CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–18 (FIN MAN); Ex. 3–18 (MAN)

a.

1.

Work in Process—Casting Department

350,000

Materials—Alloy

350,000

* Supporting calculations:

Cost of 2,530 transferred-out pounds:

Inventory in process, May 1 ……………………………………………………………………

$ 32,844

Cost to complete May 1 inventory:

Pounds started and completed in May

Supporting equivalent unit and cost per equivalent unit calculations:

Whole

Units

Equivalent Units

Materials

Conversion

Inventory in process, May 1

(60% completed)

230

0

921

in May

3 230 units + 2,500 units – 2,530 units

4 200 units × 44%

Cost per equivalent unit of materials:

$350,000

2,500

= $140 per pound

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–18 (FIN MAN); Ex. 3–18 (MAN) (Concluded)

b.

$29,760; determined as follows:

Direct materials (200 × $140) …………………………………………..

c.

Materials:

From current period ………………………………………………….

$ 140

From beginning inventory …………………………………………

(132)

Increase …………………………………………………………………..

$ 8

From current period ………………………………………………….

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

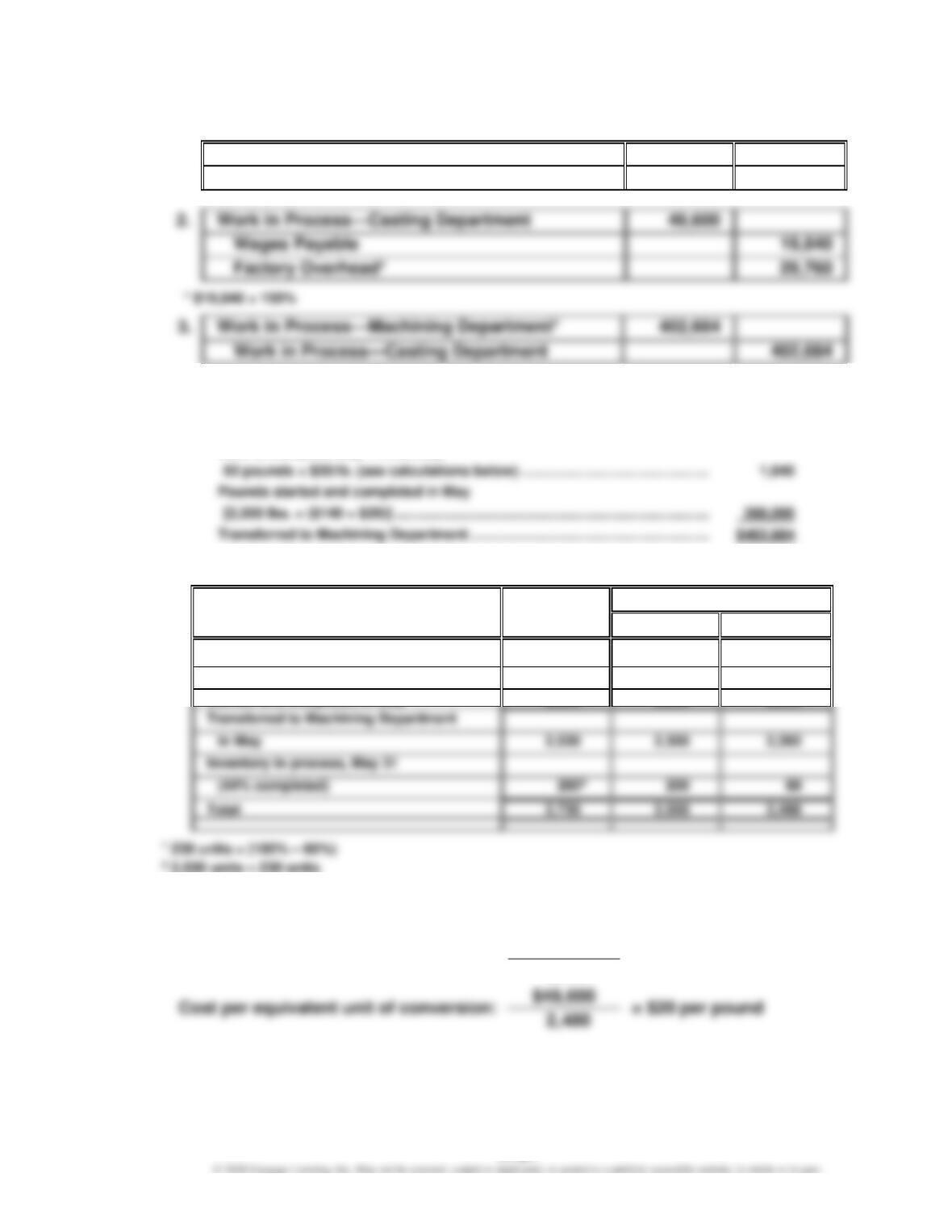

Ex. 17–19 (FIN MAN); Ex. 3–19 (MAN)

a.

1.

Work in Process—Papermaking Department

330,750

Materials—Pulp

330,750

3.

Work in Process—Converting Department*

420,925

* Supporting calculations:

Cost of 103,900 transferred-out units:

Inventory in process, March 1……………………………………………………………………….

$ 9,139

Supporting equivalent unit and cost per equivalent unit calculations:

Whole Units

Equivalent Units

Materials

Conversion

Inventory in process, March 1

(35% completed)

2,600

0

1,6901

Started and completed in March

Cost per equivalent unit of materials:

$330,750

105,000

= $3.15 per unit

Cost per equivalent unit of conversion:

$95,355

105,950

= $0.90 per unit

b.

$14,319; determined as follows:

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–20 (FIN MAN); Ex. 3–20 (MAN)

a. Cost per megawatt hour (MWh):

Fossil plant costs:

Conversion costs ………………………………………..

$40,500,000

Fuel ……………………………………………………………

10,800,000

Fossil plant megawatt hours (MWh):

Megawatts ………………………………………………….

900

Wind farm costs:

Conversion costs ………………………………………..

$2,700,000

Wind farm megawatt hours (MWh):

Megawatts ………………………………………………….

100

30,000

The wind farm, with a cost per megawatt hour of $90 as compared to the fossil

plant cost of $95 per megawatt hour, is the less costly resource.

