CHAPTER 3

Process Costing

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

* 1. Discuss the uses of a

process cost system and

how it compares to a job

order system.

1, 2, 3, 4, 5,

20

1

1

* 2. Explain the flow of costs

in a process cost system

and the journal entries to

assign manufacturing

costs.

6, 7

1, 2, 3

2

2, 3, 4

1A

units.

3

10, 11, 13, 14,

5A, 6A

14, 15

units using the FIFO

method.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Journalize transactions.

Moderate

20–30

2A

Complete four steps necessary to prepare a production

cost report.

Simple

30–40

3A

Complete four steps necessary to prepare a production

cost report.

Simple

30–40

4A

Assign costs and prepare production cost report.

Moderate

20–30

assign costs.

cost report.

costs for processes; prepare production cost report.

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

* 1. Discuss the uses of a process cost

system and how it compares to a job

order system.

Q3-1

Q3-2

Q3-3

Q3-4

Q3-5

Q3–20

E3-1

DI3-1

* 2. Explain the flow of costs in a process

cost system and the journal entries to

assign manufacturing costs.

Q3-6

Q3-7

BE3-1

BE3-2

BE3-3

DI3-2

E3-2

E3-3

E3-4

P3-1A

* 3. Compute equivalent units.

Q3–10

Q3–11

Q3–12

Q3–13

BE3-4

BE3-5

DI3-3

E3-3

E3-5

E3-6

E3-7

E3-8

E3-9

E3–10

E3–11

E3–13

E3–14

E3–15

P3–2A

P3–3A

P3-4A

P3-5A

P3–6A

* 4. Complete the four steps to prepare a

production cost report.

Q3-8

Q3–16

Q3–17

Q3–19

Q3-9

Q3–14

Q3–15

Q3–18

BE3-6

BE3-7

BE3-8

BE3-9

DI3-4

E3-3

E3-5

E3-6

E3-7

E3-8

E3-9

E3–10

E3–11

E3–13

E3–14

E3–15

P3–2A

P3-3A

P3–4A

P3–5A

P3–6A

E3–12

*5. Compute equivalent units using the

FIFO method.

Q3–21

Q3–22

BE3-10

BE3-11

BE3-12

E3–16

E3–17

E3–18

E3–19

E3–20

P3–7A

Broadening Your Perspective

BYP3-3

CD-3

BYP3-1

BYP3-2

BYP3-6

BYP3-4

BYP3-5

ANSWERS TO QUESTIONS

1. (a) Process cost.

(b) Process cost.

2. The primary focus of job order cost accounting is on the individual job. In process cost accounting, the

primary focus is on the processes involved in producing homogeneous products.

3. The similarities are: (1) all three manufacturing cost elements—direct materials, direct labor, and

4. The features of process cost accounting are: (1) separate work in process accounts for each

5. Sam is correct. The flow of costs is the same in process cost accounting as in job order cost

accounting. The method of assigning costs, however, is significantly different.

6. (a) (1) Materials are charged to production on the basis of materials requisition slips.

(2) Labor is usually charged to production on the basis of the payroll register or departmental

7. The entry to assign overhead to production is:

July 31 Work in Process—Machining ……………………………………………. 15,000

8. To prepare a production cost report, four steps are followed: (a) compute the physical unit flow,

9. Physical units to be accounted for consist of units in process at the beginning of the period plus

10. Equivalent units of production measure the work done during the period, expressed in fully com-

pleted units.

Questions Chapter 3 (Continued)

13.

Equivalent Units

Materials

Conversion Costs

Units transferred out

Work in process

12,000

12,000

14.

Units accounted for

Completed and transferred out

Units transferred out were 3,200*

Units to be accounted for

Work in process (beginning)

500

15. (a) The cost of the units transferred out is $112,000, or (14,000 X $8).

16. (a) Ann is incorrect. The report is an internal report for management.

17. The production cost report provides the basis for evaluating: (1) the productivity of a department,

(2) whether unit and total costs are reasonable, and (3) whether current performance is meeting

planned objectives.

18. The per unit conversion cost is $11.25. [Conversion costs = $6,000 – $2,400 = $3,600. Equivalent units

19. Operations costing is similar to process costing in that standardized methods are used to manufacture

20. In deciding which system to use, a cost-benefit tradeoff occurs. In a job order system, detailed

information related to the cost of the product is involved. The cost of implementing this system is

*21. Units transferred out were 2,800 (2,000 + 800).

500 X 100%

500

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 3-1

Mar. 31 Raw Materials Inventory …………………………... 50,000

Accounts Payable ……………………………… 50,000

BRIEF EXERCISE 3-2

Mar. 31 Work in Process—Assembly Department ….. 24,000

Work in Process—Finishing Department …… 26,000

Raw Materials Inventory …………………….. 50,000

BRIEF EXERCISE 3-3

Mar. 31 Work in Process—Assembly Department

($35,000 X 160%) ………………………………….. 56,000

BRIEF EXERCISE 3-4

Materials

Conversion Costs

January

45,000 (35,000 + 10,000)

39,000 (35,000 + 4,000a)

BRIEF EXERCISE 3-5

(a)

Materials

(b)

Conversion Costs

Units transferred out

Work in process, November 30

9,000

9,000

BRIEF EXERCISE 3-6

Total materials

costs

$33,000

÷

Equivalent units

of materials

10,000

=

Unit materials

cost

$3.30

costs

÷

=

cost

BRIEF EXERCISE 3-7

Assignment of Costs

Equivalent Units

Unit Cost

Transferred out

Transferred out

40,000

$11

$440,000

Work in process, 4/30

Total costs

$474,000

BRIEF EXERCISE 3-8

Total materials

costs

÷

Equivalent units

of materials

=

Unit materials

cost

BRIEF EXERCISE 3-9

Costs accounted for

Transferred out

(18,000 X $3.10)

$55,800

*BRIEF EXERCISE 3-10

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Transferred out

Work in process, 3/31

Materials

5,000

$ 6

$ 30,000

Work in process, 3/1

0

$ 0

$ 0

*BRIEF EXERCISE 3-11

Equivalent Units

Materials

Conversion

Costs

Units accounted for

Completed and transferred out

PIX COMPANY

(Partial) Production Cost Report

For the Month Ended March 31

COSTS

Materials

Conversion

Costs

Total

(2,000 X $10)

Unit costs

Total costs (a)

Costs accounted for

Transferred out

In process, March 1

$210,000

*

$320,000

**

$530,000

$ 0

Total units

*BRIEF EXERCISE 3-12

Total materials

costs

÷

Equivalent units

of materials

=

Unit materials

cost

Total conversion

Equivalent units

Unit conversion

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 3-1

1. False

DO IT! 3-2

Work in Process—Mixing …………………………………………… 10,000

Work in Process—Packaging …………………………………….. 28,000

Work in Process—Mixing …………………………………………… 12,000

DO IT! 3-2 (Continued)

Work in Process—Packaging …………………………………….. 21,000

Work in Process—Mixing ……………………………………. 21,000

DO IT! 3-3

(a) Since materials are entered at the beginning of the process, the equiva–

lent units of ending work in process are 10,000.

(b) Since ending work in process is only 70% complete as to conversion

costs, the equivalent units of ending work in process for conversion

costs are 7,000 (70% X 10,000 units).

DO IT! 3-4

(a) 0 (Work in process, March 1) + 26,000* (Started into production) = 26,000

(b) Equivalent units of production:

Materials Conversion

Units transferred out …………….. 22,000 22,000

DO IT! 3-4 (Continued)

(c) Cost reconciliation schedule

Costs accounted for

Transferred out (22,000 X $18) ………… $396,000

SOLUTIONS TO EXERCISES

EXERCISE 3-1

1. True.

2. True.

EXERCISE 3-2

April 30 Work in Process—Cooking ………………………… 21,000

30 Work in Process—Cooking ………………………… 8,500

30 Work in Process—Cooking ………………………… 31,500

Work in Process—Canning ………………………… 25,800

EXERCISE 3-3

(a) Work in process, May 1 400

Started into production 1,600

(b) and (c)

Equivalent Units

Materials

Conversion Costs

Unit costs

Units transferred out

Work in process, May 31

1,700

1,700

(d) Transferred out (1,700 X $6.60) $11,220

EXERCISE 3-4

1. Raw Materials Inventory …………………………………… 62,500

Accounts Payable …………………………………….. 62,500

4. Work in Process—Cutting ………………………………… 15,700

Work in Process—Assembly ……………………………. 8,900

Raw Materials Inventory ……………………………. 24,600

7. Work in Process—Assembly ……………………………. 67,600

Work in Process—Cutting …………………………. 67,600

8. Finished Goods Inventory ………………………………… 134,900

Work in Process—Assembly ……………………… 134,900

EXERCISE 3-5

(a)

January

May

Units to be accounted for

Beginning work in process

Started into production

0

13,000

0

21,000

(b)

(1)

Materials

(2)

Conversion Costs

11,500 (10,000 + 1,500)

January

March

13,000 (11,000 + 2,000)

15,000 (12,000 + 3,000)

12,200 (11,000 + 1,200)

12,900 (12,000 + 900)

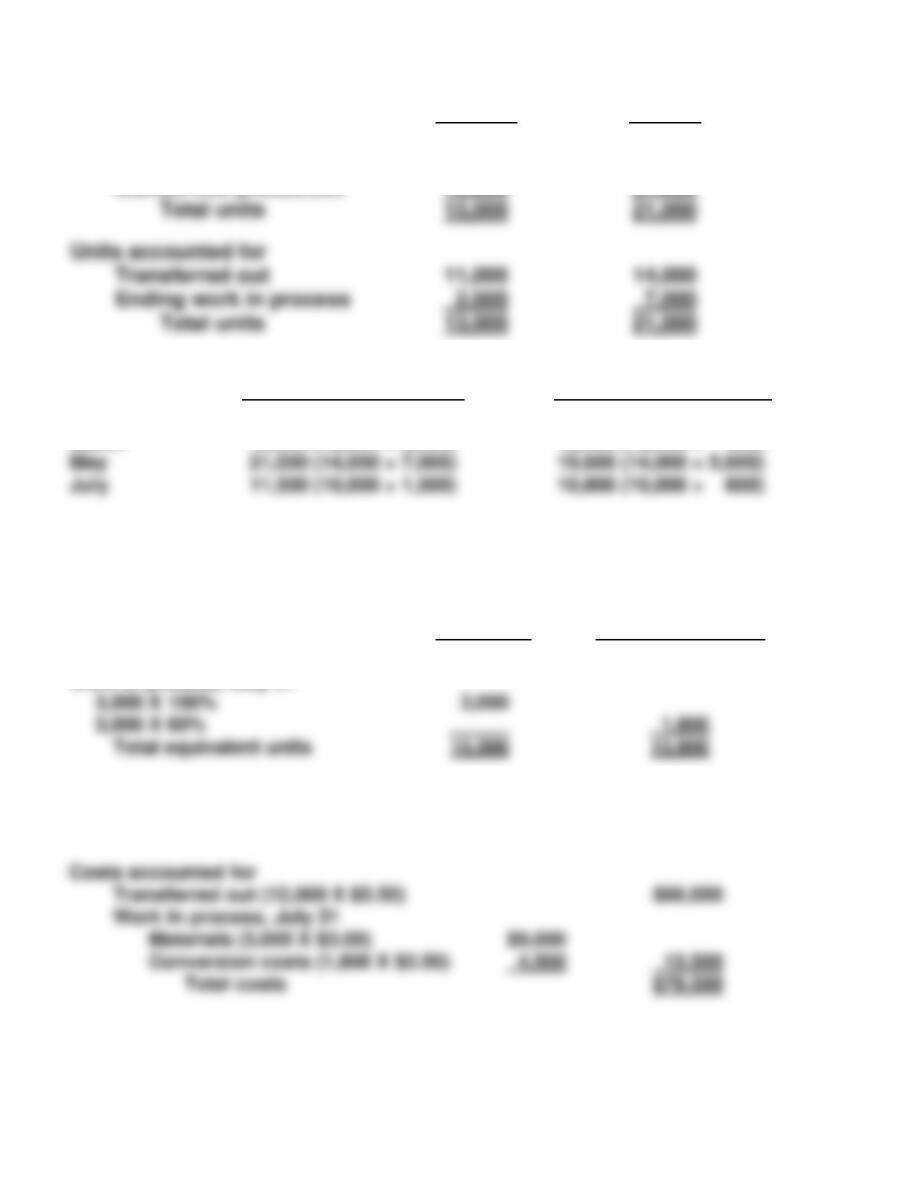

EXERCISE 3-6

(a)

