CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN)

PROCESS COST SYSTEMS

DISCUSSION QUESTIONS

1. a. An assembly-type industry using mass production methods, such as TV assembly, would use

the process cost system because the products are somewhat standard and lose their identities

as individual items. In such industries, it is neither practical nor necessary to identify output

by jobs.

2. Because all goods produced in a process cost system are identical units, it is not necessary to classify

production costs into job orders.

3. In a process cost system, the direct labor and factory overhead applied are debited to the work

4. The cost per equivalent unit is frequently determined separately for direct materials and

conversion costs because these two costs are frequently added at different rates in the production

process. For example, materials may be incurred entirely at the beginning of the process, while

conversion costs are typically incurred evenly throughout the process.

5. The cost per equivalent unit is used to allocate direct materials and conversion costs between completed

and partially completed units.

6. The transferred-in cost from Blending to Filling includes the materials costs, direct labor, and applied

factory overhead incurred to complete units in Blending.

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

BASIC EXERCISES

BE 17–1 (FIN MAN); BE 3–1 (MAN)

Steel manufacturing

Process

Business consulting

Job order

Web designer

Job order

Computer chip manufacturing

BE 17–2 (FIN MAN); BE 3–2 (MAN)

BE 17–3 (FIN MAN); BE 3–3 (MAN)

Whole

Units

Percent

Materials

Added in

October

Equivalent

Units for

Materials

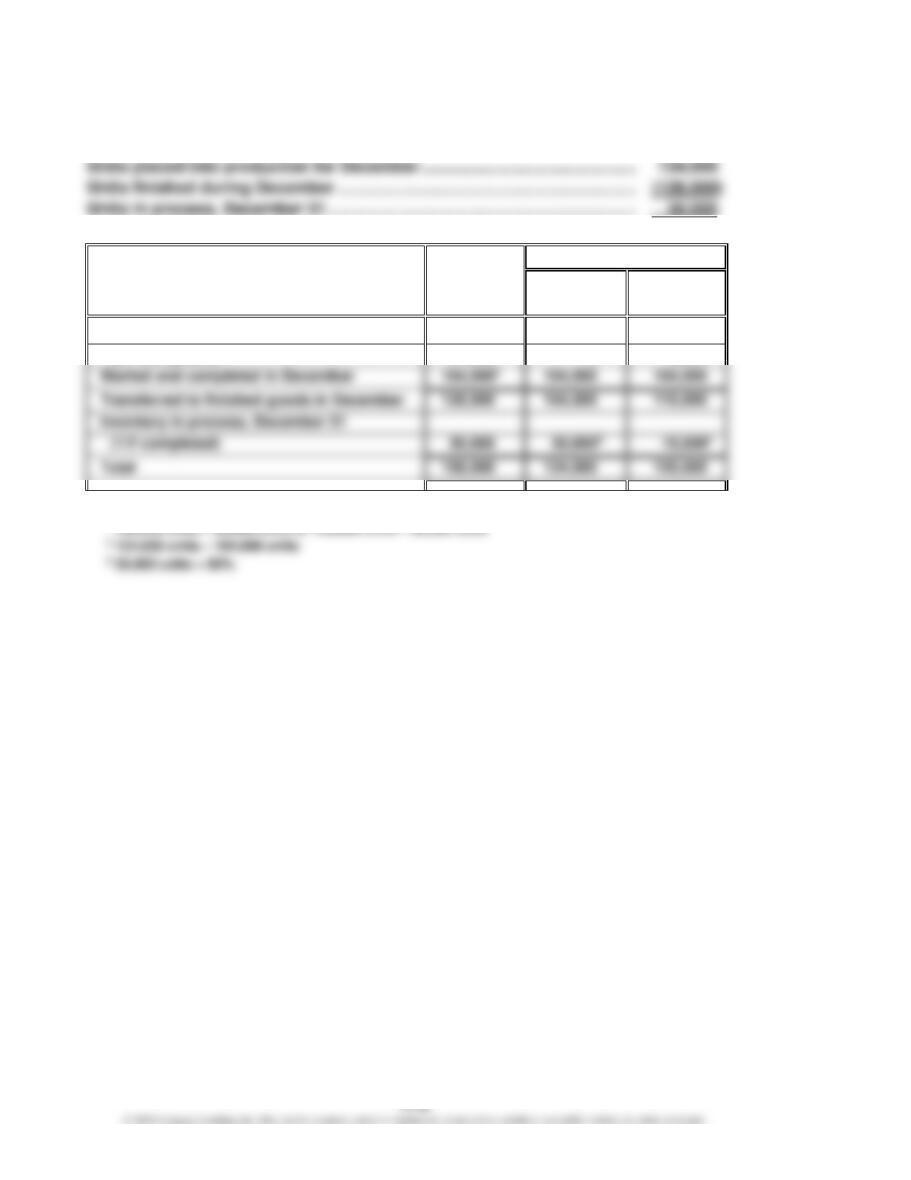

Inventory in process, October 1 ………………………..

200

0%

0

Started and completed during October ………………

3,700*

100%

3,700

Inventory in process, October 31 ………………………

BE 17–4 (FIN MAN); BE 3–4 (MAN)

Whole

Units

Percent

Conversion

Completed

in October

Equivalent

Units for

Conversion

Inventory in process, October 1 ………………………..

200

40%

80

Inventory in process, October 31 ………………………

25%

BE 17–5 (FIN MAN); BE 3–5 (MAN)

Equivalent units of direct materials:

$3,000,000

4,000

= $750 per ton

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

BE 17–6 (FIN MAN); BE 3–6 (MAN)

Direct

Materials

Costs

Conversion

Costs

Total

Costs

Inventory in process, balance ……………………………………

$ 163,800

To completed inventory in process, October 1 …………..

$ 0

$ 9,6001

9,600

Cost of completed beginning work in process ……………

$ 173,400

1 80 × $120

2 3,700 × $750

3 3,700 × $120

4 300 × $750

5 75 × $120

BE 17–7 (FIN MAN); BE 3–7 (MAN)

a.

1.

Work in Process—Rolling

3,000,000

Work in Process—Casting

3,000,000

Factory Overhead—Rolling

Wages Payable

3.

