Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 3 The Adjusting Process

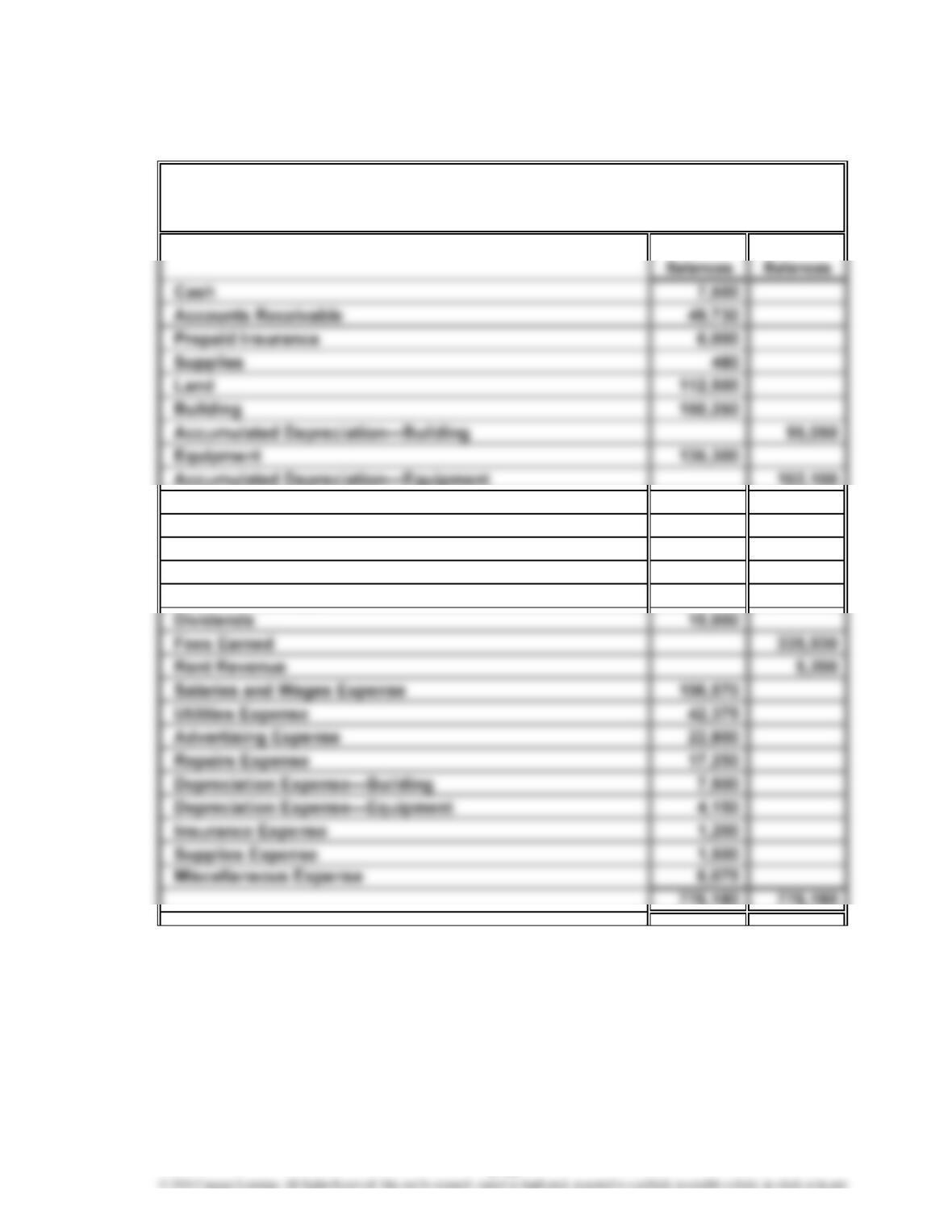

Prob. 3–5A (Concluded)

2.

Debit Credit

Accounts Payable 12,150

Unearned Rent 1,550

Salaries and Wages Payable 3,200

Common Stock 75,000

Retained Earnings 146,000

August 31, 2016

ROWLAND COMPANY

Adjusted Trial Balance

3-19

CHAPTER 3 The Adjusting Process

Prob. 3–6A

1. a. Supplies Expense

Supplies 2,750

Supplies used.

2. Total

Net Total Stockholders'

Income Assets = + Equity

Total

Liabilities

2,750

3-20

CHAPTER 3 The Adjusting Process

Prob. 3–1B

1. a. Accounts Receivable 19,750

Fees Earned 19,750

Accrued fees earned.

