Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 3

Learning Objectives

After studying this chapter, students should be able to:

1. Identify, for social security purposes, those persons covered under the law and those

services that make up employment.

2. Identify the types of compensation that are defined as wages.

3. Apply the current tax rates and wage base for FICA and SECA purposes.

4. Describe the different requirements and procedures for depositing FICA taxes and

income taxes withheld from employees’ wages.

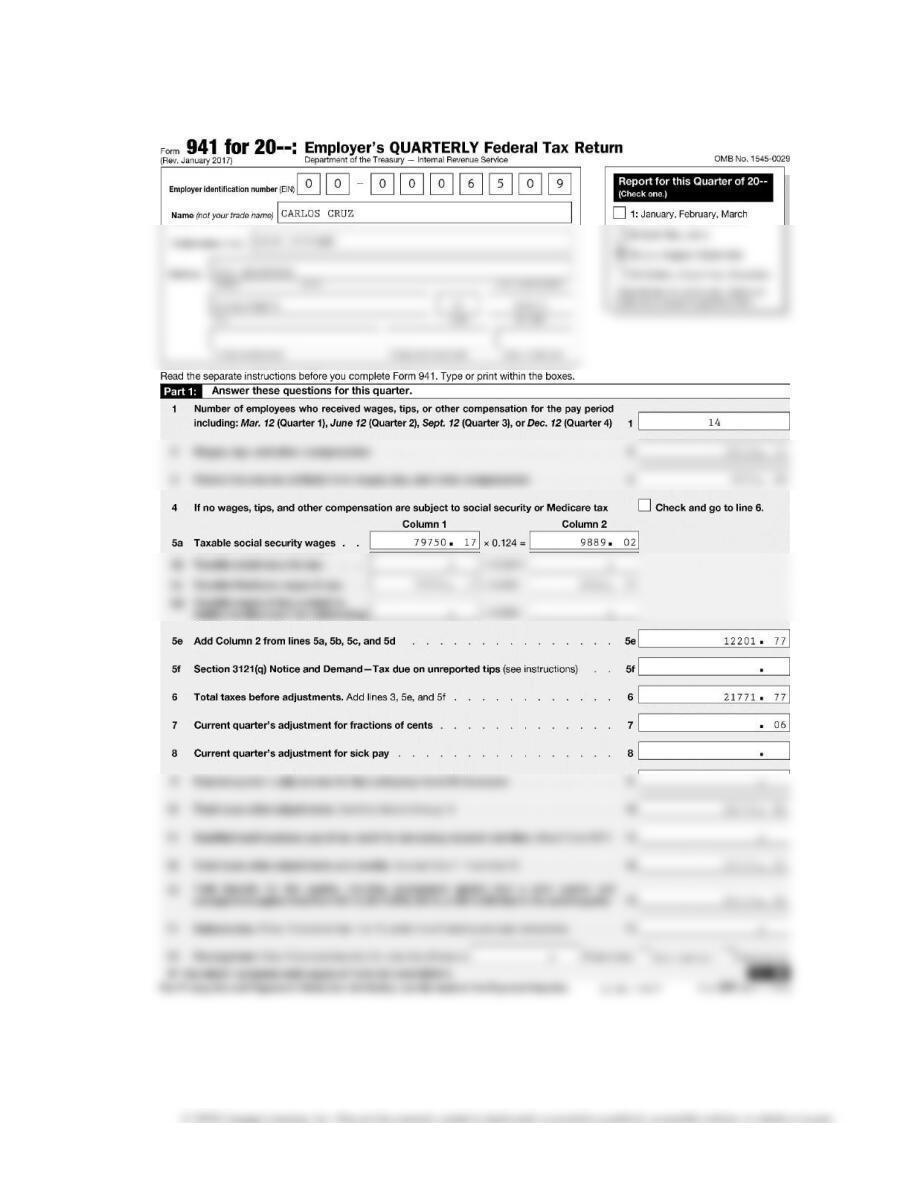

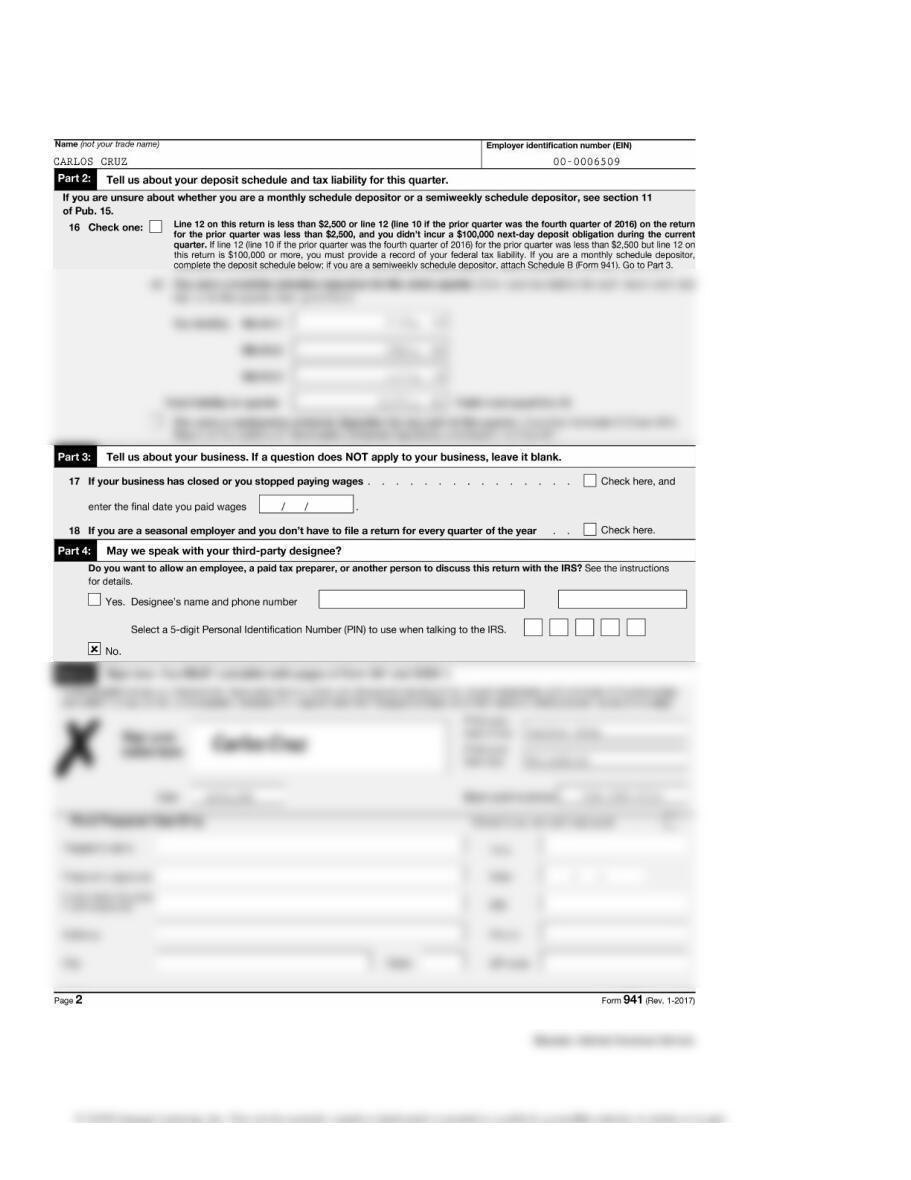

5. Complete Form 941, Employer’s Quarterly Federal Tax Return.

Contents

Chapter 3 outline:

LEARNING OBJECTIVES

COVERAGE UNDER FICA

Employer

Employee

Occupations Specifically Covered by FICA

Government Employees

International Agreements

Family Employment

Household Employee

Exempt Employees

Voluntary Coverage

Independent Contractor

Taxable Wages

Tips

Exempt Payments

Meals and Lodging

Sick Pay

Makeup Pay for Military Duty

Contributions to Deferred Compensation Plans

Payments for Educational Assistance

Tax Rates

3–2 Payroll Accounting

A SELF-EMPLOYED PERSON

Self-Employment Income

Self-Employment OASDI/HI Taxes

Taxable Year

Reporting Self-Employment Income

EMPLOYER IDENTIFICATION NUMBER

EMPLOYEE’S APPLICATION FOR SOCIAL SECURITY CARD (FORM SS-5)

