CHAPTER 3

SOLUTONS TO PROBLEMS: SET B

PROBLEM 3-1B

1. Raw Materials Inventory ……………………………………… 25,000

Accounts Payable ……………………………………….. 25,000

3. Factory Labor …………………………………………………….. 25,770

Wages Payable ……………………………………………. 25,770

5. Manufacturing Overhead …………………………………….. 36,500

Accounts Payable ……………………………………….. 36,500

6. Work in Process—Blending (900 X $28) ………………. 25,200

Work in Process—Packaging (300 X $28) …………….. 8,400

Manufacturing Overhead ……………………………… 33,600

8. Finished Goods Inventory …………………………………… 67,490

Work in Process—Packaging ……………………….. 67,490

Cost of Goods Sold ……………………………………………. 62,000

Finished Goods Inventory ……………………………. 62,000

PROBLEM 3-2B

(a)

Physical units

Units to be accounted for

Work in process, January 1

Started into production

Total units

0

50,000

50,000

(b)

Equivalent units

Materials

Conversion Costs

Units transferred out

Work in process, January 31

47,500

47,500

(c)

Unit Costs

(d) Costs accounted for

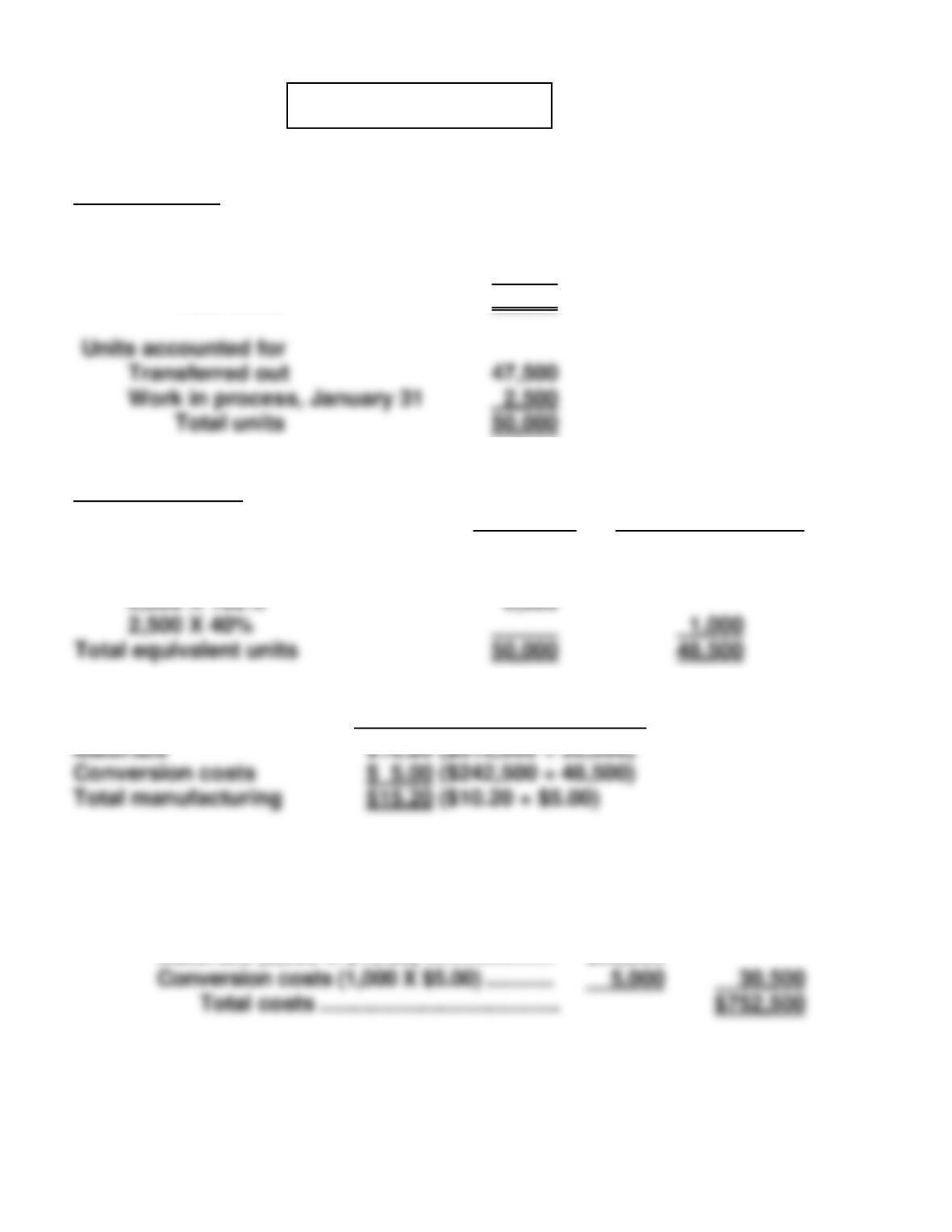

Transferred out (47,500 X $15.20) ……………… $722,000

Work in process, January 31

Materials (2,500 X $10.20) ………………… $25,500

Total units

50,000

PROBLEM 3-2B (Continued)

(e) STEINER CORPORATION

Molding Department

Production Cost Report

For the Month Ended January 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, January 1

Started into production

Total units

0

50,000

50,000

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Work in process, January 1

Total costs

Unit costs (Step 3)

Total cost

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$510,000

50,000

$10.20

$242,500

48,500

$5.00

$752,500

$15.20

Cost Reconciliation Schedule (Step 4)

Total costs

Costs accounted for

Transferred out (47,500 X $15.20)

$722,000

Units accounted for

Transferred out

Work in process, January 31

(2,500 X 40%)

