Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

185

Serial Problem, SP 3 (Continued)

Part 3

BUSINESS SOLUTIONS

Adjusted Trial Balance

December 31, 2017

Debit Credit

Cash ………………………………………………………………… $ 48,372

Accounts receivable …………………………………………. 5,668

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

186

Serial Problem, SP 3 (Continued)

Part 4

BUSINESS SOLUTIONS

Income Statement

For Three Months Ended December 31, 2017

Revenue

Computer services revenue ………………………………… $31,284

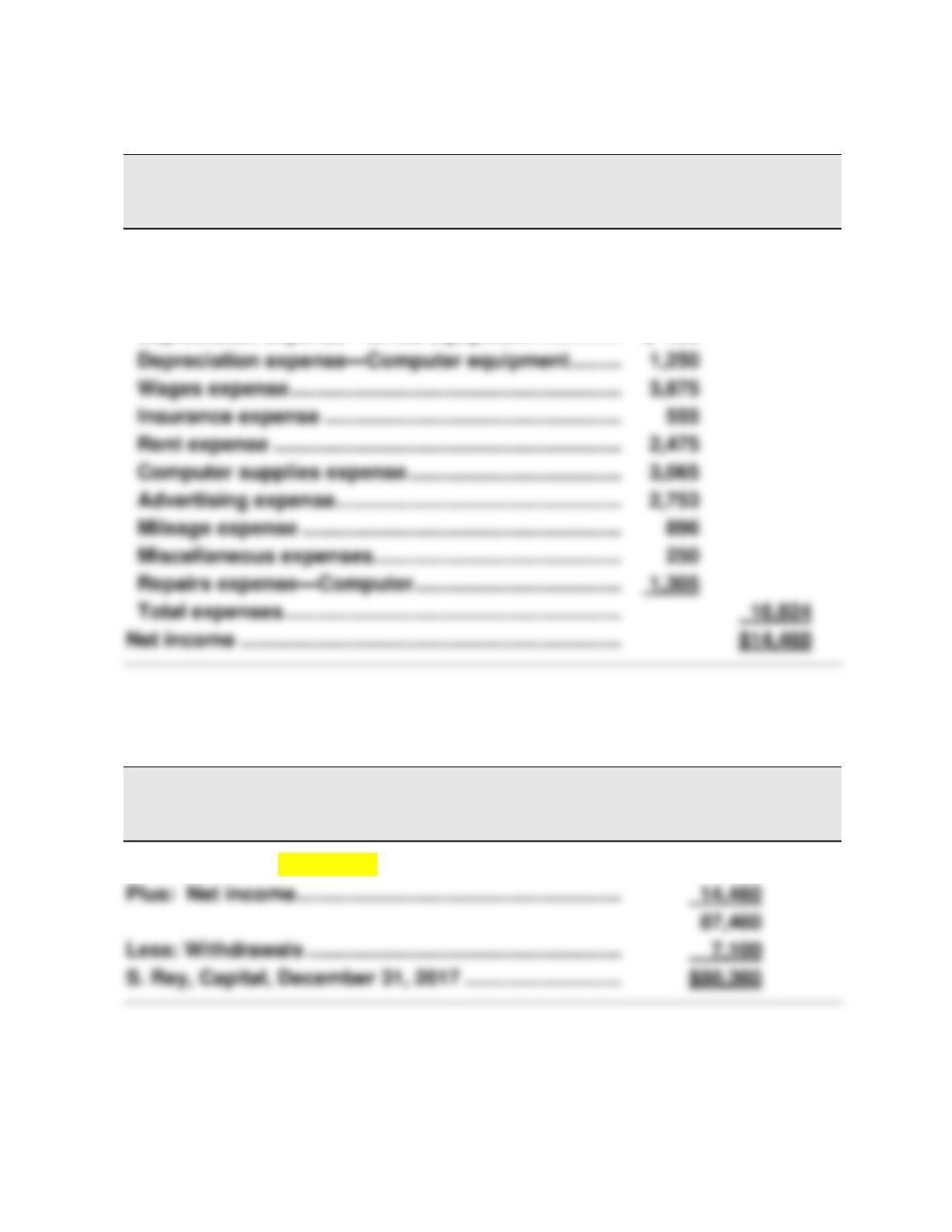

Expenses

Depreciation expense—Office equipment …………… $ 400

Part 5

BUSINESS SOLUTIONS

Statement of Owner’s Equity

For Three Months Ended December 31, 2017

S. Rey, Capital, October 1, 2017 ……………………………. $73,000

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

187

Serial Problem, SP 3 (Continued)

Part 6

BUSINESS SOLUTIONS

Balance Sheet

December 31, 2017

Assets

Cash ……………………………………………………………………… $ 48,372

Accounts receivable ……………………………………………… 5,668

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

Serial Problem, SP 3 (Continued)

[Note: Ledger includes all entries from prior three months. The Working Papers

shorten the solution by showing account balances as of November 30.]

