1. The lean philosophy focuses on reducing time, cost, and poor quality within manufacturing

and nonmanufacturing processes.

2. Move time and wait time in inventory are examples of non-value-added lead time.

3. A product-oriented layout can be designed to minimize materials movements and reduce (or

4. Long setup times lead to large production runs (batch sizes) in order to amortize the cost of

5. Pull or “make to order” manufacturing requires the manufacturer to build product only as it is

6. Product defects can cause additional costs and unpredictability in the process in the form of

scrap, rework, record keeping, and inspection. In addition, product defects can cause a

7. With supply chain management, long-term relationships are established with suppliers and

customers to improve quality, cost, and delivery. Traditional relationships are usually

8. A lean environment will result in fewer (or no) work in process control points. As a result,

9. The raw and in process inventory account combines the materials and work in process

10. Direct labor and indirect labor activities become combined in a lean environment.

CHAPTER 27 (FIN MAN); CHAPTER 12 (MAN)

LEAN PRINCIPLES, LEAN ACCOUNTING,

DISCUSSION QUESTIONS

AND ACTIVITY ANALYSIS

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

DISCUSSION QUESTIONS (Concluded)

11. A Pareto chart shows the totals of a particular attribute for a number of categories. The

12. Non-value-added activities are activities that are viewed as unnecessary from the customer’s

p

erspective. These activities are generally considered wasteful and are candidates for

elimination through process improvements.

p

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

PE 27–1A (FIN MAN); PE 12–1A (MAN)

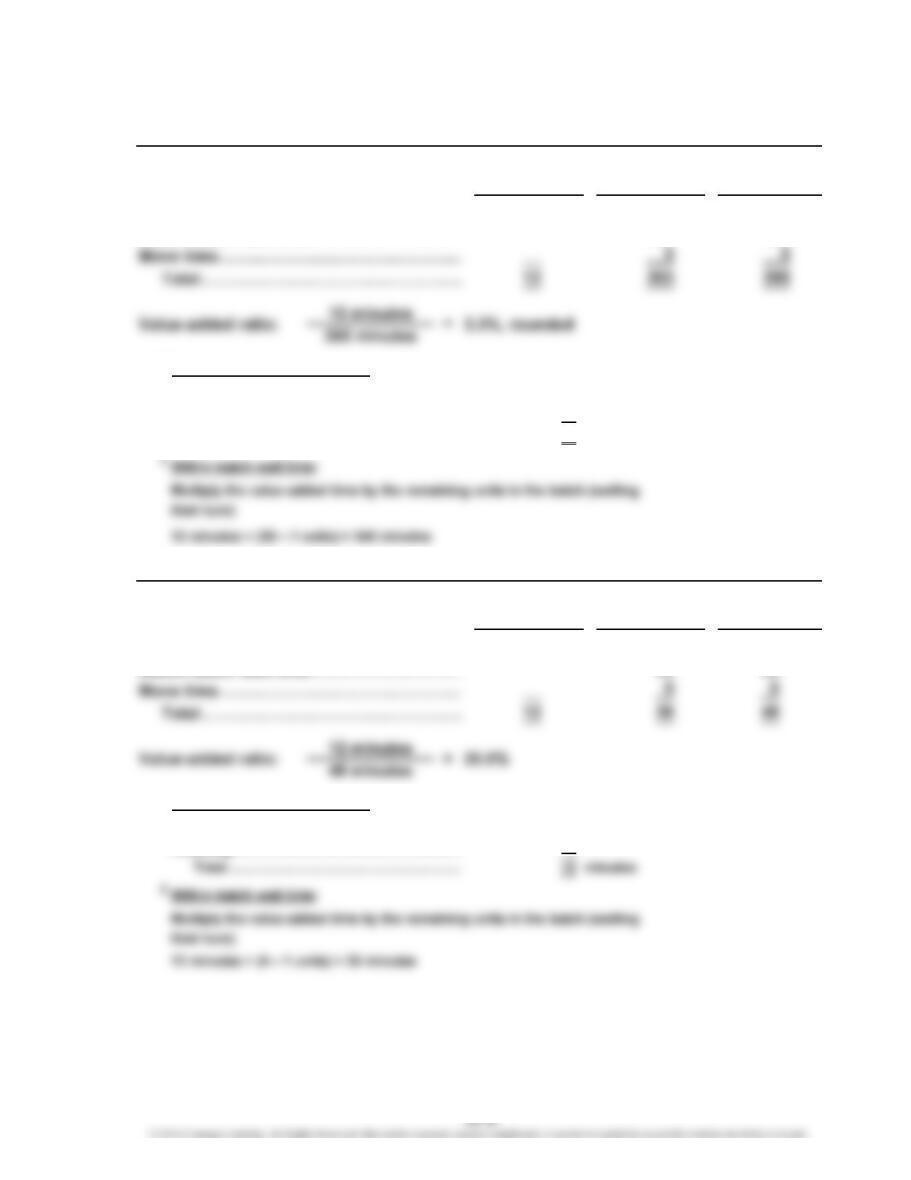

a.

V

alue-added lead time………………………

…

24 min. (14 min. + 10 min.)

Non-value-added lead time:

24 min.

728 min.

PE 27–1B (FIN MAN); PE 12–1B (MAN)

a.

V

alue-added lead time………………………

…

19 min. (11 min. + 8 min.)

Non-value-added lead time:

19 min.

1,915 min.

PE 27–2A (FIN MAN); PE 12–2A (MAN)

PE 27–2B (FIN MAN); PE 12–2B (MAN)

b. Smaller batch sizes

b. Value-added ratio: = 1.0%

PRACTICE EXERCISES

Value-added ratio:b. = 3.3%

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

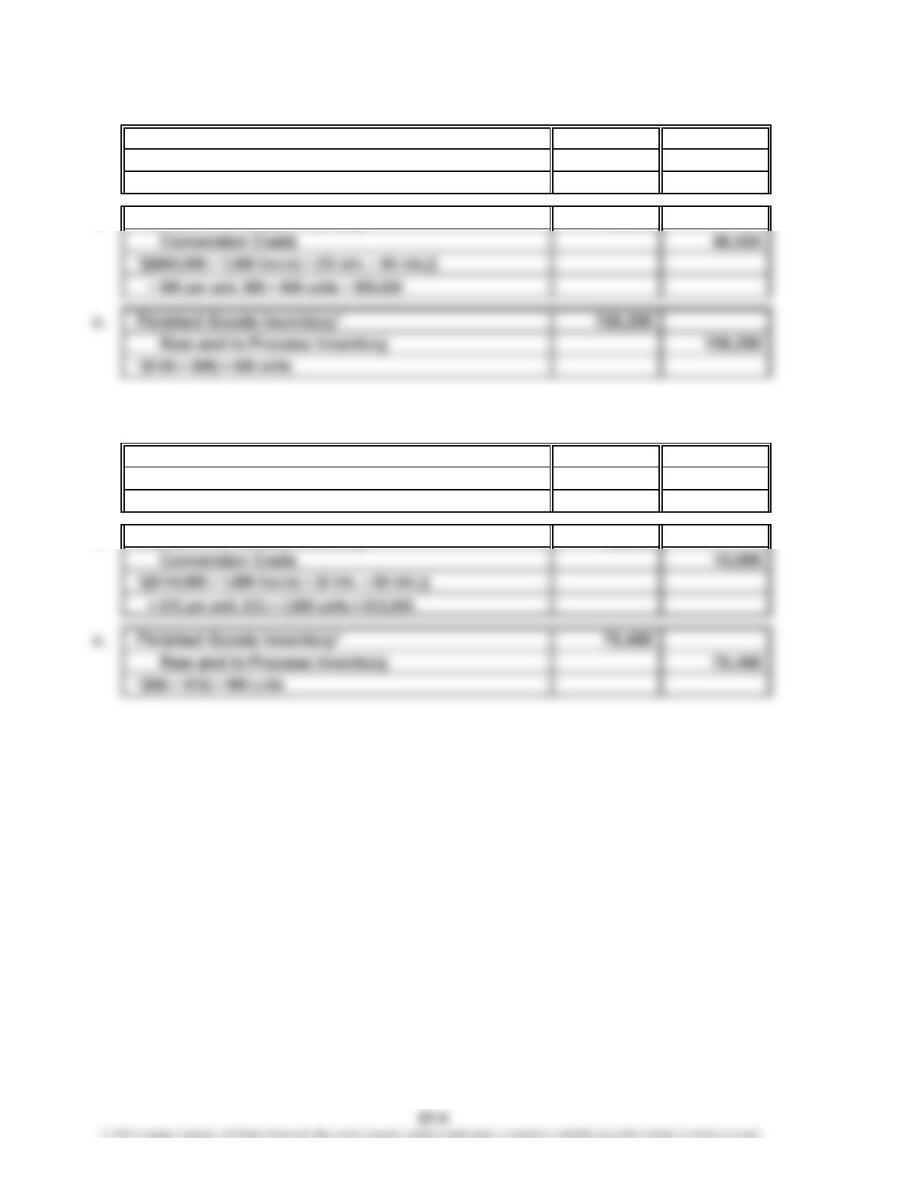

PE 27–3A (FIN MAN); PE 12–3A (MAN)

a. Raw and In Process Inventory* 112,000

Accounts Payable 112,000

*$160 per unit × 700 units

b. Raw and In Process Inventory* 56,525

PE 27–3B (FIN MAN); PE 12–3B (MAN)

a. Raw and In Process Inventory* 68,250

Accounts Payable 68,250

*$65 per unit × 1,050 units

b. Raw and In Process Inventory* 12,000

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

PE 27–4A (FIN MAN); PE 12–4A (MAN)

Quality

Cost

Prevention……………………………………

…

$183,000 61% 18.3%

PE 27–4B (FIN MAN); PE 12–4B (MAN)

Quality

Cost

Prevention……………………………………

…

$288,000 32% 9.6%

…

PE 27–5A (FIN MAN); PE 12–5A (MAN)

Inspection activity before improvement: $180,000 ÷ 25,000 units = $7.20 per unit

PE 27–5B (FIN MAN); PE 12–5B (MAN)

Inspection activity before improvement: $68,000 ÷ 16,000 units = $4.25 per unit

Quality Cost Classification Cost Sales

Sales

Total Quality Total

Cost of Quality Report

Cost of Quality Report

Percent of Percent of

Percent of

Total

Quality Cost Classification

Percent of

Total Quality

Cost

…

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–1 (FIN MAN); Ex. 12–1 (MAN)

The CEO must not have been listening very closely at the conference. Lean

manufacturing is not primarily an inventory reduction method. Lean manufacturing

is a process improvement philosophy that focuses on reducing time, cost, poor quality,

and uncertainty from a process. Large inventories are merely a symptom of poorly

designed processes. Thus, the CEO’s statement is naive. The company must first

In addition, the CEO has not provided the training or action plan for moving to lean.

The CEO has only commanded that it be done. This will create anxiety in the

workforce, and it is not consistent with employee involvement.

Ex. 27–2 (FIN MAN); Ex. 12–2 (MAN)

This is an actual situation facing the U.S. apparel industry. Warren Featherbone and

other U.S.-based apparel manufacturers are discovering the strategic power of lean

manufactures in batch sizes that are too large and too far away to respond quickly.

In addition, the retailer does not have to commit significant inventory to unknown

fashion trends when purchasing from the local company. As a result, the retailer is

able to avoid markdowns on slow-moving goods. Markdowns represent the second

largest cost to retailing operations (next to cost of merchandise sold). The retailer

must make large order commitments to the offshore manufacturer. If the product

eventually proves to be disappointing in the market, the retailer has no choice but

to incur severe markdowns to move the excess inventory. Because of significant

EXERCISES

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–3 (FIN MAN); Ex. 12–3 (MAN)

Piecework compensation is a characteristic of a traditional manufacturing philosophy

that is inconsistent with lean manufacturing. Under lean manufacturing, workers are

other cells or work on improving themselves or the process. Piecework compensation

is very inconsistent with this philosophy. Employees should not be penalized just

because the cell is operating at a slower pace (or is shut down) due to decreases in

demand. The employee has no control over the demand placed on the cell.

Management does not need to be concerned about proper motivation to work. Under

pull manufacturing, the garment will be pulled through the cell. A slow employee will

slow the whole output of the cell. The other employees will either help the slow

employee or encourage the employee to catch up with the pace of the cell.

Ex. 27–4 (FIN MAN); Ex. 12–4 (MAN)

Management is incorrect in stating that the direct labor time is equal to the lead time.

The lead time also includes the wait time and other non-value-added time required to

make the product. The different batch sizes create within-batch wait time for each unit.

Thus, the lion, which is made in batch sizes of 40 units, has assembly lead time of 480

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–5 (FIN MAN); Ex. 12–5 (MAN)

a. Long setup times have two negative consequences. First, a long setup time

consumes valuable machine capacity that could be used for productive

purposes. Second, a long setup time results in large production batch sizes

b. One obvious improvement would be to limit the trips to the tool room to one

round trip, rather than two. However, even this could be improved upon by

changing the location of the fixtures. Changing the location of the fixtures

could significantly reduce the lathe setup time. Instead of using a tool room

to control the fixtures, the appropriate fixtures for the lathe could be located

at the lathe operation. In this case, the operator would not need to walk to a

c. Turn off machine and remove fixture from lathe………

…

10 minutes

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–6 (FIN MAN); Ex. 12–6 (MAN)

Value-Added Non-Value- Total

Time Added Time Time

V

alue-added time……………………………

…

12 12

Within-batch wait time………………………

…

348 348

1

Total value-added time per unit:

Milling………………………………………………

…

5minutes

Finishing……………………………………………

…

7

Total……………………………………………

…

12 minutes

Value-Added Non-Value- Total

Time Added Time Time

V

alue-added time……………………………

…

12 12

Within-batch wait time………………………

…

36 36

1

Total value-added time per unit:

Milling………………………………………………

…

5minutes

Finishing……………………………………………

…

7

…

Lean Manufacturing Philosophy

Traditional Philosophy

1

2

1

2

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

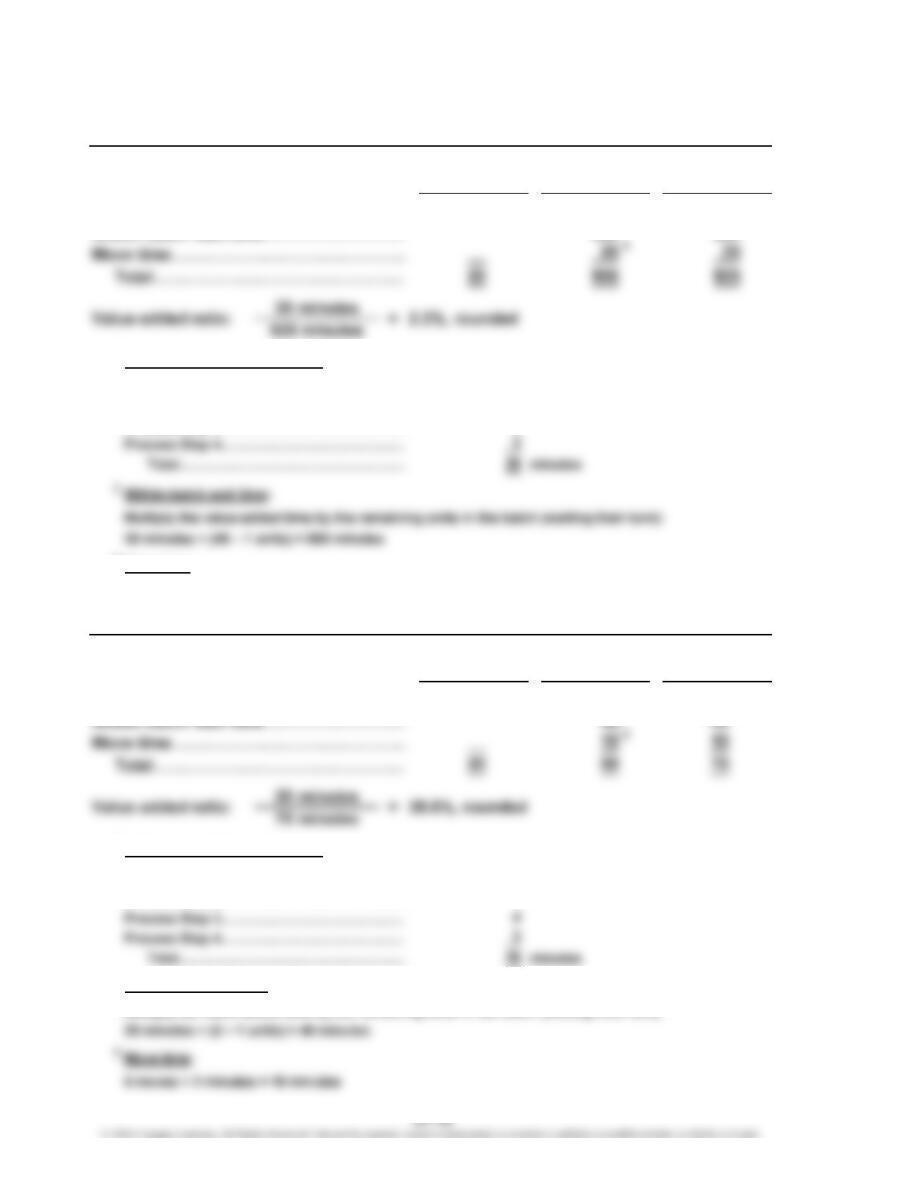

Ex. 27–7 (FIN MAN); Ex. 12–7 (MAN)

Value-Added Non-Value- Total

Time Added Time Time

V

alue-added time……………………………

…

20 20

Within-batch wait time……………………

…

880 880

1

Total value-added time per unit:

Process Step 1…………………………………

…

5 minutes

Process Step 2…………………………………

…

8

Process Step 3…………………………………

…

4

…

3

Move time:

5 moves (from raw materials to finished goods) × 5 minutes = 25 minutes

Value-Added Non-Value- Total

Time Added Time Time

V

alue-added time……………………………

…

20 20

…

1

Total value-added time per unit:

Process Step 1…………………………………

…

5 minutes

Process Step 2…………………………………

…

8

…

…

2

Within-batch wait time:

Multiply the value-added time by the remaining units in the batch (waiting their turn)

a. Present Approach

b. Proposed Lean Approach

1

2

1

2

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

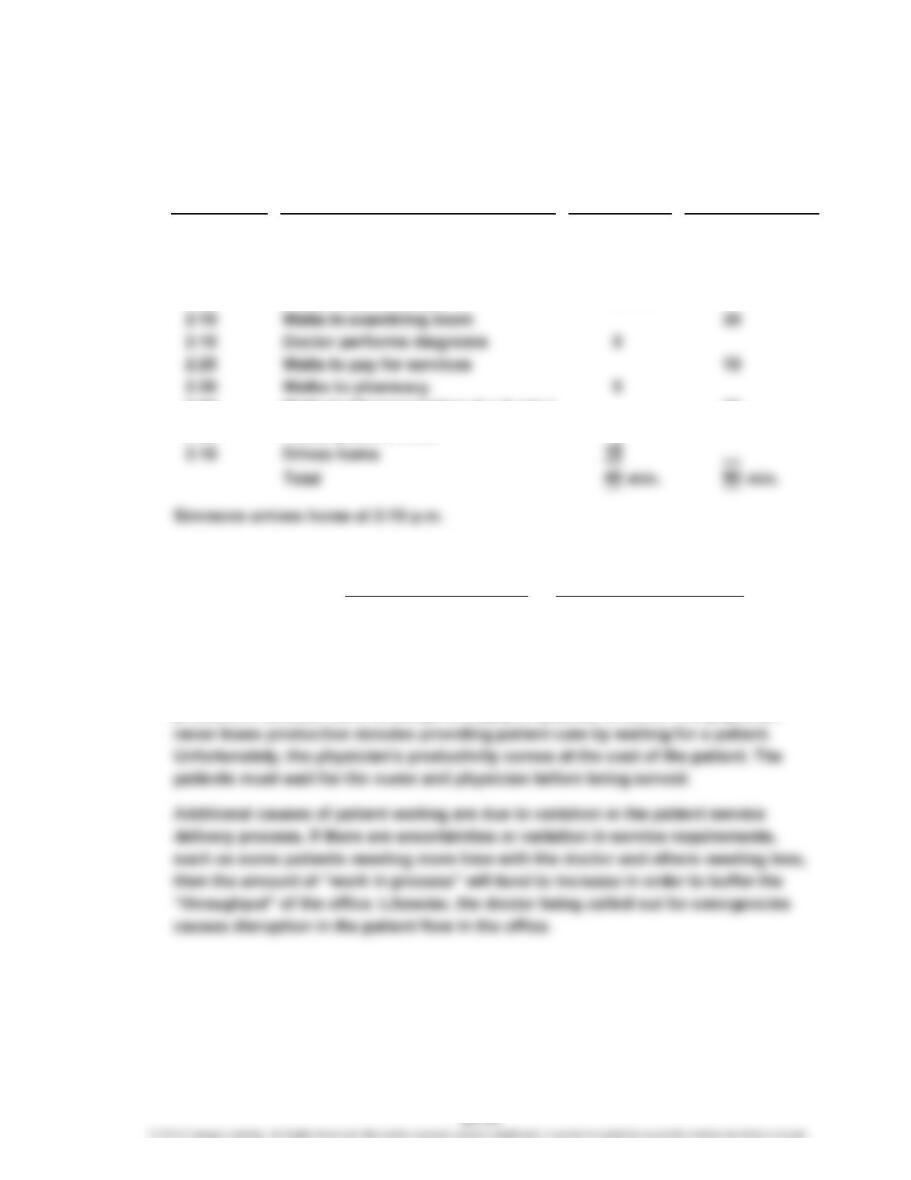

Ex. 27–8 (FIN MAN); Ex. 12–8 (MAN)

a. and b.

Elapsed

Time (a)

1:00 PM Arrives at doctor office

1:25 Waits in waiting room (5 × 5 min.) 25 min.

1:30 Waits in examining room 5

1:40 Nurse takes readings 10 min.

2:50 Waits to fill prescription (4 × 5 min.) 20

2:55 Prescription is filled 5

b. Of the total elapsed time of 130 minutes, 90 minutes is non-value-added time.

Value-Added Lead Time

Total Lead Time

d. The doctor requires patients to wait in order to increase the productivity of the office.

The patients represent the “work in process inventory” of the office, while the

physician and nurses are the critical productive resources. The clinical staff remains

productive because there is always a supply of patients to serve. The physician

Value-Added Ratio =

c.

=

Activity

(40 min. + 90 min.)

40 min. = 30.8%

Non-

Value-Added

Time

Value-Added

Time (b)

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–9 (FIN MAN); Ex. 12–9 (MAN)

a. The Japanese supply chain model is one based on long-term arrangements

and partnership. The Japanese automobile manufacturers want their

suppliers to be financially healthy because they rely on them for innovation.

b. These suppliers support the Japanese system because it provides for win-

win opportunities, whereby the customer and the supplier can both be

successful. The suppliers are concerned about their margins being

c. Supply chain management is often beneficial to the customer. However, the

customer may have to trade off between short-term and longer-term benefits.

For example, supply chain management provides the supplier the financial

incentives to invest in process and product innovation, invest in supply chain

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–10 (FIN MAN); Ex. 12–10 (MAN)

Quickie’s team approaches are very different from using a manager to hire and

evaluate employees. First, the input of many individuals goes into the hiring

decision. In this way, the viewpoints of a variety of people are brought into the

decision. Moreover, the new hire needs to “fit” with the culture of the team.

Team-based hiring can produce a higher probability of having an effective team

Team-based evaluation practices increase employee involvement. Employees

have input into decisions that affect the team, rather than having these decisions

handed down to them. This should increase the amount of empowerment and job

satisfaction enjoyed by the team members.

Ex. 27–11 (FIN MAN); Ex. 12–11 (MAN)

Shield Insurance Company should adopt lean principles in its claims

payment operations. Management should first consider changing the layout for

this process. Instead of processing the claims payments through three different

departments that are organized by process, the company could design claims

payment “cells” that are organized around different types of insurance

products or customers. For example, a cell could be created for all marine

insurance. The cell would have data input, claims audit, and claims adjustment

personnel all located together (co-located) to process marine insurance claims.

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–12 (FIN MAN); Ex. 12–12 (MAN)

a. The present Grill Rite service delivery system is an example of a push system.

Special orders are “pushed” through the system. The order is placed at the

beginning of the process and the hamburger is cooked, dressed, and then

b. A new system could be designed so that a custom order is introduced after cooking

the burger, rather than prior to cooking. In this way, hamburgers are made to order

without the use of finished goods inventory. Under this process, assume a customer

ordered a hamburger with ketchup and pickles only. The order would be received

at the dressing station. Here, a food preparer would take a hamburger off the grill

and place ketchup and pickles on the burger using materials at the dressing station

(termed point-of-use materials). The hamburger that is pulled from the grill would

create a signal (the space on the grill) for a new hamburger to be placed on the grill.

In this way, hamburgers that are cooking do not have orders assigned to them.

Note to Instructors: You may recognize that the first system described in this exercise is

similar to the method invented by McDonald’s, while Wendy’s uses the second method.

McDonald’s recently indicated that it was switching its method to work more like

Wendy’s because of its superior service characteristics. You might also note that Dell’s

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–13 (FIN MAN); Ex. 12–13 (MAN)

The production manager probably has some good points. If the accounting system does

not change when an organization embraces a lean strategy, then there will likely be

complaints. A conventional accounting system needs to have a strong accounting

control orientation. Under lean manufacturing, the accounting system can be designed

with much wider transaction control intervals. The company could have a very wide

transaction interval—such as between purchased parts transacted in and finished goods

transacted out. Thus, many transactions into and out of intermediate work in process

inventory locations would not be needed. In addition, a raw and in process inventory

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–14 (FIN MAN); Ex. 12–14 (MAN)

$420,000

2,000 hours

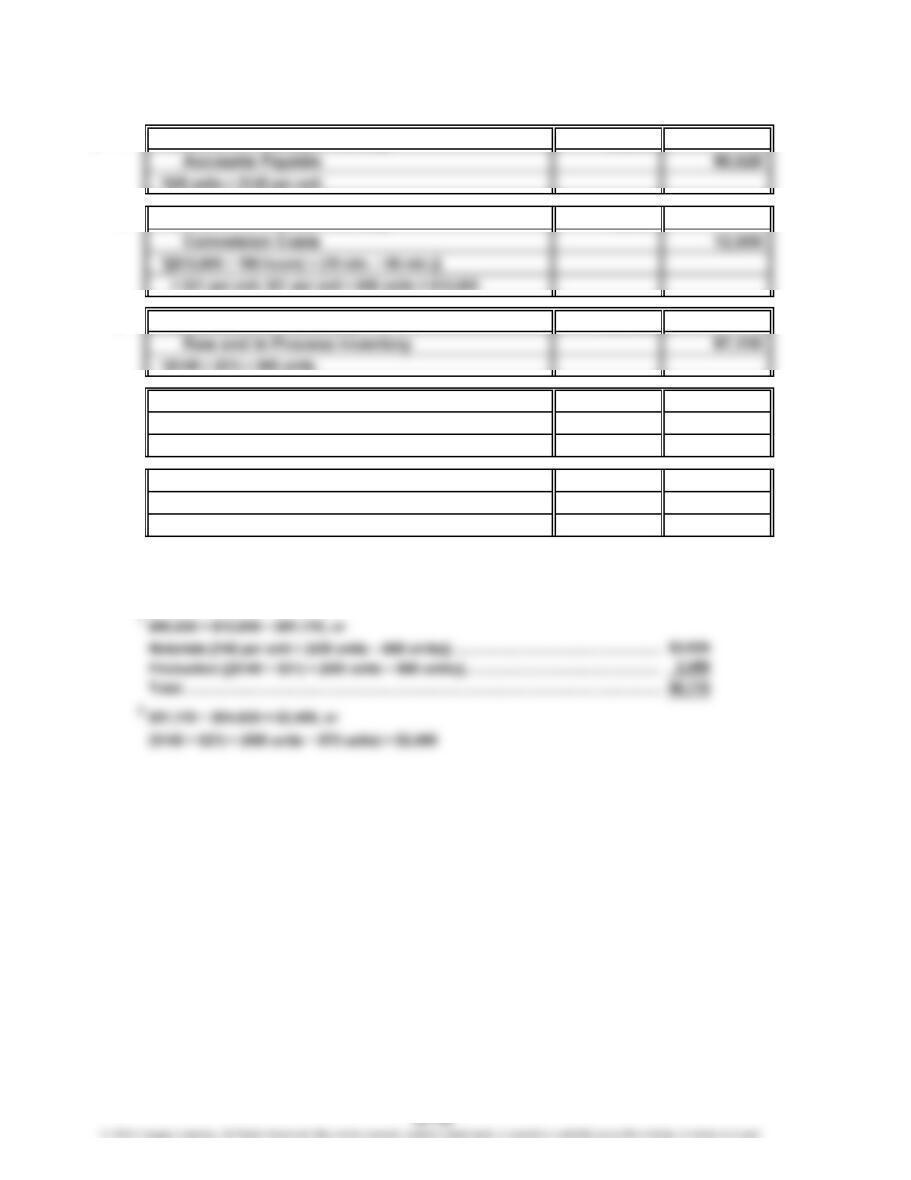

c. 1. Raw and In Process Inventory*

Accounts Payable 148,500

*1,100 units × $135 per unit

2. Raw and In Process Inventory*

3. Finished Goods Inventory*

4. Accounts Receivable*

Sales 355,100

*$1,060 units × $335 per unit

355,100

$210 per hour

a. Budgeted Cell Conversion

Cost Rate ==

183,150

148,500

34,650

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–15 (FIN MAN); Ex. 12–15 (MAN)

$193,200

2,100 hours

c. 1. Raw and In Process Inventory*

Accounts Payable 31,500

*700 units × $45 per unit

2. Raw and In Process Inventory*

3. Finished Goods Inventory*

4. Accounts Receivable*

Sales 85,760

46,580

31,500

16,100

$92 per hour

a. Budgeted Cell Conversion

Cost Rate ==

85,760

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–16 (FIN MAN); Ex. 12–16 (MAN)

a. 1. Raw and In Process Inventory* 90,625

2. Raw and In Process Inventory* 12,600

3. Finished Goods Inventory* 97,110

4. Sales* 205,200

Accounts Receivable 205,200

*$360 per unit × 570 units

Cost of Goods Sold* 94,620

Finished Goods Inventory 94,620

*($145 + $21) × 570 units

b. Raw and In Process Inventory, ending balance1……………………………

…

$6,115

Finished Goods Inventory, ending balance2…………………………………

…

$2,490

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–17 (FIN MAN); Ex. 12–17 (MAN)