Total units

PROBLEM 3-3B

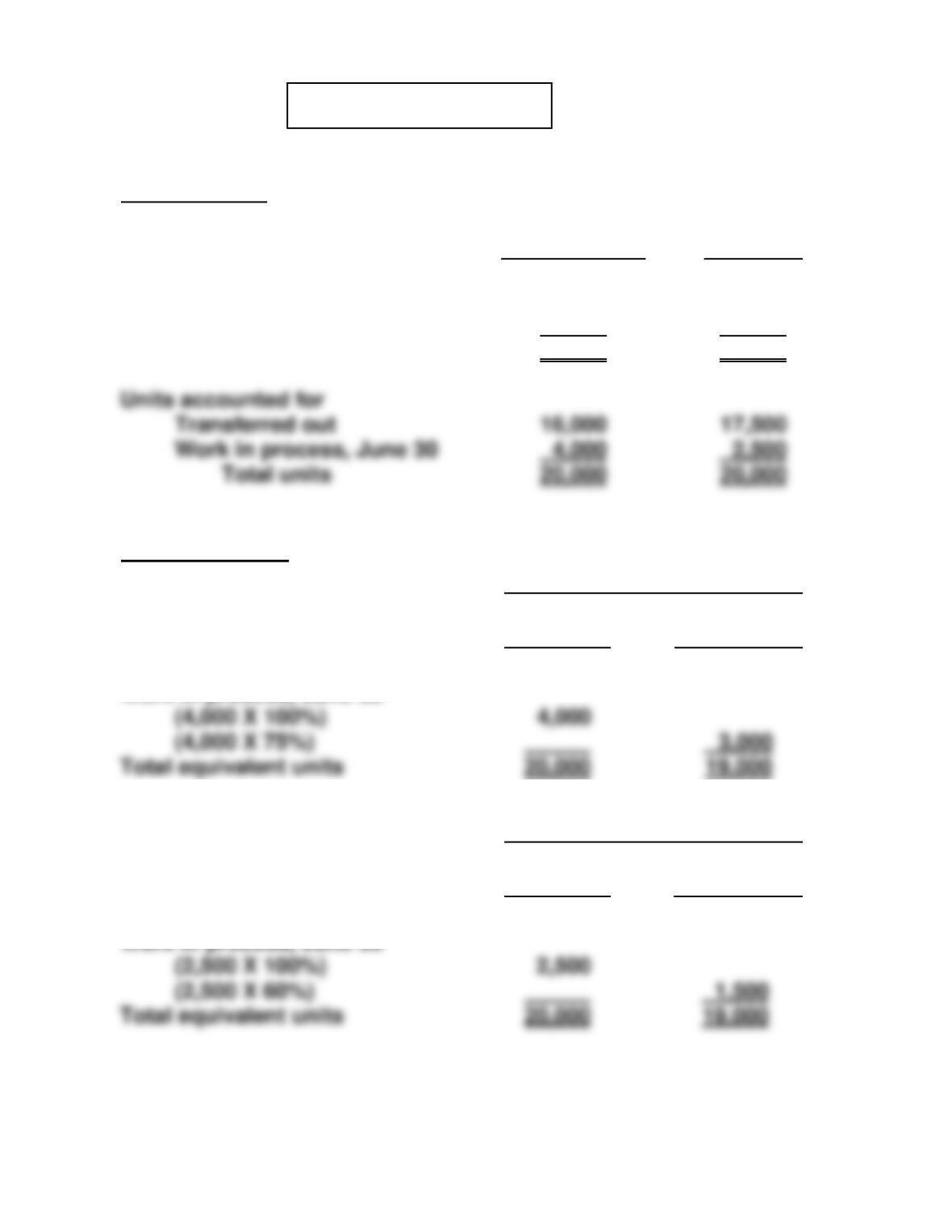

(a) (1) Physical units

R12

Refrigerators

F24

Freezers

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

20,000

20,000

0

20,000

20,000

(2) Equivalent units

R12 Refrigerators

Materials

Conversion

Costs

Units transferred out

Work in process, June 30

16,000

16,000

F24 Freezers

Materials

Conversion

Costs

Work in process, June 30

Units transferred out

17,500

17,500

Units accounted for

PROBLEM 3-3B (Continued)

(3) Unit costs

R12

Refrigerators

F24

Freezers

Materials ($840,000 ÷ 20,000)

($720,000 ÷ 20,000)

Conversion costs ($665,000(a) ÷ 19,000)

$42

35

$36

(4) R12 Refrigerators

Costs accounted for

Transferred out (16,000 X $77) …………. $1,232,000

Work in process

F24 Freezers

Costs accounted for

Transferred out (17,500 X $65) ………….. $1,137,500

Work in process

PROBLEM 3-3B (Continued)

(b) BORMAN CORPORATION

Stamping Department—Plant A

Production Cost Report

For the Month Ended June 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

20,000

20,000

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Work in process, June 1

Total costs

Unit costs (Step 3)

Total cost

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$840,000

20,000

$ 42

$665,000

19,000

$ 35

$1,505,000

$ 77

Cost Reconciliation Schedule (Step 4)

Materials (4,000 X $42)

Total costs

Costs accounted for

Transferred out (16,000 X $77)