(1)

Materials

(2)

Conversion Costs

3,000 X 100%

Units transferred out

Work in process, July 31

12,000

12,000

Work in process, July 31

Materials (3,000 X $3.00)

(b) Materials: $45,000 ÷ 15,000 = $3.00

Conversion costs: ($16,200 + $18,300) ÷ 13,800 = $2.50

Total units

EXERCISE 3-7

QUIK FURNITURE COMPANY

Sanding Department

Production Cost Report

For the Month Ended March 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, March 1

Started into production

Total units

0

10,000

10,000

Costs

Materials

Conversion

Costs

Total

Started into production

Total costs

Unit costs

Total cost

$33,000

$57,000*

$90,000

Cost Reconciliation Schedule

Total costs

Costs accounted for

Transferred out (7,000 X $10.80)

$75,600

Units accounted for

Transferred out

Work in process, March 31

(3,000 X 20%)

Total units

EXERCISE 3-8

(a)

(1)

Materials

(2)

Conversion

Costs

(b)

Materials

Conversion

Costs

Total

Unit costs

Total cost

$900,000(1)

$435,000(2)

$1,335,000

(c)

Materials (1,000 X $50)

Total costs

Transferred out (17,000 X $75)

$1,275,000

EXERCISE 3-9

(a) Materials: 30,000* + 6,000 = 36,000

(b) Materials: $72,000/36,000 = $2.00

(c) Transferred out: 30,000 X $7.00 = $210,000

Ending work in process:

1,000 X 100%

1,000

EXERCISE 3-10

(a)

Physical

Units

Equivalent Units

Beginning work in process

20,000

Units started into production

164,000

(b)

Conversion

Materials

Costs

Total

Costs incurred

Equivalent units

Unit costs

(c)

Assignment of costs:

Transferred out (160,000 X $2.55)

$408,000

Ending work in process

42,000

EXERCISE 3-11

(a)

Physical

Units

Work in process, September 30

Work in process, September 1

1,600

160,000

160,000

EXERCISE 3-11 (Continued)

Equivalent Units

Materials

Conversion Costs

Units transferred out

39,500

39,500

(b)

Materials

Total materials cost

Work in process, September 1

Direct materials

$ 20,000

Conversion Costs

Total conversion costs

Work in process, September 1

Conversion costs

Costs added to production

during September

$ 43,180

(c) Costs accounted for

Transferred out (39,500 X $15.05) $594,475

Work in process, September 30

EXERCISE 3-12

To: David Skaros

From: Student

Re: Ending inventory

The reason for any confusion related to your department’s ending inventory

quantity stems from the fact that the quantity can be measured in two different

ways, depending on what the information is used for.

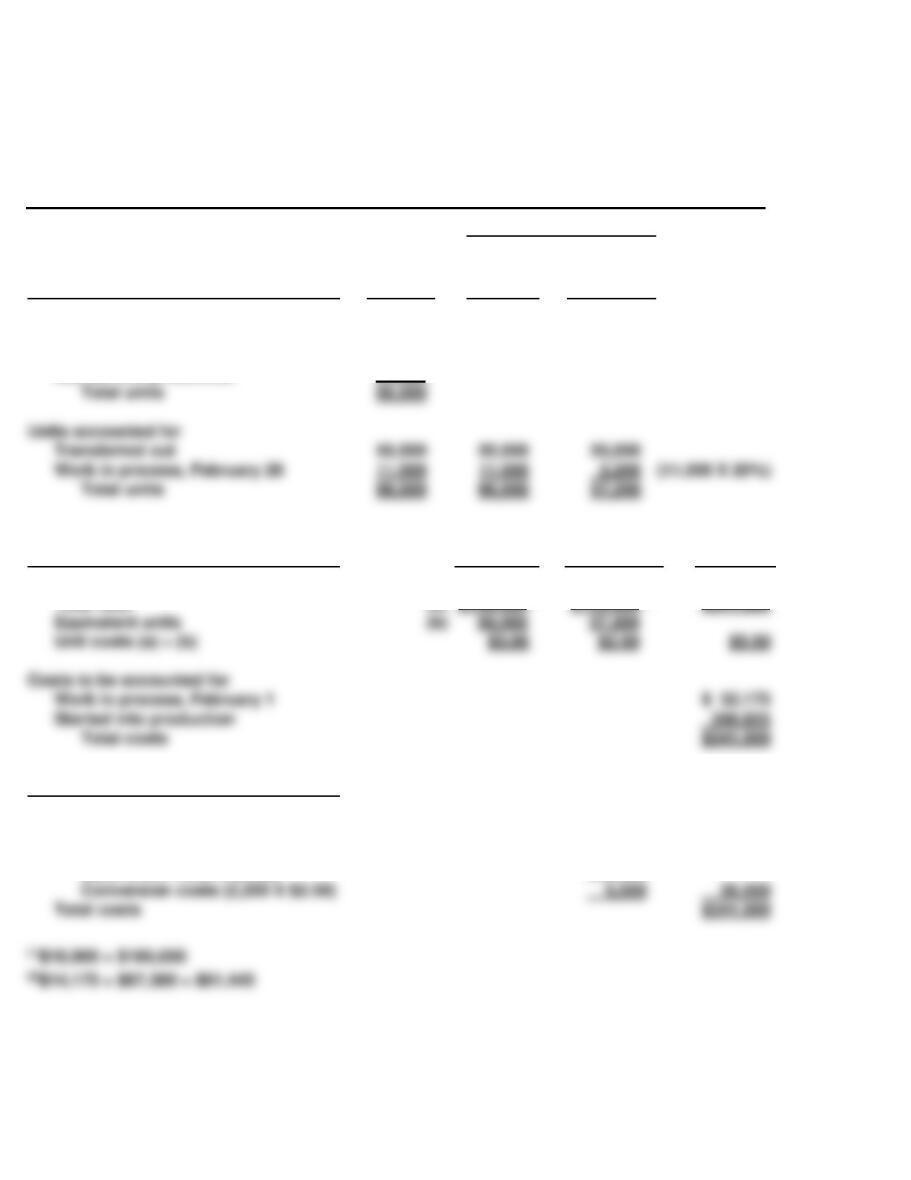

EXERCISE 3-13

HEALTHY COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversio

n

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, February 1

Started into production

15,000

51,000

Costs

Materials

Conversion

Costs

Total

Work in process, February 1

Total costs

Unit costs (Step 3)

Total cost

(a)

$198,000(1)

$143,000(2)

$341,000

Cost Reconciliation Schedule (Step 4)

Total costs

Costs accounted for

Transferred out (55,000 X $5.50)

Work in process, February 28

Materials (11,000 X $3.00)

$33,000

$302,500

Units accounted for

Transferred out

Work in process, February 28

(11,000 X 20%)

Total units

EXERCISE 3-14

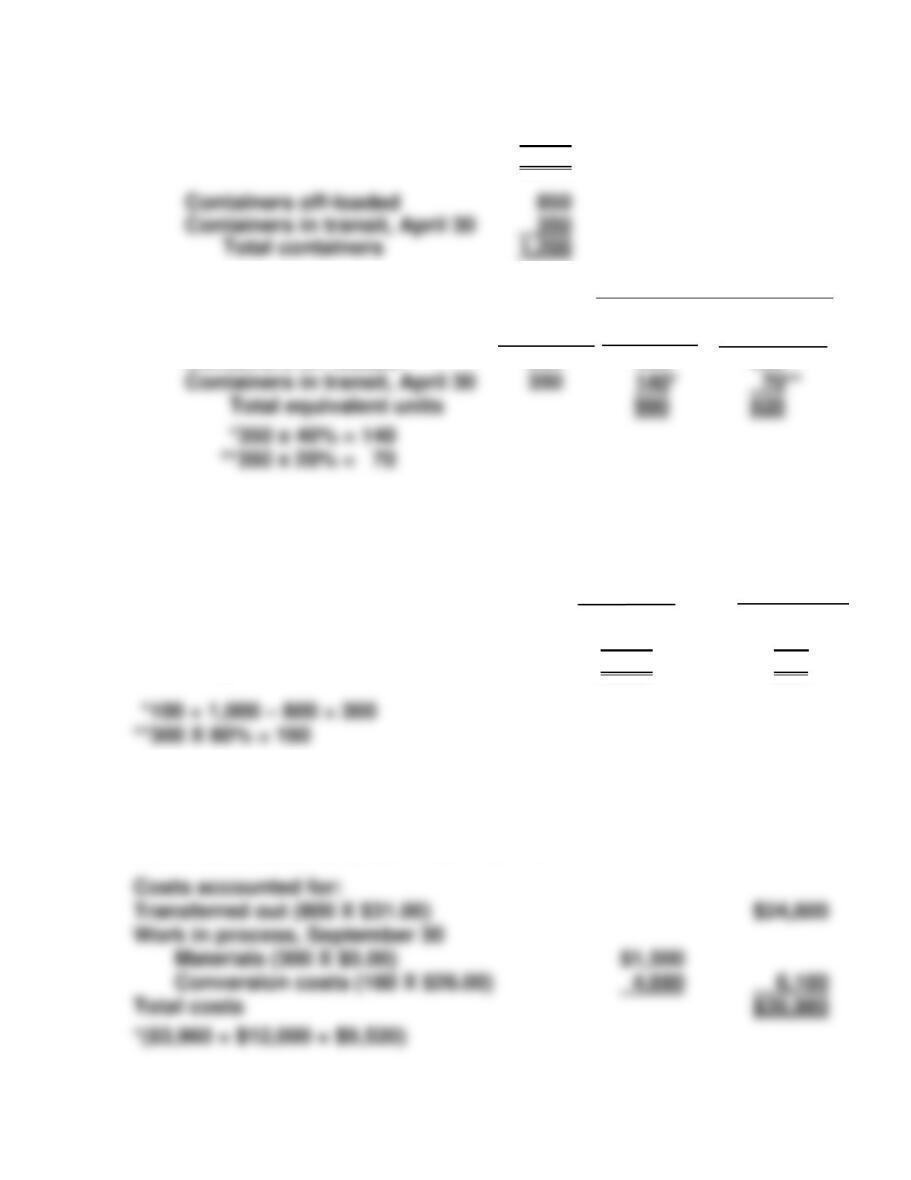

(a)

Containers in transit, April 1

0

Containers loaded

1,200

Total containers

1,200

Equivalent Units

(b)

Physical

Units

Direct

Materials

Conversion

Costs

Containers off-loaded

850

850

850

Containers in transit, April 30

350

Total equivalent units

*350 x 40% = 140

**350 x 20% = 70

EXERCISE 3-15

(a)

