CHAPTER 3

Measuring Revenues and Expenses

THINKING BEYOND THE QUESTION

How do we know how much profit our business has earned?

Revenues earned over several fiscal periods usually are allocated to each

QUESTIONS

Q3-1 The flow of cash often predates or follows the economic event to which it

is related. If financial reports are supposed to measure the economic ac-

tivities that occurred during a period, the amount of cash that flowed will

Q3-2 Agree. While the accrual measurement of revenue and expense is traced

to the accounting period in which the economic event occurred, the cash

52 Chapter 3

Q3-3 Profitability is reported on the income statement using an accrual meas-

ure. It is the difference between revenues earned and expenses con-

sumed. Profit is the amount of cash that is ultimately expected to result af-

Q3-4 Accounts Receivable links Revenue and Cash by recording the amount

Q3-5 Unearned Revenue is a liability that is reported on a company’s balance

Q3-7 At the moment the rent is paid, the company has acquired an asset. It has

purchased the exclusive right to use the landlord’s property for one

Q3-9 Subsidiary accounts are used to record the detail associated with an indi-

vidual item of importance to a company. For example, a separate subsidi-

ary account (Accounts Receivable—Sally Jobers) is maintained for each

Measuring Revenues and Expenses 53

Q3–10 Control accounts summarize the detailed information contained in subsid-

iary accounts. When decision makers outside the firm make decisions

concerning the organization, these summaries are sufficient and appropri-

Q3–11 Other common examples of period costs are interest, property taxes, rent

on office facilities, and management salaries. All of these costs generally

occur with the passage of time. In many cases, the company does not ever

Q3–12 This statement is not true. The numbers reported on a balance sheet are

related to the cost of the asset, not its current value. When an asset such

as a building or land is acquired, it is entered into the accounting records

at its cost (which is probably a good measure of its current value at that

Q3–13 The purpose of preparing a summary of general ledger account balances

Q3–14 The closing entries zero out the revenue and expense account balances at

54 Chapter 3

Q3–16 Proper accounting procedures make unethical behavior difficult. The pro-

Q3–17 Good accounting controls protect owners, creditors, and other stakehold-

EXERCISES

E3-1 Definitions of all terms are listed in the glossary.

E3-2 Net Income Net Cash Flow

Sale of wheat (all cash) $ 650,000 $650,000

Operating costs ($532,500 in cash) (585,000) (532,500)

Measuring Revenues and Expenses 55

E3-3 Received for miles traveled ($4.50 × 2,400 miles) $10,800

Expenses:

Gas 500

E3-4

Cash Flow

for September

Cash Flow

in Future

Sales Revenue

for September

E3-5

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

1

Interest Expense

–3,600

Interest Payable

3,600*

Unearned Rent

4,000

Prepaid Insurance

Accumulated Depreciation

56 Chapter 3

E3-6

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Oct. 1

Merchandise

3,600

Accounts Payable

3,600

Oct. 3

Cash

900

E3-7

Company

A

Company

B

Company

C

Cash received from customers during 2007

$300,000

$625,000

$242,000

Sales revenue for 2007

$352,500

$580,000

$260,000

Accounts receivable at beginning of 2007

$130,000

Accounts receivable at end of 2007

Company

A Revenue was $52,500 more than cash collected. Therefore, accounts

Sales Revenue

Cost of Goods Sold

Merchandise

Oct. 6

Accounts Receivable

Sales Revenue

1,800

Cost of Goods Sold

Merchandise

Oct. 9

Spoilage Expense

Merchandise

Oct. 10

Accounts Payable

Cash

Oct. 16

Cash

1,200

Accounts Receivable

Measuring Revenues and Expenses 57

Alternative presentations include:

Company A

Cash received in 2007 $300,000 Revenue for 2007 $352,500

E3-8 a.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

1

Wages Expense

–7,600

Wages Payable

7,600

2

Office Supplies Inventory

Office Supplies Expense

3

Rent Receivable

Rent Revenue

4

Depreciation Expense

Accumulated Depreciation

5

Interest Expense

Interest Payable

E3-9 a.

Past

September

Future

Total

Revenues

Expenses

$1,500

$2,500

$1,000

Cash received

Cash paid

$5,000

$5,000

58 Chapter 3

b.

Past

September

Future

Total

c.

Past

September

Future

Total

Revenues

Expenses

$7,500

$7,500

Cash received

Cash paid

$5,000

$2,500

$7,500

d.

Past

September

Future

Total

Revenues

Expenses

Cash received

Cash paid

$2,500

e.