Work in process, June 30

$1,232,000

Units accounted for

Transferred out

Work in process, June 30

Total units

PROBLEM 3-4B

(a)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

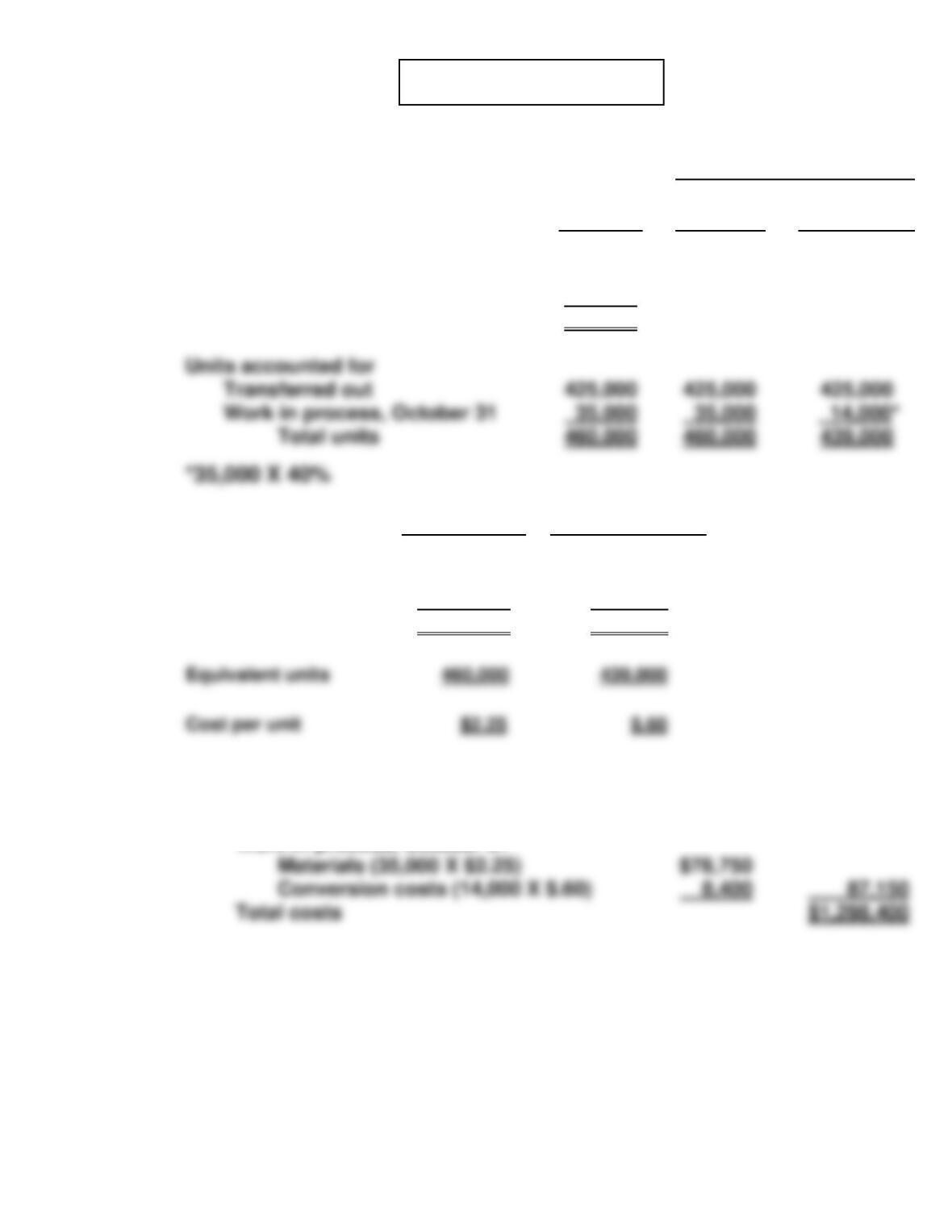

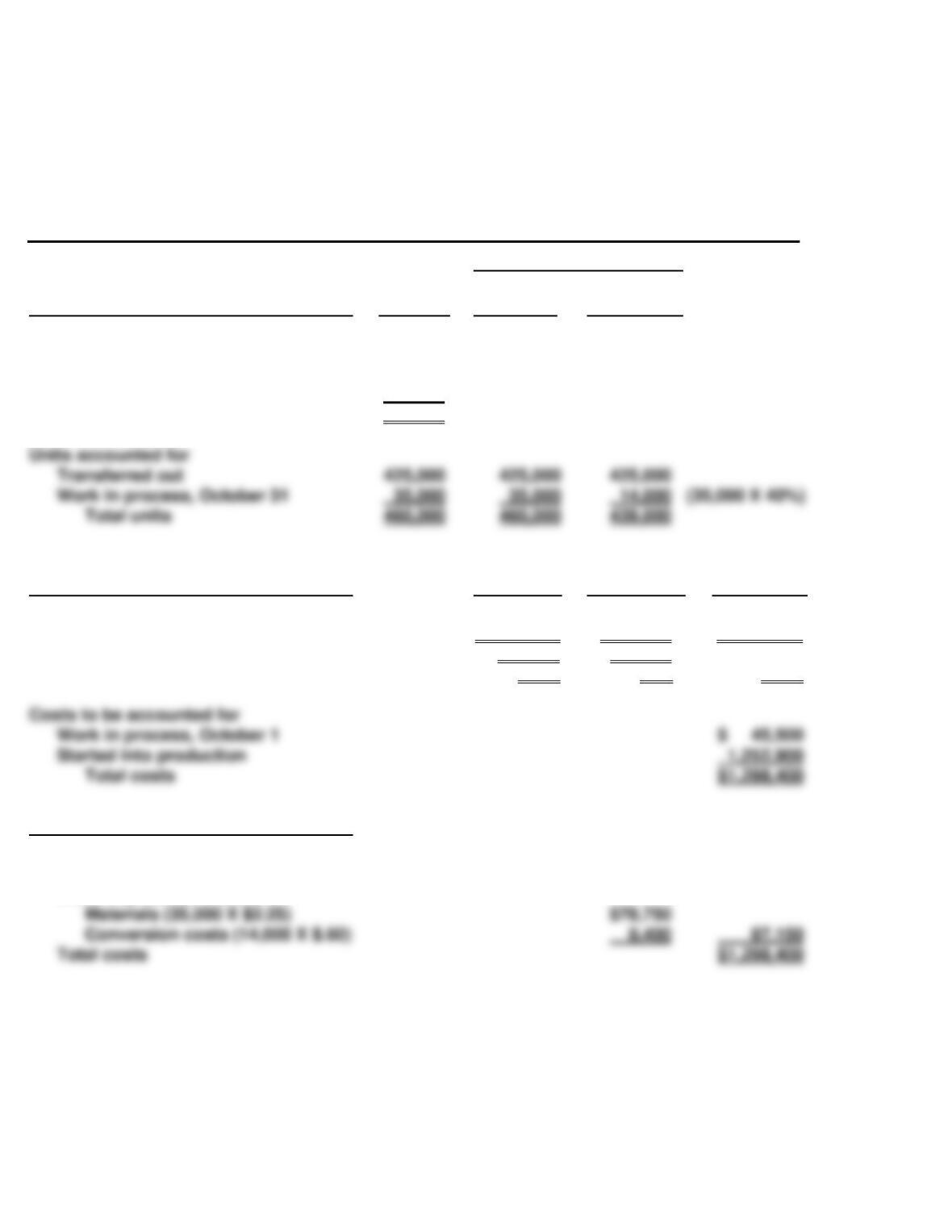

Units to be accounted for

Work in process, October 1

Started into production

Total units

25,000

435,000

460,000

Beginning work in

process

Added during month

Total

Materials cost

$ 29,000

1,006,000

$1,035,000

Conversion costs

$ 16,500

246,900

$263,400

($138,900 + $108,000)

(b)

Total costs

Costs accounted for

Transferred out (425,000 X $2.85)

Work in process, October 31

$1,211,250

Total units

35,000

460,000

PROBLEM 3-4B (Continued)

(c) LUXMAN COMPANY

Assembly Department

Production Cost Report

For the Month Ended October 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, October 1

Started into production

Total units

25,000

435,000

460,000

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Work in process, October 1

Total costs

Unit costs (Step 3)

Total cost

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$1,035,000

460,000

$2.25

$263,400

439,000

$.60

$1,298,400

$2.85

Cost Reconciliation Schedule (Step 4)

Materials (35,000 X $2.25)

Total costs

$1,298,400

Costs accounted for

Transferred out (425,000 X $2.85)

Work in process, October 31

$1,211,250

Units accounted for

Transferred out

Work in process, October 31

Total units

460,000

460,000

PROBLEM 3-5B

(a)

(1)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, May 1

Started into production

Total units

500

2,000

2,500

(2)

Materials cost

Conversion costs

Cost per unit

Beginning work in

process

Added during month

Total

$15,000

50,000

$65,000

$18,000

52,700

$70,700

($19,020 + $33,680)

(3)

