3-1

CHAPTER 3

The Accounting Information System

Learning Objectives

1. Analyze the effect of business transactions on the basic accounting equation.

2. Explain what an account is and how it helps in the recording process.

3. Define debits and credits and explain how they are used to record business transactions.

4. Identify the basic steps in the recording process.

5. Explain what a journal is and how it helps in the recording process.

3-2

Chapter Outline

Learning Objective 1 – Analyze the Effect of Business Transactions on the Basic

Accounting Equation

Accounting Information System

▪ collects and processes transactions.

▪ communicates financial information to decision makers.

▪ Factors that shape the Accounting Information System include:

o nature of the company’s business

o types of transactions

o company size

Accounting Transactions

▪ economic events that require recording in the financial statements

▪ occur when assets, liabilities, or stockholders’ equity items change as a result of

some economic event

TEACHING TIP

Provide students with examples of external events—the purchase of equipment, payment of

Analyzing Transactions—Transaction analysis – the process of identifying the specific

effects of economic events on the accounting equation

▪ The accounting equation must always balance

▪ Each transaction has a dual effect on the equation

TEACHING TIP

Illustrate transaction analysis by going through events 1–11 for Sierra Corporation. These are

the transactions that led to the financial statements shown in Chapter 1.

1. On October 1, cash of $10,000 is invested in the business by investors, in exchange for

$10,000 of Sierra Corporation common stock. Both Cash (an asset) and Common Stock

3-3

3. On October 2, Sierra purchased equipment by paying $5,000 cash to Superior

Equipment Sales Co. An equal increase and decrease in Sierra’s assets occur. Cash

decreases by $5,000 and Equipment increases by $5,000.

4. On October 2, Sierra received a $1,200 cash advance from R. Knox, a client, for guide

services for multi-day trips that are expected to be completed in the future. Both Cash

6. On October 3, Sierra paid its office rent for the month of October in cash, $900. Both

Cash and stockholders equity (Rent Expense) decrease. Expenses decrease

stockholders’ equity.

7. On October 4, Sierra paid $600 for a one-year insurance policy that will expire next year

on September 30. Cash decreases and another asset Prepaid Insurance increases.

Summarize these by using Illustration 3-3: see page 110 in the text.

TEACHING TIP

Students struggle with the difference between Supplies and Supplies Expense. Take time to

explain that supplies are recorded as an asset because they are available for future use.

TEACHING TIP

3-4

Summary of Transactions

▪ Each transaction is analyzed in terms of its effect on assets, liabilities, and

stockholders’ equity.

Learning Objective 2 – Explain What an Account is and How it Helps in the

Recording Process

Account – an individual accounting record of increases and decreases in a specific asset,

liability, or stockholders’ equity item.

▪ An account consists of three parts: (1) the title of the account, (2) a left or debit

side, and (3) a right or a credit side.

▪ In its simplest form it is referred to as a T account because the alignment of the

parts of the account resembles the letter T.

TEACHING TIP

Draw a T account on the board, in Excel or on an overhead transparency and show students

the three parts. Explain to students that we are able to evaluate and record Sierra’s

transactions using the extended balance sheet equation. However, there are only ten

TEACHING TIP

Tell students to use proper account titles in their journal entries and for their T accounts.

They should not use phrases such as ‘paid cash’, ‘bought supplies’, ‘performed services’ as

Learning Objective 3 – Define Debits and Credits and Explain How They are Used

to Record Business Transactions

Debits and Credits—The term debit means left, and credit means right. They DO NOT

mean increase or decrease.

▪ Debit is abbreviated Dr. and credit is abbreviated Cr.

3-5

Debit and Credit Procedures—Each transaction must affect two or more accounts to

keep the basic accounting equation in balance.

▪ Under the double-entry system the equality of debits and credits keeps the

equation balanced.

▪ The two-sided effect of each transaction is recorded in appropriate accounts.

▪ This helps to ensure the accuracy of the recorded amounts and helps to detect errors.

