1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and

3. Adjusting entries are necessary at the end of an accounting period to bring the ledger up to date.

5. Four different categories of adjusting entries include prepaid expenses (deferred expenses), unearned

6. Statement (a): Increases the balance of a revenue account.

8. Yes, because every adjusting entry affects expenses or revenues.

9. a. The rights acquired represent an asset.

10. a. The portion of the cost of a fixed asset deducted from revenue of the period is debited to

Depreciation Expense. It is the expired cost for the period. The reduction in the fixed asset

account is recorded by a credit to Accumulated Depreciation rather than to the fixed asset

CHAPTER 3

THE ADJUSTING PROCESS

DISCUSSION QUESTIONS

3-1

CHAPTER 3 The Adjusting Process

PE 3–1A

PE 3–1B

PE 3–2A

PE 3–2B

PE 3–3A

Supplies Expense 6,845

Supplies 6,845

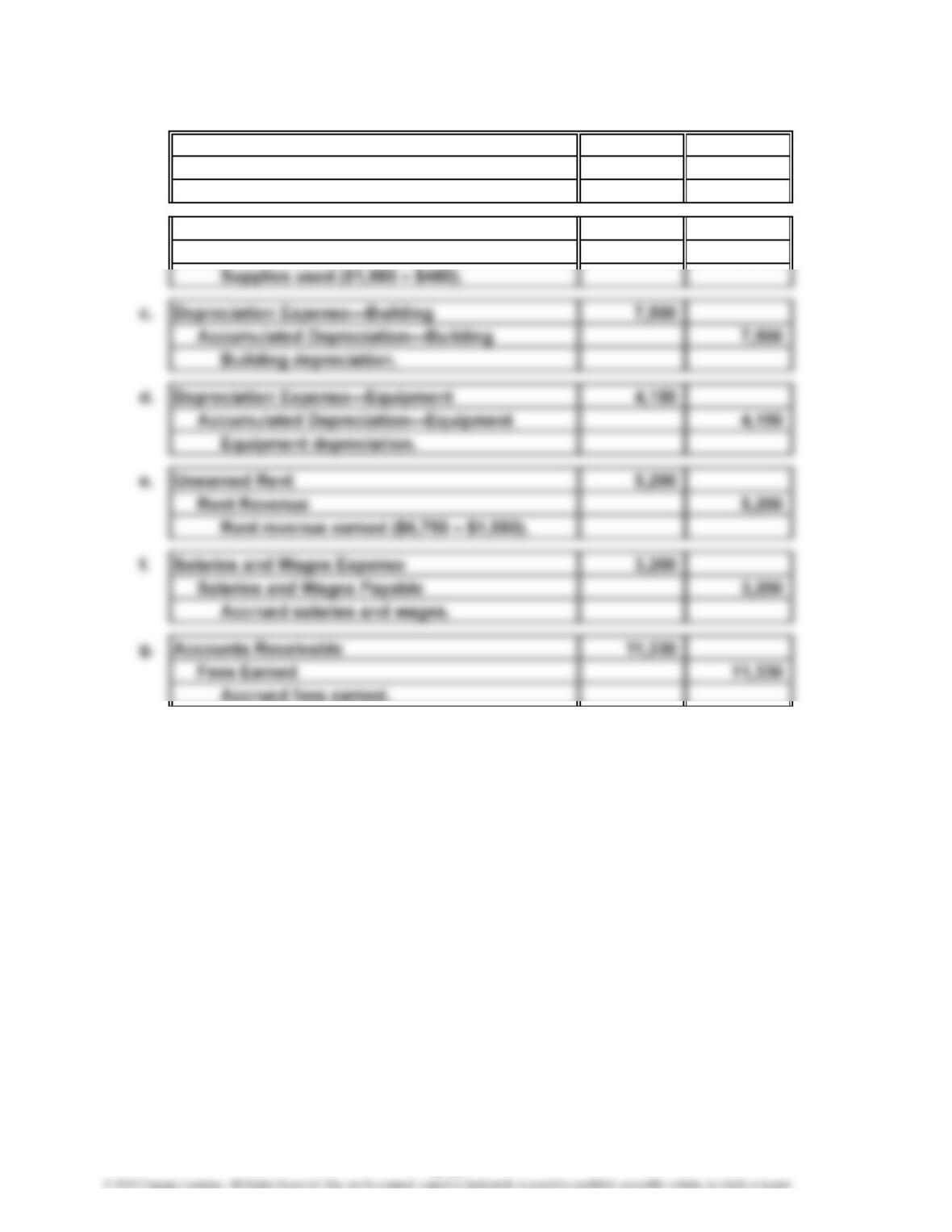

Supplies used ($3,375 + $6,450 – $2,980).

PE 3–3B

PE 3–4A

Unearned Fees 82,750

Fees Earned 82,750

Fees earned ($272,500 – $189,750).

PE 3–4B

PRACTICE EXERCISES

PE 3–5A

PE 3–5B

PE 3–6A

Salaries Expense 7,080

Salaries Payable 7,080

Accrued salaries [($11,800 ÷ 5 days) × 3 days].

PE 3–6B

PE 3–7A

Depreciation Expense 6,880

Accumulated Depreciation—Equipment 6,880

Depreciation on equipment.

PE 3–7B

3-3

CHAPTER 3 The Adjusting Process

PE 3–8A

PE 3–8B

PE 3–9A

PE 3–9B

PE 3–10A

a.

Amount Percent Amount Percent

Fees earned $725,000 100% $615,000 100%

PE 3–10B

a.

Amount Percent Amount Percent

Fees earned $1,640,000 100% $1,300,000 100%

2016 2015

Income Statements

For Years Ended December 31

HEMLOCK COMPANY

For Years Ended December 31

Income Statements

CORNEA COMPANY

20152016

3-5

CHAPTER 3 The Adjusting Process

Ex. 3–1

1. Prepaid expense 5. Unearned revenue

3. Unearned revenue 7. Accrued expense

Ex. 3–2

Accounts Receivable……………………

…

Normally requires adjustment (AR).

Cash…………………………………………

…

Does not normally require adjustment.

EXERCISES

Account Answer

3-6

CHAPTER 3 The Adjusting Process

Ex. 3–6

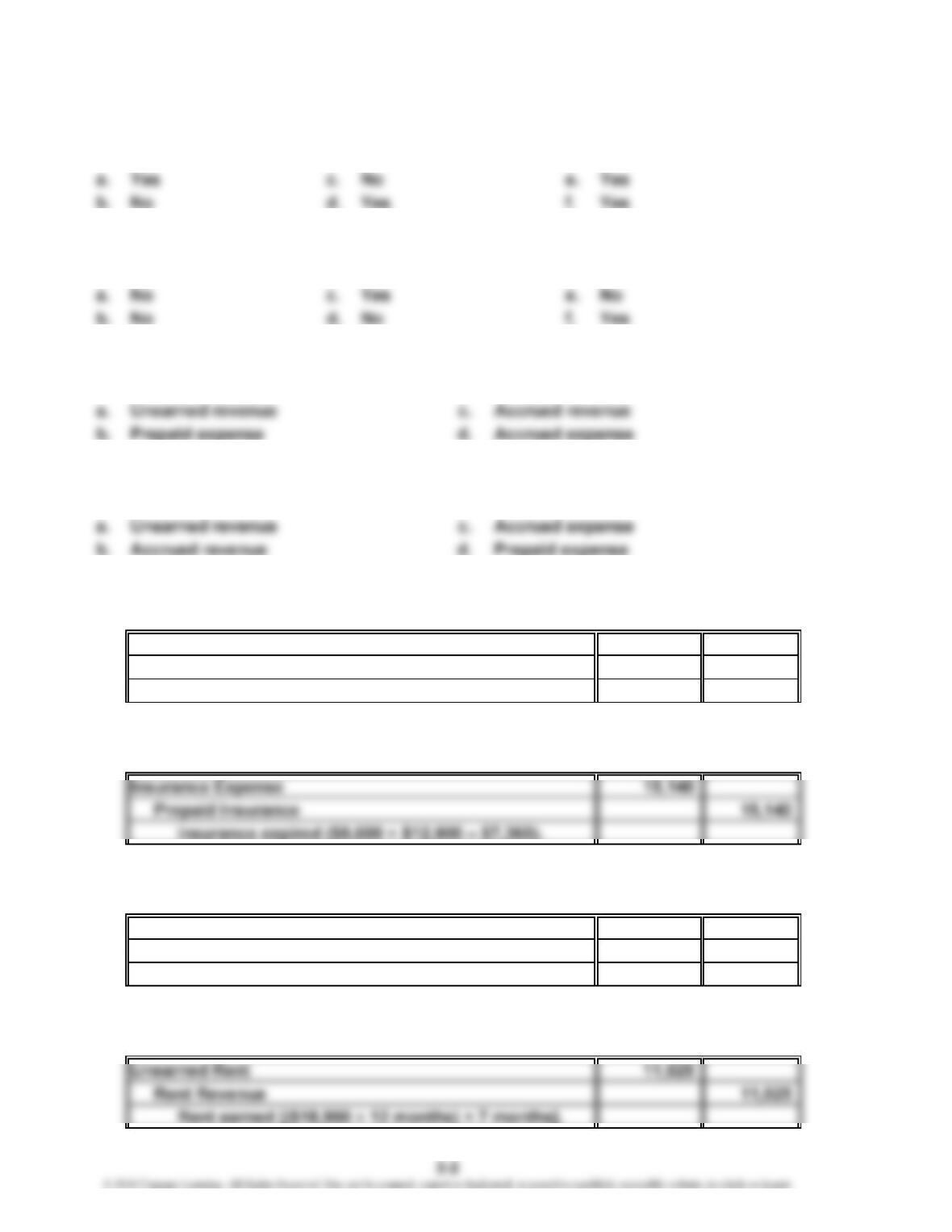

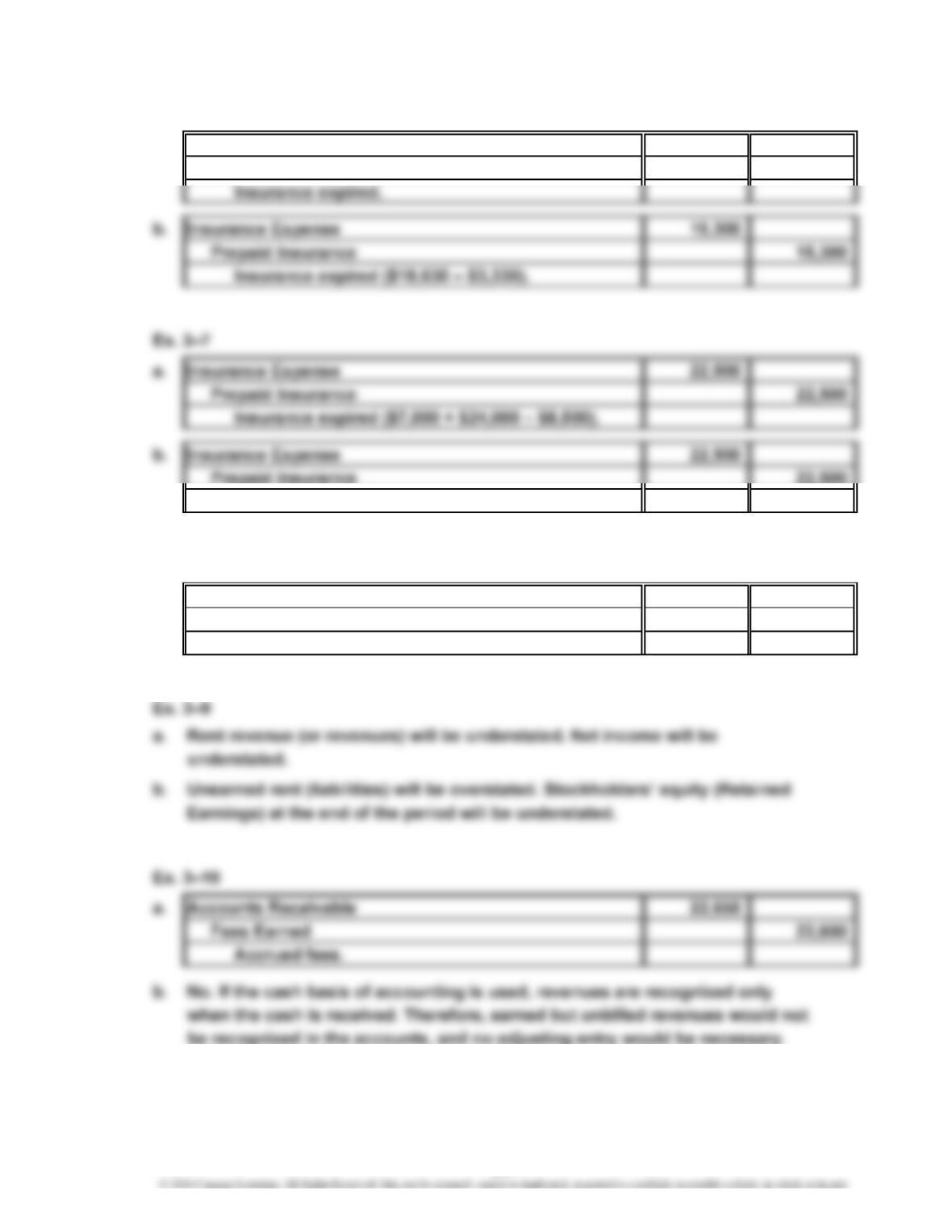

a. Insurance Expense 15,300

Prepaid Insurance 15,300

Insurance expired.

Ex. 3–8

Unearned Fees 22,510

Fees Earned 22,510

Fees earned ($36,950 – $14,440).

3-7

CHAPTER 3 The Adjusting Process

Ex. 3–11

a. Unearned Fees 82,220

Fees Earned 82,220

Salaries Payable 9,960

Accrued salaries [($16,600 ÷ 5 days) × 3 days].

b. Salaries Expense 13,280

Salaries Payable 13,280

Accrued salaries [($16,600 ÷ 5 days) × 4 days].

3-8

CHAPTER 3 The Adjusting Process

Ex. 3–17

a. Taxes Expense 40,500

Prepaid Taxes 40,500

Ex. 3–18

Depreciation Expense 10,650

Ex. 3–19

a. $12,220,000 ($28,650,000 – $16,430,000)

b. No. Depreciation is an allocation of the cost of the equipment to the periods

Ex. 3–21

Income: $5,657 million ($2,767 + $2,890)

Ex. 3–22

a. $598 million

3-9

CHAPTER 3 The Adjusting Process

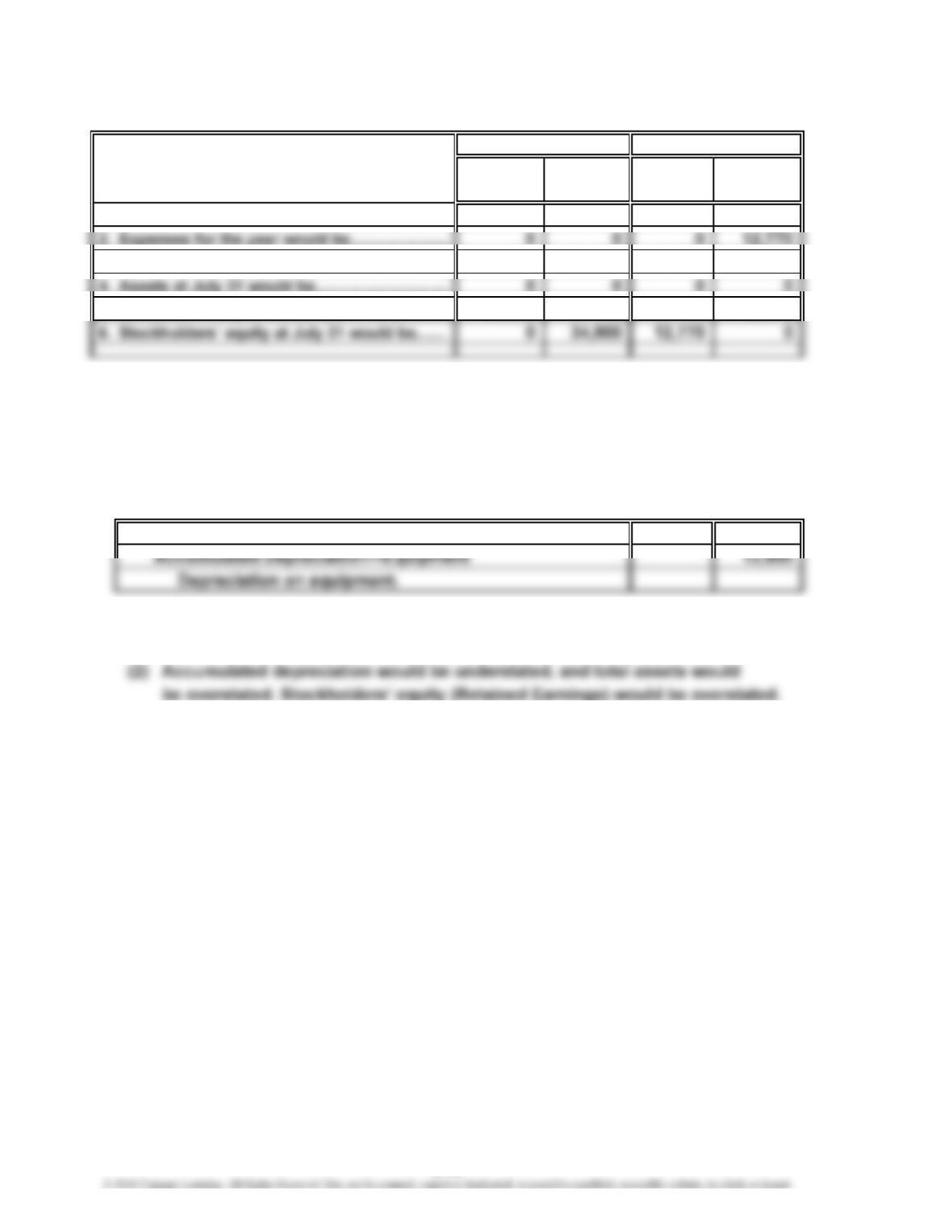

Ex. 3–23

Over- Under- Over- Under-

stated stated stated stated

1. Revenue for the year would be………………

…

$ 0 $34,900 $ 0 $ 0

3. Net income for the year would be……………

…

0 34,900 12,770 0

…

5. Liabilities at July 31 would be…………………

…

34,900 0 0 12,770

Ex. 3–24

$218,530 ($196,400 + $34,900 – $12,770)

Ex. 3–25

a. Depreciation Expense 13,900

b. (1) Depreciation expense would be understated. Net income would be

overstated.

Error (b)Error (a)

3-10

CHAPTER 3 The Adjusting Process

Ex. 3–26

1. Accounts Receivable 6

2. Supplies Expense 2

3. Insurance Expense 12

4. Depreciation Expense 4

5. Wages Expense 2

3-11

CHAPTER 3 The Adjusting Process

Ex. 3–27

1. The accountant debited Accounts Receivable for $5,000 but did not credit

Laundry Revenue. This adjusting entry represents accrued laundry revenue.

3. The accountant credited the prepaid insurance account for $3,600, but debited

the insurance expense account for only $600.

5. The accountant did not debit Wages Expense for $1,000.

The corrected adjusted trial balance is shown below.

Debit Credit

Balances Balances

Cash 7,500

Accounts Receivable 23,250

Laundry Supplies 750

Prepaid Insurance 1,600

Laundry Equipment 190,000

May 31, 2016

EVA’S LAUNDRY

Adjusted Trial Balance

3-12

CHAPTER 3 The Adjusting Process

Ex. 3–28

a. $90 million increase ($2,223 – $2,133)

4.2% ($90 ÷ $2,133) increase

b. Year 2: 9.2% ($2,223 ÷ $24,128)

Year 1: 10.2% ($2,133 ÷ $20,862)

Ex. 3–29

a.

Amount Percent

Net sales $ 62,071 100.0%

Cost of goods sold (48,260) 77.8%

Dell Inc.

3-13

CHAPTER 3 The Adjusting Process

Prob. 3–1A

1. a. Supplies Expense 4,330

Supplies 4,330

Supplies used ($5,620 – $1,290).

b. Unearned Rent 1,250

2. Adjusting entries are a planned part of the accounting process to update the

PROBLEMS

3-14

CHAPTER 3 The Adjusting Process

Prob. 3–2A

1. a. Accounts Receivable 11,150

Fees Earned 11,150

Accrued fees earned.

b. Supplies Expense 2,450

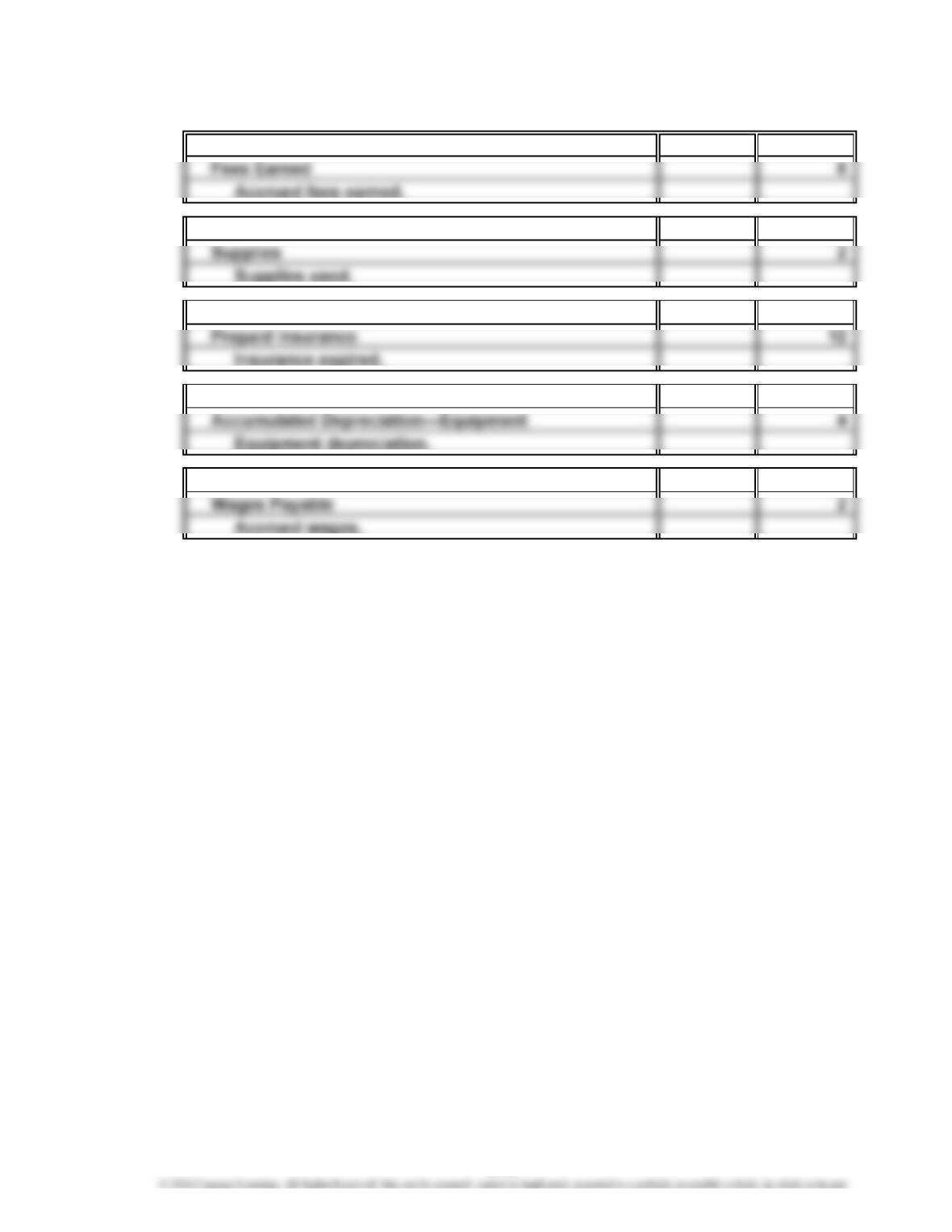

2. Fees Earned would be understated by $11,150; Wages Expense would be

3. Accounts Receivable would be understated by $11,150; total assets would be

understated by $11,150; Wages Payable would be understated by $4,840;

4. There is no effect on the “Net increase or decrease in cash” on the statement

of cash flows because adjusting entries do not affect cash.

3-15

CHAPTER 3 The Adjusting Process

Prob. 3–3A

1. a. Accounts Receivable 9,850

Fees Earned 9,850

Accrued fees earned.

b. Supplies Expense 11,540

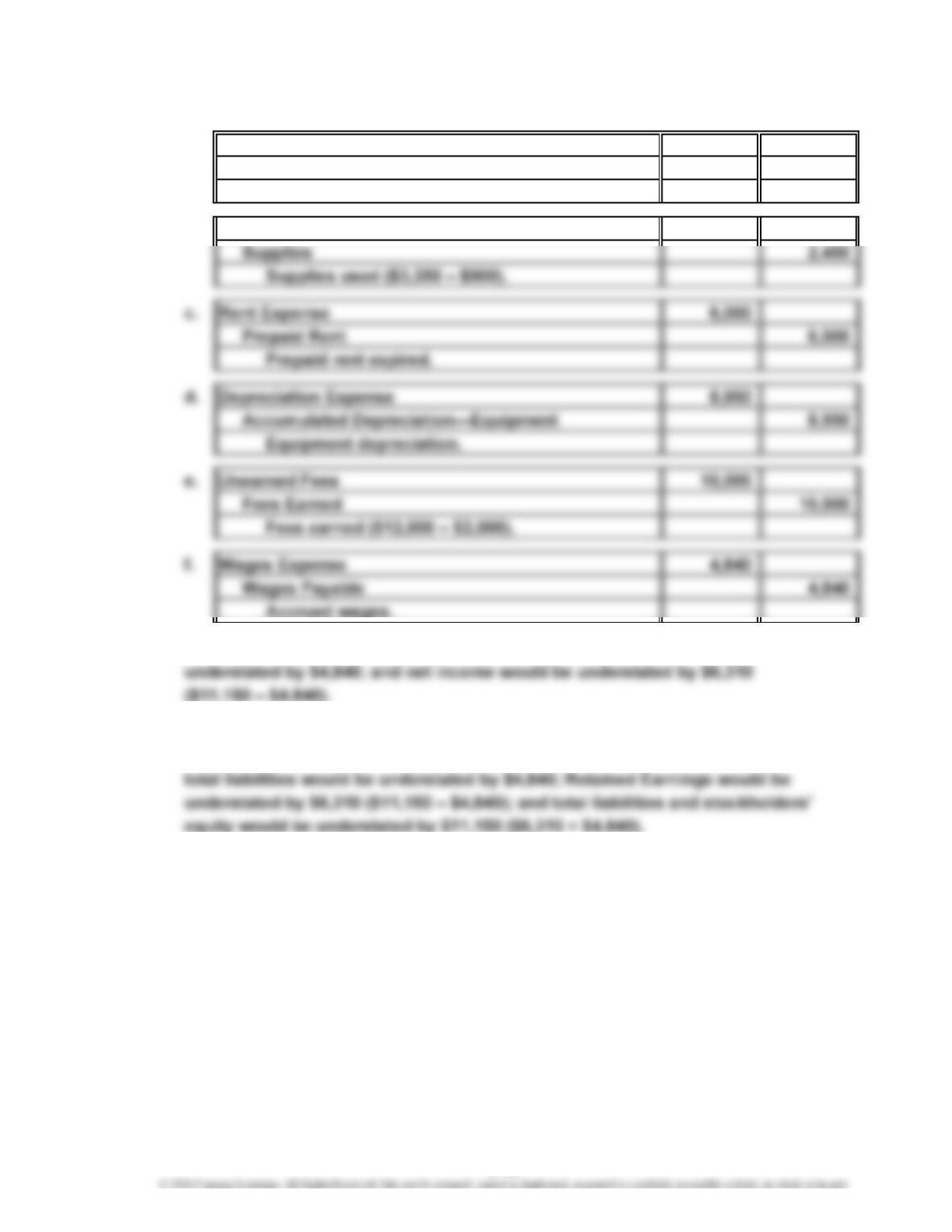

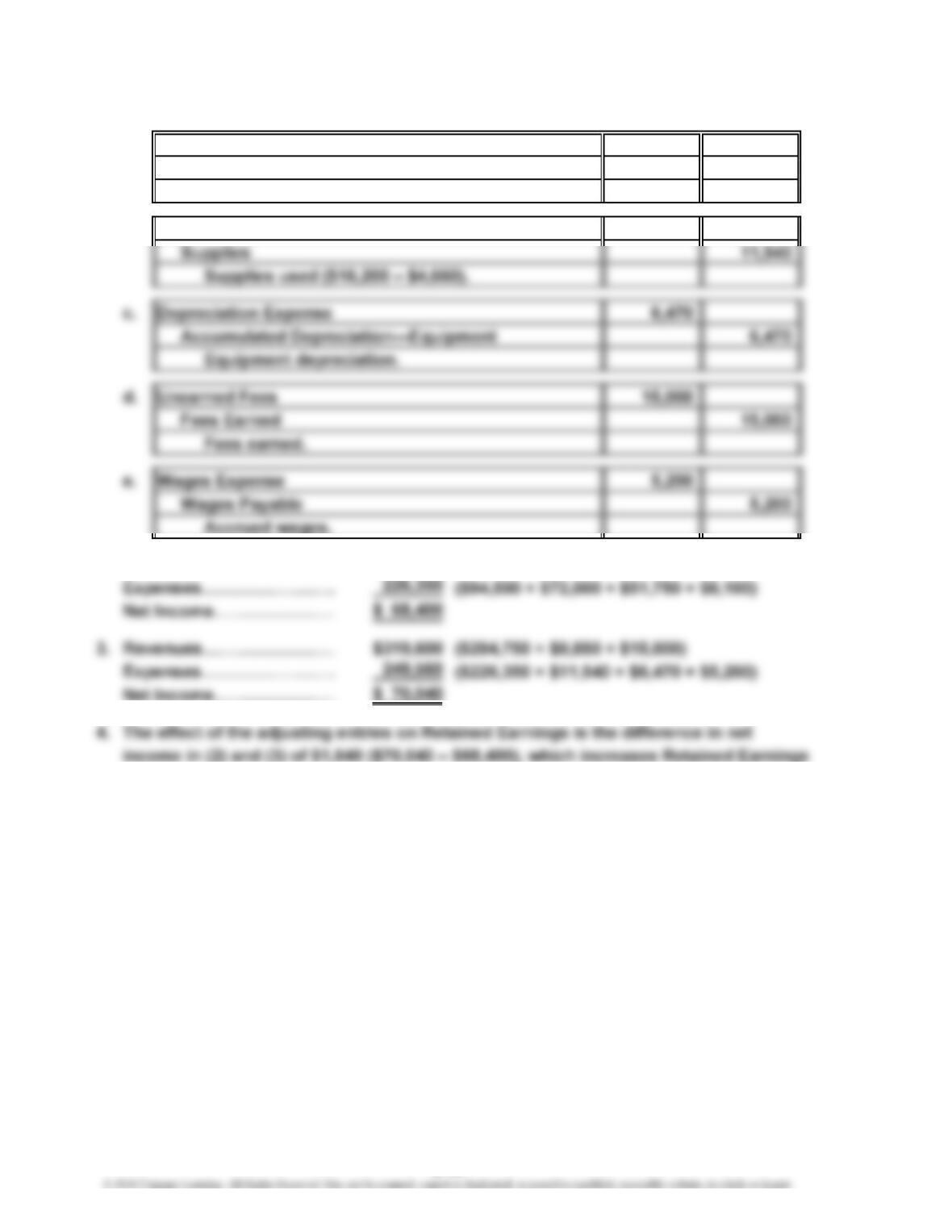

2. Revenues…………………

…

$294,750

…

s

3-16

CHAPTER 3 The Adjusting Process

Prob. 3–4A

2016

Nov. 30 Supplies Expense 8,850

Supplies 8,850

Supplies used ($11,250 – $2,400).

30 Insurance Expense 10,400

Prepaid Insurance 10,400

Insurance expired ($14,250 – $3,850).

3-17

CHAPTER 3 The Adjusting Process

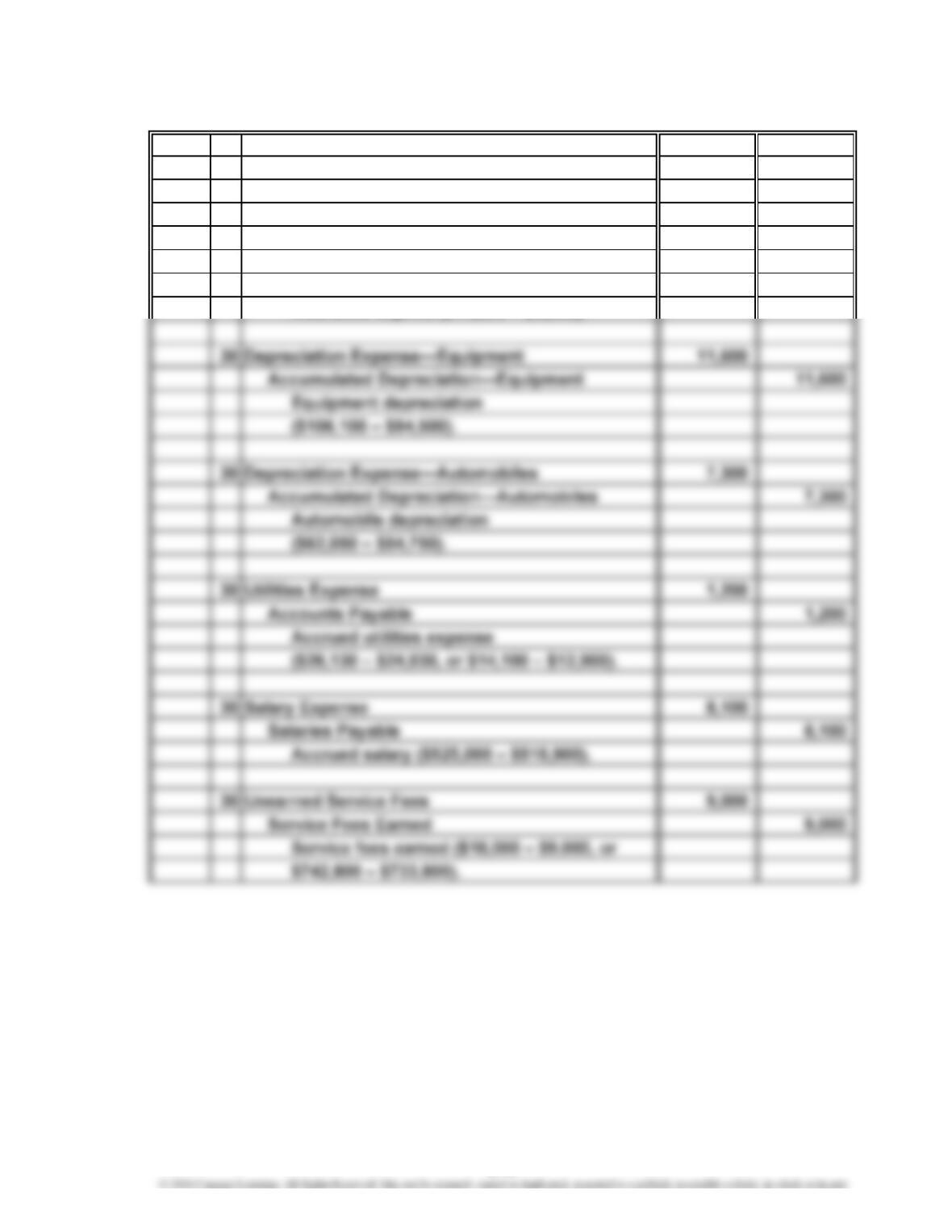

Prob. 3–5A

1. a. Insurance Expense 1,200

Prepaid Insurance 1,200

Insurance expired ($7,200 – $6,000).

b. Supplies Expense 1,500

Supplies 1,500

3-18