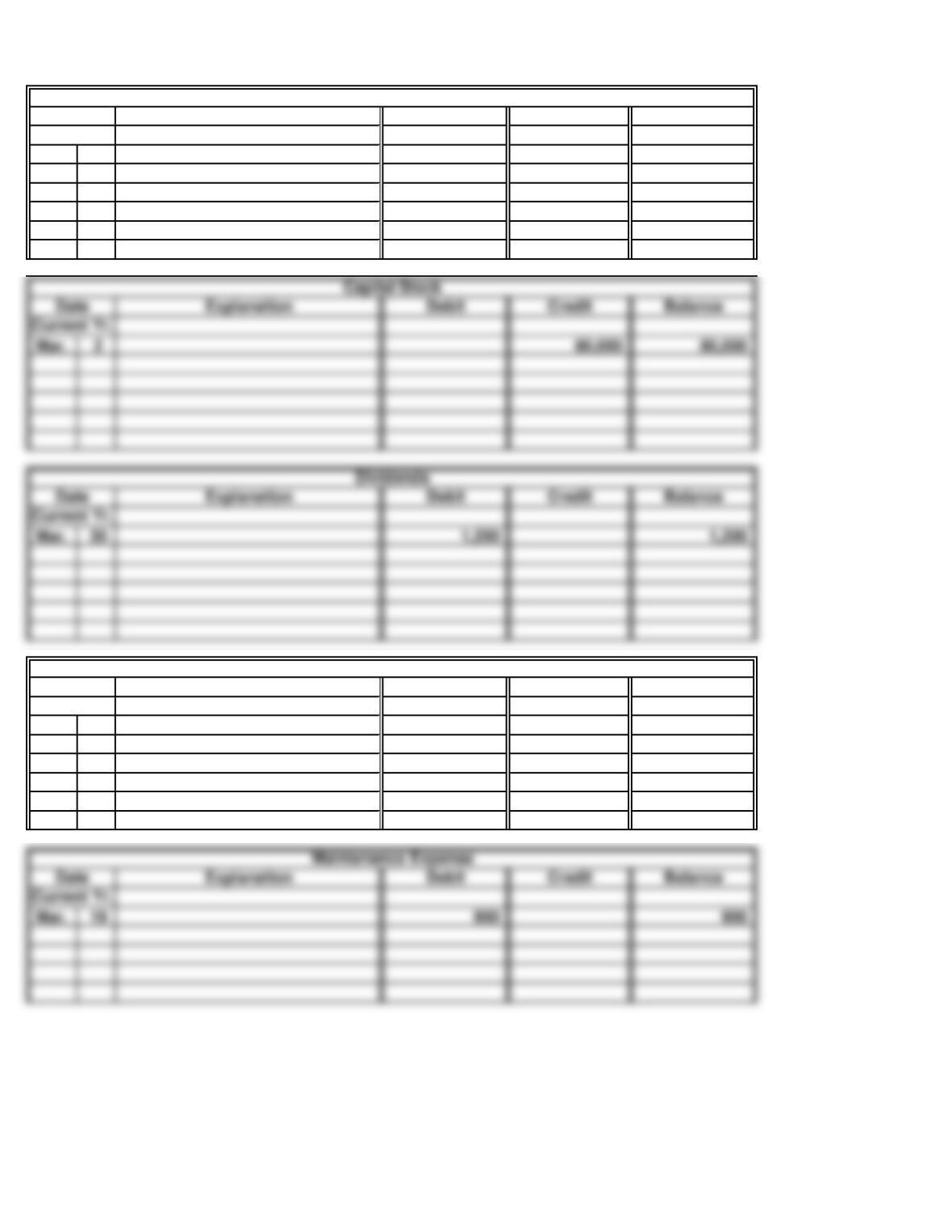

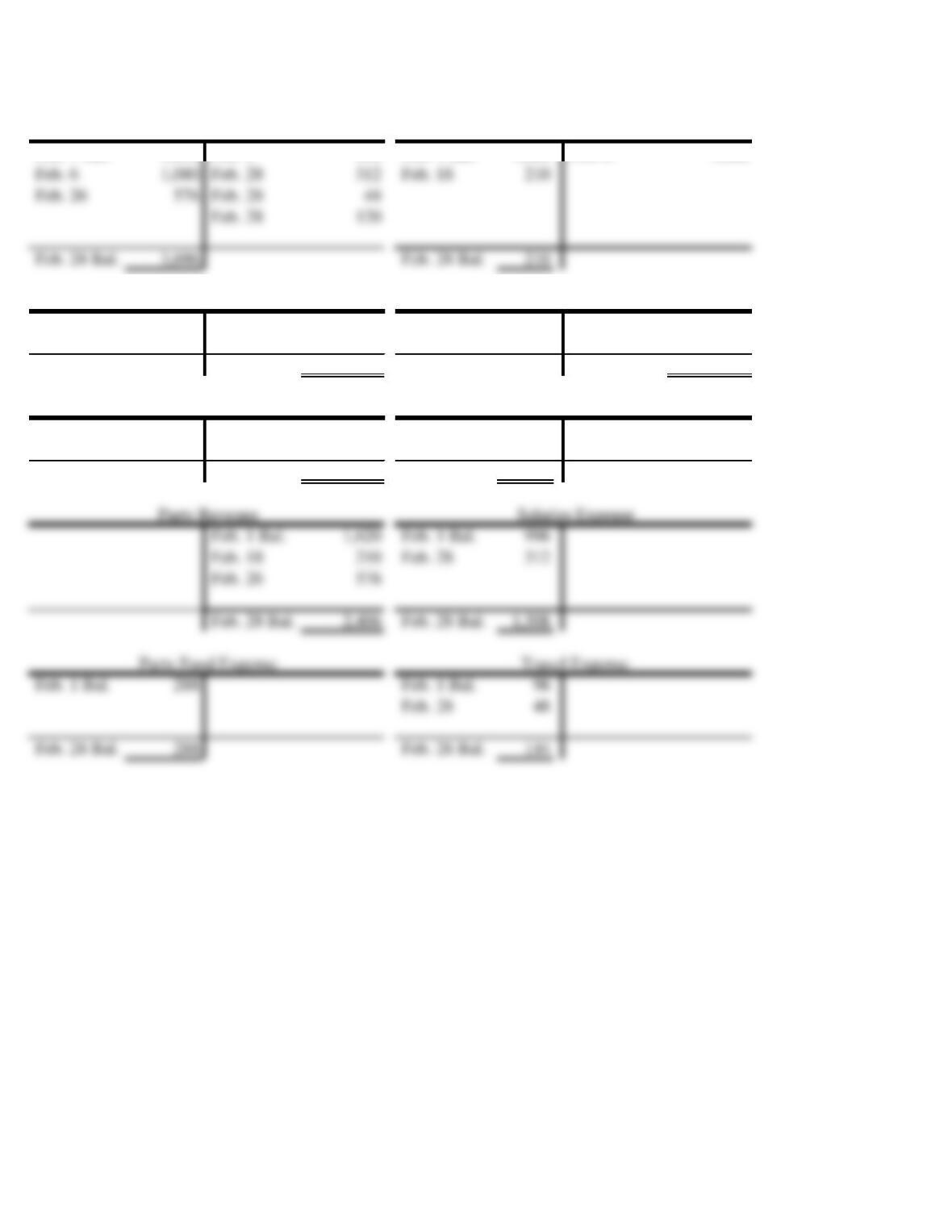

Debit Credit Balance

Mar. 30 1,200 1,200

Debit Credit Balance

Mar. 9 11,300 11,300

28 14,400 25,700

Debit Credit Balance

Mar. 19 900 900

Current Yr.

Date

Explanation

Explanation

Date

Service Revenue

Current Yr.

PROBLEM 3.4B

Date

TONE DELIVERIES (continued)

Dividend Payable

Explanation

Current Yr.

Debit Credit Balance

Mar. 2 80,000 80,000

Debit Credit Balance

Mar. 30 1,200 1,200

Current Yr.

Current Yr.

Date

Explanation

Explanation

Date

Debit Credit Balance

