CHAPTER 3 The Adjusting Process

3-19

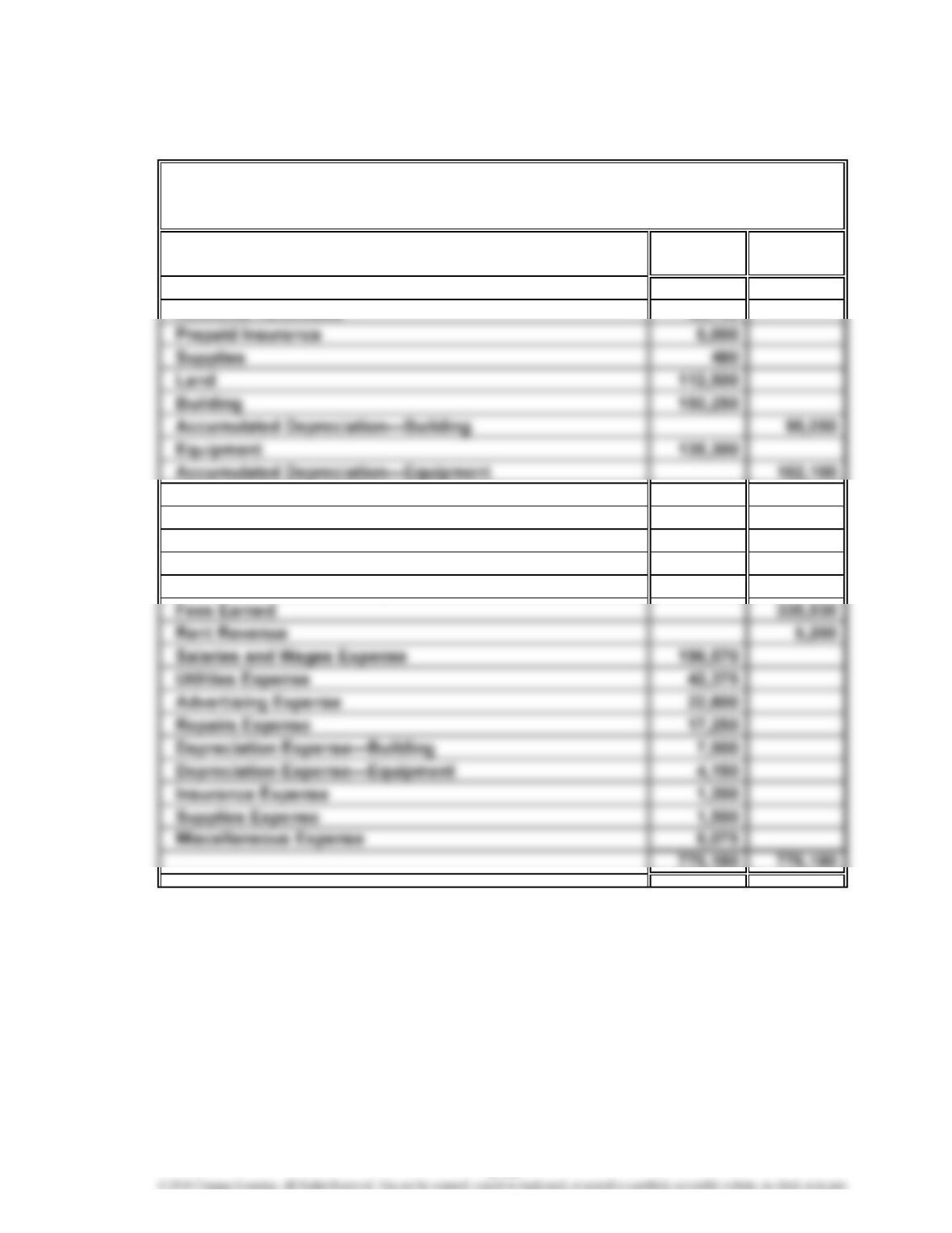

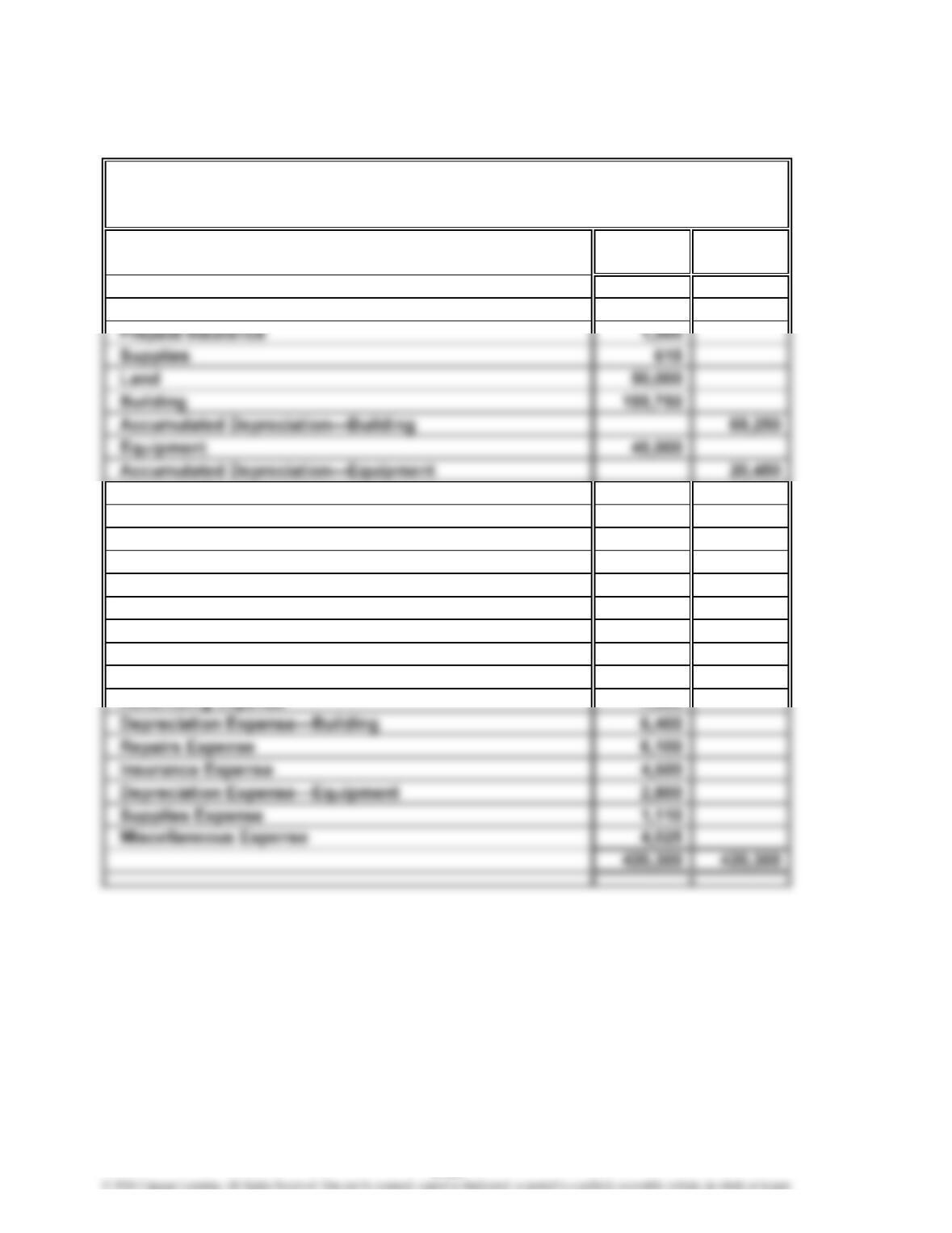

Prob. 3–5A (Concluded)

2.