b. Supplies Expense 8,150

2. Adjusting entries are a planned part of the accounting process to update the

3-21

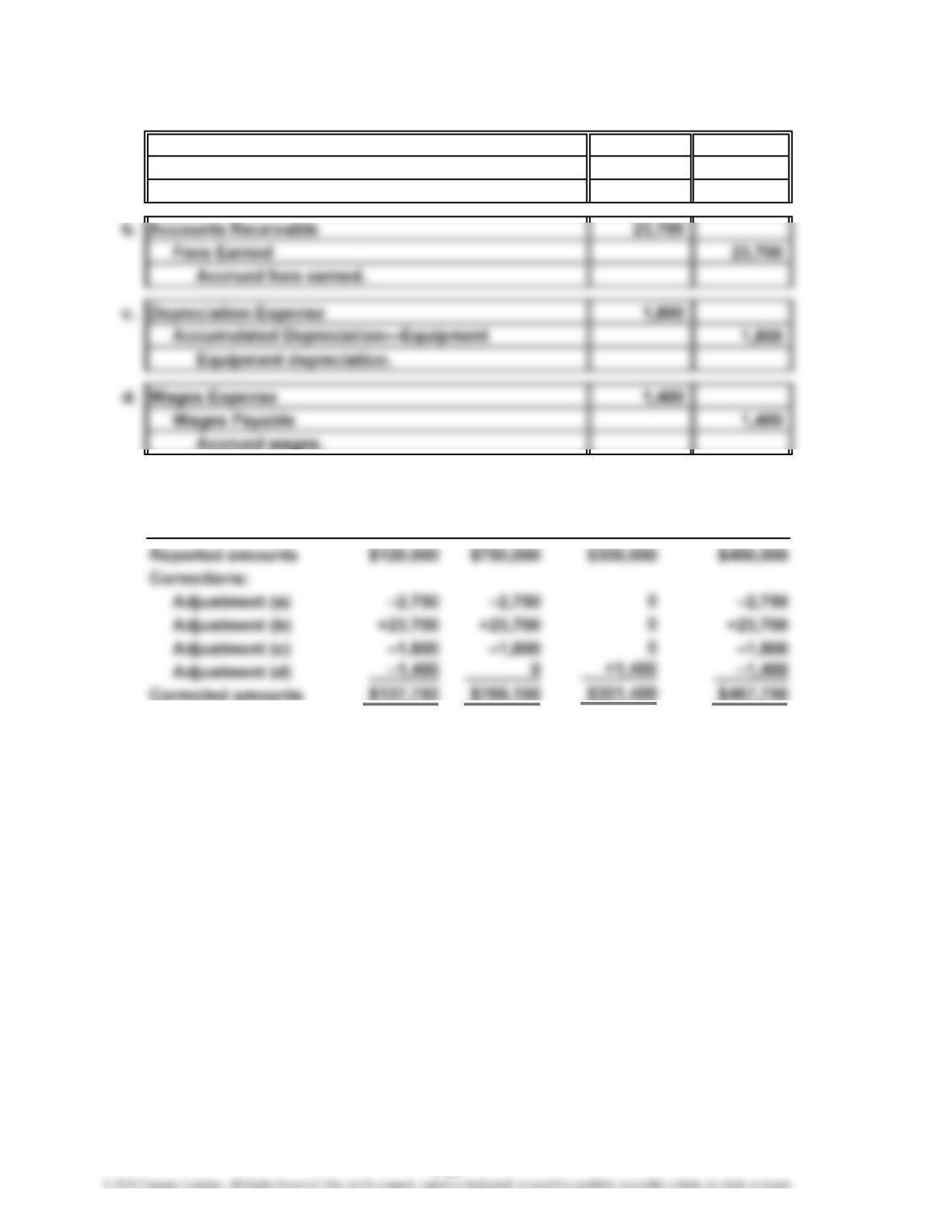

CHAPTER 3 The Adjusting Process

Prob. 3–2B

1. a. Supplies Expense 2,620

Supplies 2,620

Supplies used ($3,170 – $550).

b. Depreciation Expense 1,675

2. Fees Earned would be understated by $6,000; Depreciation Expense would

3. Accumulated Depreciation—Equipment would be understated by $1,675; total

assets would be overstated by $1,675; Unearned Fees would be overstated by

4. There is no effect on the “Net increase or decrease in cash” on the statement

of cash flows because adjusting entries do not affect cash.

3-22

CHAPTER 3 The Adjusting Process

Prob. 3–3B

1. a. Supplies Expense 5,820

Supplies 5,820

Supplies used ($7,200 – $1,380).

