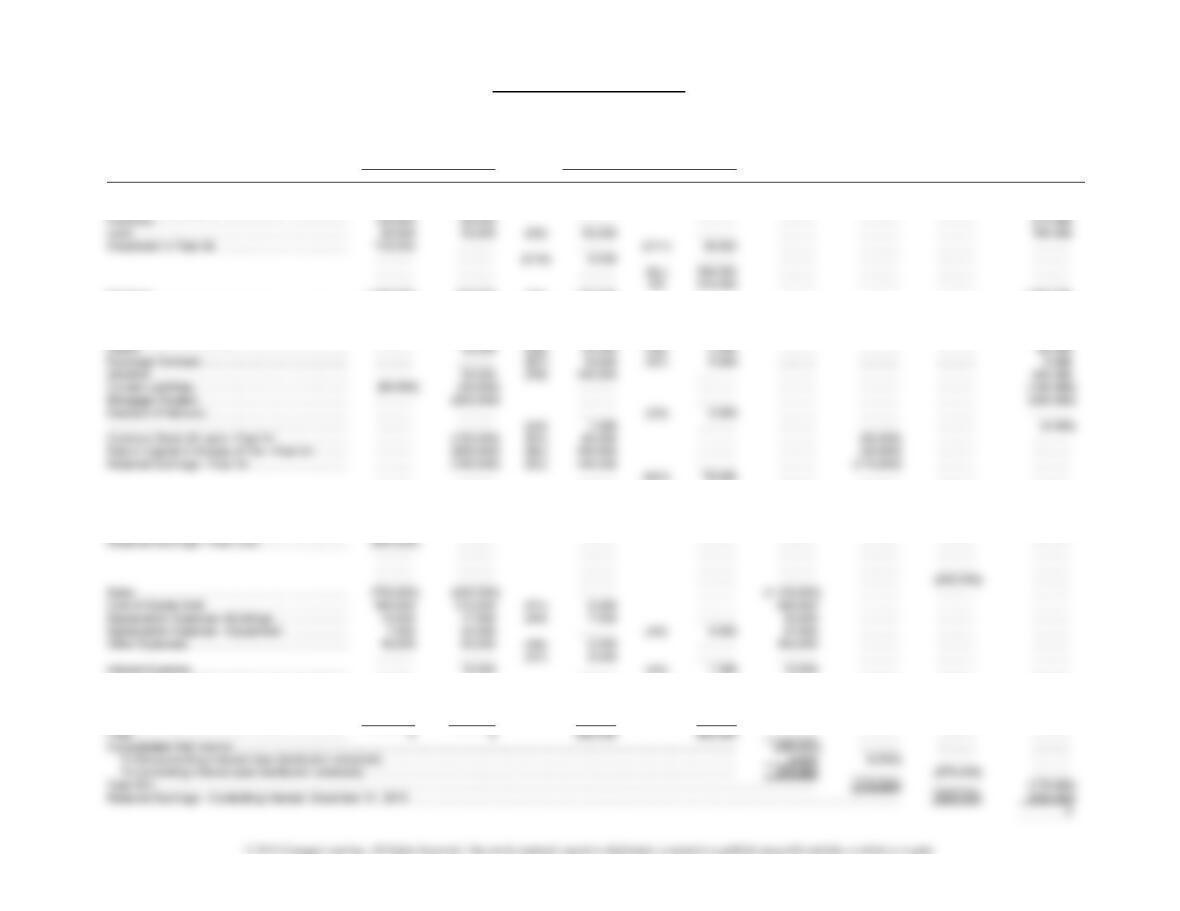

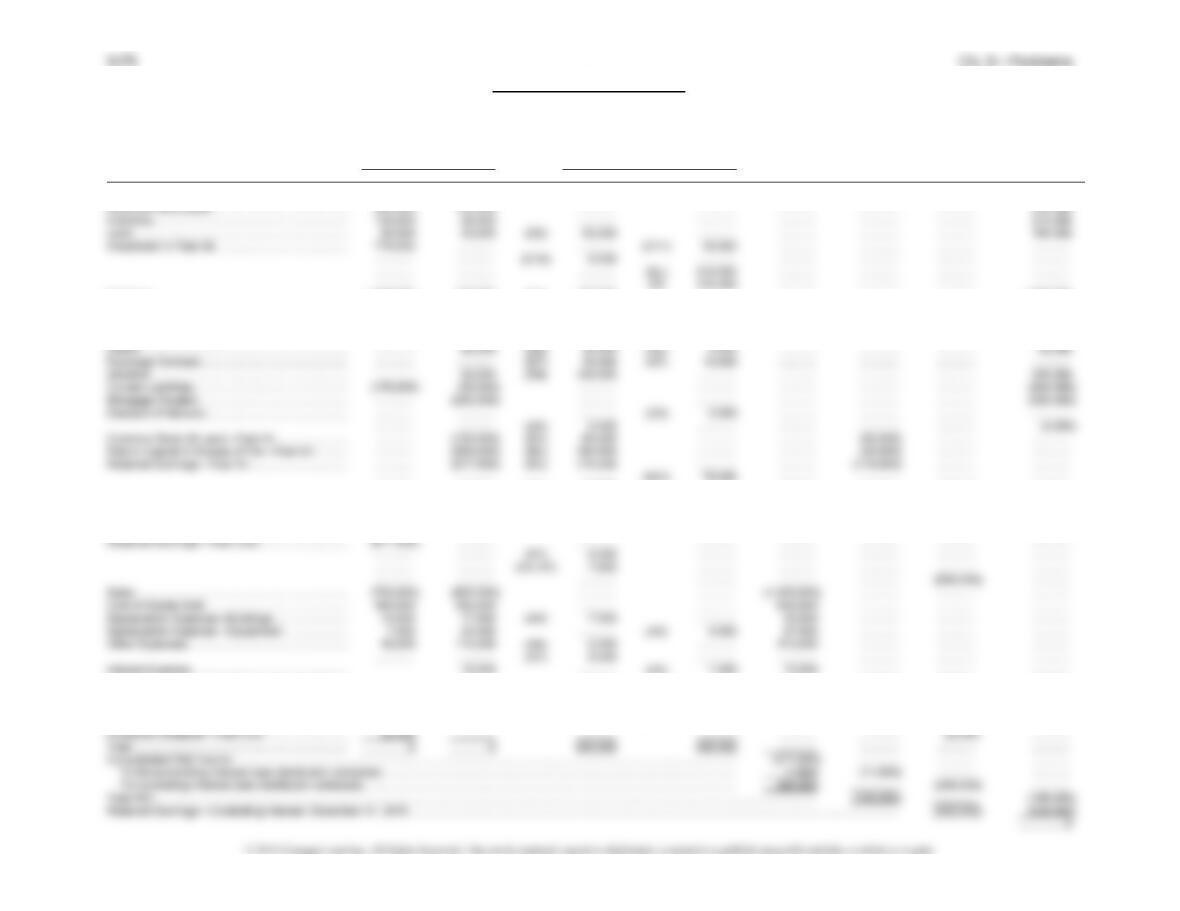

Problem 3-16, Continued

Subsidiary Fast Air Company Income Distribution

Current-year amortizations ………… $9,500 Internally generated net

income …………………………… $67,500

Adjusted income …………………… $58,000

Parent Fast Cool Company Income Distribution

Internally generated net

income …………………………… $253,000