Debit Credit

Balances Balances

Cash

7,500

Accounts Receivable 49,730

Accounts Payable 12,150

Unearned Rent 1,550

Salaries and Wages Payable 3,200

Marlene Rowland, Capital 221,000

Marlene Rowland, Drawing 15,000

August 31, 2016

ROWLAND COMPANY

Adjusted Trial Balance

CHAPTER 3 The Adjusting Process

3-20

Prob. 3–6A

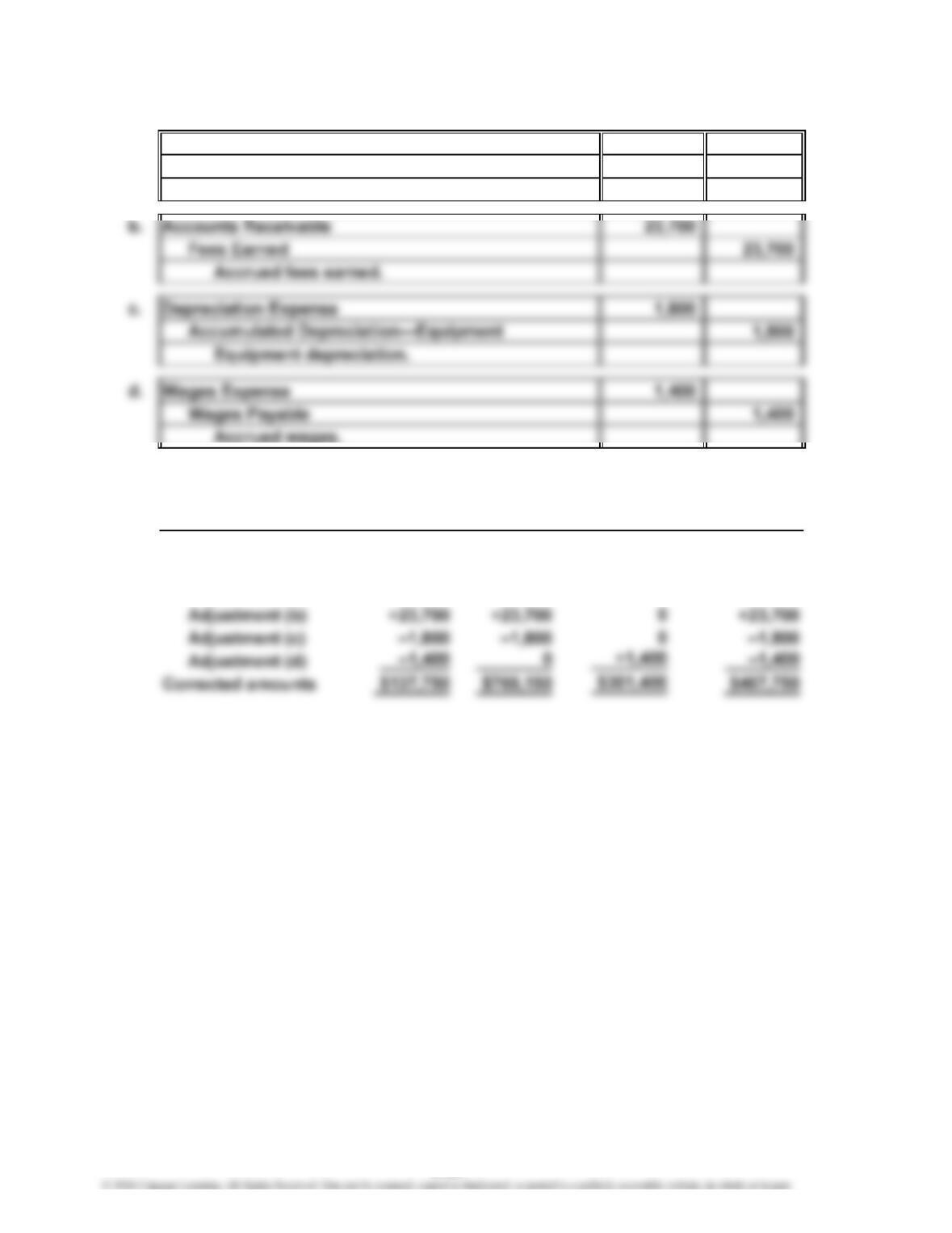

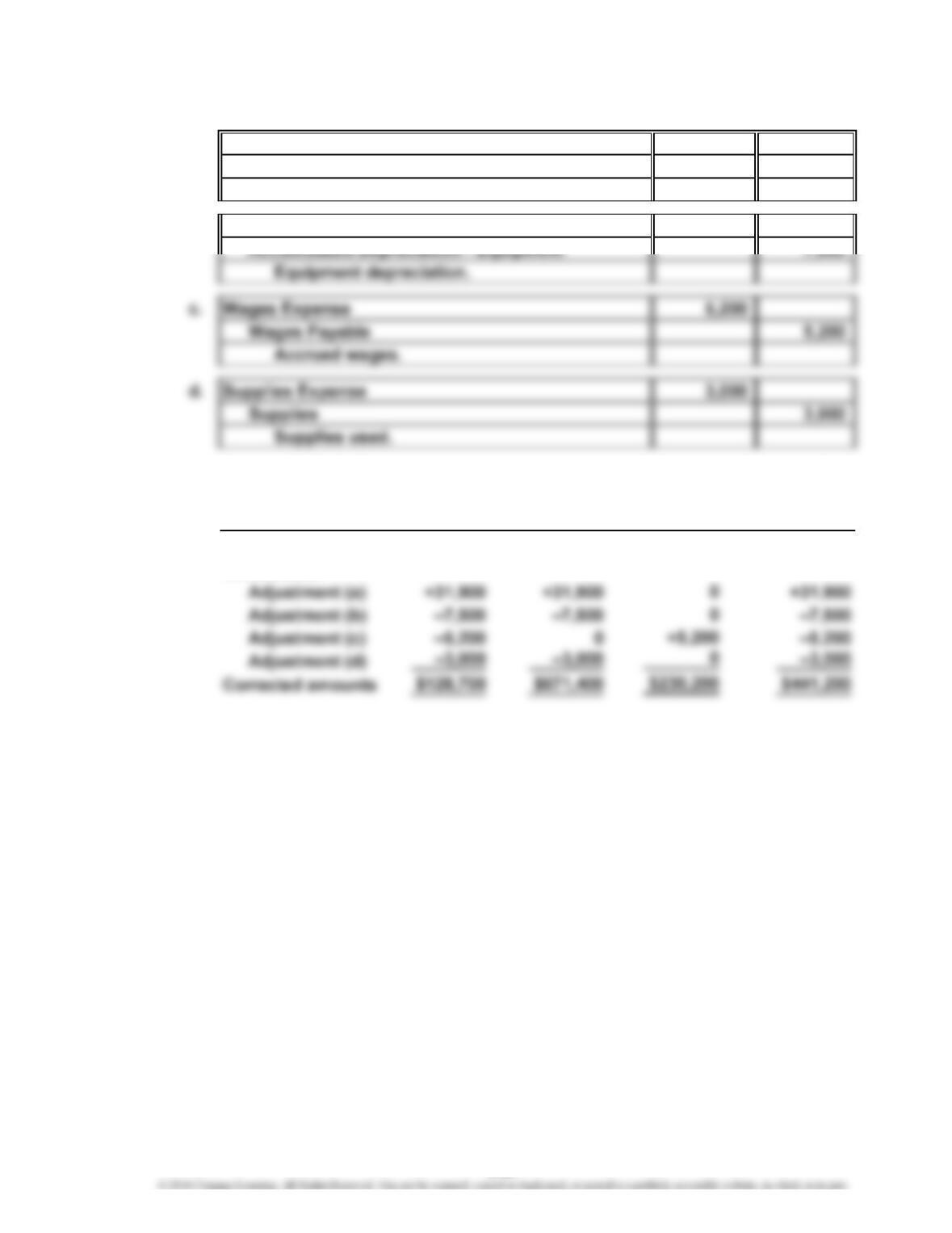

1. a. Supplies Expense

Supplies 2,750

Supplies used.

1,800

1,400

2. Total

Net Total Owner’s

