Measuring Revenues and Expenses 71

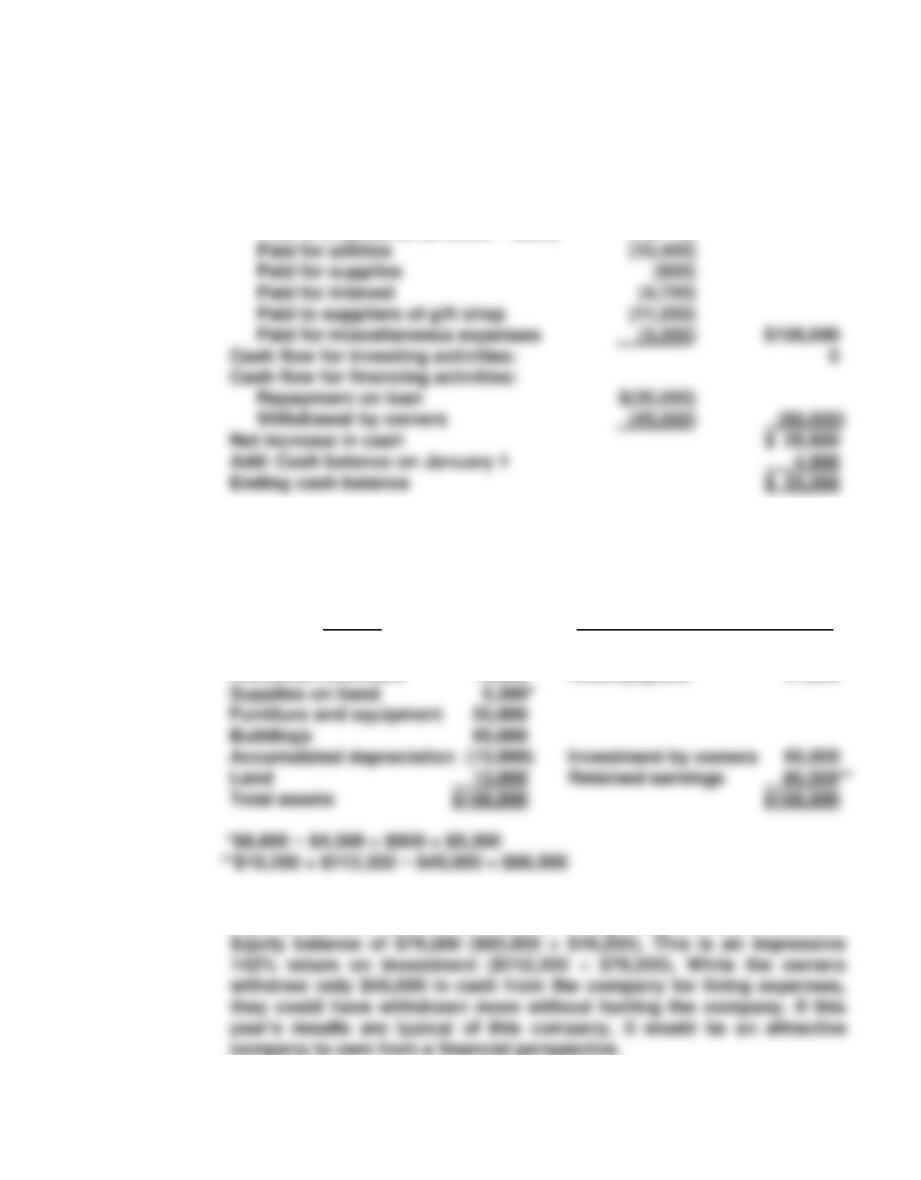

Desert Harbor Inn

Statement of Cash Flows

For the Year Ended December 31, 2007

Cash flow from operating activities:

Collected from customers $187,000

Paid to employees ($49,000 − $890) (48,110)

Desert Harbor Inn

Balance Sheet

December 31, 2007

Assets Liabilities and Owners’ Equity

Cash $ 33,590 Wages payable $ 890

Accounts receivable 13,000 Notes payable 21,500

B. From a financial perspective, this appears to be an attractive business.

It generated net income of $112,300 on a beginning–of-the-year Owners’

72 Chapter 3

P3–15 A. Zorditch.com

Income Statement

End of the First Year

Sales revenue ($173,400 + $18,200)* $191,600

Expenses:

Depreciation expense $ 5,700

B. Item Justification of change

1. Money I contributed to firm

This is not an expense. It represents

Owners’ Equity and should be report-

ed on the balance sheet.

