Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-1

CHAPTER 3

ADJUSTING ACCOUNTS FOR FINANCIAL STATEMENTS

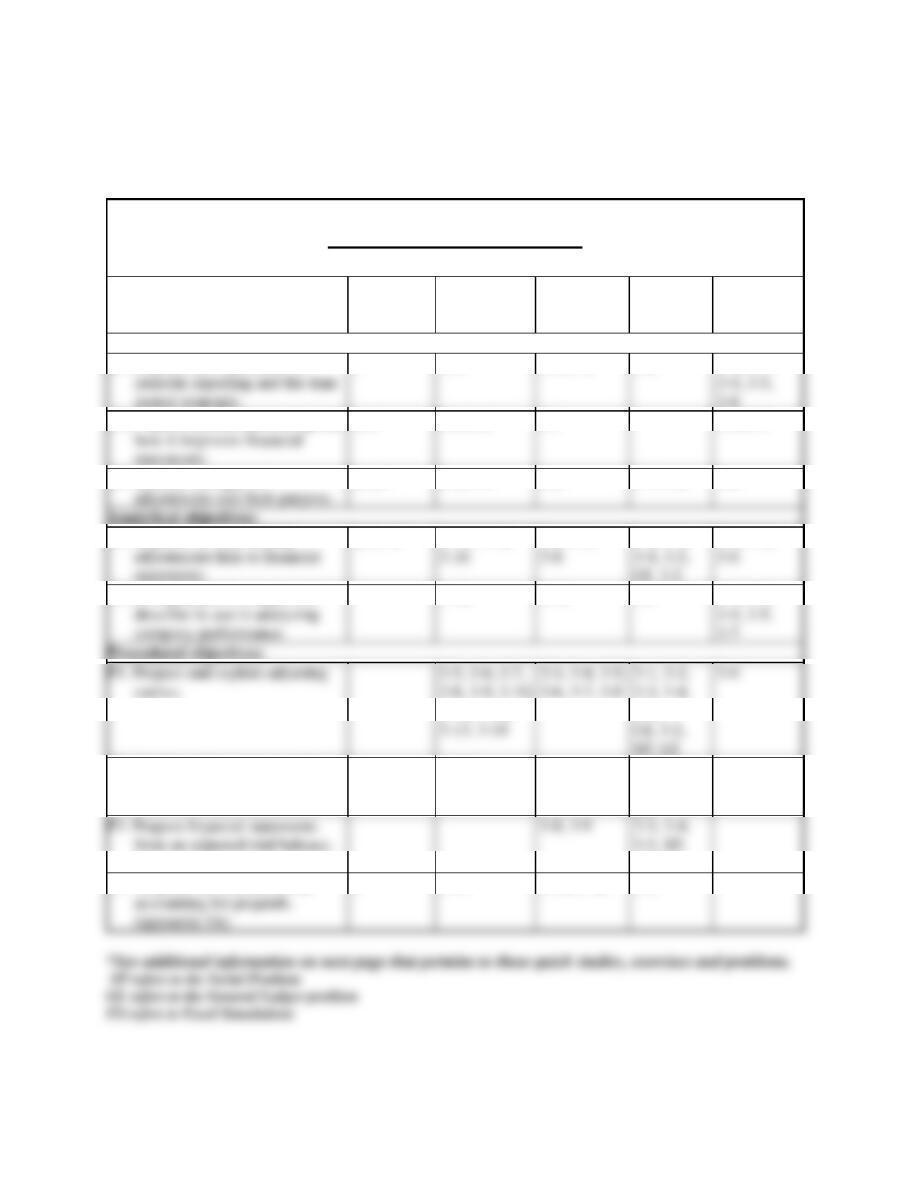

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain the importance of

3

3-1

3-3, 3-4

3-2

3-1, 3-3,

how it improves financial

C2. Explain accrual accounting and

1, 2

3-2, 3-9

3-1

3-1, 3-3

C3. Identify the types of

5, 6, 7

3-3, 3-4

3-2

3-1, 3-4

3-6

adjustments link to financial

3-16

3-8

3-4, 3-5,

GL 3-2

3-6

A1. Explain how accounting

4, 9, 10

3-13, 3-15,

3-4, 3-5,

3-2, 3-3,

3-1, 3-3,

3-7

A2. Compute profit margin and

3-18

3-10

3-5

3-1, 3-2,

3-13, 3-14

GL 3-2,

SP, ES

3-11, 3-12,

3-6,

P2. Explain and prepare an adjusted

trial balance.

