CONTINUING COOKIE CHRONICLE (Continued)

Common Stock

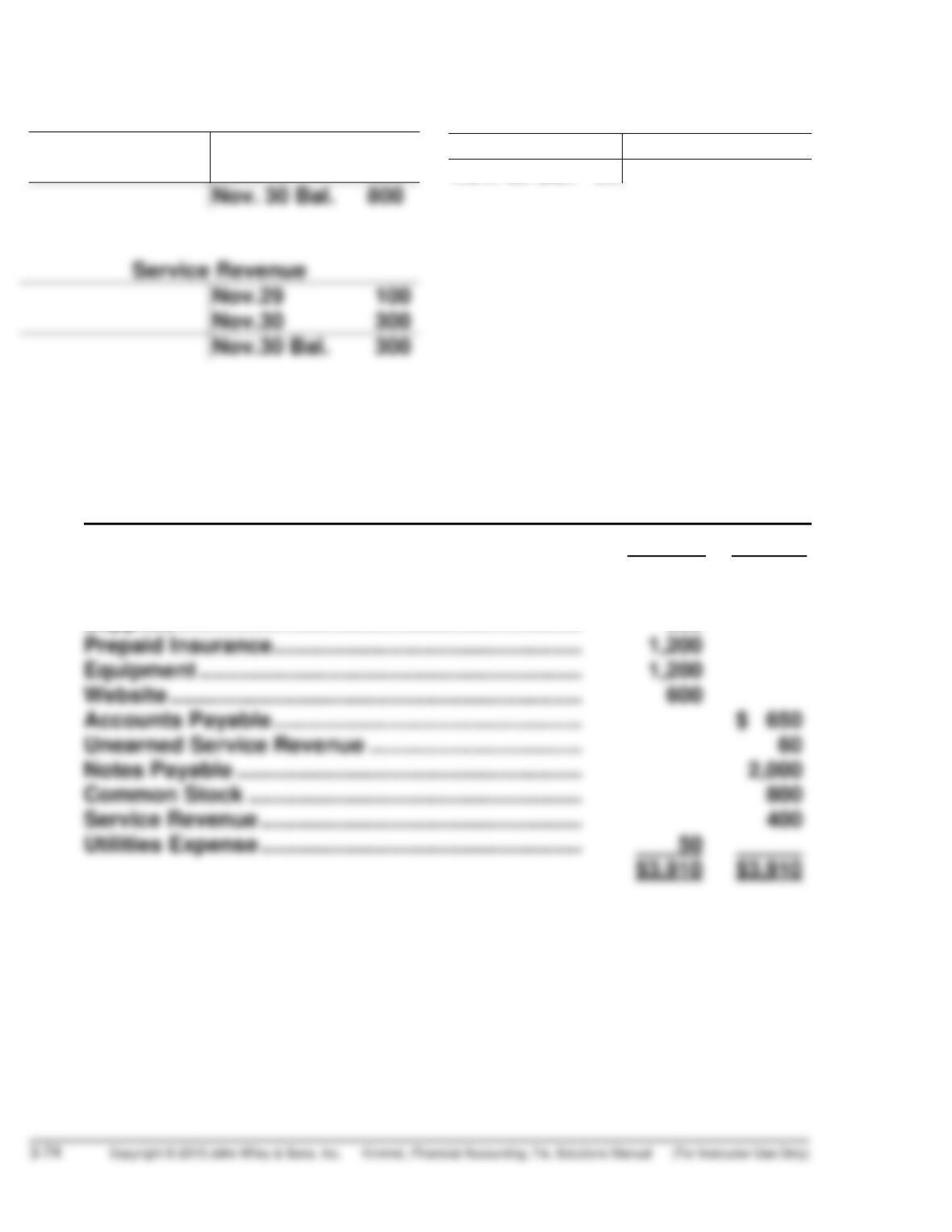

Nov. 8 500

Nov. 15 300

Utilities Expense

Nov. 30 50

Nov. 30 Bal. 50

(c) COOKIE CREATIONS INC.

Trial Balance

November 30, 2014

Debit Credit

Cash ………………………………………………………………. $ 340

Accounts Receivable ………………………………………. 300

Supplies …………………………………………………………. 220

BYP 3-1 FINANCIAL REPORTING PROBLEM

(a)

Account

Increase

Side

Decrease

Side

Normal

Balance

Common Stock

Accounts Payable

Accounts Receivable

Right/Credit

Right/Credit

Left/Debit

Left/Debit

Left/Debit

Right/Credit

Credit

Credit

Debit

(b) 1. Cash is increased.

BYP 3-2 COMPARATIVE ANALYSIS PROBLEM

(a) Tootsie Roll Hershey Company

1.

2.