Finished Goods

3,392,400

b. $234,000 ($163,800 + $3,000,000 + $462,600 – $3,392,400)

BE 17–8 (FIN MAN); BE 3–8 (MAN)

Material cost per ton, September:

$76,000

800

= $95

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

EXERCISES

Ex. 17–1 (FIN MAN); Ex. 3–1 (MAN)

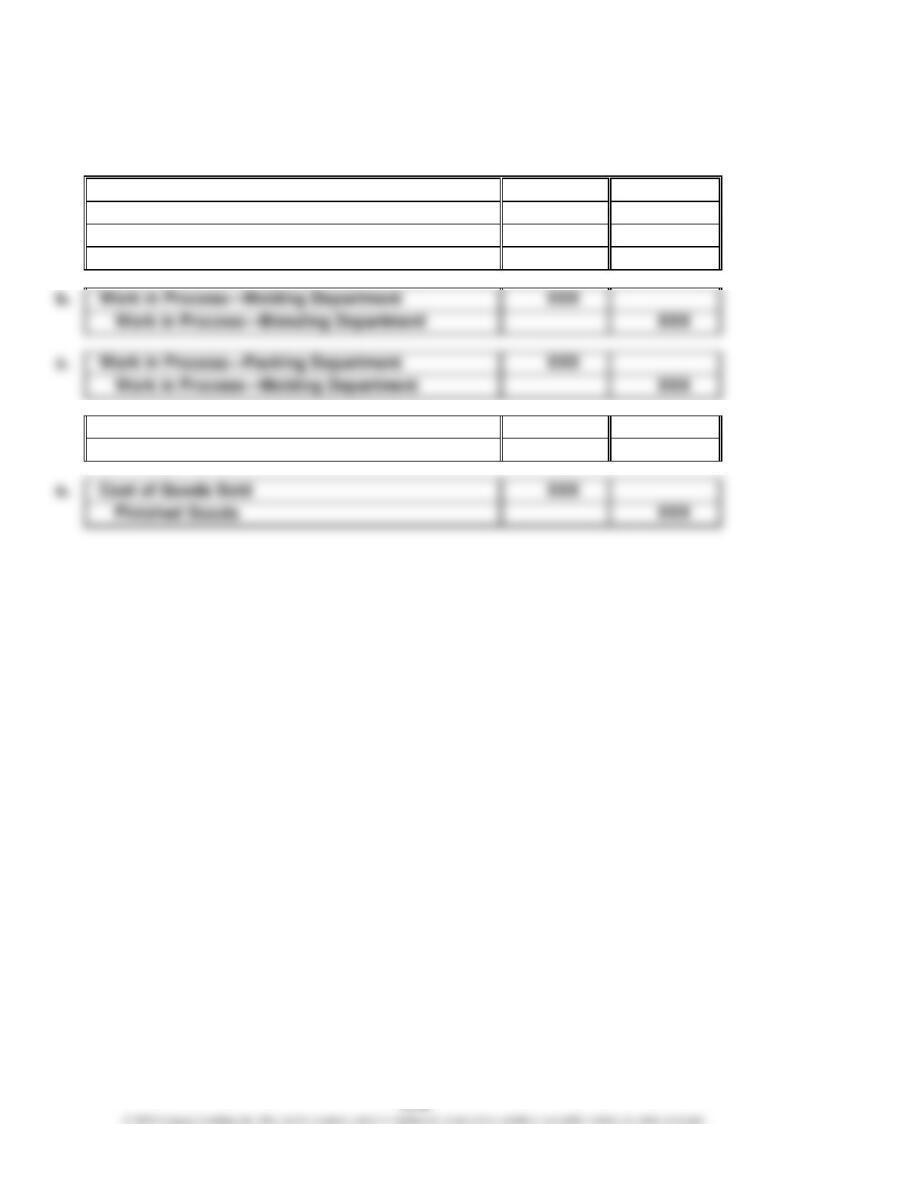

a.

Work in Process—Blending Department

XXX

Materials—Cocoa

XXX

Materials—Sugar

XXX

Materials—Dehydrated Milk

XXX

Work in Process—Blending Department

XXX

Work in Process—Packing Department

XXX

d.

Finished Goods

XXX

Work in Process—Packing Department

XXX

Cost of Goods Sold

XXX

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

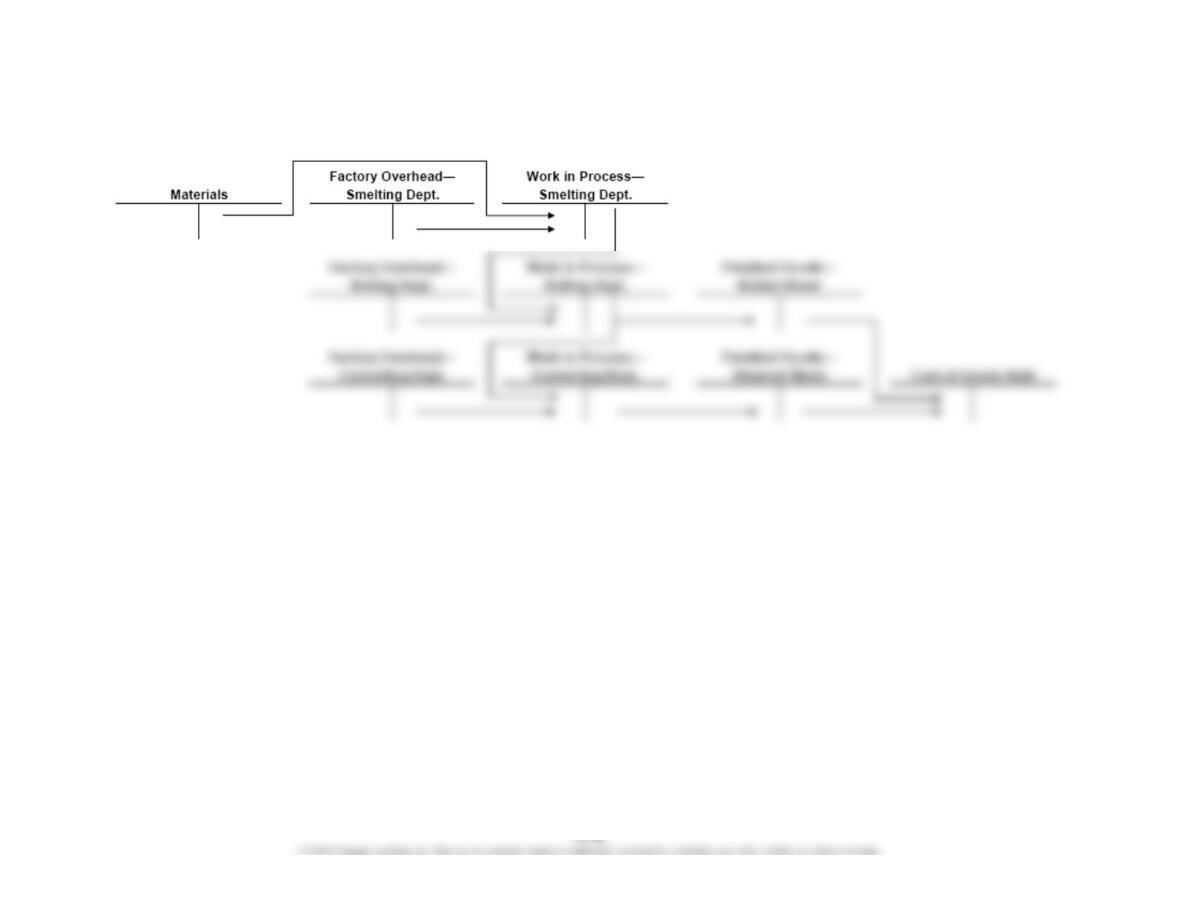

Ex. 17–2 (FIN MAN); Ex. 3–2 (MAN)