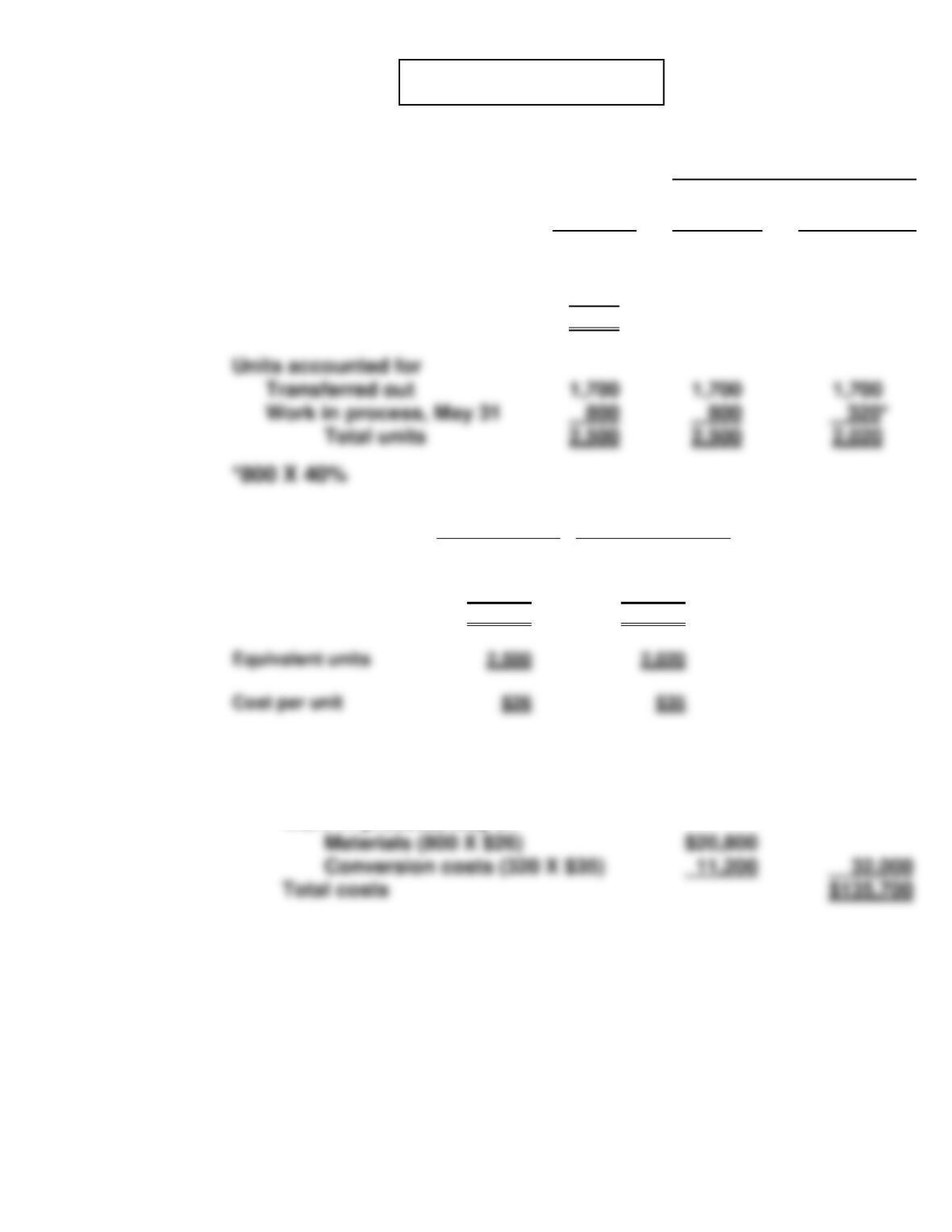

Costs accounted for

Transferred out (1,700 X $61)

Work in process, May 31

$103,700

PROBLEM 3-5B (Continued)