b. Accounts Receivable 3,900

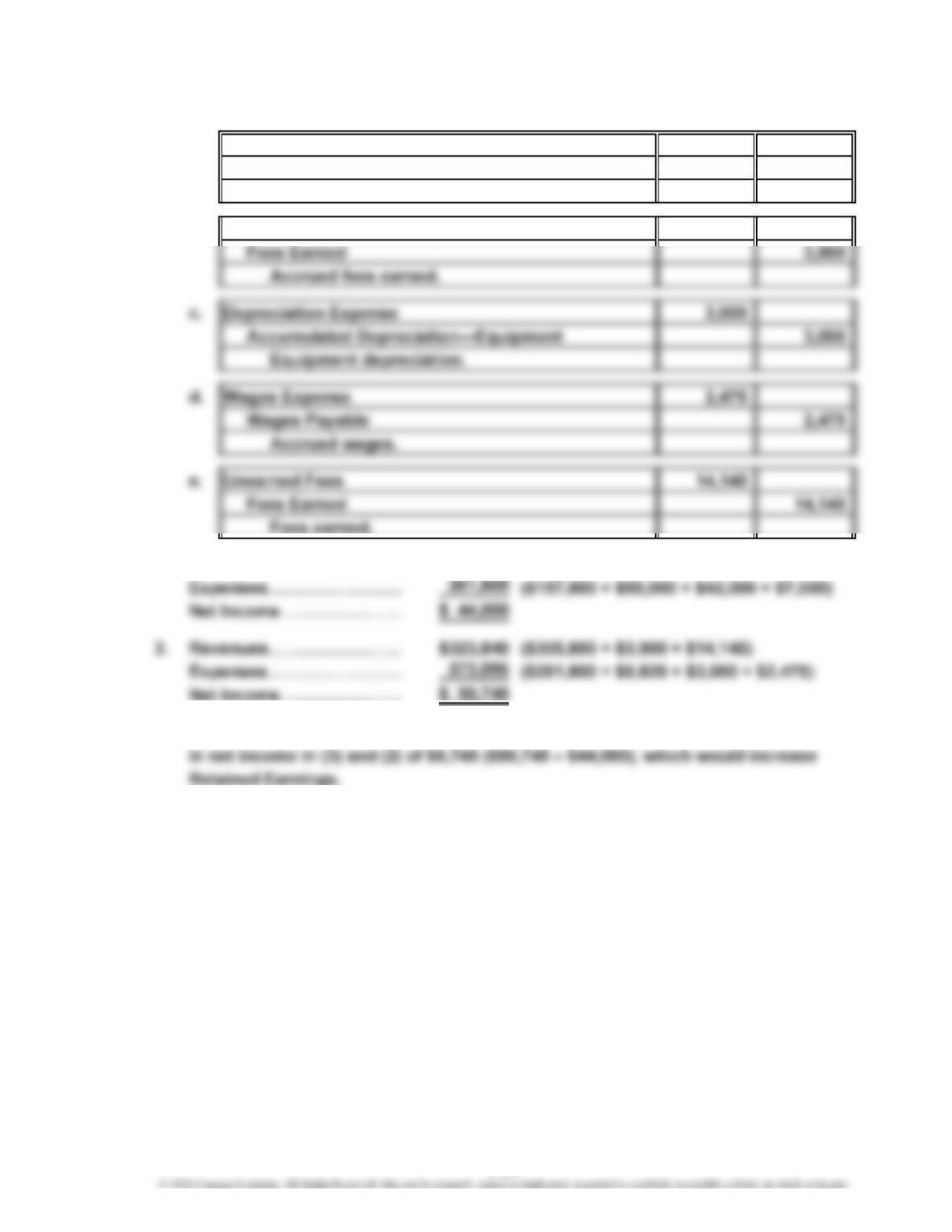

2. Revenues…………………

…

$305,800

…

4. The effect of the adjusting entries on Retained Earnings is the difference

3-23

CHAPTER 3 The Adjusting Process