Materials

Conversion

Costs

Applications transferred out

800

800

Work in process, September 30

300*

180**

Equivalent units

1,100

980

(b)

Materials: $5,500 ÷ 1,100 = $5.00

Conversion costs: $25,480* ÷ 980 = $26.00

Costs accounted for:

Transferred out (800 X $31.00)

Work in process, September 30

Materials (300 X $5.00)

Conversion costs (180 X $26.00)

Total costs

Containers off-loaded

850

Containers in transit, April 30

350

Total containers

1,200

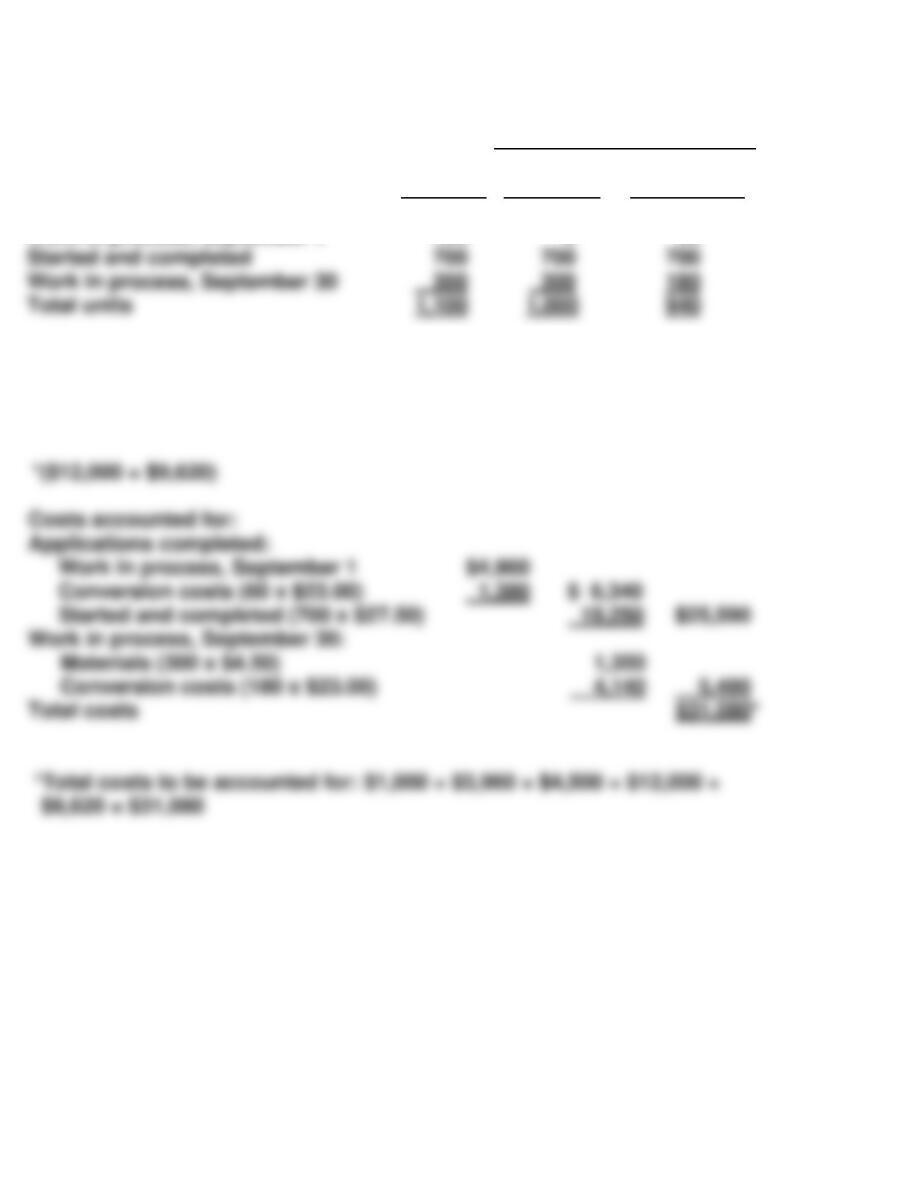

*EXERCISE 3-16

Equivalent Units

(a)

Physical

Units

Materials

Conversion

Costs

Applications completed:

Work in process, September 1

100

0

60

(b)

Materials: $4,500 ÷ 1,000 = $4.50

Conversion costs: $21,620* ÷ 940 = $23.00

1,350

Started and completed

700

Work in process, September 30

Total units

*EXERCISE 3-17

(a) (1) Materials:

Production Data

Physical

Units

Materials Added

This Period

Equivalent

Units

Work in process, August 1

Started and completed

0

10,000

0

100%

0

10,000

(2) Conversion Costs:

Production Data

Physical

Units

Work Added

This Period

Equivalent

Units

Started and completed

Total

Work in process, August 1

0

0

0

(b) Unit costs are:

Materials $45,000 ÷ 12,000 = $3.75

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

$74,700 (1)

Work in process, August 1

Started and completed

0

10,000

$ 0

$6.50

$ 0

65,000

$65,000

Work in process, August 31

Work in process, August 31

Total

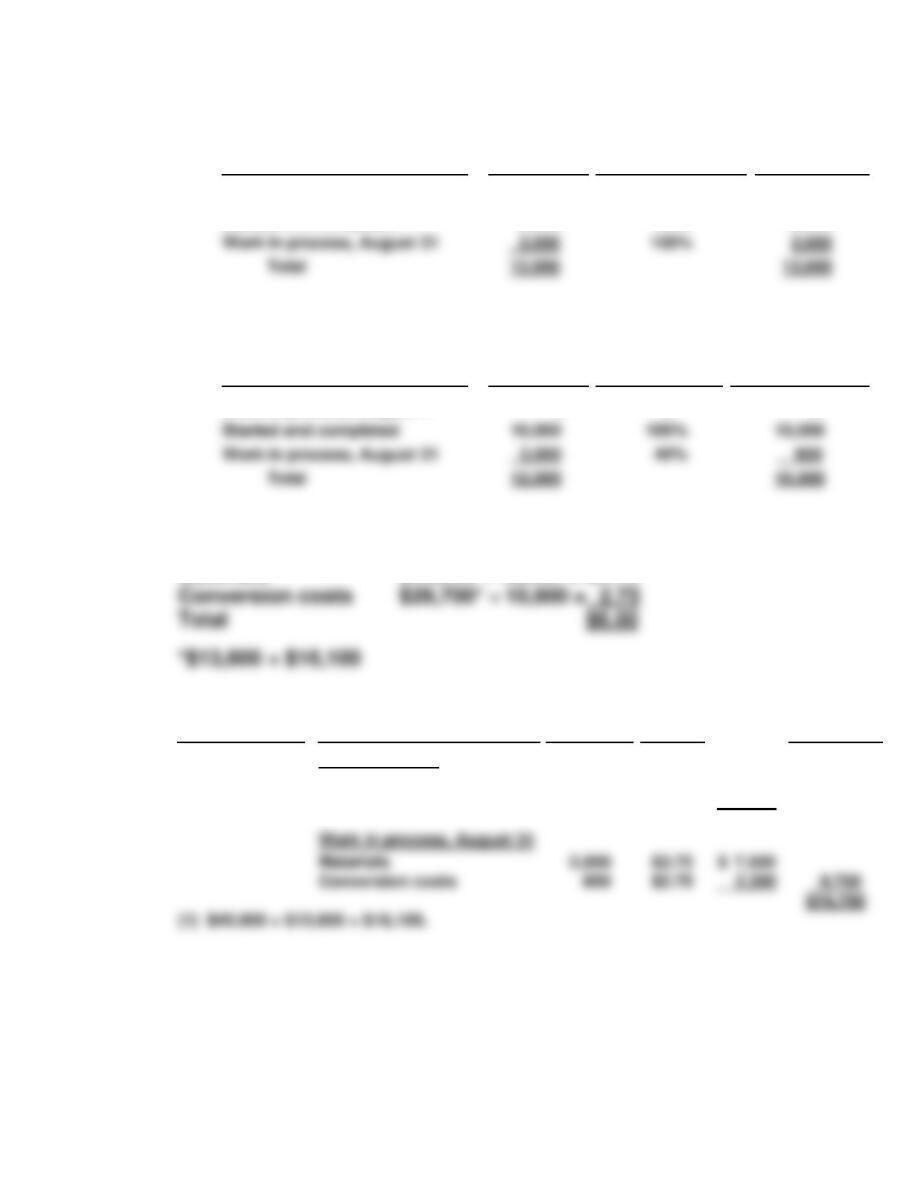

*EXERCISE 3-18

(a)

(1)

Materials

Physical

Units

Materials Added

This Period

Equivalent

Units

Work in process,

September 1

2,000

Q

0%

0

(2)

Conversion Costs

Physical

Units

Work Added

This Period

Equivalent

Units

September 1

2,000

Work in process,

(b) Materials $ 60,000 ÷ 10,000 = $ 6

(c)

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

Started and completed

Total costs transferred out

Total costs

4,800

Work in process, 9/1

Conversion costs

0

1,600

$ 0

$12

$15,200

19,200

$ 34,400

Total

*EXERCISE 3-19

(a) Work in process, March 1 800

Started into production 1,100

(b) Materials:

Production Data

Physical

Units

Materials Added

This Period

Equivalent

Units

Started and completed

Work in process, March 31

Total

700

700

Work in process, March 1

800

%100

0

(c) Conversion costs:

Production Data

Physical

Units

Work Added

This Period

Equivalent

Units

Work in process, March 31

Total

Work in process, March 1

Started and completed

800

700

70%

100%

560

700

(d) In process, March 1 ………………………………………………… $3,680

(e) 700 X ($6.00 + $2.50) = $5,950.