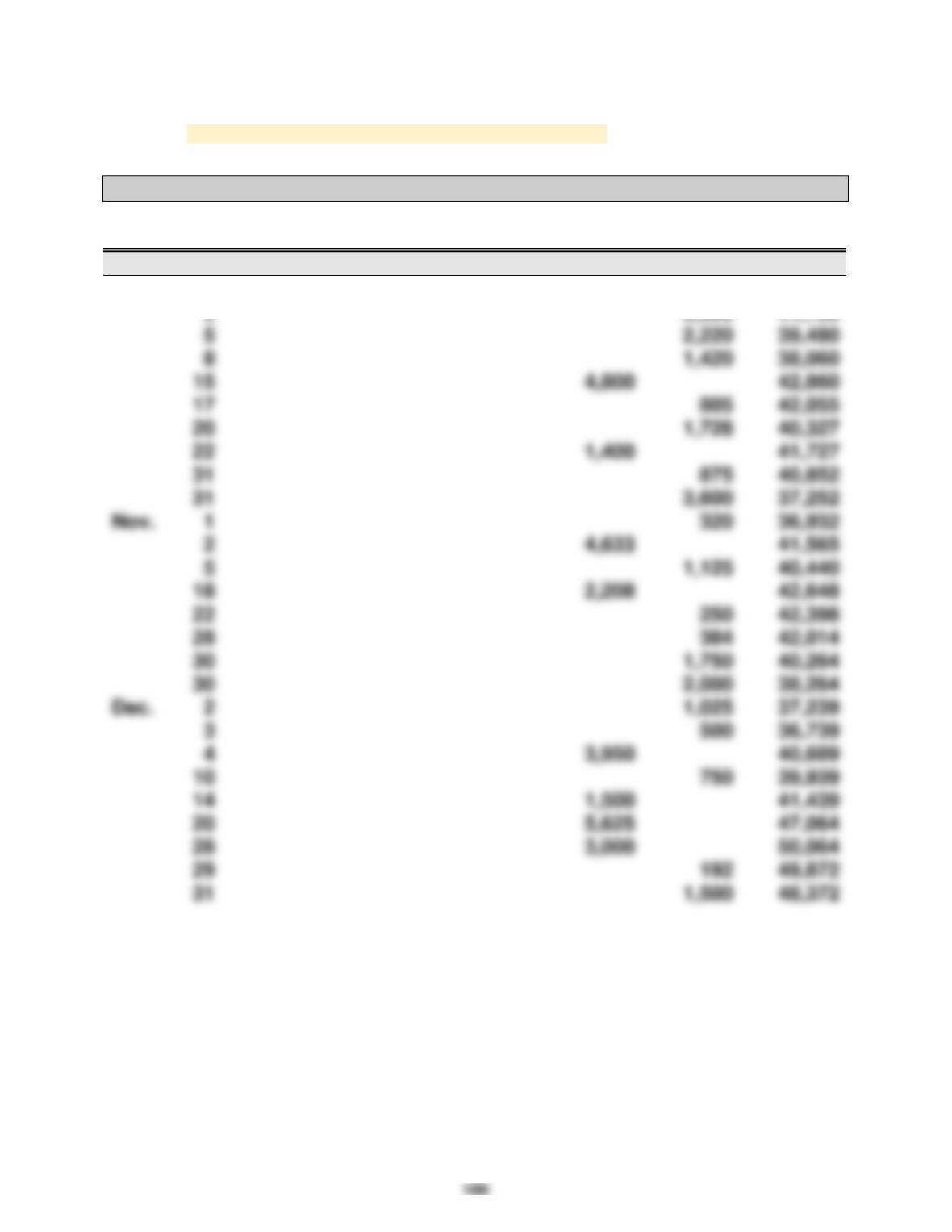

General Ledger

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

45,000

45,000

2

41,700

5

39,480

8

38,060

42,055

40,327

41,727

40,852

37,252

Nov.