Note: These figures are close to the national average and show the slight advantage

of wind farms.

b. Equivalent units of production are calculated when there are beginning or

ending inventories that are partially completed to either conversion costs or

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Appendix Ex. 17–21 (FIN MAN); Appendix Ex. 3–21 (MAN)

a. and b.

a. Whole

Units

b. Equivalent Units

of Production

Units to be accounted for:

Beginning work in process

1,900

Units started during period

15,1001

Units to be assigned costs:

Transferred to Packing Department

Inventory in process, ending

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

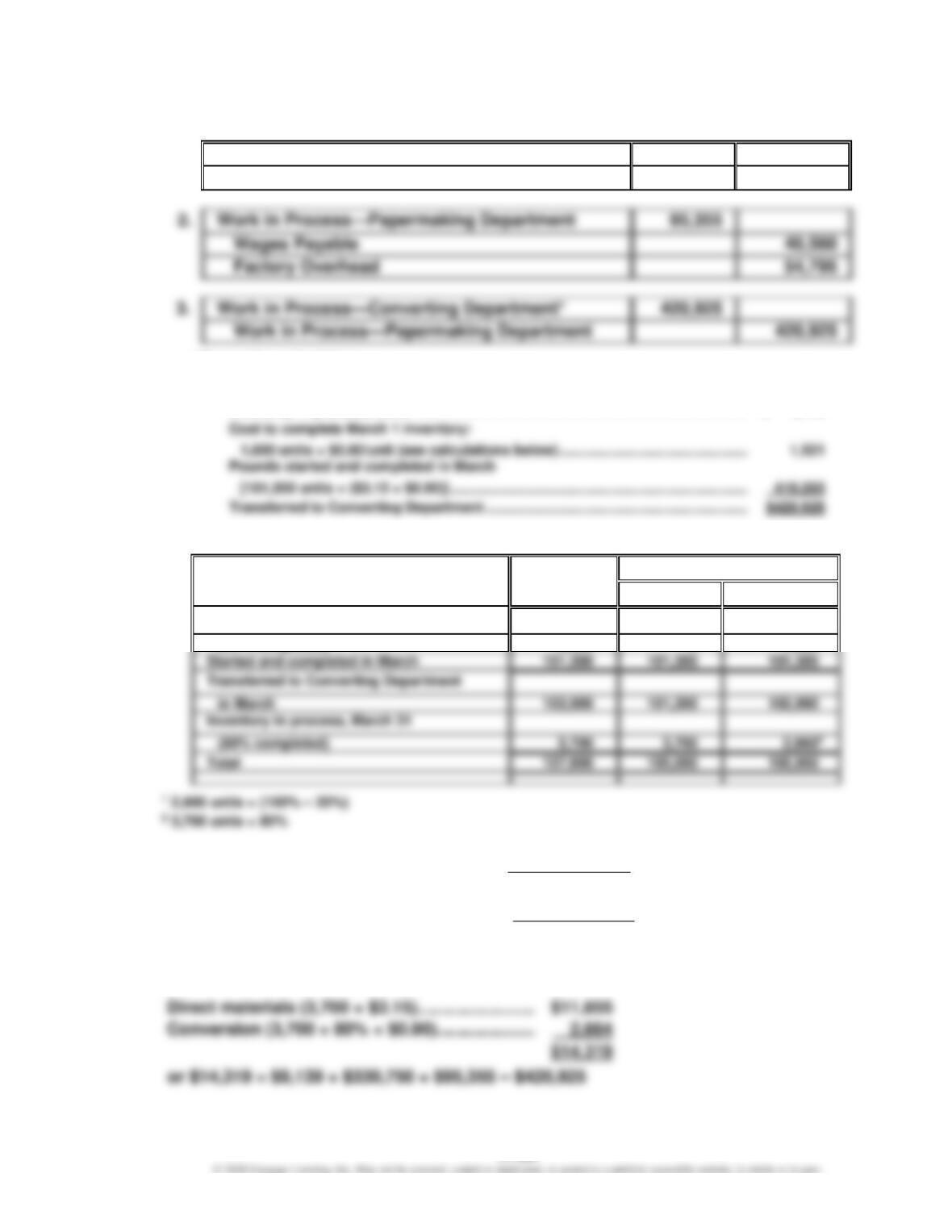

Appendix Ex. 17–22 (FIN MAN); Appendix Ex. 3–22 (MAN)

a. Drawing Department

Whole

Units

Equivalent Units

of Production

Units to be accounted for:

Beginning work in process

500

Units started during period

11,6001

Total

12,100

Transferred to Winding Department in July

Inventory in process, July 31

b. Winding Department

Whole

Units

Equivalent Units

of Production

Units to be accounted for:

Beginning work in process

350

Units started during period

11,4001

Total

11,750

Units to be assigned costs:

Transferred to finished goods in July

Inventory in process, July 31

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

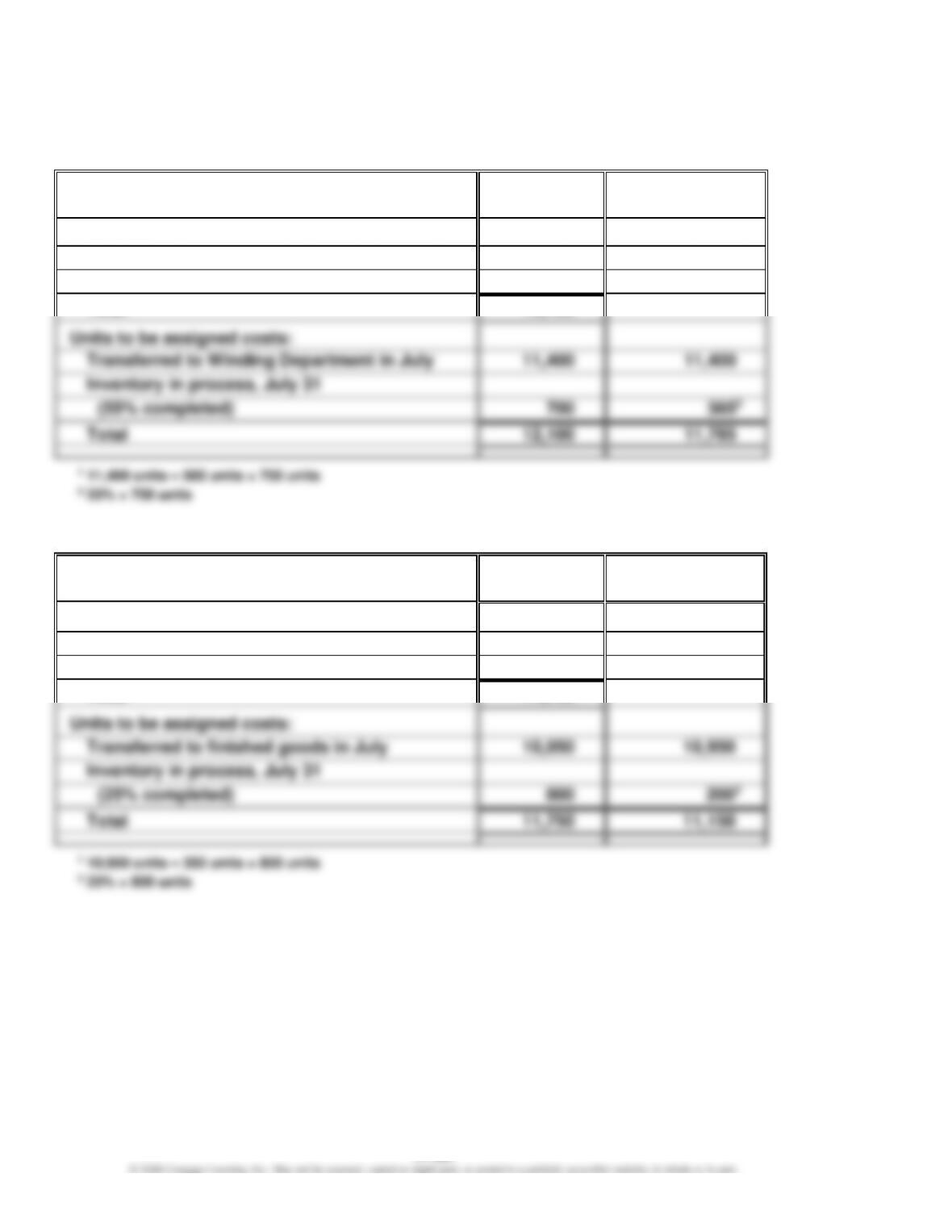

Appendix Ex. 17–23 (FIN MAN); Appendix Ex. 3–23 (MAN)

a.