(f) Materials (400 X $6.00) ……………………………………………. $2,400

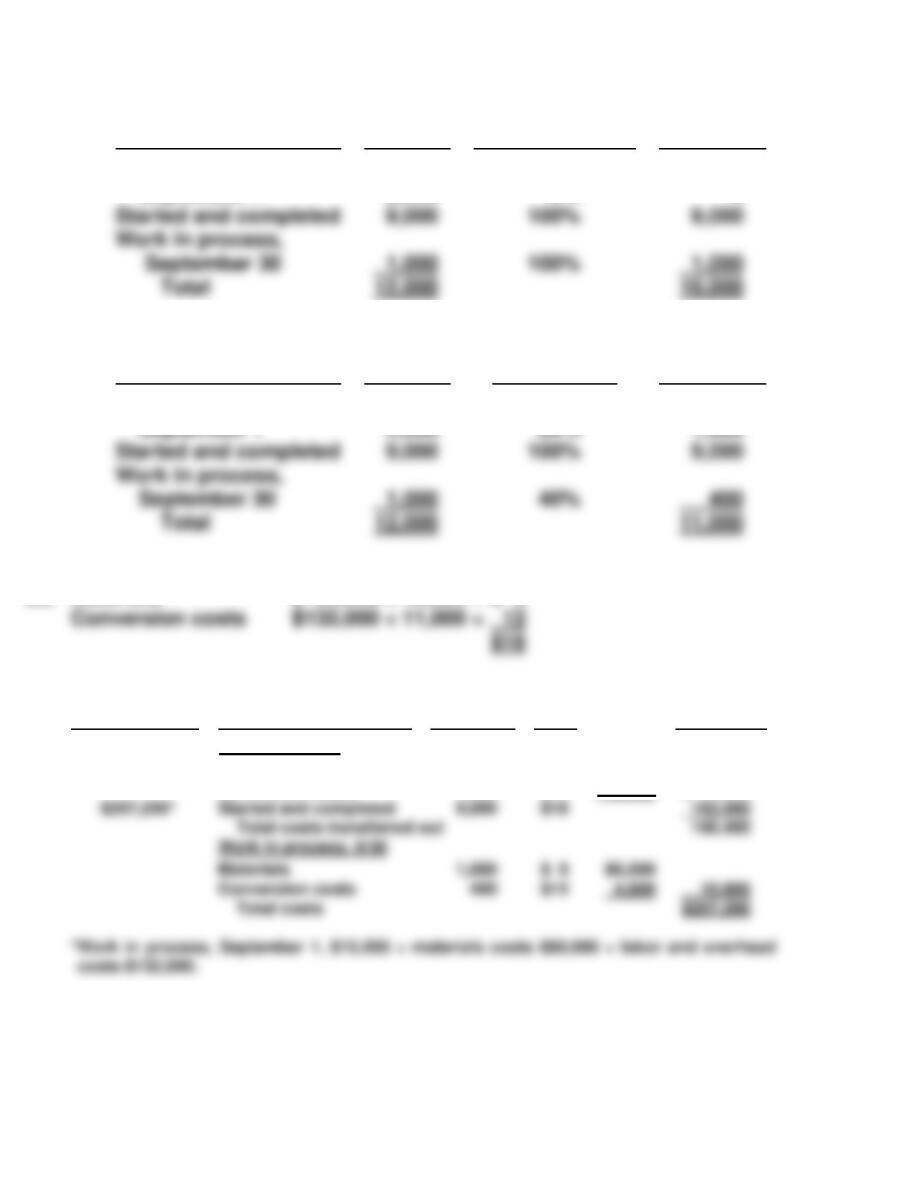

*EXERCISE 3-20

MAJESTIC COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, February 1

Started into production

Total units

15,000

64,000

79,000

Costs

Materials

Conversion

Costs

Total

Started into production

Total costs

$327,675

Unit costs (Step 3)

Costs in February

(a)

$192,000

(1)

$103,500

(2)

$295,500

Units accounted for

Total

Work in process, February 28

Total units

*EXERCISE 3-20 (Continued)

Cost Reconciliation Schedule

Costs accounted for (Step 4)

Transferred out

Work in process, February 1

Costs to complete beginning

work in process

Conversion costs

(13,500 X $1.80)

Total costs

$32,175

24,300

$ 56,475

SOLUTIONS TO PROBLEMS

PROBLEM 3-1A

1. Raw Materials Inventory ……………………………. 300,000

Accounts Payable ……………………………… 300,000

5. Manufacturing Overhead …………………………... 810,000

Accounts Payable ……………………………… 810,000

6. Work in Process—Mixing (28,000 X $23) …….. 644,000

Work in Process—Packaging

(6,000 X $23) …………………………………………. 138,000

PROBLEM 3-2A

(a)

Physical units

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

22,000

22,000

(b)

Equivalent units

Materials

Conversion Costs

2,000 X 100%

Total equivalent units

Units transferred out

20,000

20,000

(c)

Unit Costs

Total unit cost

Materials

$9.00 ($198,000 ÷ 22,000)

(d) Costs accounted for

Transferred out (20,000 X $17.00) $340,000

Total units

PROBLEM 3-2A (Continued)

(e) ROSENTHAL COMPANY

Molding Department

Production Cost Report

For the Month Ended June 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Total cost

Equivalent units

(a)

(b)

$198,000

22,000

$166,400

20,800

$364,400

Cost Reconciliation Schedule (Step 4)

Total costs

6,400

24,400

Costs accounted for

Transferred out (20,000 X $17.00)

Work in process, June 30

$340,000

Work in process, June 1

Transferred out

Work in process, June 30

(2,000 X 40%)

Total units

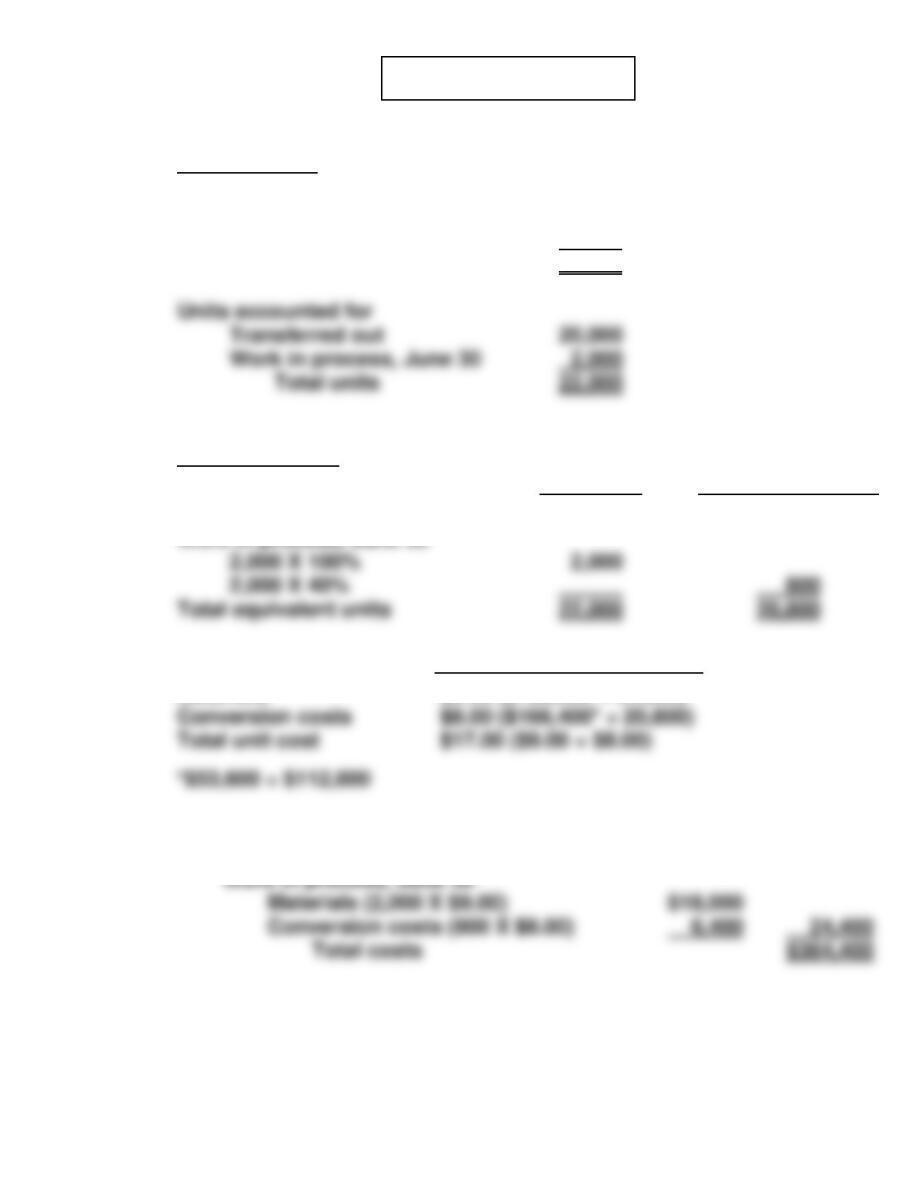

PROBLEM 3-3A

(a) (1) Physical units

T12

Tables

C10

Chairs

Units to be accounted for

Work in process, July 1

Started into production

0

20,000

0

18,000

(2) Equivalent units

T12 Tables

Materials

Conversion

Costs

Units transferred out

Work in process, July 31

17,000

17,000

C10 Chairs

Materials

Conversion

Costs

Work in process, July 31

Units transferred out

17,500

17,500

Work in process, July 31

18,000

PROBLEM 3-3A (Continued)

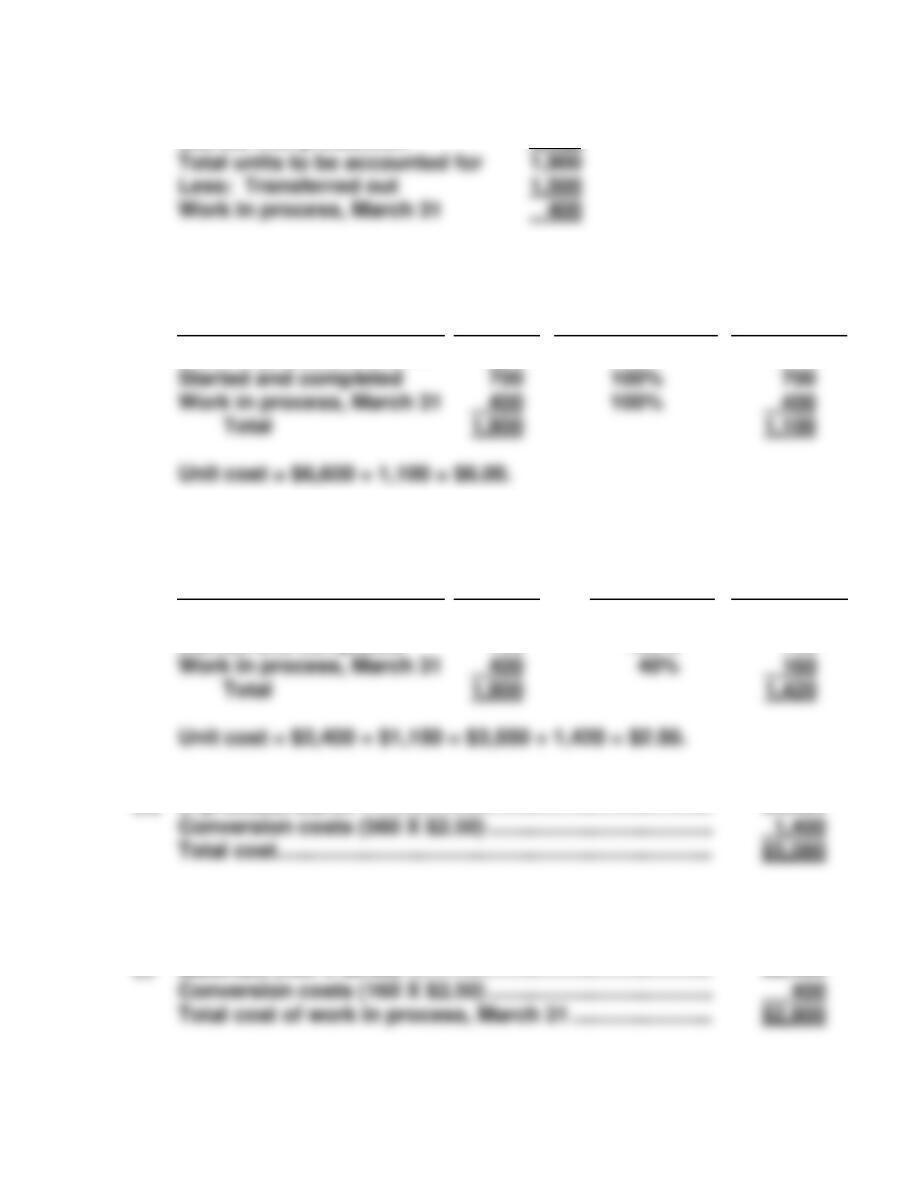

(3) Unit costs

T12

Tables

C10

Chairs

Materials ($380,000 ÷ 20,000)

$19

(4) T12 Tables

Costs accounted for

Transferred out (17,000 X $37) $629,000

C10 Chairs

Costs accounted for

Transferred out (17,500 X $28) $490,000

Work in process

PROBLEM 3-3A (Continued)