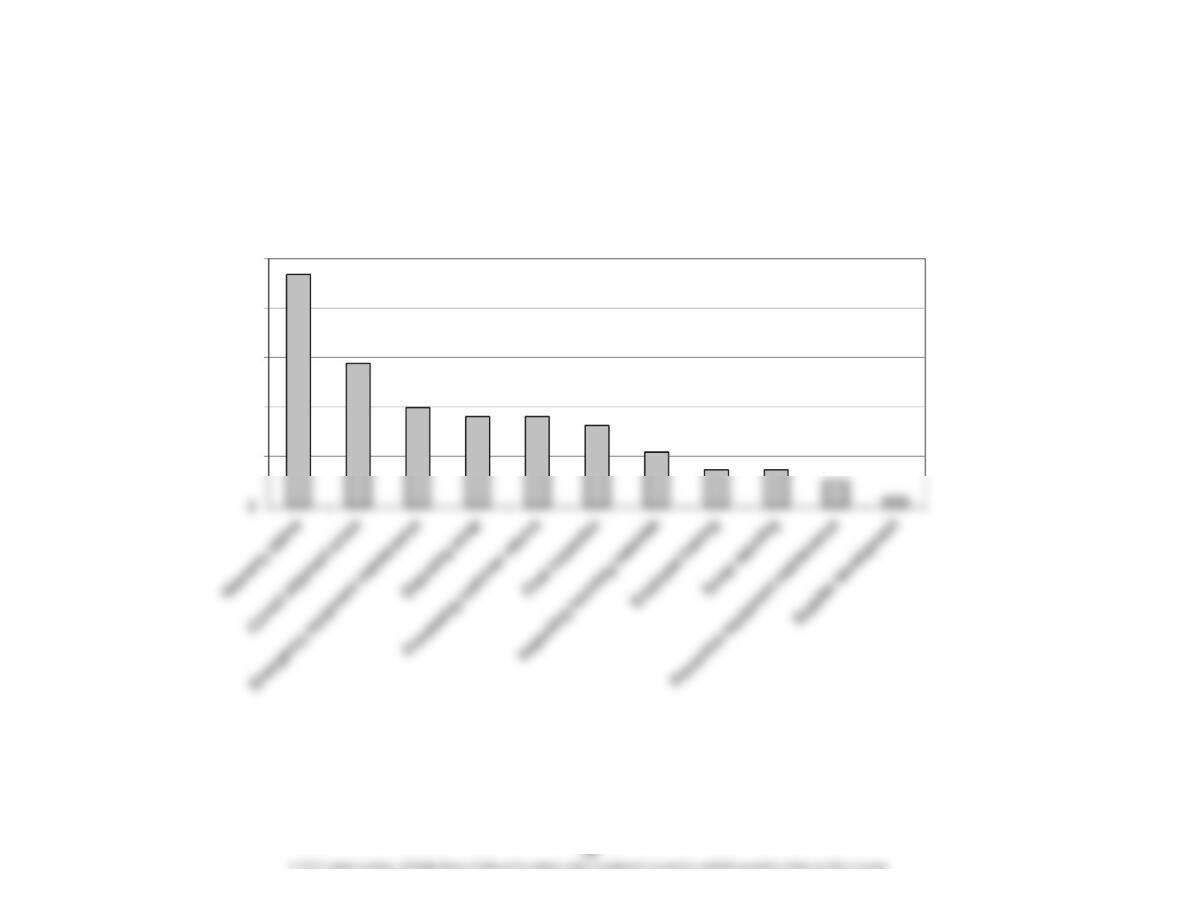

50000

100000

150000

200000

250000

Dollars

Pareto Chart of Quality Activities

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Ex. 27–18 (FIN MAN); Ex. 12–18 (MAN)

a. Activities classified by cost of quality:

Quality Activities

Correct shipment errors……………………………

…

Disposing of scrap…………………………………

…

Emergency equipment maintenance……………

…

Employee training……………………………………

…

b.

Quality

Cost

Prevention $ 72,000 8% 2.4%

Appraisal 135,000 15% 4.5%

c. The majority of the company’s quality efforts are in correcting quality problems.

This is evident by the high percentage of quality costs associated with internal and

external failure (25% + 52% = 77% of total quality costs). The highest cost activities

are warranty claims, which indicates significant field failures for the product.

Quality Cost Classification

SILICON SOLUTIONS

Cost of Quality Report

Cost Summary

Percent

of Total

Sales

Percent of

Total

Quality Cost

Quality Cost

Activity Cost Classification

$144,000 External failure

90,000 Internal failure

99,000 Internal failure

36,000 Prevention

21

…

…

…

…

…