171

Problem 3-3B (Continued)

Part 2

Adjustment (a)

Dec. 31 Insurance Expense ………………………………………… 9,500

Prepaid Insurance …………………………………… 9,500

Adjustment (d)

31 Depreciation Expense—Professional Library …. 2,400

Accumulated Depreciation—Professional

172

Problem 3-3B (Continued)

Part 3

ALONZO INSTITUTE

Adjusted Trial Balance

December 31, 2017

Debit

Credit

Cash ……………………………………………………………………………….

$ 60,000

Teaching supplies …………………………..……………………………..

Tuition fees earned ……………………………………………………….

Teaching supplies expense …………………………………………..

173

Problem 3-3B (Continued)

Part 4

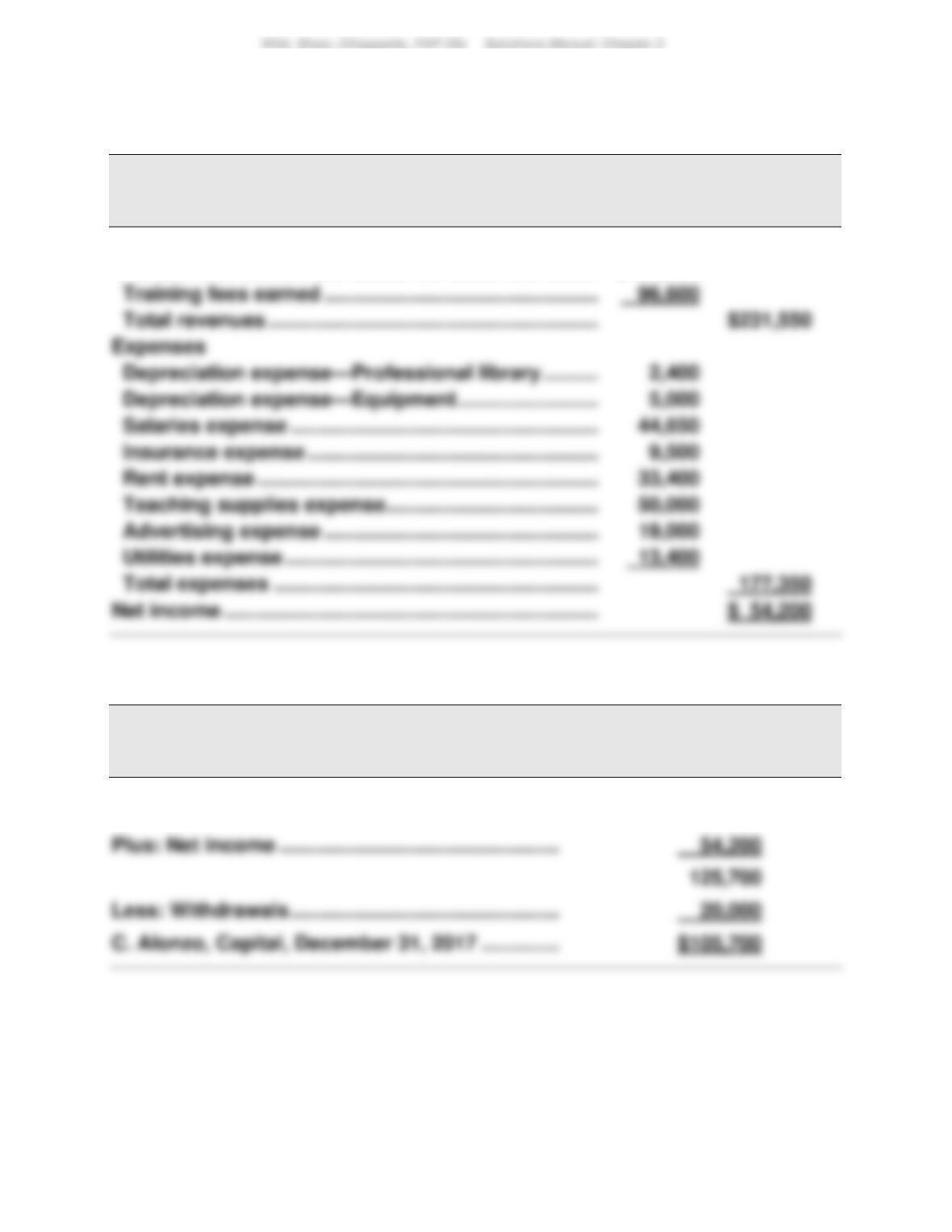

ALONZO INSTITUTE

Income Statement

For Year Ended December 31, 2017

Revenues

Tuition fees earned …………………………………………… $134,950

ALONZO INSTITUTE

Statement of Owner’s Equity

For Year Ended December 31, 2017

C. Alonzo, Capital, December 31, 2016 ………….. $ 71,500

174

Problem 3-3B (Concluded)