Verifying Social Security Numbers

RETURNS REQUIRED FOR SOCIAL SECURITY PURPOSES

Deposit Requirements (Nonagricultural Workers)

Monthly

Semiweekly

One-Day

The Safe Harbor Rule (98 Percent Rule)

Deposit Requirements for Employers of Agricultural Workers

Deposit Requirements for Employers of Household Employees

Deposit Requirements for State and Local Government Employers

Procedures for Making Deposits

Electronic Deposits

Form 941-X

Form 944

FAILURE-TO-COMPLY PENALTIES

Failure to File Employment Tax Returns

Failure to Fully Pay Employment Taxes

Failure to Make Timely Deposits

Failure to Furnish Payee Statements

Failure to Furnish Information Returns

Bad Checks

KEY TERMS

ANSWERS TO SELF-STUDY QUIZZES

KEY POINTS SUMMARY

Chapter 3 3–3

Matching Quiz (p. 3–35)

Questions for Review (p. 3–35)

1. To be classified as a “covered” employer, the person must employ one or more

law relationship of employer and employee exists, the employer is covered.

2. To be classified as a “covered” employee, an individual must perform services in a

4. Refer to Figure 3.2, which lists the Test for Independent Contractor Status. By

5. a. Employers must collect the employee’s FICA taxes on tips reported by each

employee. The employee’s FICA taxes are deducted from the wages due

6. Payments of sick pay made after the expiration of six calendar months following the

last month in which the employee worked for the employer are not taxed. The first

8. Yes. If individuals such as Luis paid OASDI taxes on wages in excess of $127,200

because of having worked for more than one employer, they are entitled to a refund

3–4 Payroll Accounting

9. For 2017, the SECA tax rates for self-employed persons are OASDI—12.4 percent

11. The deposit rules for nonagricultural employers are:

13. There are two electronic methods of deposit:

to the Treasury’s account at the Federal Reserve Bank.

14. Generally, an employer must file Form 941 each calendar quarter. Form 941 is due

on or before the last day of the month following the close of the calendar quarter for

15. The following penalties may be imposed:

a. If the employer does not file Form 941 by the due date, a percentage of the tax

Chapter 3 3–5

If, however, the employer shows to the satisfaction of the IRS that the failure to

Questions for Discussion (p. 3–35)

1. Sean Matthew’s entire salary of $250,000 will be taxed at the Employee HI rate of

1.45 percent with an additional 0.9 percent on wages in excess of $200,000. The

2. By diverting his payroll tax money to business uses, Emerald faces a penalty. It

may take the IRS as much as a year to do anything more than send overdue tax

3. If correctly treated as an employee, the employer would incur the employer OASDI

and HI tax on McGinnis’s wages. The penalty for misclassifying an employee as an

Independent Contractor will be the employer’s share of FICA taxes plus the income

4. Under FICA (as well as under FUTA and for purposes of federal income tax

withholding), amounts paid to employees that represent the difference between the

3–6 Payroll Accounting

Problem Sets (p. 3–37)

The principles and practices of payroll accounting discussed in Chapter 3 are applied in

the Problem Sets as shown below.

