CHAPTER 3

Adjusting the Accounts

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Explain the accrual basis of

accounting and the reasons

for adjusting entries.

1, 2, 3, 4, 5,

6, 7, 8, 18

1, 2, 8

1

1, 2, 3, 4, 6,

10, 11

*2. Prepare adjusting entries for

deferrals.

8, 9, 10, 11,

12, 13, 18,

19, 20

2, 3, 4, 5, 6,8

2

4, 5, 6, 7, 8,

9, 10, 11, 12,

13, 15

1A, 2A, 3A,

4A, 5A, 6A

*3. Prepare adjusting entries for

8, 14, 15, 16,

2, 7, 8

3

4, 5, 6, 7, 8,

1A, 2A, 3A,

*4. Describe the nature and

purpose of an adjusted trial

21

9, 10

4

10, 11, 13,

14

1A, 2A, 3A,

5A, 6A

*5. Prepare adjusting entries for

the alternative treatment of

deferrals.

22

11

16, 17

6A

*6. Discuss financial reporting

concepts.

23, 24, 25,

26, 27, 28

12, 13, 14,

15

18, 19, 20,

21, 22

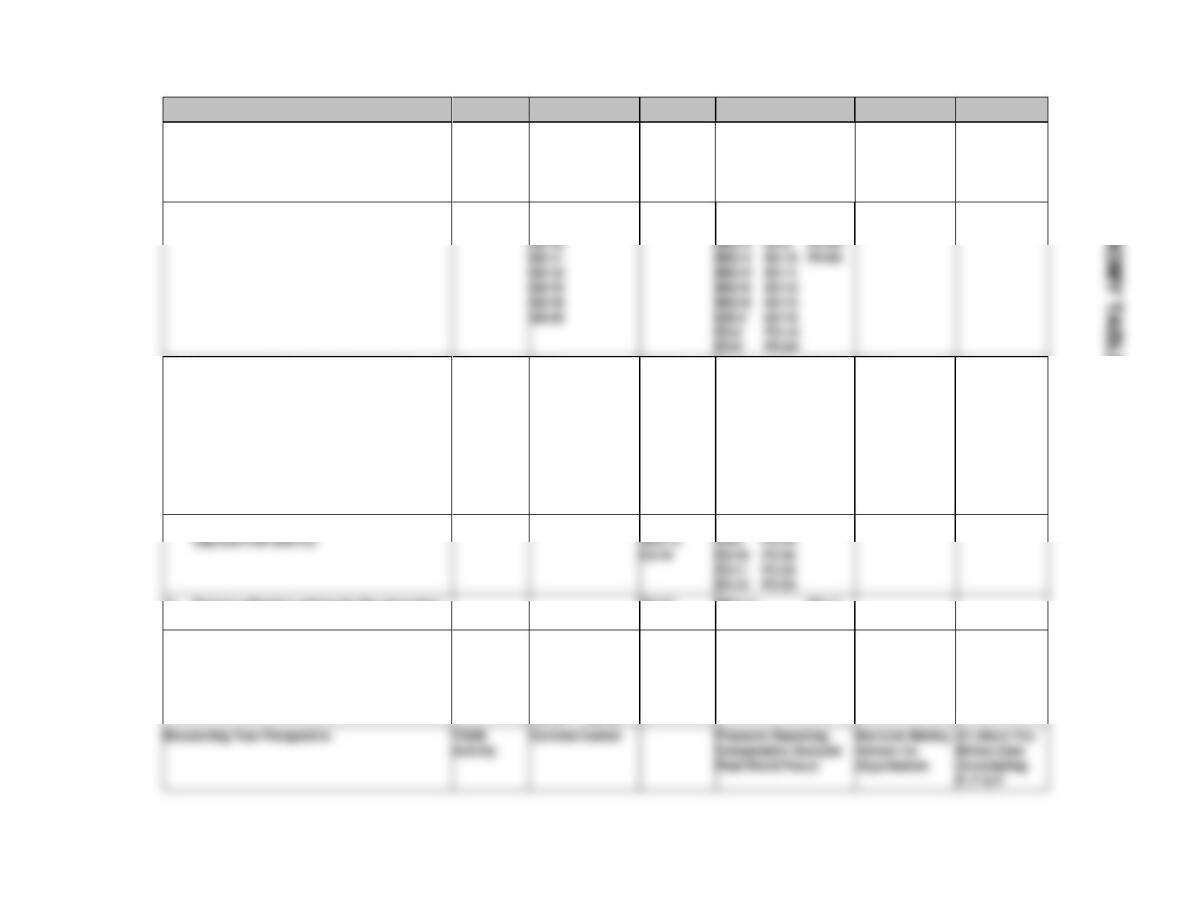

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare adjusting entries, post to ledger accounts,

and prepare an adjusted trial balance.