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–3 (FIN MAN); Ex. 3–3 (MAN)

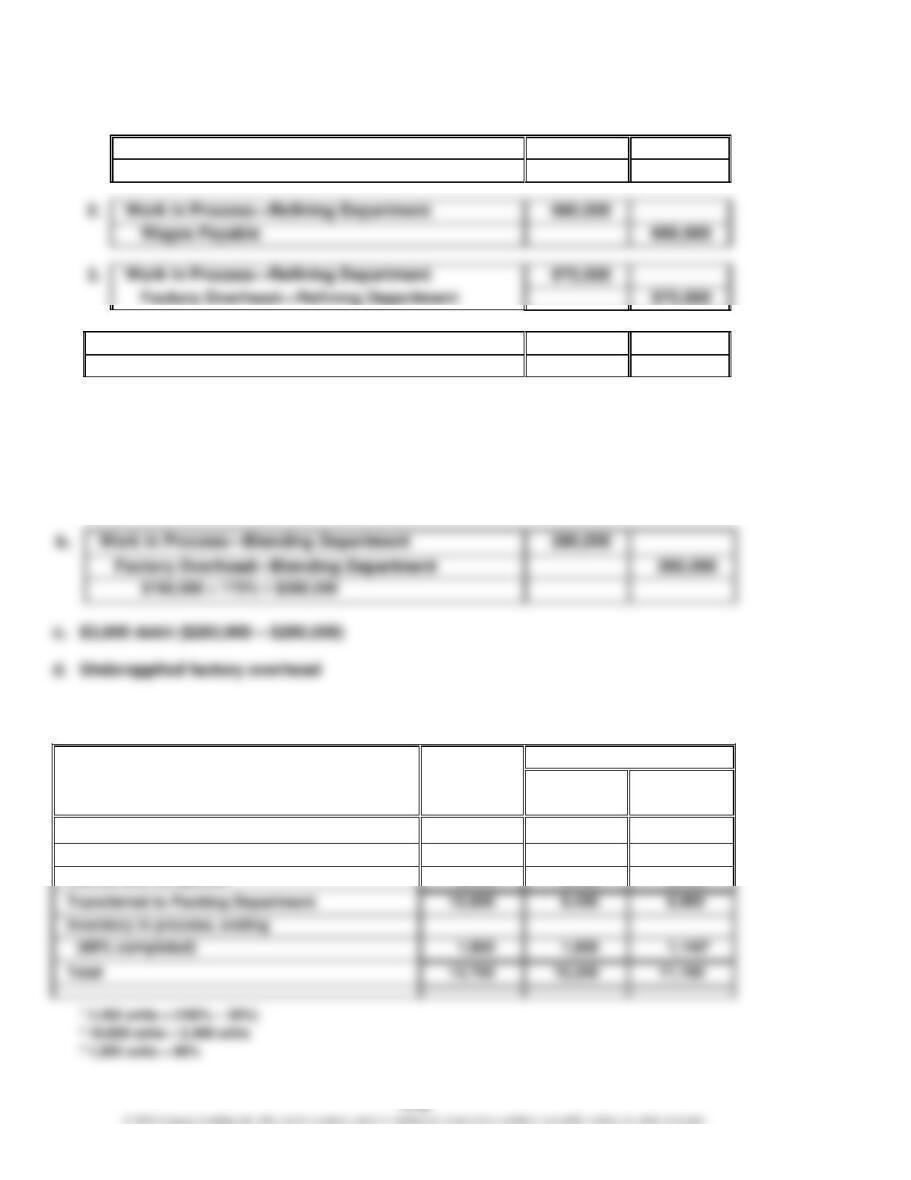

a.

1.

Work in Process—Refining Department

1,250,000

Materials

1,250,000

b.

Work in Process—Sifting Department*

2,918,000

Work in Process—Refining Department

2,918,000

* $328,000 + $1,250,000 + $660,000 + $975,000 – $295,000

Ex. 17–4 (FIN MAN); Ex. 3–4 (MAN)

a. Factory overhead rate:

$3,150,000 ÷ $1,800,000 = 175%

Ex. 17–5 (FIN MAN); Ex. 3–5 (MAN)

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Inventory in process, beginning

(35% completed)