Income Assets = + Equity

Reported amounts $120,000 $750,000 $450,000

Corrections:

Adjustment (a) –2,750 –2,750 –2,750

Total

Liabilities

$300,000

0

2,750

CHAPTER 3 The Adjusting Process

3-21

Prob. 3–1B

1. a. Accounts Receivable 19,750

Fees Earned 19,750

Accrued fees earned.

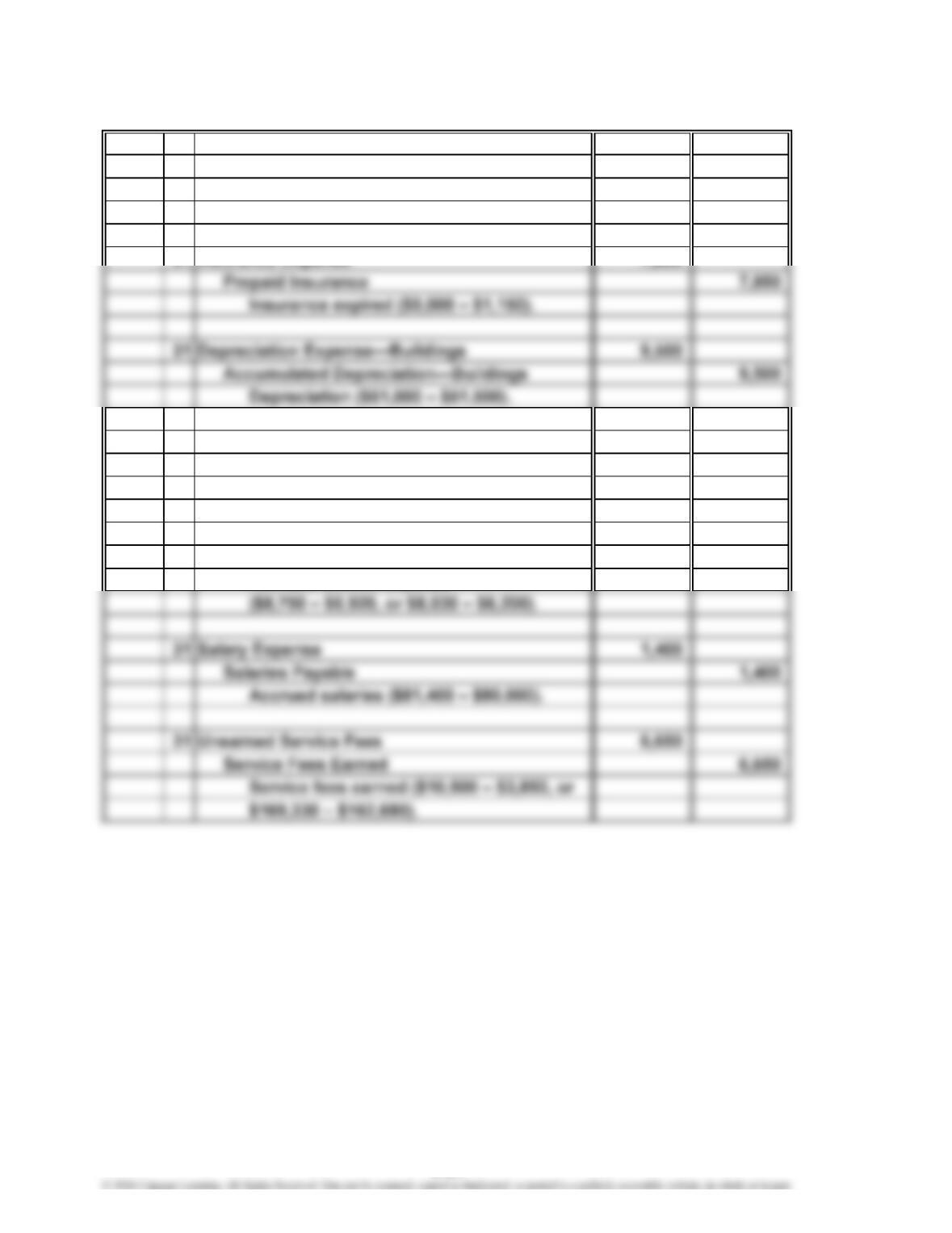

b. Supplies Expense 8,150

c. Wages Expense 2,700

Wages Payable 2,700

Accrued wages.

e. Depreciation Expense 3,200

Accumulated Depreciation—Equipment 3,200

Depreciation expense.