A loan is a liability, not an expense.

C. 1. Don’t close the business, especially if the future looks bright.

Measuring Revenues and Expenses 73

P3–16 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Dec. 31

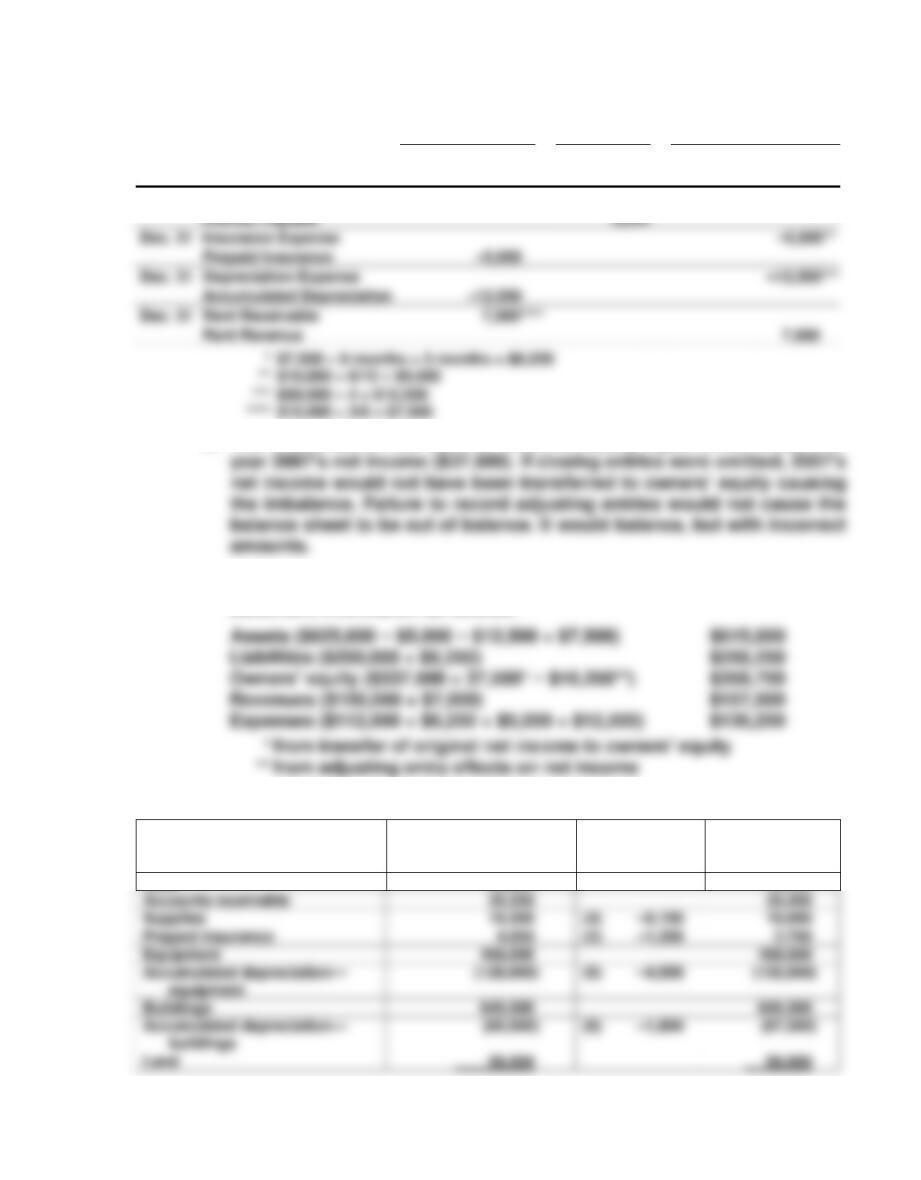

Interest Expense

–6,250*

B. The imbalance on the balance sheet is exactly equal to the amount of

C. The adjusting entries would affect the balance sheet and income

statement information as follows:

P3–17 A. and B.

