52 Chapter 3 The Adjusting Process

The T accounts follow:

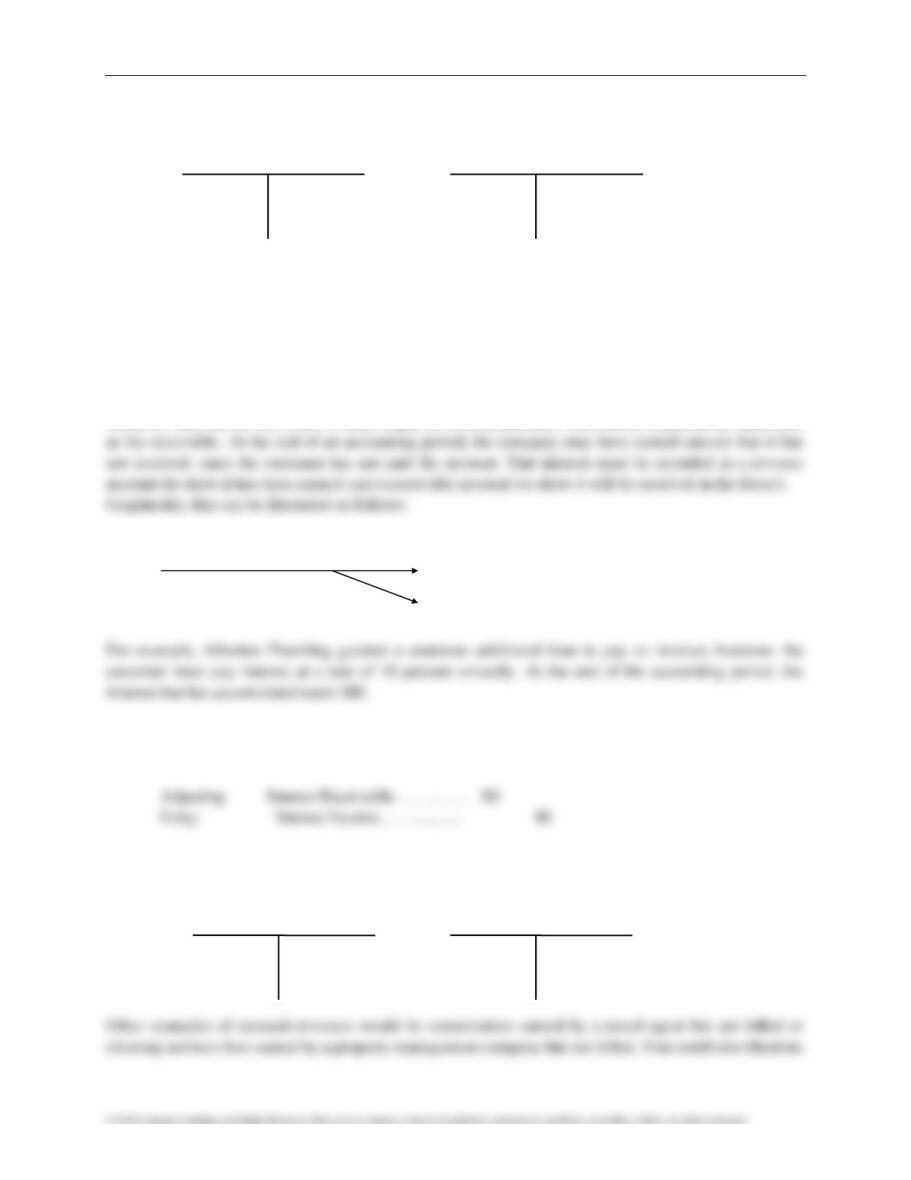

Wages Expense Wages Payable

Adj. 500 Adj. 500

DEMONSTRATION PROBLEM—Adjusting Entry for Accrued Revenues

Any revenue that a business has earned must be recorded before preparing financial statements in order to

get a true measure of profitability. The act of recording revenues that have not been received is called

accruing revenues.

One example of accrued revenue is interest. Assume that a company charges its customers interest

whenever they ask for more than 30 days to pay for a credit purchase. The interest is paid at the same time

New Data

Revenue: Interest Income

Amount of Interest

That Has Been Earned Asset: Interest Receivable

Original

Entry: None

The T accounts follow:

Interest Receivable Interest Income

Adj. 80 Adj. 80

Chapter 3 The Adjusting Process 53

the concept of accrued revenue by asking your students to estimate any wages they have earned that have

not been paid as of today.

DEMONSTRATION PROBLEM—Adjusting Entry for Depreciation

Read the following scenario to your class:

Assume that your car needs four new tires. One set of tires you are considering costs $200.