Principle or Practice Problem Set No. (A and B)

1. Calculating employee’s FICA taxes to 3–1 through 3–7, 3–9

be withheld through 3–10, 3–17

2. Calculating employer’s FICA taxes 3–1, 3–3, 3–6, 3–7,

3–9 through 3–10,

3–17

3. FICA taxes on regular earnings and 3–8

self-employment income

4. Computing monthly gross earnings, 3–10

deductions for FICA, and net earnings

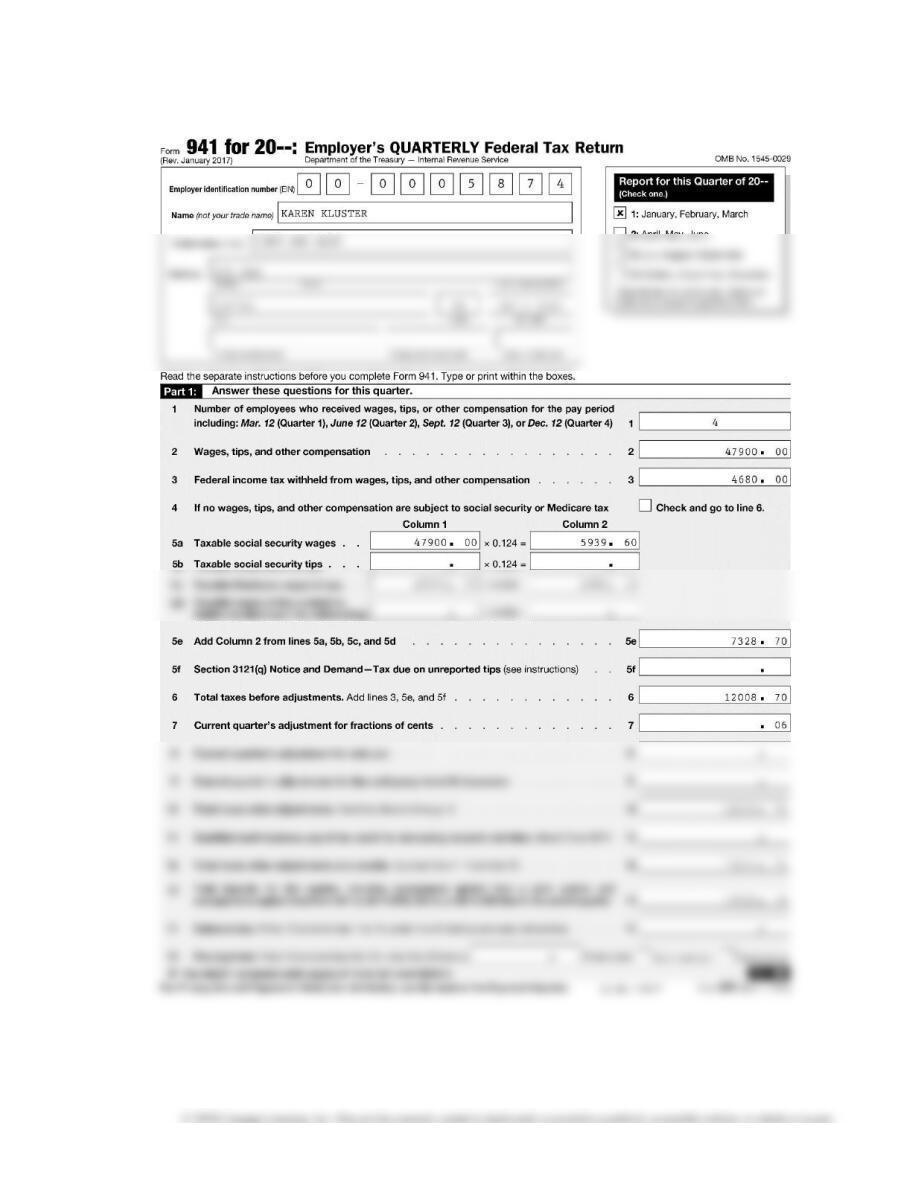

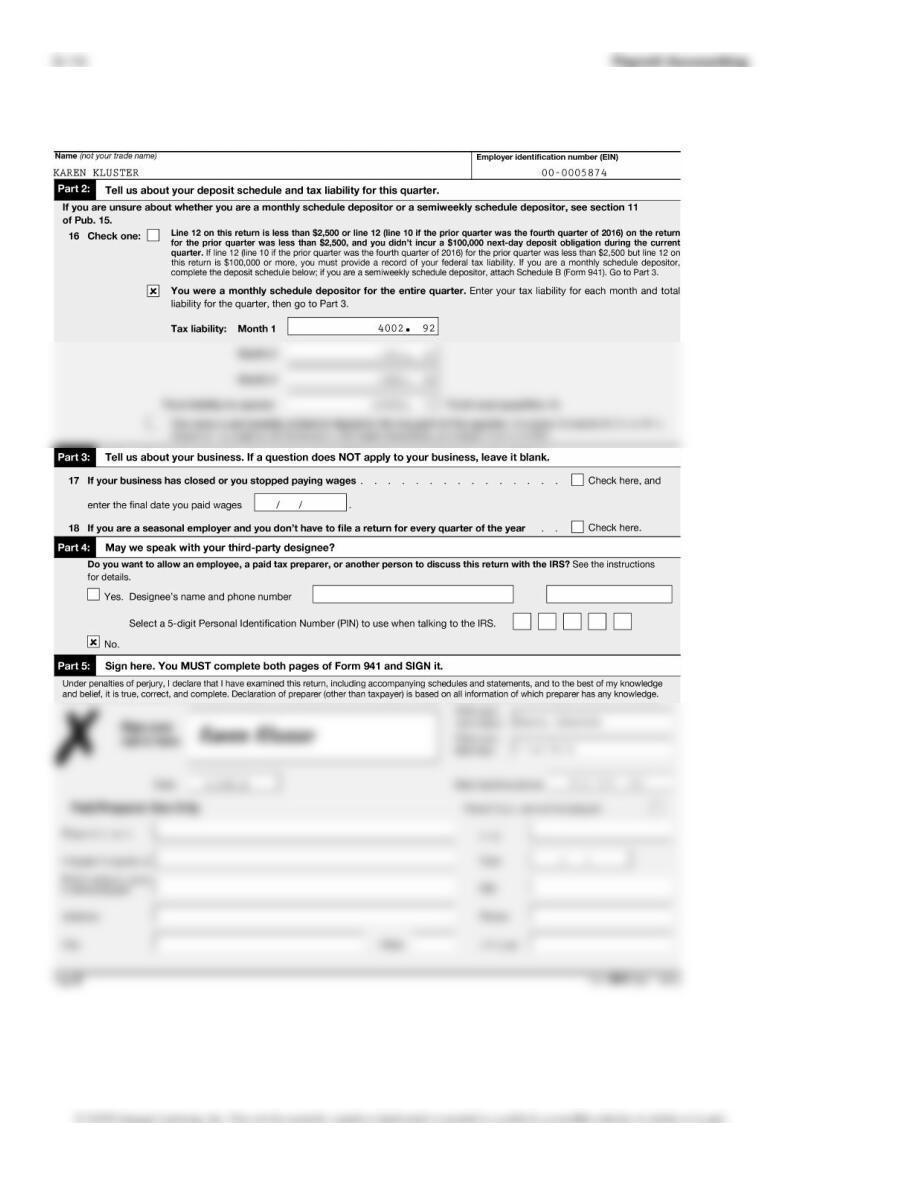