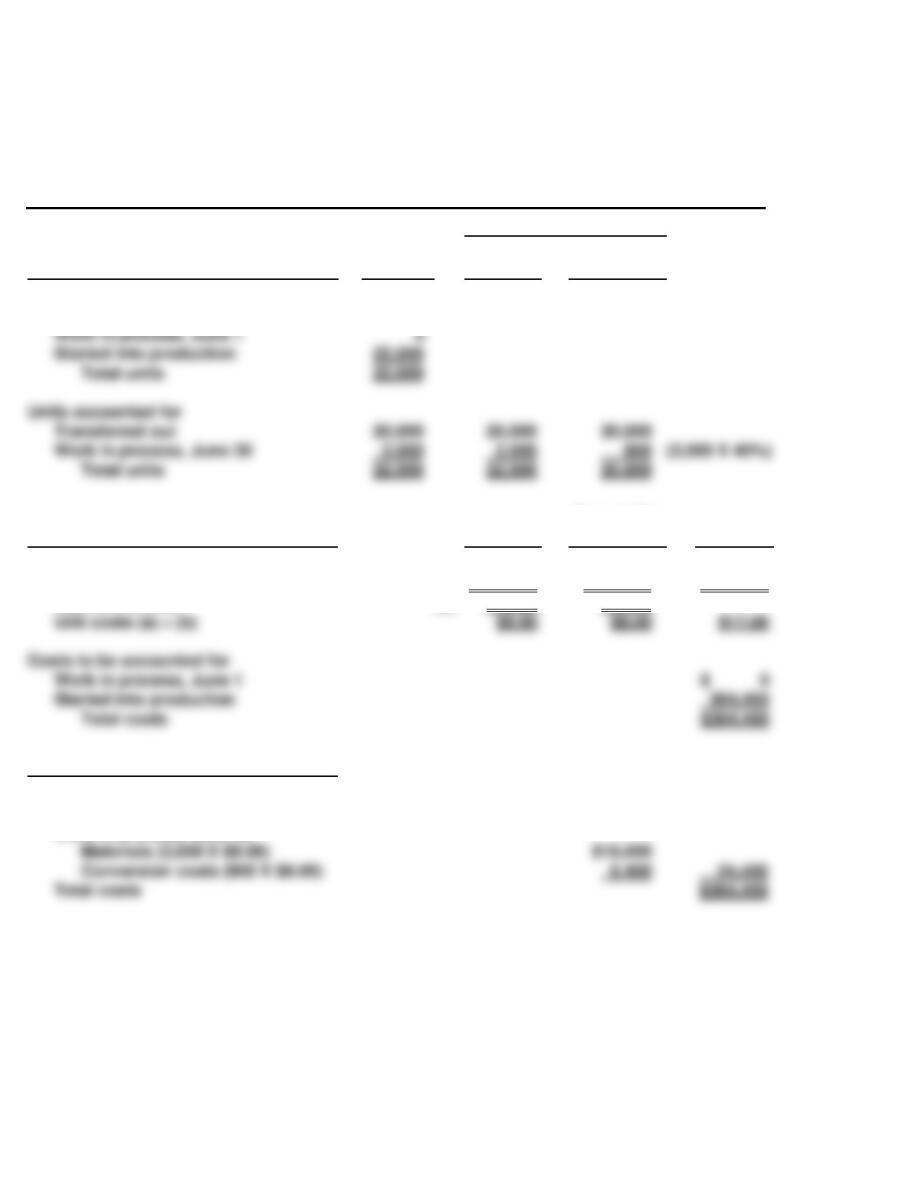

(b) THAKIN INDUSTRIES INC.

Cutting Department—Plant 1

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, July 1

Started into production

0

20,000

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Total cost

(a)

$380,000

$338,400

$718,400

Cost Reconciliation Schedule (Step 4)

Total costs

Costs accounted for

Transferred out (17,000 X $37)

$629,000

Units accounted for

Transferred out

Work in process, July 31

(3,000 X 60%)

Total units

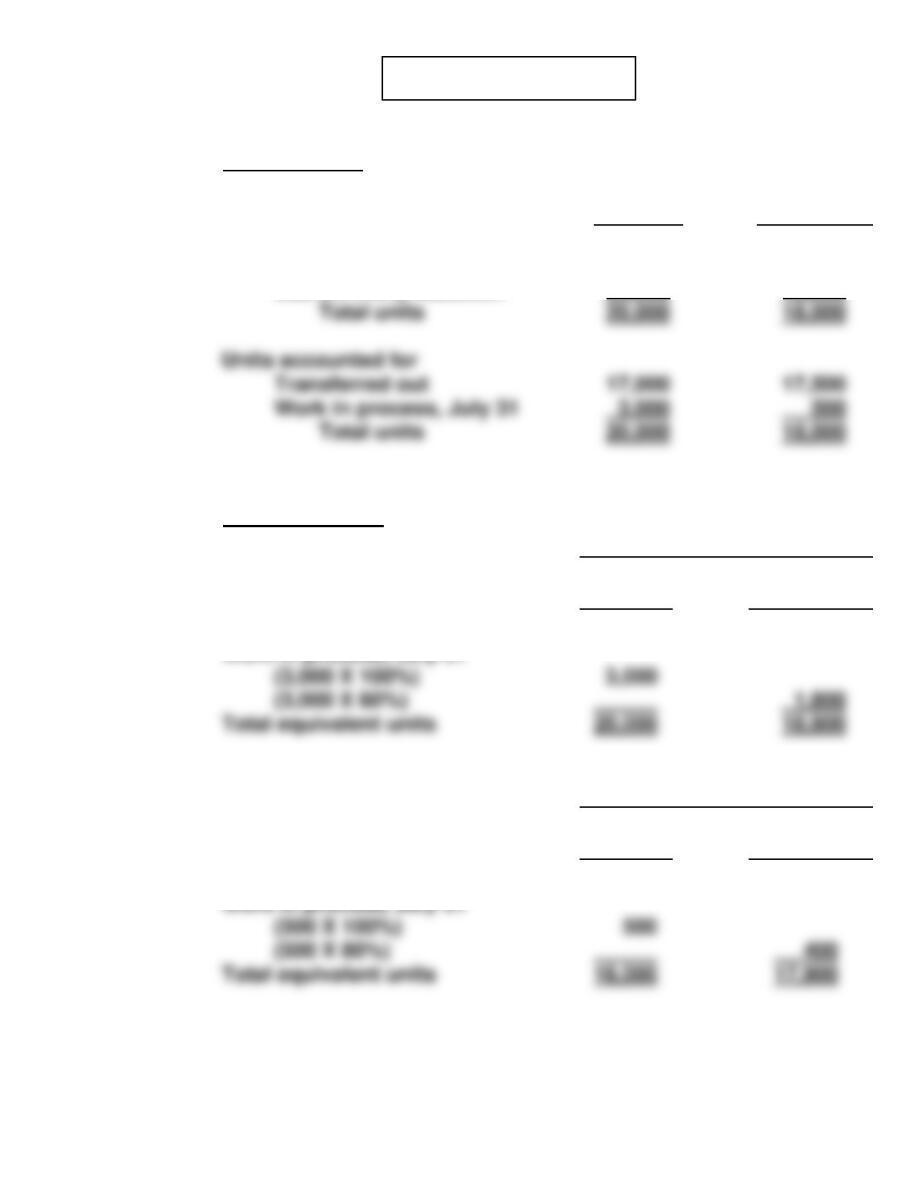

PROBLEM 3-4A

(a)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, November 1

35,000

Beginning work in

process

Added during month

Materials cost

$ 79,000

1,589,000

Conversion costs

$ 48,150

563,850

($225,920 + $337,930)

(b)

Total costs

Costs accounted for

Transferred out (670,000 X $3.30)

Work in process, November 30

Materials (25,000 X $2.40)

$60,000

$2,211,000

Total units

Work in process, November 30

Total units

695,000

25,000

695,000

25,000

695,000

PROBLEM 3-4A (Continued)

(c) RIVERA COMPANY

Assembly Department

Production Cost Report

For the Month Ended November 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, November 1

Started into production

Total units

35,000

660,000

695,000

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Total costs

Unit costs (Step 3)

Total cost

Equivalent units

(a)

(b)

$1,668,000

695,000

$612,000

680,000

$2,280,000

Cost Reconciliation Schedule (Step 4)

(10,000 X $.90)

Total costs

Costs accounted for

Transferred out (670,000 X $3.30)

Work in process, November 30

$2,211,000

Units accounted for

Transferred out

Work in process, November 30

(25,000 X 40%)

Total units

695,000

695,000

PROBLEM 3-5A

(a)

(1)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, July 1

Units accounted for

500

(2)

Beginning work

in process

Added during month

Materials cost

$ 750

2,400

Conversion costs

$ 600

2,820

($1,580 + $1,240)

(3)

Costs accounted for

Transferred out (900 X $5.10)

Work in process, July 31

$4,590

Total units

PROBLEM 3-5A (Continued)

(b) POLK COMPANY

Basketball Department

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, July 1

Started into production

500

1,000

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Total costs

(a)

$3,150

$3,420

$6,570

Cost Reconciliation Schedule (Step 4)

Total costs

Costs accounted for

Transferred out (900 X $5.10)