▪ Dr./Cr. Procedures for Assets and Liabilities

▪ The normal balance of an account is on its increase side

o The normal balance for Assets, Dividends, and Expenses is a debit balance.

o The normal balance for Liabilities, Common Stock, and is a credit balance.

▪ Stockholders’ Equity Relationships

o Common stock and retained earnings: in the stockholders’ section of the balance

See Illustration 3-16 on page 116 of the text for a Summary of the debit/credit rules.

TEACHING TIP

Show students how to record transactions in the account using the information for Sierra that

was entered in the extended balance sheet equation.

On October 1, cash of $10,000 is invested in the business by investors, in exchange for

$10,000 of Sierra Corporation common stock. Both Cash and Common Stock would increase

by $10,000.

Cash

Common Stock

3-6

Now think of the elements in Stockholders’ Equity. Three of these elements:

Common Stock,

Retained Earnings, and

Revenue

increase stockholders’ equity. Therefore these three accounts—Common Stock, Retained

Earnings, and Revenue are increased by credit entries and decreased by debit entries.

TEACHING TIP

Many students work in banks and have trouble with the rules of debits and credits. Explain

why they view the rules differently.

3-7

Learning Objective 4 – Identify the Basic Steps in the Recording Process

Steps in the Recording Process—The basic steps in the accounting process are used

by most businesses in the recording process. The steps are:

▪ Analyze each transaction in terms of its effect on the accounts. A source

Learning Objective 5 – Explain What A Journal is and How it Helps in the

Recording Process

The Journal—Transactions are initially recorded in chronological order in

journals before they are transferred to the accounts.

▪ The journal shows the debit and credit effects on specific accounts for each

transaction.

▪ Companies may use various types of journals, but every company has the most

basic form of journal, a general journal.

▪ Entering transaction data in the journal is known as journalizing.

▪ The journal makes three significant contributions to the recording process:

○ The journal discloses in one place the complete effect of a transaction.

TEACHING TIP

Show students examples of proper journal entries. Return to the example of Sierra. On

October 1, cash of $10,000 is invested in the business by investors, in exchange for $10,000

of Sierra Corporation common stock. Both Cash and Common Stock would increase by

$10,000. This transaction would be recorded in the following manner:

Date

Account Titles and Explanation

Debit

Credit

10/1

Cash ……………………………………………………………

10,000

Common Stock………………………………………..

(Issued stock for cash)

See Illustration 3-18 on page 118 of the text for more examples related to the Sierra

example.

3-8

Learning Objective 6 – Explain What a Ledger is and How it Helps in the

Recording Process

The Ledger—The entire group of accounts maintained by a company is referred to as

the ledger.

▪ The general ledger contains all of the asset, liability and stockholders’ equity

TEACHING TIP

What is a journal? Where have you heard this term before? We typically think of foreign

correspondents keeping journals. Journals are actually diaries. We can think of the journal

used in accounting as a diary that has a chronological listing of the financial transactions of a

the other accounts, accounts receivable, inventory, etc.

Learning Objective 7 – Explain What Posting is and How it Helps in the Recording

Process

Posting—the process of transferring journal entries to the ledger accounts.

▪ Posting accumulates the effects of journal transactions in the individual ledger

accounts. It involves these steps.

o In the ledger, enter in the appropriate columns of the debited account(s) the date

TEACHING TIP

Show journal entries for each of the transactions analyzed earlier.

GENERAL JOURNAL

Date

Account Titles and Explanation

Debit

Credit

2014

Oct 1

Cash ………………………………………………………………………..

10,000

Common Stock …………………………………………………..