1

36,932

2

41,565

5

40,440

42,648

42,398

42,014

40,264

38,264

Dec.

2

37,239

3

36,739

4

40,689

39,939

41,439

47,064

50,064

49,872

48,372

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

189

Serial Problem, SP 3 (Continued)

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

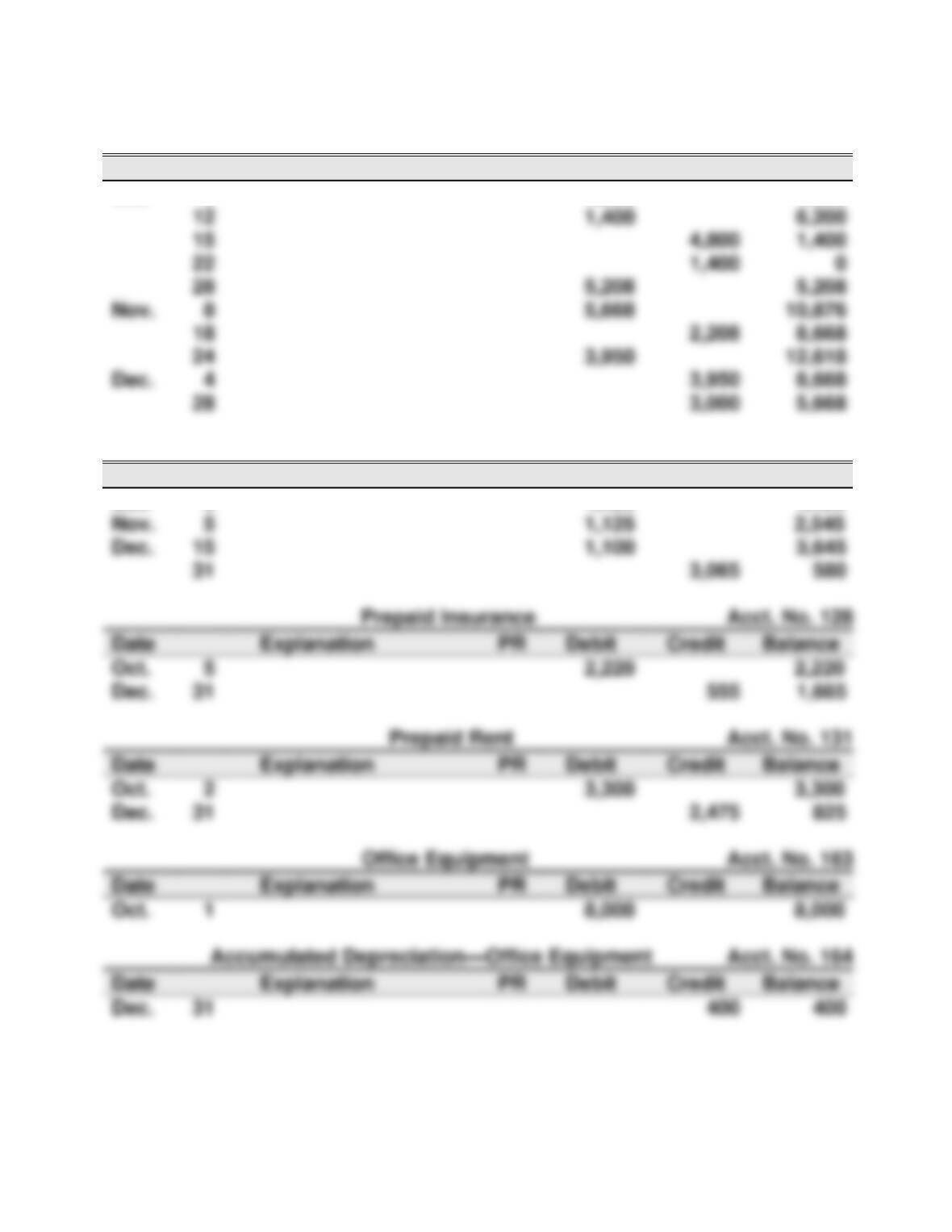

Computer Supplies

Acct. No. 126

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

Nov.