Problem 3-16, Continued

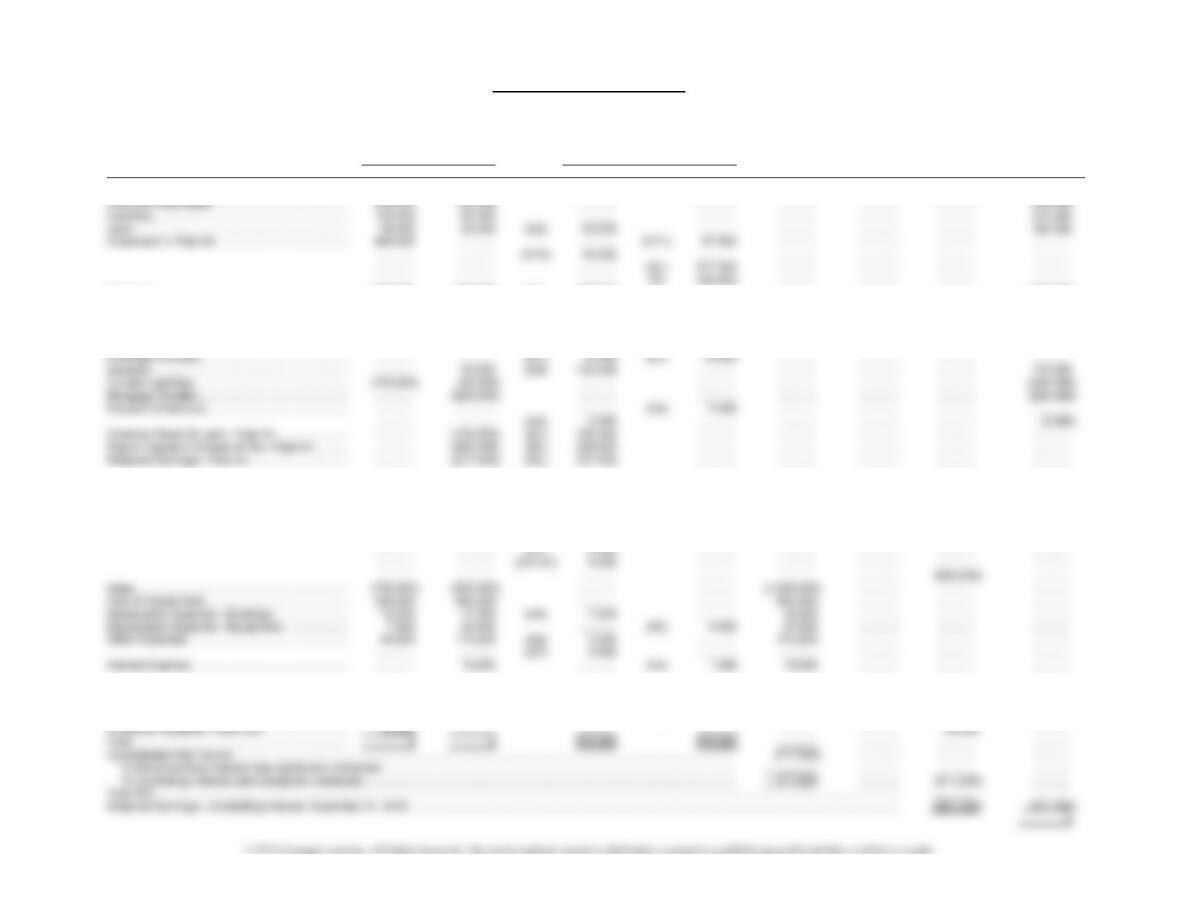

Fast Cool Company and Subsidiary Fast Air Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Fast Cool Fast Air Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………….. 396,000 99,000 ………… ………… ….…….. ………… ………… 495,000

Accounts Receivable ……………………………………. 200,000 120,000 ………… ………… ………… ………… ………… 320,000

Buildings …………………………………………………….. 1,200,000 400,000 (D4) 150,000 ………… ………… ………… ………… 1,750,000

Accumulated Depreciation …………………………….. (200,000) (85,000) ………… (A4) 15,000 ………… ………… ………… (300,000)

Equipment ………………………………………………….. 140,000 150,000 ………… (D5) 20,000 ………… ………… ………… 270,000

Accumulated Depreciation …………………………….. (80,000) (78,000) (A5) 8,000 ………… ………… ………… ………… (150,000)

…………. ………… ………… ………… ………… ………… ………… …………

…………. ………… ………… ………… ………… ………… ………… …………

Common Stock ($1 par)—Fast Cool ………………. (85,000) ………… ………… ………… ………… ..………. ………… (85,000)

Paid-In Capital in Excess of Par—Fast Cool ……. (1,215,000) ………… ………… ………… ………… ………… ………… (1,215,000)

Retained Earnings—Fast Cool ………………………. (680,500) ………… ………… (D9) 130,000 ………… ………… ………… …………

Interest Expense …………………………………………. …………. 16,000 ………… (A3) 1,000 15,000 ………… ………… …………

…………. ………… ………… ………… ………… ………… ………… …………

Subsidiary (dividend) Income ………………………… (67,500) ………… (CY1) 67,500 ………… ………… ………… ………… …………

Dividends Declared—Fast Air ……………………….. ………… 10,000 ………… (CY2) 10,000 ………… ..………. ………… …………

Dividends Declared—Fast Cool …………………….. 20,000 ………… ………… ………… ………… ………… 20,000 …………

Problem 3-16, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

PROBLEM 3-17

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $875,000 $700,000 $175,000

Less book value of interest acquired:

Common stock ($1 par) ……… $100,000

Paid-in capital in excess of par 200,000

Problem 3-17, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($65,000 fair –

$60,000 book value) ………….. $ 5,000 debit D1 1

Land ($100,000 fair – $50,000

book value) ………………………. 50,000 debit D2

Mortgage payable ($205,000

fair – $200,000 book value) … (5,000) credit D3 5 $(1,000)

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ 5,000 $ 5,000 $ — $ 5,000 (D1)

Subject to amortization:

Mortgage payable ………. 5 $ (1,000) $ (1,000) $ — $ (1,000) (A3)

Problem 3-17, Continued

Subsidiary Fast Air Company Income Distribution

Inventory adjustment ………………… $5,000 Internally generated net

Current-year amortizations ………… 9,500 income …………………………… $47,500

Parent Fast Cool Company Income Distribution

Internally generated net

income …………………………… $253,000

3-71 Ch. 3—Problems

Problem 3-17, Continued

Fast Cool Company and Subsidiary Fast Air Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Fast Cool Fast Air Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………….. 145,000 37,000 ………… ………… ….…….. ………… ………… 182,000

Accounts Receivable ……………………………………. 70,000 100,000 ………… ………… ………… ………… ………… 170,000

Buildings …………………………………………………….. 1,200,000 400,000 (D4) 150,000 ………… ………… ………… ………… 1,750,000

Accumulated Depreciation …………………………….. (176,000) (67,500) ………… (A4) 7,500 ………… ………… ………… (251,000)

Equipment ………………………………………………….. 140,000 150,000 ………… (D5) 20,000 ………… ………… ………… 270,000

Accumulated Depreciation …………………………….. (68,000) (54,000) (A5) 4,000 ………… ………… ………… ………… (118,000)

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

Common Stock ($1 par)—Fast Cool ………………. (95,000) ………… ………… ………… ………… ..………. ………… (95,000)

Paid-In Capital in Excess of Par—Fast Cool ……. (1,405,000) ………… ………… ………… ………… ………… ………… (1,405,000)

………… ………… ………… ………… ………… ………… ………… …………

Subsidiary (Dividend) Income ……………………….. (38,000) ………… (CY1) 38,000 ………… ………… ………… ………… …………

Dividends Declared—Fast Air ……………………….. ………… 10,000 ………… (CY2) 8,000 ………… 2,000 ………… …………

Dividends Declared—Fast Cool …………………….. 20,000 ………… ………… ………… ………… ………… 20,000 …………

Problem 3-17, Concluded

Eliminations and Adjustments:

PROBLEM 3-18

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ……………………………………. $875,000 $700,000 $175,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $875,000 $700,000 $175,000

Less book value of interest acquired:

Common stock ($1 par) ………. $100,000

3-73 Ch. 3—Problems

Problem 3-18, Continued

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($65,000 fair –

$60,000 book value) ………….. $ 5,000 debit D1 1

Mortgage payable ($205,000

fair – $200,000 book value) … (5,000) credit D3 5 $(1,000)

Land ($100,000 fair –

$50,000 book value) ………….. 50,000 debit D2

(2)

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Inventory …………………… 1 $ 5,000 $ — $ 5,000 $ 5,000 (D1)

Subject to amortization:

Mortgage payable ………. 5 $ (1,000) $ (1,000) $(1,000) $ (2,000) (A3)

Buildings …………………… 20 7,500 7,500 7,500 15,000 (A4)

Equipment…………………. 5 (4,000) (4,000) (4,000) (8,000) (A5)

Problem 3-18, Continued

Subsidiary Fast Air Company Income Distribution

Current-year amortizations ………… $9,500 Internally generated net

income …………………………… $67,500

Parent Fast Cool Company Income Distribution

Internally generated net

income …………………………… $253,000

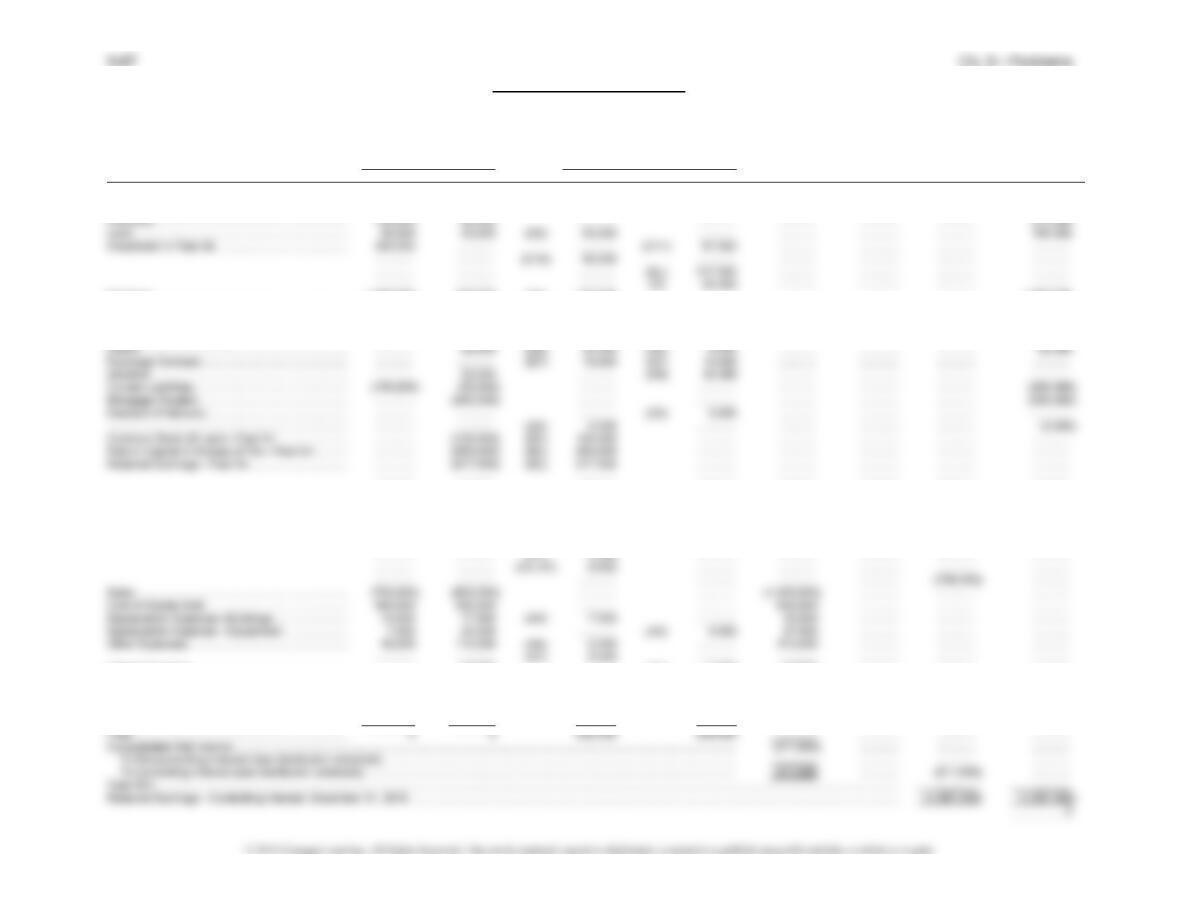

Problem 3-18, Continued

