3-79 Ch. 3—Problems

Problem 3A-1, Concluded

See solution to Problem 3-2 for value analysis, D&D schedule, and amortization schedules.

Eliminations and Adjustments:

(CY) Eliminate the current-year entries made in the investment account and in the

subsidiary income account.

(EL) Eliminate the pro rata share of Solar Company equity balances at the beginning

Income Distribution Schedules

Solar Company

Building depreciation ………………… $3,000 Internally generated net

income ………………………………. $90,000

Adjusted income ………………………. $87,000

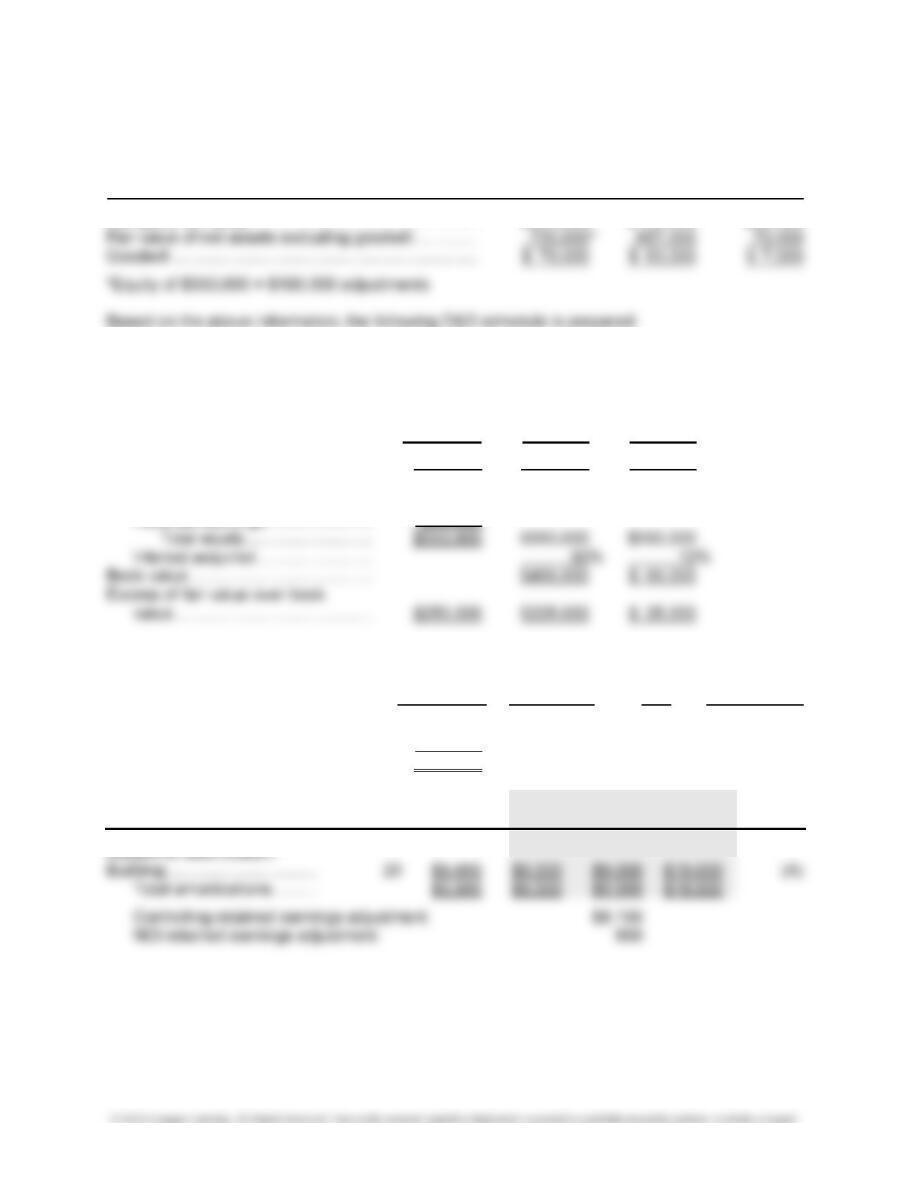

PROBLEM 3A-2

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ………………………………………….. $1,040,000 $850,000 $190,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $1,040,000 $850,000 $190,000

Less book value of interest acquired:

Common stock ($10 par) …………. $ 150,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Land ………………………………………….. $ 20,000 debit D1

Equipment ………………………………….. 80,000 debit D2 10 $8,000

Problem 3A-2, Continued

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

Subject to amortization:

Equipment ……………………….. 10 $ 8,000 $ 8,000 $16,000 $24,000 (A2)

Eliminations and Adjustments:

(CY) Eliminate the current-year entries made in the investment account to arrive at the

January 1, 2017, balance:

(CY1) 80% of subsidiary loss.

determination and distribution of excess schedule:

(D1) Increase Land by $20,000.

(D3) Increase Building by $60,000.

(A2) Record $8,000 annual increase in equipment depreciation for current and prior years.

See account adjustment schedule.

(A3) Record $3,000 annual increase in building depreciation for current and prior years.