2,400

0

1,5601

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

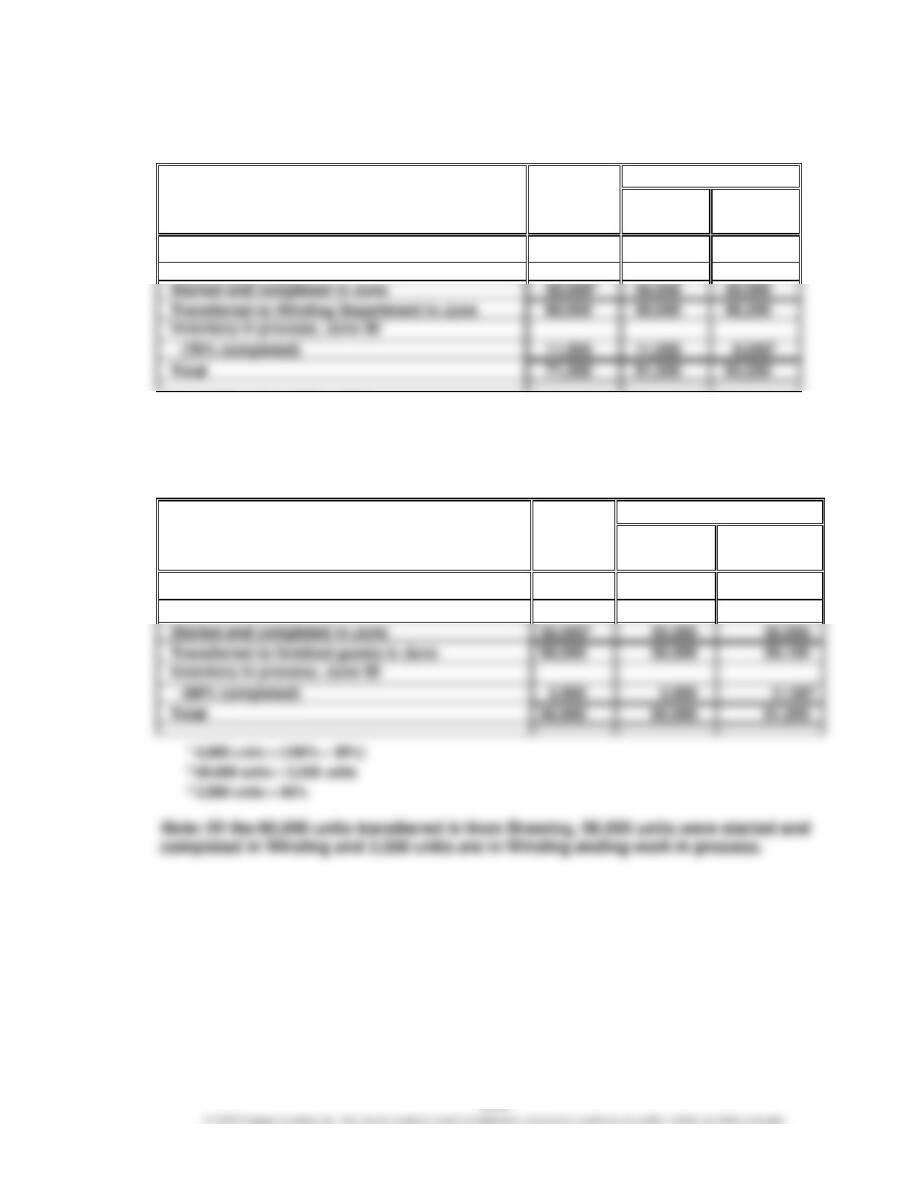

Ex. 17–6 (FIN MAN); Ex. 3–6 (MAN)

a. Drawing Department

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Inventory in process, June 1

(38% completed)

10,000

0

6,2001

50,0002

60,000

Inventory in process, June 30

(70% completed)

11,500

8,0503

71,500

1 10,000 units × (100% – 38%)

2 60,000 units – 10,000 units

3 11,500 units × 70%

b. Winding Department

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Inventory in process, June 1

(35% completed)

4,000

0

2,6001

Inventory in process, June 30

(60% completed)

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–7 (FIN MAN); Ex. 3–7 (MAN)

a.

Units in process, December 1 ……………………………………………………………..

24,000

b.

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Inventory in process, December 1

(3/4 completed)

24,000

0

6,0001

1 24,000 units × (100% – 75%)

2 128,000 units – 24,000 units or 134,000 units – 30,000 units

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–8 (FIN MAN); Ex. 3–8 (MAN)

a. 1. $1.75 ($234,500 ÷ 134,000 units)

Work in Process—Baking Department balance, December 1 ……………

$116,700

Conversion costs incurred during December

(6,000 equivalent units × $4.20) ……………………………………………………

25,200

Cost of beginning work in process completed during December ……..

$141,900

5. $115,500, determined as follows:

Direct materials ($1.75 × 30,000 units) ……………………………………………

$ 52,500

Conversion costs ($4.20 × 15,000 equivalent units) …………………………

63,000

Cost of ending work in process ……………………………………………………..

$115,500

Note: The cost of the ending work in process is also the balance of Work in

Process—Baking Department as of December 31.

b. The conversion costs in December increased by $0.05 per equivalent unit, determined

as follows:

Work in Process—Baking Department balance, December 1 ……………

$116,700

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–9 (FIN MAN); Ex. 3–9 (MAN)

Equivalent units of production:

Cereal

(in pounds)

Boxes

(in boxes)

Conversion

Cost

(in boxes)

Inventory in process, March 1 ………………………

0

0

800

Supporting explanation:

The whole unit inventory in process on March 1 includes both the cereal in the

hopper and the boxes in the carousel and, thus, includes no equivalent units for the

material during the current period. The reason is because the costs for the cereal

and boxes were introduced to the Packing Department in February. Because

conversion costs are incurred only when the cereal is filled into boxes, all 800

boxes of the March 1 inventory in process will have conversion costs incurred in

March.

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–10 (FIN MAN); Ex. 3–10 (MAN)

a.

Direct labor ……………………………………………………….……………………………….

$28,100

Factory overhead applied……………………………………………………………………

12,598

Total conversion cost …………………………………………………………………………

$40,698

b.

Equivalent units of production for conversion costs:

Conversion cost per equivalent unit:

$40,698

90,440

= $0.45 conversion cost per equivalent unit

c.

Equivalent units of production for direct materials costs:

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

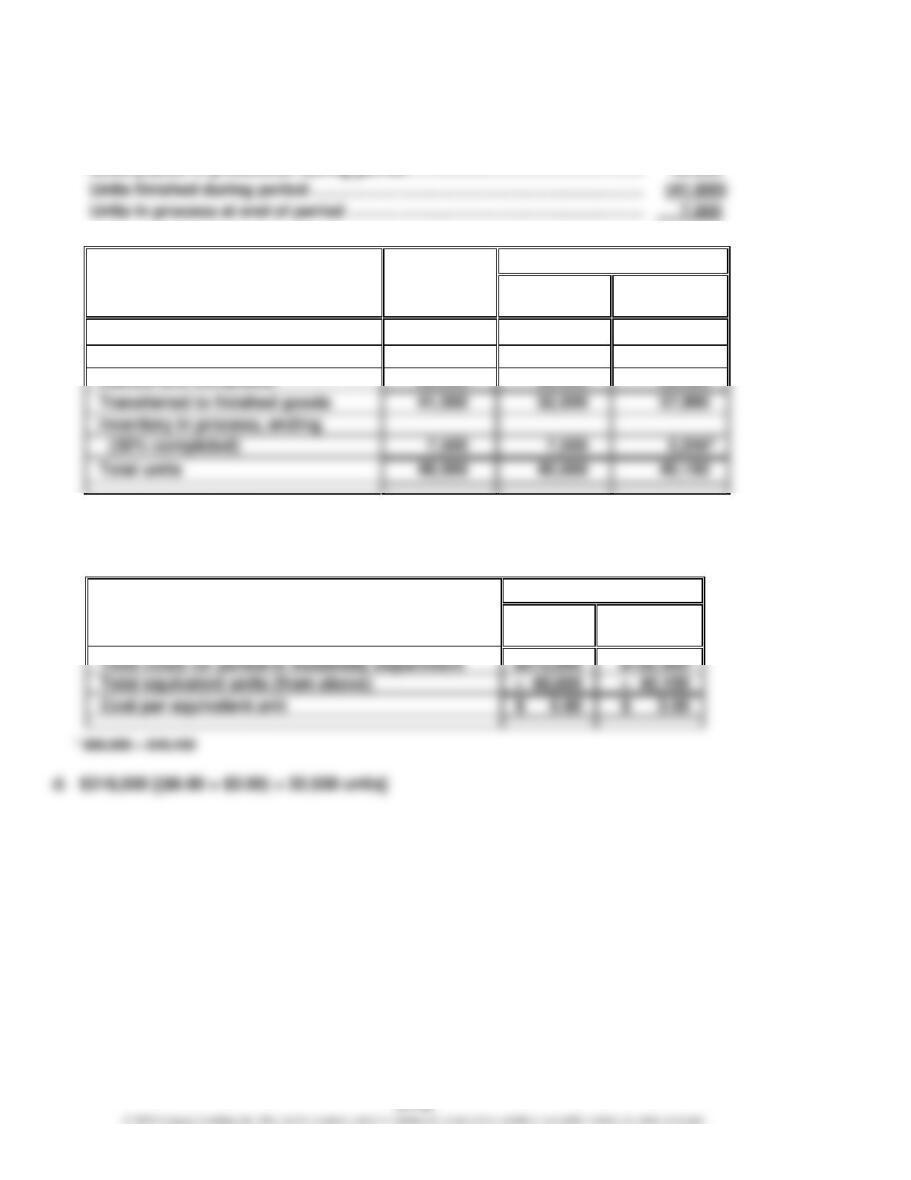

Ex. 17–11 (FIN MAN); Ex. 3–11 (MAN)

a.

Units in process at beginning of period ……………………………………………….

9,000

b.

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Inventory in process, beginning

(40% completed)

9,000

0

5,4001

Started and completed

Transferred to finished goods

Inventory in process, ending

1 9,000 units × (100% – 40%)

2 40,000 units – 7,500 units

3 7,500 units × 30%

c.

Costs

Direct

Materials

Conversion

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–12 (FIN MAN); Ex. 3–12 (MAN)

a.

1.

$88,560; determined as follows:

Beginning work in process balance ……………………………………………….

$72,360

Conversion costs incurred during period

(5,400 equivalent units × $3.00) ……………………………………………………

16,200

2.

Cost of beginning work in process …………………………………………………

*

($6.80 + $3.00) × 32,500 units

3.

$57,750; determined as follows:

Direct materials ($6.80 × 7,500 units) ………………………………………………

$51,000

4.

$9.84 ($88,560 ÷ 9,000 units)

b. Yes. The production costs per unit decreased during the current period. The

cost per unit of the units started and completed during the period is $9.80

($6.80 + $3.00). Because the cost per unit of the beginning work in process is

$9.84 [see a. 4 above], the production costs during the current period must

have decreased.

Beginning work in process ……………………………………………………………

Deduct direct materials cost incurred in prior period

($6.80 × 9,000 units, cost per unit unchanged) ………………………………

(61,200)

Conversion costs incurred in prior period ………………………………………

$ 11,160

Less prior-period conversion cost per equivalent unit

Decrease in conversion cost per equivalent unit during

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–13 (FIN MAN); Ex. 3–13 (MAN)

The errors are listed below.

1. In computing the equivalent units for conversion costs applicable to the June 1

inventory, the 6,400 units are multiplied by 3/5 rather than 2/5, which is the

portion of the work completed in June. Therefore, the equivalent units should be

2,560 (6,400 × 2/5) instead of 3,840.

2. In computing the equivalent units for conversion costs for units started and

3. The correct equivalent units for conversion costs should be 53,400, instead of 53,480,

as computed below.

To process units in inventory on June 1:

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–14 (FIN MAN); Ex. 3–14 (MAN)