Account Balance Be-

fore Adjustment

Adjustments

Account

Balance After

Adjustment

Cash

52,500

52,500

Accounts receivable

35,250

35,250

Supplies

19,200

10,050

Prepaid insurance

Buildings

649,500

Interest Payable

Dec. 31

Insurance Expense

Prepaid Insurance

Dec. 31

Depreciation Expense

Accumulated Depreciation

Dec. 31

Rent Receivable

Rent Revenue

74 Chapter 3

Total assets

1,072,500

1,055,700

Unearned revenues

36,000

(3) –12,000

24,000

Accounts payable

27,900

27,900

Interest payable

6,000

(5) 3,000

9,000

C. The net income earned during the year has not yet been transferred to

retained earnings. This is true for both the unadjusted account balance

column (column 1) and for the adjusted account balance column (col-

umn 3).

D. The closing entries need to be identified. Closing entries have the ef-

E. Net income before adjustments $58,500

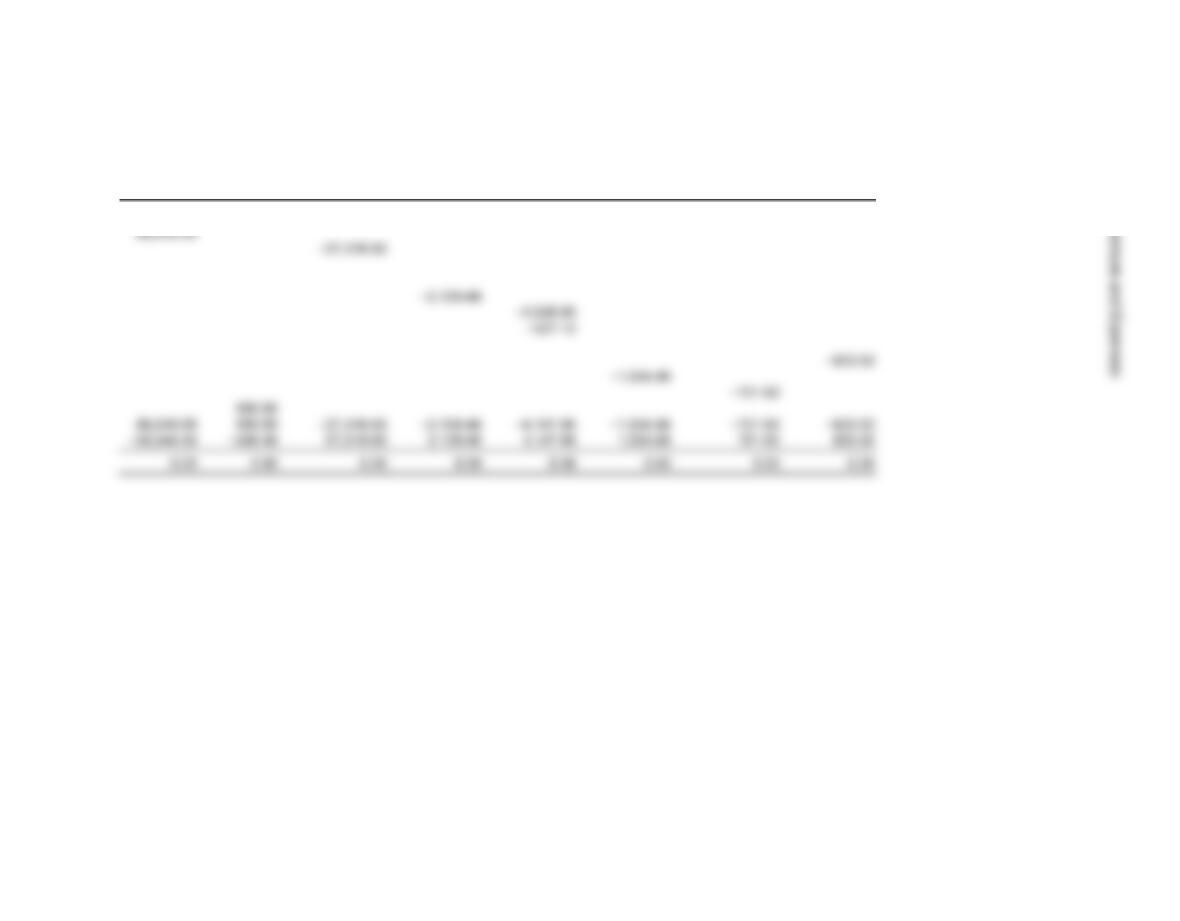

P3–18 a.