Debit Credit Balance

Debit Credit Balance

Date

Explanation

PROBLEM 3.4B

Date

TONE DELIVERIES (continued)

Fuel Expense

Explanation

Salaries Expense

Date

Explanation

d.

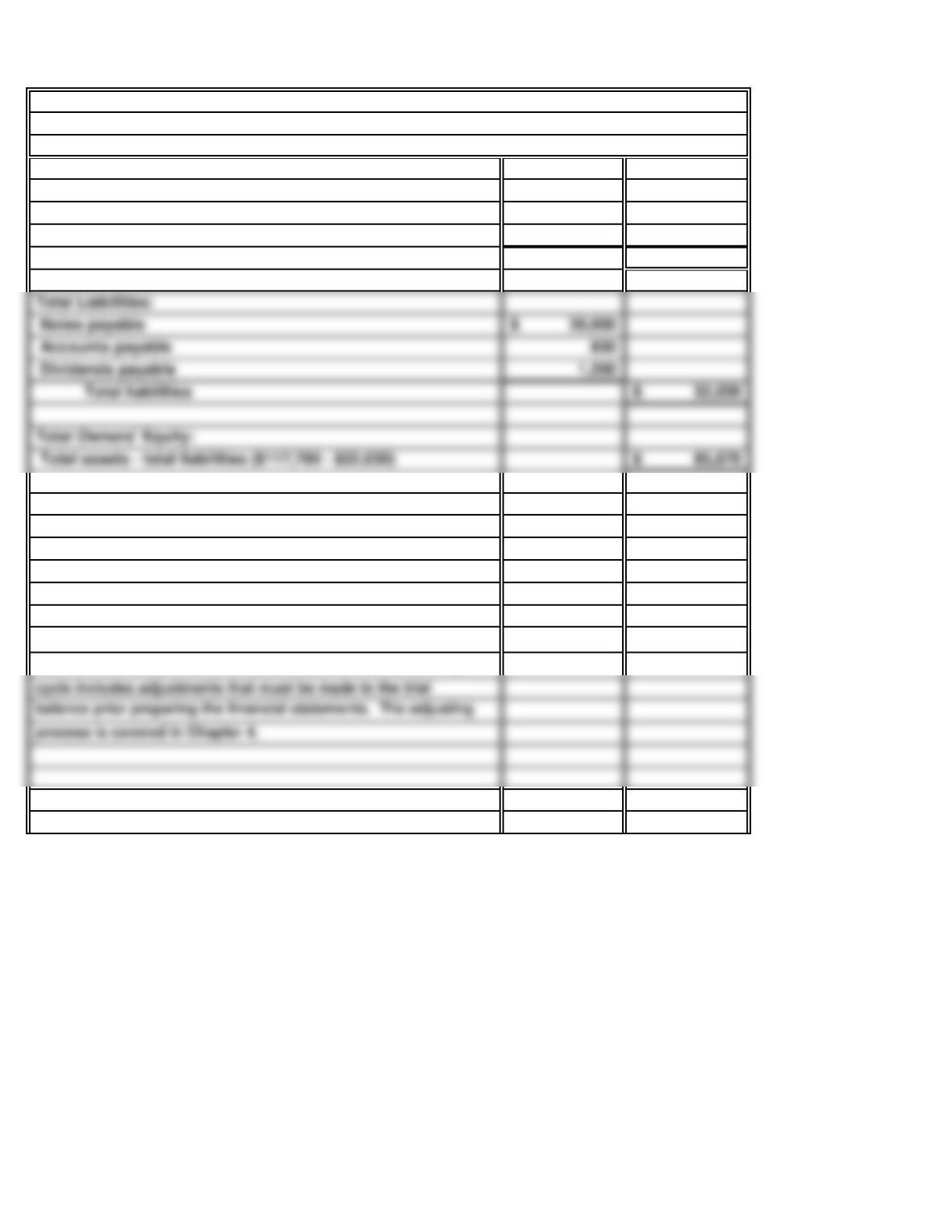

50,800$

21,900

45,000

30,000$

830

PROBLEM 3.4B

TONE DELIVERIES

March 31, Current Year

Cash

TONE DELIVERIES (continued)

Trial Balance

Accounts payable

Accounts receivable

Notes payable

Truck

Dividends payable

Capital stock

Retained earnings

Rent expense

Service revenue

Maintenance expense

Salaries expense

Dividends

Fuel expense

e.