$4,590

Units accounted for

Total units

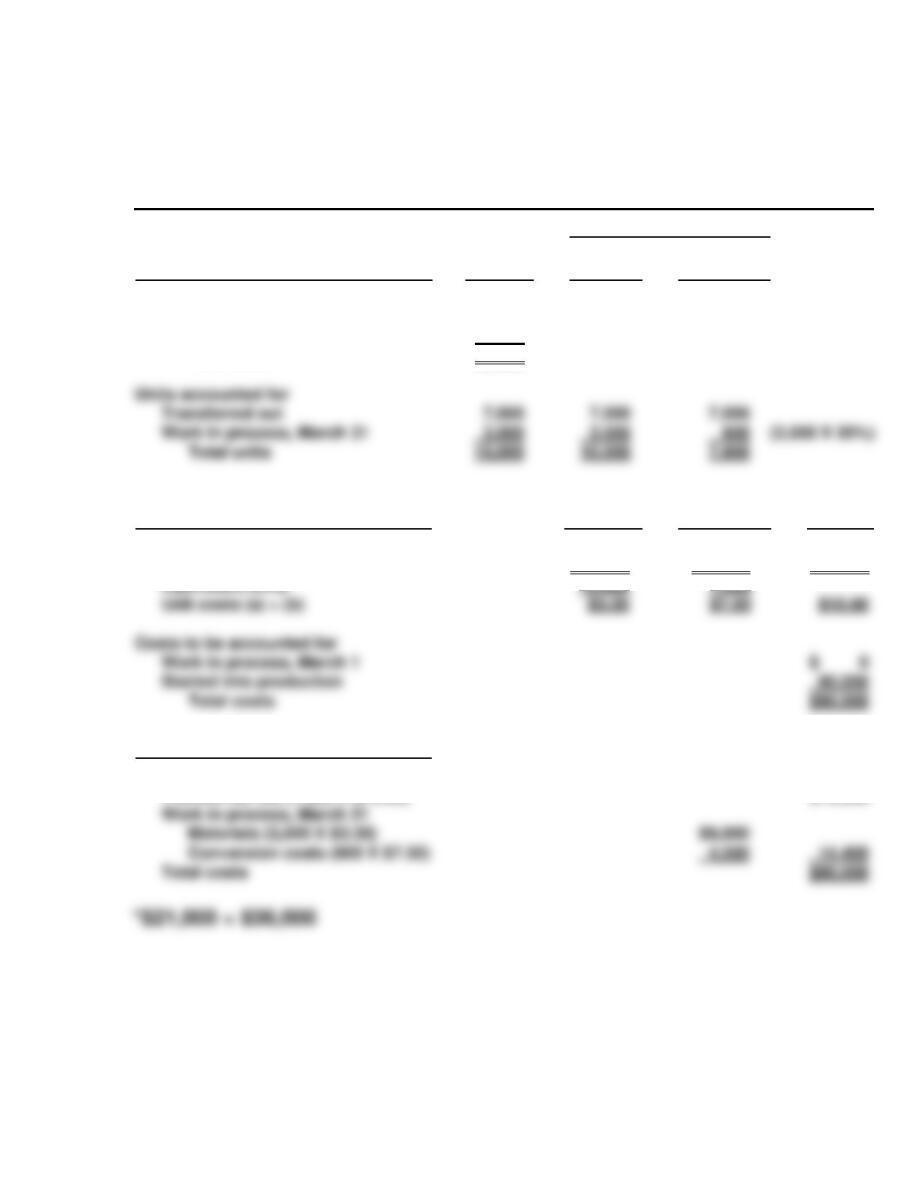

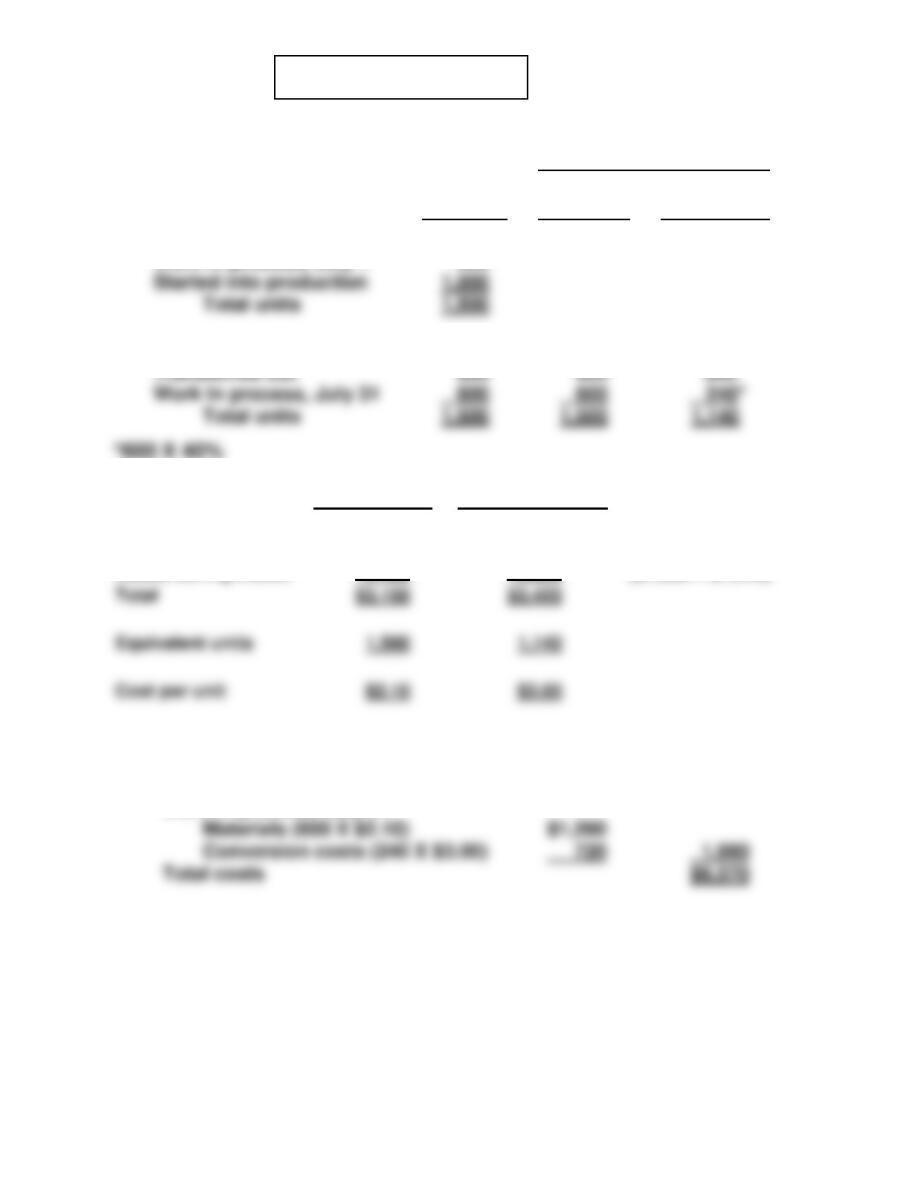

PROBLEM 3-6A

(a) Computation of equivalent units:

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units accounted for

Transferred out

Work in process, October 31

120,000

120,000

120,000

Computation of October unit costs

(b) Cost Reconciliation Schedule

Costs accounted for

Transferred out (120,000 X $2.35) $282,000

Work in process, October 31

Total units

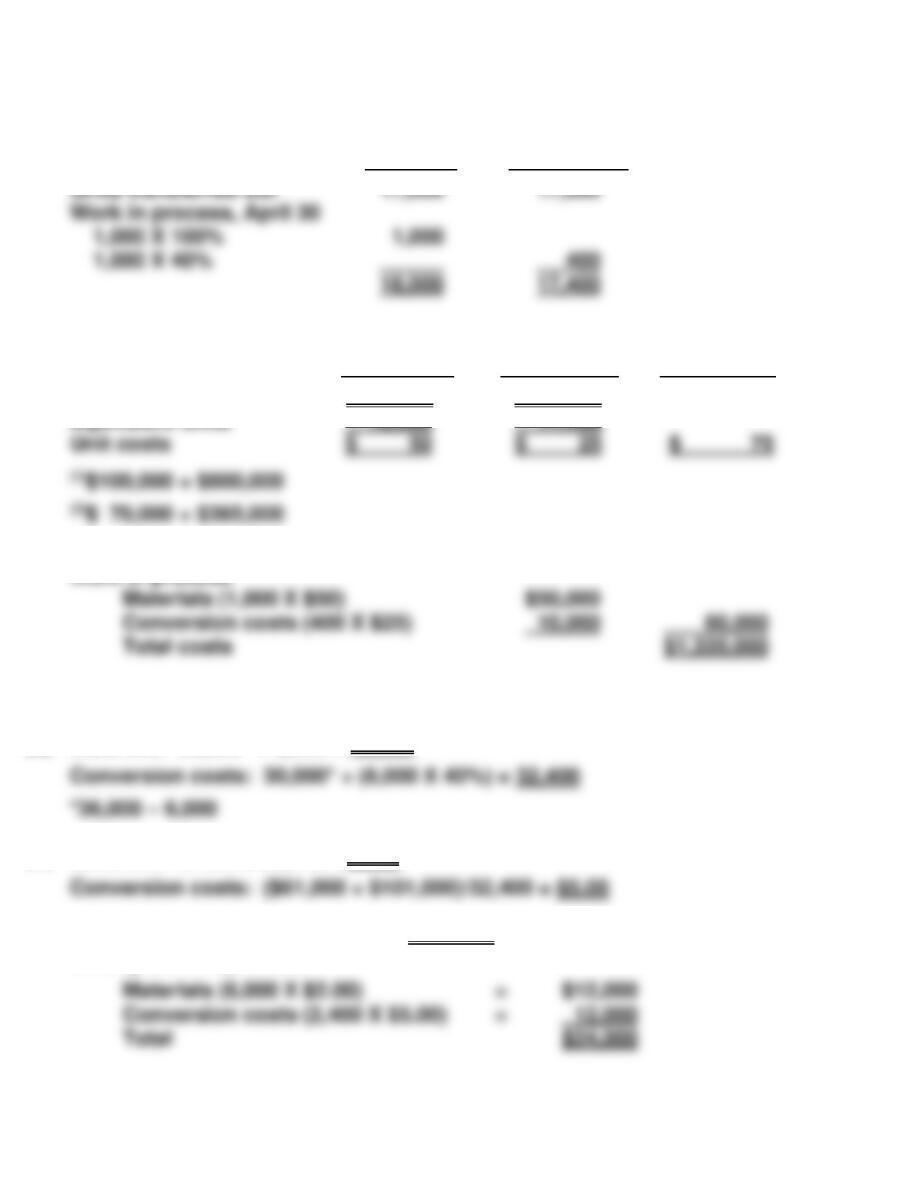

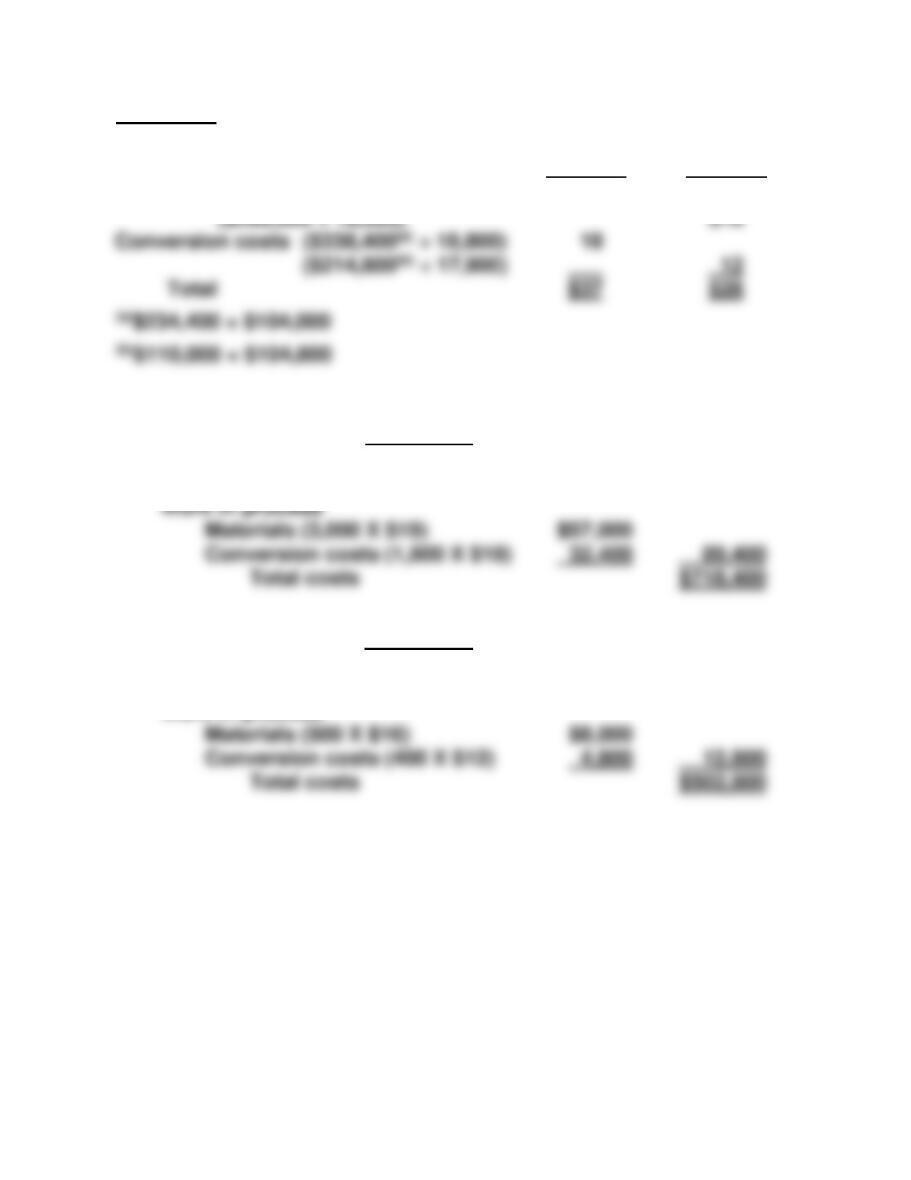

*PROBLEM 3-7A

(a) Bicycles

(1) Equivalent units—Materials

Physical

Units

Materials

Added

This Period

Equivalent

Units

Work in process, March 1

200

* 0%*

0

(2) Unit costs

Materials

Conversion

Costs

Costs in March (a)

