CCC3 (Continued)

(a) (Continued)

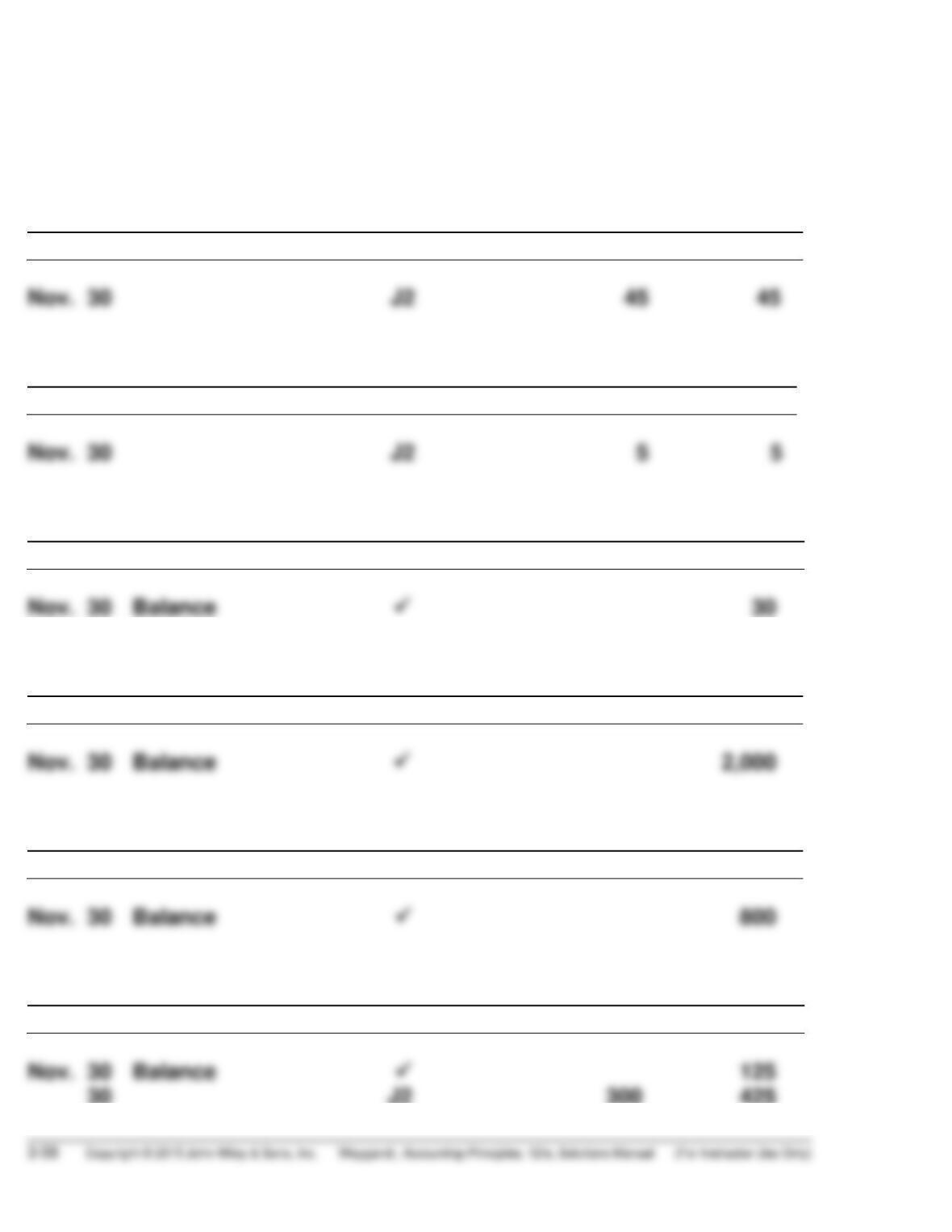

Accounts Payable

Date

Explanation

Ref.

Debit

Credit

Balance

Nov. 30 J2 45 45

Interest Payable

Date

Explanation

Ref.

Debit

Credit

Balance

Unearned Service Revenue

Date

Explanation

Ref.

Debit

Credit

Balance

Nov. 30 Balance ✓ 30

Notes Payable

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Nov. 30 Balance ✓ 800

Service Revenue

Date

Explanation

Ref.

Debit

Credit

Balance

30 J2 300 425

CCC3 (Continued)

(a) (Continued)