Total Assets:

50,800$

21,900

45,000

117,700$

The above figures are most likely not the amounts to be

reported in the balance sheet dated March 31. The accounting

Accounts receivable

Total assets

Trucks

PROBLEM 3.4B

TONE DELIVERIES (concluded)

Cash

Total Liabilities:

Total assets – total liabilities ($117,700 – $32,030)

Accounts payable

Dividends payable

Total Owners’ Equity:

Notes payable

Total liabilities

Revenue –Expenses = Assets –Liabilities =

NE NE NE INE I

PROBLEM 3.5B

60 Minutes, Strong

DR. CRAVATI, DMD

Balance Sheet

Income Statement

a.

Owners’

Equity

Transaction

Net

Income

Aug. 1

NE NE NE I I NE

NE NE NE I I NE

Aug. 4

Aug. 9

b.

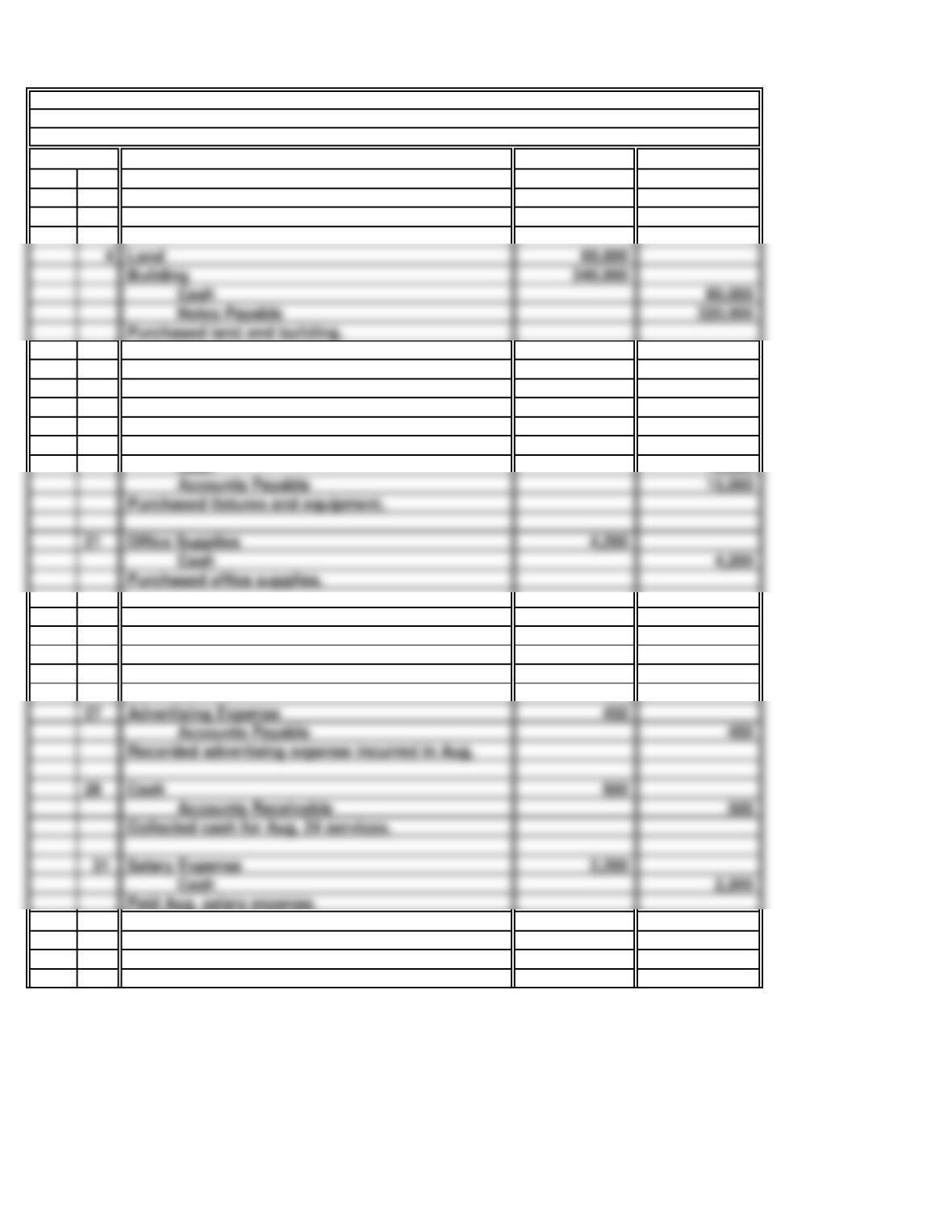

Aug. 1 280,000

Capital Stock 280,000

9 75,000

Cash 75,000

16 25,000

Cash 10,000

Accounts Payable 15,000

21 4,200

Cash 4,200

Office Supplies

Purchased fixtures and equipment.

Purchased office supplies.

24 1,000

12,000

Service Revenue 13,000

27 450

Accounts Payable 450

28 500

Accounts Receivable 500

31 2,200

Cash 2,200

Collected cash for Aug. 24 services.

Salary Expense

Cash

Recorded advertising expense incurred in Aug.

Advertising Expense

Issued 1,000 shares of capital stock.

Cash

PROBLEM 3.5B

DR. CRAVATI, DMD (continued)

Current Yr.

General Journal

Medical Instruments

Cash

Office Fixtures and Equipment

Purchased medical instruments.

Recorded dental service revenue earned.

Accounts Receivable

Cash 80,000

Notes Payable 320,000

Land

Building

Purchased land and building.

c.

