Brief

Exercises

B. Ex. 3.1

B. Ex. 3.2

B. Ex. 3.3

B. Ex. 3.4 Analysis

B. Ex. 3.5

B. Ex. 3.6

B. Ex. 3.7

B. Ex. 3.8

B. Ex. 3.9

B. Ex. 3.10

Exercises

3.1

3.2

3.3

3.4

3.5

3.6 Analysis

3.7

3.8 Revenue, expenses, and dividends Analysis

3.9 Financial statement effects Analysis

3.10 Preparing a trial balance Analysis

3.11 Preparing a trial balance Analysis

3.12

3.13

3.14 Analysis

3.15

CHAPTER 3

THE ACCOUNTING CYCLE:

CAPTURING ECONOMIC EVENTS

Communication, analysis

3-1–3-3, 3-7, 3-10

Real World: Home Depot, Inc.

Using an annual report

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Objectives

Learning

Accounting terminology

The matching principle

Journal and ledger relationships

3-6, 3-7

3-6, 3-7

Analysis

The accounting cycle

Skills

Debit and credit rules

Analysis

Analysis

Analysis, judgment

Analysis, judgment

Recording transactions

Topic

3-1, 3-2, 3-5, 3-9,

3-10

3-3–3-5

Analysis

Analysis

Analysis

3-3, 3-6

3-6, 3-7

3-6, 3-7

Analysis

3-2–3-6

3-2–3-6

Analysis

3-3, 3-5, 3-8, 3-9

3-3, 3-5, 3-8, 3-9

Accounting equation relationships

Analysis, communication

Analysis

3-3, 3-6, 3-8

3-3, 3-6, 3-8

Preparing a trial balance

Analyzing transactions

Analyzing transactions

Real World: Apple Computer Net

income and owners’ equity

3-3, 3-5, 3-8, 3-9

3-3, 3-6, 3-7

3-7, 3-8

3-3, 3-8

Analysis

Recording transactions

Realization and matching principles

Topic

Expense recognition

3-9

3-2–3-5

Revenue realization

Accounting equation relationships

3-6, 3-8

3-4, 3-6–3-8

Learning

Objectives

Preparing a trial balance

Analysis

3-1–3-10

Skills

Analysis

3-6, 3-7

Communication, analysis

Changes in retained earnings

Matching principle

Revenue realization

Analysis

3-6, 3-7

Problems

Sets A, B

3.1 A,B

3.2 A,B Recording journal entries and

3.3 A,B

3.4 A,B

3.5 A,B

3.6 A,B Short comprehensive problem

3.7 A,B Short comprehensive problem

3.8 A,B

3.1 Revenue recognition 3-7, 3-10

3.2 Income measurement 3-6, 3-7, 3-10

3.3 3-6, 3-7, 3- 10

3.4 3-6

Learning

3-3–3-8

3-3–3-8

3-3–3-5

Objectives

Analysis, communication

Topic

Skills

3-7–3-9

Analysis, communication

3-1–3-10

3-1–3-10

Analysis, judgment,

communication

The accounting cycle

The accounting cycle

Analysis, communication

Communication, judgment

Communication, judgment,

analysis

Recording journal entries and

identifying their effects on the

accounting equation

identifying their effects on the

accounting equation

Recording journal entries and

identifying their effects on the

accounting equation

Communication,

technology, judgment,

3-3–3-9

Real World: PC Connection –

Revenue from various sources

(Internet)

3-3, 3-8

Analyzing the effects of errors

Analysis, judgment,

communication

Critical Thinking Cases

Whistle-Blowing

(Ethics, fraud & corporate governance)

Analysis, communication

Analysis

Analysis, communication,

judgment

Communication, judgment,

analysis

Problems (Sets A and B)

30 Medium

30 Medium

35 Medium

60 Strong

50 Strong

50 Strong

50 Strong

Home Team Corporation/Blind River, Inc.

3.6 A,B

Donegan’s Lawn Care Service/Clown Around, Inc.

Requires students to journalize and post transactions, prepare a

trial balance, and understand various relationships among financial

statement elements.

Requires students to analyze the effects of errors on financial

statement elements.

Requires students to journalize and post transactions, prepare a

trial balance, and understand various relationships among financial

statement elements.

3.7 A,B

Sanlucas, Inc./Ahuna, Inc.

3.8 A,B

50 Strong

3.4 A,B

3.1 A,B

A company engages in numerous transactions during its first

month of operations. Students are required to journalize each

transaction and analyze the effect of each transaction on the

accounting equation.

Heartland Construction/North Enterprises

3.2 A,B

Weida Surveying, Inc./Dana, Inc.

