Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–4A (FIN MAN); Prob. 12–4A (MAN) (Concluded)

4. Percentages of total activity cost that are value- and non-value-added:

V

alue-added………………………………………

…

39%

5. The ER has 61% of its total costs as non-value-added. This is a very significant

$ 62,400

Percent of Total

Department Cost

Activity

Cost

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–1B (FIN MAN); Prob. 12–1B (MAN)

1. HD Hogg’s purchasing policy is very short-sighted. It does not involve

developing partnerships with suppliers. HD Hogg should consider changing

its arm’s-length policy and work on building a long-term supply chain strategy

with its suppliers. With a supply chain strategy, HD Hogg can begin to

2. The hidden costs beyond the price include the costs associated with the

higher inventory required by Iron Horse Frames’ delivery schedule. These

inventory costs include additional space, handling, obsolescence, financing,

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–1B (FIN MAN); Prob. 12–1B (MAN) (Concluded)

3. If the financing costs are 12%, then the additional cost of the inventory could be

determined as follows:

At the beginning of July, the new shipment of 4,500 frames arrives. Assuming that

the frame supply runs out by the end of the quarter, the average inventory for the

The inventory carrying cost can be estimated as follows:

Average frames in inventory for the quarter………………

…

2,250

×

Price per frame…………………………………………………

…

$300

Total inventory investment……………………………………

…

$675,000

Interest rate per quarter (12% ÷ 4)……………………………

…

3%

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–2B (FIN MAN); Prob. 12–2B (MAN)

