Chapter 03 – The Accounting Cycle: End of the Period

Solution:

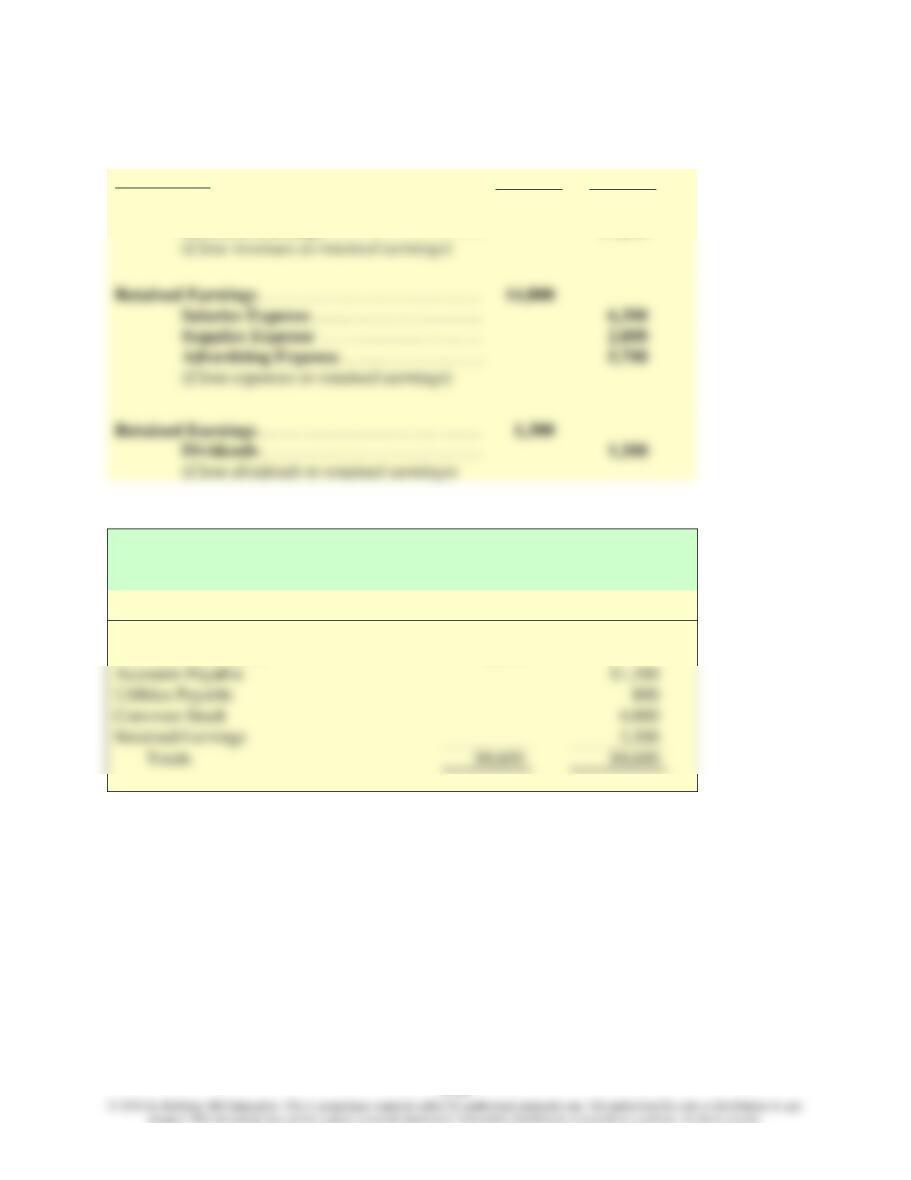

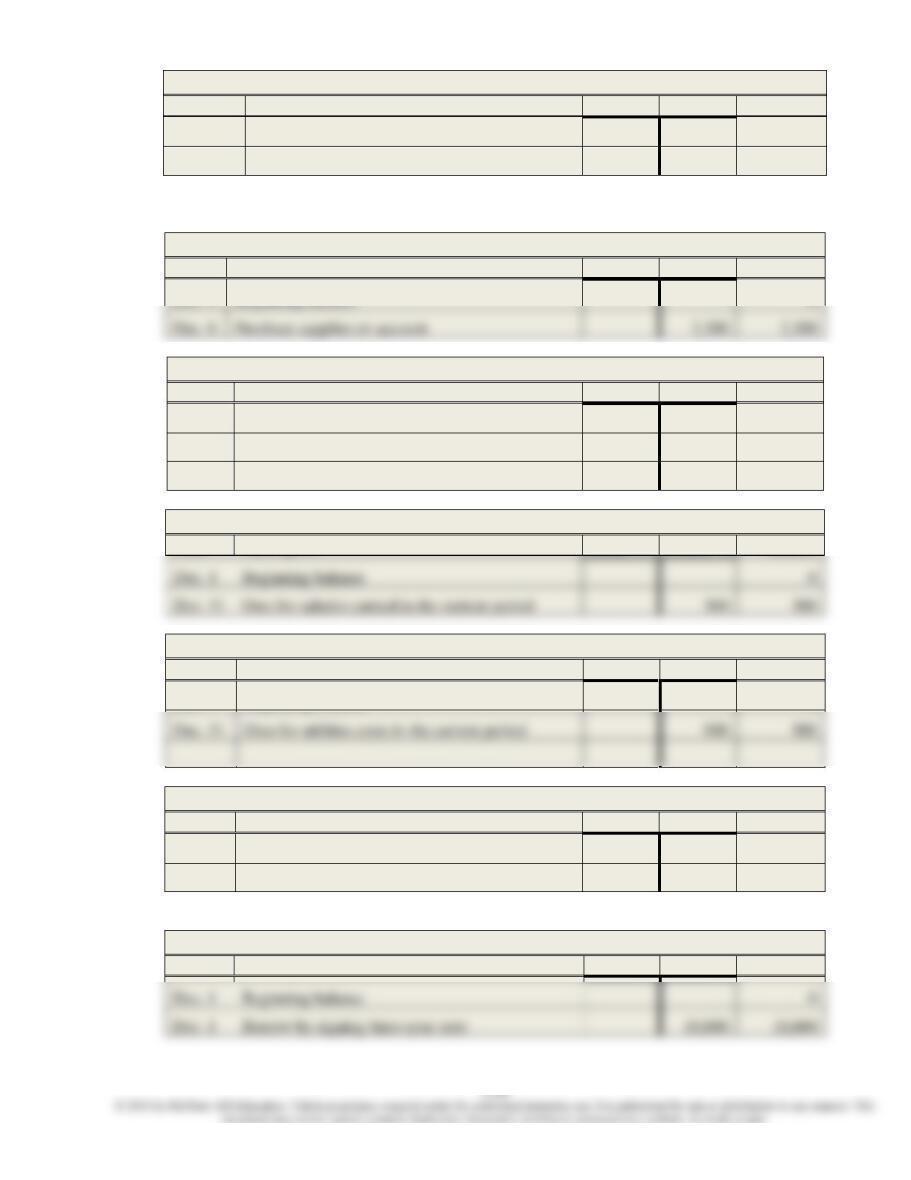

1. Closing entries

December 31

Debit

Credit

Service Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . .

17,200

Retained Earnings . . . . . . . . . . . . . . . . . .

17,200

Salaries Expense . . . . . . . . . . . . . . . . . . .

Supplies Expense . . . . . . . . . . . . . . . . . .

Advertising Expense . . . . . . . . . . . . . . . .

Retained Earnings . . . . . . . . . . . . . . . . . . . . . . . . .

2. Post-closing trial balance

Accounts Payable

Utilities Payable

Common Stock

Retained Earnings

3. The balance of retained earnings increases by $1,100 from the adjusted trial balance to the

post-closing trial balance. The balance increases by the amount of net income ($2,400) and

decreases by the amount of dividends ($1,300).