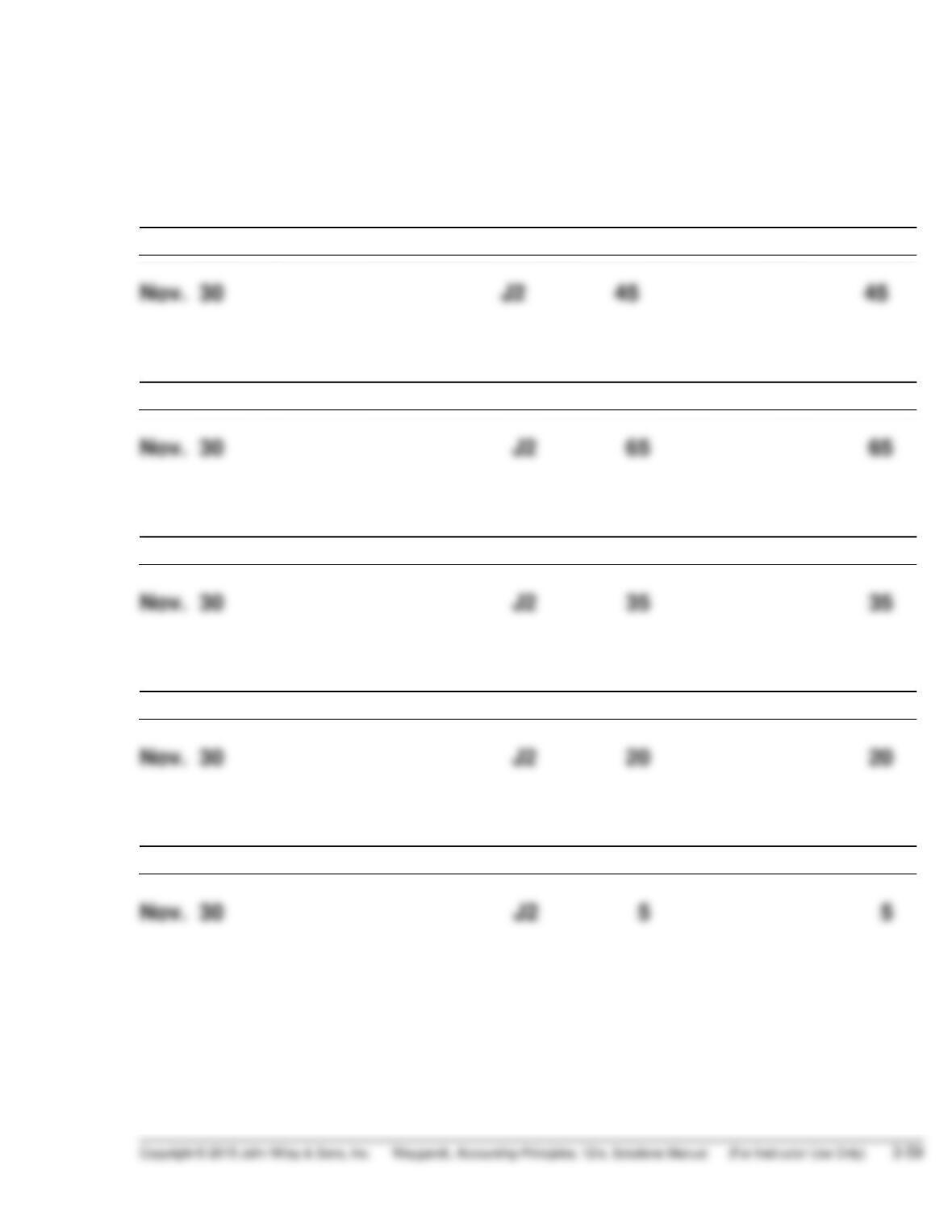

Utilities Expense

Date

Explanation

Ref.

Debit

Credit

Balance

Nov. 30 J2 45 45

Advertising Expense

Date

Explanation

Ref.

Debit

Credit

Balance

Supplies Expense

Date

Explanation

Ref.

Debit

Credit

Balance

Depreciation Expense

Date

Explanation

Ref.

Debit

Credit

Balance

Nov. 30 J2 20 20

Interest Expense

Date

Explanation

Ref.

Debit

Credit

Balance

CCC3 (Continued)

(b)

COOKIE CREATIONS

Adjusted Trial Balance

November 30, 2016

Account Debit Credit

Cash …………………………………………………………………… $ 245

Accounts Receivable …………………………………………… 300

Supplies ……………………………………………………………… 90

Interest Payable …………………………………………………… 5

Unearned Service Revenue ………………………………….. 30

Notes Payable ……………………………………………………… 2,000

Owner’s Capital …………………………………………………… 800

Service Revenue …………………………………………………. 425

Utilities Expense …………………………………………………. 45

Advertising Expense ……………………………………………. 65

CCC3 (Continued)

(c)

Revenues

Service revenue …………………………………………………… $425

Expenses

Advertising expense…………………………………………….. $65

Utilities expense ………………………………………………….. 45

Yes, Cookie Creations has been profitable in November. It has a profit of

$255 which is more than one half of the revenue earned in November.

COOKIE CREATIONS

Owner’s Equity Statement

For the Month Ended November 30, 2016

Owner’s Capital, November 1, 2016 ……………………………… $ 0

Add: Investment ………………………………………………………… 800

CCC3 (Continued)

(c) (Continued)

[Note: Balance Sheet is not required—shown for information purposes

only.]