Account Type

A. Prepaid Insurance

Asset

B. Retained Earnings

C. Accumulated Depreciation

Asset (negative)

D. Wages Expense

Expense

Wages payable

(1) 4,350

4,350

Notes payable

Common stock

Retained earnings

Rent revenues

(3) 12,000

Wages expense

(1) –4,350

Supplies expense

(4) –9,150

Insurance expense

(2) –1,350

Interest expense

(5) –3,000

Depreciation expense

(6) –6,300

Net income

58,500

46,350

Measuring Revenues and Expenses 75

G. Supplies

Asset

H. Insurance Expense

Expense

P3–19 Mary should be suspicious. The procedures being used permit the sales

rep to receive commissions the rep has not earned. Some of the sales re-

ported for the customer are fictitious. Rather than reducing sales revenue

when the sales are canceled, an expense is recorded. This procedure

overstates revenues and overstates expenses. Because the rep is paid a

P3–20 MEMO

TO: Flora Wiser

FROM: (Student’s Name)

SUBJECT: Processing accounting information

I. Unearned Rent

Liability

Asset

K. Notes Payable

Liability

Expense

Asset

O. Accounts Receivable

Asset

Liability

Q. Supplies Expense

Expense

R. Depreciation Expense

Expense

76 Chapter 3

I have been asked to provide a summary of accounting information pro-

cesses to help you obtain a better understanding of accounting systems

and how they convert data to useful information. In this memo, I will sum-

marize the basic purpose of accounting systems and the processes used

to accomplish this purpose. I will be pleased to meet with you to answer

questions or to discuss other related matters.

Business activities occur in the day-to-day operations of a company. Data

about a company’s business activities are recorded in a company’s infor-

mation system. Some of these data are in the form of financial measures.

These financial measures are recorded in the company’s accounting sys-

tem by identifying specific accounts that are affected by the activities.

Once financial data are recorded in individual accounts, the account bal-

ances are updated periodically. Two primary levels of detail are main-

A company maintains subsidiary accounts for management purposes. It

reports control account balances in financial statements to external users

In addition to updating account balances as transactions occur, an ac-

counting system must adjust these accounts periodically for activities that

Measuring Revenues and Expenses 77

Once all account balances have been updated at the end of a fiscal period,

these balances are used to prepare financial statements. Financial state-

ments are summaries of account balances prepared in specific formats to

P3–22

1

2

3

4

5

6

7

8

9

10

CASES

C3-1

This sales plan has manipulation, distortion, and fraud written all over it. In gen-

eral, very little is favorable. The underlying motivation for each aspect of this plan

appears to be temporary personal enrichment of Flash and his (her?) regional

78 Chapter 3

If these “forced sales” are not reported explicitly as such, creditors and investors

will be misled as to the true amount of this year’s sales and profits. Also, some

distributors have been told they may return these “special” purchases that remain

unsold. At minimum, this is likely to cause unhappiness if returns cannot be

made. This technique cannot be used again next year because distributors will al-

Measuring Revenues and Expenses 79

C3-2

Students will first have to decide what information they wish to provide before an-

alyzing the data in the problem. Based on the chapter discussion, students might

reasonably prepare some or all of the following:

a. Summary of all cash flows

Each of these items is shown below. Because the results of these analyses are so

Interesting questions might include the following:

1. Why are the measurements for net cash flow ($20,950), net cash flow from

operations ($7,950), and net income (loss of $1,610) so different?