Swan Dance Academy

Post-Closing Trial Balance

December 31

Account Title

Debit

Credit

Cash

$3,400

Accounts Receivable

6,200

Chapter 03 – The Accounting Cycle: End of the Period

Key Points by Learning Objective

LO3-1 Understand when revenues and expenses are recorded.

The revenue recognition principle states that we record revenue in the period in which we

LO3-2 Distinguish between accrual-basis and cash-basis accounting.

The difference between accrual-basis accounting and cash-basis accounting is timing. Under

LO3-3 Demonstrate the purposes and recording of adjusting entries.

Adjusting entries are a necessary part of accrual-basis accounting. They help to update the

balances of assets, liabilities, revenues, and expenses at the end of the accounting period for

LO3-4 Post adjusting entries and prepare an adjusted trial balance.

LO3-5 Prepare financial statements using the adjusted trial balance.

Chapter 03 – The Accounting Cycle: End of the Period

LO3-6 Demonstrate the purposes and recording of closing entries.

Closing entries serve two purposes: (1) to transfer the balances of temporary accounts (revenues,

LO3-7 Post closing entries and prepare a post-closing trial balance.

Chapter 03 – The Accounting Cycle: End of the Period

Common Mistakes

Common Mistake

When recording the interest payable on a borrowed amount, students sometimes mistakenly

credit the liability associated with the principal amount (Notes Payable). We record interest

payable in a separate account (Interest Payable), to keep the balance owed for principal separate

from the balance owed for interest.

Common Mistake

Common Mistake

Students sometimes believe that closing entries are meant to reduce the balance of Retained

Earnings to zero. Retained Earnings is a permanent account, representing the accumulation of all

revenues, expenses, and dividends over the life of the company.

Students sometimes mistakenly include the Cash account in an adjusting entry. Typical adjusting

Chapter 03 – The Accounting Cycle: End of the Period

Decision Points

Question

Accounting Information

Analysis

Can the company

generate revenues that

Revenues and expenses

reported in the income

Revenues measure sales to customers

during the year. Expenses measure the

Question

Accounting Information

Analysis

The amounts reported

for revenues and

expenses represent

activity over what

period of time?

Income statement

Revenue and expense accounts

measure activity only for the current

reporting period (usually a month,

quarter, or year). At the end of each

period, they are closed and begin the

Chapter 03 – The Accounting Cycle: End of the Period

Career Corner

Career Corner

In practice, accountants do not prepare closing entries. Virtually all companies have accounting

software packages that automatically update the Retained Earnings account and move the

temporary accounts at the end of the year. Of course, accounting information systems go far

beyond automatic closing entries. In today’s competitive global environment, businesses demand

information systems that can eliminate redundant tasks and quickly gather, process, and

Chapter 03 – The Accounting Cycle: End of the Period

Ethical Dilemma

Ethical Dilemma

You have recently been employed by a large clothing retailer. One of your tasks is to help

prepare financial statements for external distribution. The company’s lender, National Savings &

Loan, requires that financial statements be prepared according to generally accepted accounting

principles (GAAP). During the months of November and December 2018, the company spent $1

million on a major TV advertising campaign. The $1 million included the costs of producing the

commercials as well as the broadcast time purchased to run them. Because the advertising will be

aired in 2018 only, you charge all the costs to advertising expense in 2018, in accordance with

requirements of GAAP.

The company’s chief financial officer (CFO), who hired you, asks you for a favor. Instead of

charging the costs to advertising expense, he asks you to set up an asset called prepaid

advertising and to wait until 2019 to record advertising expense. The CFO explains, “This ad

campaign has produced significant sales in 2018, but I think it will continue to bring in

customers throughout 2019. By recording the ad costs as an asset, we can match the cost of the

advertising with the additional sales in 2019. Besides, if we expense the advertising in 2018, we

will show an operating loss in our income statement. The bank requires that we continue to show

profits in order to maintain our loan in good standing. Failure to remain in good standing could

mean we’d have to lay off some of our recent hires.” As an employee, should you knowingly

record advertising costs incorrectly if asked to do so by your superior? Does your answer change

if you believe that misreporting will save employee jobs?