Aerial Views/Tone Deliveries, Inc.

Calls for a detailed analysis of numerous transactions,

journalizing, and the application of the realization and matching

principles.

3.5 A,B

Dr. Schekter, DVM/Dr. Cravati, DMD

Requires students to journalize and post transactions, prepare a

trial balance, and understand the relationships between the income

statement and balance sheet.

Environmental Services, Inc./Lyons, Inc.

3.3 A,B

Requires students to journalize transactions and to understand the

relationship between the income statement and the balance sheet.

Requires students to journalize and post transactions, prepare a

trial balance, and understand the relationships between the income

statement and balance sheet.

Critical Thinking Cases

Revenue Recognition 15 Medium

Measuring Income

Whistle-Blowing 5 Easy

Ethics, Fraud & Corporate Governance

PC Connection 10 Easy

Revenue from Various Sources

Internet

3.1

3.2

Requires students to draw conclusions concerning the point at which various

companies should recognize revenue.

Students are to determine whether a company’s methods of measuring income

are fair and reasonable. Also requires students to distinguish between net

income and cash flow.

30 Strong

Using 10-K reports, students are asked to identify revenue from various

sources.

3.3

Students are asked to consider the legal and ethical implications of engaging

in fraudulent reporting activities.

3.4

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

3. Asset accounts:

4.

5.

No, the term debit means an entry on the left-hand side of an account; the term credit simply

a. Increases are recorded by debits

Although it has no obligation to issue financial statements to creditors or investors, Baker

Construction still should maintain an accounting system. For a start, the company probably has

numerous reporting obligations other than financial statements. These include income tax

Assets are located on the left side of the balance sheet equation; an increase in an asset account is

6.

7.

8.

9.

Operating profitably causes an increase in owners’ equity. Usually, this increase in equity is

The term expenses means the cost of the goods and services used up or consumed in the process

of obtaining revenue. Expenses cause a decrease in owners’ equity. To determine the net income

Revenue represents the price of goods sold and of services rendered to customers during the

for another asset (cash) and does not constitute revenue.

No, net income does not represent an amount of cash. The entire amount of cash owned by a

10.

11.

13.

14.

15.

Revenue is considered realized at the time that services are rendered to customers or goods sold

Some of the more analytical functions performed by accountants include determining the

A dividend is a distribution of assets (usually cash) by a corporation to its stockholders.

Dividends reduce both assets and owners’ equity (specifically, the Retained Earnings account).

The matching principle indicates that expenses should be recognized in the period (or periods)

The trial balance provides proof that the ledger is in balance. A trial balance does not, however,

12.

B. Ex. 3.1 a.

b.

1360,000

360,000

B. Ex. 3.2 Oct.

Capital Stock ……………………………………

Issued capital stock at $72 per share.

Cash ……………………………………………………

SOLUTIONS TO BRIEF EXERCISES

6. Prepare financial statements.

8. Prepare an after-closing trial balance.

3. Prepare a trial balance.

7. Journalize and post closing entries.

4. Make end-of-period adjustments.

5. Prepare an adjusted trial balance.

1. Journalize transactions.

4. Help make business decisions.

3. Maintain a documentary record of business activities.

2. Establish accountability for assets and transactions.

1. Evaluate the efficiency of operations.

4300,000

120,000

180,000

600,000

Paid cash dividend.

Collected amount owed from Health One Insurance.

Accounts Payable ……………………………………….

Cash …………………………………………………

Purchased surgical supplies on account.

Dividends ……………………………………………

Cash …………………………………..

Surgical Supplies …………………………………….

Accounts Receivable …………………..

Accounts Payable ……………………..

Paid account payable to Zeller Laboratories.

Notes Payable ………………………….

Cash ……………………………………

Diagnostic Equipment ……………………………………….

B. Ex. 3.3 a. Jan. 18 400,000

400,000

B. Ex. 3.4 Owners’

Expenses Liabilities Equity

Cash ……………………………………………………

Capital Stock ……………………………………

Issued capital stock for $400,000.

Assets

Revenue

100,000

Paid for radio ad to be aired on January 24.

Advertising Expense ……………………………………….

Cash …………………………………..

Cash ……………………………………………………

Notes Payable ……………………………………

Service Revenue….. …………………..

Cash…………….. …………………………………….

Provided services to clients.

Service Revenue ……………………..

Accounts Receivable …………………………………..

Cash…….. ……………………………………………

Provided services to clients on account.

Accounts Receivable …………………………………………………

B. Ex. 3.5

B. Ex. 3.6 a.

b.