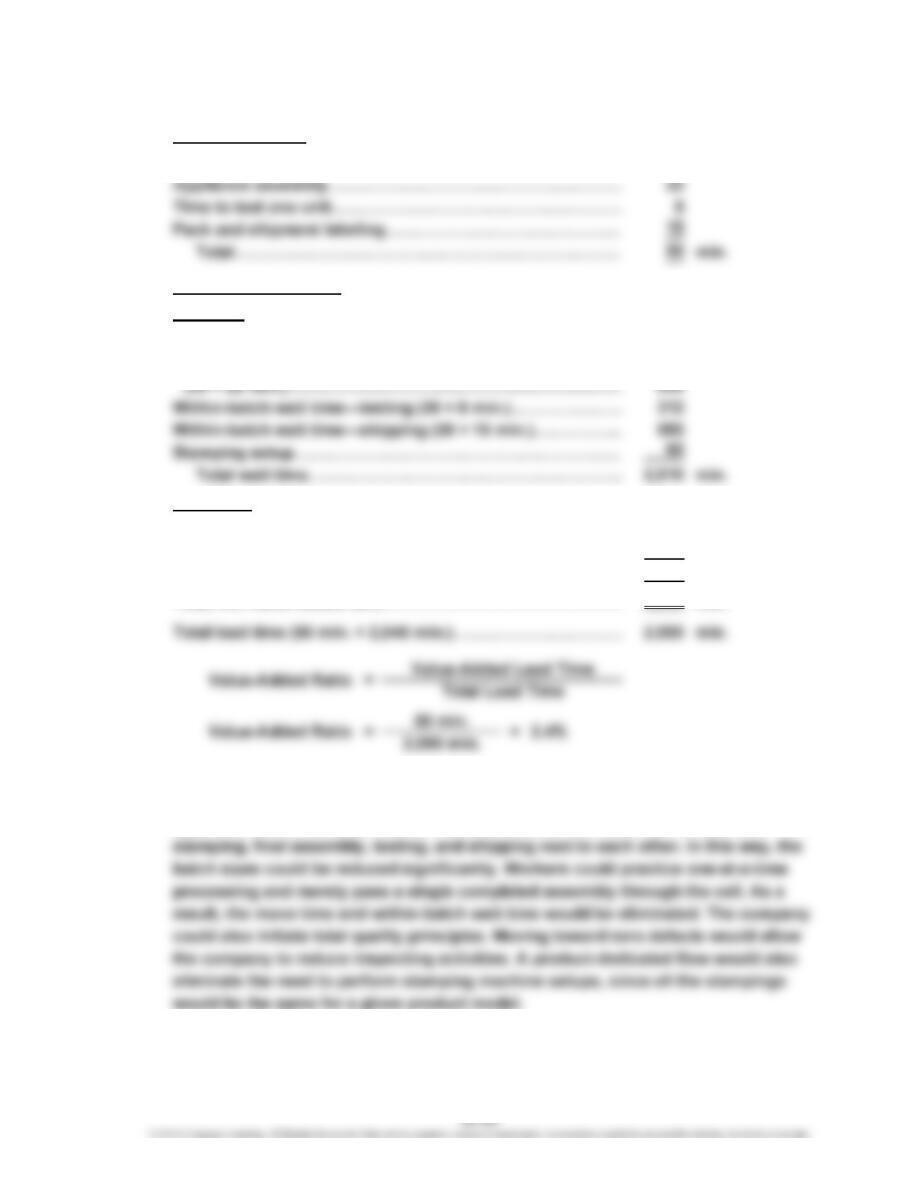

1. Value-added time:

Stamping……………………………………………………………

…

5 min.

Non-value-added time:

Wait time:

Within-batch wait time—stamping (39 × 5 min.)……………

…

195 min.

Within-batch wait time—final assembly

Move time:

Move from stamping to final assembly………………………

…

10 min.

Move from final assembly to testing…………………………

…

25

Total move time……………………………………………………

…

35 min.

Total non-value-added time……………………………………… 2,045 min.

2. The existing process is very wasteful. The company could improve the process

by changing the layout from a process orientation to a product orientation. Each

appliance model could be formed into a production cell. Each cell would have

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–3B (FIN MAN); Prob. 12–3B (MAN)