The manufacturer estimates that these tires will last 20,000 miles. If you drive about

10,000 miles per year, that equates to two years.

It is common to break the cost of a long-term asset into a cost per year or a cost per month when

evaluating whether or not to purchase the asset. Allocating the cost of an asset (such as the tires) to the

years it is used makes it easier to determine the yearly expense of owning the asset. The cost of owning

the $300 set of tires is $75 per year.

The accrual basis of accounting requires business owners to allocate the cost of fixed assets to the years

they are used. This process is called depreciation.

Consider the following example. A florist purchases a delivery van for $12,000. The van will last three

years. What is the florist’s cost per year for this van? (Answer: $4,000.)

The florist’s accountant is required to record depreciation on the delivery van for the following two

reasons:

1. Whenever an asset is used up in running a business, it must be recorded as an expense. Similar to

54 Chapter 3 The Adjusting Process

years. Therefore, a portion of the cost of the van must be matched against the revenue earned in each

of those three years.

Graphically, this can be illustrated as follows:

New Data

Asset: Delivery Expense: Depreciation

Van Portion of the Van’s Expense

Usefulness That Has

Expired

The journal entries to record the purchase of the van and the first year’s depreciation are as follows:

Original Delivery Van………………………… 12,000

Entry: Cash………………………………….. 12,000

The T accounts follow:

Delivery Van Depreciation Expense—Delivery Van

12,000 Adj. 4,000

Bal. 12,000 Bal. 4,000

Why use a contra account to record the adjusting entry for depreciation? Why not just reduce the delivery

van account directly?

2. Any depreciation recorded on a fixed asset is just an estimate of the asset’s usefulness that has

expired. This estimate is maintained in a separate account. For accounting purposes, we assign this

As you cover the adjusting entries for depreciation, you will probably need to emphasize the following

points:

1. A fixed asset must be owned and used by the business.

3. Depreciation is not related to the value of the asset.

4. The normal balance of the accumulated depreciation account is a credit.

TEACHING SUGGESTION—Use of an Accumulated Depreciation Account

To help students understand the purpose of accumulated depreciation contra-accounts, show the following

example:

Company 1 Company 2

Net book value of Equipment $10,000 $10,000

Without using a contra account, both companies look identical. Now show the following:

Company 1 Company 2

Equipment $100,000 $11,000

WRITING EXERCISE—Adjusting Entry for Depreciation

To see how well your students have grasped the concept of depreciation, ask them to write an answer to

the following question (also shown on TM 3-6):

56 Chapter 3 The Adjusting Process

Assume that you are the accountant for Computer Consultants. Prior to this year, Computer

Consultants operated out of a leased office. However, the company purchased its own

office building this year. The building is in an area where real estate values have been

increasing an average of 6 percent per year.

Possible explanation: The response should address the fact that cost, accumulated depreciation, and

ultimately book value are not trying to match the market value of an asset. The market value can go up or

down, depending on the current economic climate. The goal of accounting for fixed assets is to spread the

initial investment cost over a reasonable expected life of the asset. This cost is periodically transferred

through the adjusting process and the accumulated depreciation account. Students should also mention the

OBJECTIVE 3

Summarize the adjustment process.

SYNOPSIS

Exhibit 8 shows a summary of all the adjustments in this chapter. All adjustments must be completed

prior to completing the financial statements for the period. Exhibit 9 shows the journal entry for each

adjustment, and Exhibit 10 shows the result of the adjustments after posting in the general ledger.

Relevant Example Exercises and Exhibits

• Example Exercise 3-8 Effect of Omitting Adjustments

SUGGESTED APPROACH

This objective illustrates the posting of adjusting entries.

Chapter 3 The Adjusting Process 57

Handout 3-1 presents two exercises to assess your students’ understanding of adjusting entries. The

student is given to option to track account balances using T accounts or the “Effect on Adjusting Entry”

column of the handout to determine account balances. The use of T accounts may be more intuitive for

students. In order to be successful with this exercise, students must understand which accounts are

increased and decreased as the result of the adjustment process.