$50,000

**$55,900**

Started and completed

Work in process, March 31

Total

Physical

Conversion

Added

Equivalent

Started and completed

Work in process, March 31

*PROBLEM 3-7A (Continued)

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

***$125,180***

Work in process, March 1

Conversion

40

$ 65

$19,280

2,600

Tricycles

(1) Equivalent units—Materials

Physical

Units

Materials

Added

This Period

Equivalent

Units

Work in process, March 1

100

* 0%*

0

Started and completed

940

Total

60

Equivalent units—Conversion costs

Physical

Units

Conversion

Added

This Period

Equivalent

Units

Work in process, March 1

100

25% (1 – .75) 25

Started and completed

940 (1,000 – 60)

Total

Total costs transferred out

Work in process, March 31

Total costs

*PROBLEM 3-7A (Continued)

(2) Unit costs

Materials

Conversion

Costs

Costs in March (a)

$30,000

$34,300**

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

***$70,425***

Work in process, March 1

Conversion

25

$35

$ 6,125

875

Equivalent units (b)

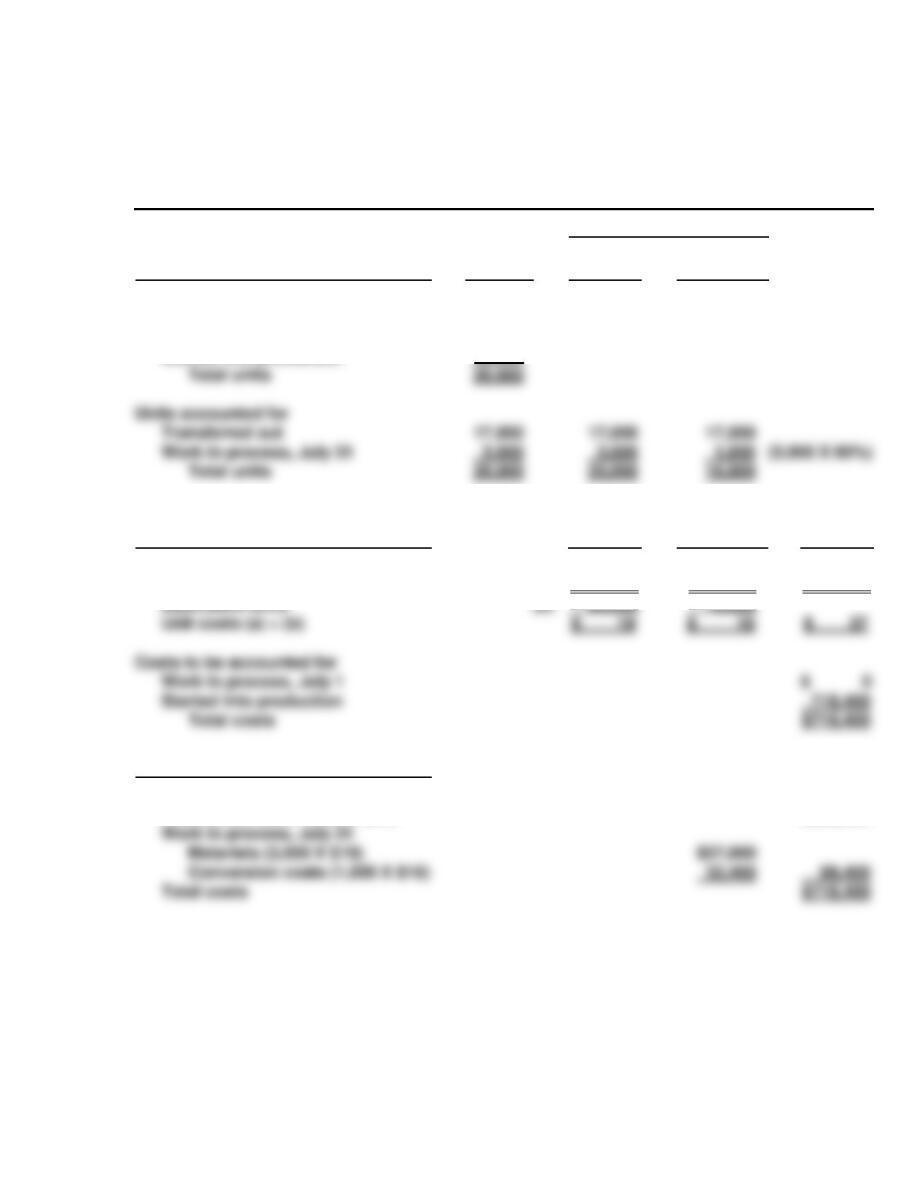

*PROBLEM 3-7A (Continued)

(b) OWEN COMPANY

Production Cost Report—Bicycles

For the Month Ended March 31

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Total units

Units to be accounted for

Work in process, March 1

Units accounted for

Completed and transferred out

Work in process, March 1

200

200

0

40

Costs

Materials

Conversion

Costs

Total

Started and completed (700 X $115)

Work in process, March 31

Total costs

Unit costs (Step 3)

Costs in March (a)

Equivalent units (b)

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out

Work in process, March 1

Conversion costs to complete

$50,000

1,000

$19,280

$ 55,900

860

$105,900

Started into production

Total units

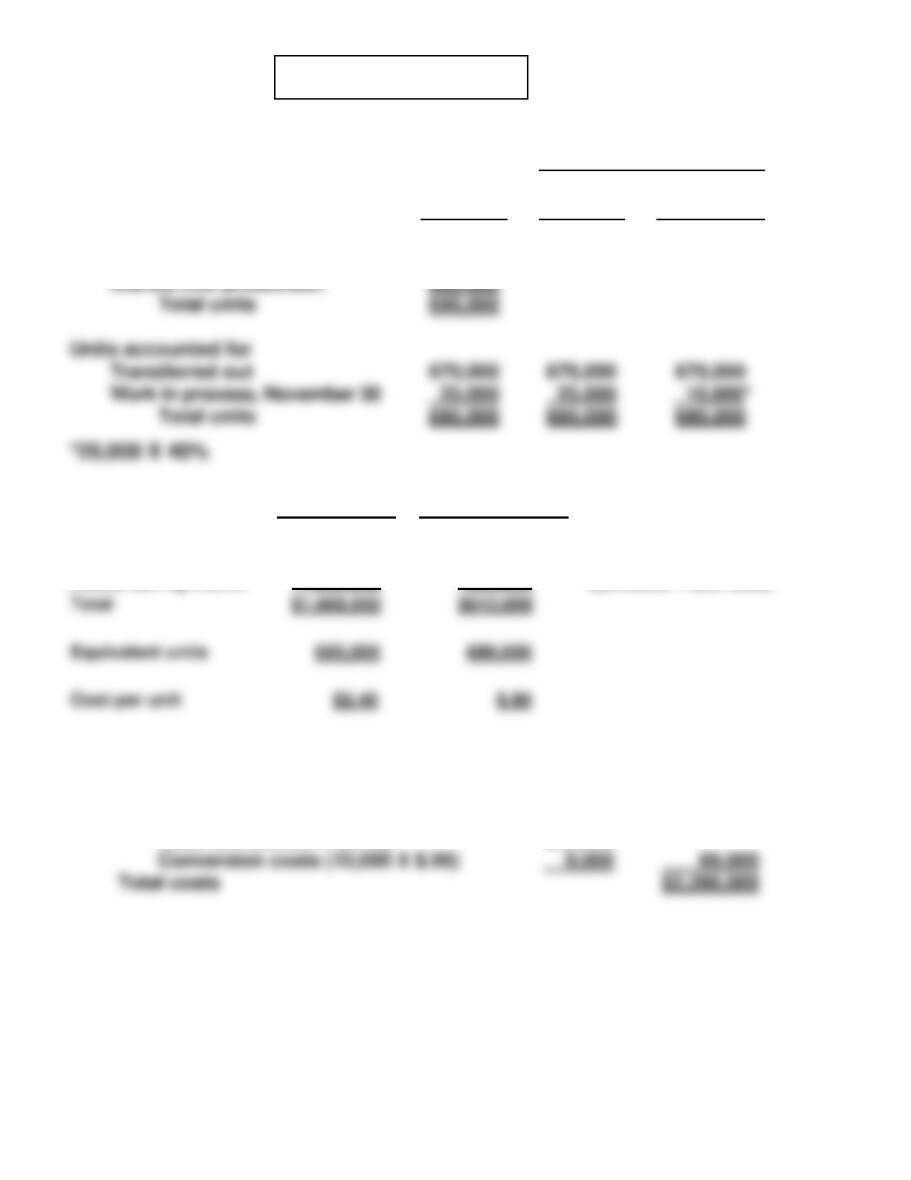

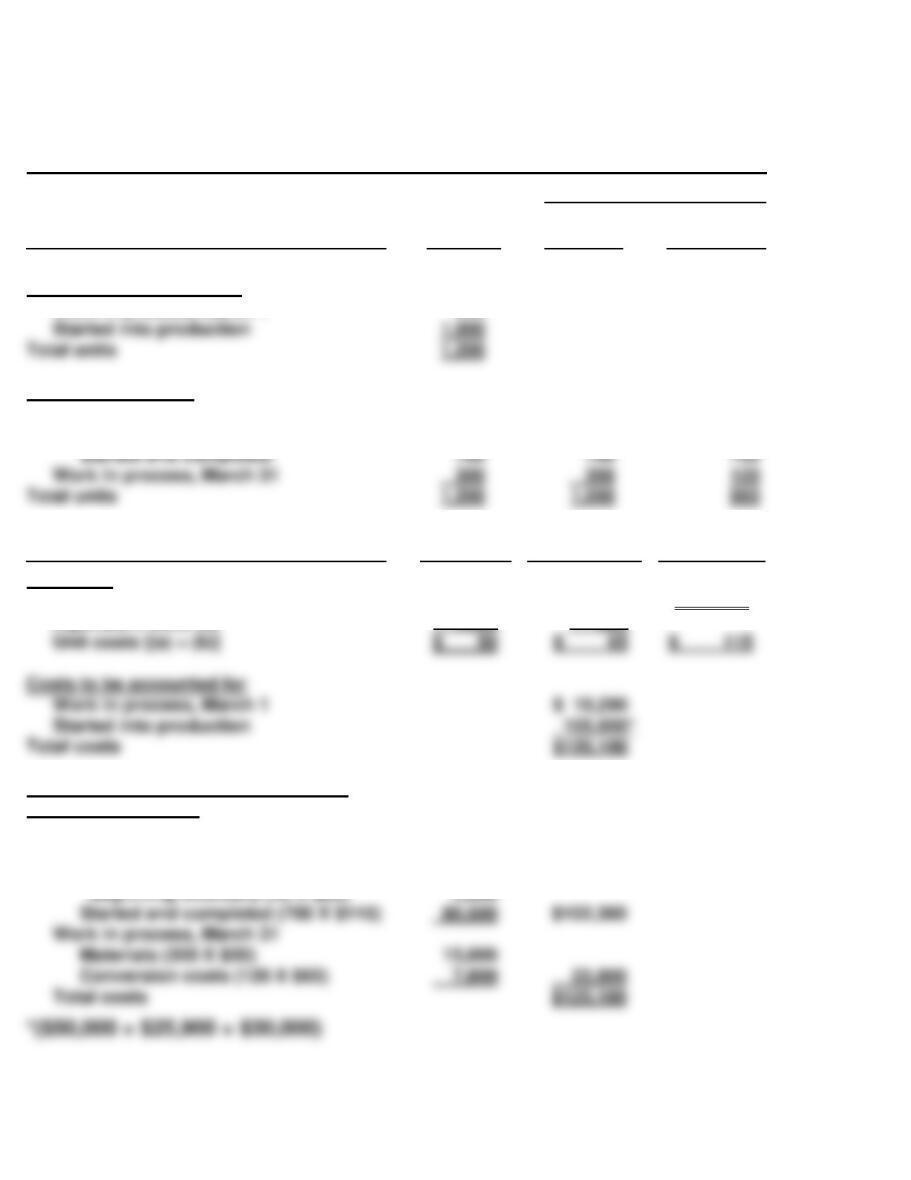

CD-3 DECISION-MAKING AT CURRENT DESIGNS

CURRENT DESIGNS

Fabrication Department

Production Cost Report

For the Month Ended April 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, April 1