Units in process, May 1 ………………………………………………………………………

4,200

Units placed into production for May…………………………………………………..

Units finished during May …………………………..………………………………………

b.

Whole

Units

Equivalent

Units of

Production

Units to be accounted for:

Beginning work in process

4,200

Units started during the period

23,600

Total

27,800

Units to be assigned costs:

Transferred to finished goods in May

Inventory in process, May 31

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Appendix Ex. 17–24 (FIN MAN); Appendix Ex. 3–24 (MAN)

a. and b.

a. Whole

Units

b. Equivalent

Units of

Production

Units to be accounted for:

Beginning work in process

900

c. Cost per Equivalent Unit =

Total Production Costs

Total Equivalent Units

Cost per Equivalent Unit =

*

$61,740

8,820 units

= $7.00

* $2,466 + $34,500 + $16,200 + $8,574

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

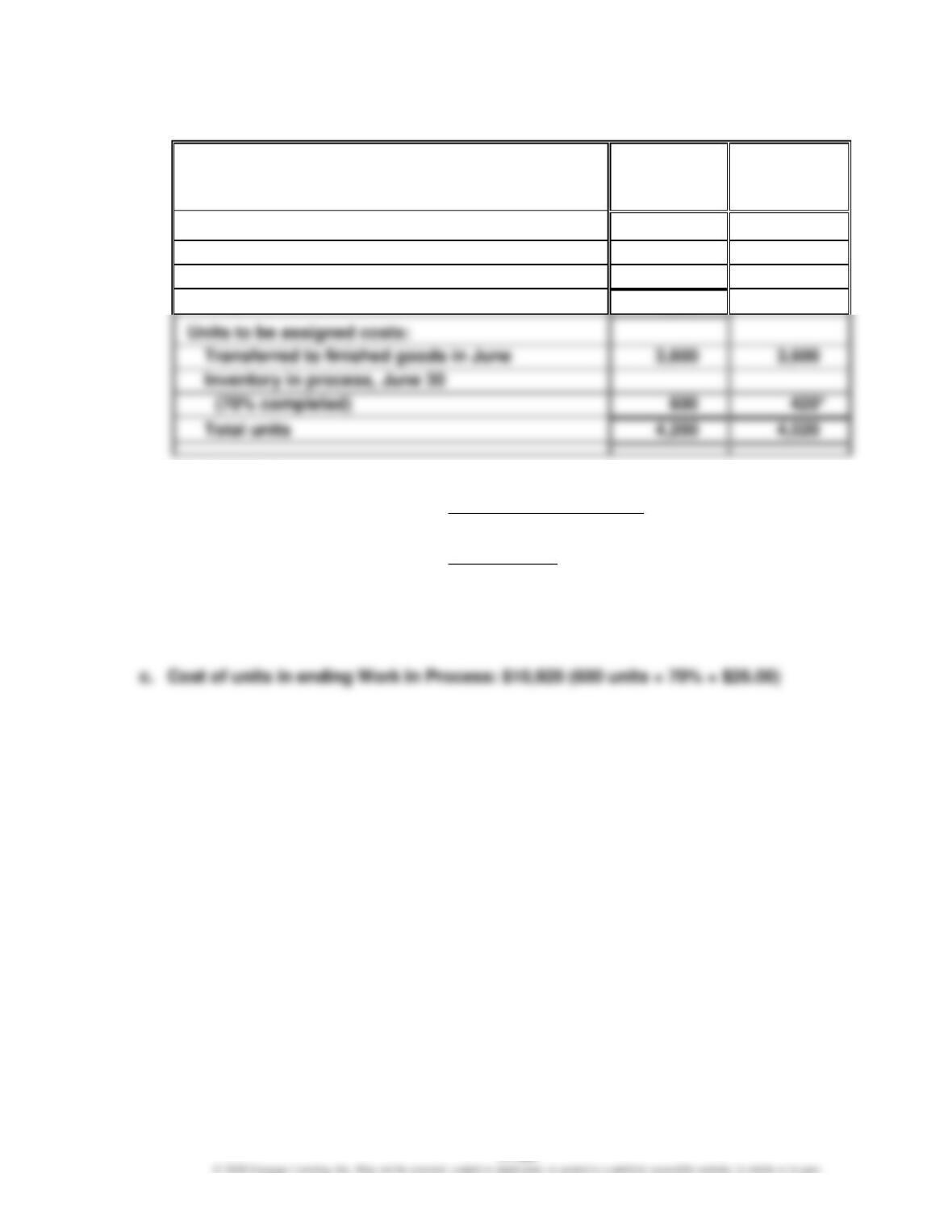

Appendix Ex. 17–25 (FIN MAN); Appendix Ex. 3–25 (MAN)

a.

Whole

Units

Equivalent

Units of

Production

Units to be accounted for:

Beginning work in process

500

Units started during the period

3,700

Total

4,200

Transferred to finished goods in June

3,600

Inventory in process, June 30

4,200

* 70% × 600 units

Cost per Equivalent Unit =

Total Production Costs

Total Equivalent Units

Cost per Equivalent Unit =

**

$104,520

4,020 units

= $26.00

** $5,000 + $49,200 + $25,200 + $25,120

b. Cost of units transferred to Finished Goods: $93,600 (3,600 units × $26.00)

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Appendix Ex. 17–26 (FIN MAN); Appendix Ex. 3–26 (MAN)