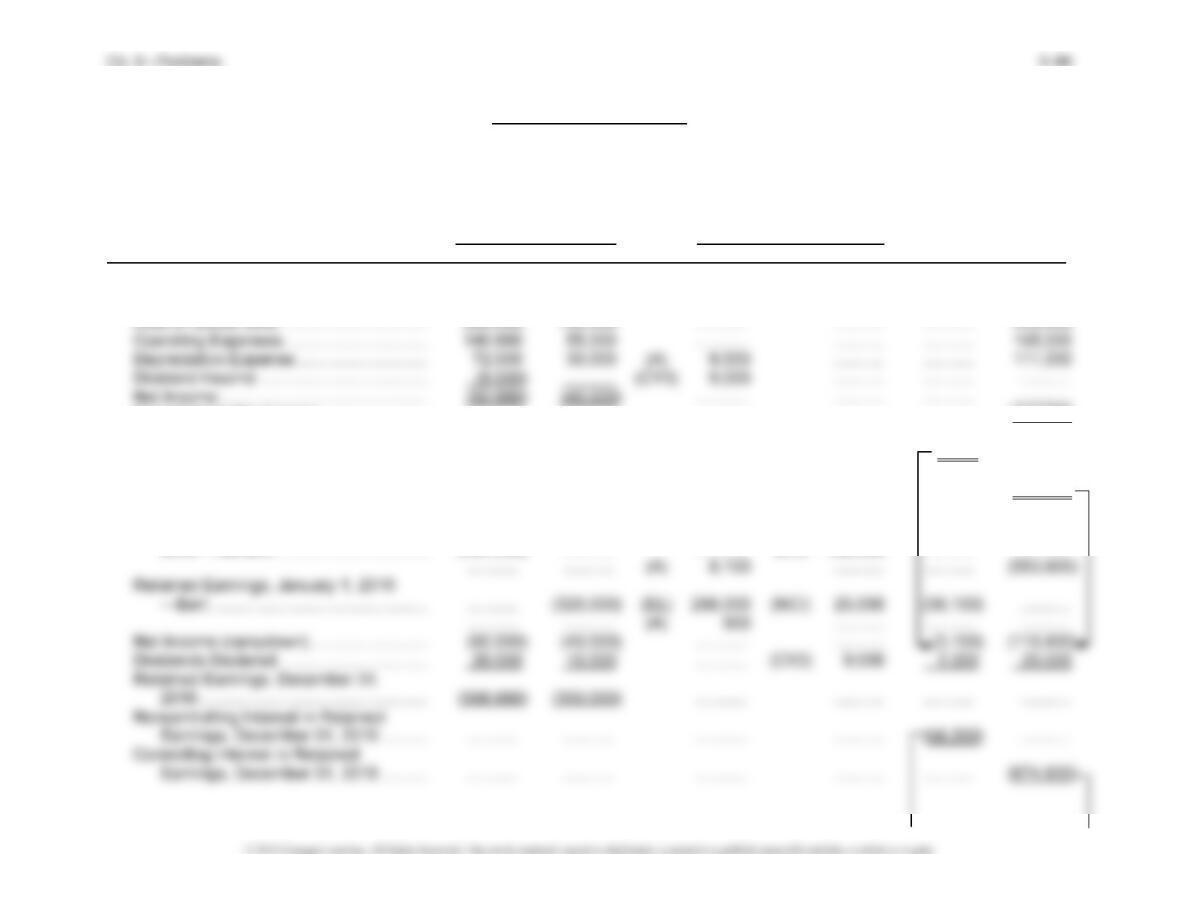

Problem 3A-2, Continued

Baker Enterprises and Kohlenberg International

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Baker Kohlenberg Dr. Cr. Interest dated

Income Statement:

Sales ………………………………………………. (650,000) (320,000) ……….. ……….. ……….. (970,000)

Cost of Goods Sold …………………………… 260,000 240,000 ……….. ……….. ……….. 500,000

Operating Expense …………………………… 170,000 70,000 ……….. ……….. ……….. 240,000

schedule)…………………………………………. ……….. ……….. ……….. ……….. 6,200 ………..

Controlling Interest (see distribution

schedule)…………………………………………. ……….. ……….. ……….. ……….. ……….. (130,200)

Retained Earnings:

Retained Earnings, January 1, 2017—

Baker …………………………………………. (625,000) ……….. (A2–A3) 17,600 ……….. ……….. (607,400)

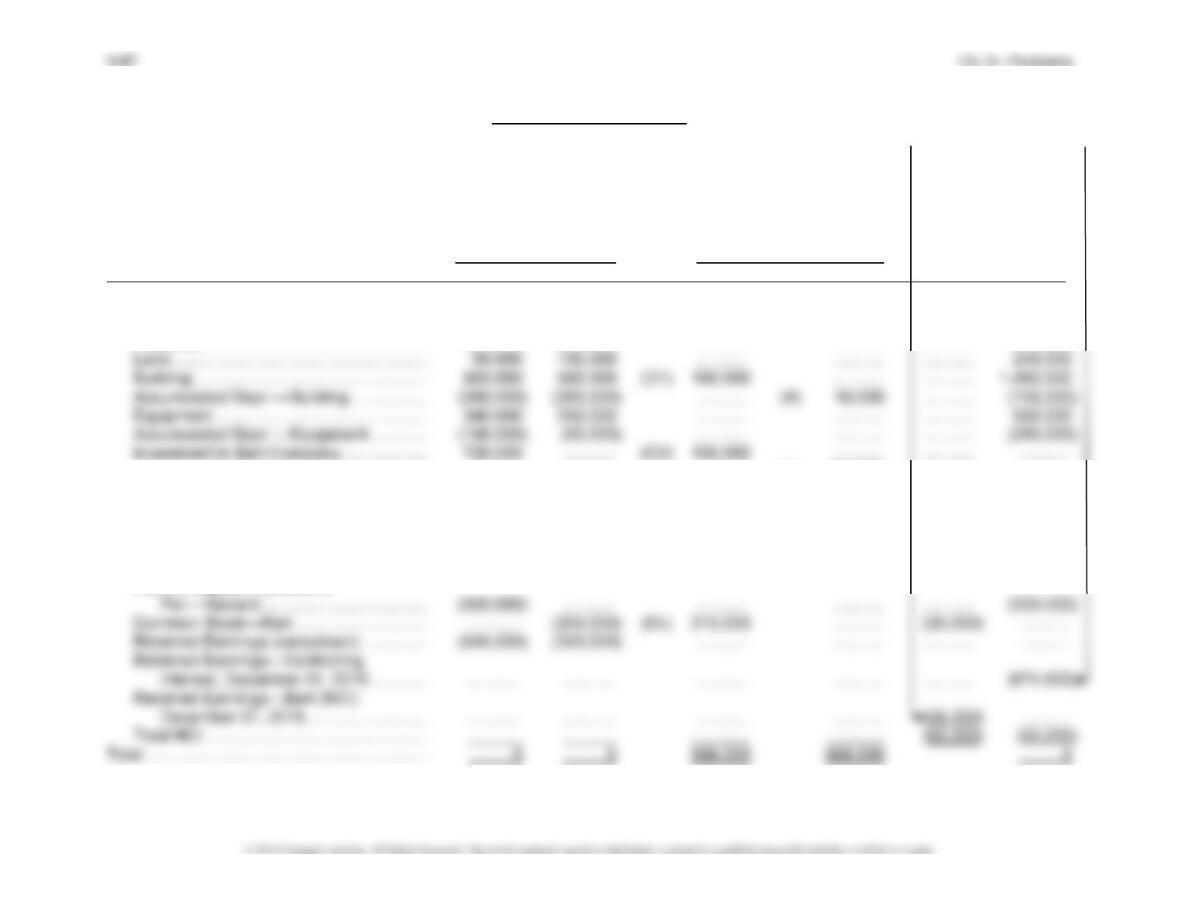

Problem 3A-2, Continued

Baker Enterprises and Kohlenberg International

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

(Concluded)

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Baker Kohlenberg Dr. Cr. Interest dated

Balance Sheet:

Cash ……………………………………………….. 288,000 170,000 ……….. ……….. ……….. 458,000

Inventory …………………………………………. 135,000 400,000 ……….. ……….. ……….. 535,000

Goodwill ………………………………………….. ……….. ……….. (D4) 130,000 ……….. ……….. 130,000

Liabilities …………………………………………. (248,000) (40,000) ……….. ……….. ……….. (288,000)

Bonds Payable …………………………………. ……….. (200,000) ……….. ……….. ……….. (200,000)

Common Stock—Baker ……………………… (1,200,000) ……….. ……….. ……….. ……….. (1,200,000)

Common Stock—Kohlenberg ……………… ……….. (150,000) (EL) 120,000 ……….. (30,000) ………..