Thus, Breeze Camp Ground will recognize advertising expense in the months that

B. Ex. 3.7 a.

b.

d.

This fee was earned in May and represents revenue of that month, despite the fact

that collection will not be made until June.

The collection of an account receivable does not increase owners’ equity and does

not represent revenue.

Revenue is recognized when it is earned. Thus, KPRM Radio will recognize revenue

from Breeze Camp Ground in the months that the ads are aired (at $500 per ad):

Expenses are matched to the periods in which they contribute to generating revenue.

An investment by stockholders does not constitute revenue. Although this

investment causes an increase in owners’ equity, this increase was not earned. It did

Beginning Retained Earnings (1/1) ………

108,000$

378,000$

288,000

B. Ex. 3.8 a.

b.

c.

B. Ex. 3.9

B. Ex. 3.10

Gasoline purchased is an expense because it is ordinarily used up in the current

Payment to an employee for services rendered in March is a March expense. Such a

The purchase of a copying machine does not represent an expense. The asset Cash is

exchanged for the asset Office Equipment, without any change in owners’ equity.

Revenue is recognized when it is earned, not necessarily when cash is received.

Expenses are recognized when they are incurred, not necessarily when cash is paid.

d.

The dividend does not constitute an expense. Unlike payments for advertising, rent,

Ex. 3.1 a.

Ex. 3.2 a.

Gasoline (15,000 miles at 30 mpg. = $3.20/gal.) ………………………………….

Registration and license ………………………………………………………….

Depreciation …………………………………………………………………………

Repairs and maintenance ……………………………………………………………

Annual total……………………………………………………………………..

1,000$

b.

Insurance ………………………………………………………………………..

Costs of owning and operating an automobile (estimates will vary; the following list is

only an example):

SOLUTIONS TO EXERCISES

Accounting period

Although you spent no money during this trip, you incurred significant costs. For

Realization principle

Matching principle

Net income

None (This statement describes the accounting convention of conservatism.)

Ex. 3.3 Nov. 1 144,000

144,000

Notes payable ………………………………………………….

Accounts payable ………………………………………………

Capital stock ……………………………………………………

Building ………………………………………………………..

Office equipment ……………………………………………….

Vehicles ………………………………………………………..

87,600$

84,000

Land ……………………………………………………………

Cash …………………………………………………………..

Ex. 3.4

AVENSON INSURANCE COMPANY

Trial Balance

November 30, Current Year

Capital Stock ………………………………………

Cash ……………………………………………………………

114,000

Notes Payable …………………………………

Office Equipment …………………………………………………..

Cash …………………………………………

Vehicles ………………………………………………………..

Accounts Payable ………………………………

Accounts Payable ……………………………………………..

Office Equipment ……………………………..

Notes Payable ………………………………………………..

Cash …………………………………………

Notes Payable …………………………………

Land ………………………………………………………………….

Building ……………………………………………………….

Cash ……………………………………………..