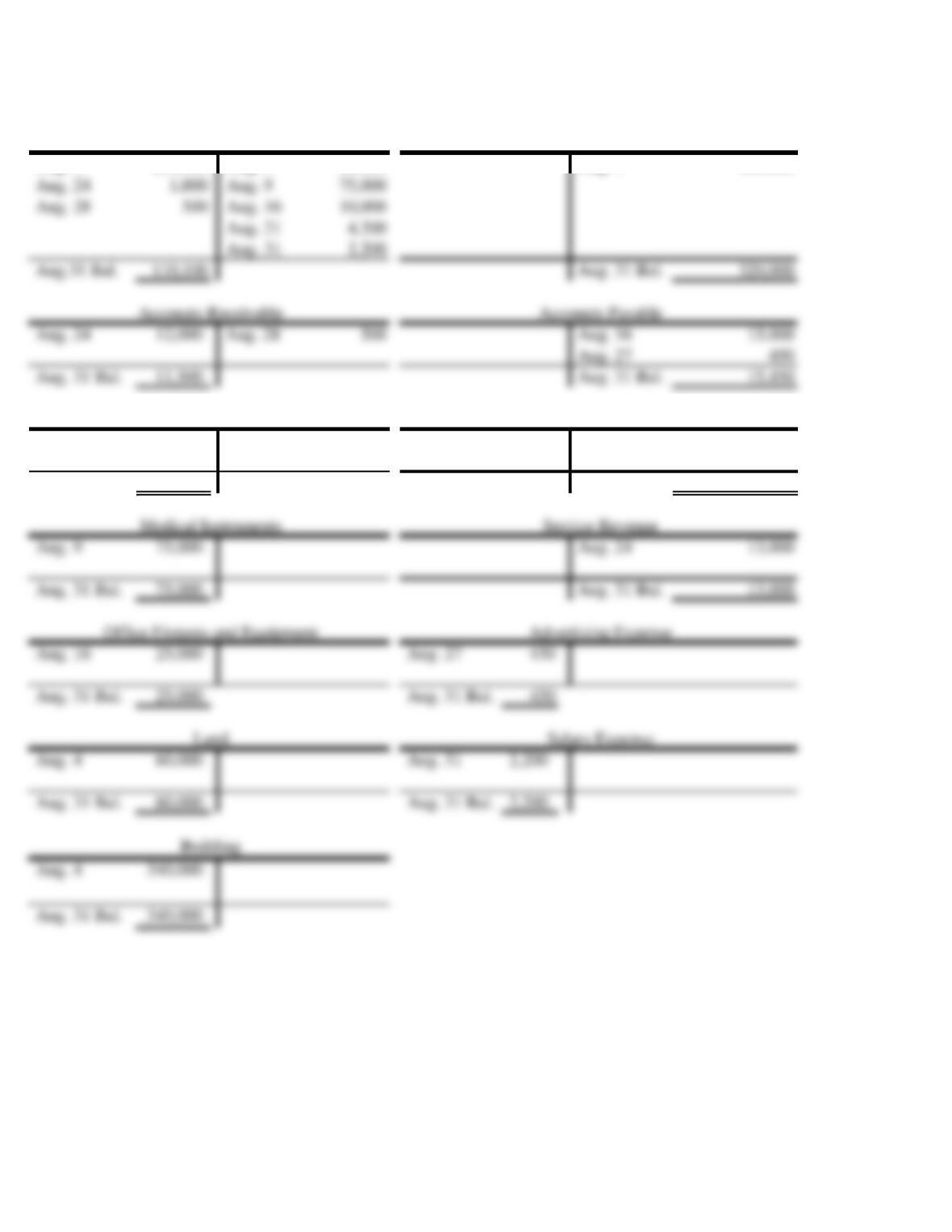

Aug. 1 280,000 Aug. 4 80,000 Aug. 4 320,000

Aug. 21 4,200 Aug. 1 280,000

Aug. 31 Bal. 4,200 Aug. 31 Bal. 280,000

Aug. 9 75,000 Aug. 24 13,000

Aug. 31 Bal. 75,000 Aug. 31 Bal. 13,000

Aug. 16 25,000 Aug. 27 450

Aug. 31 Bal. 25,000 Aug. 31 Bal. 450

Aug. 4 60,000 Aug. 31 2,200

Aug. 31 Bal. 60,000 Aug. 31 Bal. 2,200

PROBLEM 3.5B

DR. CRAVATI, DMD (continued)

Notes Payable

Capital Stock

Cash

Office Supplies

Aug. 24 1,000 Aug. 9 75,000

Aug. 28 500 Aug. 16 10,000

Aug.31 Bal. 110,100 Aug. 31 Bal. 320,000

Aug. 24 12,000 Aug. 28 500 Aug. 16 15,000

Aug. 31 Bal. 11,500 Aug. 31 Bal. 15,450

d.