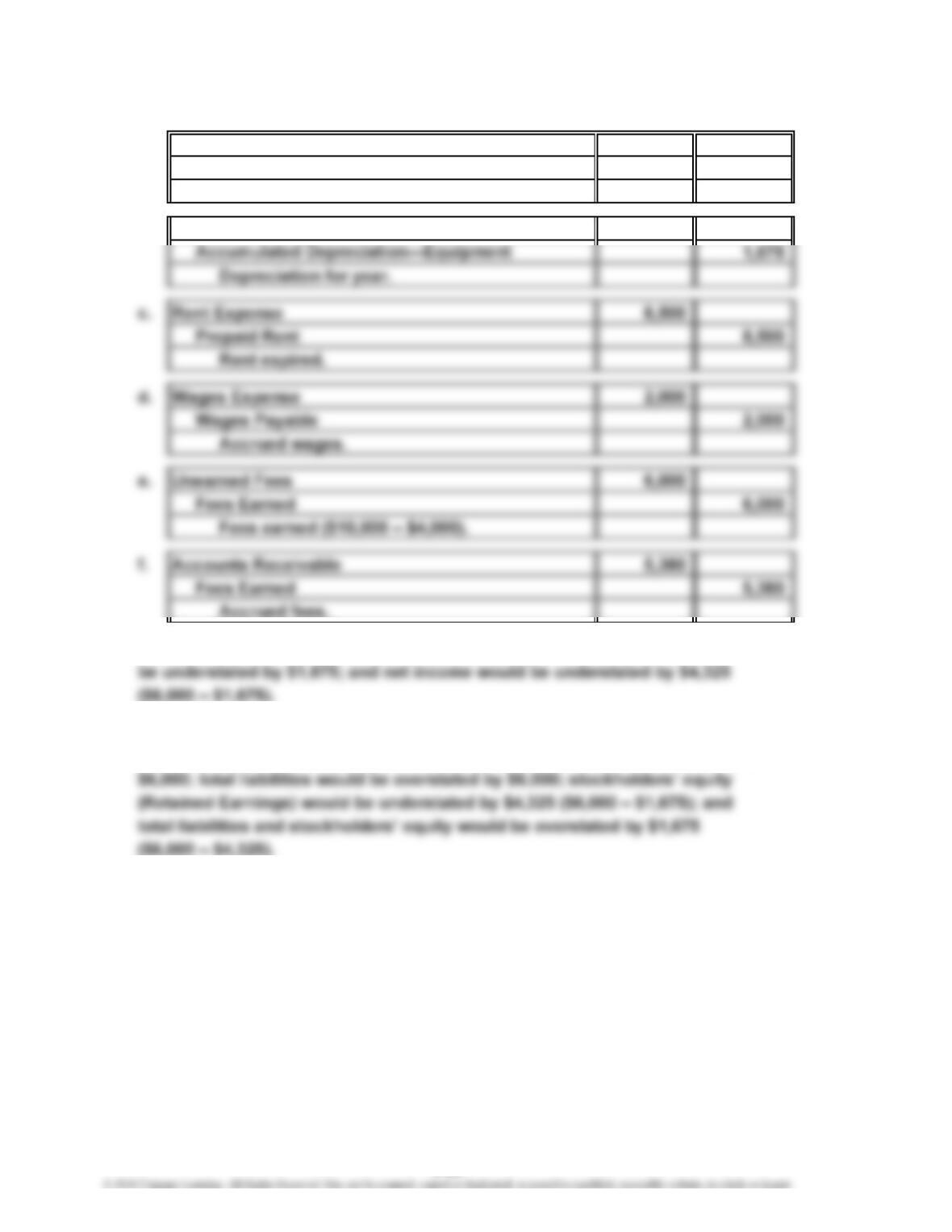

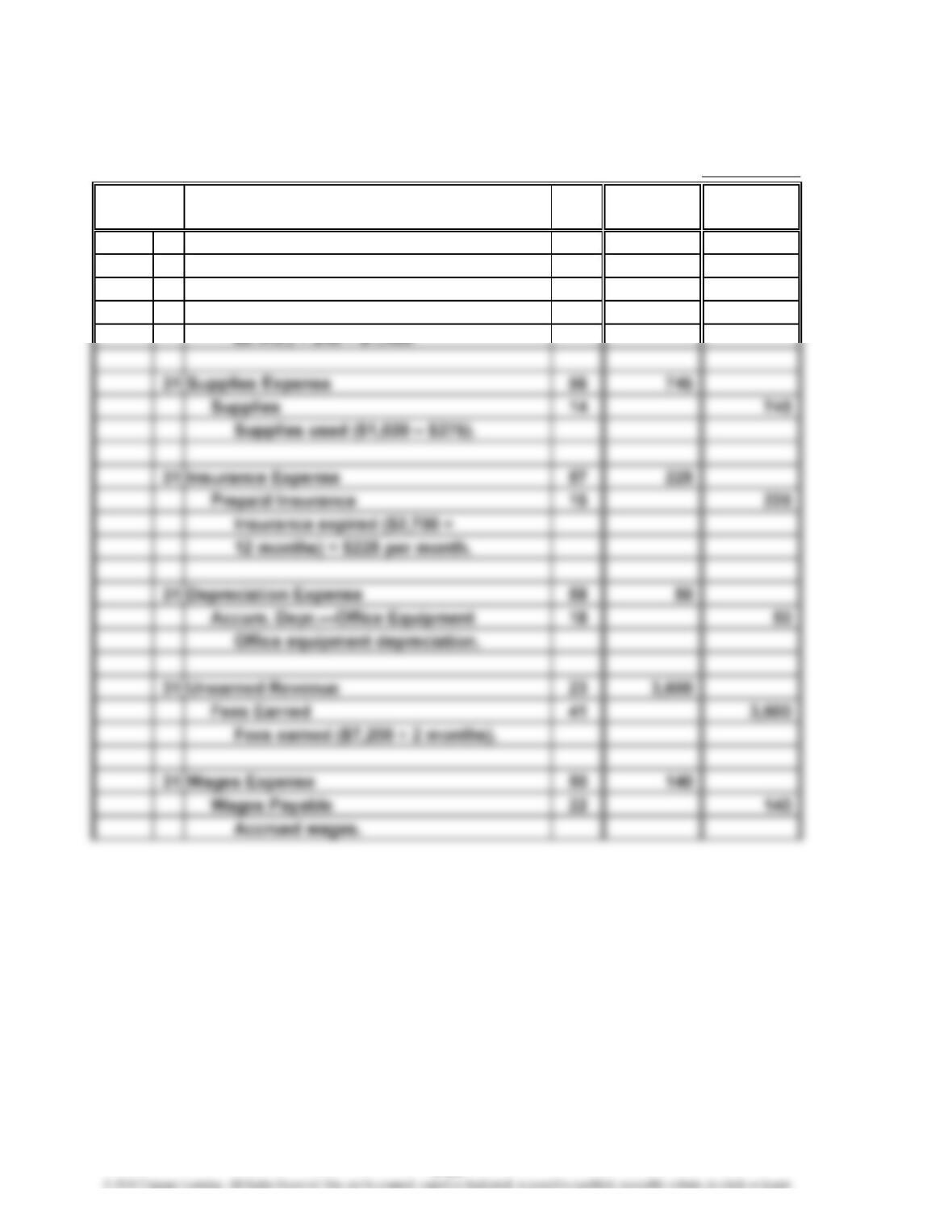

Prob. 3–4B

2016

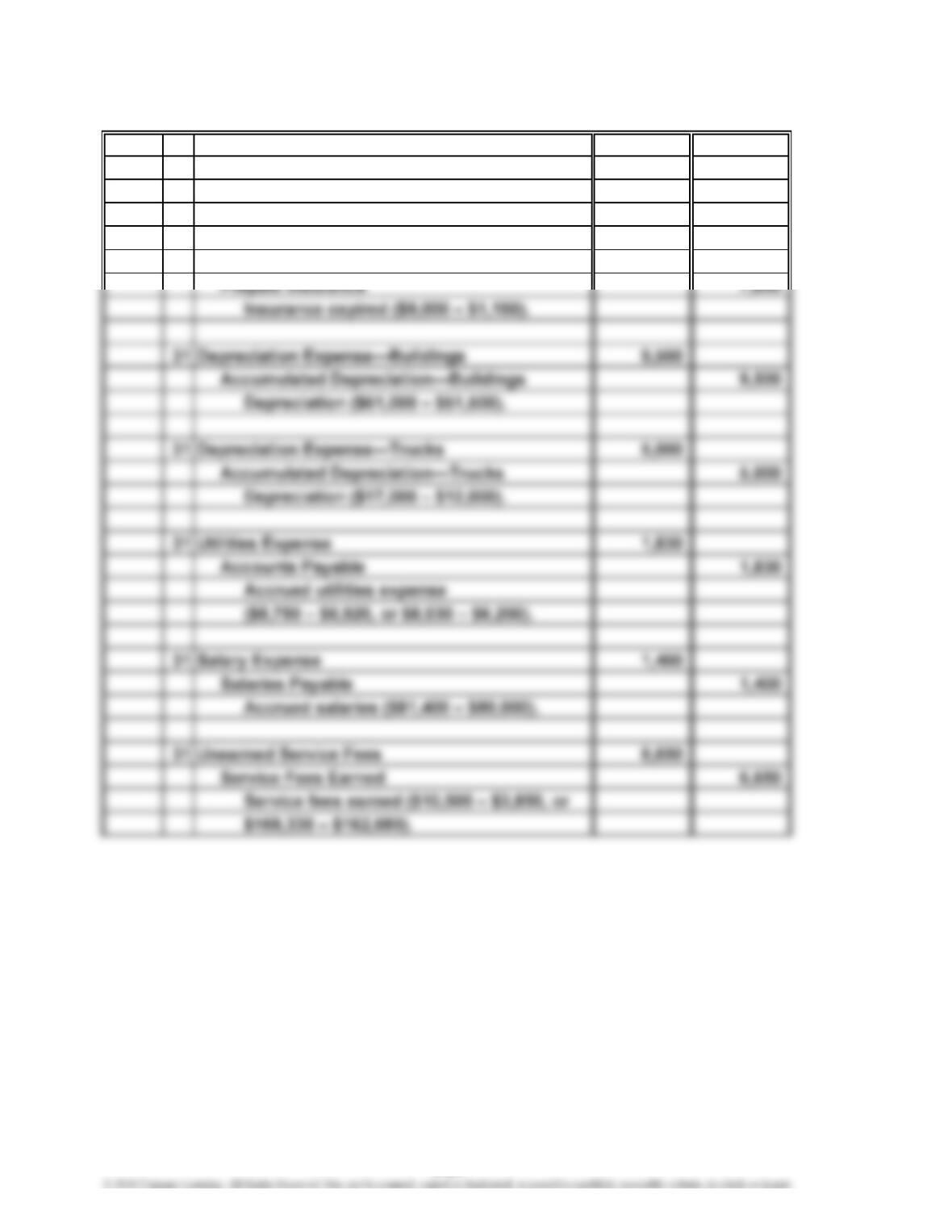

Mar. 31 Supplies Expense 4,025

Supplies 4,025

Supplies used ($6,200 – $2,175).