2. Did Softech.com have a good first quarter?

3. What are the financial prospects for the second quarter?

a. Summary of Cash Flows:

Purchase of new office furniture $ (500)

80 Chapter 3

b. Summary of Cash Flows Segmented by

Financing, Investing, and Operating Activities

Financing activities:

Loan from bank $ 4,000

c. Net Cash Flow from Operating Activities

Cash receipts:

From accounts receivable $ 6,800

d. Income Statement

Revenues:

Sales $18,000

Expenses:

Measuring Revenues and Expenses 81

e. Balance Sheet

Assets Liabilities and Stockholders’ Equity

Cash $25,190 Accounts payable2 $ 9,450

82 Chapter 3

P3–21

Accounts Accumulated Wages Notes Investment by Retained

Date Cash Receivable Supplies Inventory Equipment Depreciation Payable Payable Owners Earnings

9/30/2007 $ 4,238.72 $ — $ 2,343.28 $235,892.35 $55,650.00 −$12,353.00 $ — $123,452.88 $100,000.00 $62,318.47

10/31/2007 38,246.50

10/31/2007 −27,318.93

The Book Wermz The Book Wermz

Balance Sheet Income Statement

October 31, 2007 For October 2007

Assets Liabilities & Equity Revenues

Measuring Revenues and Expenses 83

P3-21 continued

Service Cost of Supplies Wages Rent Depreciation Interest

Sales Revenues Goods Sold Expense Expense Expense Expense Expense

$ — $ — $ — $ — $ — $ — $ — $ —

84 Chapter 3

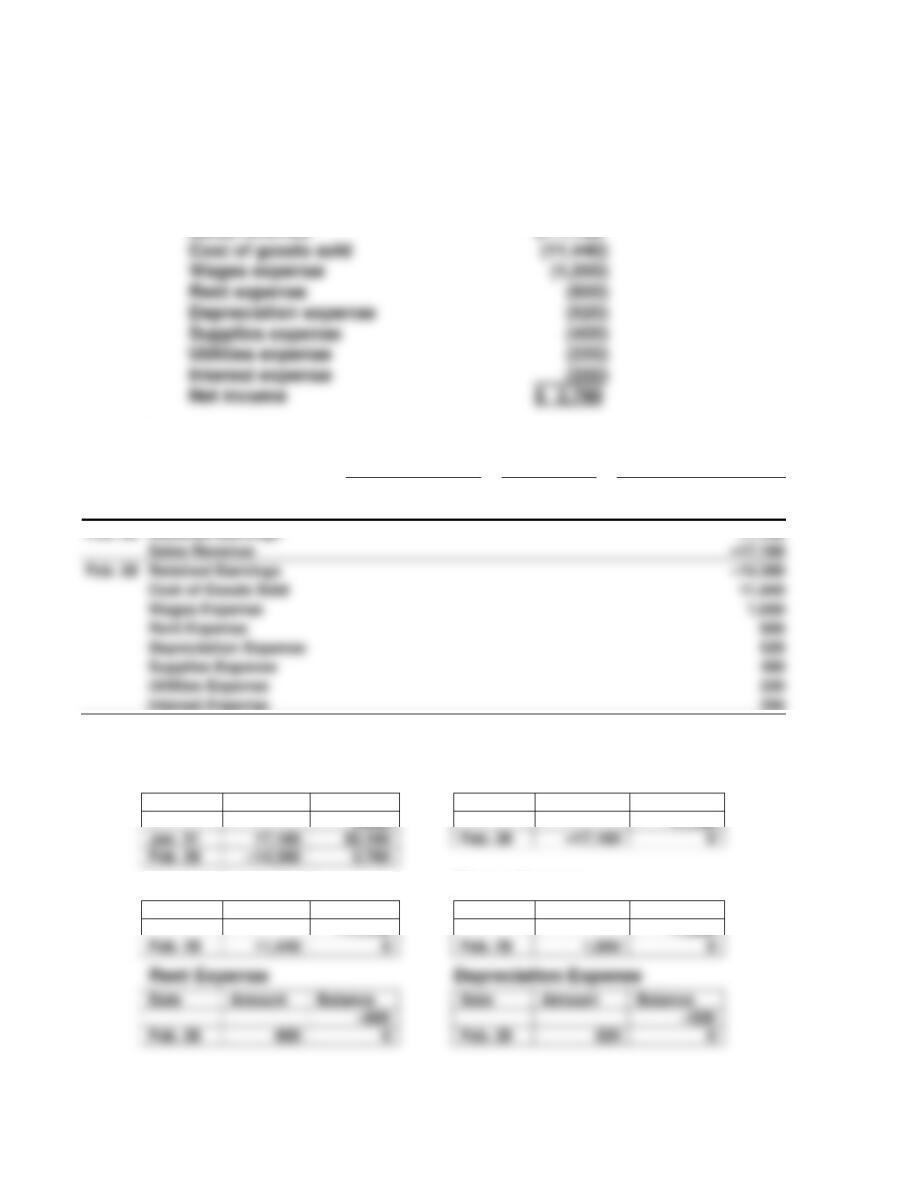

COMPREHENSIVE REVIEW 1

a. Favorite Cookie Company

Income Statement

For the Month Ended February 28, 2007

Sales revenue $ 17,160

b.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Feb. 28

Retained Earnings

Sales Revenue

Feb. 28