110,100$

11,500

4,200

75,000

25,000

Accounts receivable

Office supplies

Medical instruments

Office fixtures and equipment

Cash

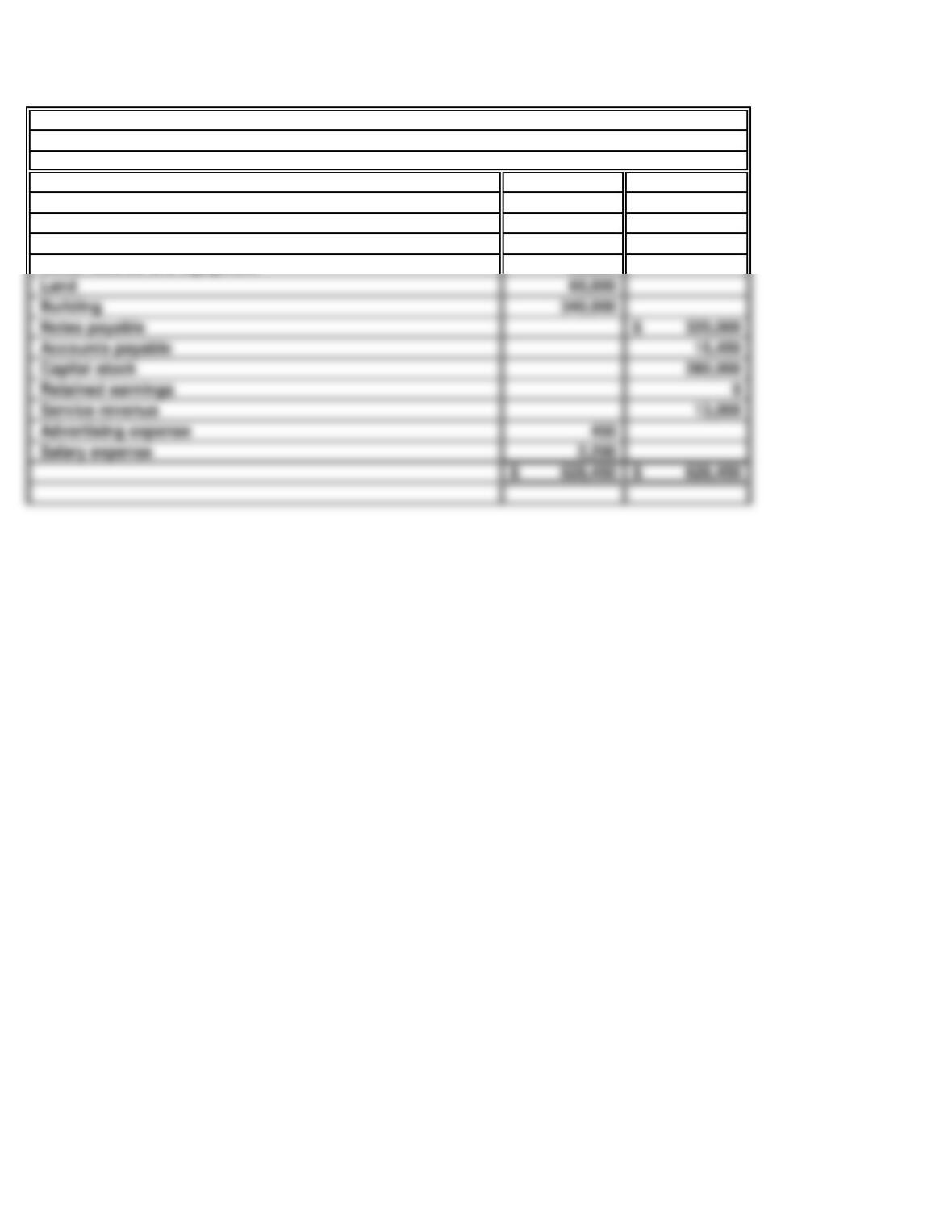

Trial Balance

PROBLEM 3.5B

DR. CRAVATI, DMD (continued)

DR. CRAVATI, DMD

August 31, Current Year

Salary expense

Notes payable

Service revenue

Advertising expense

Accounts payable

Capital stock

Retained earnings

Land

Building

e.

$ 450

2,200 2,650

month of operations:

Service revenue

Total assets – total liabilities ($625,800 – $335,450)

Salary expense

Net income (profit)

Less: Advertising expense

Total Owners’ Equity:

As shown below, the business was profitable in its first

Total Assets:

110,100$

11,500

320,000$

15,450

335,450$

Accounts payable

Total liabilities

Notes payable

Total Liabilities:

PROBLEM 3.5B

DR. CRAVATI, DMD (concluded)

Cash

Accounts receivable

Office supplies

Land

Total assets

Building

Medical instruments

Office fixtures and equipment

a.