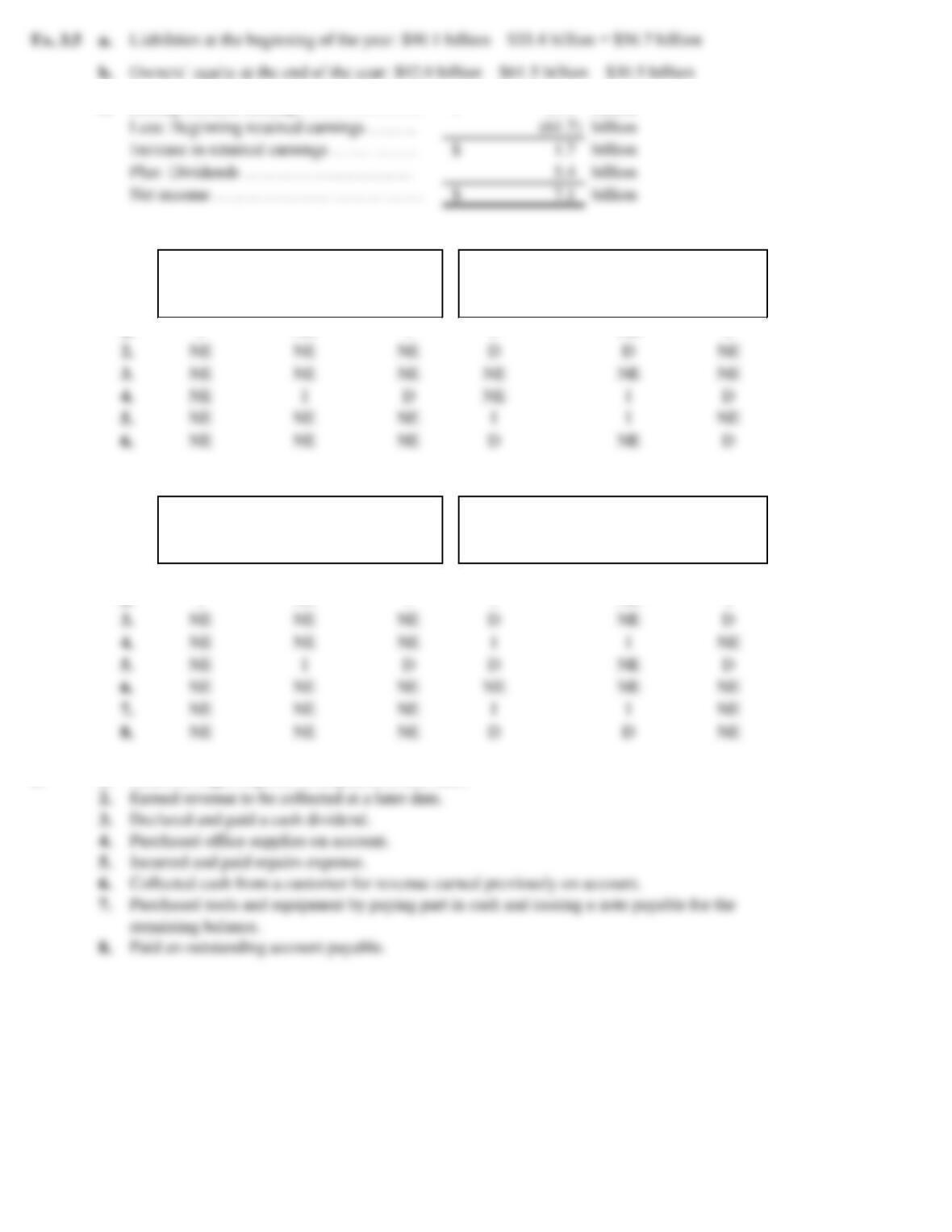

c. billion

Less: Beginning retained earnings ….…..

Increase in retained earnings …..………..

Plus: Dividends …………………………..…

Net income ……………………………….

Ex. 3.6

Revenue –Expenses = Assets –Liabilities =

INE I I NE I

NE I D NE I D

3.

2.

5.

6.

4.

Ex. 3.7

a.

Revenue –Expenses = Assets –Liabilities =

NE I D NE I D

INE I I NE I

NE I D D NE D

8.

5.

7.

3.

6.

b. 1.

Paid an outstanding account payable.

Earned revenue to be collected at a later date.

Declared and paid a cash dividend.

Purchased office supplies on account.

Incurred and paid repairs expense.

Collected cash from a customer for revenue earned previously on account.

Owners’

Equity

Balance Sheet

Balance Sheet

1.

Income Statement

Net

Income

Owners’

Equity

Ending retained earnings ……………………

63.4$

2.

Trans-

action

Trans-

action

Incurred wages expense to be paid at a later date.

1.

Net

Income

Income Statement

Ex. 3.5 a.

Liabilities at the beginning of the year: $90.1 billion – $33.4 billion = $56.7 billion

Owners’ equity at the end of the year: $92.0 billion – $61.5 billion = $30.5 billion

Ex. 3.8 a. Apr. 5 Accounts Receivable …………………………… 13,200

Drafting Fees Earned ……………………

13,200

b.

June 10: Payment of an account payable.

June 25: Payment of a dividend payable.

May 17: Declaration of a cash dividend.

The following transactions will not cause a change in net income.

13,200

Paid amount owed to Bob Needham, CPA.

Paid cash dividend declared May 17.

Declared cash dividend; payment due June 25.