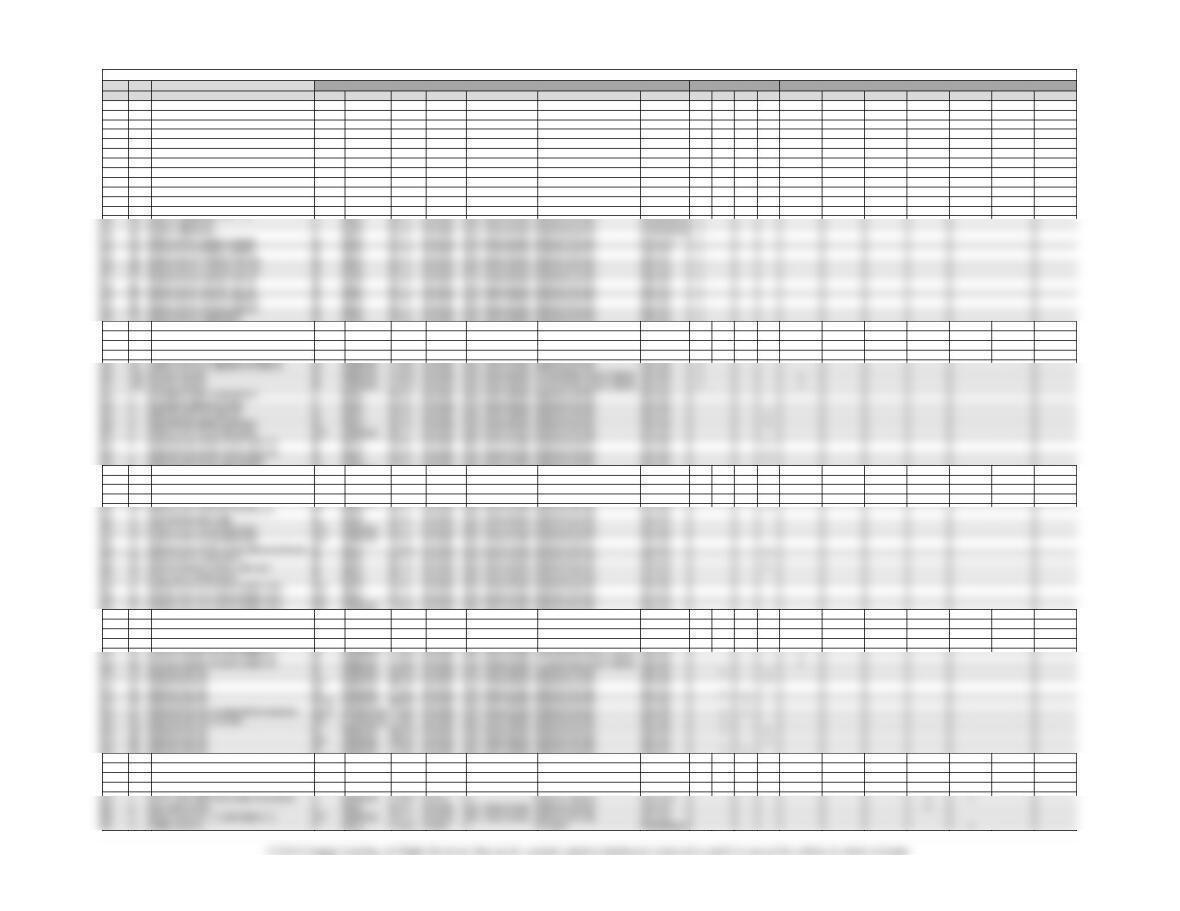

The solution to Part 1 of Handout 3-1 is presented below.

Zeller Company Effect of Zeller Company

Unadjusted Trial Balance Adjusting Adjusted Trial Balance

Dec. 31 Entry Dec. 31

DR CR DR CR

Cash 300 Cash 300

Accounts Receivable 20 + 55 Accounts Receivable 75

Supplies 80 – 70 Supplies 10

Equipment 600 Equipment 600

Accumulated Depreciation 30 + 20 Accumulated Depreciation 50

OBJECTIVE 4

Prepare an adjusted trial balance.

SYNOPSIS

After journalizing and posting the adjusting entries, an adjusted trial balance is prepared. Exhibit 11

shows the adjusted trial balance as of December 31, 2015. The next chapter will show how the financial

statements are prepared from this information.

Key Terms and Definitions

• Adjusted Trial Balance – The trial balance prepared after all the adjusting entries have been

posted.

58 Chapter 3 The Adjusting Process

Relevant Example Exercises and Exhibits

• Example Exercise 3-9 Effect of Errors on Adjusted Trial Balance

• Exhibit 11 – Adjusted Trial Balance

SUGGESTED APPROACH

This objective introduces the adjusted trial balance. Explain to students that like the unadjusted trial

balance, the trial balance is merely copying information from the general ledger to the trial balance.

Accounts with balances are copied from the general ledger in the order in which they appear, and the

balance is copied to the proper column (debit or credit). The final step is to “foot” the columns and

compare the debit and credit balances. You may want to point out that in the accounting cycle, the trial

OBJECTIVE 5

Describe and illustrate the use of vertical analysis in evaluating a company’s performance

and financial condition.