$189,000

2,100 hours

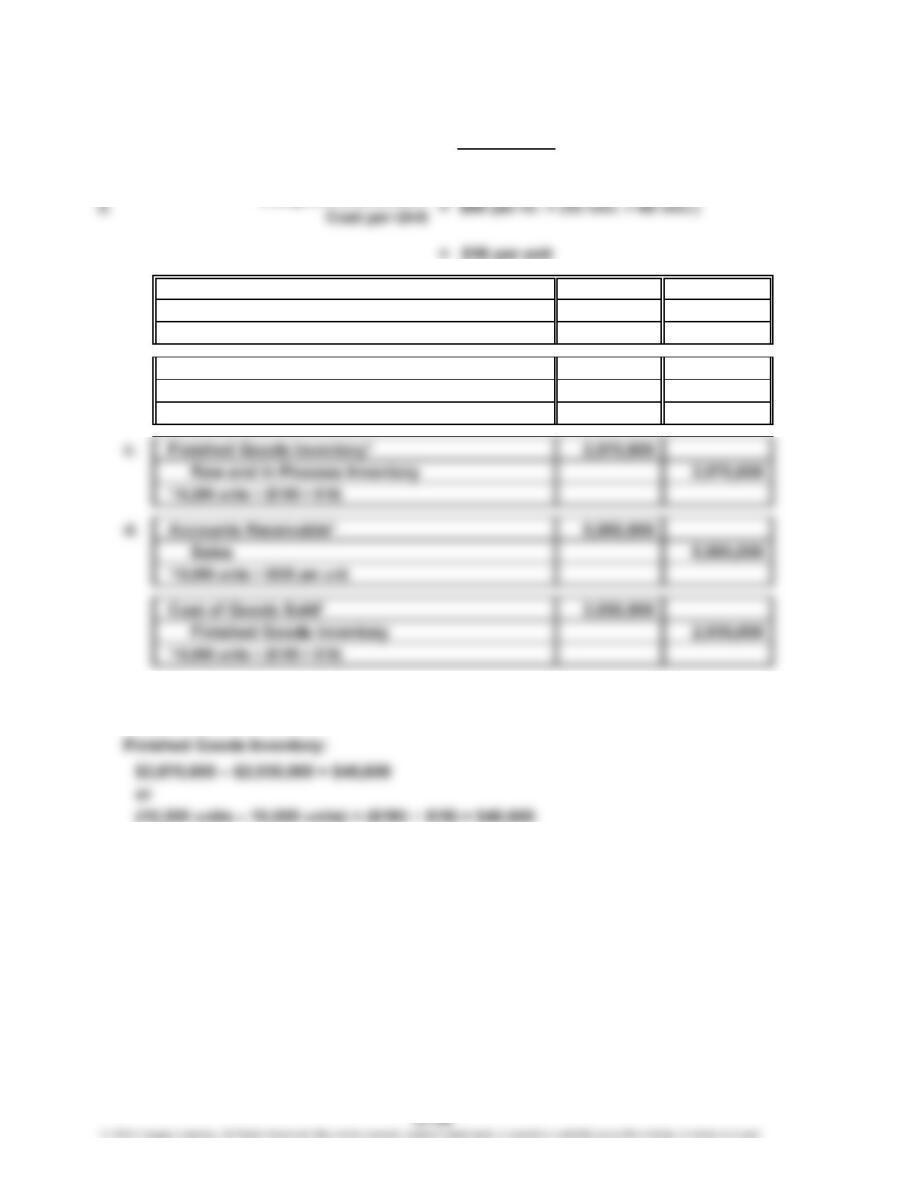

3. a. Raw and In Process Inventory*

Accounts Payable 1,979,500

*10,700 units × $185 per unit

b. Raw and In Process Inventory*

Conversion Costs 189,000

*10,500 units × $18 per unit

4. Raw and In Process Inventory:

$1,979,500 + $189,000 – $2,070,600 = $97,900

1,979,500

189,000

$90 per hour

1. Budgeted Cell Conversion

Cost Rate ==

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–3B (FIN MAN); Prob. 12–3B (MAN) (Concluded)

5. Lean accounting is different from traditional accounting in a number of respects.

Most importantly, lean accounting is simplified and uses minimal control. As a

result, the number of transactions is reduced, and the control intervals between

adjacent work in process transaction points are widened. In many lean

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–4B (FIN MAN); Prob. 12–4B (MAN)