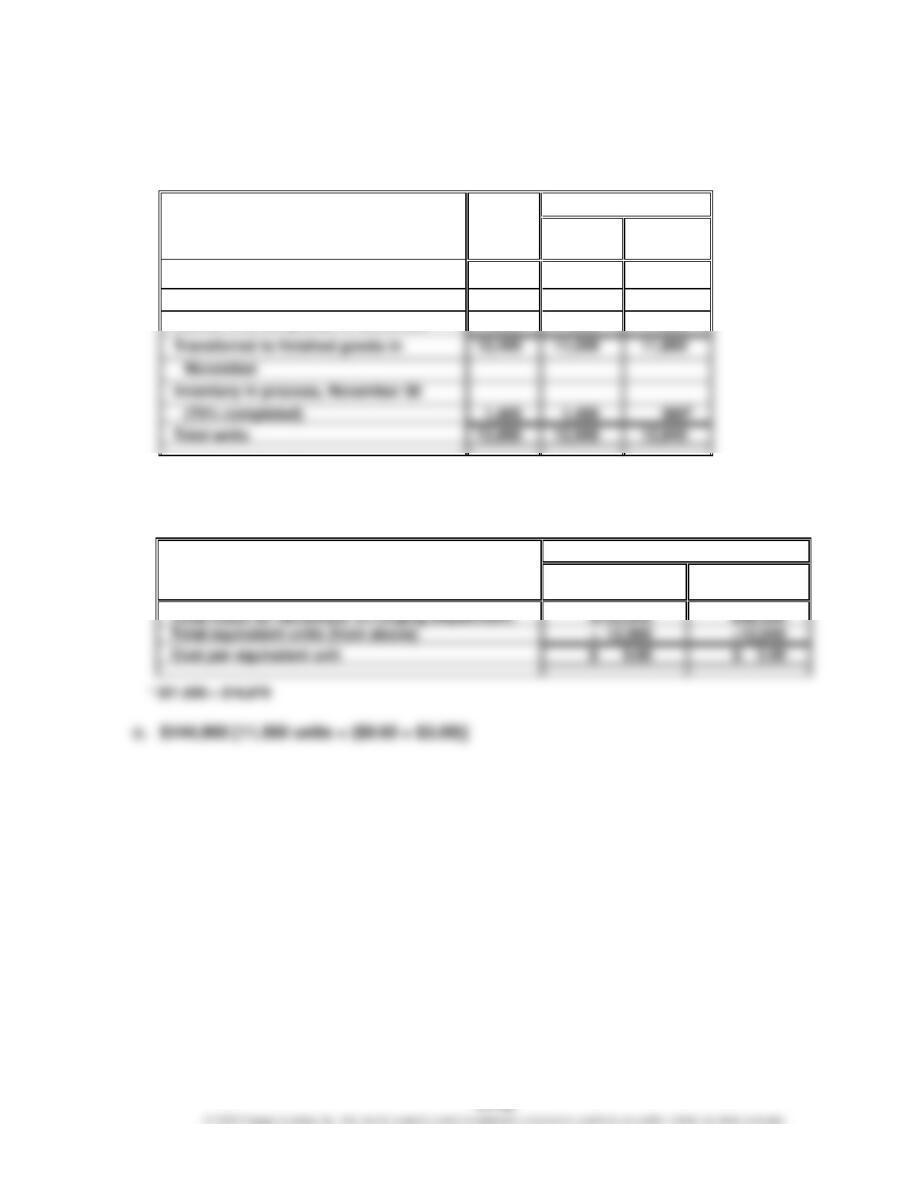

a. 12,400 units (900 + 12,900 – 1,400)

b.

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Inventory in process, November 1

(60% completed)

900

0

3601

Started and completed in November

11,5002

11,500

11,500

Transferred to finished goods in

12,400

11,500

11,860

Inventory in process, November 30

1,400

13,800

12,840

1 900 units × (100% – 60%)

2 12,900 units – 1,400 units

3 1,400 units × 70%

Costs

Direct

Materials

Conversion

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–15 (FIN MAN); Ex. 3–15 (MAN)

a.

$11,646; determined as follows:

Beginning work in process balance …………………………………………………

$10,566

Conversion costs incurred during November

(360 equivalent units × $3.00) ………………………………………………………..

1,080

Cost of beginning work in process completed during November ……….

$11,646

c.

$16,380; determined as follows:

Direct materials ($9.60 × 1,400 units) ………………………………………………..

$13,440

Conversion costs ($3.00 × 980 equivalent units) ……………………………….

2,940

Cost of ending work in process inventory ………………………………………..

$16,380

Note: The cost of the ending work in process is also the ending balance of the Work in

Process—Forging Department as of November 30.

Conversion cost per equivalent unit: $2.90 ($1,566* ÷ 540 units**)

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

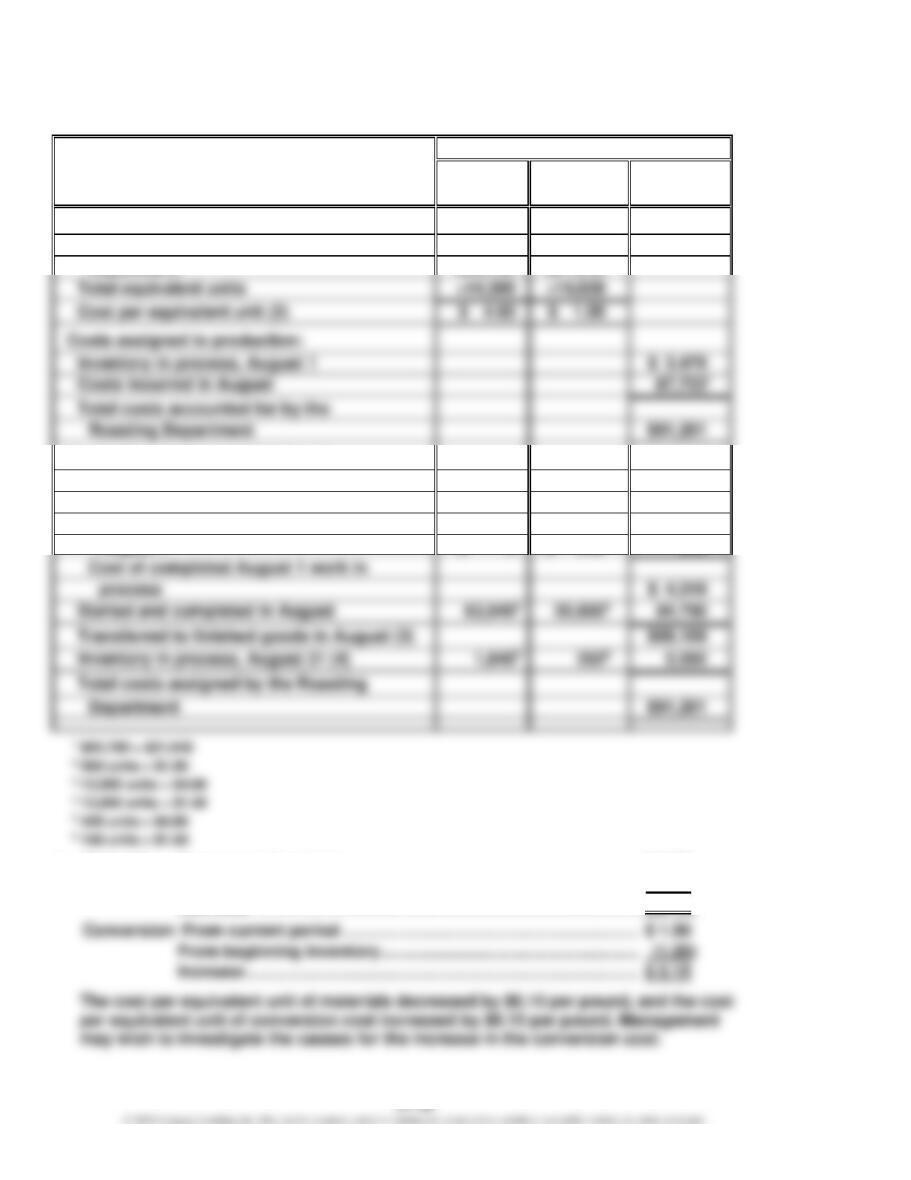

Ex. 17–16 (FIN MAN); Ex. 3–16 (MAN)

a.