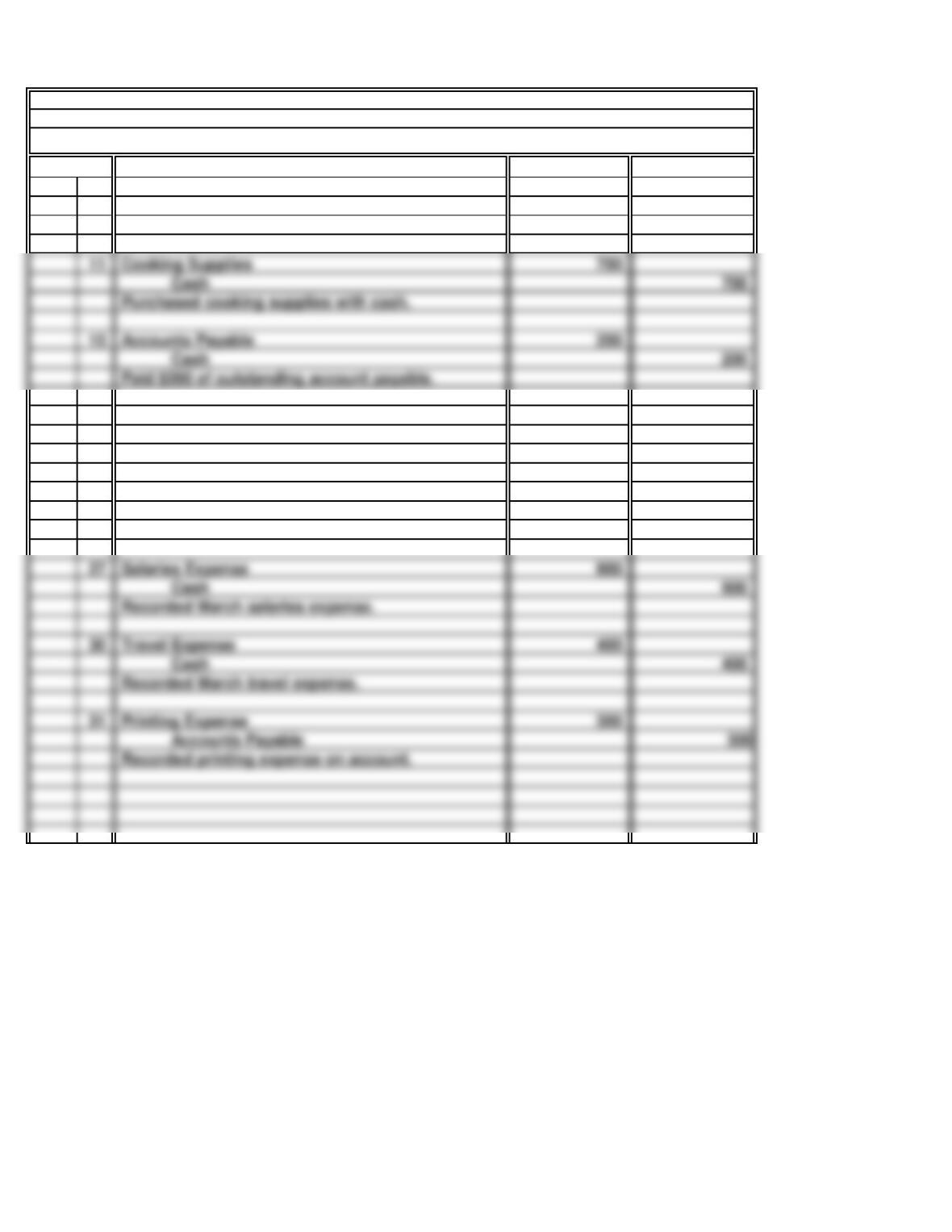

Feb. 2 900

Cash 900

28 312

Cash 312

28 48

Cash 48

28 120

Cash 120

Dividends

Paid travel expenses incurred in February.

Declared and distributed dividend to Ralph

Travel Expense

Jaschob.

General Journal

PROBLEM 3.6B

50 Minutes, Strong

CLOWN AROUND, INC.

Current Yr.

Accounts Payable

Paid $900 in partial settlement of outstanding

accounts payable.

Salaries Expense

February.

Paid clown salaries for work performed in

Accounts Receivable 1,080

18 210

Party Revenue 210

26 576

Party Revenue 576

Accounts Receivable

Cash

Billed and collected cash for performing at

Collected $1,080 in full settlement of outstanding

Cash

The entire amount is due March 15.

accounts receivable.

Billed Sunflower Child Care for clown services.

several birthday parties.

b.

Feb. 1 Bal. 3,420 Feb. 2 900 Feb. 1 Bal. 1,080 Feb. 6 1,080

Feb. 2 900 Feb. 1 Bal. 960 Feb. 1 Bal. 2,400

Feb. 28 Bal. 60 Feb. 28 Bal. 2,400

Feb. 1 Bal. 900 Feb. 1 Bal. 0

Feb. 28 120

Feb. 28 Bal. 900 Feb. 28 Bal. 120

Feb. 1 Bal. 1,620 Feb. 1 Bal. 996

Feb. 28 Bal. 2,406 Feb. 28 Bal. 1,308

Feb. 1 Bal. 288 Feb. 1 Bal. 96

Feb. 28 Bal. 288 Feb. 28 Bal. 144

Party Food Expense

Dividends

Retained Earnings

PROBLEM 3.6B

CLOWN AROUND, INC. (continued)

Accounts Receivable

Capital Stock

Cash

Accounts Payable

Feb. 6 1,080 Feb. 28 312 Feb. 18 210

Feb. 26 576 Feb. 28 48

Feb. 28 Bal. 3,696 Feb. 28 Bal. 210

c.

3,696$

210

60$

d.

Cash

Accounts payable

Dividends are not an expense. Thus, they are not deducted from revenue in the determination of

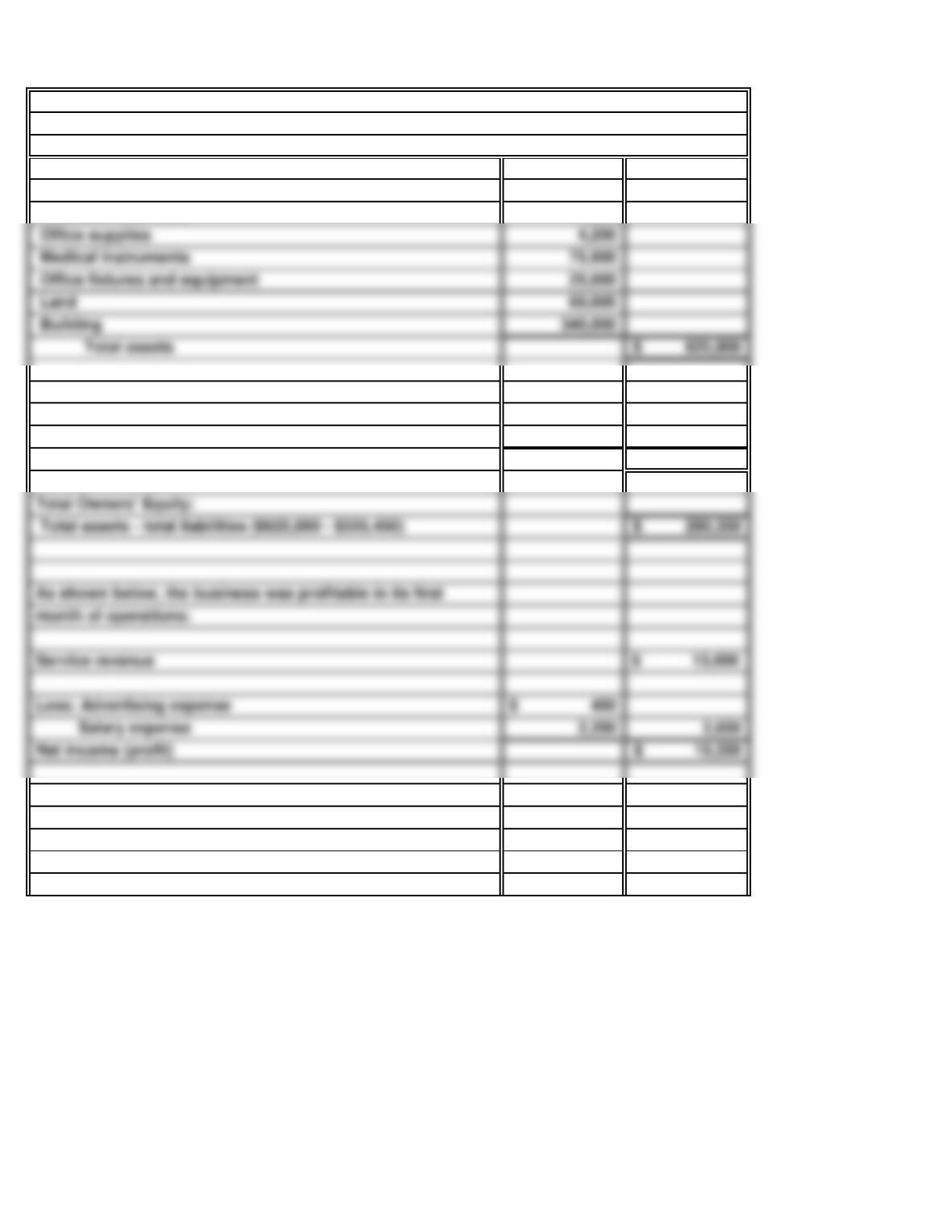

February 28, Current Year

Accounts receivable

(concluded)

PROBLEM 3.6B

CLOWN AROUND, INC.