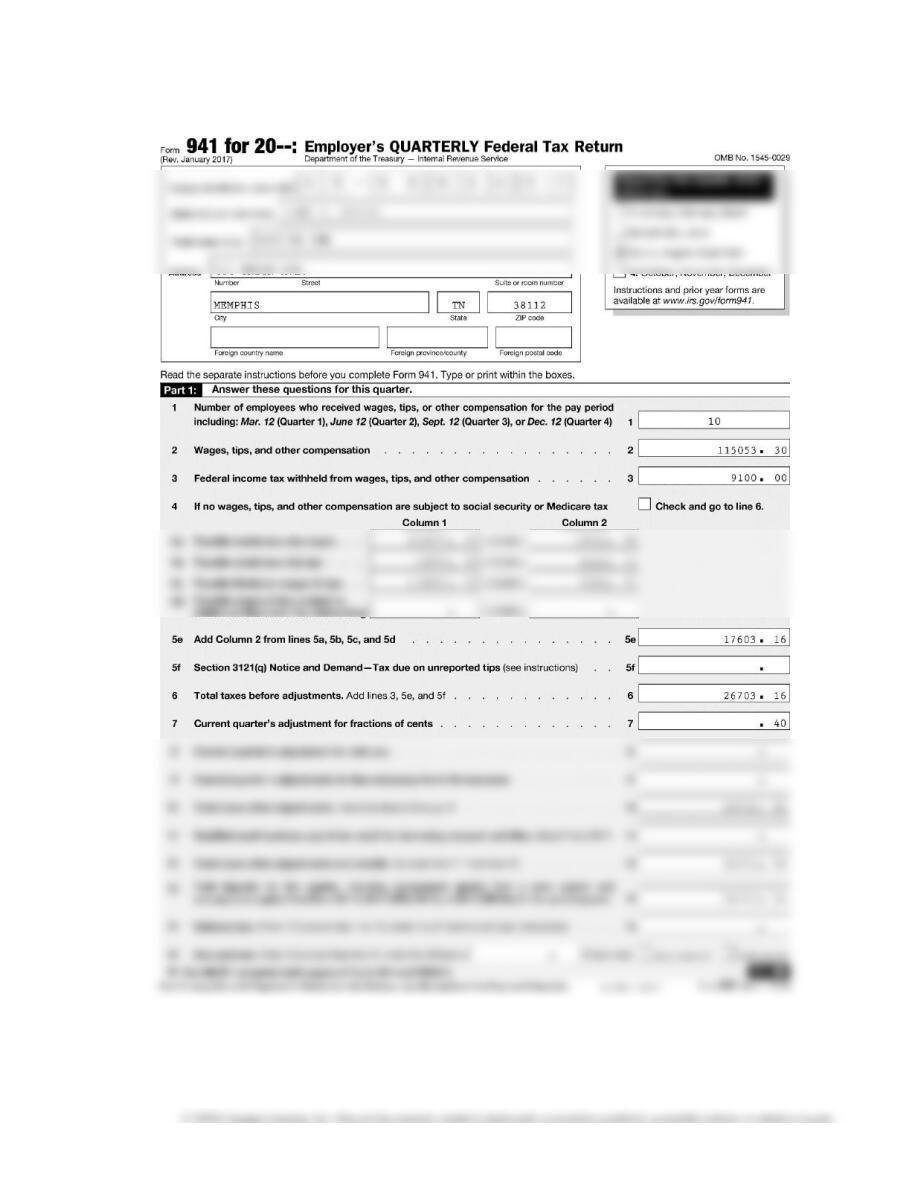

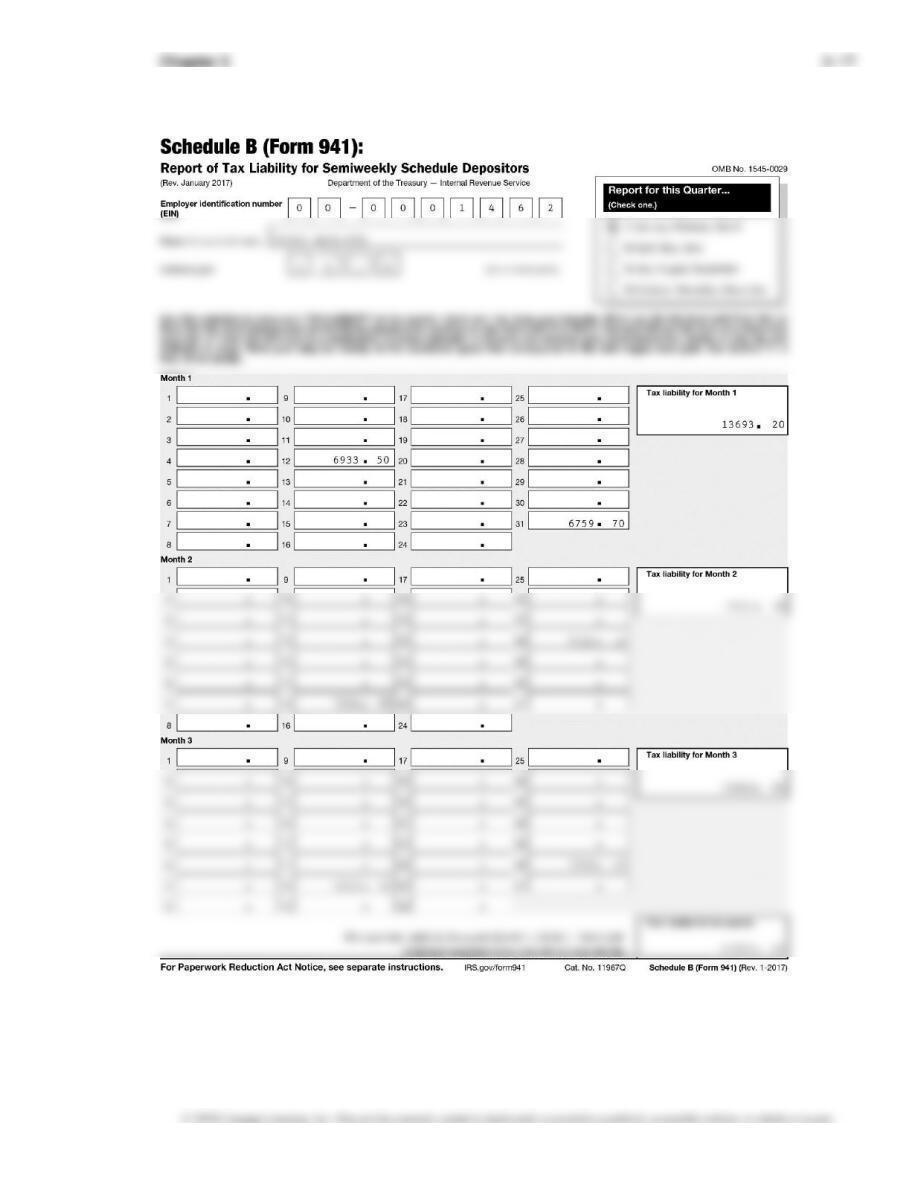

5. Completing Form 941 3–11 through 3–15

6. Calculating penalty for failure to make 3–16

timely deposit

Chapter 3 3–7

Solutions—Problem Set A

3–1A.

Biweekly

Employee Taxable FICA Taxes

No. Employee Name Wages OASDI HI

711 Castro, Manny $ 1,000.00 $ 62.00 $ 14.50

512 Corrales, Pat 968.00 60.02 14.04

3–2A.

OASDI HI

3–3A.

OASDI HI

3–4A.

3–8 Payroll Accounting

3–5A.