2. Adjusting entries are a planned part of the accounting process to update the

CHAPTER 3 The Adjusting Process

Prob. 3–2B

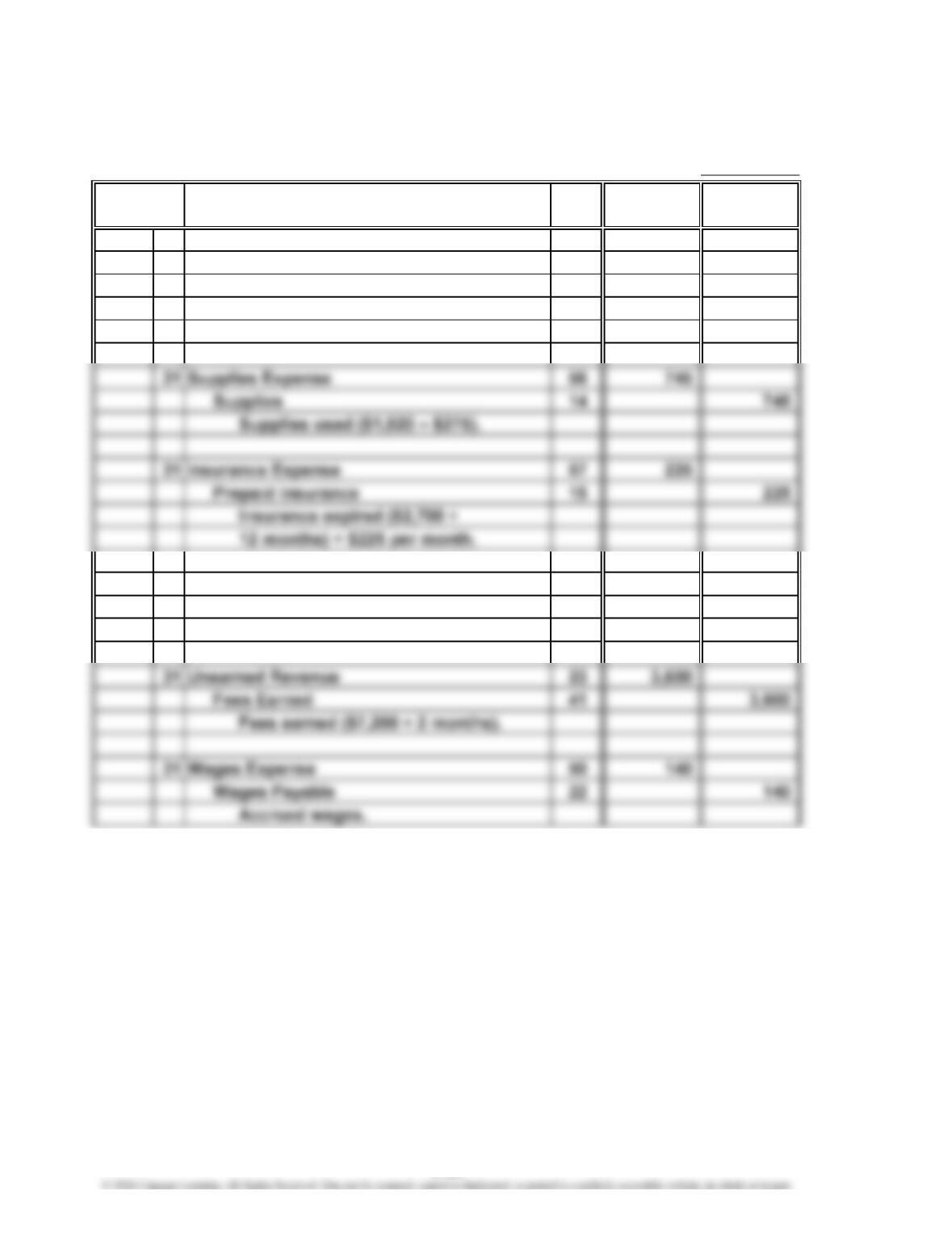

1. a. Supplies Expense 2,620

Supplies 2,620

Supplies used ($3,170 – $550).

b. Depreciation Expense 1,675

Accumulated Depreciation—Equipment 1,675

Depreciation for year.