(b) SWINN COMPANY

Bicycle Department

Production Cost Report

For the Month Ended May 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

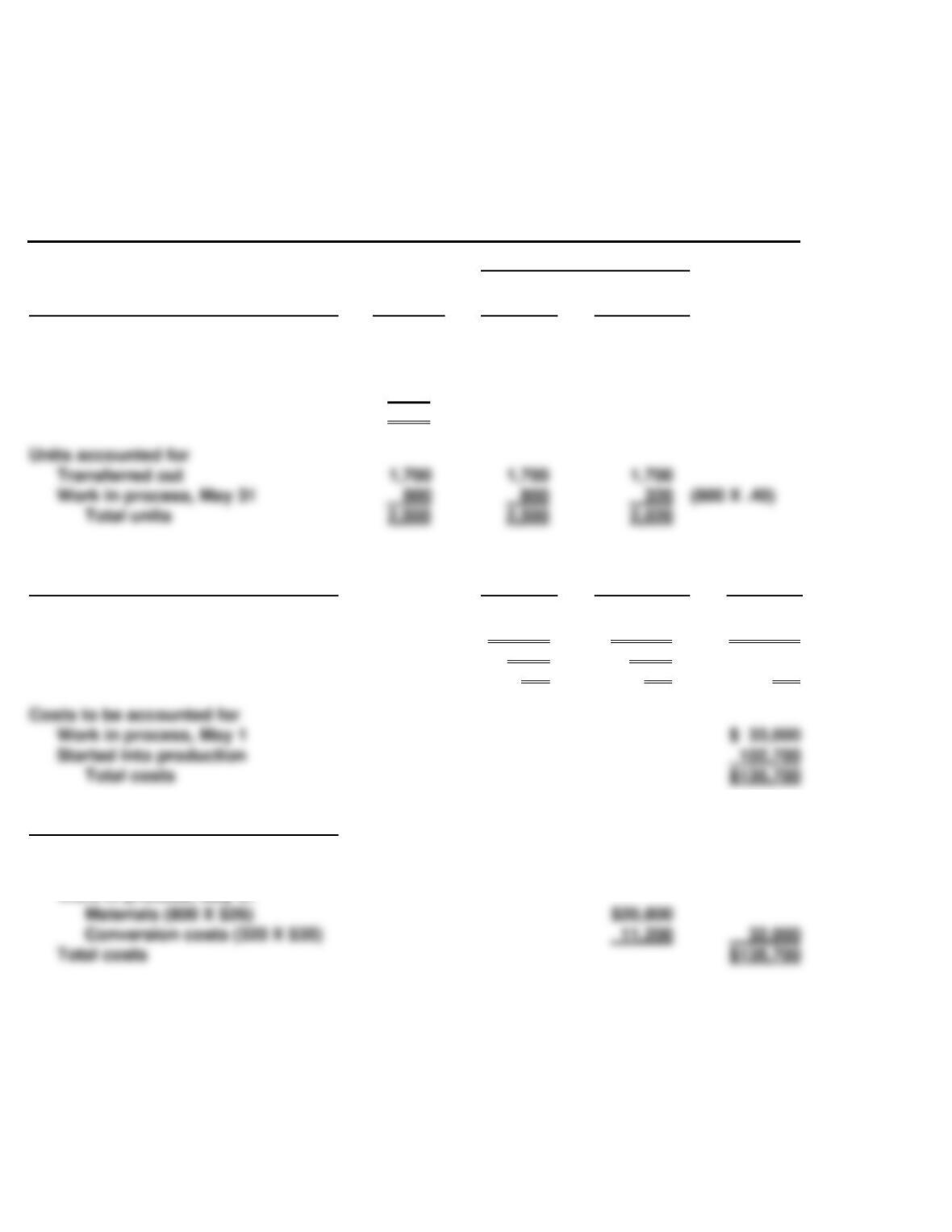

Units to be accounted for

Work in process, May 1

Started into production

Total units

500

2,000

2,500

Costs

Materials

Conversion

Costs

Total

Costs to be accounted for

Total costs

Unit costs (Step 3)

Total cost

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$65,000

2,500

$26

$70,700

2,020

$35

$135,700

$61

Cost Reconciliation Schedule (Step 4)

Total costs

Costs accounted for

Transferred out (1,700 X $61)

Work in process, May 31

$103,700

Units accounted for

Transferred out

1,700

Work in process, May 31

(800 X .40)

Total units

2,500

2,500

PROBLEM 3-6B

(a) Computation of equivalent units:

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units accounted for

Transferred out

Work in process, March 31

66,000

66,000

66,000

Computation of March unit costs

(b) Cost Reconciliation Schedule

Costs accounted for

Transferred out (66,000 X $3.40)……………….. $224,400

Work in process, March 31

*PROBLEM 3-7B

(a) Basketballs

(1) Equivalent units—Materials

Physical

Units

Materials

Added

This Period

Equivalent

Units

Work in process, August 1

Started and completed

Work in process, August 31

Total