Problem 3A-2, Concluded

Subsidiary Kohlenberg International Income Distribution

Internally generated net loss ……. $20,000

Building depreciation ………………. 3,000

Equipment depreciation ………….. 8,000

Parent Baker Enterprises Income Distribution

80% × Kohlenberg adjusted Internally generated net

3-85 Ch. 3—Problems

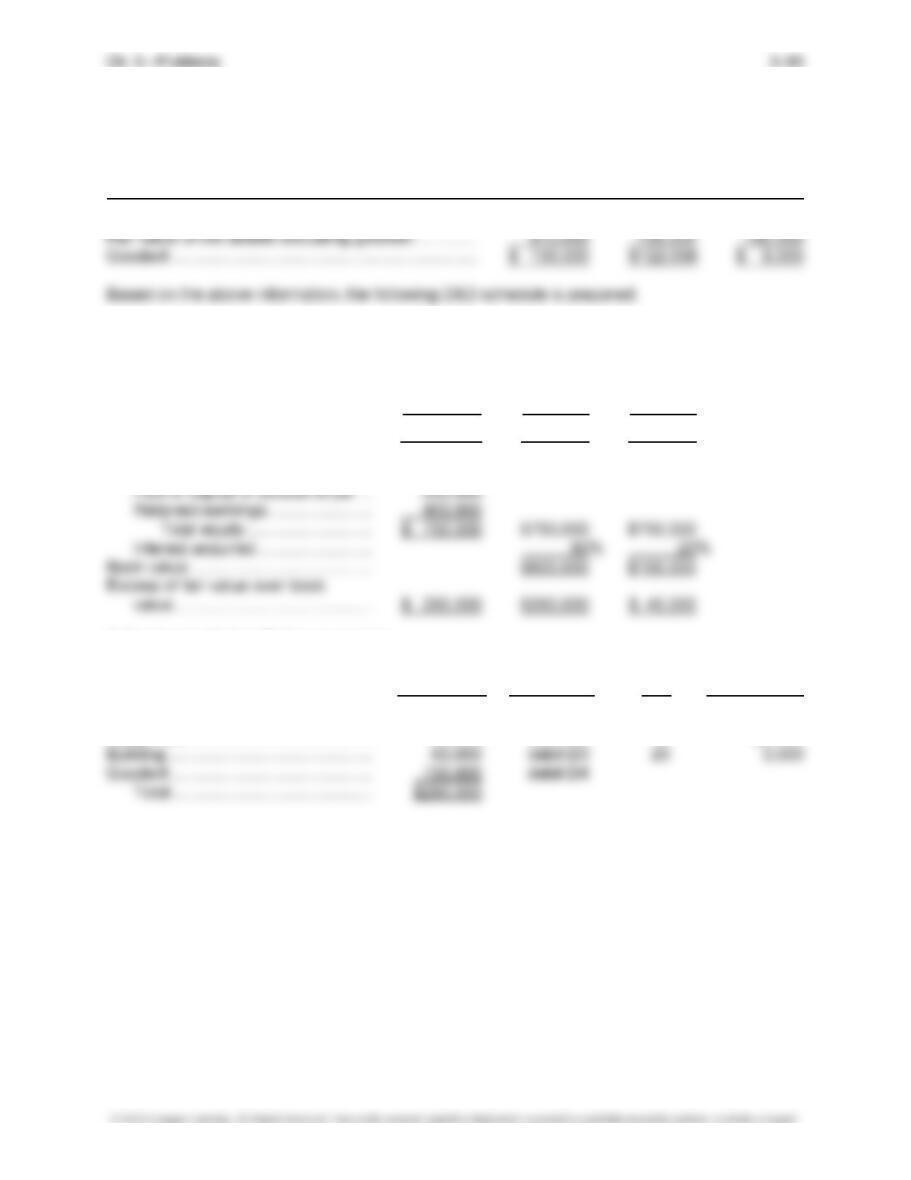

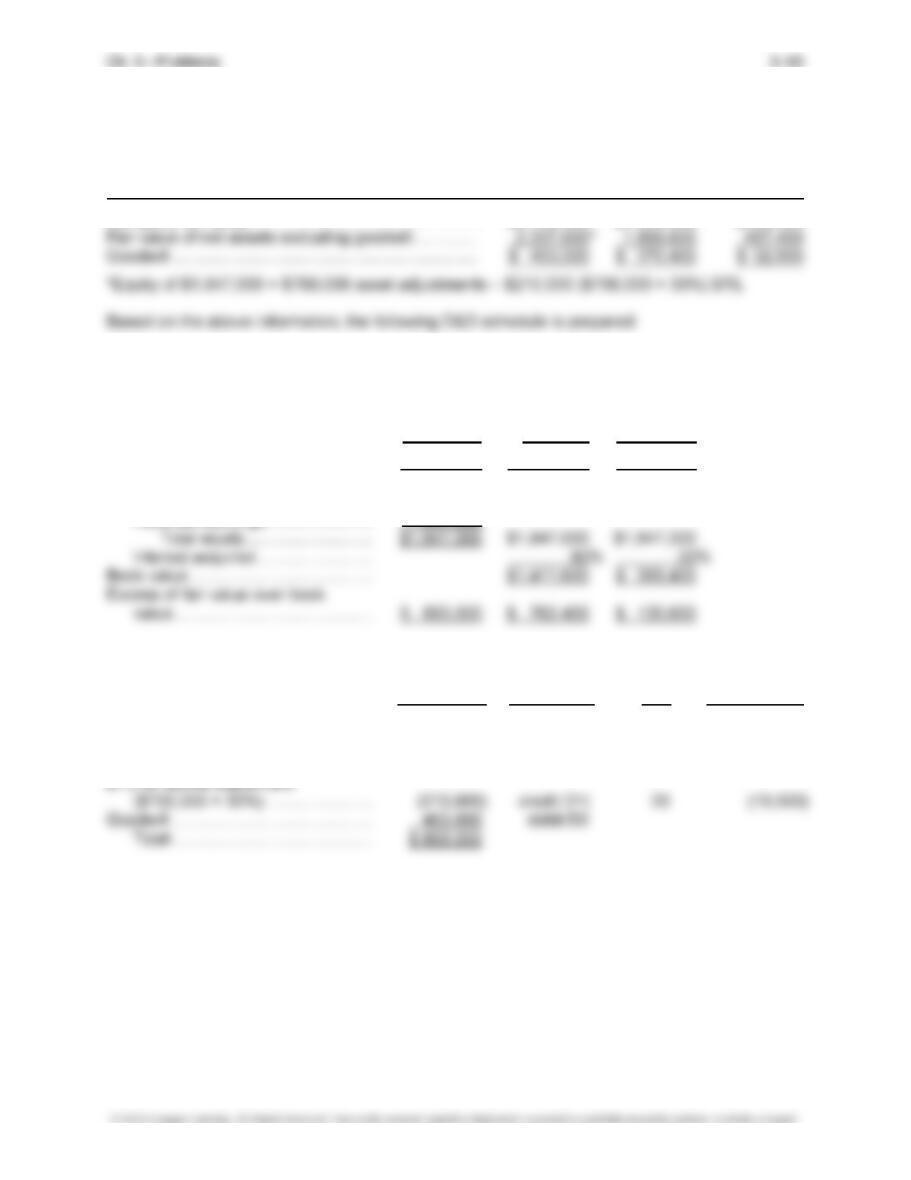

PROBLEM 3A-3

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (90%) (10%)