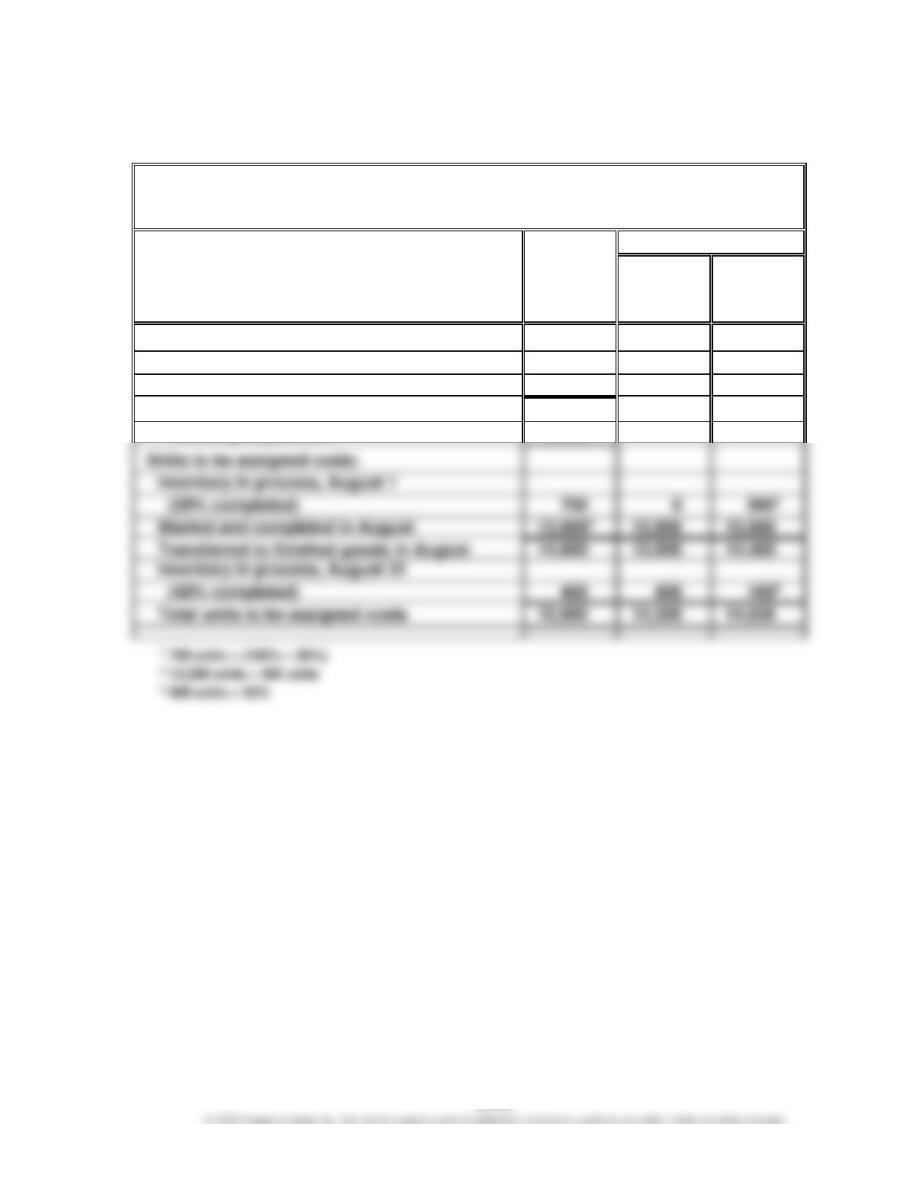

Morning Brew Coffee Company

Cost of Production Report—Roasting Department

For the Month Ended August 31

UNITS

Whole

Units

Equivalent Units

Direct

Materials

(1)

Conversion

(1)

Units charged to production:

Inventory in process, August 1

700

Received from materials storeroom

14,300

Total units accounted for by the

Roasting Department

15,000

Units to be assigned costs:

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

Ex. 17–16 (FIN MAN); Ex. 3–16 (MAN) (Concluded)

COSTS

Costs

Direct

Materials

Conversion

Total

Costs per equivalent unit:

Total costs for August in Roasting

Total equivalent units

Cost per equivalent unit (2)

Costs assigned to production:

Inventory in process, August 1

Costs incurred in August

Total costs accounted for by the

Roasting Department

Costs allocated to completed and

partially completed units:

Inventory in process, August 1 balance

$ 3,479

To complete inventory in process,

Cost of completed August 1 work in

b.

Materials:

From current period ……………………………………………………………………..

$ 4.60

From beginning inventory ……………………………………………………….

(4.70)

Decrease ……………………………………………………………………………………

Conversion: From current period ……………………………………………………….

$ 1.50

From beginning inventory ……………………………………………………….

(1.35)