2. Fees Earned would be understated by $6,000; Depreciation Expense would

3. Accumulated Depreciation—Equipment would be understated by $1,675; total

assets would be overstated by $1,675; Unearned Fees would be overstated by

3-22

CHAPTER 3 The Adjusting Process

3-23

Prob. 3–3B

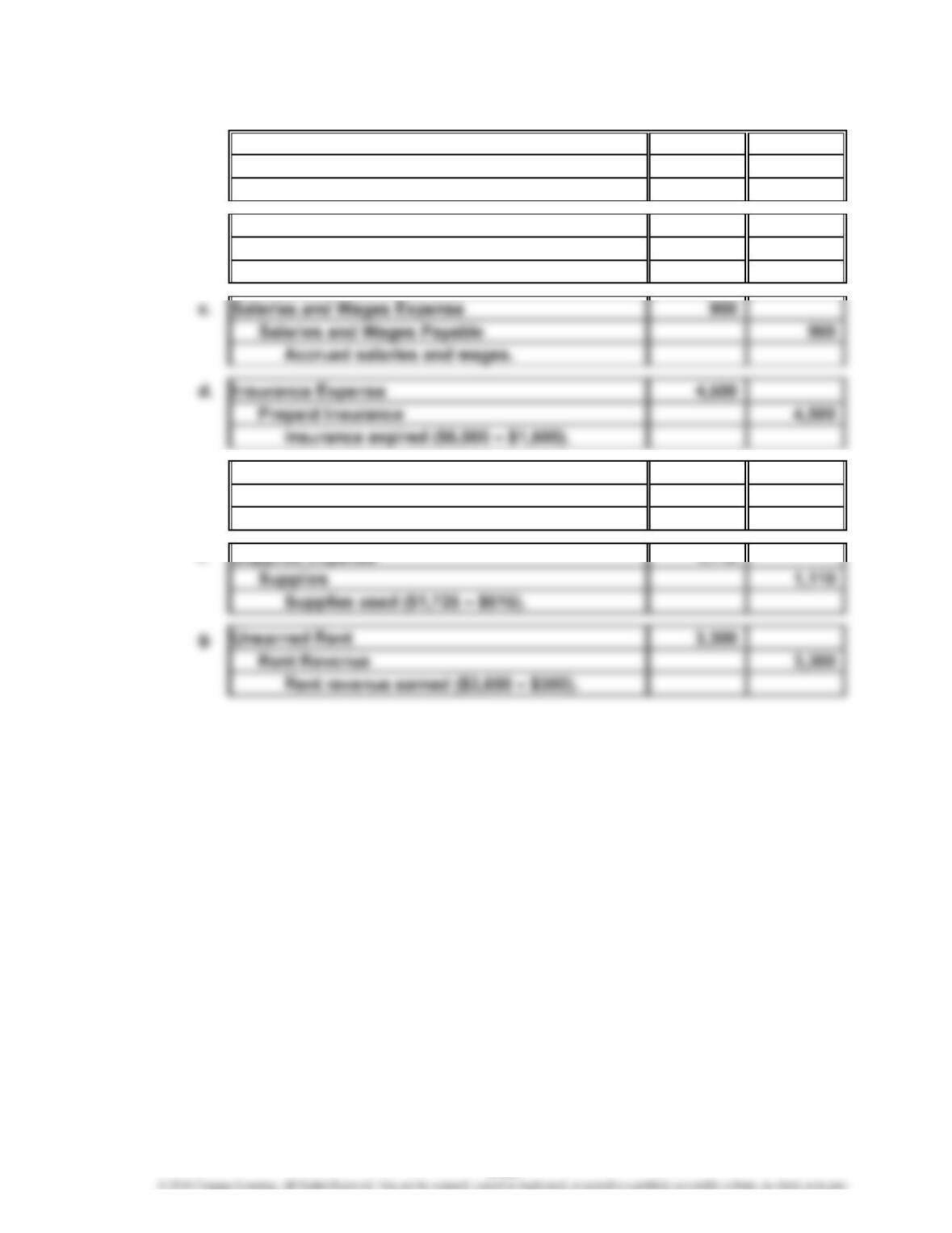

1. a. Supplies Expense 5,820

Supplies 5,820

Supplies used ($7,200 – $1,380).

b. Accounts Receivable 3,900

d. Wages Expense 2,475

Wages Payable 2,475

Accrued wages.

2.

Revenues……………………

$305,800

Expenses……………………

261,800 ($157,800 + $55,000 + $42,000 + $7,000)

Revenues……………………

Expenses……………………

4. The effect of the adjusting entries on Diana Keck, Capital is the difference

CHAPTER 3 The Adjusting Process

3-24

Prob. 3–4B

2016

Mar. 31 Supplies Expense 4,025

Supplies 4,025

Supplies used ($6,200 – $2,175).

31 Insurance Expense 7,850

31

Depreciation Expense—Trucks

5,000

Accumulated Depreciation—Trucks 5,000

Depreciation ($17,000 – $12,000).

31 Utilities Expense 1,830

Accounts Payable 1,830

Accrued utilities expense

CHAPTER 3 The Adjusting Process

3-25

Prob. 3–5B

1. a.

Depreciation Expense—Building

6,400

Accumulated Depreciation—Building 6,400

Building depreciation.

b. Depreciation Expense—Equipment 2,800

Accumulated Depreciation—Equipment 2,800

Equipment depreciation.

Accrued salaries and wages.

e. Accounts Receivable 10,200

Fees Earned 10,200

Accrued fees earned.

Supplies used ($1,725 – $615).

Rent revenue earned ($3,600 – $300).

CHAPTER 3 The Adjusting Process

3-26

Prob. 3–5B (Concluded)

2.

Debit Credit

Balances Balances

Cash 10,200

Accounts Receivable 44,950

Accounts Payable 3,750

Unearned Rent 300

Salaries and Wages Payable 900

Joni Reece, Capital 153,550

Joni Reece, Drawing 8,000

Fees Earned 168,800

Rent Revenue 3,300

Salaries and Wages Expense 57,750

Utilities Expense 14,100

Advertising Expense 7,500

July 31, 2016

REECE FINANCIAL SERVICES CO.

Adjusted Trial Balance

CHAPTER 3 The Adjusting Process

3-27

Prob. 3–6B

1. a. Accounts Receivable

Fees Earned 31,900

Accrued fees earned.

b. Depreciation Expense

3,000

5,200

2. Total

Net Total Owner’s

Income Assets = + Equity

Reported amounts $112,500 $650,000 $425,000

Corrections:

31,900

7,500

Total

Liabilities

$225,000

CHAPTER 3 The Adjusting Process

3-28

1.