ALONZO INSTITUTE

Balance Sheet

December 31, 2017

Assets

Cash …………………………………………………………………… $ 60,000

Problem 3-4B (45 minutes) — Part 1

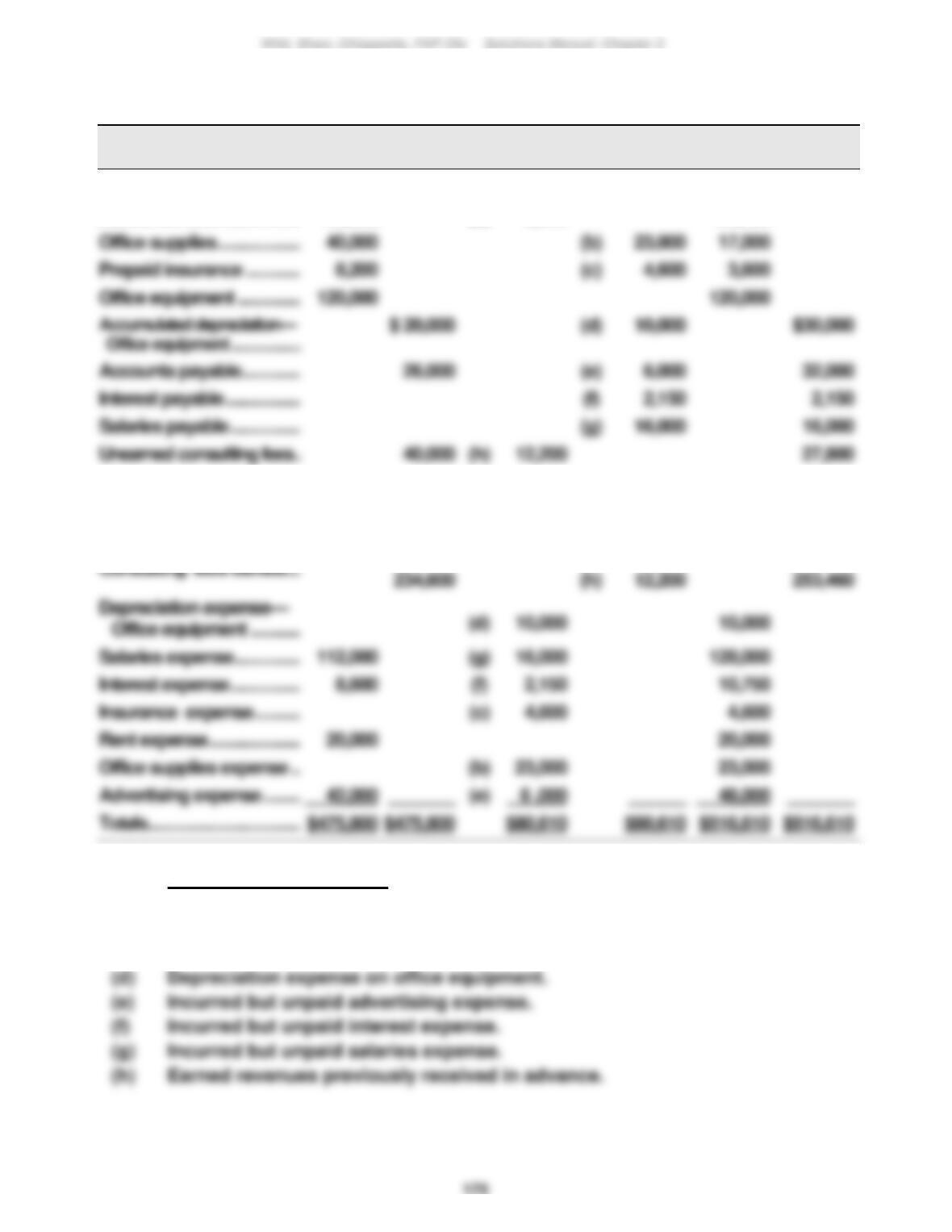

Account

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Cash …………………………………….

