An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Value-added time (minutes):

Assembly of PC board

Stereo assembly

Time to test one unit

Pack and label

Total

Non-value-added time (minutes):

Wait time:

Within-batch wait time – PC board assembly

Within-batch wait time – final assembly

Within-batch wait time – testing

Within batch wait time – shipping

Test setup

Total wait time

Move time:

Move from PC board assembly to final assembly

Move from final assembly to testing

Total move time

Total non-value-added time

Total lead time (minutes)

Value-Added Time / Total Time = Value-Added Ratio

2.

[Key essay answer here]

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

0%

Problem 27(12)-2A

Name:

Section:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Value-added time (minutes):

Assembly of PC board 5

Stereo assembly 15

Non-value-added time (minutes):

Wait time:

Within-batch wait time – PC board assembly 220

Within-batch wait time – final assembly 660

Move time:

Move from PC board assembly to final assembly 10

Move from final assembly to testing 20

2.

Cells with non-gray backgrounds are protected and cannot be edited.

The existing process is very wasteful. The company could improve the process by changing

the layout from a process orientation to a product orientation. Each stereo model could be

formed into a production cell. Each cell would have PC board assembly, final assembly, and

shipping next to each other. In this way, the batch sizes could be reduced significantly.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

Problem 27(12)-2A

Name:

Solution

Section:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Value-added time (minutes):

Stamping

Appliance assembly

Time to test one unit

Pack and label

Total

Non-value-added time (minutes):

Wait time:

Within-batch wait time – stamping

Within-batch wait time – final assembly

Within-batch wait time – testing

Within batch wait time – shipping

Stamping setup

Total wait time

Move time:

Move from stamping to final assembly

Move from final assembly to testing

Total move time

Total non-value-added time

Total lead time (minutes)

Value-Added Time / Total Time = Value-Added Ratio

2.

[Key essay answer here]

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

0%

Problem 27(12)-2B

Name:

Section:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Value-added time (minutes):

Stamping 5

Non-value-added time (minutes):

Wait time:

Within-batch wait time – stamping 195

Within-batch wait time – final assembly 858

Move time:

2.

Cells with non-gray backgrounds are protected and cannot be edited.

The existing process is very wasteful. The company could improve the process by changing

the layout from a process orientation to a product orientation. Each appliance model could

be formed into a production cell. Each cell would have stamping, final assembly, and

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

Problem 27(12)-2B

Name:

Solution

Section:

ON

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Budgeted cell conversion cost rate:

Total Conversion Cost / Planned Production Hours = Rate per Hour

2.

Budgeted cell conversion cost per unit

Rate per Hour Time = Cost per Unit

3. Debit Credit

a.

b.

c.

d.

4.

Ending balances:

Raw and In Process Inventory

Finished Goods Inventory

5.

[Key essay answer here]

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Account

Cells with non-gray backgrounds are protected and cannot be edited.

Problem 27(12)-3A

Name:

Section:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Budgeted cell conversion cost rate:

Total Conversion Cost / Planned Production Hours = Rate per Hour

$660,000 2,200 $300.00

2.

Budgeted cell conversion cost per unit

Rate per Hour Time = Cost per Unit

$300 0.250 $75.00

3. Debit Credit

a. 1,620,000

1,620,000

4.

Ending balances:

Raw and In Process Inventory $74,250

5.

Lean accounting is different from traditional accounting in a number of respects. Most importantly, lean

accounting is simplified and uses minimal control. As a result, the number of transactions are reduced,

and the control intervals between adjacent work in process transaction points are widened. In many

these costs do not need to be allocated, since they are included directly in the cell’s conversion cost.

Problem 27(12)-3A

Name:

Solution

Section:

Raw and In Process Inventory

Accounts Payable

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

Key Code:

Account

Cells with non-gray backgrounds are protected and cannot be edited.

Conversion Costs

Finished Goods Inventory

Raw and In Process Inventory

Accounts Receivable

Finished Goods Inventory

Cost of Goods Sold

Raw and In Process Inventory

“raw and in process inventory” account. Direct labor is frequently eliminated as a cost category and is

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Budgeted cell conversion cost rate:

Total Conversion Cost / Planned Production Hours = Rate per Hour

2.

Budgeted cell conversion cost per unit:

Rate per Hour Time = Cost per Unit

3. Debit Credit

a.

b.

c.

d.

4.

Ending balances:

Raw and In Process Inventory

Finished Goods Inventory

5.

[Key code here]

Answers are entered in the cells with gray backgrounds.

Problem 27(12)-3B

Name:

Section:

Score:

Key Code:

Instructions

Account

Cells with non-gray backgrounds are protected and cannot be edited.

0%

[Key essay answer here]

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Budgeted cell conversion cost rate:

Total Conversion Cost / Planned Production Hours = Rate per Hour

$189,000 2,100 $90.00

2.

Conversion Costs

Finished Goods Inventory

Raw and In Process Inventory

Accounts Receivable

Finished Goods Inventory

Cost of Goods Sold

Budgeted cell conversion cost per unit:

3. Debit Credit

a. 1,979,500

1,979,500

b. 189,000

4.

Ending balances:

Raw and In Process Inventory $97,900

5.

Accounts Payable

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

Account

Cells with non-gray backgrounds are protected and cannot be edited.

Problem 27(12)-3B

Name:

Solution

Section:

Raw and In Process Inventory

Raw and In Process Inventory

Lean accounting is different from traditional accounting in a number of respects. Most importantly, lean

accounting is simplified and uses minimal control. As a result, the number of transactions is reduced,

result, these costs do not need to be allocated, since they are included directly in the cell’s conversion

“raw and in process inventory” account. Direct labor is frequently eliminated as a cost category and is

instead included as a conversion cost of the cell. The cell conversion cost is also applied to the raw

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

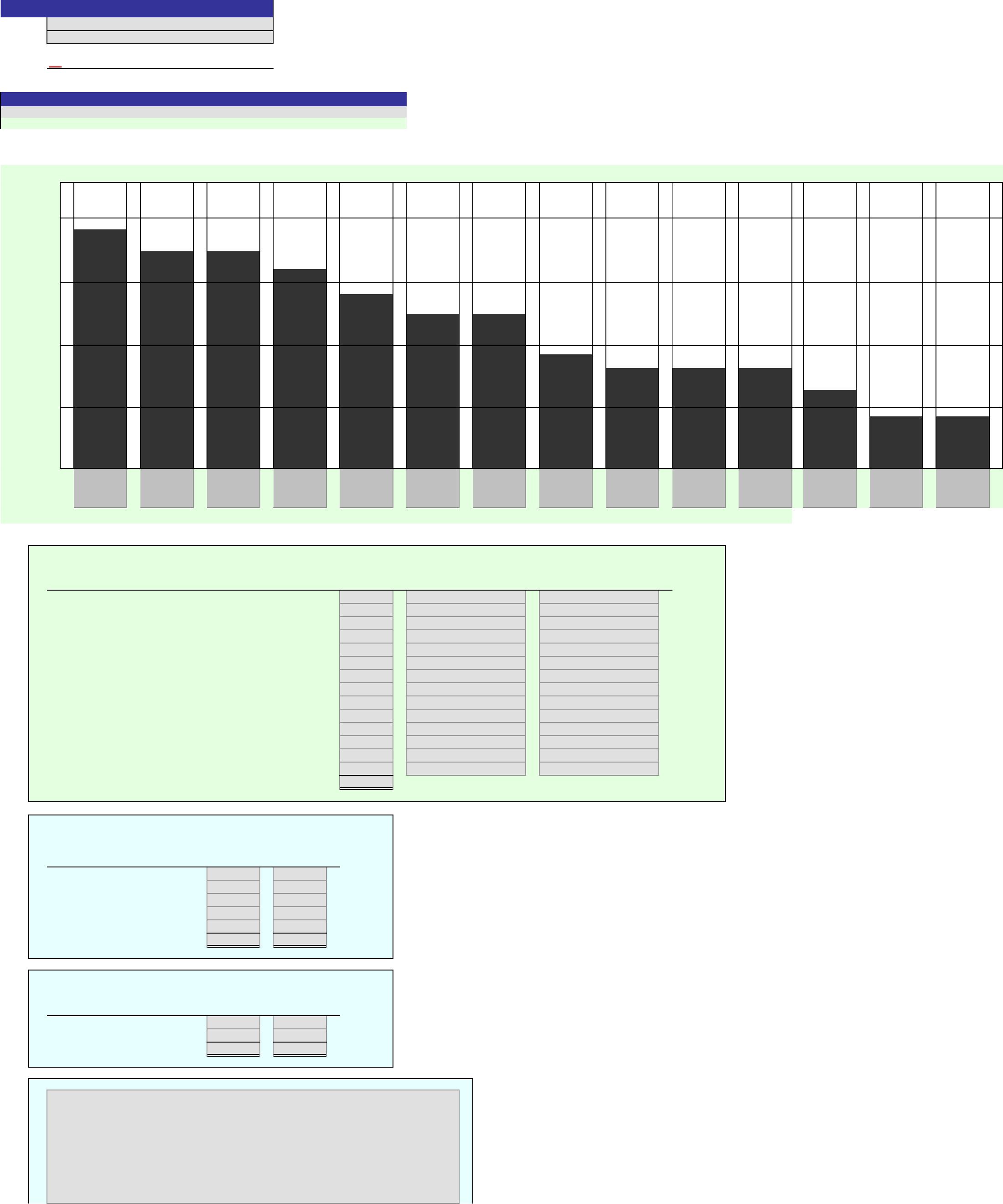

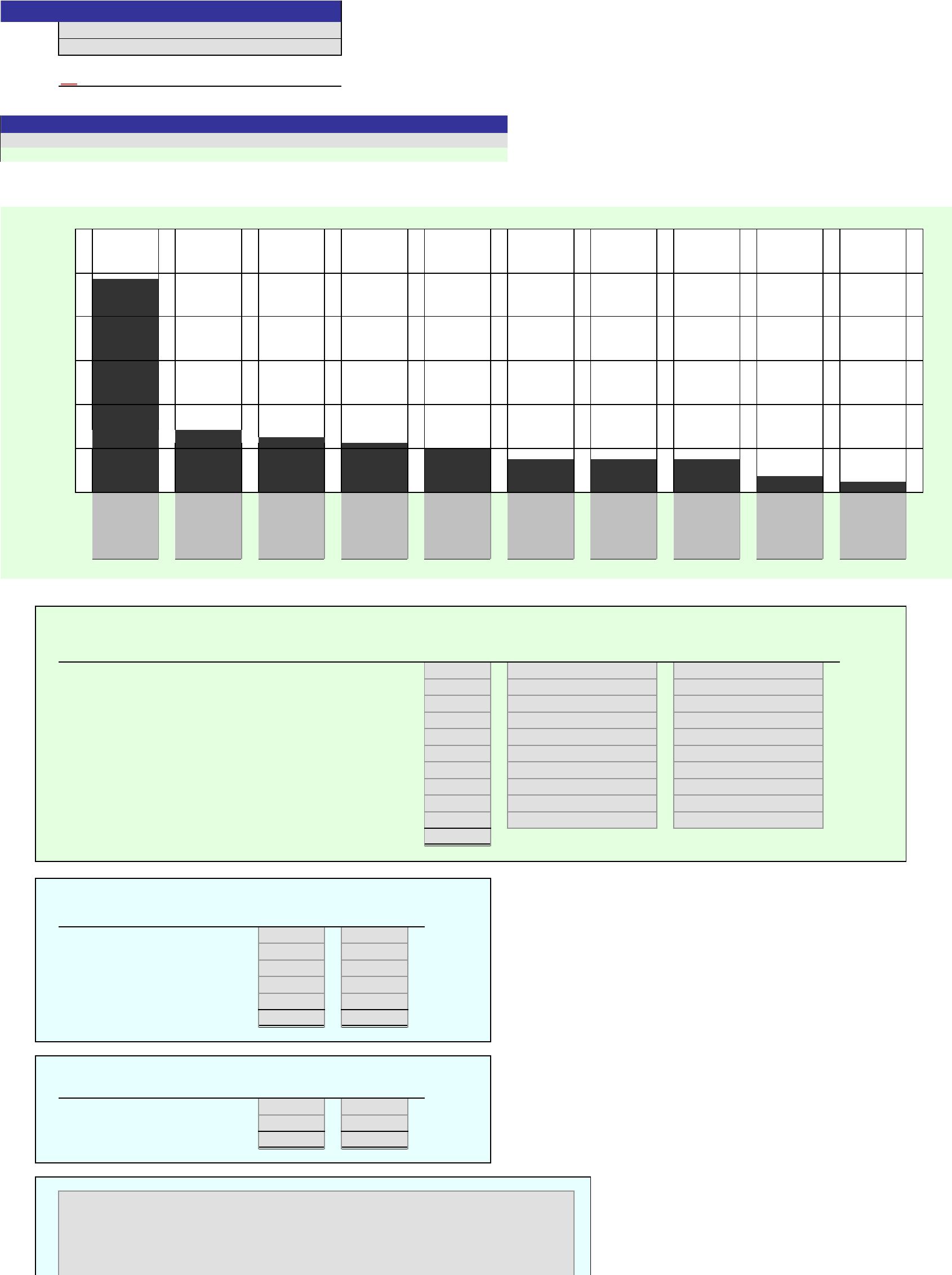

In the chart, choose the correct title for each bar.

1.

2.

Activity

Quality Activities Cost

Patient registration

Verifying patient information

Assigning patients

Searching/waiting for doctore

Doctor exam

Waiting for transport

Transporting patients

Verifying lab orders

Searching for equipment

Incorrect labs

Lab tests

Counting supplies

Looking for supplies

Staff training

Total

3.

Percent of

Quality Cost Activity Total

Classification Cost Department Cost

Prevention

Appraisal

Internal failure

External failure

Other patient care

Total

4.

Percent of

Activity Total

Cost Department Cost

Value-added

Non-value-added

Total

5.

$20,000

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

$5,000

Problem 27(12)-4A

Name:

Section:

Cells with non-gray backgrounds are protected and cannot be edited.

Pareto Chart⎯Quality Activities

Value–Added/

Cost of Quality

Classification

Non-Value-Added

Classification

$10,000

[Key essay answer here]

$15,000

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

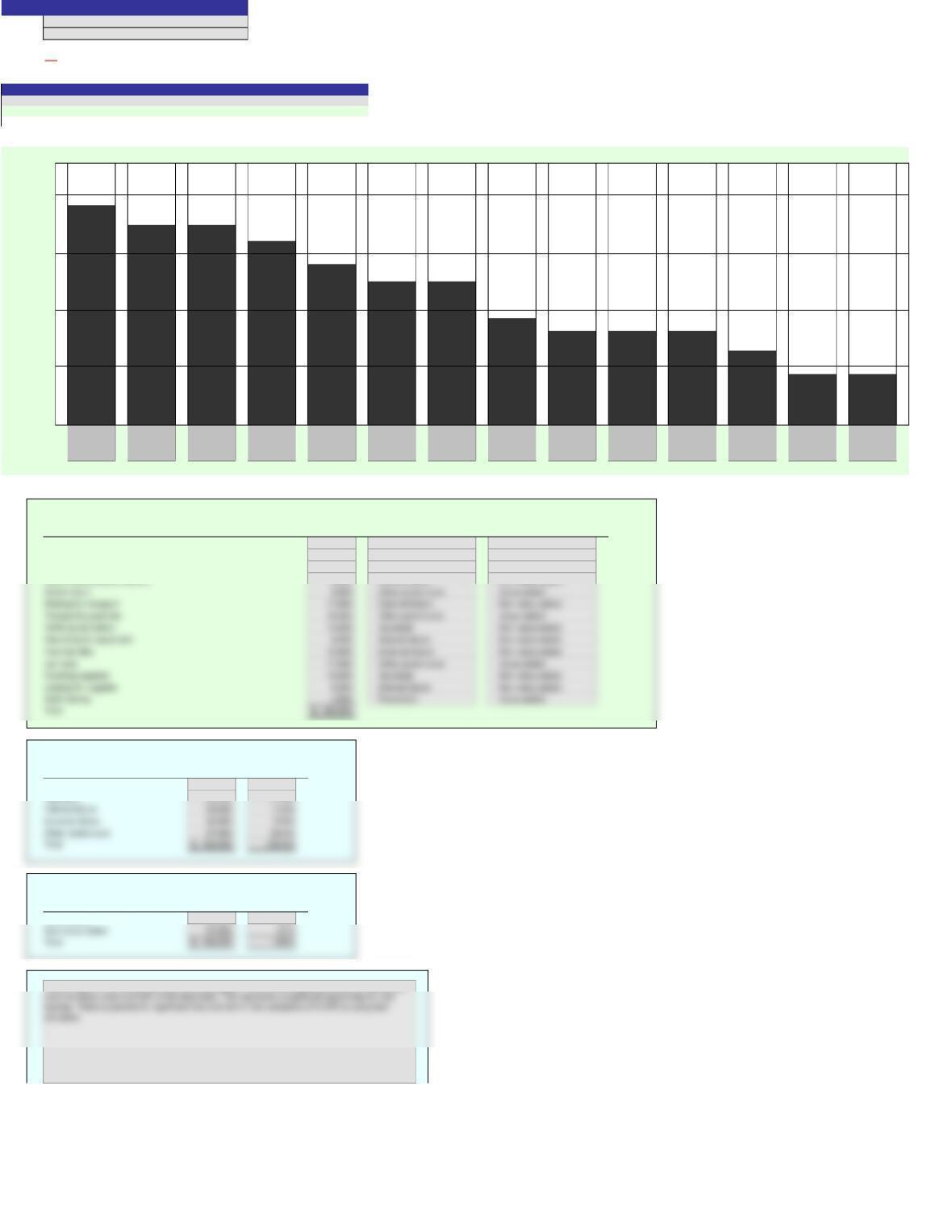

In the chart, choose the correct title for each bar.

1.

Counting

supplies

Lab tests

Waiting for

transports

Transport-ing

patients

Verifying lab

orders

Assigning

patients

Incorrect labs

Verifying

patient

information

Looking for

supplies

Searching for

equipment

Searching/

waiting for

doctor

Patient

registration

Doctor exam Staff training

2.

Activity

Quality Activities Cost

Patient registration 6,400$

Verifying patient information 9,600

Assigning patients 12,800

Searching/waiting for doctore 8,000

3.

Percent of

Quality Cost Activity Total

Classification Cost Department Cost

Prevention 4,800$ 3.0%

Appraisal 43,200 27.0%

4.

Percent of

Activity Total

Cost Department Cost

Value-added 62,400$ 39%

5.

Key Code:

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

Pareto Chart⎯Quality Activities

Cells with non-gray backgrounds are protected and cannot be edited.

Problem 27(12)-4A

Name:

Solution

Section:

ON

$5,000

Value–Added/

Non-Value-Added

Classification

Value-added

Cost of Quality

Classification

Other patient care

Appraisal

Other patient care

Non-value-added

Value-added

Non-value-added

$20,000

$15,000

$10,000

Internal failure

The ER has 61% of its total costs as non-value-added. This is a very significant amount. Internal and

Other patient care

External failure

Other patient care

Value-added

Non-value-added

Non-value-added

Value-added

Non-value-added

Value-added

Appraisal

Non-value-added

Value-added

Non-value-added

Non-value-added

Internal failure

Prevention

External failure

Other patient care

Appraisal

Internal failure

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

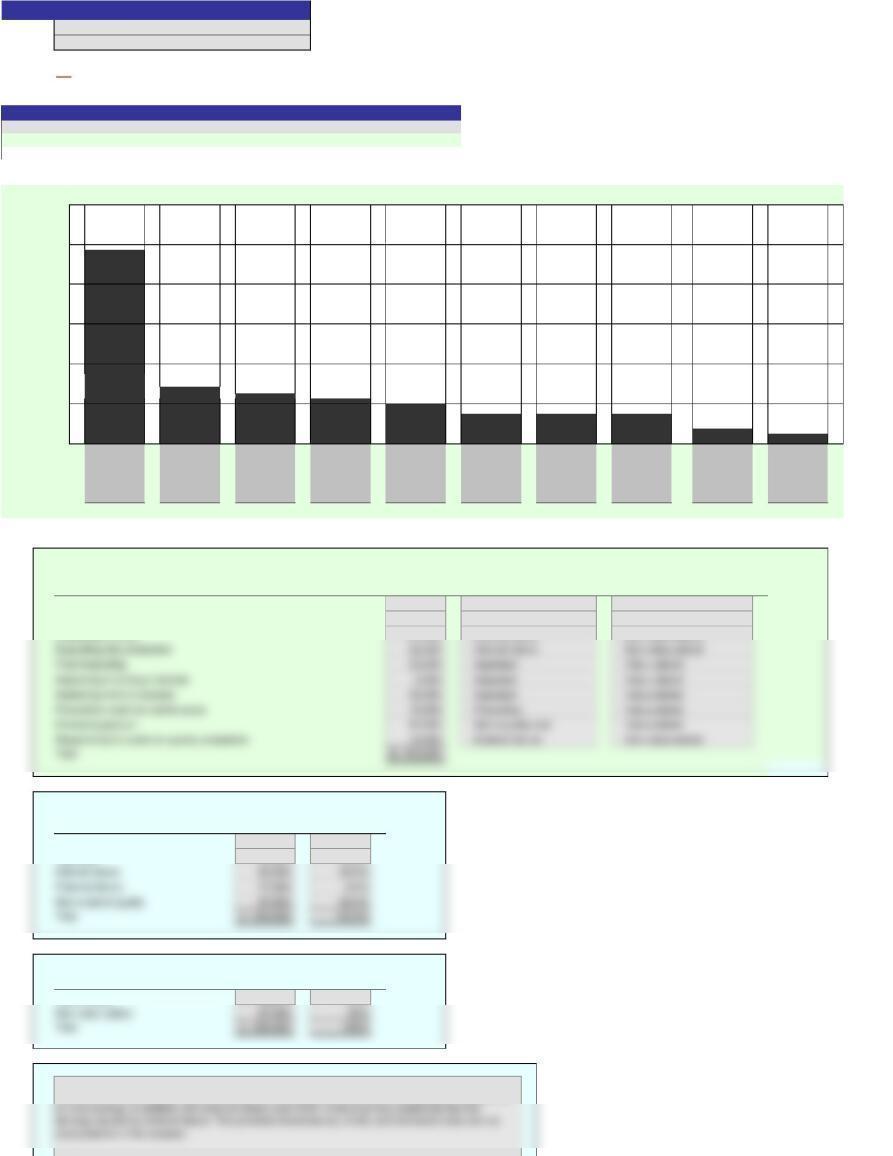

Enter a zero in cells you would otherwise leave blank.

1.

2.

Activity

Quality Activities Cost

Correcting invoice errors

Disposing of incoming materials with poor quality

Disposing of scrap

Expediting late production

Final inspecting

Inspecting incoming materials

Inspecting work in process

Preventive machine maintenance

Producing product

Responding to customer quality complaints

Total

3. Percent of

Quality Cost Activity Total

Classification Cost Department Cost

Prevention

Appraisal

Internal failure

External failure

Not a cost of quality

Total

4. Percent of

Activity Total

Cost Department Cost

Value-added

Non-value-added

Total

5.

$100,000

$40,000

$20,000

$80,000

$60,000

[Key essay answer here]

$0

Value-Added/

Cost of Quality

Classification

Non-Value-Added

Classification

Problem 27(12)-4B

Name:

Section:

Pareto Chart⎯Department Activities

$120,000

Cells with non-gray backgrounds are protected and cannot be edited.

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

1.

Producing

product

Disposing

scrap

Inspecting

work in

process

Expediting

late

production

Final

inspecting

Disposing

incoming

materials with

poor quality

Preventive

machine

mainten-ance

Responding

to customer

complaints

Correcting

invoice errors

Inspecting

incoming

materials

2.

Activity

Quality Activities Cost

Correcting invoice errors 7,500$

Disposing of incoming materials with poor quality 15,000

Disposing of scrap 27,500

3. Percent of

Quality Cost Activity Total

Classification Cost Department Cost

Prevention 15,000$ 6.0%

Appraisal 50,000 20.0%

4. Percent of

Activity Total

Cost Department Cost

Value-added 162,500$ 65%

5.

Non-value-added

Non-value-added

Cost of Quality

Classification

External failure

Internal failure

Internal failure

The company has 65% of its total costs as value-added. However, there is still room for significant

improvement. Internal failure represents 26% of the total costs. This represents significant opportunity

Non-Value-Added

Classification

Non-value-added

Pareto Chart⎯Department Activities

$0

$20,000

$40,000

$80,000

Problem 27(12)-4B

Name:

Solution

Section:

Value-Added/

$60,000

ON

Score:

$100,000

$120,000

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

Value-added

Non-value-added

Value-added

Non-value-added

Value-added

Value-added

Value-added

Internal failure

Appraisal

Appraisal

Appraisal

Prevention

Not a quality cost

External failure