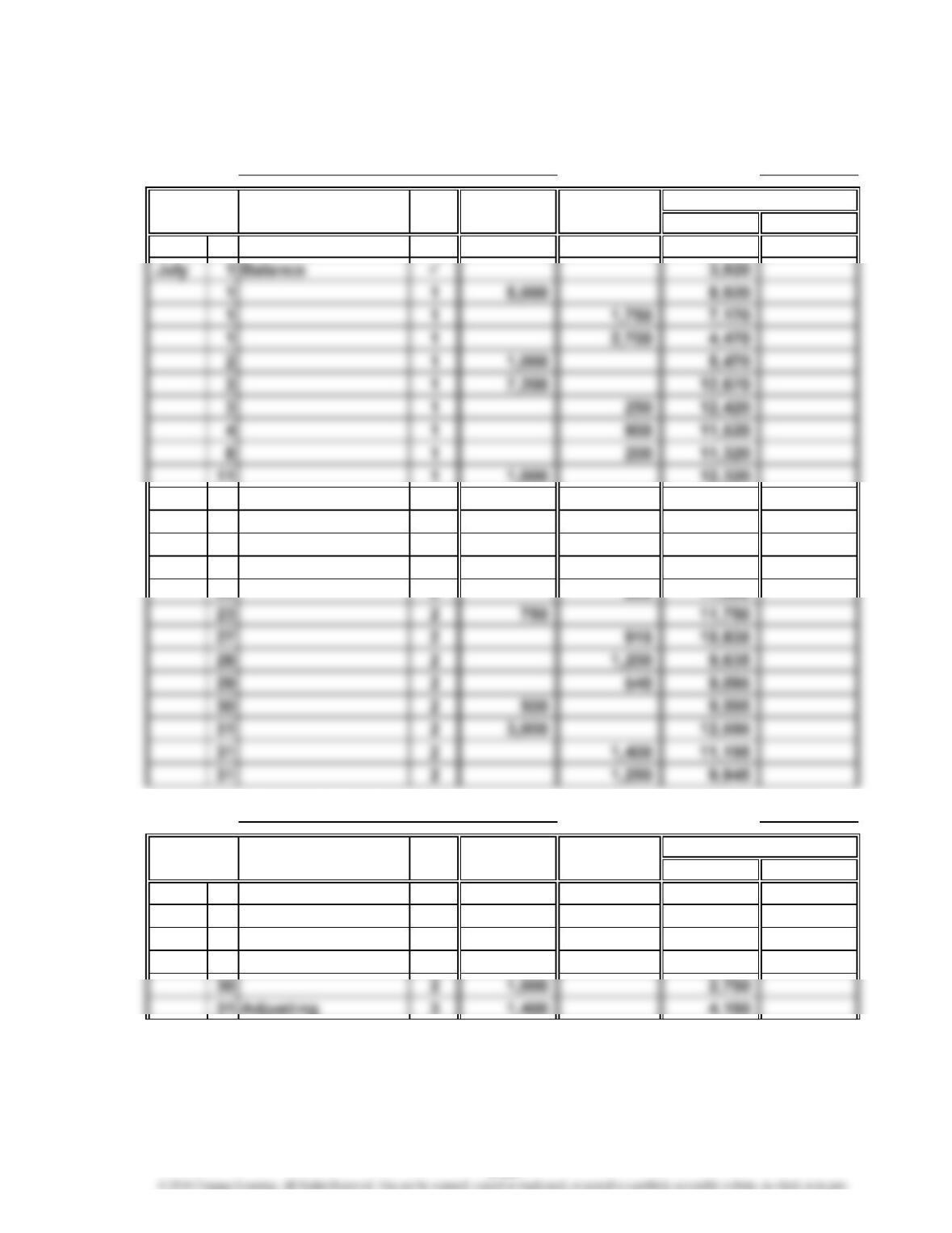

Page 3

Post.

Ref. Debit Credit

2016

July 31 Accounts Receivable 12 1,400

Fees Earned 41 1,400

Accrued fees earned (115 hrs. –

80 hrs.) × $40 = $1,400.

Supplies used ($1,020 – $275).

Insurance expired ($2,700 ÷

12 months) = $225 per month.

31 Depreciation Expense 58 50

Accum. Depr.—Office Equipment 18 50

Office equipment depreciation.

Fees earned ($7,200 ÷ 2 months).

Accrued wages.

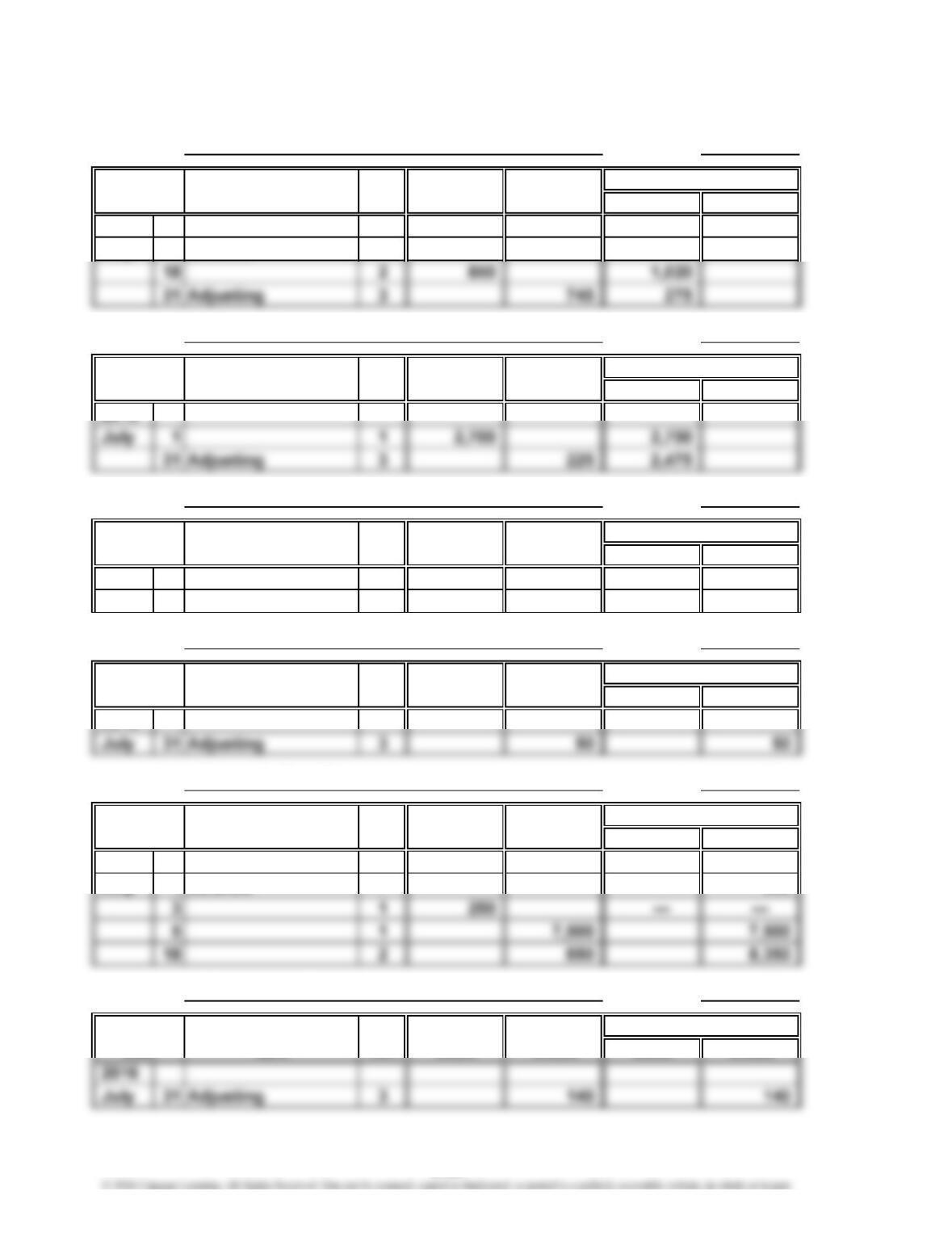

CONTINUING PROBLEM

Date

JOURNAL

Adjusting Entries

Description

CHAPTER 3 The Adjusting Process

3-29

Continuing Problem (Continued)

2.