10,000

(Issued stock for cash)

3-9

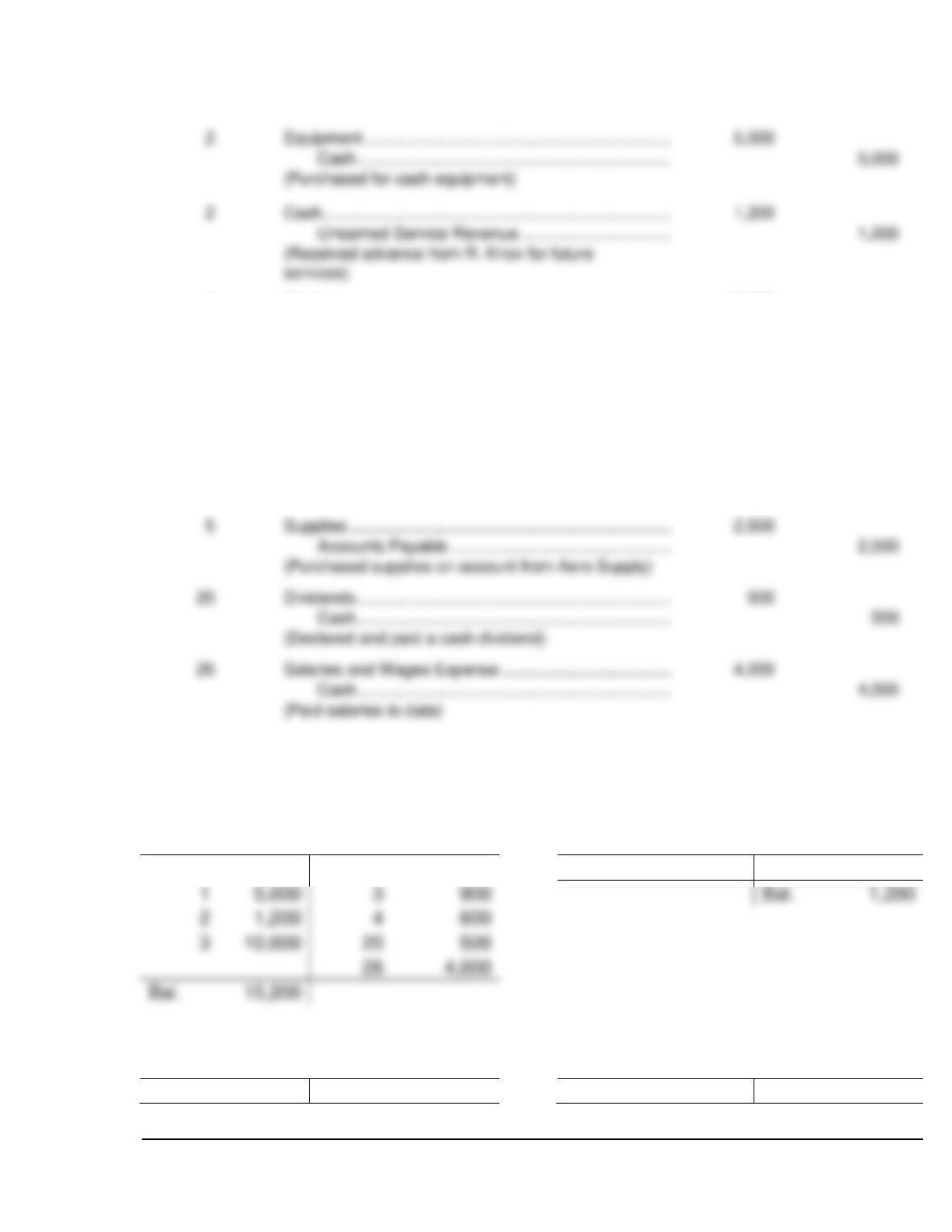

1

Cash ………………………………………………………………………..

5,000

Notes Payable ……………………………………………………

5,000

(Issued 3-month, 12% note payable for cash)

2

Equipment ………………………………………………………………..

5,000

Cash …………………………………………………………………

5,000

(Purchased for cash equipment)

2

Cash ………………………………………………………………………..

1,200

Unearned Service Revenue …………………………………

1,200

3

Cash ………………………………………………………………………..

10,000

Service Revenue ………………………………………………..

10,000

(Received cash for services provided)

3

Rent Expense ……………………………………………………….