500

1,400

600

2,500

(2,000 – 600)

* 0%*

100%

100%

0

1,400

600

2,000

(2) Unit costs

Materials

Conversion

Costs in August (a)

$1,600

**$2,280**

Units

Conversion

This Period

Units

Work in process, August 1

500

Started and completed

Total

2,500

(2,000 – 600)

1,900

*PROBLEM 3-7B (Continued)

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

***$5,005***

Work in process, August 1

Conversion

200

1.20

$1,125

240

Soccer balls

(1) Equivalent units—Materials

Physical

Units

Materials

Added

This Period

Equivalent

Units

Total

2,200

2,000

Work in process, August 1

Started and completed

200

1,850

(2,000 – 150)

* 0%*

100%

0

1,850

Equivalent units—Conversion

Physical

Units

Conversion

Added

This Period

Equivalent

Units

Work in process, August 1

200

20% (1 – .8) 40

Started and completed

Total

1,850

150

2,200

(2,000 – 150)

1,995

Started and completed

Total costs transferred out

2.00

2,800

$4,165

Total costs

$5,005

*PROBLEM 3-7B (Continued)

(2) Unit costs

Materials

Conversion

Costs in August (a)

$2,800

$2,394**

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Total mfg. costs

Transferred out

***$5,644***

Work in process, August 31

Conversion costs

Total costs

Work in process, August 1

Conversion

40

$1.20

$ 450

48

*PROBLEM 3-7B (Continued)