November 15

Name and Title

Annual

Salary

OASDI

Taxable

Earnings

OASDI

Tax

HI

Taxable

Earnings

HI

Tax

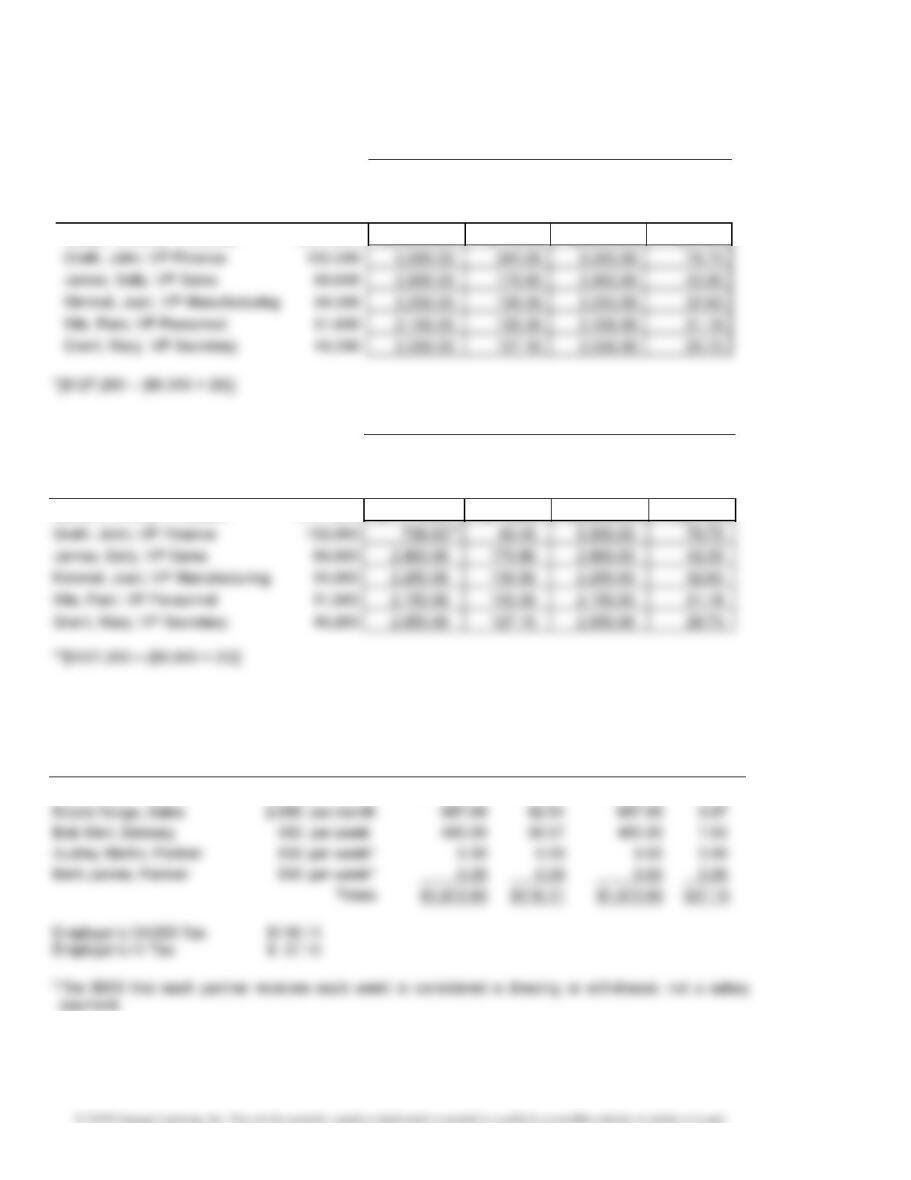

Hanks, Timothy, President $151,200 $1,200.00* $ 74.40 $6,300.00 $91.35

December 31

Name and Title

Annual

Salary

OASDI

Taxable

Earnings

OASDI

Tax

HI

Taxable

Earnings

HI

Tax

Hanks, Timothy, President $151,200 $ 0.00 $ 0.00 $6,300.00 $91.35

3–6A.

Name and Position

Salary

OASDI

Taxable

Earnings

OASDI

Tax

HI

Taxable

Earnings

HI

Tax

Zena Vertin, Office $ 700 per week $ 700.00 $ 43.40 $ 700.00 $10.15

Chapter 3 3–9

3–7A.

3–8A.

3–9A.

Employee

Annual

Salary

OASDI

Taxable

Wages

OASDI

Tax

HI

Taxable

Wages

HI

Tax

Utley, Genna $ 37,040 $ 3,086.67 $ 191.37 $ 3,086.67 $ 44.76

Werth, Norm 48,900 4,075.00 252.65 4,075.00 59.09

3–10A.

Employees

Total

Monthly

Payroll

OASDI

Taxable

Wages

OASDI

Tax

HI

Taxable

Wages

HI

Tax

Full-Time Office:

Adaiar, Gene ............................................................................... $ 2,450.00 $ 2,450.00 $ 151.90 $ 2,450.00 $ 35.53

Crup, Jason ................................................................................. 2,300.00 2,300.00 142.60 2,300.00 33.35

3–10 Payroll Accounting

Chapter 3 3–11

3–11A.

3–12 Payroll Accounting

3–12A.

Chapter 3 3–13

3–13A.

3–13A. Concluded

Source: Internal Revenue Service.

Chapter 3 3–15

3–14A.

3–14A. Concluded

3–15A. (a)

Source: Internal Revenue Service.