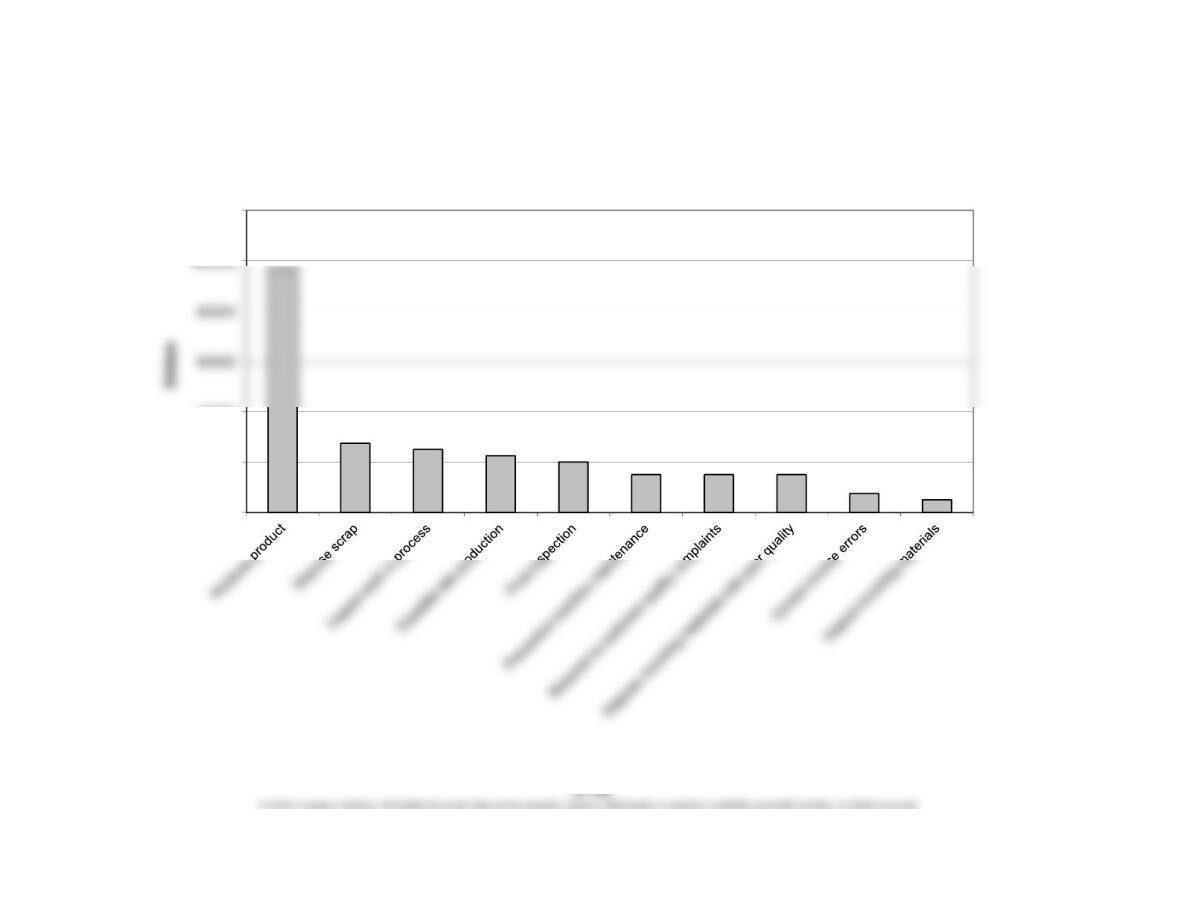

1.

0

20000

40000

120000

Pareto Chart of Activities

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–4B (FIN MAN); Prob. 12–4B (MAN) (Continued)

2. Activity classifications:

Activity

Cost

Correcting invoice errors……

…

$7,500

Disposing of incoming

materials with poor quality…

…

15,000

Disposing of scrap……………

…

27,500

Expediting late production…… 22,500

Final inspection………………… 20,000

3. Percent of total activity cost for each quality cost (and nonquality cost)

classification:

Prevention………………………………………… 6%

Percent of Total

Department Cost

Activity

Cost

$ 15,000

50,000

Internal failure

Internal failure

Appraisal

Quality Cost Classification

Cost of Quality Non-Value-Added

Non-value-added

Value-added

Non-value-added

Non-value-added

Non-value-added

Classification

Classification

Value-Added/

Activity

External failure

Internal failure

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

Prob. 27–4B (FIN MAN); Prob. 12–4B (MAN) (Concluded)

3. Percentages of total activity cost that are value- and non-value-added:

V

alue-added………………………………………… 65%

4. The company has 65% of its total costs as value-added. However, there is still room

for significant improvement. Internal failure represents 26% of the total costs. This

$162,500

Percent of Total

Department Cost

Activity

Cost

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

CP 27–1 (FIN MAN); CP 12–1 (MAN)

The controller should confront the plant manager. The plant manager is attempting

to skew the sampling results by giving the sampled items special treatment. The

original intent of the sampling plan is to represent the average performance of the

manufacturing process. Thus, the tagged items should receive no better treatment

than the average product being produced. The plant manager’s memo will cause the

lead times reported to central management to be much better than they actually are.

Thus, it is possible that salespersons and marketing personnel will begin to make

shipping commitments to customers based on the reported lead times. Since the plant

is unable to perform for all products at the reported levels, customers may be left

angry when the commitments are not met.

CASES & PROJECTS

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

CP 27–2 (FIN MAN); CP 12–2 (MAN)

Clark’s claim that the inventory doesn’t cost the company anything is likely not true. At

the very minimum, inventory requires working capital to be used. The financing cost

associated with the working capital represents a cost to the company. In addition, the

inventory requires space, insurance, security, and movement. Thus, these additional

costs will be incurred to store the inventory. Beyond the carrying (interest) and storage

CP 27–3 (FIN MAN); CP 12–3 (MAN)

All three charts indicate a steadily deteriorating situation. It seems clear that Maxxim is

not employing lean strategies. The inventory is growing steadily, yet the company

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

CP 27–4 (FIN MAN); CP 12–4 (MAN)