(b) HOLIDAY COMPANY

Production Cost Report—Basketballs

For the Month Ended August 31

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

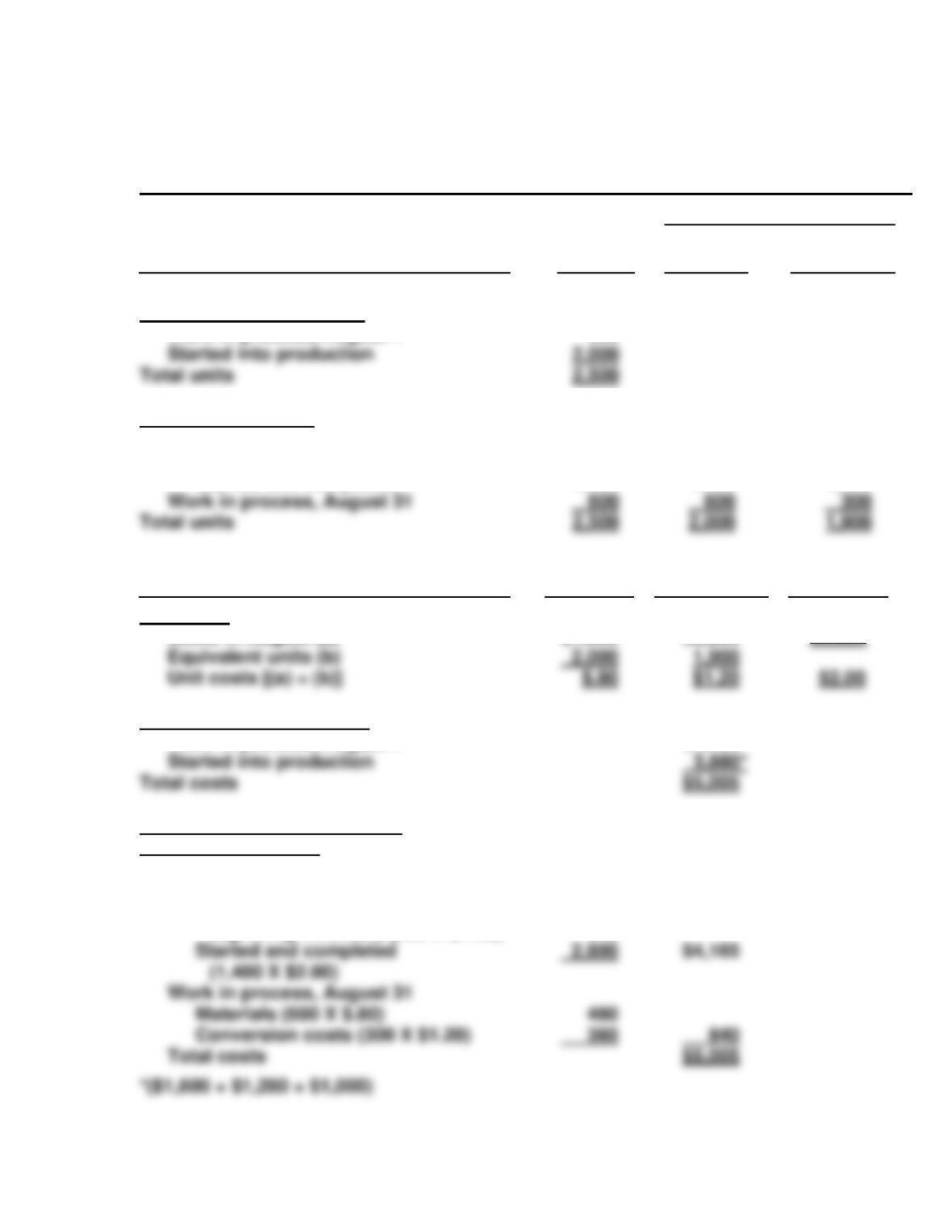

Started into production

Units to be accounted for

Work in process, August 1

Units accounted for

Completed and transferred out

Work in process, August 1

Started and completed

500

500

1,400

0

1,400

200

1,400

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Costs in August (a)

Costs to be accounted for

Work in process, August 1

Cost Reconciliation Schedule

Costs accounted for

Transferred out

Work in process, August 1

Conversion costs to complete

beginning inventory (200 X $1.20)

$1,600

$1,125

240

$2,280

$1,125

$3,880

(1,400 X $2.00)

Materials (600 X $.80)