31 Insurance Expense 7,850

3-24

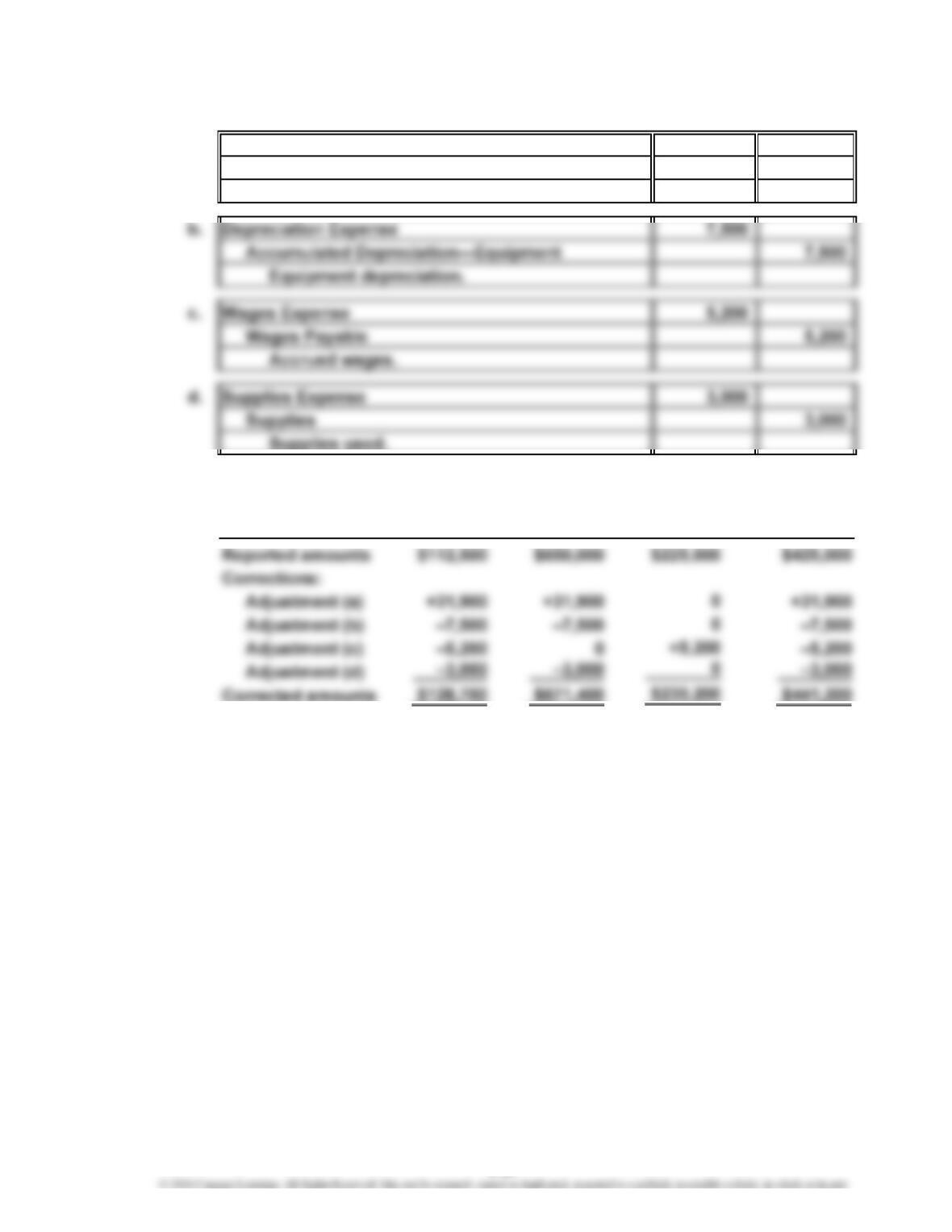

CHAPTER 3 The Adjusting Process

Prob. 3–5B

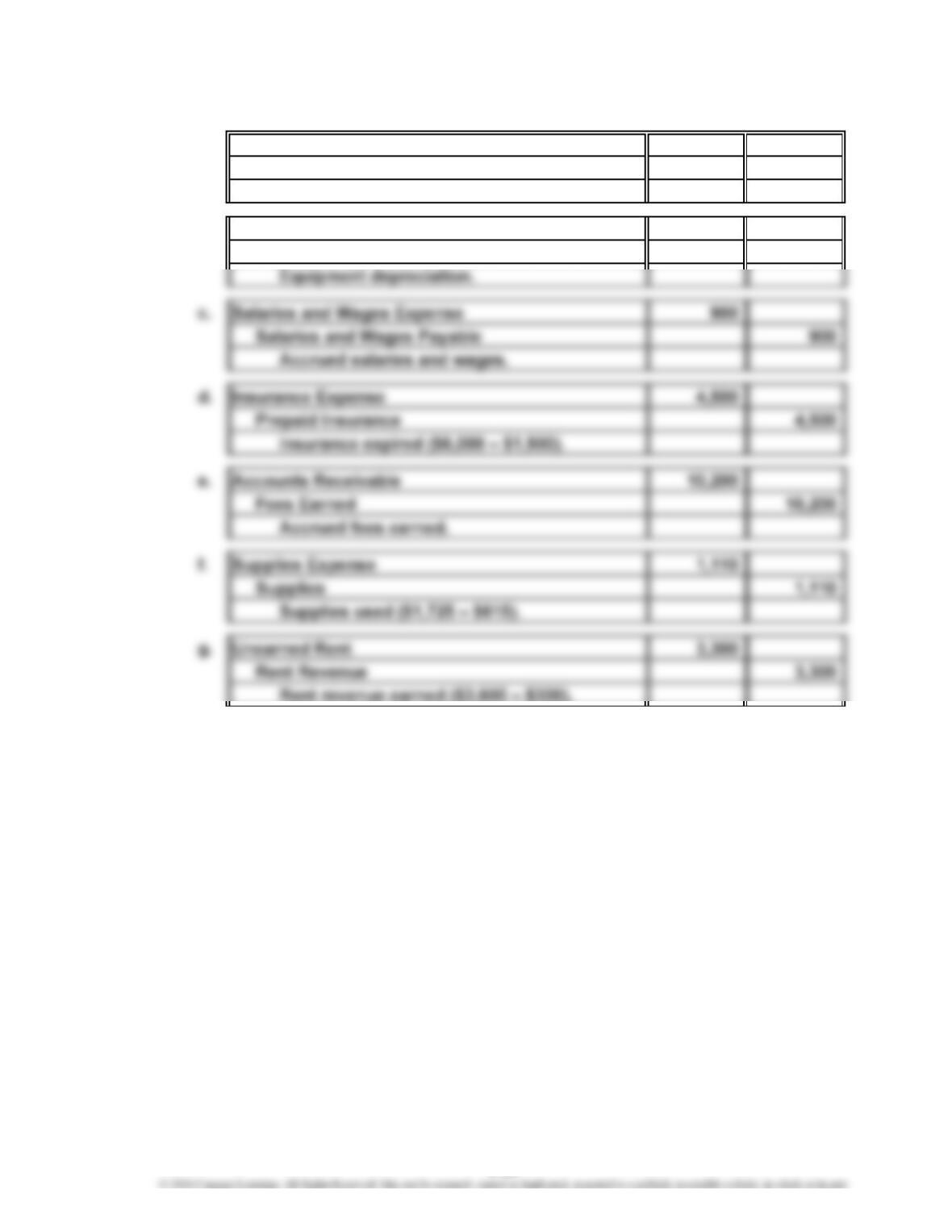

1. a. Depreciation Expense—Building 6,400

Accumulated Depreciation—Building 6,400

Building depreciation.

b. Depreciation Expense—Equipment 2,800

Accumulated Depreciation—Equipment 2,800

3-25

CHAPTER 3 The Adjusting Process

Prob. 3–5B (Concluded)

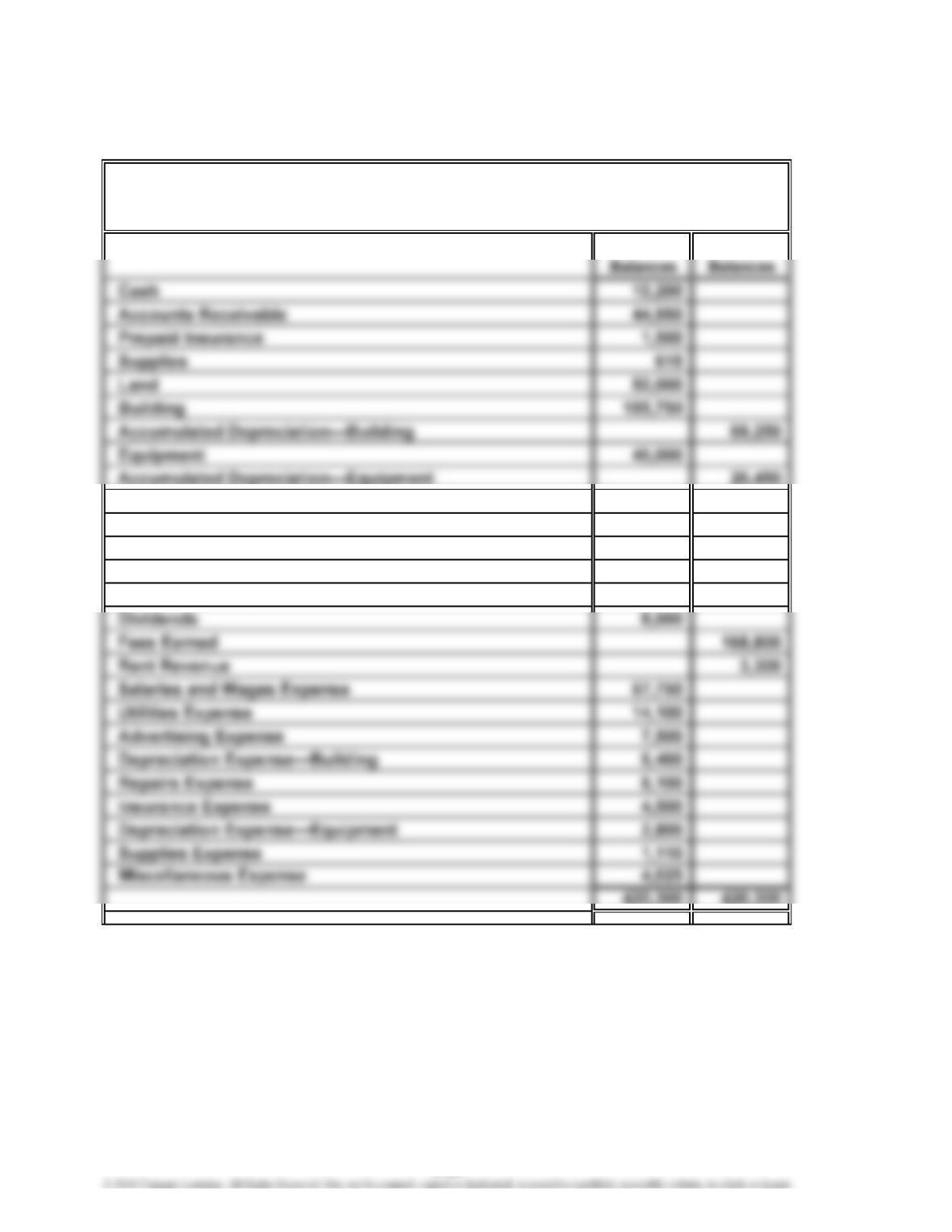

2.

Debit Credit

Accounts Payable 3,750

Unearned Rent 300

Salaries and Wages Payable 900

Common Stock 60,000

Retained Earnings 93,550

July 31, 2016

REECE FINANCIAL SERVICES CO.

Adjusted Trial Balance

3-26

CHAPTER 3 The Adjusting Process

Prob. 3–6B

1. a. Accounts Receivable

Fees Earned 31,900

Accrued fees earned.