Company fair value ………………………………………….. $800,000 $720,000 $80,000

Based on the above information, the following D&D schedule is prepared:

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………………… $800,000 $720,000 $ 80,000

Less book value of interest acquired:

Common stock ($10 par) …………. $350,000

Retained earnings ………………….. 200,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Building ……………………………………… $180,000 debit D1 20 $9,000

Goodwill …………………………………….. 70,000 debit D2

Total …………………………………. $250,000

Annual Current Prior

Account Adjustments Life Amount Year Years Total Key

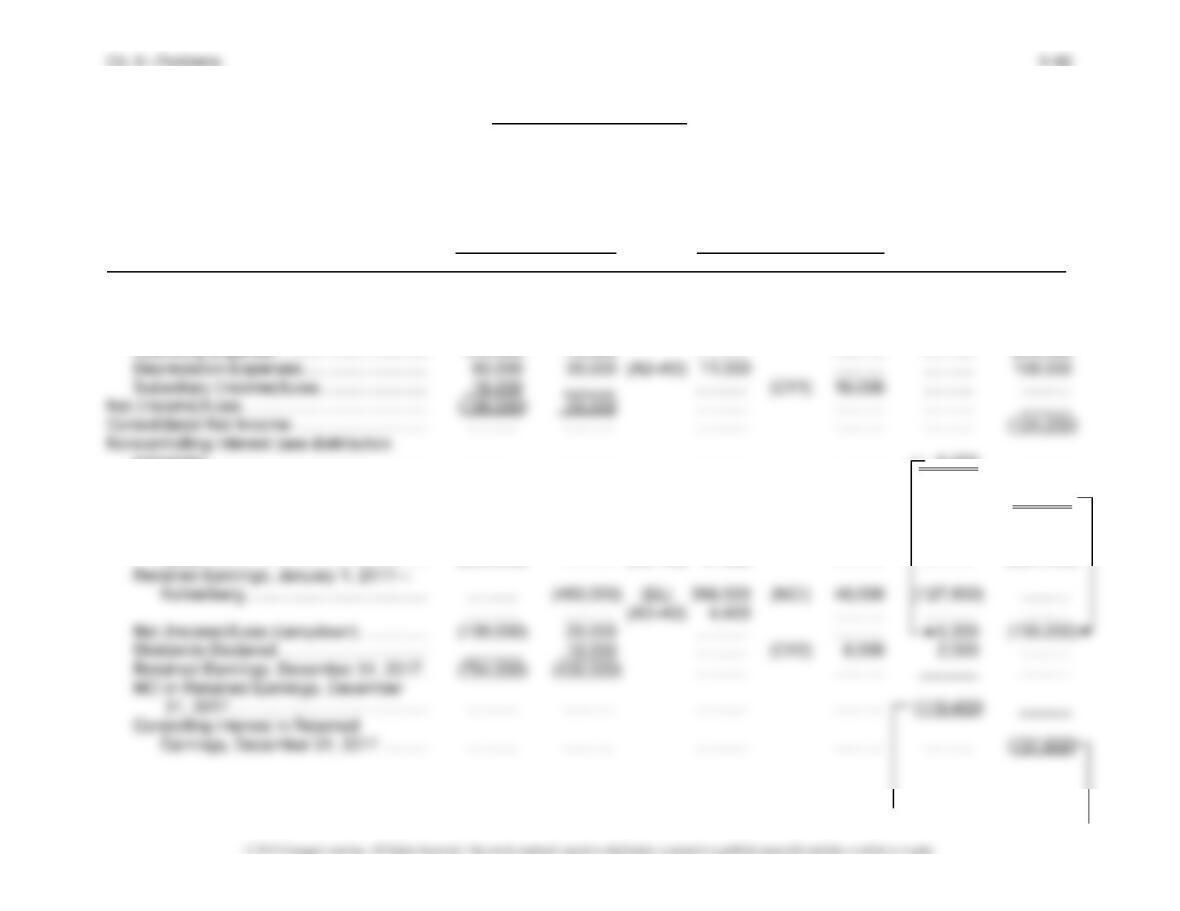

Problem 3A-3, Continued

Harvard Company and Subsidiary Bart Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Harvard Bart Dr. Cr. Interest dated

Income Statement:

Sales ………………………………………………. (580,000) (280,000) ……….. ……….. ……….. (860,000)

Consolidated Net Income …………………… ……….. ……….. ……….. ……….. ……….. (114,000

Noncontrolling Interest (see

distribution schedule) …………………… ……….. ……….. ……….. ……….. (3,100) ………..

Controlling Interest (see

distribution schedule) …………………… ……….. ……….. ……….. ……….. ……….. (110,900)

Retained Earnings Statement:

Retained Earnings, January 1,

2016—Harvard ……………………………. (484,000) ……….. ……….. (CV) 108,000 ……….. ………..