Key Issues

• Recording all advertising expense in 2018 (instead of delaying a portion until 2019) has

the effect of reducing net income.

• Since the bank requires the company to maintain profitability, recording all advertising

expenses in 2018 causes the company to lose good standing.

• Strictly following the rules of accounting vs. the use of discretion

• What is the role of an employee? Do the right thing or do what your boss tells you?

Option 1: Expense advertising costs immediately per GAAP

• GAAP guidelines are in place for accountants to follow, and the correct action is to

expense the advertising costs in the current year, regardless of what the CFO says and

regardless of the consequences.

Option 2: Establish a prepaid advertising account to delay the recognition of some expenses

Chapter 03 – The Accounting Cycle: End of the Period

• Why do I have to be the employee to take on the burden of standing up to the CFO? Is

my job not to do as I am told?

• The CFO has a point. If we don’t set up the prepaid account, long-term ramifications

such as violating the debt covenant with the bank would not be good for the company.

Plus, this prepaid account is just a timing issue, as we will still eventually report all of the

expense related to advertising.

• Am I not simply protecting my fellow employees’ jobs by complying with the CFO’s

request?

Chapter 03 – The Accounting Cycle: End of the Period

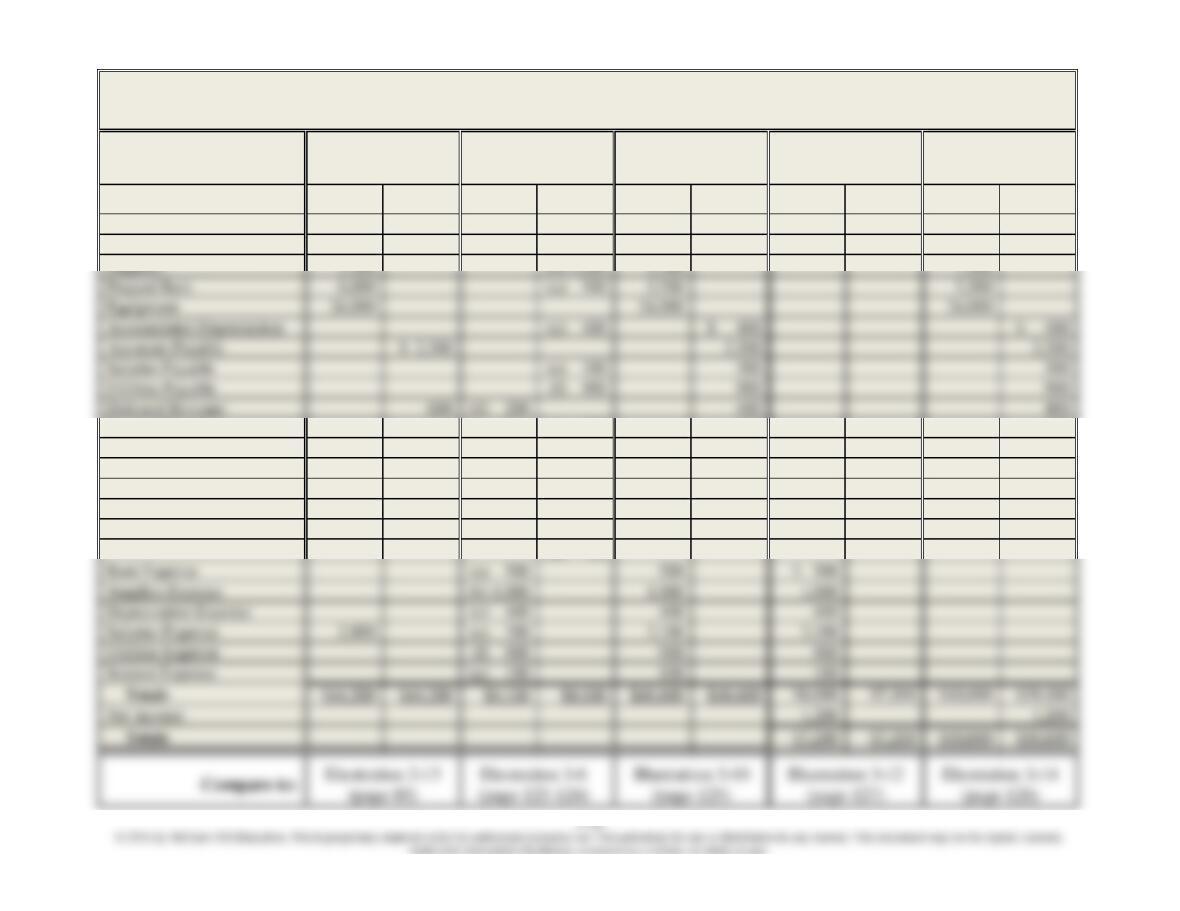

EAGLE GOLF ACADEMY

Worksheet

December 31

Unadjusted

Trial Balance

Adjusting

Entries

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Accounts

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Cash

$ 6,900

$ 6,900

$ 6,900

Accounts Receivable

2,000

(h) 700

2,700

2,700

Supplies

(b) 1,000

Prepaid Rent

Equipment

Accumulated Depreciation

Accounts Payable

Salaries Payable

300

300

Utilities Payable

Deferred Revenue

600

(d) 200

400

400

Interest Payable

(g) 100

100

100

Notes Payable

10,000

10,000

10,000