Accounts Receivable

Net Property, Plant, and

Equipment

debit

debit

1.

2.

Inventories

Provision for Income

Taxes

debit

debit

(b) The following other accounts are ordinarily involved:

1. Increase in Accounts Receivable: Service Revenue or Sales Reve-

nue is increased (credited).

BYP 3-3 RESEARCH CASE

(a) The reason the Green Bay Packers’ issue an annual report is because

they are a publicly owned, nonprofit company. They issue the report to

(b) At the time that the article was written the owners of the NFL teams

and the players’ labor union were negotiating a new contract. Knowing

(c) Since some of the cost of the stadium that the Packers play in is

(d) The Packers’ revenues increased during recent years. However,

BYP 3-4 INTERPRETING FINANCIAL STATEMENTS

CHIEFTAIN INTERNATIONAL, INC.

(a) One of the primary advantages to Chieftain of having no long-term debt

is that there is room for growth through the use of debt and the

(b) An advantage to Chieftain from having a large cash balance is that

cash is available to finance such things as the drilling of new wells and

(c) Accounts payable, as purchases on credit, represent interest-free loans.

BYP 3-5 REAL-WORLD FOCUS

(a) CPAs work in public accounting, business and industry, government,

and education.

(b) A CPA needs:

strong leadership,

(c) Salary ranges are: $5 1,500 – $74,250 during the first three years for a CPA

at a large firm;

BYP 3-6 DECISION MAKING ACROSS THE ORGANIZATION

(a) May 1 Cash ………………………………………………………. 15,000

Common Stock ………………………………… 15,000

5 Correct.

7 Cash ………………………………………………………. 500

Unearned Service Revenue ………………. 500

(b) The error in the entries of May 14 and May 20 would prevent the trial

balance from balancing.

(c) Net income as reported …………………………………… $ 4,500

Add: 5/9, Supplies expense ……………………………. $1,500

(d) Cash as reported …………………………………………….. $12,475

Add: 5/9, Purchase on account ………………………. $1,500

BYP 3-7 COMMUNICATION ACTIVITY

To: Accounting Instructor

From: Accounting Student

Re: Steps in Recording Process

In the first transaction, bills totaling $6,000 were sent to customers for

services provided. Therefore, the asset Accounts Receivable is increased

$6,000 and the revenue Service Revenue is increased $6,000. Debits increase

assets and credits increase revenues, so the journal entry is:

In the second transaction, $2,000 was paid in salaries to employees. Therefore,

the expense Salaries and Wages Expense is increased $2,000 and the asset

Cash is decreased $2,000. Debits increase expenses and credits decrease

assets, so the journal entry is:

BYP 3-8 ETHICS CASE

(a) The stakeholders in this situation are:

• Jennifer VanPelt, assistant chief accountant.

(b) By adding $1,000 to the Equipment account, that account total is inten-

tionally misstated. By not locating the error causing the imbalance,

(c) Jennifer’s alternatives are:

1. Miss the deadline but find the error causing the imbalance.

BYP 3-9 ETHICS CASE

(a) Employees in the rail unit accelerated revenue in each of the fourth

quarters from 2000 to 2003. That is, revenue that should have been

(b) One possible motivation for engaging in this activity is that bonuses

are frequently based on annual results. If it appeared that the rail unit

(c) The employees were fired. In addition, the matter was being investigated

by the Securities and Exchange Commission (SEC).

(d) To restate financial statements means to actually issue new financial

statements to replace those that were previously issued. We are told

BYP 3-10 ALL ABOUT YOU

We address the issue of contingent liabilities in greater detail in Chapter

10. Our primary interest in this exercise is to engage students in a

discussion regarding the general nature of the financial statement

elements (assets, liabilities, equity, revenues and expenses).

(a) By taking out the bank loan your friend has incurred a liability. You do

not have a liability unless your friend defaults, or unless it becomes

(b) Accounting standards have specific requirements regarding account-

ing for situations where there is uncertainty regarding whether a liability

has been incurred. Those standards require an evaluation of the pro-

(c) Losing your job would not create a financial liability, although it would

most certainly reduce your revenues. You are obviously concerned that

you might lose your job, but you don’t have specific information that

would suggest that it will happen. Therefore, you probably don’t have

IFRS 3-1 CONCEPTS AND APPLICATION

In deciding whether the U.S. should adopt IFRS, the SEC should consider

the following:

• Whether IFRS is sufficiently developed and consistent in application

• Whether the IASB is sufficiently independent

• Whether IFRS is established for the benefit to investors

IFRS 3-2 INTERNATIONAL FINANCIAL REPORTING PROBLEM

Account Financial Statement Position in Financial Statement

Share capital Consolidated

Balance Sheet

Equity

Goodwill Consolidated

Non-current assets