Retained Earnings

Cost of Goods Sold

Wages Expense

1,000

Rent Expense

600

Depreciation Expense

520

Supplies Expense

400

Utilities Expense

220

Interest Expense

200

Ledger

Retained Earnings Sales Revenue

Date

Amount

Balance

Date

Amount

Balance

3,000

17,160

Jan. 31

Feb. 28

0

Feb. 28

5,780

Cost of Goods Sold Wages Expense

Date

Amount

Balance

Date

Amount

Balance

–11,440

–1,000

Feb. 28

Feb. 28

0

Date

Amount

Balance

Date

Amount

Balance

Measuring Revenues and Expenses 85

Supplies Expense Utilities Expense

Date

Amount

Balance

Date

Amount

Balance

c. Favorite Cookie Company

Post-Closing Summary of Account Balances

February 28, 2007

Account Balance

Assets:

Total Assets 50,580

Liabilities:

Accounts Payables 1,400

Owners’ Equity:

Contribution by Owners 10,000

Retained Earnings 5,780

Feb. 28

Feb. 28

Date

Amount

Balance

Feb. 28

86 Chapter 3

d. Favorite Cookie Company

Balance Sheet

At February 28, 2007

Assets

Cash $ 7,740

Accounts receivable 4,100

Liabilities and Owners’ Equity

Accounts payable $ 1,400

Unearned revenue 3,000

Measuring Revenues and Expenses 87

COMPREHENSIVE REVIEW 2

a. Additional Transactions and Adjustments

Accounts

Cash

Other

Assets

Liabilities

Contributed

Capital

Retained

Earnings

A.

Sales Revenue

8,400

Accounts Receivable

8,400

Cost of Goods Sold

(4,300)

F.

Wages Payable

(600)

Wages Expense

(3,700)

Cash

(4,300)

G.

Interest Payable

(900)

Cash

(900)

H.

Supplies Expense

Supplies

Wages Expense

Wages Payable

Interest Expense

(1,000)

Interest Payable

1,000

K.