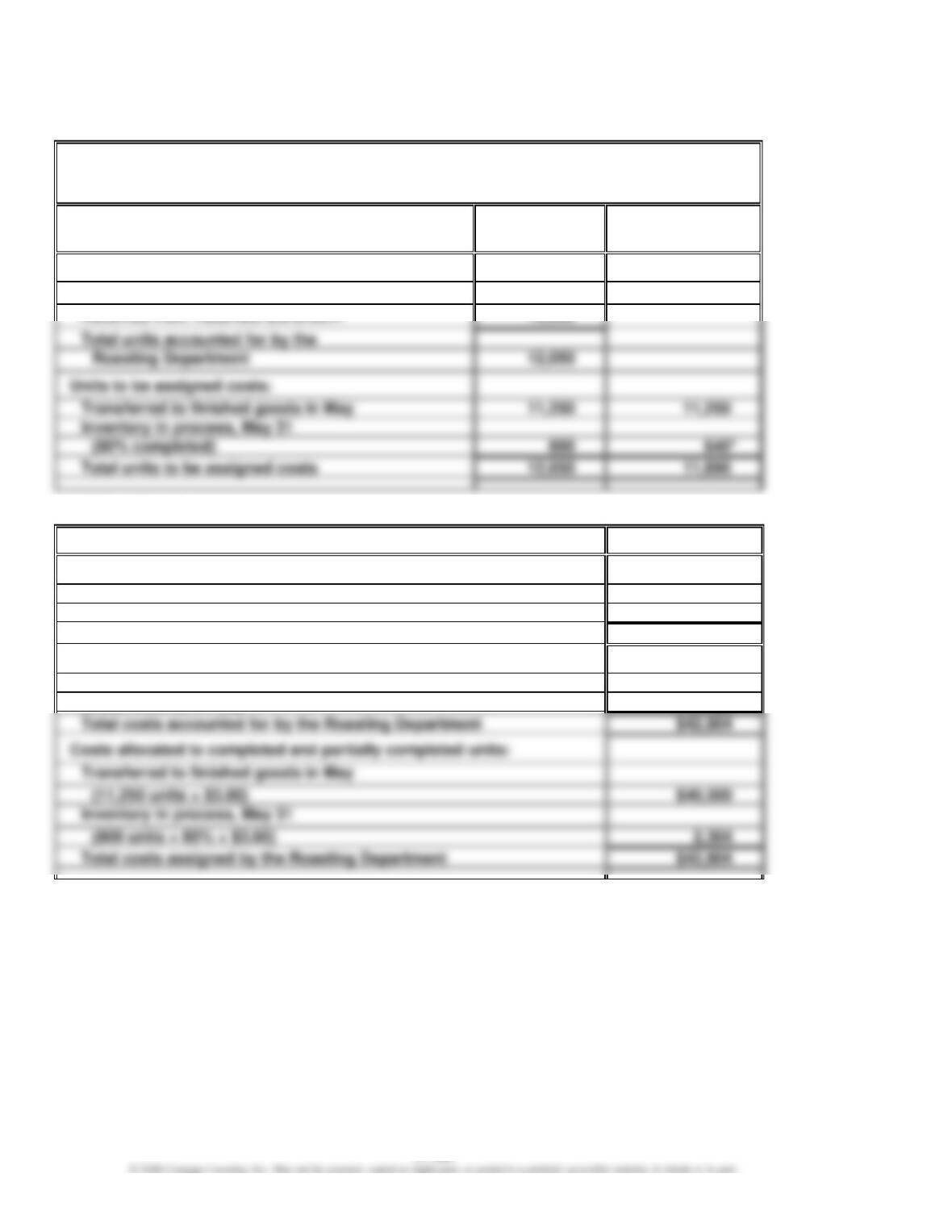

Highlands Coffee Company

Cost of Production Report—Roasting Department

For the Month Ended May 31

UNITS

Whole

Units

Equivalent Units

of Production

Units charged to production:

Inventory in process, May 1

1,150

Received from materials storeroom

Units to be assigned costs:

Transferred to finished goods in May

11,250

Total units to be assigned costs

11,890

* 80% × 800 units

COSTS

Costs

Cost per equivalent unit:

Total costs for May in Roasting Department

$42,8041

Total equivalent units

÷11,890

Cost per equivalent unit

$ 3.60

Costs assigned to production:

Inventory in process, May 1

$ 1,700

Costs incurred in May

41,1042

Total costs accounted for by the Roasting Department

Costs allocated to completed and partially completed units:

Transferred to finished goods in May

Total costs assigned by the Roasting Department

1 $1,700 + $28,600 + $12,504

2 $28,600 + $12,504

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

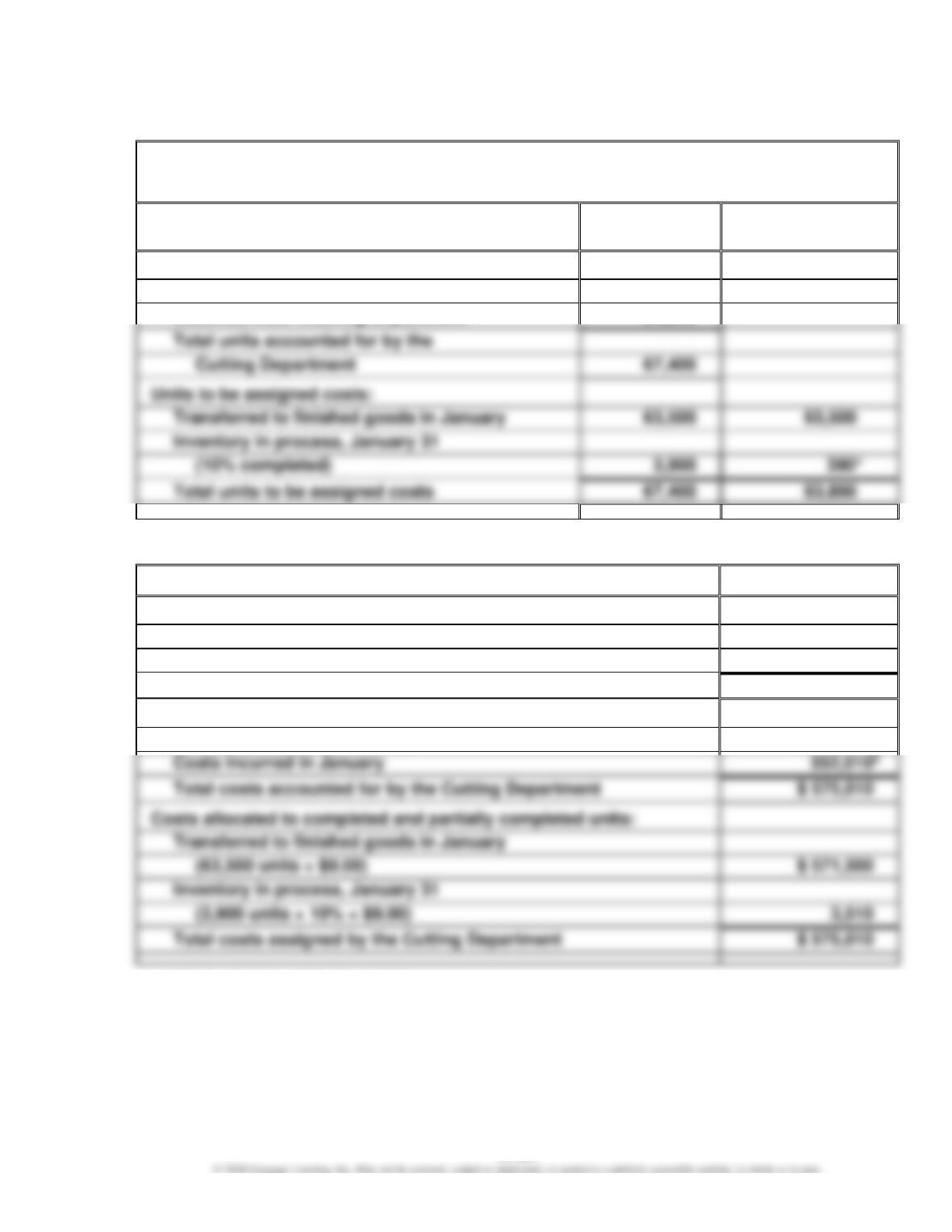

Appendix Ex. 17–27 (FIN MAN); Appendix Ex. 3–27 (MAN)

Dalton Carpet Company

Cost of Production Report—Cutting Department

For the Month Ended January 31

UNITS

Whole

Units

Equivalent Units

of Production

Units charged to production:

Inventory in process, January 1

3,400

Received from Weaving Department

64,000

Total units accounted for by the

Units to be assigned costs:

Transferred to finished goods in January

63,500

Inventory in process, January 31

3,900

* 10% × 3,900 units

COSTS

Cost per equivalent unit:

Total costs for January in Cutting Department

$ 575,0101

Total equivalent units

÷ 63,890

Cost per equivalent unit

$ 9.00

Costs assigned to production:

Inventory in process, January 1

$ 23,000

Costs incurred in January

Total costs accounted for by the Cutting Department

Costs allocated to completed and partially completed units:

Transferred to finished goods in January

Inventory in process, January 31

1 $23,000 + $366,200 + $105,100 + $80,710

2 $366,200 + $105,100 + $80,710

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

PROBLEMS

Prob. 17–1A (FIN MAN); Prob. 3–1A (MAN)

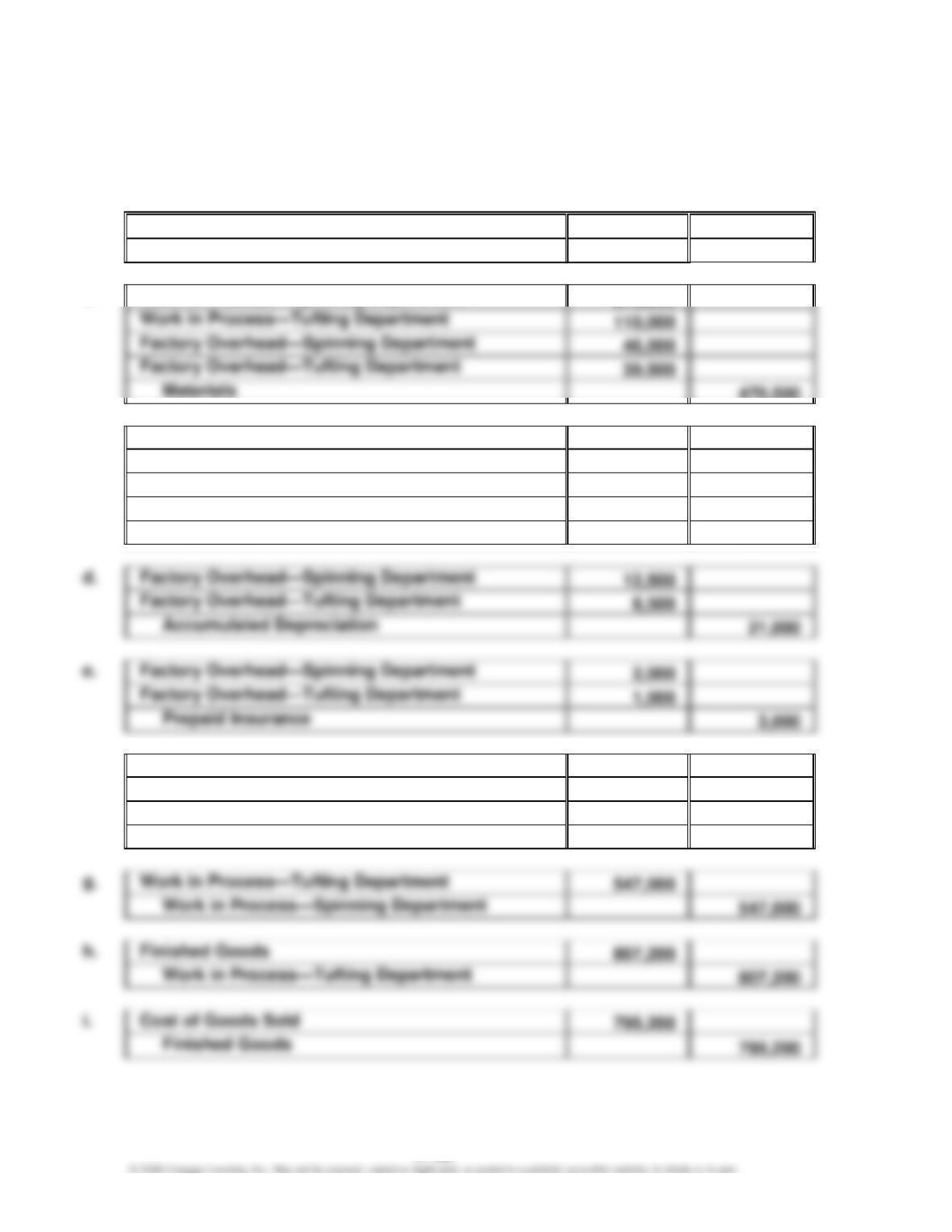

1.

a.

Materials

500,000

Accounts Payable

500,000

b.

Work in Process—Spinning Department

275,000

Work in Process—Tufting Department

110,000

Factory Overhead—Spinning Department

46,000

Factory Overhead—Tufting Department

39,500

470,500

c.

Work in Process—Spinning Department

185,000

Work in Process—Tufting Department

98,000

Factory Overhead—Spinning Department

18,500

Factory Overhead—Tufting Department

9,000

Wages Payable

310,500

Factory Overhead—Spinning Department

12,500

Factory Overhead—Tufting Department

Accumulated Depreciation

21,000

e.

Factory Overhead—Spinning Department

Factory Overhead—Tufting Department

1,000

Prepaid Insurance

f.

Work in Process—Spinning Department

80,000

Work in Process—Tufting Department

55,000

Factory Overhead—Spinning Department

80,000

Factory Overhead—Tufting Department

55,000

Work in Process—Tufting Department

547,000

Work in Process—Spinning Department

547,000

Finished Goods

807,200

Work in Process—Tufting Department

807,200

Cost of Goods Sold

795,200

795,200

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Prob. 17–1A (FIN MAN); Prob. 3–1A (MAN) (Concluded)

2.

Materials

Work in

Process—

Spinning Dept.

Work in

Process—

Tufting Dept.

Finished

Goods

Balance, January 1 ….

$ 17,000

$ 35,000

$ 28,500

$ 62,000

Debits …………………….

500,000

540,0001

810,0002

807,200

Balance, January 31 ..

3.

Factory Overhead—

Spinning Dept.

Factory Overhead—

Tufting Dept.

Balance, January 1 ……..

$ 0

$ 0

Debits ………………………..

79,0001

58,0002

Credits ……………………….

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

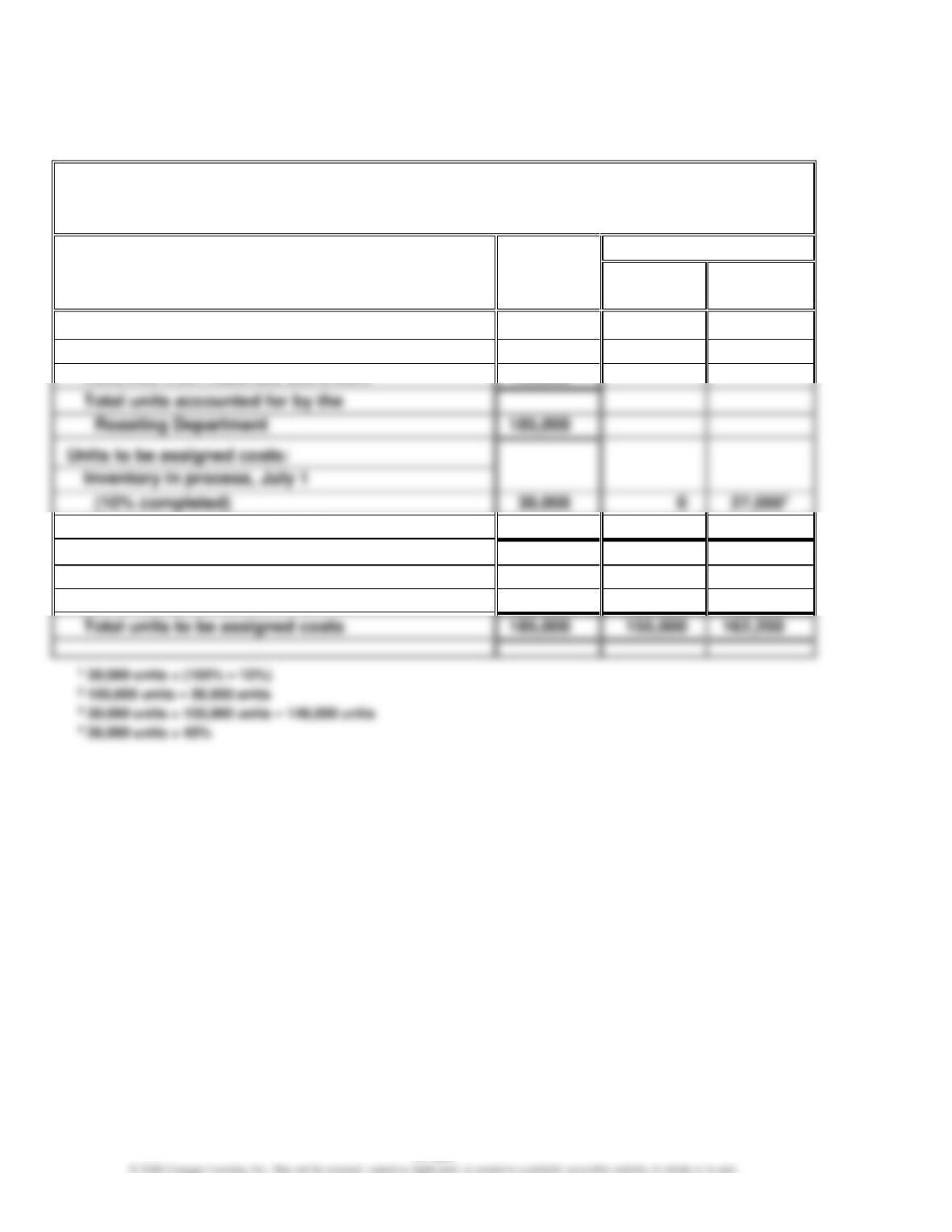

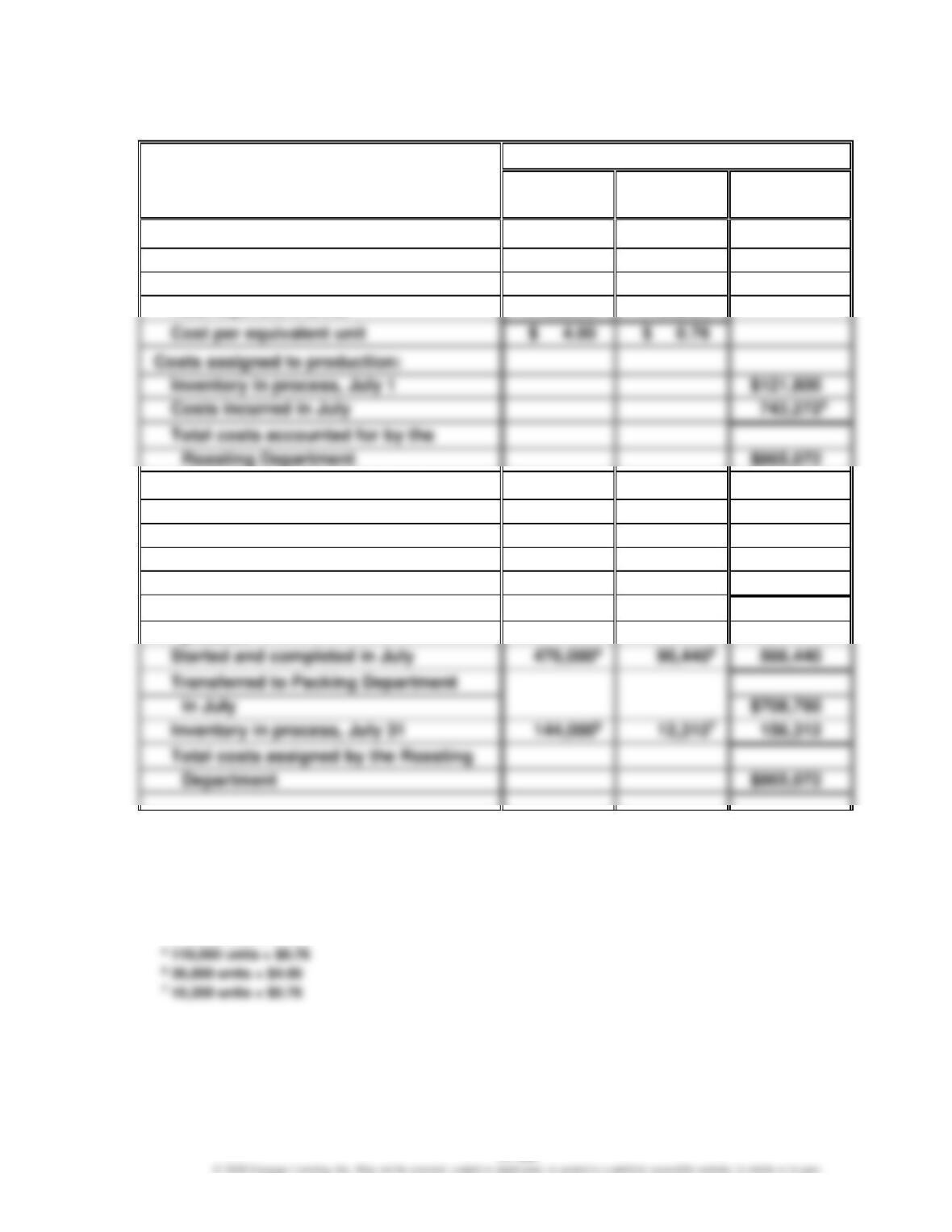

Prob. 17–2A (FIN MAN); Prob. 3–2A (MAN)

1.

Hana Coffee Company

Cost of Production Report—Roasting Department

For the Month Ended July 31

UNITS

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Units charged to production:

Inventory in process, July 1

30,000

Total units accounted for by the

Roasting Department

30,000

Started and completed in July

119,0002

119,000

119,000

Transferred to Packing Department in July

149,000

119,000

146,000

Inventory in process, July 31

(45% completed)

36,0003

36,000

16,200

Total units to be assigned costs

155,000

162,200

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Prob. 17–2A (FIN MAN); Prob. 3–2A (MAN) (Continued)

COSTS

Costs

Direct

Materials

Conversion

Total

Cost per equivalent unit:

Total costs for July in Roasting

Department

$620,000

$123,2721

Total equivalent units

÷155,000

÷162,200

Cost per equivalent unit

Costs assigned to production:

Inventory in process, July 1

Costs incurred in July

Costs allocated to completed and

partially completed units:

Inventory in process, July 1 balance

$121,800

To complete inventory in process,

July 1

$ 0

$ 20,5203

20,520

Cost of completed July 1 work in

$142,320

process

Started and completed in July

Transferred to Packing Department

in July

$708,760

Inventory in process, July 31

Total costs assigned by the Roasting

Costs transferred to Packing Department: $708,760

Work in process, July 31: 36,000 units at a cost of $156,312

1 $90,000 + $33,272

2 $620,000 + $90,000 + $33,272

3 27,000 units × $0.76

4 119,000 units × $4.00

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Prob. 17–2A (FIN MAN); Prob. 3–2A (MAN) (Concluded)

2.

Direct materials cost increased from $3.98 in June to $4.00 in July.

Conversion cost decreased from $0.80 in June to $0.76 in July.

Computations:

Direct materials: $3.98 ($119,400 ÷ 30,000 units)

Conversion: $0.80; determined as follows:

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

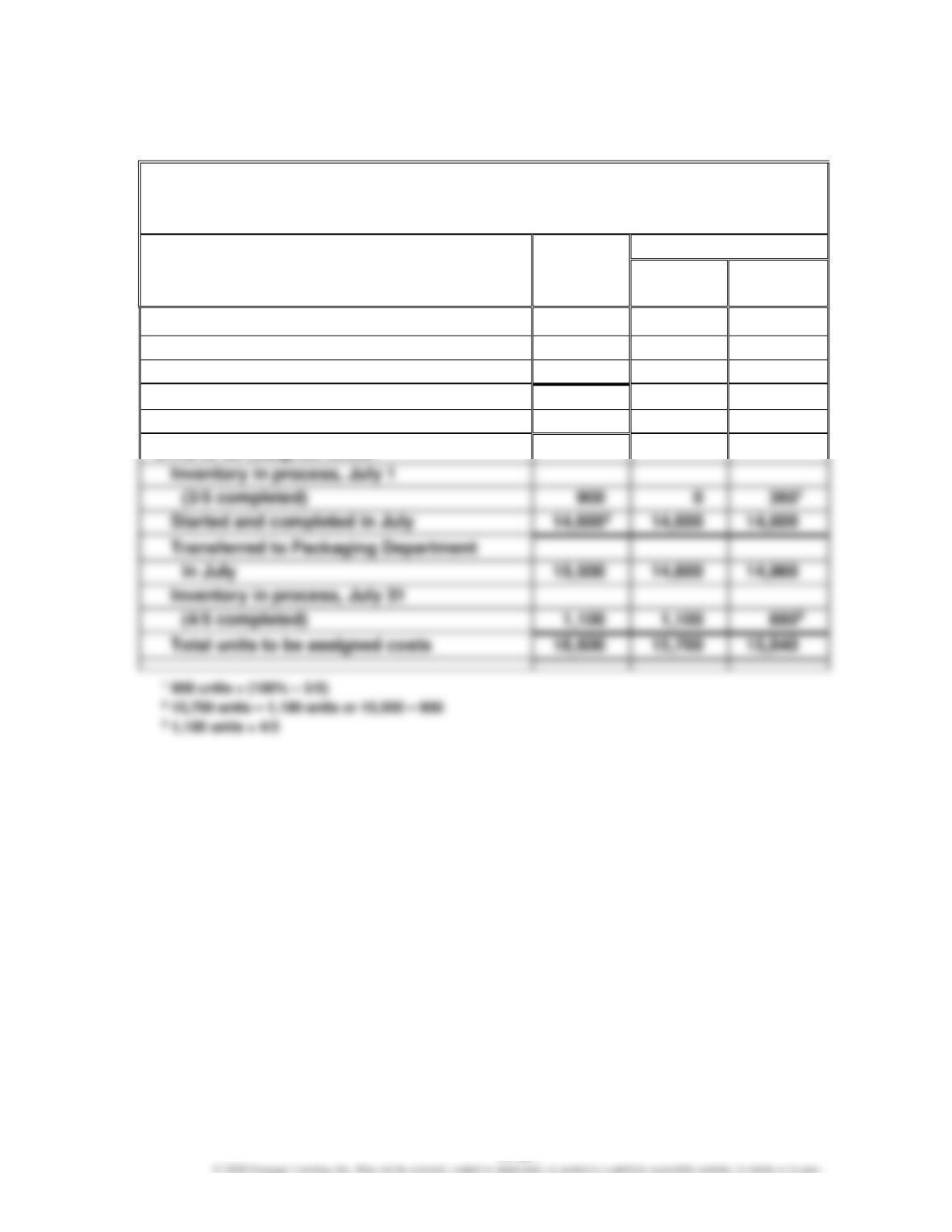

Prob. 17–3A (FIN MAN); Prob. 3–3A (MAN)

1.

White Diamond Flour Company

Cost of Production Report—Sifting Department

For the Month Ended July 31

UNITS

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Units charged to production:

Inventory in process, July 1

900

Received from Milling Department

15,700

Total units accounted for by the

Sifting Department

16,600

Inventory in process, July 1

14,600

Transferred to Packaging Department

Inventory in process, July 31

(4/5 completed)

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

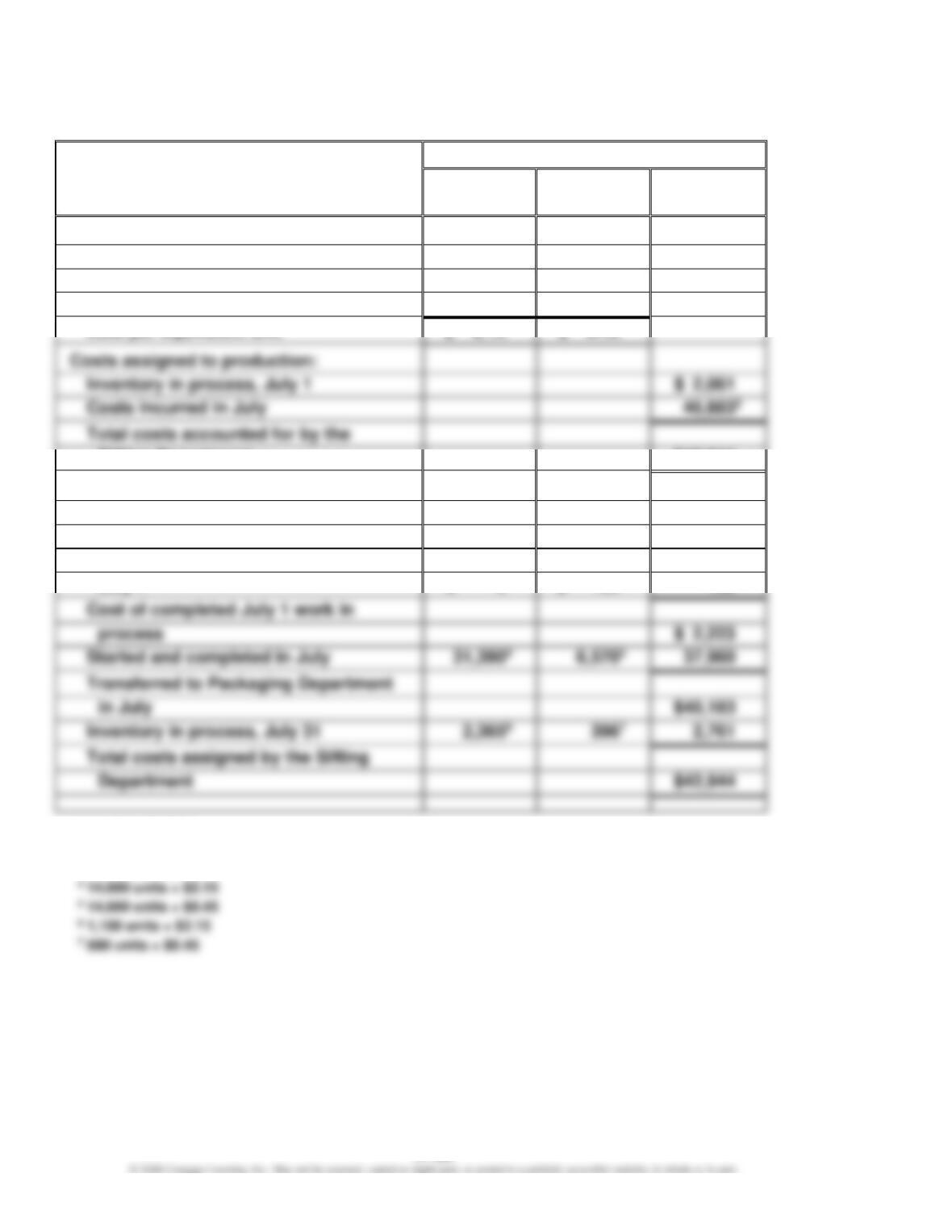

Prob. 17–3A (FIN MAN); Prob. 3–3A (MAN) (Continued)

COSTS

Costs

Direct

Materials

Conversion

Total

Cost per equivalent unit:

Total costs for July in Sifting

Department

$33,755

$ 7,1281

Total equivalent units

÷15,700

÷15,840

Cost per equivalent unit

Costs assigned to production:

Inventory in process, July 1

Costs incurred in July

Total costs accounted for by the

Sifting Department

$42,944

Costs allocated to completed and

partially completed units:

Inventory in process, July 1 balance

$ 2,061

To complete inventory in process,

Cost of completed July 1 work in

Started and completed in July

Transferred to Packaging Department

Inventory in process, July 31

2,761

Total costs assigned by the Sifting

1 $4,420 + $2,708

2 $33,755 + $4,420 + $2,708

3 360 units × $0.45

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Prob. 17–3A (FIN MAN); Prob. 3–3A (MAN) (Concluded)

2.

Work in Process—Sifting Department

33,755

Work in Process—Milling Department

33,755

3. Direct materials: $0.10 increase ($2.15 – $2.05)

Conversion: $0.05 increase ($0.45 – $0.40)

4. The cost of production report may be used as the basis for allocating product

costs between Work in Process and Transferred-Out (or Finished) Goods. The

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

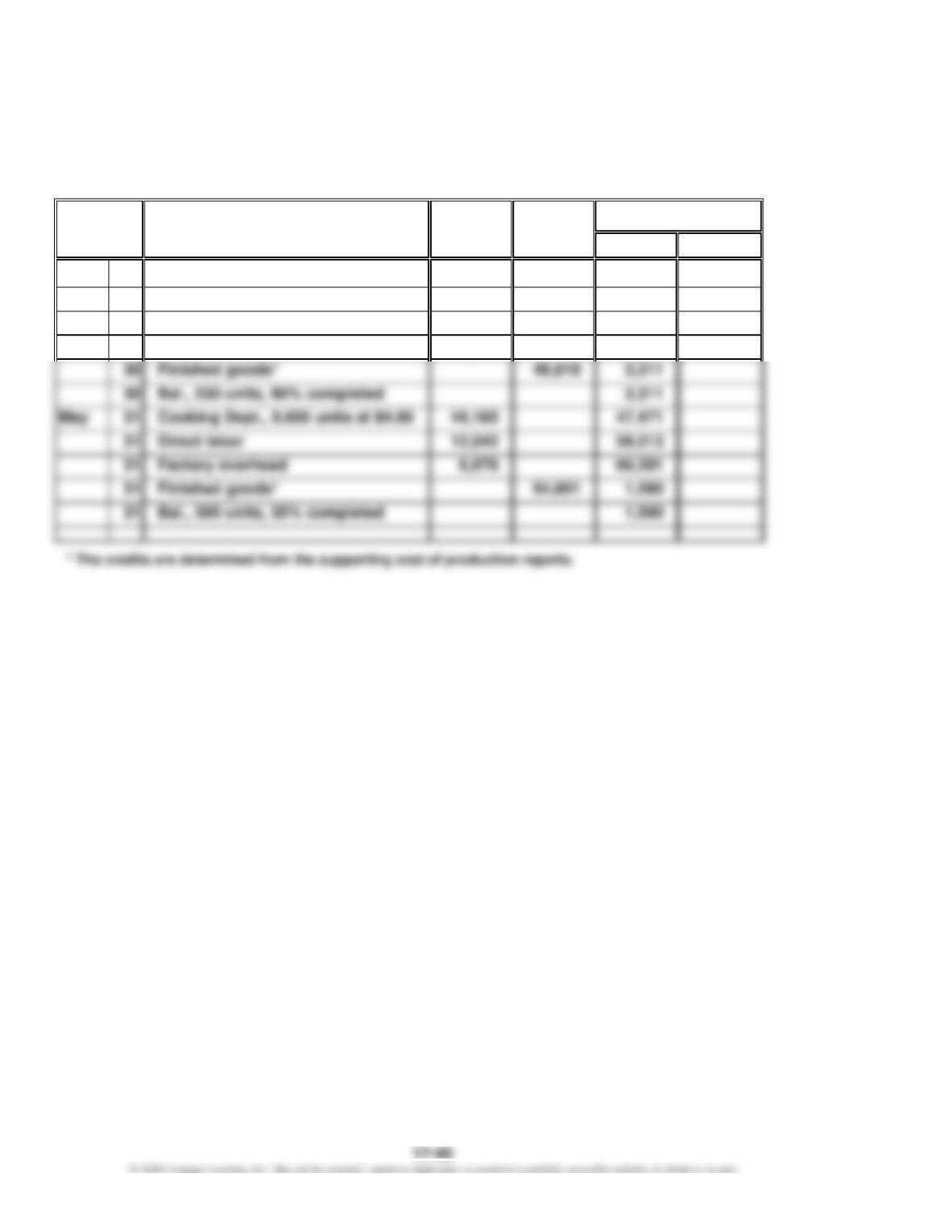

Prob. 17–4A (FIN MAN); Prob. 3–4A (MAN)

1. and 2.

Work in Process—Filling

Date

Item

Dr.

Cr.

Balance

Dr.

Cr.

Apr.

1

Bal., 800 units, 30% completed

3,860

30

Cooking Dept., 7,800 units at $4.40

34,320

38,180

30

Direct labor

8,562

46,742

30

Factory overhead

6,387

53,129

31

Direct labor

12,042

59,513

31

Bal., 300 units, 35% completed