900

Cash …………………………………………………………………

900

(Paid cash for October office rent)

4

Prepaid Insurance……………………………………………………..

600

Cash …………………………………………………………………

600

(Paid 1-year policy; effective date October 1)

5

Supplies …………………………………………………………………..

2,500

Accounts Payable ………………………………………………

2,500

(Purchased supplies on account from Aero Supply)

Dividends …………………………………………………………………

500

Cash …………………………………………………………………

500

(Declared and paid a cash dividend)

Salaries and Wages Expense …………………………………….

4,000

Cash …………………………………………………………………

4,000

(Paid salaries to date)

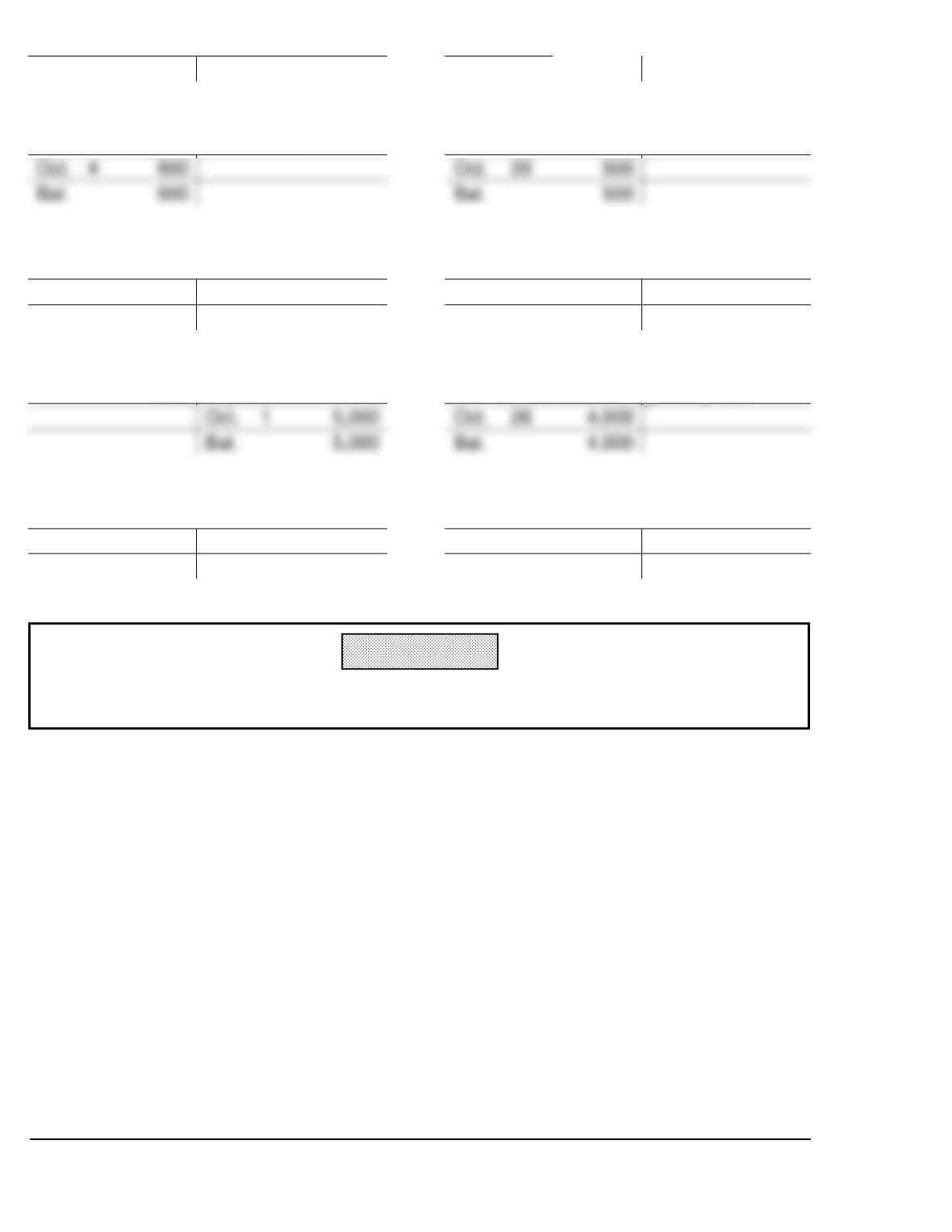

GENERAL LEDGER

Cash

Unearned Service Revenue

Oct. 1

10,000

Oct. 2

5,000

Oct. 2

1,200

1

3

Bal.

2

4

3

10,000

Bal.

15,200

Supplies

Common Stock

Oct. 5

2,500

Oct. 1

10,000

3-10

Bal.

2,500

Bal.

10,000

Prepaid Insurance

Dividends

Oct. 4

Oct. 20

Bal.

600

Bal.

500

Equipment

Service Revenue

Oct. 2

5,000

Oct. 3

10,000

Bal.

5,000

Bal.

10,000

Notes Payable

Salaries and Wages Expense

Oct. 1

Oct. 26

4,000

Bal.

Bal.

4,000

Accounts Payable

Rent Expense

Oct. 5

2,500

Oct. 3

900

Bal.

2,500

Bal.

900

TEACHING TIP

Ask students to compare the information in the General Journal with the information in the

General Ledger. Which is more useful?

3-11

Learning Objective 8 – Explain the Purposes of a Trial Balance

The trial balance—list accounts and their balances on a specific date.The primary purpose

of the trial balance is to prove the mathematical equality of debits and credits after

posting.

A trial balance

▪ uncovers errors in journalizing and posting.

▪ is useful in the preparation of financial statements.

▪ is limited in that it will balance but not uncover errors when:

o A transaction is not journalized.

Learning Objective 9 – Classify Cash Activities as Operating, Investing, or

Financing.

Keeping An Eye On Cash—The Statement of cash flows categorizes the inflows and

outflows of cash during in a given period into three types of activities.

▪ Operating activities are the types of activities the company performs to generate

profits. These can include cash received or spent to directly support the company’s

3-12

IFRS

A Look at IFRS