Simple

40–50

2A

Prepare adjusting entries, post, and prepare adjusted

trial balance, and financial statements.

Simple

50–60

3A

Prepare adjusting entries and financial statements.

Moderate

40–50

4A

Prepare adjusting entries.

Moderate

30–40

Prepare adjusting entries, adjusted trial balance,

40–50

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 3

ADJUSTING THE ACCOUNTS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Simple

4–6

BE2

1, 2

AN

Moderate

6–8

BE3

2

AN

Simple

3–5

BE4

2

AN

Simple

3–5

BE5

2

AN

Simple

2–4

BE6

2

AN

Simple

2–4

BE7

3

AN

Simple

4–6

BE8

AN

Simple

5–7

BE9

4

AP

Simple

4–6

BE10

4

AP

Simple

2–4

BE11*

5

AN

Moderate

3–5

BE12*

6

C

Simple

3–5

BE13*

6

C

Simple

2–4

BE14*

6

C

Simple

2–4

BE15*

6

C

Simple

1–2

DI1

1

K

Simple

2–4

DI2

2

AN

Simple

6–8

DI3

3

AN

Simple

4–6

DI4

4

AN

Moderate

20–30

EX1

1

C

Simple

3–5

EX2

1

E

Moderate

10–15

EX3

1

AP

Simple

6–8

EX4

AN

Simple

5–6

EX5

2, 3

AN

Moderate

10–15

EX6

AN

Moderate

10–12

EX7

2, 3

AN

Moderate

8–10

EX8

2, 3

AN

Moderate

8–10

EX9

2, 3

AN

Simple

8–10

EX10

AN

Moderate

8–10

EX11

1–4

AN

Moderate

12–15

EX12

AN

Moderate

8–10

EX13

2–4

AN

Simple

8–10

ADJUSTING THE ACCOUNTS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX15

2, 3

AN, S

Moderate

8–10

EX16*

5

AN

Moderate

6–8

EX17*

5

AN

Moderate

10–12

EX18*

Simple

EX19*

6

C

Simple

EX20*

6

C

Simple

EX21*

AN

Simple

10–20

EX22*

6

AN

Simple

10–20

P1A

2–4

AN

Simple

40–50

P2A

2–4

AN

Simple

50–60

P3A

2–4

AN

Moderate

40–50

P4A

2, 3

AN

Moderate

30–40

P5A

2–4

AN

Moderate

60–70

P6A

2–5

AN

Moderate

40–50

BYP1

AN

Simple

10–15

BYP2

—

AN

Simple

10–15

BYP3

AN

Simple

10–15

BYP4

AN

Simple

10–15

BYP5

—

AN

Moderate

15–20

BYP6

1–4

S

Moderate

15–20

BYP7

1–4

C

Simple

10–15

BYP8

1–4

Moderate

10–15

BYP9

E

Moderate

10–15

BYP10

E

Moderate

10–15

BYP11

—

Simple

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Explain the accrual basis of accounting and

the reasons for adjusting entries.

DI3-1

Q3-1

Q3-2

Q3-3

Q3-4

Q3-6

Q3-7

Q3-8

BE3-1

E3-1

Q3-5

E3-3

Q3–18

BE3-2

BE3-8

E3-4

E3–10

E3–11

E3-2

*2. Prepare adjusting entries for deferrals.

Q3-8

Q3-9

Q3–18

BE3-2

E3-7

E3-8

P3–3A

P3–4A

E3–15

*3. Prepare adjusting entries for accruals.

Q3-8

Q3–14

Q3–15

Q3–19

Q3–20

Q3–17

Q3–16

Q3–18

BE3-2

BE3-7

BE3-8

DI3-3

E3-4

E3-5

E3-6

E3-7

E3-8

E3-9

E3–10

E3–11

E3–12

E3–13

E3–15

P3–1A

P3–2A

P3–3A

P3–4A

P3–5A

P3–6A

E3–15

*4. Describe the nature and purpose of an

Q3–21

BE3-9

DI3-4

P3–1A

*5. Prepare adjusting entries for the alternative

treatment of deferrals.

Q3–22

BE3-11

E3–16

E3–17

P3–6A

*6. Discuss financial reporting concepts

Q3–23

BE3-12 E3-20

BE3-13 Q3-24

BE3-14 Q3-25

BE3-15 Q3-26

E3-18 Q3–27

E3-19 Q3–28

E3–21

E3–22

ANSWERS TO QUESTIONS

1. (a) Under the time period assumption, an accountant is required to determine the relevance of

each business transaction to specific accounting periods.

(b) An accounting time period of one year in length is referred to as a fiscal year. A fiscal year

that extends from January 1 to December 31 is referred to as a calendar year. Accounting

periods of less than one year are called interim periods.

4. Information presented on an accrual basis is more useful than on a cash basis because it reveals

relationships that are likely to be important in predicting future results. To illustrate, under accrual

accounting, revenues are recognized when the performance obligation is satisfied so they can be

related to the economic environment in which they occur. Trends in revenues are thus more

meaningful.

5. Expenses of $4,500 should be deducted from the revenues in April. Under the expense

recognition principle efforts (expenses) should be matched with accomplishments (revenues).

6. No, adjusting entries are required by the revenue recognition and expense recognition principles.

7. A trial balance may not contain up-to-date information for financial statements because:

(1) Some events are not journalized daily because it is not efficient to do so.

(2) The expiration of some costs occurs with the passage of time rather than as a result of daily

transactions.

(3) Some items may be unrecorded because the transaction data are not yet known.

12. Equipment ………………………………………………………………………………….. $18,000

Less: Accumulated Depreciation—Equipment …………………………………. 6,000 $12,000

Questions Chapter 3 (Continued)

*13. In the adjusting entry for an unearned revenue, a liability is debited and a revenue is credited.

*14. Asset and revenue. An asset would be debited and a revenue would be credited.

*15. An expense is debited and a liability is credited in the adjusting entry.

*18. (a) Accrued revenues. (d) Accrued expenses or prepaid expenses.

(b) Unearned revenues. (e) Prepaid expenses.

(c) Accrued expenses. (f) Accrued revenues or unearned revenues.

*19. (a) Salaries and Wages Payable. (d) Supplies Expense.

*20. Disagree. An adjusting entry affects only one balance sheet account and one income statement

account.

*21. Financial statements can be prepared from an adjusted trial balance because the balances of

all accounts have been adjusted to show the effects of all financial events that have occurred

during the accounting period.

*22. For Supplies Expense (prepaid expense): expenses are overstated and assets are understated.

The adjusting entry is:

Assets (Supplies) …………………………………………………………………………. XX

**23. (a) The primary objective of financial reporting is to provide financial information that is useful to

investors and creditors for making decisions about providing capital.

(b) The fundamental qualitative characteristics are relevance and faithful representation. The

enhancing qualities are comparabiIity, consistency, verifiability, timeliness, and

understandability.

Questions Chapter 3 (Continued)

*25. Comparability results when different companies use the same accounting principles.

Consistency means using the same accounting principles and methods from year to year within

the same company.

*26. The constraint is the cost constraint. The cost constraint allows accounting standard setters to

weigh the cost that companies will incur to provide information against the benefit that financial

statement users will gain from having the information available.

*27. Accounting relies primarily on two measurement principles. Fair value is sometimes used when

market price information is readily available. However, in many situations reliable market price

SOLUTIONS TO BRIEF EXERCISES

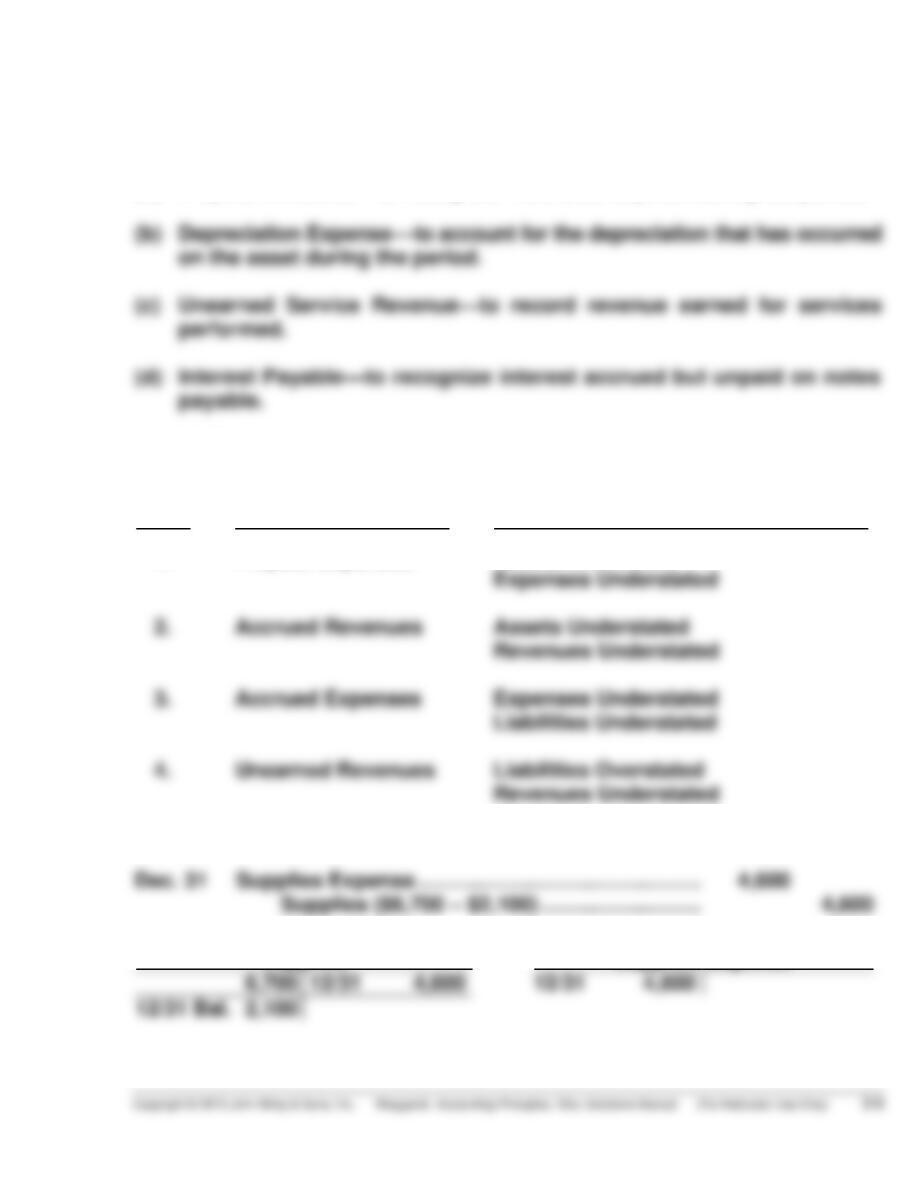

BRIEF EXERCISE 3-1

(a) Prepaid Insurance—to recognize insurance expired during the period.

(b) Depreciation Expense—to account for the depreciation that has occurred

on the asset during the period.

BRIEF EXERCISE 3-2

Item

(a)

Type of Adjustment

(b)

Account Balances before Adjustment

1.

Prepaid Expenses

Assets Overstated

Expenses Understated

2.

Accrued Revenues

Assets Understated

Revenues Understated

3.

Accrued Expenses

Expenses Understated

Liabilities Understated

4.

Unearned Revenues

Liabilities Overstated

Revenues Understated

BRIEF EXERCISE 3-3

Dec. 31 Supplies Expense ………………………………………… 4,600

Supplies

Supplies Expense

6,700

12/31 4,600

12/31 4,600

12/31 Bal. 2,100

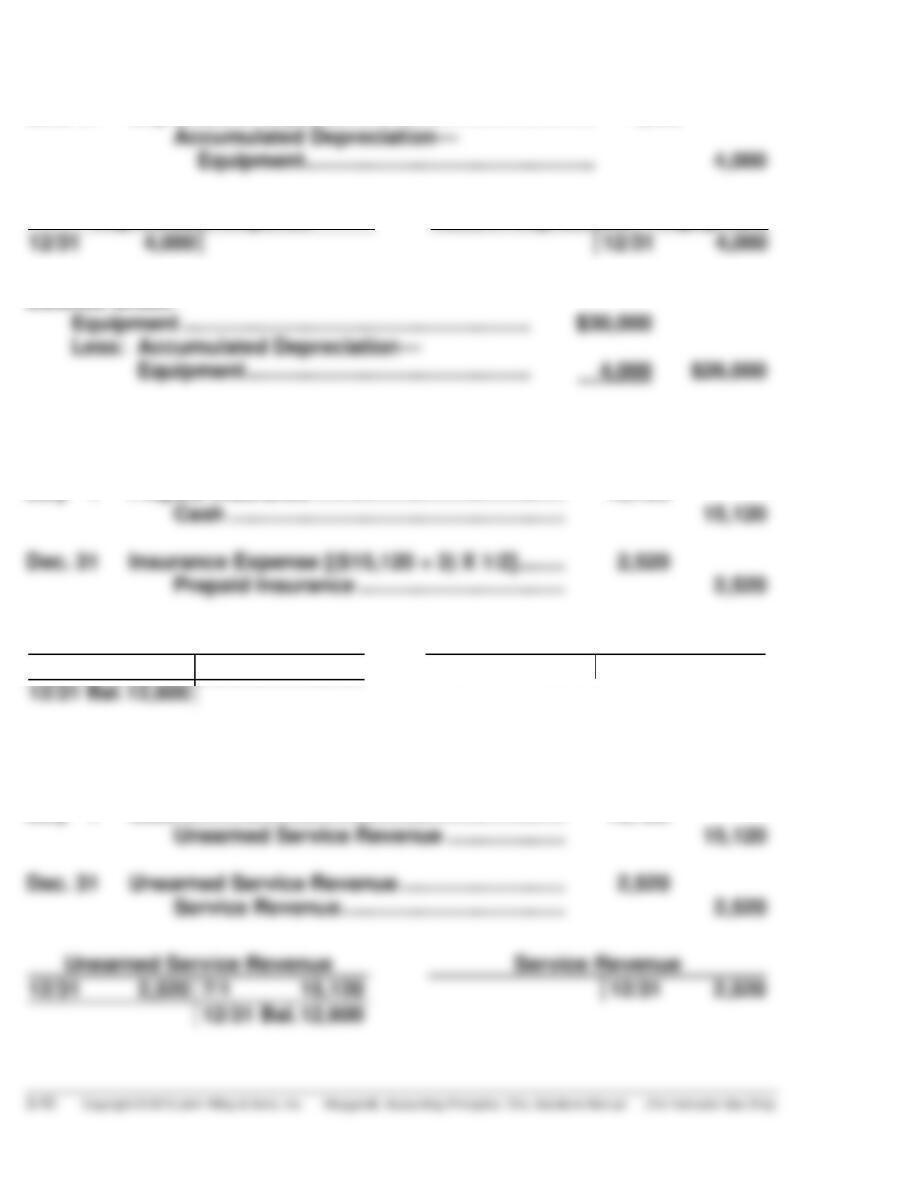

BRIEF EXERCISE 3-4

Dec. 31 Depreciation Expense …………………………………… 4,000

Accumulated Depreciation—

Equipment …………………………………………. 4,000

Depreciation Expense

Accum. Depreciation—Equipment

12/31 4,000

12/31 4,000

Balance Sheet:

BRIEF EXERCISE 3-5

July 1 Prepaid Insurance ……………………………………. 15,120

Cash ………………………………………………… 15,120

Prepaid Insurance

Insurance Expense

7/1 15,120

12/31 2,520

12/31 2,520

BRIEF EXERCISE 3-6

July 1 Cash ……………………………………………………….. 15,120

Unearned Service Revenue ……………….. 15,120

Dec. 31 Unearned Service Revenue ………………………. 2,520

Service Revenue ……………………………….. 2,520

12/31 2,520

7/1 15,120

12/31 2,520

BRIEF EXERCISE 3-7

1. Dec. 31 Interest Expense …………………………………… 400

Interest Payable ……………………………… 400

BRIEF EXERCISE 3-8

Account

(a)

Type of Adjustment

(b)

Related Account

Accounts Receivable

Accrued Revenues

Service Revenue

Prepaid Insurance

Prepaid Expenses

Insurance Expense

Prepaid Expenses

Depreciation Expense

Interest Payable

Accrued Expenses

Interest Expense

Unearned Service Revenue

Unearned Revenues

Service Revenue

BRIEF EXERCISE 3-9

WILDER COMPANY

Income Statement

For the Year Ended December 31, 2017

Revenues

Service revenue ……………………………………………. $39,000

Expenses

Salaries and wages expense …………………………. $16,000

BRIEF EXERCISE 3-10

WILDER COMPANY

Owner’s Equity Statement

For the Year Ended December 31, 2017

Owner’s capital, January 1 ……………………………………………………. $15,600

Add: Net income …………………………..……………………………………… 14,200

*BRIEF EXERCISE 3-11

(a) Apr. 30 Supplies ……………………………………………….. 400

Supplies Expense …………………………... 400

BRIEF EXERCISE 3-12

(a) Predictive value.

(b) Confirmatory value.

BRIEF EXERCISE 3-13

(a) Relevant.

BRIEF EXERCISE 3-14

(a) 1. Predictive value.

BRIEF EXERCISE 3-15

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 3-1

DO IT! 3-2

1. Insurance Expense ………………………………………………. 300

Prepaid Insurance …………………………………………. 300

(To record insurance expired)

2. Supplies Expense ($2,500 – $1,100) ………………………. 1,400

DO IT! 3-3

1. Salaries and Wages Expense ……………………………….. 1,300

Salaries and Wages Payable…………………………... 1,300

(To record accrued salaries)

DO IT! 3-4

(a) The net income is determined by adding revenues and subtracting

expenses. The net income is computed as follows:

Revenues

Service revenue………………………………………… $11,360

Rent revenue ……………………………………………. 1,100

(b) Total assets and liabilities are computed as follows:

Assets

Cash ………………………………………………………… $ 5,360

Accounts receivable …………………………………. 480

Liabilities

Notes payable …………………………………………… $ 4,000

Accounts payable …………………………………….. 790

(c) Owner’s Capital at June 30, 2017, can be computed in one of two ways.

Using the basic accounting equation (Assets = Liabilities + Owner’s

Equity), we find that total assets are $18,780 and total liabilities are

$5,530; therefore, Owner’s Equity (Owner’s Capital) is $13,250 ($18,780 –

$5,530).

Another way to compute the Owner’s Capital at June 30, 2017, is as

follows:

SOLUTIONS TO EXERCISES

EXERCISE 3-1

1. True.

2. True.

3. False. Many business transactions affect more than one of these artificial

time periods. For example, the purchase of a building affects expenses

for many years.

EXERCISE 3-2

(a) Accrual-basis accounting records the transactions that change a

company’s financial statements in the periods in which the events

occur rather than in the periods in which the company receives or pays

(b) Politicians might desire a cash-basis accounting system over an accrual-

basis system because if an accrual-accounting system is used, it could

EXERCISE 3-2 (Continued)

(c) Dear Senator,

It is my understanding, after having taken a beginning course in account-

ing principles, that the Federal government uses a cash-basis system

rather than an accrual-basis accounting system.

I am shocked at such a practice! There must be billions of dollars of

EXERCISE 3-3

(a) Cash received from revenue……………………………………. $108,000

Cash paid for expenses ………………………………………….. (72,000)

EXERCISE 3-4

1. Unearned revenue.

2. Accrued expense.

3. Accrued expense.

EXERCISE 3-5

1. Interest Expense ……………………………………………. 300

Interest Payable

($10,000 X 9% X 4/12) …………………………….. 300

2. Supplies Expense ………………………………………….. 1,550

Supplies ($2,450 – $900) …………………………... 1,550

3. Depreciation Expense …………………………………….. 1,000

Accumulated Depreciation—Equipment ……. 1,000

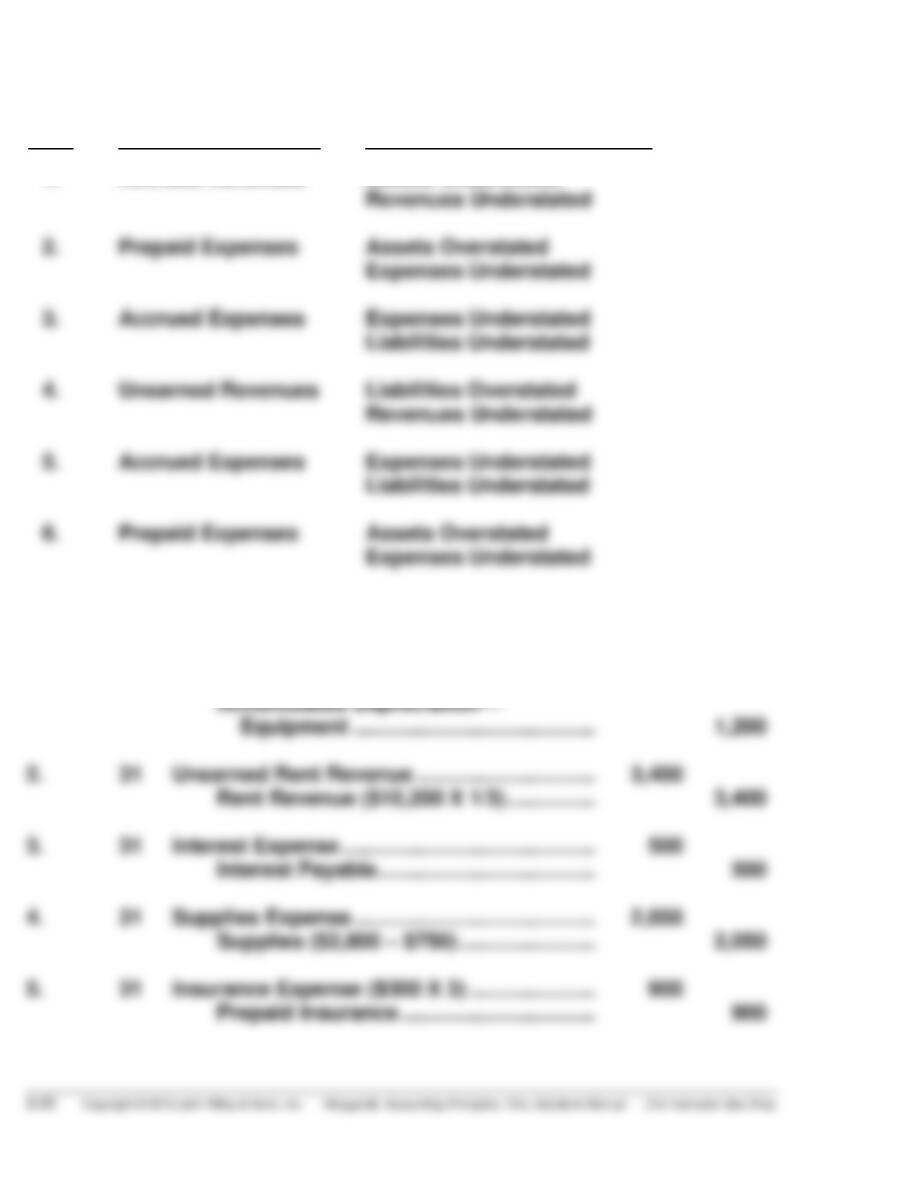

EXERCISE 3-6

Item

(a)

Type of Adjustment

(b)

Accounts before Adjustment

1.

Accrued Revenues

Assets Understated

Revenues Understated

2.

Assets Overstated

Expenses Understated

3.

Accrued Expenses

Expenses Understated

Liabilities Understated

4.

Unearned Revenues

Liabilities Overstated

Revenues Understated

5.

Accrued Expenses

Expenses Understated

EXERCISE 3-7

1. Mar. 31 Depreciation Expense ($400 X 3) …………….. 1,200

Accumulated Depreciation—

Equipment ………………………………….. 1,200