Fast Cool Company and Subsidiary Fast Air Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Fast Cool Fast Air Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………….. 392,000 99,000 ………… ………… ….…….. ………… ………… 491,000

Buildings …………………………………………………….. 1,200,000 400,000 (D4) 150,000 ………… ………… ………… ………… 1,750,000

Accumulated Depreciation …………………………….. (200,000) (85,000) ………… (A4) 15,000 ………… ………… ………… (300,000)

Equipment ………………………………………………….. 140,000 150,000 ………… (D5) 20,000 ………… ………… ………… 270,000

Accumulated Depreciation …………………………….. (80,000) (78,000) (A5) 8,000 ………… ………… ………… ………… (150,000)

………… ………… (D1) 1,000 ………… ………… ………… ………… …………

………… ………… (A3–A7) 1,900 ………… ………… ………… ………… …………

Common Stock ($1 par)—Fast Cool ………………. (95,000) ………… ………… ………… ………… ..………. ………… (95,000)

Paid-In Capital in Excess of Par—Fast Cool ……. (1,405,000) ………… ………… ………… ………… ………… ………… (1,405,000)

………… ………… ………… ………… ………… ………… ………… …………

………… ………… ………… ………… ………… ………… ………… …………

Subsidiary (Dividend) Income ………………………… (54,000) ………… (CY1) 54,000 ………… ………… ………… ………… …………

Dividends Declared—Fast Air ……………………….. ………… 10,000 ………… (CY2) 8,000 ………… 2,000 ………… …………