SYNOPSIS

Vertical analysis is a comparison of an amount from a financial statement with a total amount from the

same statement. The total amount chosen is identified as being 100%, and each line in the statement is

shown as a percentage of that total. This analysis is useful for analyzing changes over time. As such, at a

minimum, two years of financial data are needed. Vertical analysis is shown for J. Holmes, Attorney-at–

Law and Pandoroa Media, Inc., using the income statement.

Key Terms and Definitions

• Vertical Analysis – An analysis that compares each item in a current statement with a total

amount within the same statement.

Chapter 3 The Adjusting Process 59

Relevant Example Exercises and Exhibits

• Example Exercise 3-10 Vertical Analysis

SUGGESTED APPROACH

This objective introduces the value of vertical analysis as a tool to indicate relationships within the

financial statement. It is also often used to examine changes in these relationships between time periods,

which in turn demonstrate how a company is performing.

It is valuable to compare the vertical analysis figures of a company against its industry averages.

Averages are published by trade associations and financial information services. Significant differences

should be investigated.

Handout 3-1

Part 1: Zeller Company needs to record the following adjusting entries:

a) Supplies on hand on Dec. 31 were $10.

Use T accounts to record the effect of each adjusting entry and then determine the balances on Zeller’s adjusted trial

balance. You may also use the column labeled “Effect of Adjusting Entry” to track changes in account balances.

Zeller Company Effect of Zeller Company

Unadjusted Trial Balance Adjusting Adjusted Trial Balance

Dec. 31 Entry Dec. 31

DR CR DR CR

Cash 300 Cash

Accounts Receivable 20 Accounts Receivable

Supplies 80 Supplies

Equipment 600 Equipment

Accumulated Depreciation 30 Accumulated Depreciation

Accounts Payable 240 Accounts Payable

Matrix Company

Trial Balance

Dec. 31

Unadjusted Adjusted

Cash 1,500 1,500

Accounts Receivable 700 700

Supplies 200 140

Prepaid Insurance 400 210

Accounts Payable 600 600

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP – APC Bloom‘s EE Excel GL SMH FAI Service Real Writing Ethics Internet Group

DQ 1 1 Easy 5 min. Analytic FN – Measurement Cash vs. Accrual Remembering

DQ 2 1 Easy 5 min. Analytic FN – Measurement Cash vs. Accrual Remembering

DQ 3 1 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 4 1 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 5 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 6 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 7 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 8 3 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 9 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 10 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

PE 1A Accounts requiring adjustment 1 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering x

PE 1B Accounts requiring adjustment 1 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering x

PE 7B Adjustment for depreciation 2 Easy 10 min. Analytic FN – Measurement Adjusting Entries Applying x

PE 8A Effect of omitting adjustments 3 Moderate 10 min. Analytic FN – Measurement Adjusting Entries Applying x

PE 8B Effect of omitting adjustments 3 Moderate 10 min. Analytic FN – Measurement Adjusting Entries Applying x

PE 9A Effect of errors on adjusted trial balance 4 Moderate 10 min. Analytic FN – Measurement Adjusting Entries Applying x

EX 9 Effect of omitting adjusting entry 2,3 Moderate 5 min. Analytic FN – Measurement Adjusting Entries Applying

EX 10 Adjusting enty for accrued fees 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Applying x

EX 11 Adjusting entries for unearned and accrued fees 2 Easy 5 min. Analytic FN – Measurement Adjusting Entries Applying x

EX 12 Effect of omitting adjusting entry 2,3 Moderate 5 min. Analytic FN – Measurement Adjusting Entries Applying

EX 24 Effects of errors on financial statements 2,3 Moderate 10 min. Analytic FN – Measurement Adjusting Entries Applying

EX 25 Adjusting entries for depreciation 2,3 Easy 5 min. Analytic FN – Measurement Adjusting Entries Applying x

EX 26 Adjusting entries from trial balances 4 Moderate 10 min. Analytic FN – Measurement Adjusting Entries Applying x

EX 27 Adjusting entries from trial balances 4 Challenging 15 min. Analytic FN – Measurement Adjusting Entries Applying

PR 4B Adjusting entries 2,3,4 Moderate 45 min. Analytic FN – Measurement Adjusting Entries Applying x

PR 5B Adjusting entries and adjusted trial balances 2,3,4 Challenging 1 hour Analytic FN – Measurement Adjusting Entries Applying x x

PR 6B Adjusting entries and errors 2,3 Challenging 1 hour Analytic FN – Measurement Adjusting Entries Applying x

Continuing Problem x

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS