Chapter 03 – The Accounting Cycle: End of the Period

Solution

Adjusting entry type: Accrued revenue.

December 31 (adjusting entry)

Debit

Credit

January 9 (external transaction)

Chapter 03 – The Accounting Cycle: End of the Period

Problem #3

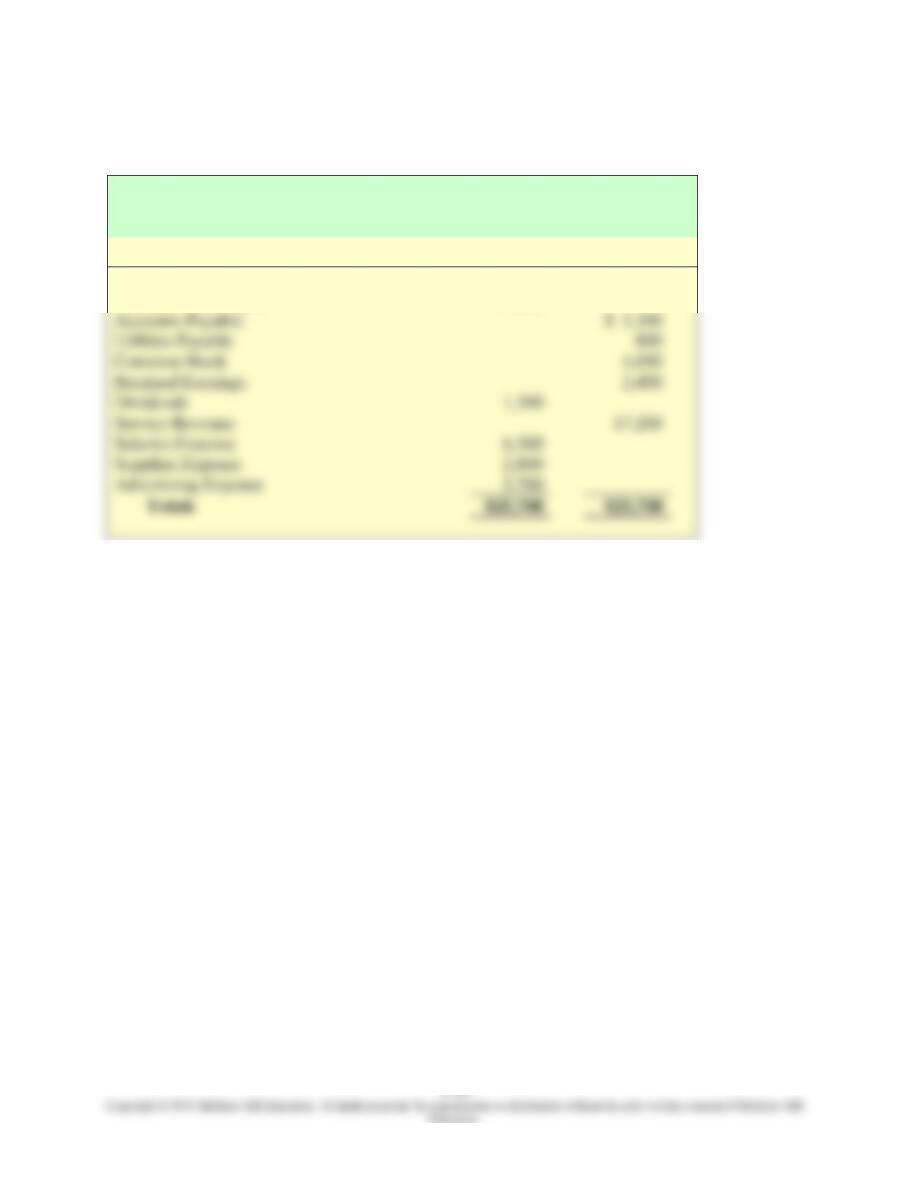

Below is the adjusted trial balance of Swan Dance Academy for December 31.

Swan Dance Academy

Adjusted Trial Balance

December 31

Account Title

Debit

Credit

Cash

$ 3,400

Accounts Receivable

6,200

Accounts Payable

Utilities Payable

Common Stock

Retained Earnings

Dividends

1,300

Service Revenue

Salaries Expense

6,300

Supplies Expense

2,800

Advertising Expense

5,700

Required:

1. Prepare closing entries.

2. Prepare a post-closing trial balance.

3. Compare the balances of retained earnings in the adjusted trial balance and the post-closing

trial balance.

Chapter 03 – The Accounting Cycle: End of the Period

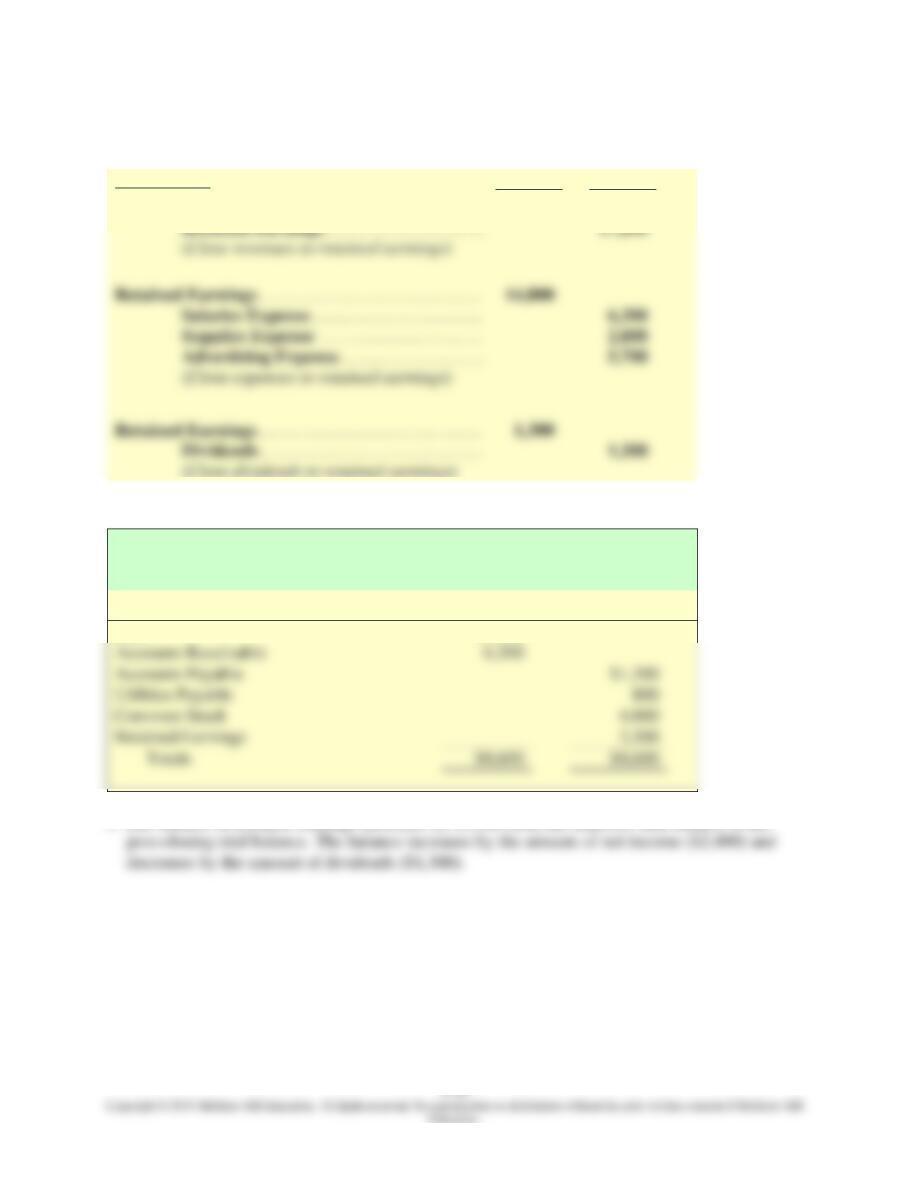

Solution:

1. Closing entries

December 31

Debit

Credit

Service Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . .

17,200

Retained Earnings . . . . . . . . . . . . . . . . . .

17,200

Salaries Expense . . . . . . . . . . . . . . . . . . .

Supplies Expense . . . . . . . . . . . . . . . . . .

Advertising Expense . . . . . . . . . . . . . . . .

Retained Earnings . . . . . . . . . . . . . . . . . . . . . . . . .

2. Post-closing trial balance

Accounts Payable

Common Stock

3. The balance of retained earnings increases by $1,100 from the adjusted trial balance to the

Swan Dance Academy

Post-Closing Trial Balance

December 31

Account Title

Debit

Credit

Cash

$3,400

Chapter 03 – The Accounting Cycle: End of the Period

Common Mistakes

Common Mistakes made by students are highlighted in each of the chapters. With greater

awareness of the potential pitfalls, student can avoid making the same mistakes and gain a deeper

understanding of the chapter material.

Common Mistake

customers, regardless of when cash is received from those customers. Similarly, you might think

that expenses can be recorded only when cash is paid, but we record expenses when costs are

presumed to have been used to help generate revenues, regardless of when cash is paid.

It’s easy at first to think that revenue should be recorded only when cash is received. However,

Common Mistake

When a cash prepayment has occurred, students sometimes confuse the initial cash entry (the

prepayment) with the adjusting entry that follows. The cash flow is not the adjusting entry. The

adjusting entry is to recognize the expense that has occurred after the cash flow.

Common Mistake

When recording the interest payable on a borrowed amount, students sometimes mistakenly

Common Mistake

entries will never include the Cash account. Note that no adjusting entries are posted to the Cash

account in Illustration 3–9.

Students sometimes mistakenly include the Cash account in an adjusting entry. Typical adjusting

Common Mistake

Students sometimes believe that closing entries are meant to reduce the balance of Retained

Chapter 03 – The Accounting Cycle: End of the Period

Decision Points and Decision Maker’s Perspective

Decision Points and Decision Maker’s Perspectives are provide throughout each chapter to give

insight into how measurement and communication of financial accounting information help

decision makers.

Decision Points

Question

Accounting Information

Analysis

The amounts reported

Income statement

Revenue and expense accounts

Decision Maker’s Perspective

Is the Balance Sheet Like a Photo or an MRI?

In Chapter 1, we mentioned that a balance sheet is like a photograph since it shows events at a

point in time, whereas an income statement is like a video since it shows events over time. This

Chapter 03 – The Accounting Cycle: End of the Period

Ethical Dilemma

You have recently been employed by a large clothing retailer. One of your tasks is to help

prepare financial statements for external distribution. The company’s lender, National Savings &

Loan, requires that financial statements be prepared according to generally accepted accounting

principles (GAAP). During the months of November and December 2021, the company spent $1

million on a major TV advertising campaign. The $1 million included the costs of producing the

commercials as well as the broadcast time purchased to run them. Because the advertising will be

aired in 2021 only, you charge all the costs to advertising expense in 2021, in accordance with

requirements of GAAP.

Key Issues

• Recording all advertising expense in 2021 (instead of delaying a portion until 2022) has

the effect of reducing net income.

• Since the bank requires the company to maintain profitability, recording all advertising

expenses in 2021 causes the company to lose good standing.

• Strictly following the rules of accounting vs. the use of discretion

• What is the role of an employee? Do the right thing or do what your boss tells you?

Option 1: Expense advertising costs immediately per GAAP

• GAAP guidelines are in place for accountants to follow, and the correct action is to

Option 2: Establish a prepaid advertising account to delay the recognition of some expenses

• Why do I have to be the employee to take on the burden of standing up to the CFO? Is

my job not to do as I am told?

Chapter 03 – The Accounting Cycle: End of the Period

Chapter 03 – The Accounting Cycle: End of the Period

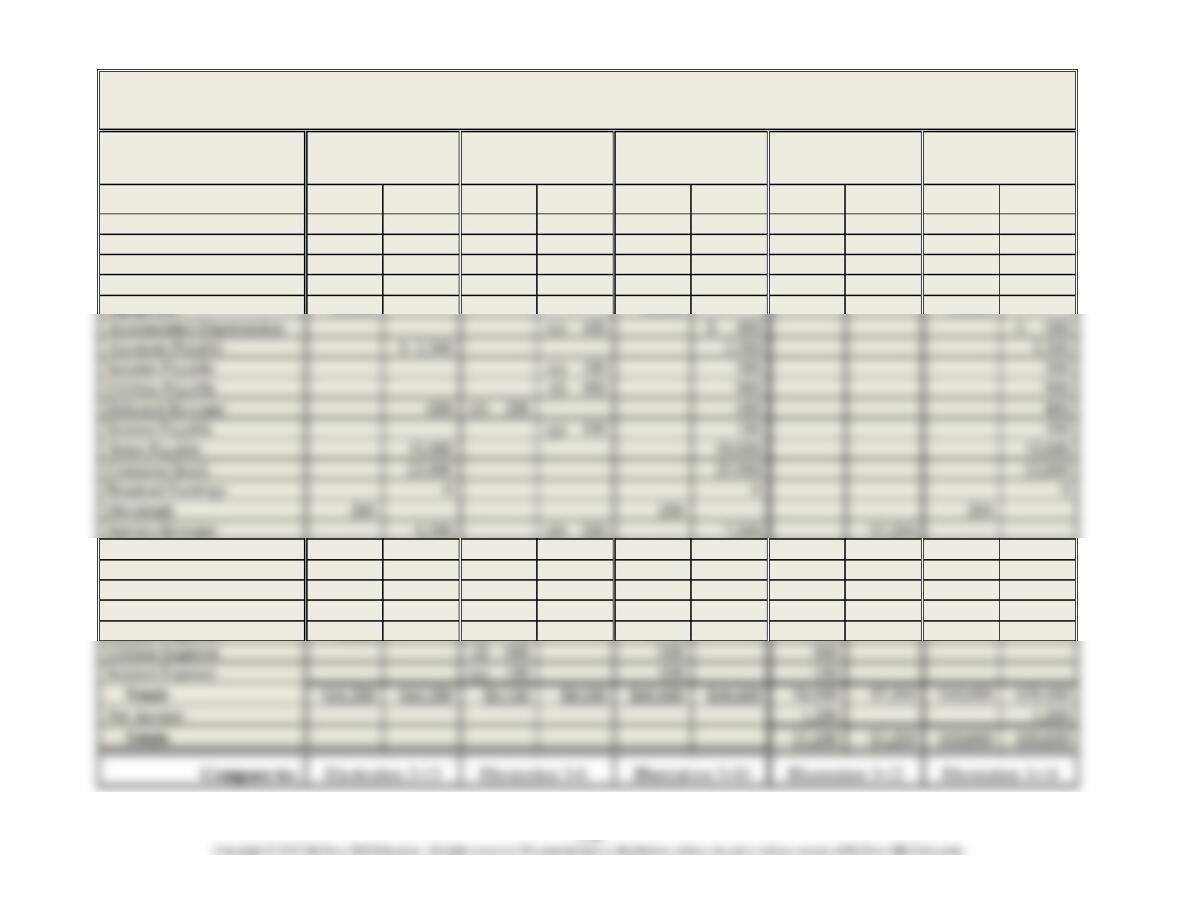

EAGLE SOCCER ACADEMY

Worksheet

December 31

Unadjusted

Trial Balance

Adjusting

Entries

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Accounts

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Cash

$ 6,900

$ 6,900

$ 6,900

Accounts Receivable

2,000

(h) 700

2,700

2,700

Supplies

2,300

(b) 1,000

1,300

1,300

Prepaid Rent

6,000

(a) 500

5,500

5,500

Equipment

24,000

24,000

24,000

Accumulated Depreciation

(c) 400

Accounts Payable

Salaries Payable

(e) 300

Utilities Payable

900

900

Deferred Revenue

(d) 200

Interest Payable

(g) 100

Notes Payable

Common Stock

Retained Earnings

Dividends

200

200

200

Service Revenue

(d) 200

(h) 700

Rent Expense

(a) 500

500

$ 500

Supplies Expense

(b) 1,000

1,000

1,000

Depreciation Expense

(c) 400

400

400

Salaries Expense

2,800

(e) 300

3,100

3,100

Utilities Expense

(f) 900

900

Interest Expense

(g) 100

100

$4,100

$6,000

Net Income

1,200

$7,200

Chapter 03 – The Accounting Cycle: End of the Period

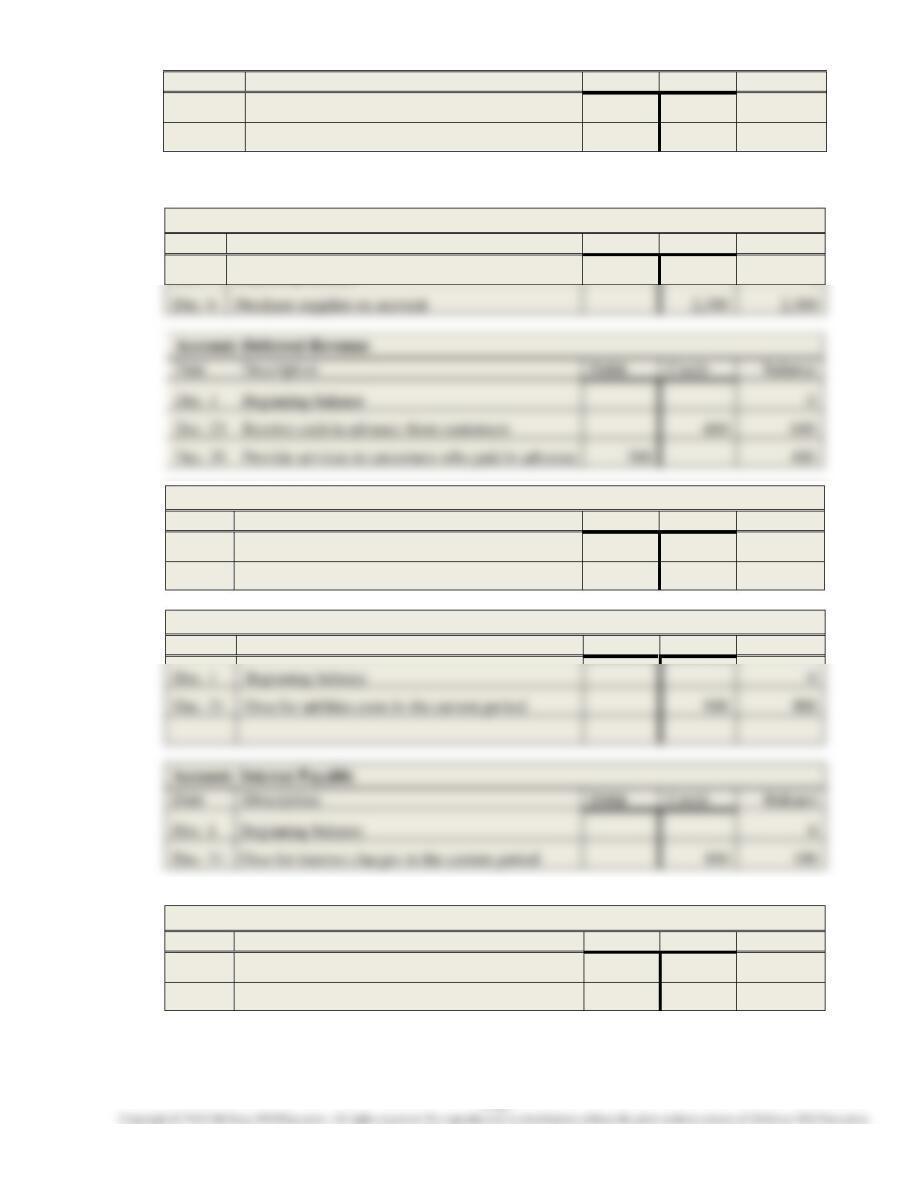

General Ledger of Eagle Soccer Academy After Adjusting Entries

(Illustration 3-9, page 124)

ASSETS

Account: Cash

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Issue common stock for cash

25,000

25,000

Dec. 1

Borrow by signing three-year note

Dec. 1

Purchase equipment for cash

11,000

Dec. 1

Prepay rent with cash

5,000

Dec. 23

Receive cash in advance from customers

9,900

Dec. 28

Pay salaries to employees

7,100

Dec. 30

Pay cash dividends

6,900

Account: Accounts Receivable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 17

Provide services to customers on account

2,000

2,000

Dec. 31

Bill customers for services during the month

700

2,700

Account: Supplies

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 6

Purchase supplies on account

2,300

2,300

Dec. 31

Consume supplies during the current period

1,300

Account: Prepaid Rent

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Prepay rent with cash

6,000

Dec. 31

Reduce prepaid rent due to passage of time

5,500

Account: Equipment

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Purchase equipment for cash

24,000

24,000

Account: Accumulated Depreciation

Chapter 03 – The Accounting Cycle: End of the Period

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Depreciate equipment

400

400

LIABILITIES

Account: Accounts Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 6

Purchase supplies on account

2,300

Account: Deferred Revenue

Date

Description

Debit

Credit

Dec. 1

Beginning balance

Dec. 23

Receive cash in advance from customers

Dec. 31

Provide services to customers who paid in advance

200

400

Account: Salaries Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Owe for salaries earned in the current period

300

300

Account: Utilities Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Owe for utilities costs in the current period

Account: Interest Payable

Date

Description

Debit

Credit

Balance

Dec. 1

0

Dec. 31

100

Account: Notes Payable

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Borrow by signing three-year note

10,000

10,000

Chapter 03 – The Accounting Cycle: End of the Period

STOCKHOLDERS’ EQUITY

Account: Common Stock

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Issue common stock for cash

25,000

25,000

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

Account: Dividends

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

Dec. 30

Pay cash dividends

200

Account: Service Revenue

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 12

Providing training to customers for cash

4,300

4,300

Dec. 17

Providing training to customers on account

2,300

6,300

Dec. 31

Provide services to customers who paid in advance

200

6,500

Dec. 31

Bill customers for services during the month

700

7,200

Account: Rent Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Reduce prepaid rent due to passage of time

500

Account: Supplies Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Consume supplies during the period

1,000

Account: Depreciation Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 31

Depreciate equipment

400

400

Chapter 03 – The Accounting Cycle: End of the Period

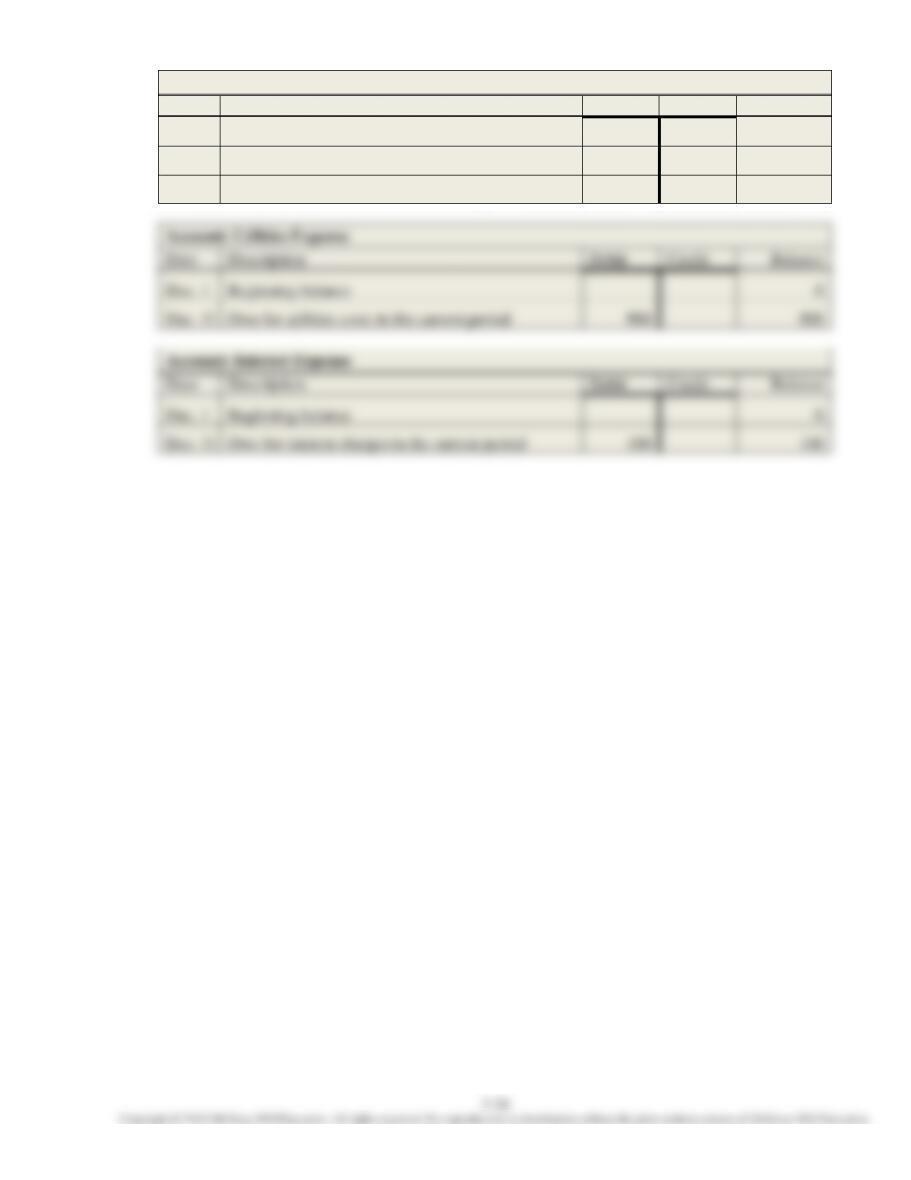

Account: Salaries Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 6

Pay salaries to employees

2,800

2,800

Dec. 31

Owe for salaries earned in the current period

300

3,100

Date

Description

Debit

Credit

Dec. 1

Beginning balance

Dec. 31

Owe for utilities costs in the current period

Account: Interest Expense

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

Dec. 31

Owe for interest charges in the current period