Trial Balance

CLOWN AROUND, INC.

Retained earnings

Party revenue

Dividends

Capital stock

Salaries expense

Travel expense

Party food expense

a.

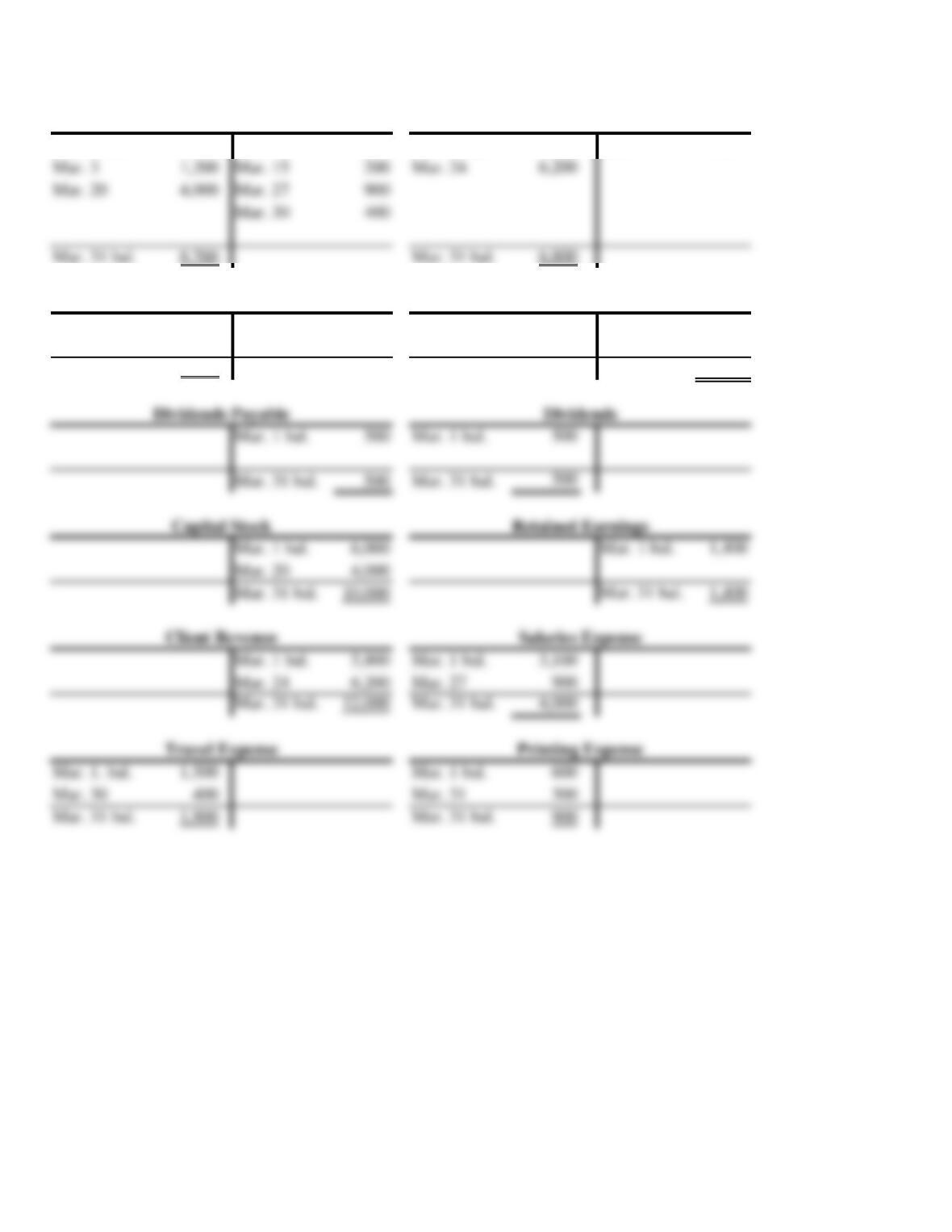

Mar. 3 1,200

Accounts Receivable 1,200

20 4,000

Capital Stock 4,000

24 6,200

Client Revenue 6,200

27 900

Cash 400

31 300

Accounts Payable 300

Recorded printing expense on account.

Recorded March salaries expense.

Printing Expense

Recorded March travel expense.

Salaries Expense

Recorded revenue on account.

Accounts Receivable

Collected $1,200 from Kim Mitchell on account.

Issued additional shares of capital stock.

Cash

Cash

PROBLEM 3.7B

50 Minutes, Strong

Current Yr.

General Journal

AHUNA, INC.

Cash 700

15 200

Cash 200

Cooking Supplies

Purchased cooking supplies with cash.

Accounts Payable

Paid $200 of outstanding account payable.

b.

Cash

Mar. 1 bal. 5,700 Mar. 11 700 Mar. 1 bal. 1,800 Mar. 3 1,200

Cooking Supplies Accounts Payable

Mar. 1 bal. 800 Mar. 15 200 Mar. 1 bal. 300

Mar. 11 700 Mar. 31 300

Mar. 31 bal. 1,500 Mar. 31 bal. 400

Accounts Receivable

PROBLEM 3.7B

AHUNA, INC. (continued)

Mar. 3 1,200 Mar. 15 200 Mar. 24 6,200

Mar. 31 bal. 8,700 Mar. 31 bal. 6,800

c.

8,700$

6,800

1,500

400$

d.

The company has not paid the dividends it previously declared as evidenced by the $500

PROBLEM 3.7B

AHUNA, INC. (concluded)

Trial Balance

Cash

AHUNA, INC.