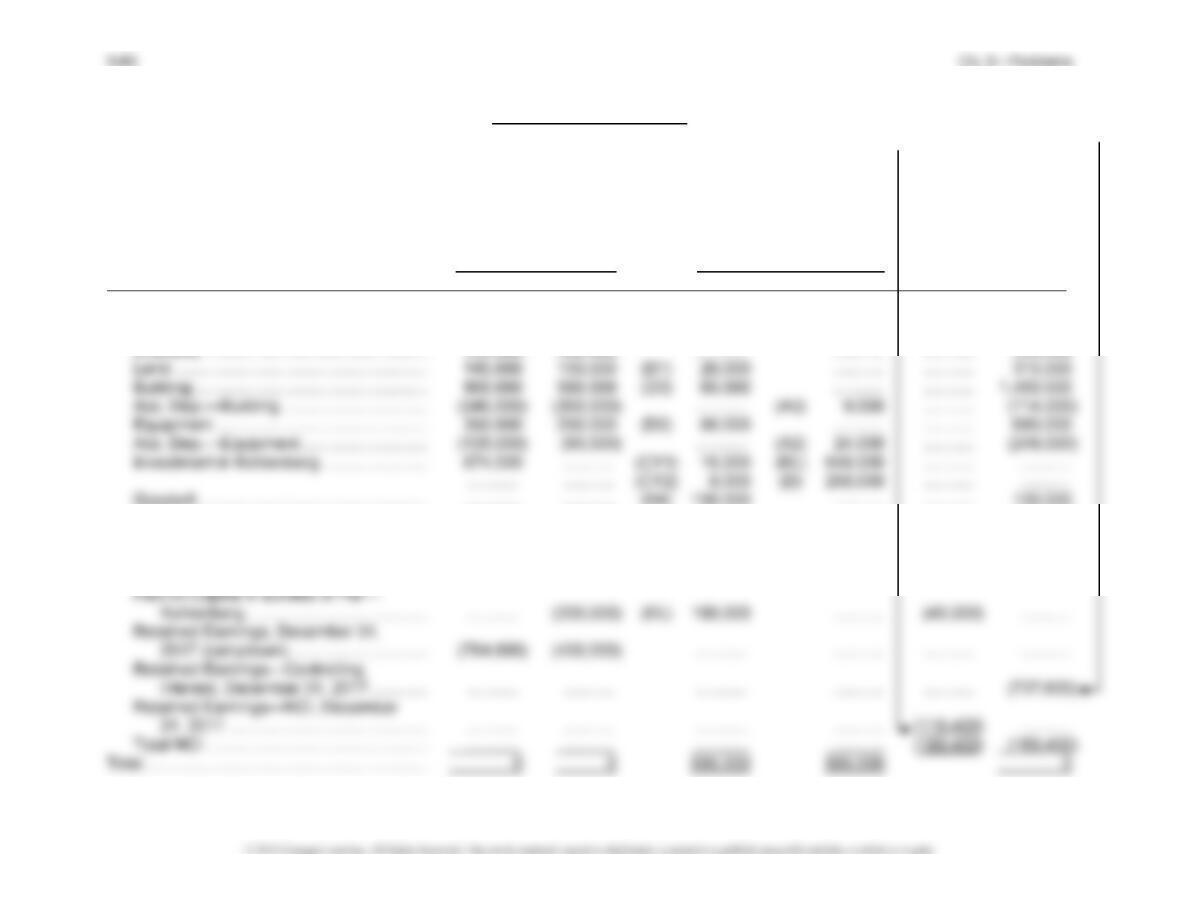

Problem 3A-3, Continued

Harvard Company and Subsidiary Bart Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Harvard Bart Dr. Cr. Interest dated

Balance Sheet:

Cash ……………………………………………….. 330,000 170,000 ……….. ……….. ……….. 500,000

Inventory …………………………………………. 260,000 340,000 ……….. ……….. ……….. 600,000

……….. ……….. ……….. (EL) 603,000 ……….. ………..

……….. ……….. ……….. (D) 225,000 ……….. ………..

Goodwill ………………………………………….. ……….. ……….. (D2) 70,000 ……….. ……….. 70,000

Current Liabilities ……………………………… (123,000) (60,000) ……….. ……….. ……….. (183,000)

Bonds Payable …………………………………. ……….. (200,000) ……….. ……….. ……….. (200,000)

Common Stock—Harvard ………………….. (800,000) ……….. ……….. ……….. ……….. (800,000)

Paid-In Capital in Excess of

Problem 3A-3, Concluded

Eliminations and Adjustments:

(CV) Convert from the cost to the equity method as of January 1, 2016 [90% × ($320,000 –

$200,000)].

(CY2) Eliminate the 90% ownership portion of the subsidiary dividends.

(EL) Eliminate the 90% ownership portion of the subsidiary equity accounts against the

(A) Record amortizations resulting from the revaluations of entry 3. Record $9,000 annual

increase in building depreciation for current and prior years. See amortization

schedule.

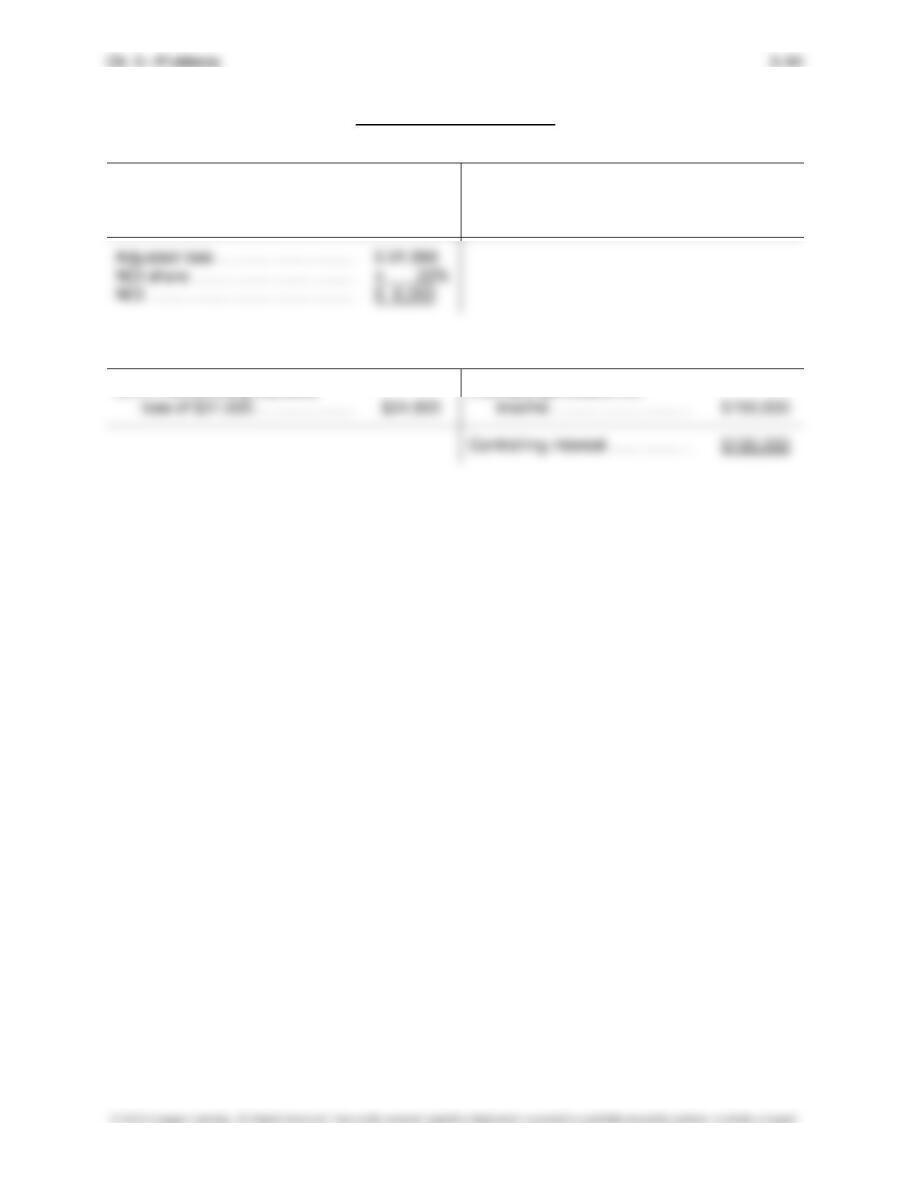

Subsidiary Bart Company Income Distribution

Building depreciation ………………… $9,000 Internally generated net

income …………………………… $40,000

PROBLEM 3B-1

Entry to record investment:

Problem 3B-1, Concluded

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (90%) (10%)

Company fair value ………………………………………….. $800,000 $720,000 $80,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………………… $800,000 $720,000 $ 80,000

Less book value of interest acquired:

Common stock ($10 par) …………. $100,000

Paid-in capital in excess of par … 150,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Inventory ($200,000 fair – $150,000

book value)……………………………. $ 50,000 debit D1

Depreciable fixed assets ($500,000

fair – $400,000 book value) ……… 100,000 debit D2 20 $5,000

Investment in marketable securities

($170,000 – $150,000 book value) 20,000 debit D3

PROBLEM 3B-2

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ………………………………………….. $2,740,000 $2,240,000 $500,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $2,740,000 $2,240,000 $ 500,000

Less book value of interest acquired:

Common stock ($100 par) ……….. $1,000,000

Retained earnings ………………….. 847,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Depreciable fixed assets

($2,800,000 fair – $2,100,000

book value)……………………………. $ 700,000 debit D1 20 $ 35,000

3-91 Ch. 3—Problems

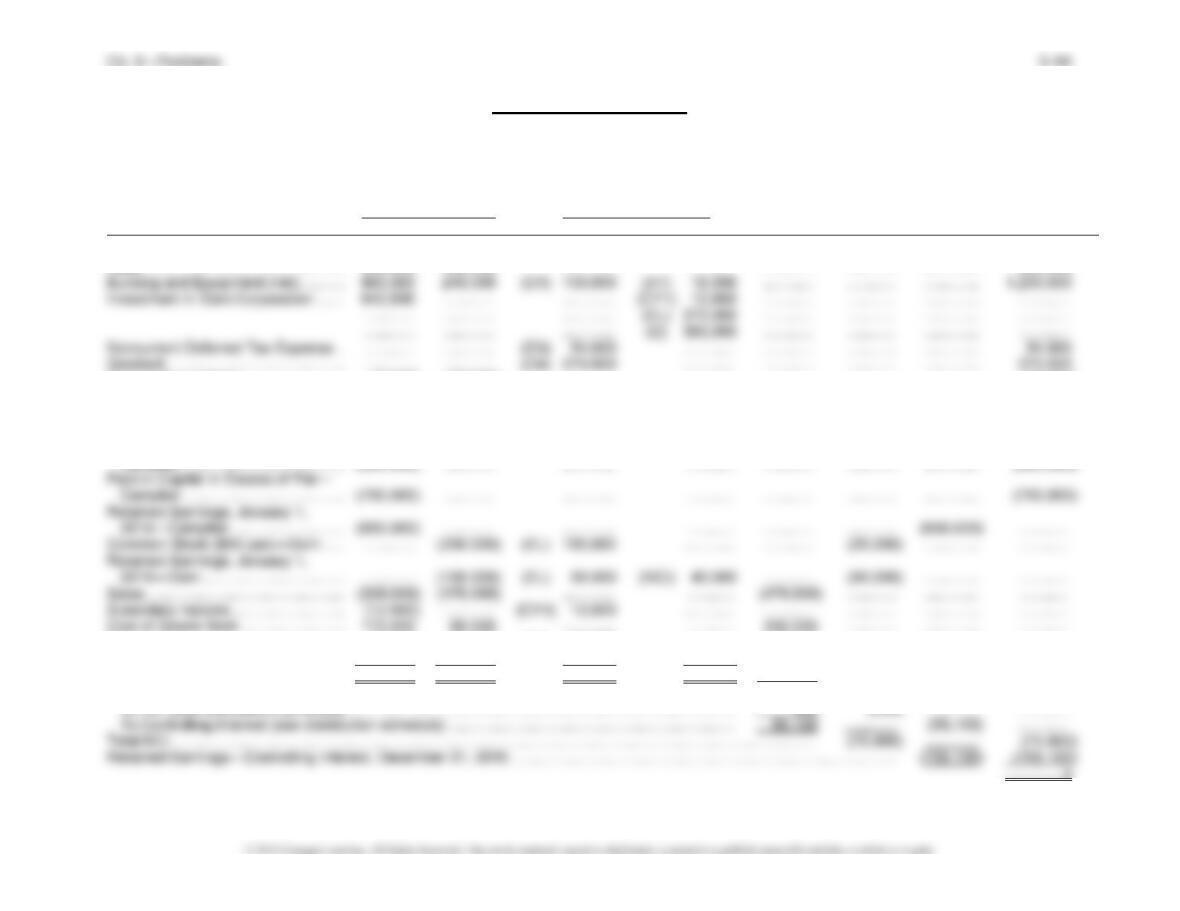

Problem 3B-2, Continued

Todd Company and Subsidiary Keller Company

Worksheet for Consolidated Balance Sheet

December 31, 2016

Financial Eliminations Non-

Statements and Adjustments controlling Consoli-

Todd Keller Dr. Cr. Interest dated

Cash ………………………………………….. 1,200,000 50,000 …………. ………….. ………….. 1,250,000

Accounts Receivable …………………… 2,400,000 300,000 …………. ………….. ………….. 2,700,000

Payables ……………………………………. (7,200,000) (1,750,000) …………. ………….. ………….. (8,950,000)

Accruals …………………………………….. (1,615,000) (400,000) …………. ………….. ………….. (2,015,000)

Deferred Tax Liability …………………… …………. ………….. …………. (D1t) 210,000 ………….. (210,000)

Common Stock ($100 par)—Todd …. (1,000,000) ………….. …………. ………….. ………….. (1,000,000)

Eliminations and Adjustments:

(CY) N/A because worksheet is prepared on the same day as consolidation.

(EL) Elimination of 80% of the subsidiary equity against the investment.