$ 45,000

$ 45,000

Accounts receivable …………..

60,000

(a)

6,660

66,660

Office supplies …………………….

40,000

(b)

23,000

17,000

Prepaid insurance ………………

Office equipment ………………..

Accounts payable ……………….

26,000

(e)

32,000

Interest payable …………………..

Salaries payable ………………….

(g)

16,000

16,000

Unearned consulting fees …….

40,000

(h)

12,200

27,800

Long–term notes payable …..

75,000

75,000

Z. Yan, Capital ……………………..

80,200

80,200

Z. Yan, Withdrawals ……………

20,000

20,000

12,200

Salaries expense …………………

16,000

Interest expense ………………….

2,150

10,750

Insurance expense …………….

Rent expense ………………………

20,000

20,000

Office supplies expense …….

23,000

23,000

Advertising expense …………..

(a)

6,660

Adjustment Descriptions

(a) Earned but uncollected revenues.

(b) Cost of office supplies used.

(c) Cost of expired insurance coverage.

176

Problem 3-4B (continued)

Part 2

YAN CONSULTING COMPANY

Income Statement

For Year Ended December 31, 2017

Revenues

Consulting fees earned ……………………………….. $253,460

Expenses

YAN CONSULTING COMPANY

Statement of Owner’s Equity

For Year Ended December 31, 2017

Z. Yan, Capital, December 31, 2016 ……………….. $ 80,200

177

Problem 3-4B (Concluded)

Part 2

YAN CONSULTING COMPANY

Balance Sheet

December 31, 2017

Assets

Cash ……………………………………………………………………..

$ 45,000

Accounts receivable ……………………………………………..

Accumulated depreciation—Office equipment ……….

Total assets …………………………………………………………..

$222,260

Liabilities

Accounts payable ………………………………………………….

$ 32,000

Salaries payable ……………………………………………………

Unearned consulting fees ……………………………………..

Total liabilities ………………………………………………………

178

Problem 3-5B (50 minutes)

Part 1

SPEEDY COURIER

Income Statement

For Year Ended December 31, 2017

Revenues

Delivery fees earned ………………………………. $611,800

SPEEDY COURIER

Statement of Owner‘s Equity

For Year Ended December 31, 2017

L. Horace, Capital, December 31, 2016 ……… $125,000

179

Problem 3-5B (Concluded)

SPEEDY COURIER

Balance Sheet

December 31, 2017

Assets

Cash …………………………………………………………….

$ 58,000

Accounts receivable ……………………………………..

120,000

Notes receivable (due in 90 days)…………………….

210,000

Trucks ………………………………………………………….

Accumulated depreciation—Trucks ……………….

Equipment …………………………………………………….

Accumulated depreciation—Equipment …………

Total assets ………………………………………………….

$663,000

Liabilities

Accounts payable …………………………………………

$134,000

Salaries payable ……………………………………………

Unearned delivery fees ………………………………….

Total liabilities ………………………………………………

Equity

Part 2

Profit margin = $86,000 / $645,800 = 13.3%

180

Problem 3-6BA (40 minutes)

Part 1

Method that records prepaid expenses and unearned revenues in balance sheet accounts

Apr. 1 Prepaid Consulting Fees ………………………………. 2,450

Cash …………………………..…………………………. 2,450

May 1 Prepaid Advertising ……………………………………… 4,450

Cash …………………………..…………………………. 4,450

Paid for future advertising.

23 Cash …………………………………………………………… 10,450

Unearned Service Fees …………………………. 10,450

Received fees in advance.

181

Problem 3-6BA (Continued)

Part 2

Method that records prepaid expenses and unearned revenues in income statement accounts

Apr. 1 Consulting Fees Expense ……………………………. 2,450

Cash …………………………..……………………….. 2,450

Paid for future consulting services.

23 Cash …………………………………………………………… 10,450

Service Fees Earned …………………………….. 10,450

Received fees in advance.