5

1,125

2,545

Dec.

1,100

3,645

3,065

Date

Explanation

PR

Debit

Credit

Balance

Oct.

5

2,220

2,220

Dec.

1,665

Date

Explanation

PR

Debit

Credit

Balance

Oct.

2

3,300

3,300

Dec.

2,475

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

8,000

8,000

Date

Explanation

PR

Debit

Credit

Balance

Dec.

1,400

6,200

4,800

1,400

1,400

5,208

5,208

Nov.

8

5,668

2,208

8,668

3,950

3,000

5,668

190

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

8

1,420

Dec.

1,100

Date

Explanation

PR

Debit

Credit

Balance

Dec.

Date

Explanation

PR

Debit

Credit

Balance

Dec.

1,500

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

Date

Explanation

PR

Debit

Credit

Balance

3,600

3,600

Nov.

2,000

5,600

Dec.

1,500

Date

Explanation

PR

Debit

Credit

Balance

Date

Explanation

PR

Debit

Credit

Balance

Dec.

1,250

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

191

Serial Problem, SP 3 (Continued)

Computer Services Revenue

Acct. No. 403

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

Depreciation Expense—Office Equipment

Acct. No. 612

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

Acct. No. 613

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

Acct. No. 623

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

Nov.

30

1,750

2,625

Dec.

10

31

Acct. No. 637

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

28

5,208

Nov.

2

4,633

8

5,668

24

3,950

Dec.

20

5,625

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

192

Serial Problem, SP 3 (Concluded)

Rent Expense

Acct. No. 640

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

2,475

2,475

Computer Supplies Expense

Acct. No. 652

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

3,065

3,065

Acct. No. 655

Date

Explanation

PR

Debit

Credit

Balance

20

1,728

1,728

Dec.

1,025

2,753

Acct. No. 676

Date

Explanation

PR

Debit

Credit

Balance

Nov.

28

Dec.

29

Acct. No. 677

Date

Explanation

PR

Debit

Credit

Balance

Nov.

22

Acct. No. 684

Date

Explanation

PR

Debit

Credit

Balance

17

Dec.

1,305

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

193

Reporting in Action — BTN 3-1

1. The chapter states that the “revenue recognition principle requires that

2. Apple provides information on revenue recognition in its Note 1 titled

“Summary of Significant Accounting Policies.” It reports that “The

3. For fiscal year-end September 26, 2015, the profit margin is ($ millions):

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

Comparative Analysis — BTN 3-2

($ millions)

1. Apple

Current year, profit margin = $53,394 / $233,715 = 22.8%

2. Apple was more successful on the basis of profit margin in the current

Ethics Challenge — BTN 3-3

1. GAAP requires that annual deprecation be accumulated in a contra–

asset account, called Accumulated Depreciation. While property, plant,

2. One strength of Smith’s method would be the ease of preparing the

balance sheet. The property, plant, and equipment balance in the

3. While both approaches would lead to the same total assets on the

balance sheet, GAAP requires Boland’s approach. As a professional,

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

195

Communicating in Practice — BTN 3-4

Taking It to the Net — BTN 3-5

1. The Gap’s main brands (stores) are The Gap, Old Navy, and Banana

2. The Gap’s fiscal year–end is January 31, 2015. It appears that The Gap’s

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

196

Teamwork in Action — BTN 3-6

Note that there is no specific solution to this activity. Still, the presentation

of each expert team should reflect the following summary points:

Before Adjusting

Balance Sheet Income Statement

Type Account Account Adjusting Entry

Prepaid expenses Asset overstated Expense understated Dr. Expense

Cr. Asset*

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

197

Entrepreneurial Decision — BTN 3-7

1. a. To record the collection of cash from sale of the gift certificate in

advance of delivery of merchandise to the customer:

Cash …………………………………………………………… 300

2. Carrying less inventory would allow the company to save the costs of

3. If the company carries additional inventory, it can potentially sell more

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 3

198

Hitting the Road — BTN 3-8

There is no formal solution to this field activity. The instructor may wish to

Global View — BTN 3-9

1. Samsung (KRW in millions)

Current year, profit margin = ₩19,060,144/ ₩ 200,653,482 = 9.5%

2. Apple is slightly more successful on the basis of profit margin in the

current year relative to Google. However, Apple and Google are both