(D)/(NCI) Distribute the balance of the investment account, $762,400 and the $130,600 NCI adjustment, to the specific subsidiary

Ch. 3—Problems 3–92

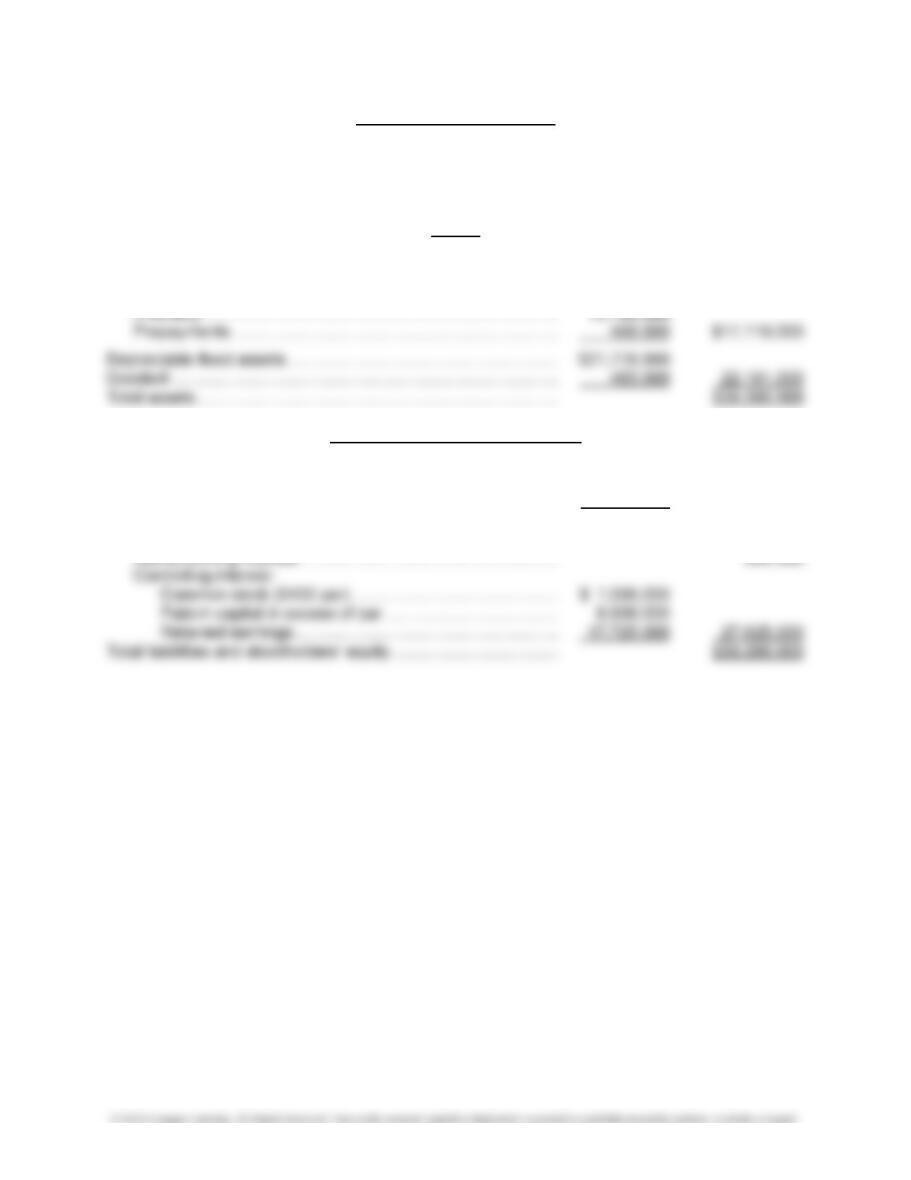

Problem 3B-2, Concluded

Todd Company and Subsidiary Keller Company

Consolidated Balance Sheet

December 31, 2016

Assets

Current assets:

Cash …………………………………………………………………………. $ 1,250,000

Accounts receivable ……………………………………………………. 2,700,000

Liabilities and Stockholders’ Equity

Payables ………………………………………………………………………… $ 8,950,000

Accruals …………………………………………………………………………. 2,015,000

Deferred tax liability …………………………………………………………. 210,000

Total liabilities …………………………………………………………………. $11,175,000

Stockholders’ equity:

PROBLEM 3B-3

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (90%) (10%)

Company fair value ……………………………………. $700,000 $630,000 $70,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………….. $700,000 $630,000 $ 70,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Building and equipment …………. $100,000 debit D1 10 $10,000

DTL on above adjustment ………. (30,000) credit D1t 10 (3,000)

Problem 3B-3, Continued

(2) Campton Corporation and Subsidiary Dorn Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Campton Dorn Dr. Cr. Statement NCI Earnings Sheet

Current Assets …………………………… 150,000 100,000 …………. ………… ………… ………… …………. 250,000

Land …………………………………………. 400,000 100,000 …………. ………… ………… ………… …………. 500,000

Current Tax Liability ……………………. (9,000) (12,000) …………. ………… ………… ………… …………. (21,000)

Deferred Tax Liability ………………….. (6,000) ………… (D2) 6,000 ………… ………… ………… …………. …………

Other Current Liabilities ………………. (130,000) (100,000) …………. ………… ………… ………… …………. (230,000)

Deferred Tax Liability ………………….. ………… ………… (A1t) 3,000 (D1t) 30,000 ………… ………… …………. (27,000)

Common Stock ($5 par)—

Campton ………………………………… (500,000) ………… …………. ………… ………… ………… …………. (500,000)

Expenses…………………………………… 89,000 50,000 (A1) 10,000 ………… 149,000 ………… ……….… …………

Provision for Tax ………………………… 15,000 12,000 …………. (A1t) 3,000 24,000 ………… …………. …………