Past

September

Future

Total

Revenues

Expenses

Cash received

Cash paid

E3–10

Cash Flow

for June

Cash Flow

in July

Wages

Expense

for June

Cash paid for prior wages

$5,800

Cash paid for June wages

$4,200

$48,400

Total cash paid in June for wages

E3–11

January

February

March

Total for

Quarter

Cash paid for interest

Interest expense

Revenues

Expenses

Cash received

$6,000

Cash paid

Measuring Revenues and Expenses 59

E3–12

2007

2008

2009

Total for

3 Years

Cash paid for equipment

$600,000

$0

$0

$600,000

E3–13

April

May

June

Total for

3 Months

Cash paid for utilities

$850

$1,025

$1,150

$3,025

Utilities expense

$850

$1,025

$1,150

$3,025

E3–14

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

a.

Interest Expense

–1,200

Interest Payable

Rent Revenue

c.

Insurance Expense

–2,000

Prepaid Insurance

–2,000

Depreciation Expense

Accumulated Depreciation

E3–15 a. Merchandise—Canvas Material +$20,000

Accounts Payable—Ramirez, Inc. +$20,000

Depreciation expense

$200,000

$200,000

$200,000

$600,000

60 Chapter 3

E3–16 Assets Liabilities Equity Net Income

Year-end amounts

before correction $7,625 $2,820 $4,805 $1,200

E3–17 a. The purpose of closing the books is to empty out all of the revenue and

b.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Dec. 31

Retained Earnings

2,200

Sales Revenue

Retained Earnings

Cost of Goods Sold

Wages Expense

Utilities Expense

Depreciation Expense

Insurance Expense

Supplies Expense

Interest Expense

E3–18 a.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Dec. 31

Retained Earnings

3,315

Service Revenue

Retained Earnings

Measuring Revenues and Expenses 61

Internet Service Expense

35

b. Assets:

Cash 20,600

Accounts Receivable 2,250

E3–19 a.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Dec. 31

Retained Earnings

290,000

Sales Revenue

Retained Earnings

Insurance Expense

Wages Expense

Utilities Expense

Depreciation Expense

62 Chapter 3

b. Post-closing summary

Assets:

Cash 10,500

Liabilities:

Accounts Payable 31,000

Owners’ Equity:

Contributed Capital 84,500

E3–20 a. The purpose of closing the books is to empty out all of the revenue

b.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Dec. 31

Retained Earnings

7,600

Sales Revenue

Retained Earnings

Cost of Goods Sold

2,840

Wages Expense

1,015

Utilities Expense

Depreciation Expense

Insurance Expense

Supplies Expense

Interest Expense

Measuring Revenues and Expenses 63

PROBLEMS

P3-1 M E M O R A N D U M

DATE: (today’s date)

TO: Robin Garrison

FROM: (student’s name)

RE: Klinger Realty operating results

Managers (and other parties) are interested in measuring the results of

transformation processes that occur during a fiscal period. As with many

that from a cash basis measurement.

Cash payments are measured and recorded when cash is paid out

to suppliers of goods or services to be sold to customers. The difference

between cash receipts and cash payments is net cash flow.

Under the accrual basis system of measurement, revenues are

measured and recorded when they have been earned, that is, at the point

64 Chapter 3

performed for customers during a period, but all work was on credit to be

collected during the subsequent period. None of the $200,000 would show

up on the current cash basis report, though all the work was completed.

P3-2 Hardy’s reasoning about the revenues is correct. Revenues should be

recorded on the accrual basis during the period the sales occur. A com-

plete reporting of the transaction would include Accounts Receivable on a

balance sheet noting that $50,000 of the amount was still owed by cus-

tomers. Hardy’s reasoning about the cost of goods sold is incorrect. Ex-

P3-3 The key to each event is a clear definition of revenue. Revenue is an in-

crease in assets as a result of goods sold or services rendered. Applying

this definition to each event yields the following results:

Measuring Revenues and Expenses 65

P3-4

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

March 15

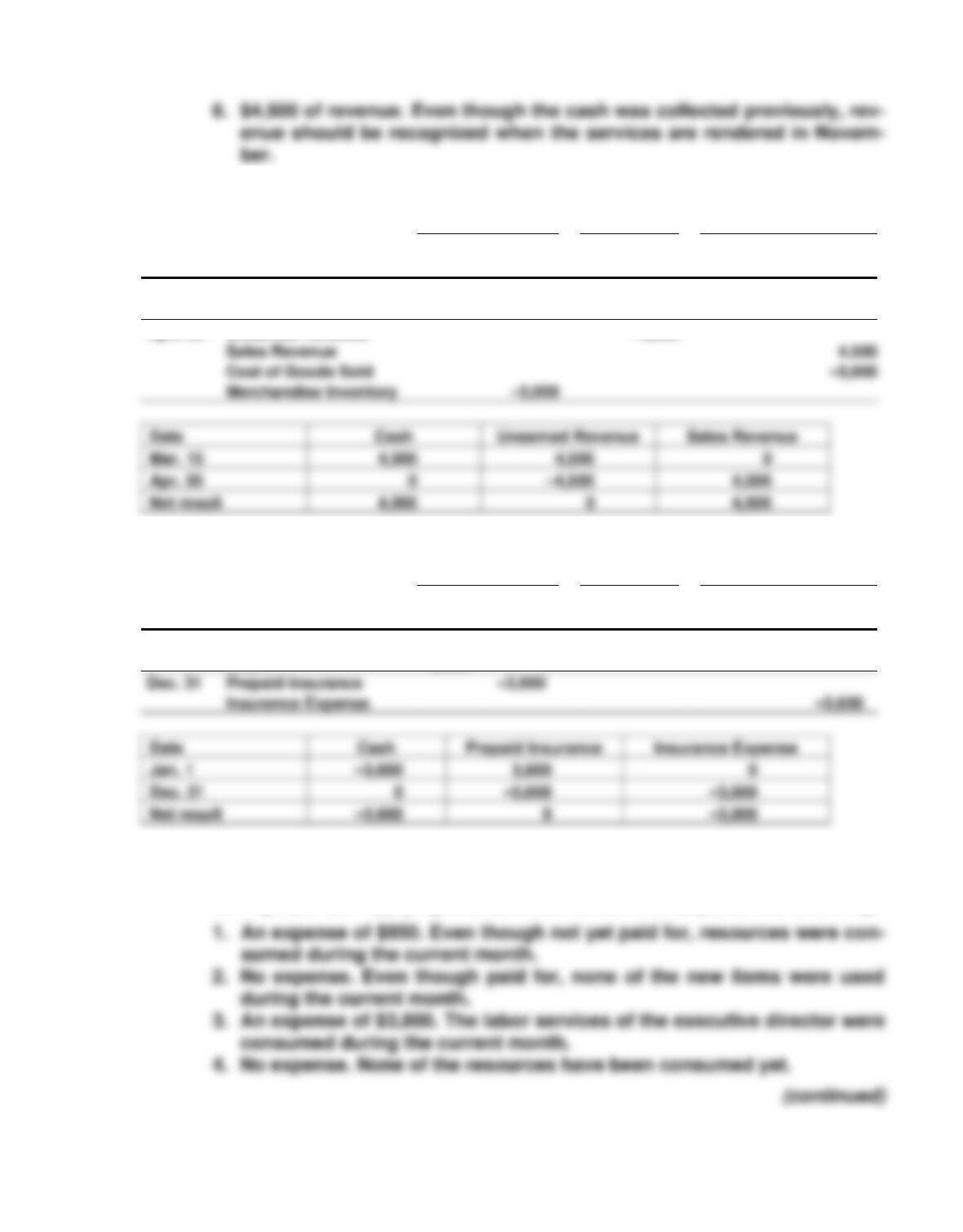

Cash

4,500

Unearned Revenue

4,500

April 30

Unearned Revenue

–4,500

Sales Revenue

Cost of Goods Sold

Merchandise Inventory

P3-5

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Jan. 1

Prepaid Insurance

3,600

Cash

–3,600

Dec. 31

Insurance Expense

Prepaid Insurance

P3-6 The key to each event is a clear definition of expense. An expense is the

consumption of resources in producing or providing goods or services

during a period. Applying this definition to the events yields the following:

66 Chapter 3

month of May.

P3-7 a. Because accounts receivable increased during the month, the cash col-

lections were less than the amount of sales. Further, this difference is

equal to the increase in accounts receivable. Therefore, cash collec-

tions from customers are as follows:

P3-8 Carlyle Company

Income Statement

For the First Year

Revenues ($235,000 + $80,000) $315,000

P3-9 A. Tinker’s financial report relied improperly on cash basis numbers. Prof-

its should be measured on the accrual basis. Sales should be included

Measuring Revenues and Expenses 67

B. The other partners would be foolish to sell out based on Tinker’s in-

A proper income statement and distribution of profits would show the

following:

Tinker, Evers, and Chance

Income Statement

For Fiscal 2007

Revenues $7,600,000

Expenses:

P3–10 A. The Water Fun Store

Net Cash Flow from Operating Activities

For August

Cash receipts:

Collected from customers ($5,350 + $3,700) $ 9,050

68 Chapter 3

B. The Water Fun Store

Accrual Basis Income Statement

For August

Sales ($7,350 + $6,350) $13,700

Expenses:

Cost of goods sold ($3,600 + $2,400) $6,000

P3–11 A. Based on the income statement and changes in the balance sheet, the

following transactions must have occurred:

1. Revenue from services rendered totaled $840,000. It was billed and

B. Explanation of the changes in cash:

Beginning cash balance $ 43,725

Measuring Revenues and Expenses 69

P3–12 A. Caldwell Furniture Repair

Income Statement

For March

Revenues $ 7,600

Expenses:

B. Explanation of the cash account:

Beginning balance $ 0

Owner investment 2,000

C. At the end of March there is an incomplete transformation cycle. A

70 Chapter 3

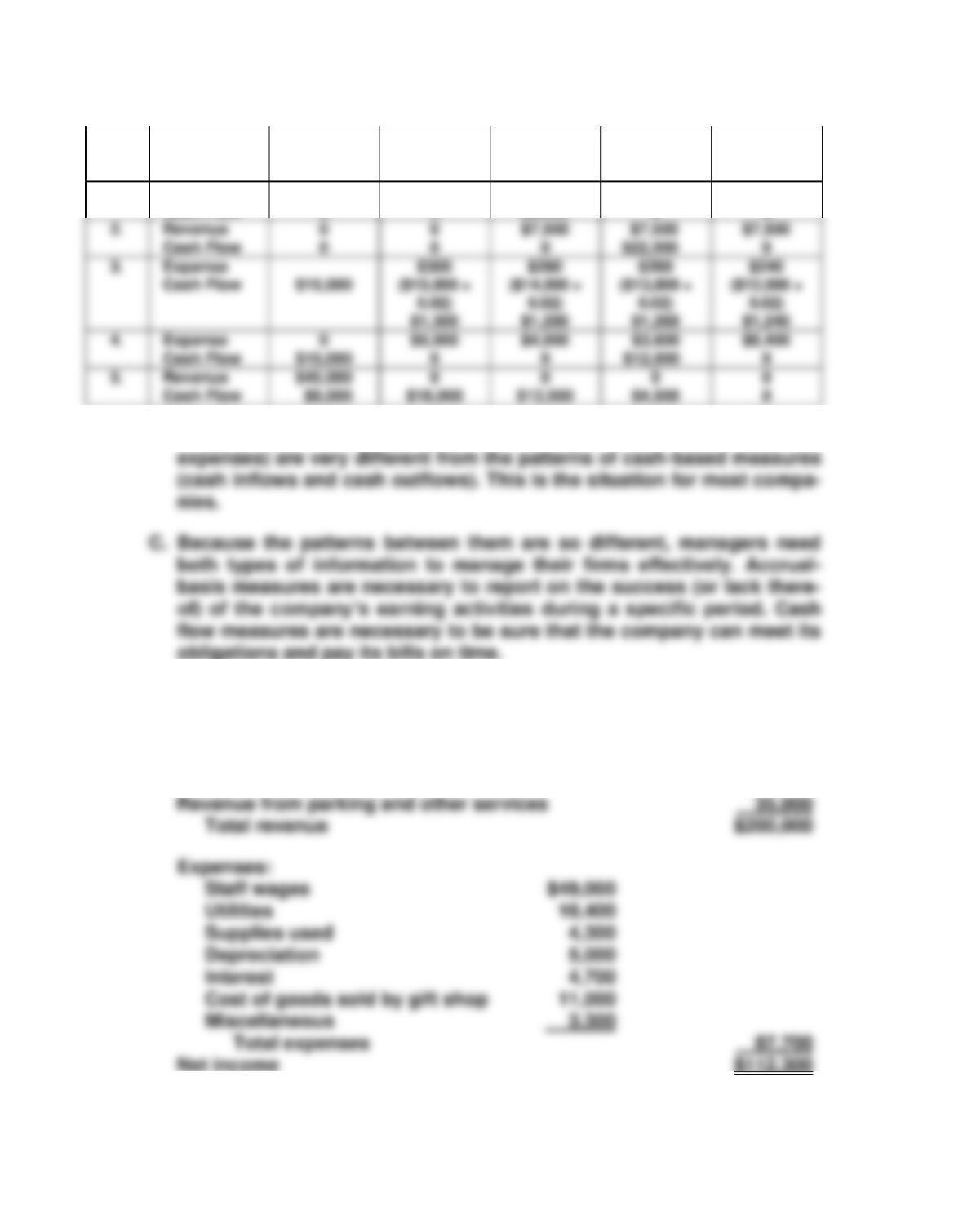

P3–13 A.

Event

Revenue,

Expense, or

Cash Flow?

Month of

February

Month of

March

Month of

April

Month of

May

Month

of June

1.

Expense

Cash Flow

0

0

$1,200

0

$1,200

$3,600

$1,200

0

0

0

B. In this problem, the patterns of accrual-based measures (revenues and

P3–14 A. Desert Harbor Inn

Income Statement

For the Year Ended December 31, 2007

Revenue from room rentals $165,000

2.

Revenue

Cash Flow

0

0

0

0

$7,500

0

$7,500

$7,500

0

4.

Expense

Cash Flow

0

$6,000

0

$4,000

0

$8,400

0