Started into production

Total units

30

72

102

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Total cost*

Equivalent units

Unit costs [(a) ÷ (b)]

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (67 X $950)

Work in process, April 30

(a) $25,900

(b) 74

$ 350

$48,600

81

$ 600

$74,500

$ 950

$63,650

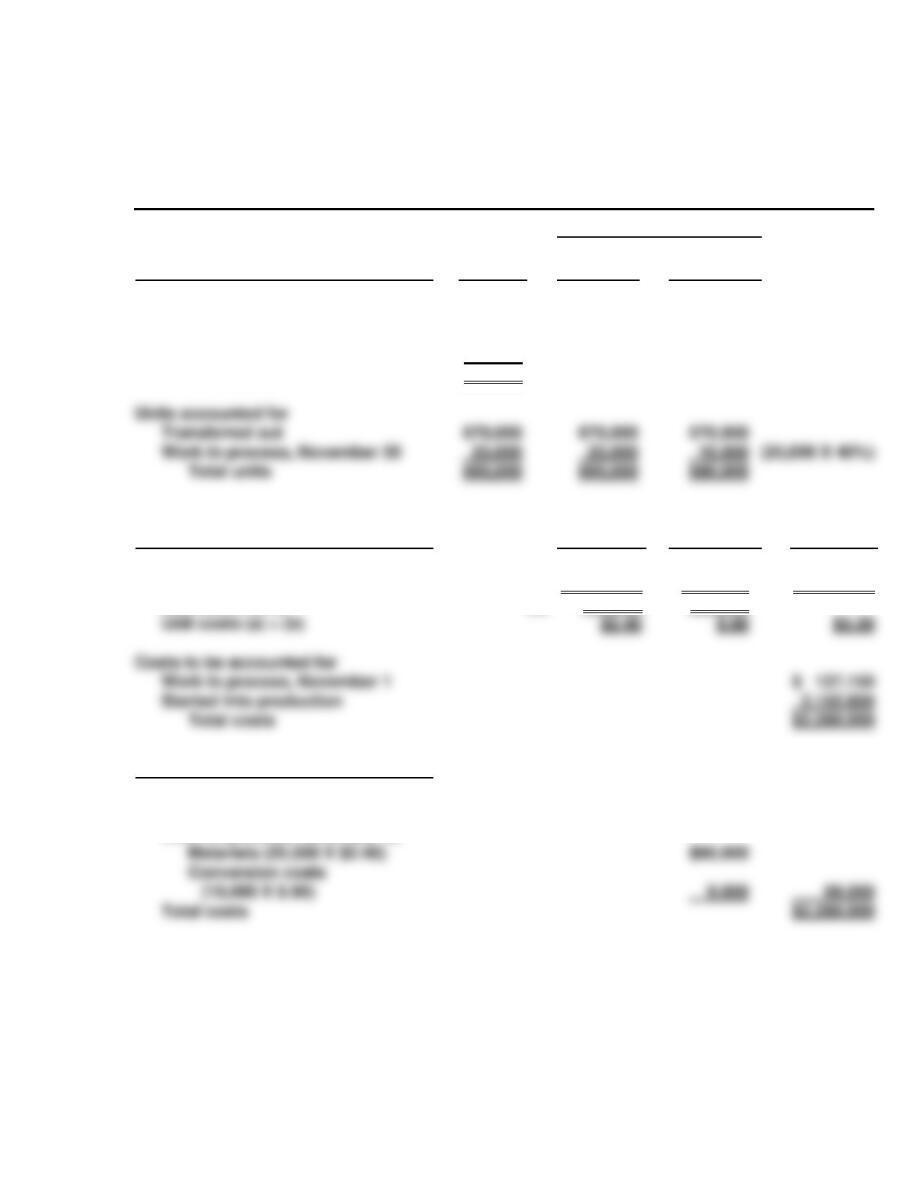

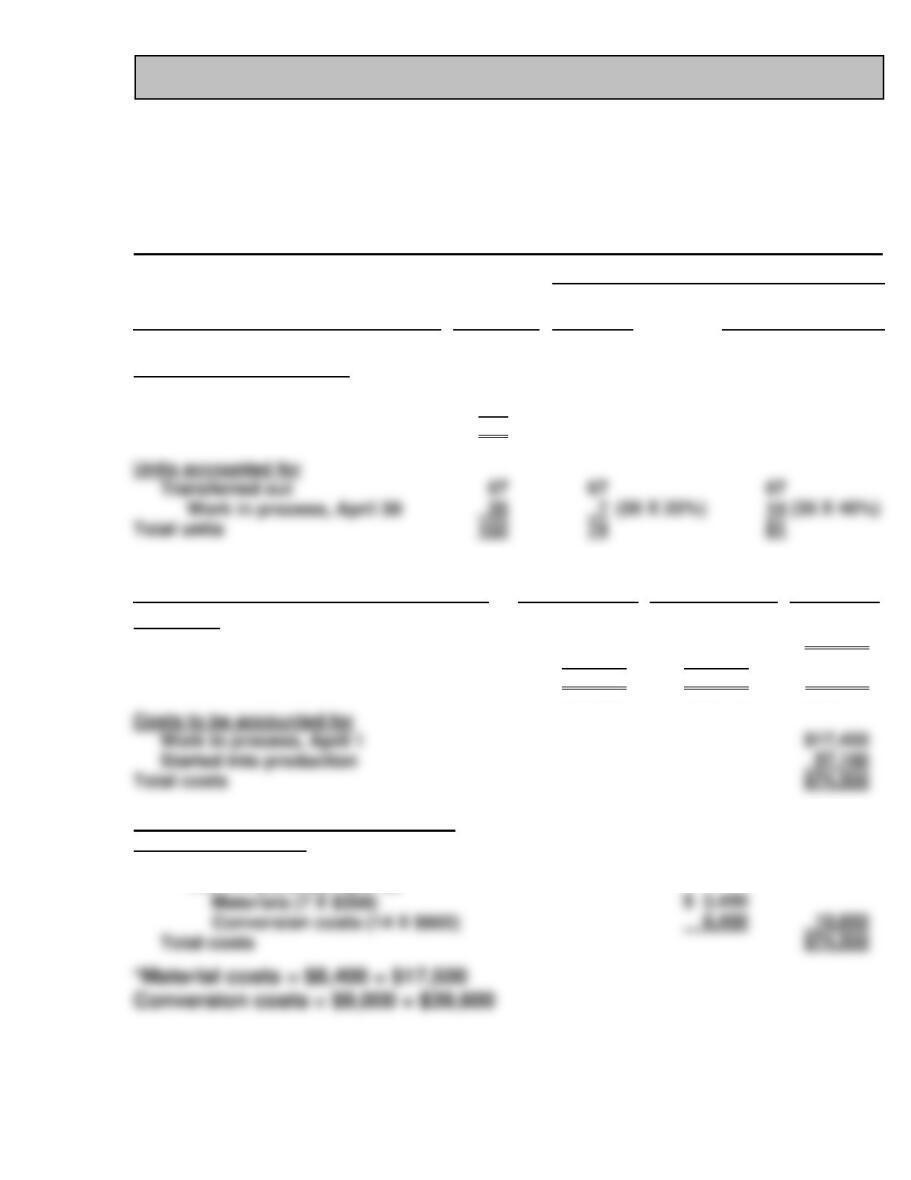

BYP 3-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) The unit cost suggests that Joe took the highest total costs and divided

these costs by the units started into production. The highest total costs

BYP 3-1 (Continued)

(c) FLORIDA BEACH COMPANY

Mixing Department

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, July 1

8,000

Costs

Materials

Conversion

Costs

Total

Total costs

Unit costs (Step 3)

Total cost

(a)

$594,000

$832,000

$1,426,000

Cost Reconciliation Schedule (Step 4)

Total costs

$1,426,000

Costs accounted for

Units accounted for

Transferred out

Work in process, July 31

(5,000 X 20%)

Total units

108,000

BYP 3-2 MANAGERIAL ANALYSIS

(a) The unit cost of materials is $150 ($450,000 ÷ 3,000).

(b) The materials cost of the goods transferred out is $375,000 (2,500 X

$150). Conversion costs, therefore, are $225,000 ($600,000 – $375,000),

BYP 3-3 REAL-WORLD FOCUS

(a) The outer shell of the paintballs is made from a mixture that includes

water, sweeteners, food ingredients, and most importantly, gelatin. All

of the ingredients used to make paintballs are food grade, biodegradable

products. The “paint” filling inside a paintball is comprised of the same

inert ingredient used in cough syrup, as well as crayon wax.

After mixing the gelatin and other materials, the mixture is heated, and

(b) Materials: water, sweeteners, food ingredients, gelatin, “cough syrup

material”, crayon wax, and food coloring.

Labor: People would be needed run the various machines.

(c) This would appear to be a perfect situation for the use of process

costing. Paintballs are a high volume product, and the paintballs are

very homogenous. While there may be some differences in various

BYP 3-4 COMMUNICATION ACTIVITY

To: Diane Barone, Regional Sales Manager

From: Student, Accounting Manager

Re: Production Cost Reports

Diane, congratulations again on your promotion! It’s going to be great

working with you. It kind of reminds me of our days at Dairy-Freeze after

school (although this work is more fun, and it certainly pays better!).

BYP 3-4 (Continued)

At the end of the month, we need to record what we finished and what still

remains undone. Equivalent units are the way we measure the amount of

work we have done on our work in process. It’s kind of like comparing the

contents of 4-ounce cups with the contents of 12–ounce cups. It doesn’t

make sense to compare by counting the number of cups you have. You

need to find out how many ounces you have in one set; then you can get a

BYP 3-5 ETHICS CASE

(a) The stakeholders in this situation are:

Jan Wooten, molding department head.

Tony Ferneti quality control inspector.

BYP 3-6 CONSIDERING PEOPLE, PLANET, AND PROFIT

(a) Some of the costs that the company now faces include:

• Monetary damages: The company paid $21.4 million in fines as a

result of an OSHA investigation; $1.6 billion to compensate those

affected by the accident; and $1 billion to repair and update its

refinery (plus an additional $250 million to install safety valves)

• Bad publicity

(b) Some steps that the company could have taken to reduce the environ–

mental failure costs include:

• Install up to date safety equipment

• Increase the frequency and efficacy of inspections