Account No. 11

Post.

Item Ref. Debit Debit Credit

2016

250

900

200

1,750

2,700

13 111,620

14 110,420

16 22,000 12,420

21 211,800

800

915

1,400

1,200

Account No. 12

Post.

Item Ref. Debit Debit Credit

2016

July 1 Balance 1,000

2 1 — —

23 21,750 1,750

Balance

CreditDate

Account: Cash

700

Account: Accounts Receivable

1,200

620

Date Credit

Balance

1,000

CHAPTER 3 The Adjusting Process

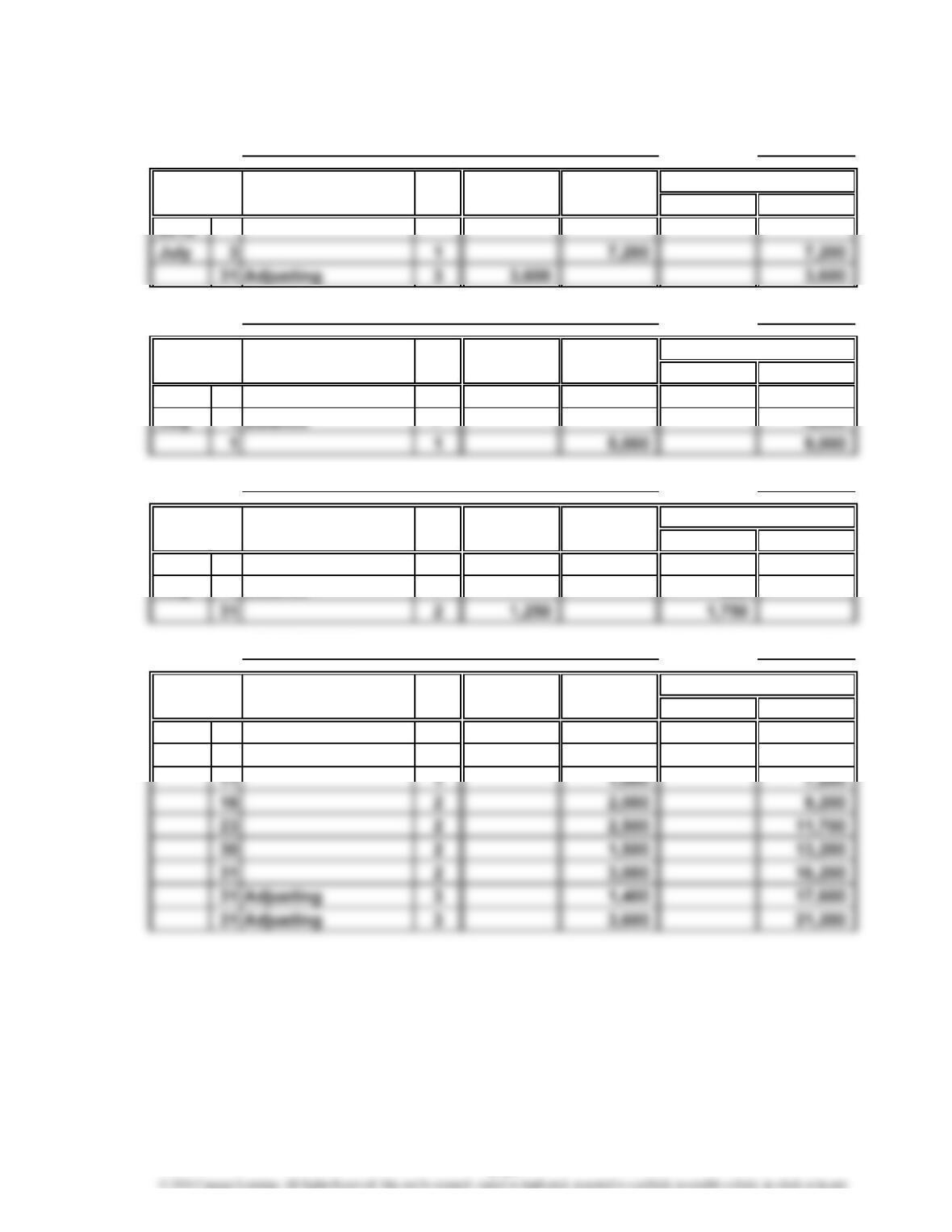

3-30

Continuing Problem (Continued)

Account No. 14

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 170

Account No. 15

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 17

Post.

Item Ref. Debit Credit Debit Credit

2016

July 5 1 7,500 7,500

Account No. 18

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 21

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 250

Account No. 22

Post.

Item Ref. Debit Credit Debit Credit

Balance

Date

Balance

Balance

Balance

Date

Account: Office Equipment

Date

Account:

Balance

Account: Accounts Payable

Date

Balance

Account: Wages Payable

Date

Accumulated Depreciation—Office Equipment

Account: Supplies

Account: Prepaid Insurance

Date

CHAPTER 3 The Adjusting Process

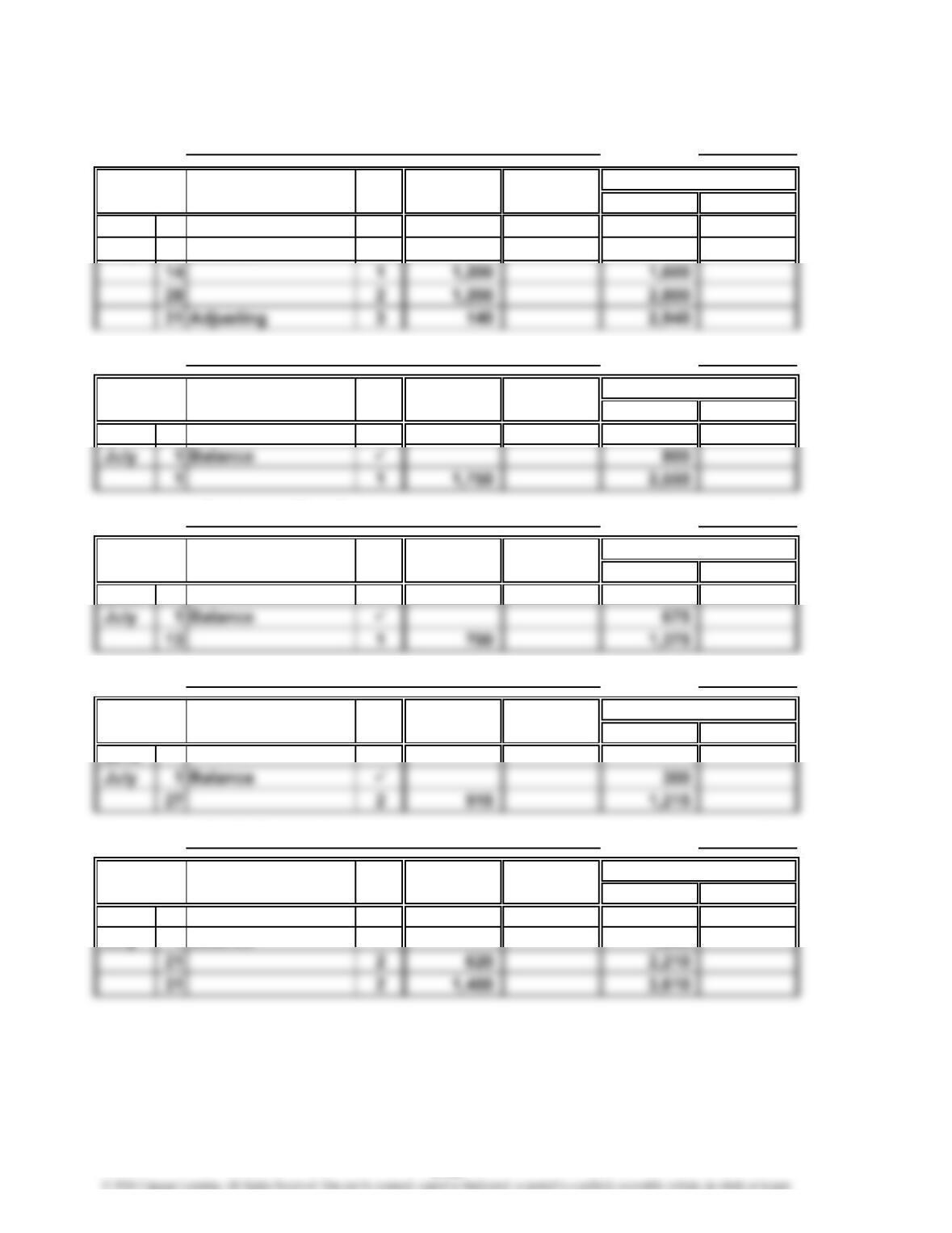

Continuing Problem (Continued)

Account No. 23

Post.

Item Ref. Debit Credit Debit Credit

Account No. 31

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 32

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 500

Account No. 41

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 6,200

Account: Unearned Revenue

Account: Peyton Smith, Capital

Balance

Balance

Date

Date

Account: Peyton Smith, Drawing

Balance

Date

Account: Fees Earned

Balance

Date

3-31

CHAPTER 3 The Adjusting Process

3-32

Continuing Problem (Continued)

Account No. 50

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 400

Account No. 51

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 52

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 53

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 54

Post.

Item Ref. Debit Credit Debit Credit

2016

July 1 Balance 1,590

Balance

Date

Balance

Balance

Balance

Date

Account: Utilities Expense

Date

Account:

Date

Balance

Account: Wages Expense

Music Expense

Account:

Office Rent Expense

Account: Equipment Rent Expense

Date

CHAPTER 3 The Adjusting Process

3-33

Continuing Problem (Continued)

Account No. 55

Post.

Item Ref. Debit Credit Debit Credit

Account No. 56

Post.

Item Ref. Debit Credit Debit Credit

2016

Account No. 57

Post.

Item Ref. Debit Credit Debit Credit

2016

July 31 Adjusting 3 225 225

Account No. 58

Post.

Item Ref. Debit Credit Debit Credit

Account: Insurance Expense

Account: Depreciation Expense

Date

Balance

Balance

Date

Balance

Account: Advertising Expense

Date

Balance

Account: Supplies Expense

Date

CHAPTER 3 The Adjusting Process

3-34

Continuing Problem (Concluded)

3.

Debit Credit

Balances Balances

Cash 9,945

Accounts Receivable 4,150

Supplies 275

Fees Earned 21,200

Music Expense 3,610

Wages Expense 2,940

Office Rent Expense 2,550

PS MUSIC

Adjusted Trial Balance

July 31, 2016

CHAPTER 3 The Adjusting Process

CP 3–1

It is acceptable for Daryl to prepare the financial statements for Squid Realty Co. on

an accrual basis. The revision of the financial statements to include the accrual of

CP 3–2

Revenue is normally recorded when the services are provided or when the

goods are delivered (title passes) to the buyer. By waiting until after the services

are provided, the expenses of providing the services can be more accurately

measured and matched against the related revenues. Also, at this point, the

provider of the services has a right to demand payment for the services if

payment hasn’t already been received.

Note to Instructors: The following points might also be worth discussing:

(1) The receipt of revenue from customers in advance of a flight represents

(2) At the end of the airline’s accounting period, it would have adjusting entries

related to such items as the following:

●Accrued wages for employees

CASES & PROJECTS

3-36

CP 3–3

a. There are several indications that adjusting entries were not recorded before

the financial statements were prepared, including:

1. All expenses on the income statement are identified as “paid” items and

not as “expenses.”

b. Likely accounts requiring adjustment include:

1. Accumulated Depreciation—Truck for depreciation expense.

3. Insurance (paid) expense for unexpired insurance.

5. Utilities accrued.

CP 3–4

Note to Instructors: The purpose of this activity is to familiarize students with

behaviors that are common in codes of conduct. In addition, this activity

addresses an actual ethical dilemma for students related to doing their

homework. Consider asking students to look up your school’s Student Code

of Conduct and discuss its implications for the behaviors described in this case.

An excerpt from one such Honor Code is shown below.

Students must share the responsibility for creating and maintaining an atmosphere

of honesty and integrity. Students should be aware that personal experience in

completing assigned work is essential to learning. Permitting others to prepare their