International companies use the same set of procedures and records to keep track of

transaction data. Thus, the material in Chapter 3 dealing with the account, general rules of

debit and credit, and steps in the recording process—the journal, ledger, and chart of

accounts—is the same under both GAAP and IFRS.

KEY POINTS

• Transaction analysis is the same under IFRS and GAAP but, as you will see in later

chapters, different standards sometimes impact how transactions are recorded.

• Rules for accounting for specific events sometimes differ across countries. For example,

European companies rely less on historical cost and more on fair value than U.S.

• A trial balance under IFRS follows the same format as shown in the textbook.

• As shown in the textbook, dollars signs are typically used only in the trial balance and

the financial statements. The same practice is followed under IFRS, using the currency

of the country that the reporting company is headquartered.

• In February 2010, the SEC expressed a desire to continue working toward a single set

of high-quality standards. In deciding whether the United States should adopt IFRS,

some of the issues the SEC said should be considered are:

▪ Whether IFRS is sufficiently developed and consistent in application.

▪ Whether the IASB is sufficiently independent.

▪ Whether IFRS is established for the benefit of investors.

LOOKING TO THE FUTURE

The basic recording process shown in this textbook is followed by companies across the globe.

It is unlikely to change in the future. The definitional structure of assets, liabilities, equity,

revenues, and expenses may change over time as the IASB and FASB evaluate their overall

conceptual framework for establishing accounting standards.

3-13

Chapter 3 Review

✓ What is the basic accounting equation? How do business transactions effect the basic

accounting equation?

✓ What is an account and how does it help in the recording process?

✓ Define debit and credit and explain how they are used to record business transactions.

✓ What are the basic steps in the recording process?

✓ What is a journal? How does it help in the recording process?

✓ What is a ledger? How does it help in the recording process?