Increase ……………………………………………………………………………………

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

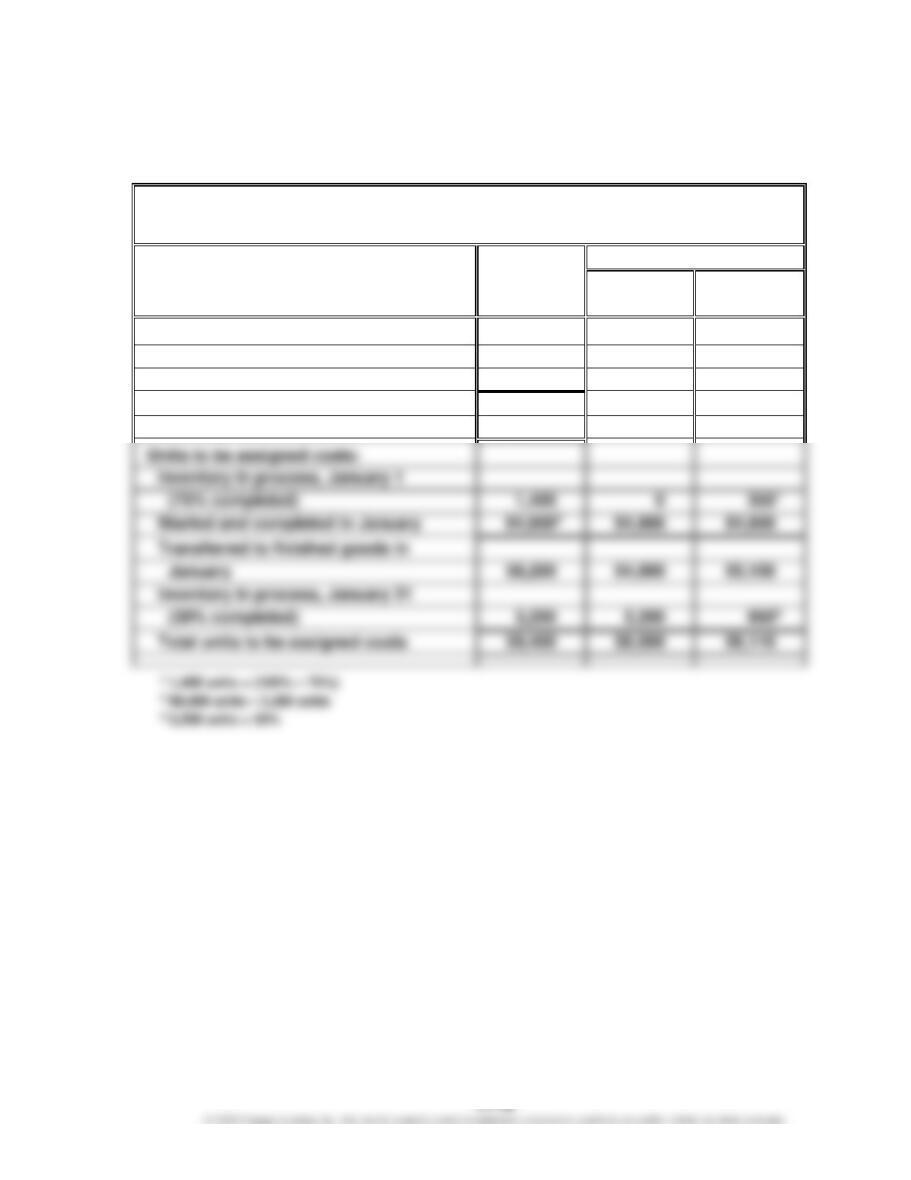

Ex. 17–17 (FIN MAN); Ex. 3–17 (MAN)

a.

Karachi Carpet Company

Cost of Production Report—Cutting Department

For the Month Ended January 31

UNITS

Whole

Units

Equivalent Units

Direct

Materials

Conversion

Units charged to production:

Inventory in process, January 1

1,400

Received from Weaving Department

58,000

Total units accounted for by the

Cutting Department

59,400

Units to be assigned costs:

Inventory in process, January 1

Started and completed in January

Transferred to finished goods in

Inventory in process, January 31

(30% completed)

CHAPTER 17 (FIN MAN); CHAPTER 3 (MAN) Process Cost Systems

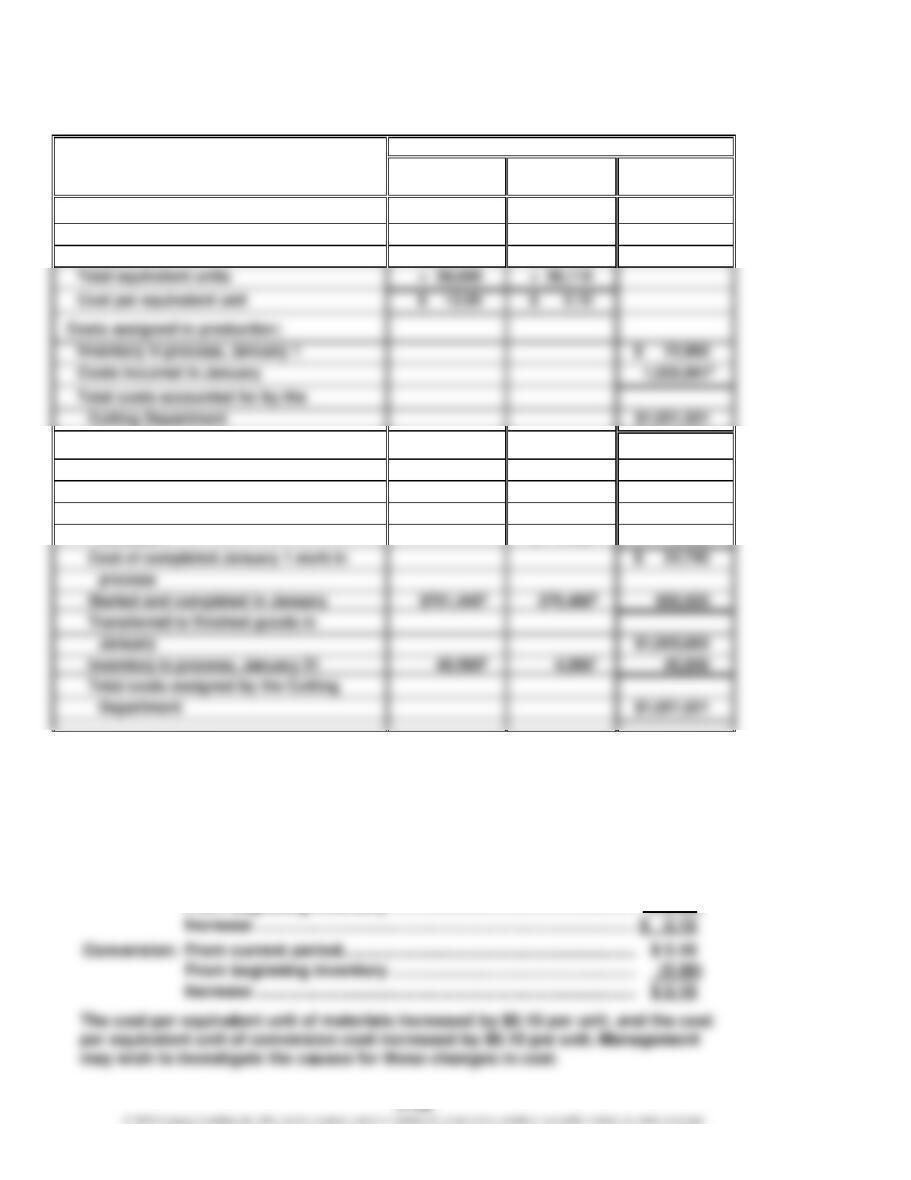

Ex. 17–17 (FIN MAN); Ex. 3–17 (MAN) (Concluded)

COSTS

Costs

Direct

Materials

Conversion

Total

Costs per equivalent unit:

Total costs for January in Cutting

Department

$742,400

$286,1611

Total equivalent units

Cost per equivalent unit

Inventory in process, January 1

$ 22,960

Costs incurred in January

Total costs accounted for by the

Cutting Department

Cost allocated to completed and

partially completed units:

Inventory in process, January 1 balance

$ 22,960

To complete inventory in process,

January 1

Cost of completed January 1 work in

$ 24,745

Transferred to finished goods in

Total costs assigned by the Cutting

$ 1,7853

1,785

1 $134,550 + $151,611

2 $742,400 + $134,550 + $151,611

3 350 units × $5.10

4 54,800 units × $12.80

5 54,800 units × $5.10

6 3,200 units × $12.80

7 960 units × $5.10

b.

Materials:

From current period ……………………………………………………….

$ 12.80