2. Total

Net Total Stockholders'

Income Assets = + Equity

Total

Liabilities

31,900

3-27

CHAPTER 3 The Adjusting Process

1.

Page 3

Post.

Ref. Debit Credit

2016

July 31 Accounts Receivable 12 1,400

Fees Earned 41 1,400

Accrued fees earned (115 hrs. –

CONTINUING PROBLEM

Date

JOURNAL

Adjusting Entries

Description

3-28

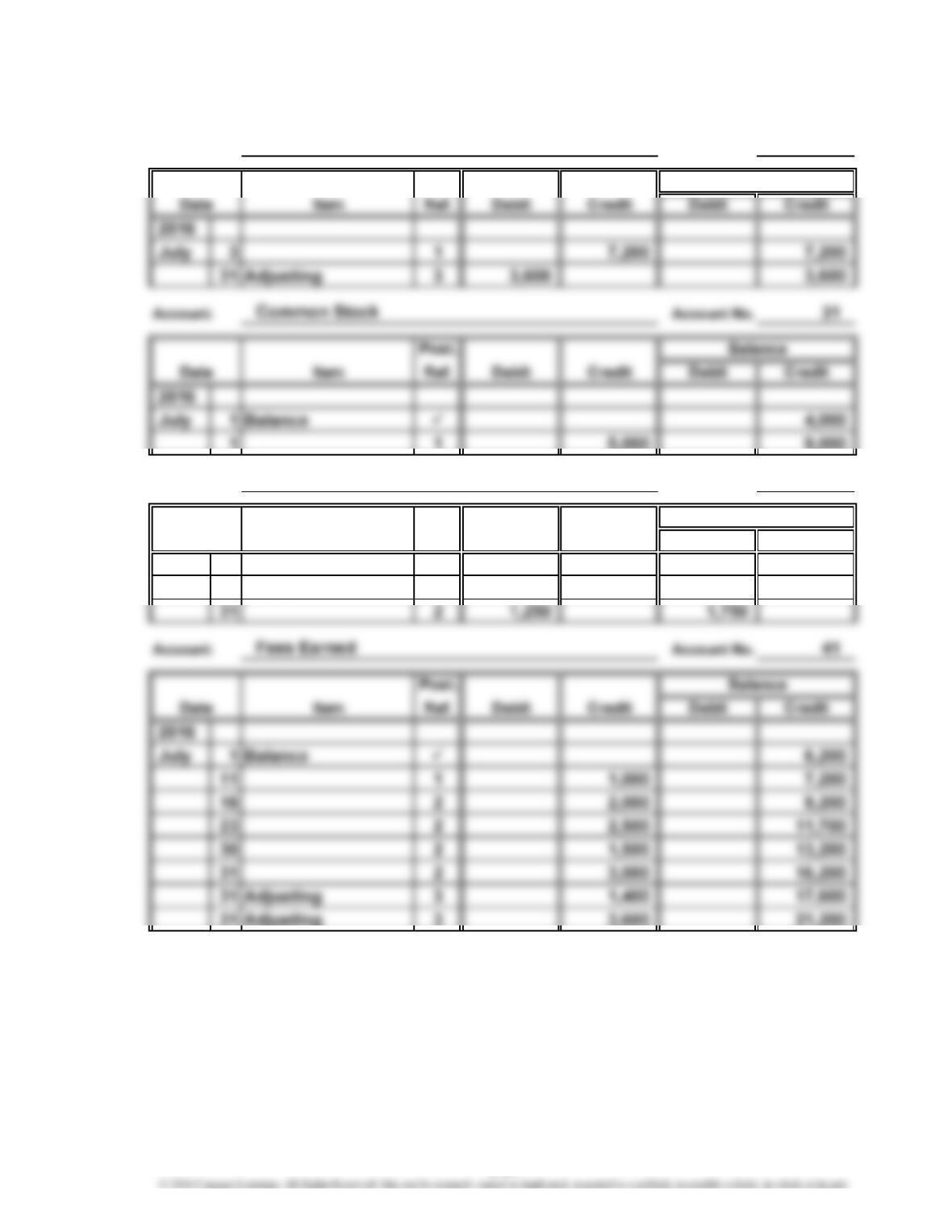

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

2.

Account No. 11

Post.