COOKIE CREATIONS

Balance Sheet

November 30, 2016

Assets

Cash …………………………………………………………………….. $ 245

Accounts receivable ………………………………………………. 300

Supplies ……………………………………………………………….. 90

Liabilities and Owner’s Equity

Liabilities

Notes payable …………………………………………………… $2,000

Accounts payable …………………………..…………………. 45

BYP 3-1 FINANCIAL REPORTING PROBLEM

(a) Items that may result in adjusting entries for prepayments are:

1. Other current assets (per balance sheet).

2. Property, plant and equipment, net (per balance sheet).

(b) Accrual adjusting entries were probably made for accounts payable,

accrued expenses, and income taxes payable.

BYP 3-2 COMPARATIVE ANALYSIS PROBLEM

PepsiCo

Coca-Cola

(a)

Net increase (decrease) in property,

plant, and equipment (net) from 2012 to

2013.

$(561,000,000)

$31,000,000

(b)

and administrative expenses

from 2012 to 2013.

(c)

Increase (decrease) in long-term debt

(obligations) from 2012 to 2013.

$789,000,000

$861,000,000

Increase (decrease) in net income from

2012 to 2013.

Increase (decrease) in cash

and cash equivalents from 2012 to 2013.

$(378,000,000)

BYP 3-3 COMPARATIVE ANALYSIS PROBLEM

1.

Amazon

Wal-mart

(a)

Increase (decrease) in interest

expense, from 2012 to 2013.

$49,000,000

$(96,000,000)

(b)

Increase (decrease) in net income

from 2012 to 2013.

$313,000,000

$1,369,000,000

(c)

Increase (decrease) in cash from

$1,336,000,000

BYP 3-4 REAL–WORLD FOCUS

Answers will vary depending on the company and article chosen by

the student.

BYP 3-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) HAPPY CAMPER PARK

Income Statement

For the Quarter Ended March 31, 2017

Revenues

Rent revenue ($90,000 – $15,000) ……………. $75,000

Expenses

Salaries and wages expense

[$29,800 + ($300 X 2)] …………………………... $30,400

Advertising expense ($5,200 + $110) ……….. 5,310

(b) The generally accepted accounting principles pertaining to the income

statement that were not recognized by Erica were the revenue recognition

principle and the expense recognition principle. The revenue recognition

principle states that revenue is recognized when the performance

obligation is satisfied. The $15,000 for summer rentals has not been

BYP 3-6 COMMUNICATION ACTIVITY

Dear Ms. Taylor:

Upon reviewing the accounts of your company at the end of the year,

I discovered that adjusting entries were not made.

Adjusting entries are made at the end of the accounting period to ensure

that the revenue recognition and expense recognition principles required

under generally accepted accounting principles are followed. The use of

Adjusting entries are needed because the trial balance may not contain an

up–to-date and complete record of transactions and events for the

following reasons:

1. Some events are not journalized daily because it is not efficient to

do so. Examples are the use of supplies and the earning of wages

by employees.

There are four types of adjusting entries:

1. Prepaid expenses—expenses paid in cash and recorded as assets

before they are used or consumed.

2. Unearned revenues—revenues received in cash and recorded as

liabilities before they are earned.

BYP 3-6 (Continued)

3. Accrued revenues—revenues earned but not yet received in cash

or recorded.

4. Accrued expenses—expenses incurred but not yet paid in cash or

recorded.

BYP 3-7 ETHICS CASE

(a) The stakeholders in this situation are:

Zoe Baas, controller.

The president of Russell Company.

Russell Company stockholders.

(b) 1. It is unethical for the president to place pressure on Zoe to misstate

net income by requesting her to prepare incorrect adjusting entries.

BYP 3-8 ALL ABOUT YOU

We address the issue of contingent liabilities in greater detail in Chapter

11. Our primary interest in this exercise is to engage students in a

discussion regarding the general nature of the financial statement

elements (assets, liabilities, equity, revenues and expenses).

(a) By taking out the bank loan your friend has incurred a liability. You do

not have a liability unless your friend defaults, or unless it becomes

clear that he will default. The loan application may, however, require you

to disclose any guarantees that you have signed, since they represent

potential liabilities.

(c) Losing your job would not create a financial liability, although it would

most certainly reduce your revenues. You are obviously concerned that

you might lose your job, but you don’t have specific information that

would suggest that it will happen. Therefore, you probably don’t have

an obligation to disclose this information to the bank. However, unless

BYP 3-9 CONSIDERING PEOPLE, PLANET, AND PROFIT

The balance sheet should provide a fair representation of what a company

owns and what it owes. If significant obligations of the company are not

reported on the balance sheet, the company’s net worth (its equity) will be

overstated. While it is true that it is not possible to estimate the exact

amount of future environmental cleanup costs, it is becoming clear that

companies will be held accountable.

BYP 3-10 FASB CODIFICATION ACTIVITY

(a) Revenues are inflows or other enhancements of assets of an entity or

settlements of its liabilities (or a combination of both) from delivering

or producing goods, rendering services, or other activities that

constitute the entity’s ongoing major or central operations.

IFRS 3-1 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Note 3.7 indicates that revenue is measured as the fair value of

consideration received or receivable by the Group for goods supplied

net of sales rebates and excluding VAT and trade discounts.

(b) Note 3.7 states that revenue from the sale of goods is recognized when

the Group has transferred to the buyer the significant risks and

rewards of ownership of the goods.