3-17

3-3, 3-4,

GL 3-2, SP,

ES

P3. Prepare financial statements

from an adjusted trial balance.

3-8, 3-9

3-3, 3-4,

3-5, SP,

GL 3-2

accounting for prepaids.

P4A. Explain the alternatives in

8

3-19

3-11, 3-12

3-6

periodic reporting and the time

3-4, 3-5,

3-8

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises and

Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and Problems. It allows

instructors to monitor, promote, and assess student learning. It can be used in practice, homework, or exam mode.

Connect Insight

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto–graded and provide

instant feedback to the student.

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me

tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student.

Synopsis of Chapter Revisions

NEW opener—re:char and entrepreneurial assignment.

Streamlined accrual-basis vs cash-basis section.

New box on how accounting is used to clawback false gains.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-3

Chapter Outline

Notes

I. Timing and Reporting

A. The Accounting Period

To provide timely information, accounting systems prepare reports

at regular intervals.

1. Time-period principle assumes that an organization’s activities

can be divided into specific time periods such as a month, a

2. Annual reporting period:

a. Calendar year—January 1 to December 31.

b. Fiscal year—any twelve consecutive months or 52 weeks

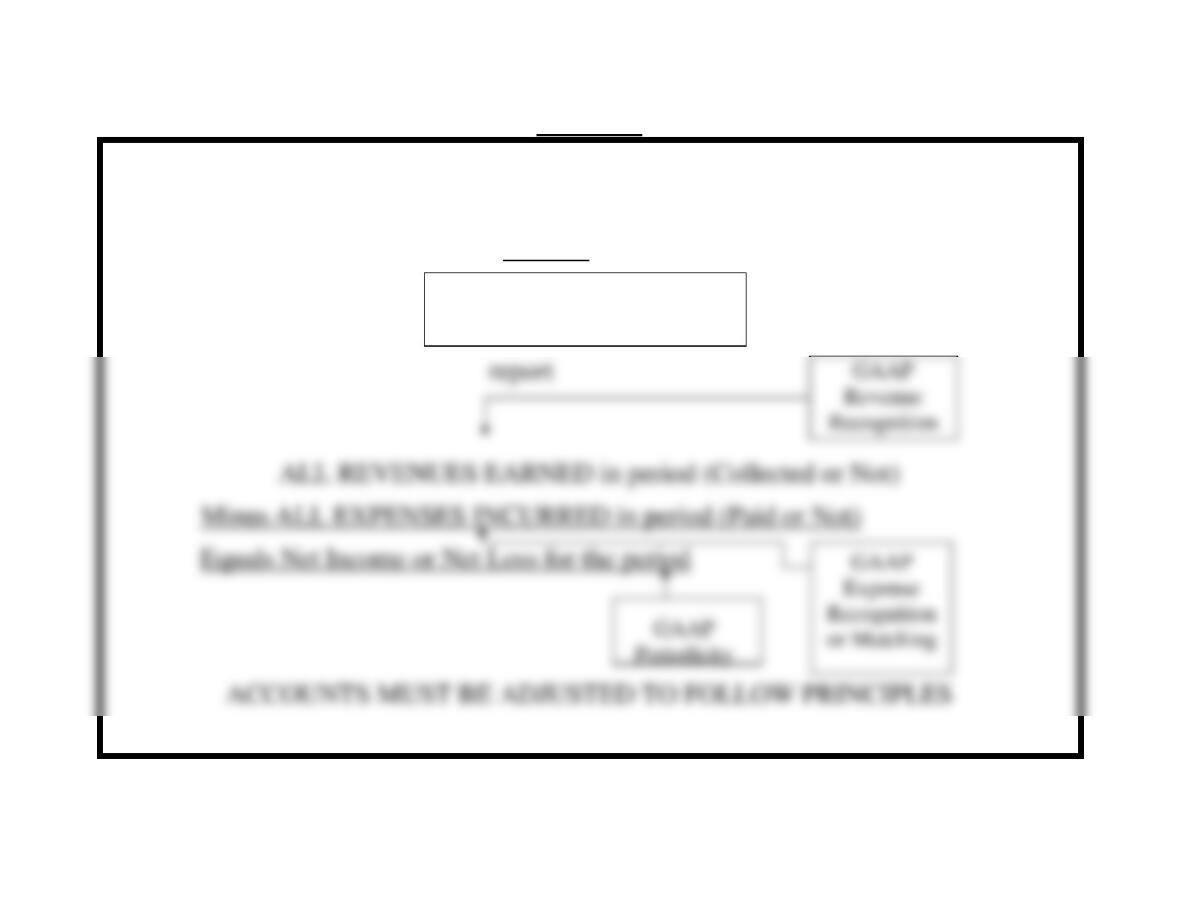

B. Accrual Basis versus Cash Basis

Accrual basis is consistent with GAAP. Improves

1. Accrual basis—applies adjustments so that revenues are

recognized when services and products are delivered and

2. Cash basis—revenues are recognized when cash is received

and expenses are recognized when cash is paid. Cash basis is

not consistent with GAAP.

C. Recognizing Revenues and Expenses

1. The revenue recognition principle requires revenue be

recorded when goods or services are provided to customers.

2. The expense recognition (or matching) principle aims to

record expenses in the same period as the revenues earned as a

result of these expenses.

II. Adjusting Accounts—An adjusting entry is recorded to bring an asset

or liability account balance to its proper amount. This entry also

updates the related expense or revenue account.

Adjustments are necessary for transactions that extend over more

than one period.

three-month quarter, a six-month interval, or a year for

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-4

Chapter Outline

Notes

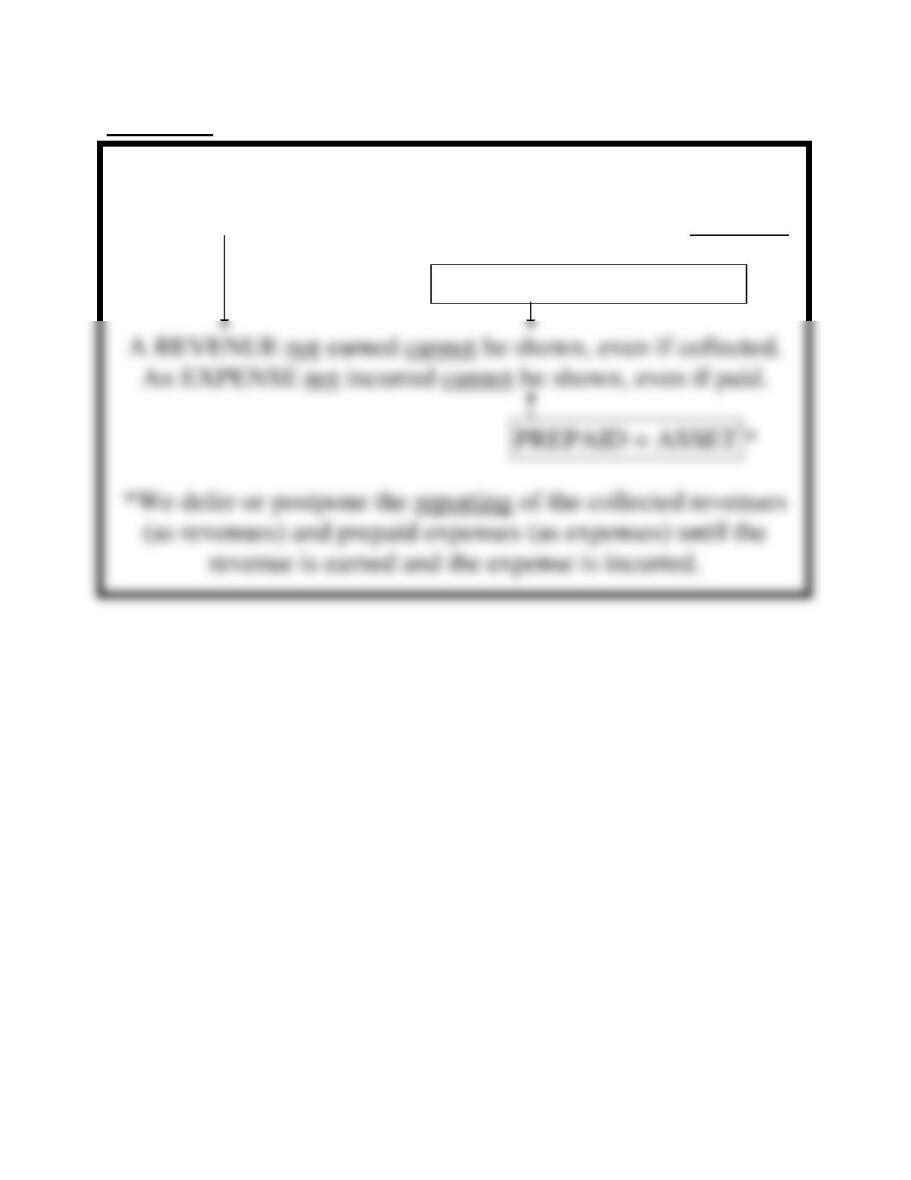

B. Adjusting Prepaid (Deferred) Expenses

1. Prepaid expenses (including depreciation) are assets paid for

expenses and decreasing (crediting) assets (with the exception

of depreciation on plant and equipment).

2. Common prepaid items are supplies, prepaid insurance,

prepaid rent and depreciation.

3. Adjusting entries for prepaids involve increasing (debiting)

1. Depreciation is the process of allocating the cost of plant

assets over their expected useful lives.

2. Adjusting entries for depreciation expense involve increasing

(debiting) expenses and increasing (crediting) a special

3. Book value is a term used to describe the asset less its contra-

asset (accumulated-depreciation).

D. Adjusting Unearned (Deferred) Revenues

(liabilities) become earned revenues (revenues).

1. Unearned revenues (also called deferred revenues) are

liabilities created by cash received in advance of providing

2. Adjusting entries for unearned revenues involve increasing

(crediting) revenues and decreasing (debiting) unearned

revenues.

E. Adjusting Accrued Expenses

increasing (debiting) expenses and increasing (crediting)

2. Common accrued expenses are salaries, interest, rent, and

taxes.

3. Adjusting entries for recording accrued expenses involve

called deferred expenses, are assets. As the assets are used,

their costs become expenses.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-5

Chapter Outline

Notes

F. Adjusting Accrued Revenues

2. Accrued revenues commonly result from partially completed

jobs or interest earned.

3. Adjusting entries for recording accrued revenues involve

increasing (debit) assets and increasing (credit) revenues. (The

asset is a “receivable.”)

G. Links to Financial Statements

Each adjusting entry affects one or more income statement

III. Trial Balance and Financial Statements

A. Adjusted Trial Balance

A list of accounts and balances prepared after adjusting entries are

recorded and posted to the ledger.

IV. Preparing Financial Statements—Prepare financial statements

directly from information in the adjusted trial balance. The following

preparation order shows the flow of information from one statement to

another:

A. Income Statement

B. Statement of Owner’s Equity

V. Decision Analysis—Profit Margin

A. Used to evaluate operating results by measuring the ratio of a

company’s net income to sales. Also called return on sales.

revenue.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-6

Chapter Outline

Notes

VI. Appendix 3A—Alternative Accounting for Prepayments

A. Prepaid expenses may originally be recorded with debits to

expense accounts instead of assets. If so, then adjusting entries

must transfer the cost of the unused portions from expense

If so, then adjusting entries must transfer the unearned portions

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-7

VISUAL #3-1

ACCRUAL BASIS ACCOUNTING

(Follows GAAP)

requires that the

Income Statement

(for a period)

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-8

VISUAL #3-2

DEFERRALS

The converse of statements in Visual #3-1 also applies.

Revenue not earned or expense not incurred results in Deferrals*

UNEARNED = LIABILITY *

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

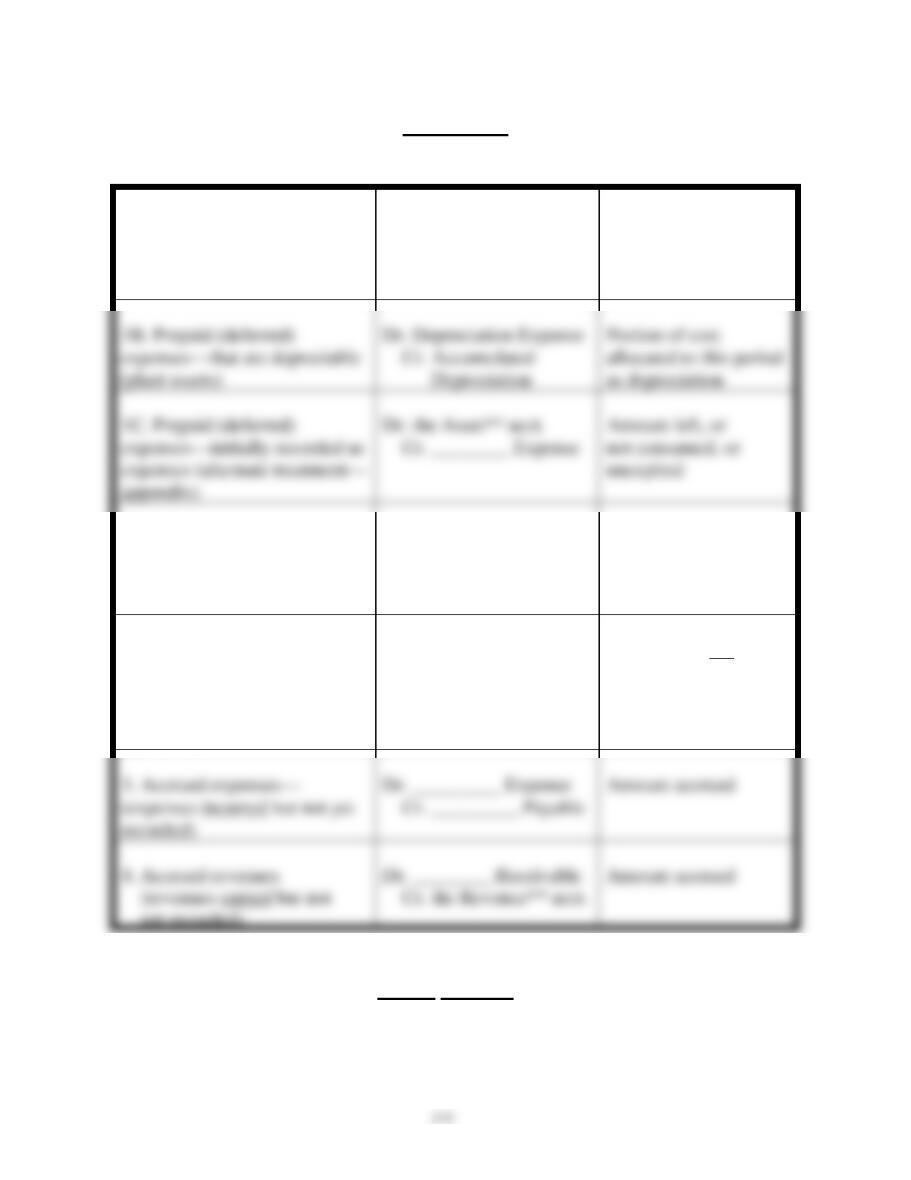

VISUAL #3-3

ADJUSTMENTS

TYPE

GENERALIZED*

ENTRY

AMOUNT

1A. Prepaid (deferred)

expenses—initially recorded as

assets

Dr. _________ Expense

Cr. the Asset* acct.

Amount used, or

consumed, or expired

1C. Prepaid (deferred)

appendix)

Dr. the Asset** acct.

Cr. ________ Expense

Amount left, or

not consumed, or

2A. Unearned revenues—

(revenue received in advance)

initially record as liability

(unearned account)

Dr. Unearned ________

Cr. the Revenue** acct.

Amount earned to date

2B. Unearned revenues—

(revenue received in advance)

initially recorded as a revenue

(alternate treatment—

appendix)

Dr. the Revenue** acct.

Cr. Unearned________

Amount still not

earned

3. Accrued expenses—

recorded)

Cr. _________ Payable

Amount accrued

4. Accrued revenues

Dr. ________ Receivable

Amount accrued

*Note: (1) Each adjustment affects a Balance Sheet Account and an Income

Statement Account and (2) CASH NEVER appears in an adjustment.

**Title or account name varies.

3-10

Chapter 3 Alternate Demonstration Problem – 1

On July 1, 2017, Howard M. Tenant, Inc., rents office space from John Q.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

Solution: Chapter 3 Alternate Demonstration Problem – 1

Tenant

Landlord

7/1/17

Prepaid Rent …………….

2,400

Cash ………………………..

2,400

Cash

2,400

2,400

12/31/17

Rent Expense …………..

Unearned Rent Rev.

Prepaid Rent ……..

Rent Revenue

12/31/18

Rent Expense …………..

1,200

Unearned Rent Rev.

1,200

*Prepaid Rent …….

1,200

Rent Revenue

1,200

12/31/19

*Rent Expense ………….

Unearned Rent Rev.

Prepaid Rent ……..

Rent Revenue

Unearned Rent

An Alternative Solution (Based on the Appendix)

Tenant

Landlord

7/1/17

Rent Expense …………..

2,400

Cash ………………………..

2,400

Cash ………………….

2,400

Rent Rev. ………….

2,400

12/31/17

Prepaid Rent ……………

1,800

Rent Rev.

1,800

1,800

*12/31/18

Rent Expense …………..

1,200

Unearned Rent Rev.

1,200

Prepaid Rent ……..

1,200

Rent Revenue

1,200

*12/31/19

Rent Expense …………..

Unearned Rent Rev.

Prepaid Rent ……..

Rent Revenue

3-12

Chapter 3 Alternate Demonstration Problem – 2

The trial balance of Large Company, Inc., at the end of its annual

accounting period is as follows:

LARGE COMPANY, INC.

Trial Balance

December 31, 2017

Cash ………………………………………………………………..

$ 4,000

Accounts Receivable………………………………..

400

Supplies …………………………………………………………

Equipment ………………………………………………………

Accumulated Depreciation—Equipment ……………

$ 2,000

Revenue ………………………………………………………….

Salaries Expense ……………………………………………..

Totals ………………………………………………………………

$54,000

$54,000

Additional information:

1. Expired insurance, $400.

Required:

Prepare adjusting entries.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

3-13

Chapter 3 Solution: Alternate Demonstration Problem – 2

1.

Insurance Expense …………………………………….

400

Prepaid Insurance ………………………………..

400

Supplies Expense ………………………………………

1,300

Supplies ………………………………………………

1,300

Depreciation Expense Equip. ……………………..

1,000

Accumulated Depreciation Equip. …………

1,000

Salaries Expense ……………………………………….

Salaries Payable …………………………………..

Accounts Receivable …………………………………

Revenue ……………………………………………..

500