Item Ref. Debit Debit Credit

2016

13 1 11,620

14 1 10,420

16 2 2,000 12,420

21 2 11,800

22 2 11,000

Item Ref. Debit Debit Credit

2016

July 1 Balance 1,000

21 ——

23 2 1,750 1,750

Account: Cash

Balance

CreditDate

700

1,200

620

800

Date Credit

1,000

3-29

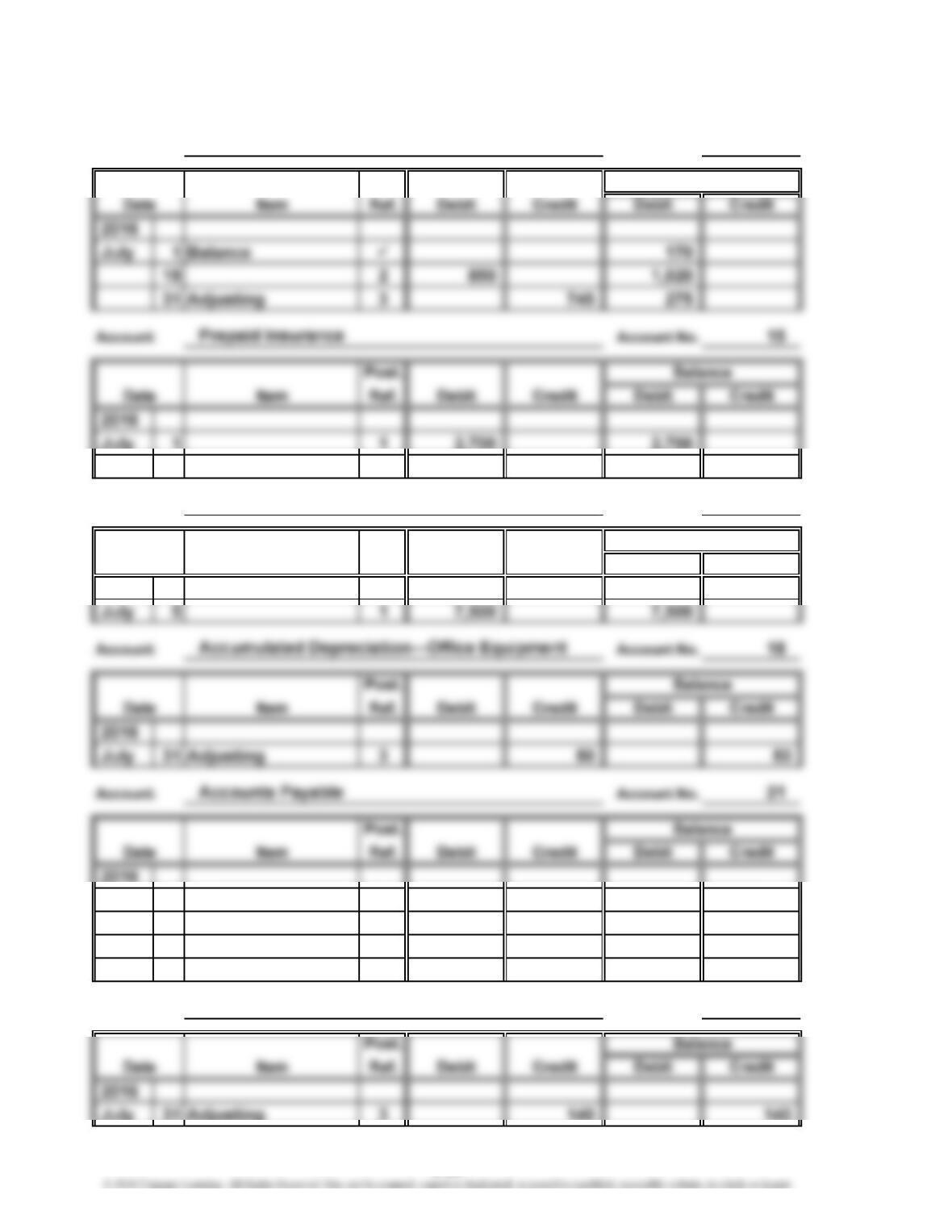

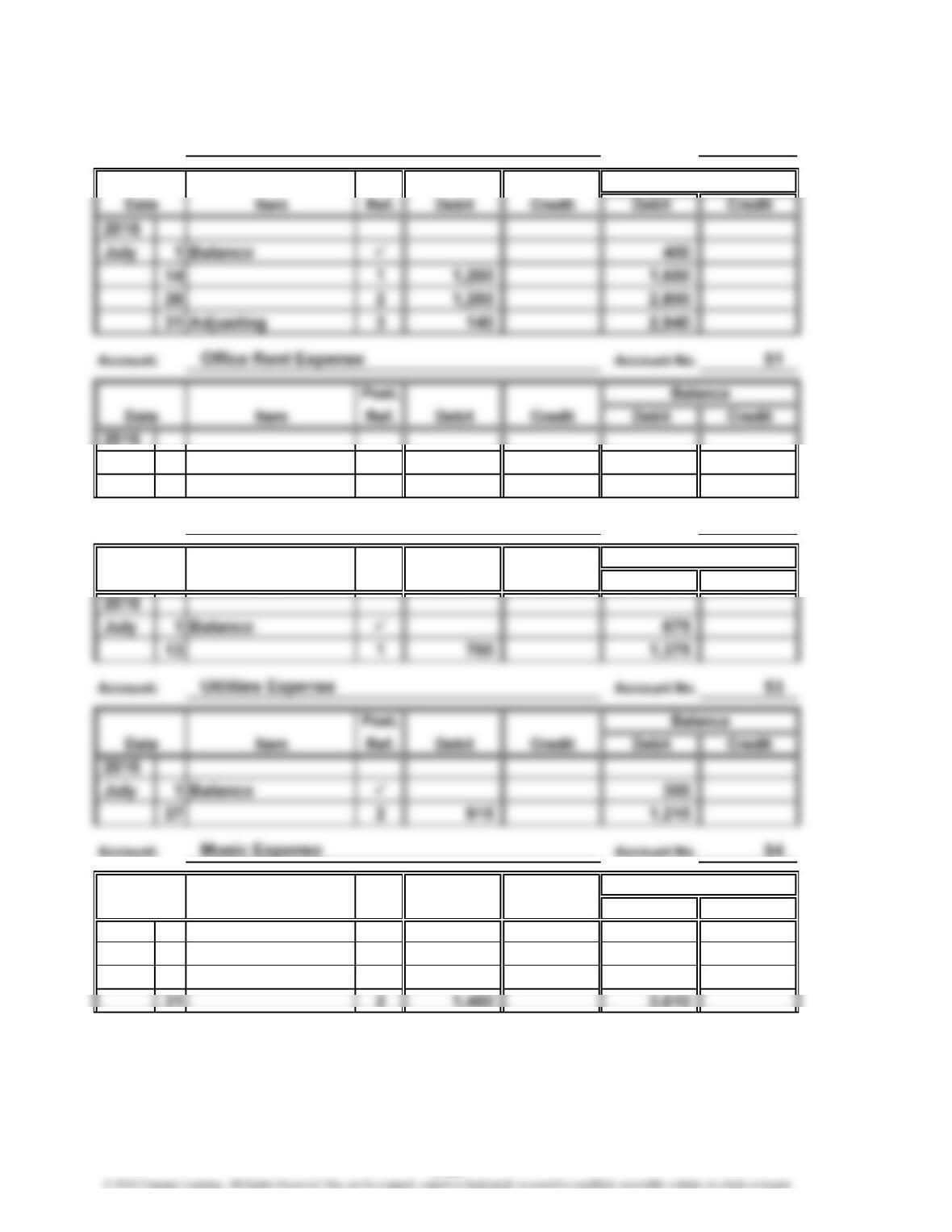

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 14

Post.

31 Adjusting 3 225 2,475

Account No. 17

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 250

3 1 250 — —

5 1 7,500 7,500

18 2 850 8,350

Account No. 22

Balance

Balance

Account: Office Equipment

Date

Account: Wages Payable

Account: Supplies

3-30

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 23

Post.

Account No. 33

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 500

Account:

Account: Unearned Revenue

Balance

Dividends

Balance

Date

3-31

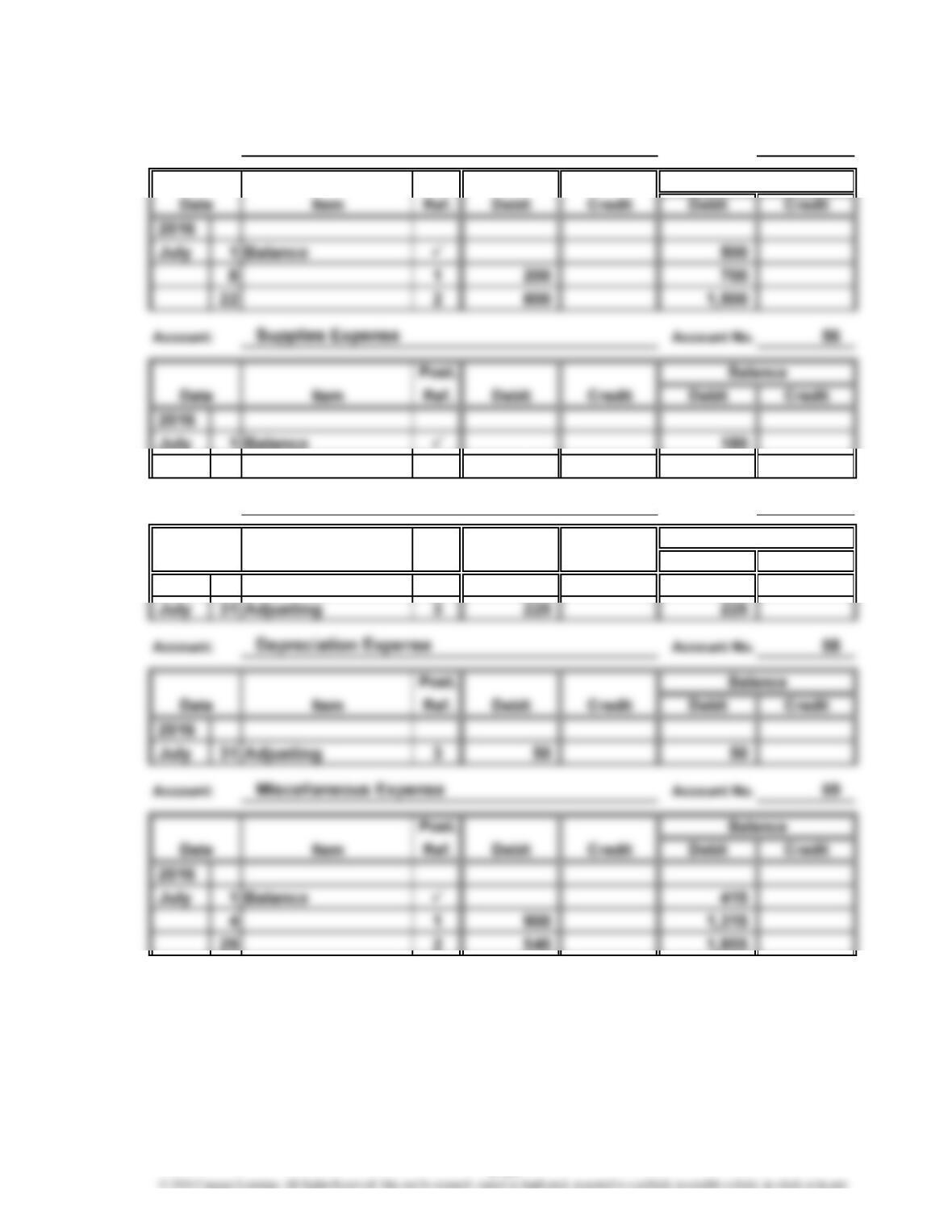

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 50

Post.

July 1 Balance 800

1 1 1,750 2,550

Account No. 52

Post.

Item Ref. Debit Credit Debit Credit

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 1,590

21 2 620 2,210

Balance

Date

Balance

Date

Balance

Account: Wages Expense

Account: Equipment Rent Expense

3-32

CHAPTER 3 The Adjusting Process

Continuing Problem (Continued)

Account No. 55

Post.

31 Adjusting 3 745 925

Account No. 57

Post.

Item Ref. Debit Credit Debit Credit

2016

Account: Insurance Expense

Date

Balance

Balance

Account: Advertising Expense

3-33

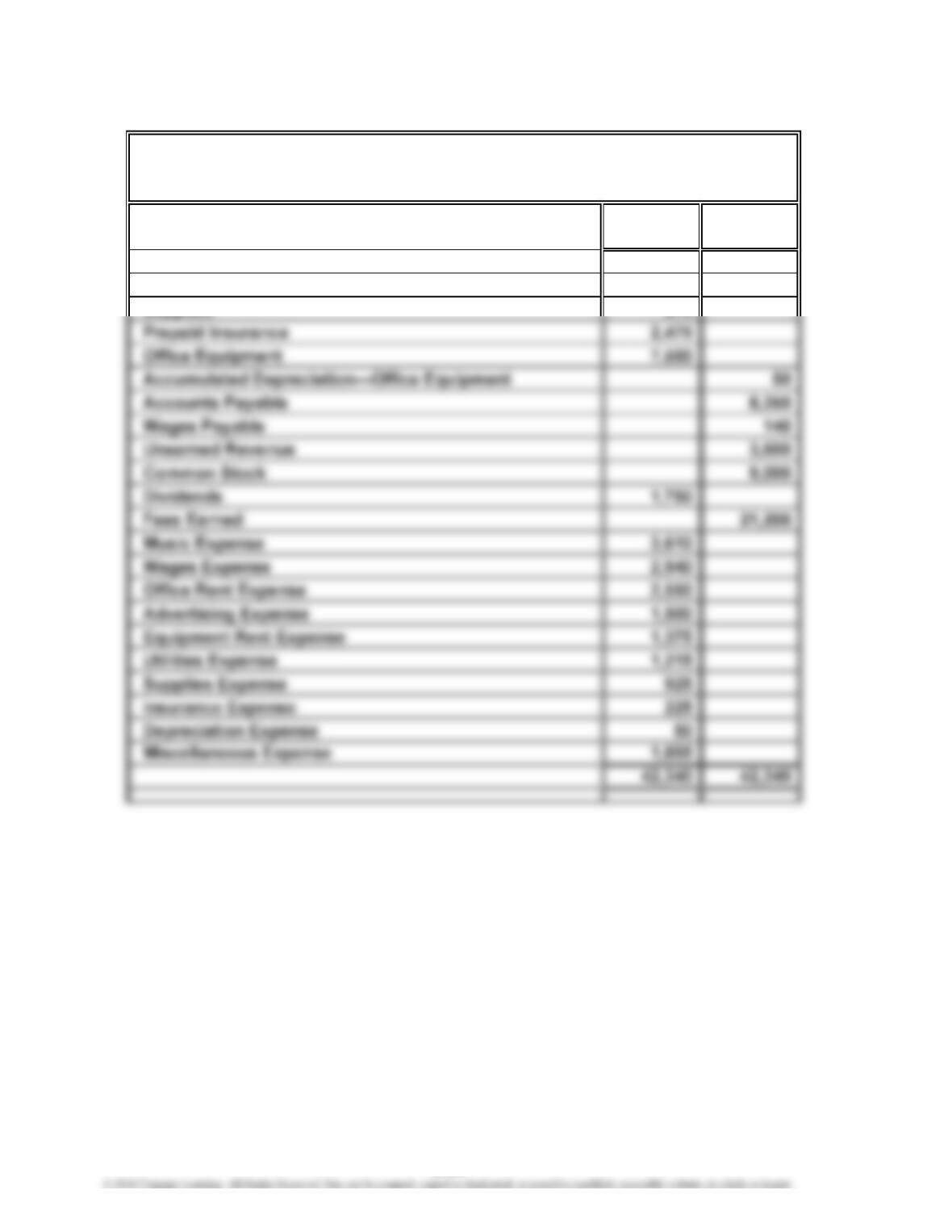

CHAPTER 3 The Adjusting Process

Continuing Problem (Concluded)

3.

Debit Credit

Balances Balances

Cash 9,945

Accounts Receivable 4,150

Supplies 275

PS MUSIC

Adjusted Trial Balance

July 31, 2016

3-34

CHAPTER 3 The Adjusting Process

CP 3–1

It is acceptable for Daryl to prepare the financial statements for Squid Realty Co. on

an accrual basis. The revision of the financial statements to include the accrual of

CP 3–2

Revenue is normally recorded when the services are provided or when the

goods are delivered (title passes) to the buyer. By waiting until after the services

are provided, the expenses of providing the services can be more accurately

(1) The receipt of revenue from customers in advance of a flight represents

(2) At the end of the airline’s accounting period, it would have adjusting entries

related to such items as the following:

●Accrued wages for employees

CASES & PROJECTS

CHAPTER 3 The Adjusting Process

CP 3–3

1. All expenses on the income statement are identified as “paid” items and

not as “expenses.”

3. No supplies, accounts payable, or wages payable are reported on the

1. Accumulated Depreciation—Truck for depreciation expense.

3. Insurance (paid) expense for unexpired insurance.

5. Utilities accrued.

CP 3–4

Note to Instructors: The purpose of this activity is to familiarize students with

behaviors that are common in codes of conduct. In addition, this activity

addresses an actual ethical dilemma for students related to doing their