Depreciation Expense

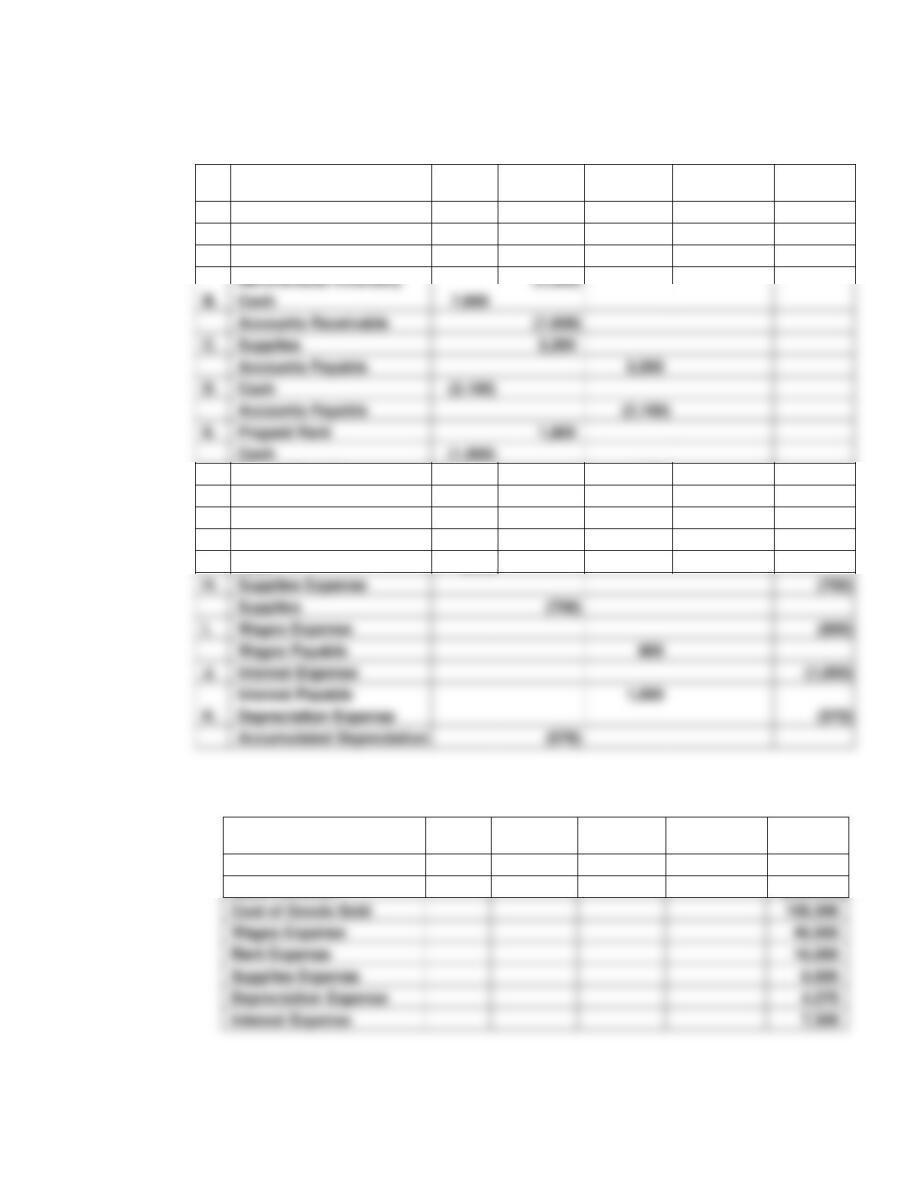

b. Closing Entries

Accounts

Cash

Other

Assets

Liabilities

Contributed

Capital

Retained

Earnings

Retained Earnings

16,430

Sales Revenue

(206,400)

Cost of Goods Sold

109,300

Wages Expense

46,500

Supplies Expense

6,600

Depreciation Expense

4,270

Merchandise Inventory

B.

Cash

Accounts Receivable

C.

Supplies

3,200

Accounts Payable

3,200

D.

Cash

(2,100)

Accounts Payable

Prepaid Rent

1,800

Cash

(1,800)

88 Chapter 3

c. Summary of Account Balances

The solution below is more comprehensive than that required by the

Summary

Additional

Adjusted

Summary

Closing

Post-

Closing

Calculations for

Additional Column

Cash

5,000

(1,500)

3,500

3,500

7,600 – 2,100 – 1,800 –

4,300 – 900

Accounts Receivable

8,000

800

8,800

8,800

8,400 – 7,600

Supplies

3,600

6,100

6,100

3,200 – 700

Prepaid Rent

1,800

3,600

3,600

1,800

Property and

Accumulated De-

Total Assets

Accounts Payable

7,200

7,200

3,200 – 2,100

Wages Payable

2,200

200

2,400

2,400

Interest Payable

100

1,000

1,000

Merchandise

Notes Payable,

Long-Term

76,400

76,400

76,400

Contributed Capital

80,000

80,000

80,000

Retained Earnings

37,200

37,200

16,430

53,630

Equity

Sales Revenue

8,400

Cost of Goods Sold

Rent Expense

16,000

Supplies Expense

6,600

Depreciation Expense

4,270

Interest Expense

7,300

Net Income

19,100

16,430

Total Liabilities &

Measuring Revenues and Expenses 89

d. Income Statement and Balance Sheet

Orlando Co.

Income Statement

For the Year Ended October 31, 2007

Sales Revenue $ 206,400

Orlando Co.

Balance Sheet

October 31, 2007

Assets

Cash $ 3,500

Accounts Receivable 8,800

Total Assets $ 220,630

Liabilities & Owners’ Equity

Accounts Payable $ 7,200

Wages Payable 2,400