31 Prepaid Consulting Fees …………………………..… 450

Consulting Fees Expense …………………….. 450

182

Problem 3-6BA (Concluded)

Part 3

There are no differences between the two methods in terms of the amounts

that appear on the financial statements. In both cases, the financial

statements reflect the following:

Prepaid consulting fees as of May 31 ………………………………….. $ 450

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

183

SERIAL PROBLEM – SP 3

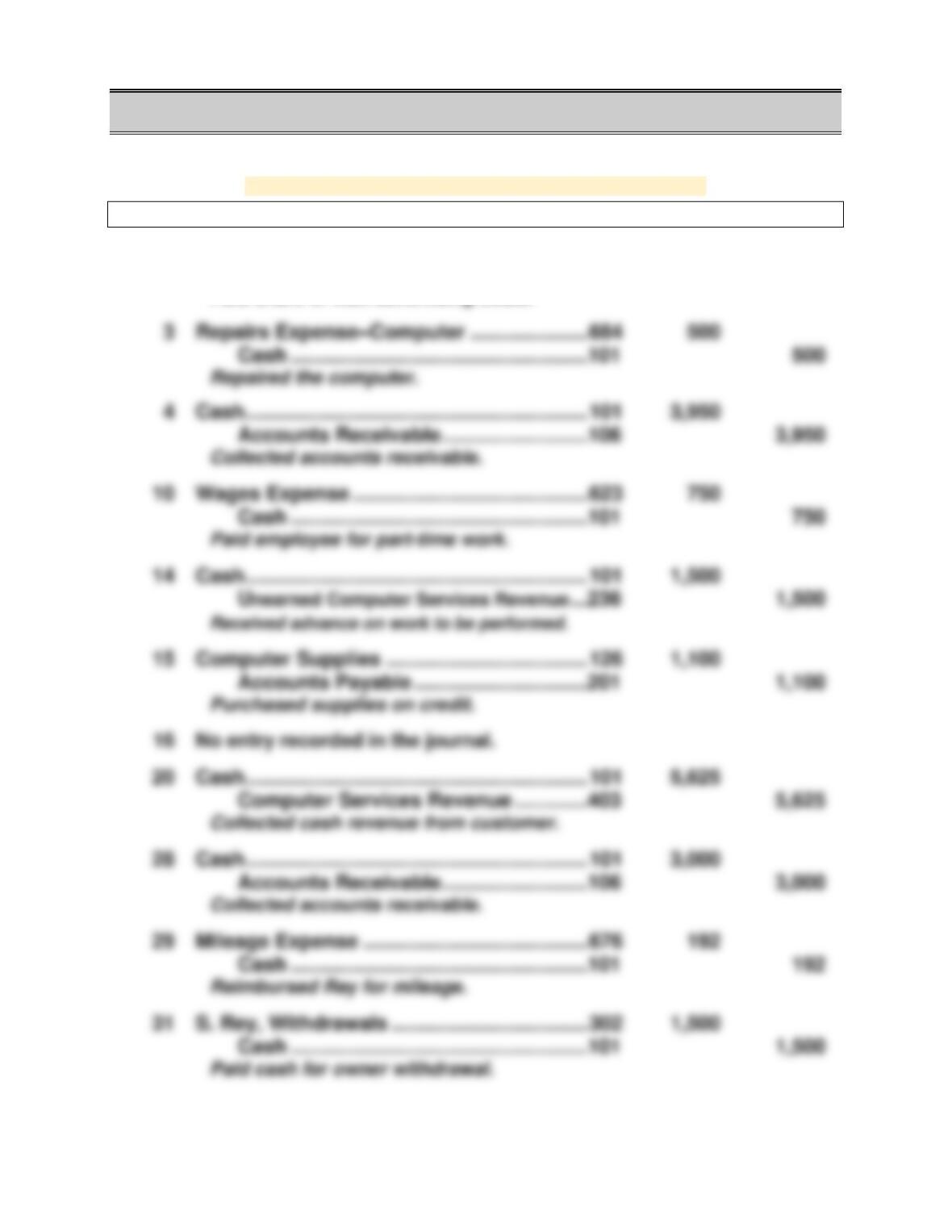

Serial Problem, Business Solutions (180 minutes) — Part 1

<Note: The general ledger is displayed at the end of Part 6>

Journal entries

Dec. 2 Advertising Expense ……………………………. 655 1,025

Cash …………………………..…………………101 1,025

Paid share of mall advertising costs.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

184

Serial Problem, SP 3 (Continued)

Part 2

Adjusting entries

31 Wages Expense ……………………………………….623 500

Wages Payable ………………………………….210 500

Adjustment for accrued wages.