Ch. 3—Problems 3–76

Problem 3-18, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

3-77 Ch. 3—Problems

APPENDIX PROBLEMS

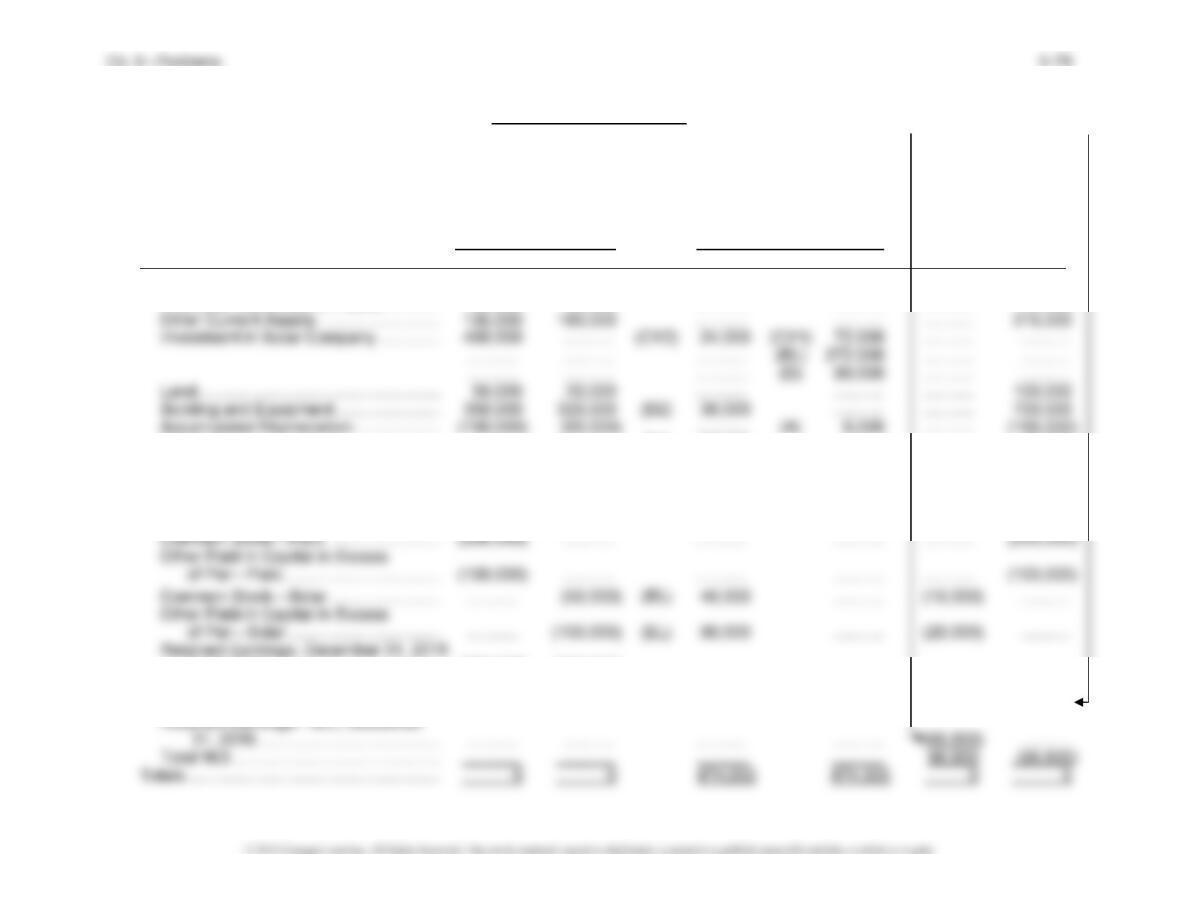

(1) See part (1) of solution to Problem 3-2.

(2) Paro Company and Solar Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Paro Solar Dr. Cr. Interest dated

Income Statement:

Net Sales ………………………………………. (520,000) (450,000) ……….. ……….. ……….. (970,000)

Cost of Goods Sold ………………………… 300,000 260,000 ……….. ……….. ……….. 560,000

Operating Expenses ……………………….. 120,000 100,000 (A) 3,000 ……….. ……….. 223,000

distribution schedule) ………………… ……….. ……….. ……….. ……….. ……….. (169,600)

Retained Earnings Statement:

Balance, January 1, 2016—Paro ……… (214,000) ……….. (D1) 8,000 ……….. ……….. ………..

………………………………………………. ……….. ……….. (A) 2,400 ……….. ……….. (203,600)

Balance, January 1, 2016—Solar …….. ……….. (190,000) (EL) 152,000 ……….. (55,400) ………..

………………………………………………. ……….. ……….. ……….. (NCI) 20,000 ……….. ………..

………………………………………………. ……….. ……….. (D1) 2,000 ……….. ……….. ………..

………………………………………………. ……….. ……….. (A) 600 ……….. ……….. ………..

Problem 3A-1, Continued

Paro Company and Solar Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Paro Solar Dr. Cr. Interest dated

Consolidated Balance Sheet:

Inventory, December 31, 2016 …………. 100,000 50,000 ……….. ……….. ……….. 150,000

Goodwill ……………………………………….. ……….. ……….. (D3) 60,000 ……….. ……….. 60,000

Other Intangibles ……………………………. 20,000 ……….. ……….. ……….. ……….. 20,000

Current Liabilities …………………………… (120,000) (40,000) ……….. ……….. ……….. (160,000)

Bonds Payable ………………………………. ……….. (100,000) ……….. ……….. ……….. (100,000)

Other Long-Term Liabilities ……………… (200,000) ……….. ……….. ……….. ……….. (200,000)

(carrydown) ……………………………… (336,000) (250,000) ……….. ……….. ……….. ………..

Retained Earnings—Controlling

Interest, December 31, 2016 ………. ……….. ……….. ……….. ……….. ……….. (323,200)