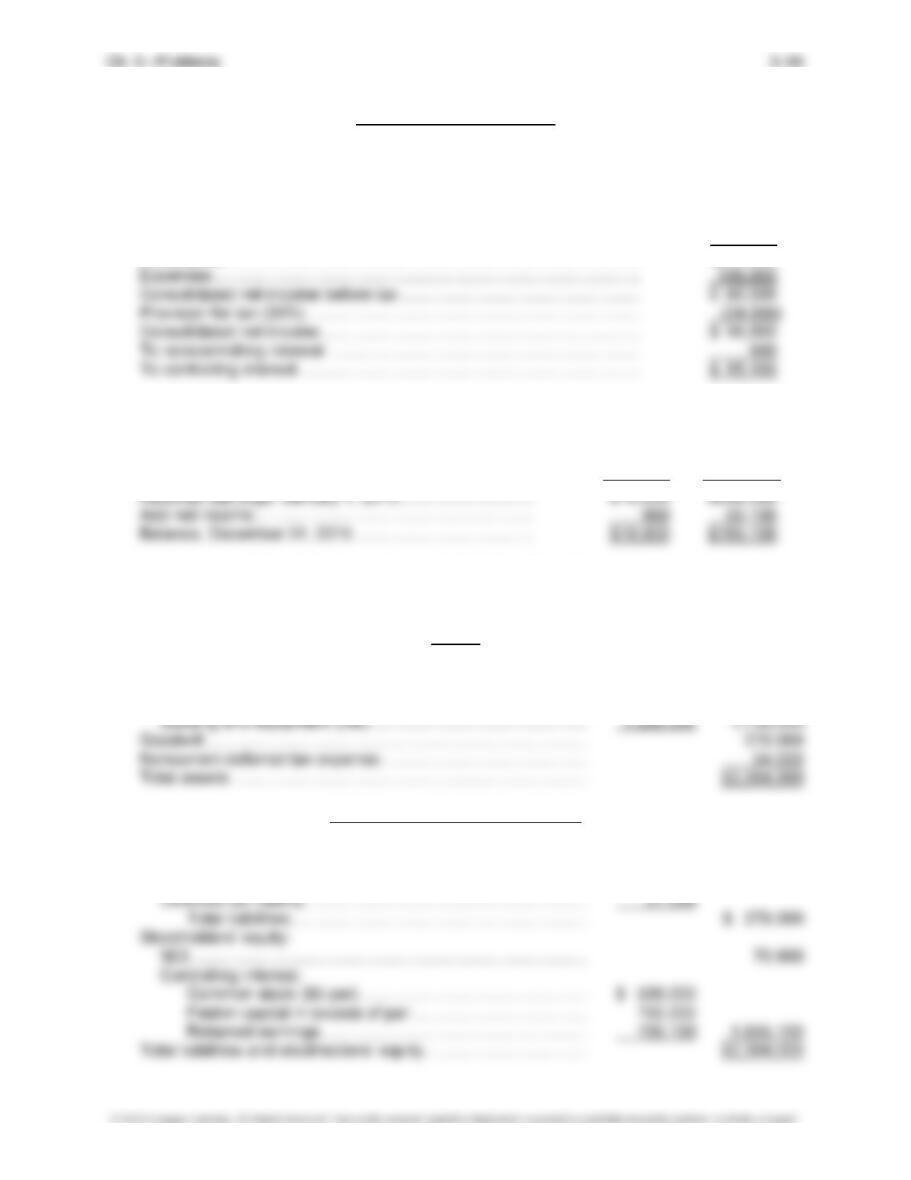

Total ………………………………………. 0 0 725,600 725,600 ………… ………… …………. …………

Consolidated Net Income ………………………………………………………………………………………….……… (56,000) ………… …………. …………

To NCI (see distribution schedule) ……………………………………………………………………………….… 900 (900) …………. …………

3-95 Ch. 3—Problems

Problem 3B-3, Continued

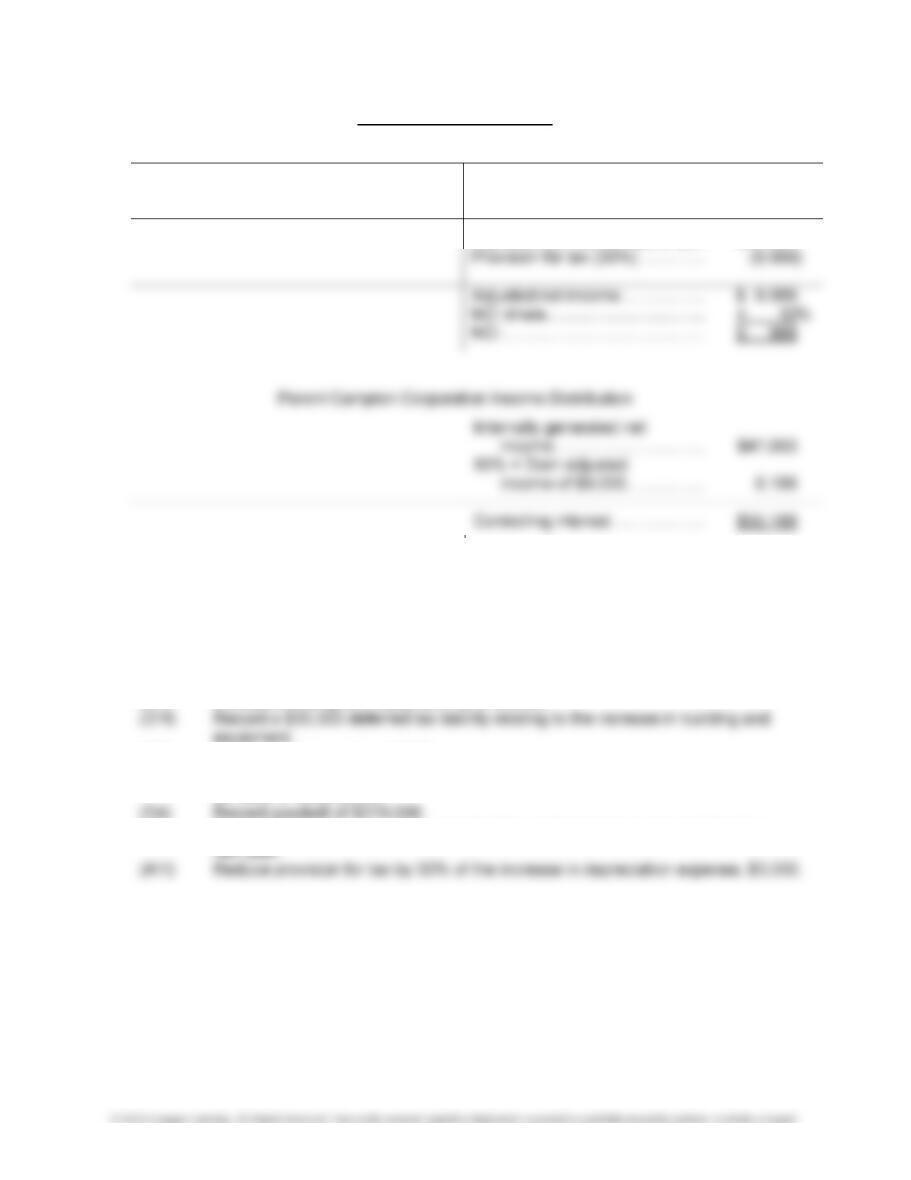

Subsidiary Dorn Corporation Income Distribution

Internally generated

Equipment depreciation …. (A1) $10,000 income before tax ……………. $40,000

Adjusted net income before tax . $30,000

Eliminations and Adjustments:

(CY1) Eliminate current-year investment entries.

(EL) Eliminate the 90% ownership portion of the subsidiary equity accounts against

the investment.

(D)/(NCI) Distribute the excess cost and NCI adjustment in accordance with the determina-

tion and distribution of excess schedule:

(D1) Increase building and equipment by $100,000.

(D2) Record current portion of DTA.

(D3) Record a noncurrent DTA of $54,000 for the portion of the tax loss carryover to

be used in future years.

(A1) Record $10,000 annual increase in building and equipment depreciation for cur-

Problem 3B-3, Concluded

(3) Campton Corporation and Subsidiary Dorn Corporation

Consolidated Income Statement

For Year Ended December 31, 2015

Sales ……………………………………………………………………………………….. $479,000

Cost of goods sold …………………………………………………………………….. 250,000

Gross profit ………………………………………………………………………………. $229,000

Campton Corporation and Subsidiary Dorn Corporation

Retained Earnings Statement

For Year Ended December 31, 2015

NCI

Controlling

Campton Corporation and Subsidiary Dorn Corporation

Consolidated Balance Sheet

December 31, 2015

Assets

Current assets ……………………………………………………………….. $ 250,000

Property, plant, and equipment:

Land …………………………………………………………………………. $ 500,000

Liabilities and Stockholders’ Equity

Liabilities:

Current liabilities …………………………………………………………. $ 230,000

Current tax liability ………………………………………………………. 21,000