Common Stock

25,000

25,000

25,000

Retained Earnings

0

0

0

Dividends

200

200

200

Service Revenue

6,300

(d) 200

7,200

$7,200

(h) 700

Rent Expense

(a) 500

500

Supplies Expense

(b) 1,000

Depreciation Expense

(c) 400

Salaries Expense

2,800

(e) 300

3,100

3,100

Utilities Expense

900

900

Interest Expense

(g) 100

100

100

$4,100

$7,200

Net Income

$7,200

Chapter 03 – The Accounting Cycle: End of the Period

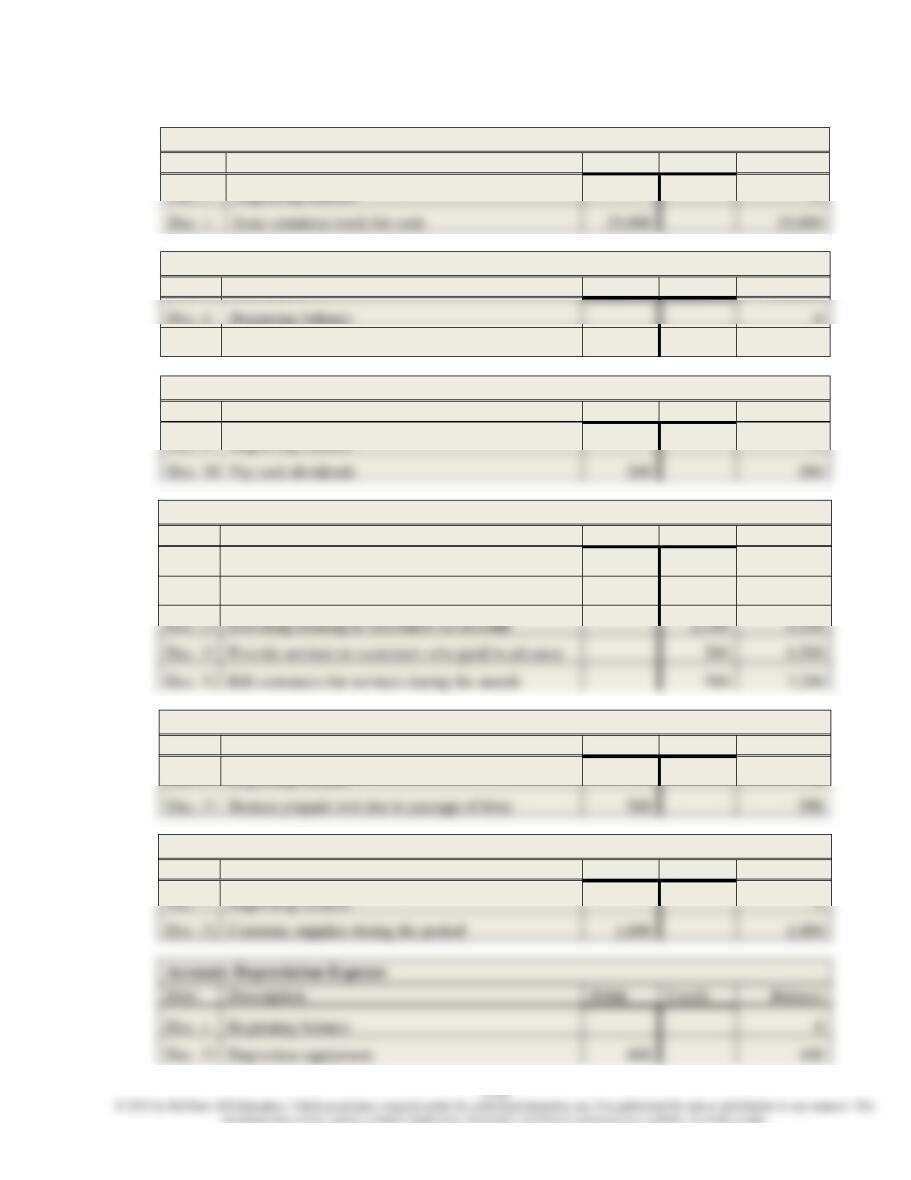

General Ledger of Eagle Golf Academy After Adjusting Entries

(Illustration 3-9, page 124)

ASSETS

Account: Cash

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Issue common stock for cash

25,000

25,000

Dec. 1

Borrow by signing three-year note

Dec. 1

Purchase equipment for cash

11,000

Dec. 1

Prepay rent with cash

6,000

5,000

Dec. 23

Receive cash in advance from customers

600

9,900

Dec. 28

Pay salaries to employees

2,800

7,100

Dec. 30

Pay cash dividends

200

6,900

Account: Accounts Receivable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 17

Provide services to customers on account

2,000

Dec. 31

Bill customers for services during the month

2,700

Account: Supplies

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 6

Purchase supplies on account

2,300

Dec. 31

Consume supplies during the current period

1,000

1,300

Account: Prepaid Rent

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Prepay rent with cash

6,000

6,000

Dec. 31

Reduce prepaid rent due to passage of time

500

5,500

Account: Equipment

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Purchase equipment for cash

24,000

24,000

Chapter 03 – The Accounting Cycle: End of the Period

Account: Accumulated Depreciation

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Depreciate equipment

400

400

LIABILITIES

Account: Accounts Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 6

Purchase supplies on account

Account: Deferred Revenue

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 23

Receive cash in advance from customers

600

600

Dec. 31

Provide services to customers who paid in advance

200

400

Account: Salaries Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

Dec. 31

Owe for salaries earned in the current period

Account: Utilities Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Owe for utilities costs in the current period

Account: Interest Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Owe for interest charges in the current period

100

100

Account: Notes Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

Dec. 1

Borrow by signing three-year note

Chapter 03 – The Accounting Cycle: End of the Period

STOCKHOLDERS’ EQUITY

Account: Common Stock

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Issue common stock for cash

Account: Retained Earnings

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Account: Dividends

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 30

Pay cash dividends

Account: Service Revenue

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 12

Providing training to customers for cash

4,300

4,300

Dec. 17

Providing training to customers on account

Dec. 31

Provide services to customers who paid in advance

6,500

Dec. 31

Bill customers for services during the month

Account: Rent Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Reduce prepaid rent due to passage of time

Account: Supplies Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Consume supplies during the period

Account: Depreciation Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Chapter 03 – The Accounting Cycle: End of the Period

Account: Salaries Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 6

Pay salaries to employees

Dec. 31

Owe for salaries earned in the current period

Account: Utilities Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Owe for utilities costs in the current period

Account: Interest Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Owe for interest charges in the current period