Ex. 3.9 Transaction Net Income Assets Liabilities Equity

a. NE INE I

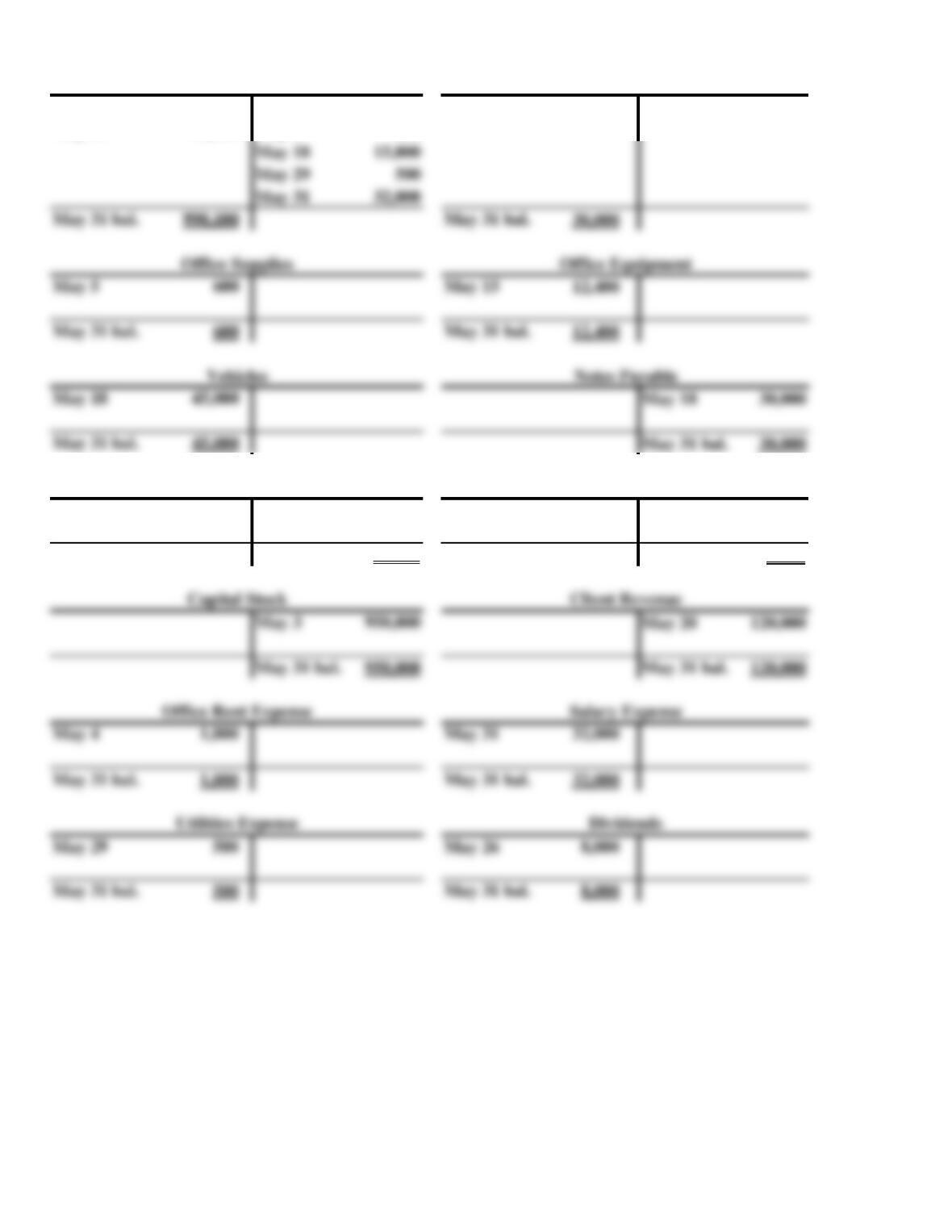

Ex. 3.10 a. May 3 Cash……………………………………………. 950,000

Capital Stock…………………………….

950,000

20 120,000

Client Revenue………………………..

120,000

Salary Expense…………………………………

Paid salary expense incurred in May.

Declared dividend to be distributed in June.

Utilities Expense………………………………

Paid May utilities.

Accounts Receivable…………………………

Billed clients for services on account.

Issued capital stock for $950,000.

4

5

15

Paid May office rent expense.

Purchased office supplies.

Purchased office equipment on account. Amount

b.

Cash

May 3 950,000 May 4 1,800 May 20 120,000 May 30 90,000

May 30 90,000 May 5 600

Accounts Payable Dividends Payable

May 15 12,400 May 26 8,000

May 31 bal. 12,400 May 31 bal. 8,000

May 3 950,000 May 20 120,000

Accounts Receivable

May 18 15,000

May 29 500

May 31 bal. 990,100 May 31 bal. 30,000

May 5 600 May 15 12,400

May 31 bal. 600 May 31 bal. 12,400

May 18 45,000 May 18 30,000

May 31 bal. 45,000 May 31 bal. 30,000

c.

Janet Enterprises Incorporated

Trial Balance

May 31, Current Year

Debit Credit

Cash……………………………………. 990,100$

Accounts receivable………………………

30,000

Office rent expense………………………

Ex. 3.11 a. Sep. 2 Cash……………………………………………. 1,170,000

Capital Stock…………………………….

1,170,000

Issued capital stock for $1,170,000.

Recorded and paid salary expense.