March 31, Current Year

Accounts receivable

Cooking supplies

Accounts payable

Retained earnings

Printing expense

Travel expense

Salaries expense

Client revenue

Capital stock

Dividends payable

Dividends

Net Total

Total

Owners‘

Error Income Assets Liabilities Equity

NE UNE U

NE O O NE

PROBLEM 3.8B

10 Minutes, Difficult

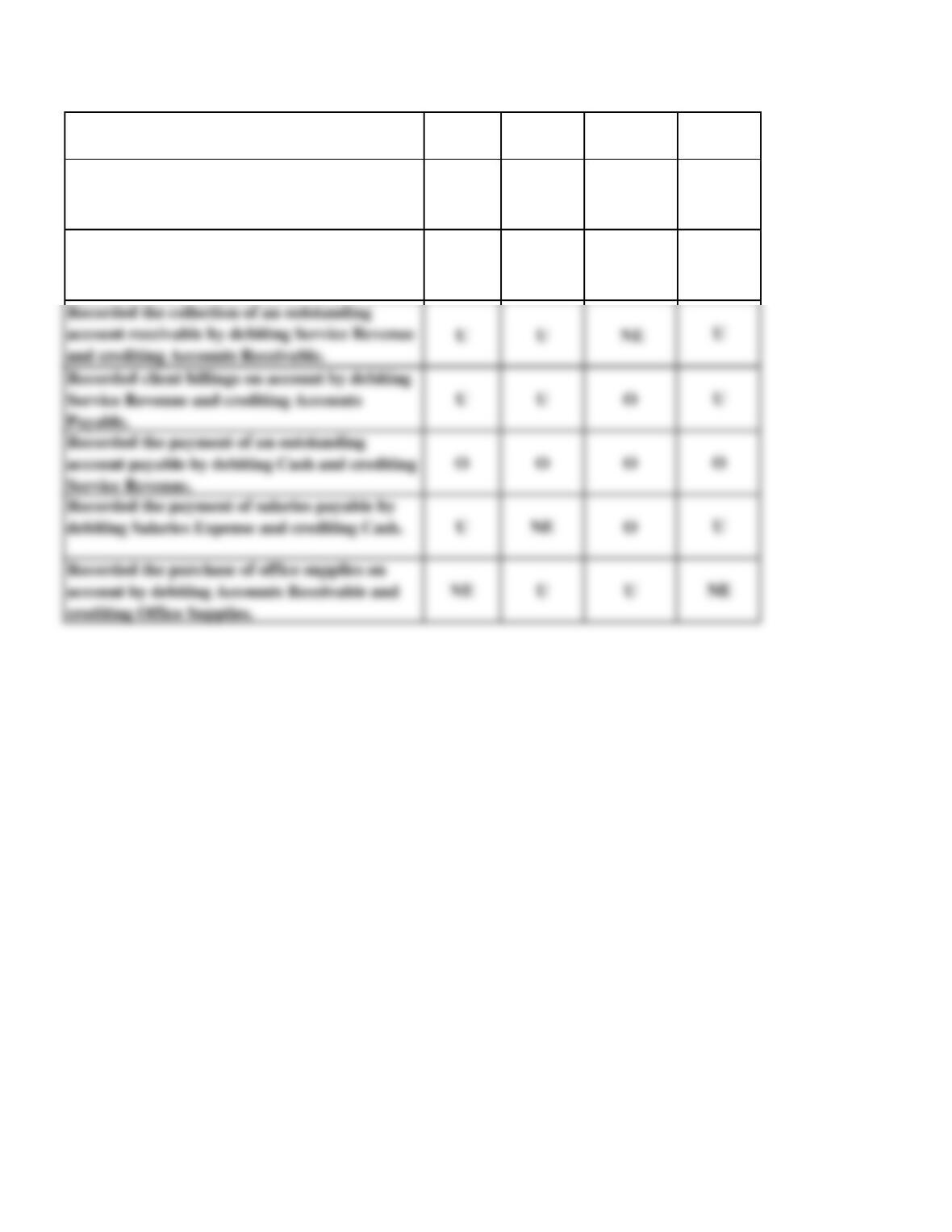

Recorded the issuance of capital stock by

debiting Capital Stock and crediting Cash.

BLIND RIVER, INC.

Recorded the payment of an account payable by

debiting Cash and crediting Accounts Payable.

a.

b.

c.

SOLUTIONS TO CRITICAL THINKING CASES

Periods that magazines are mailed to customers. The “goods” that a magazine publisher delivers

REVENUE RECOGNITION

Revenue is realized in the period that services are rendered to customers or goods are delivered to

customers. Using this principle as a guide, the three independent situations are analyzed below:

Period of flight. Airlines earn revenue by rendering a service—transportation—to their

Period furniture sold. In this case the furniture store delivers goods to its customers and acquires

CASE 3.1

15 Minutes, Medium

a.

(1)

(2)

(3)

(4)

(5)

b.

CASE 3.2

30 Minutes, Strong

It is not reasonable to report the entire $150,000 value of the equipment as an expense in the

The state-of-the-art printing equipment valued at $150,000 is an asset , not an expense. By

Charging weekly expenditures for business supplies directly to expense is reasonable, but

Income taxes on the Morris family’s salaries are personal expenses, not expenses of the

MEASURING INCOME

Discussion of “fairness and reasonableness” of income measurement policies:

Given that most revenue is received in cash and that credit terms are constant, recognizing

Morris’s salary of $60,000 is “fair and reasonable” because it has been agreed upon by both

ETHICS, FRAUD & CORPORATE GOVERNANCE

It is certainly unethical, and probably illegal, for Ed Grimm‘s boss to demand that Ed knowingly

engage in fraudulent reporting activities in order to retain his job. Ed may have been told that he would

be insulated from any responsibility or legal liability, but in reality, this may not be an acceptable

WHISTLE-BLOWING

CASE 3.3

5 Minutes, Easy

10 Minutes, Easy

A recent 10-K (see the MD&A) shows that sales of products to public sector clients has averaged

PC CONNECTION

CASE 3.4

INTERNET