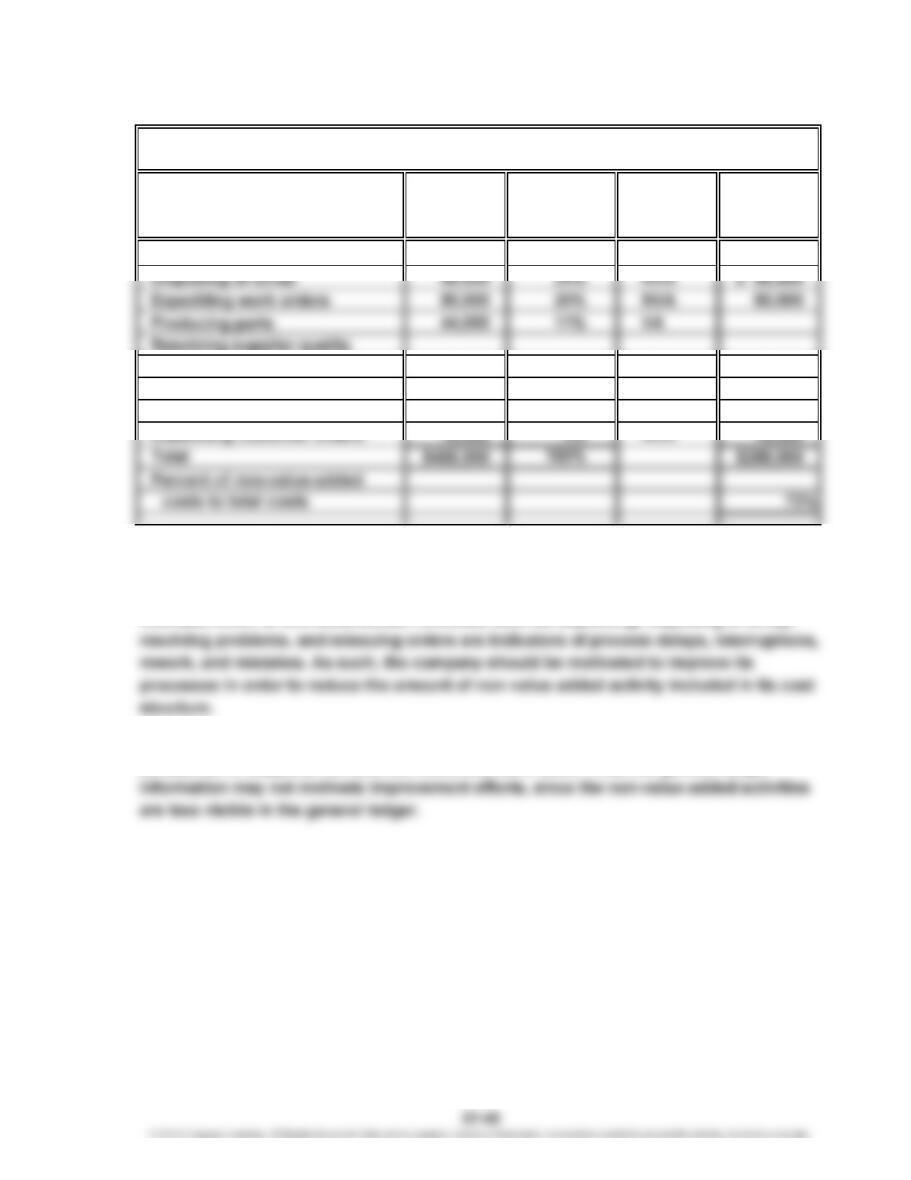

Non-Value-

Total Classifi- Added

Cost cation Costs

Processing sales orders $ 68,000 17% VA

Resolving supplier quality

problems 56,000 14% NVA 56,000

Reissuing corrected

purchase orders 40,000 10% NVA 40,000

The activity information can be separated into the value-added and non-value-added

components. When this is done, it becomes clear that the company has a large

percentage of non-value-added activities. Seventy-two percent of Pryor's factory

overhead effort is non-value-added. Activities such as expediting, disposing of scrap,

The general ledger report provides information only about where money is spent, such

as salaries or supplies, not how the resources were used. Thus, the general ledger

PRYOR COMPANY

Activity

Value-Added/Non-Value-Added Activities Report

Percent

of Total

CHAPTER 27 Lean Principles, Lean Accounting, and Activity Analysis

CP 27–5 (FIN MAN); CP 12–5 (MAN)

This would be a good assignment for groups of students to report back to the class. Each

of the groups will likely go to different restaurants at different times of the day and will

have different results. The results could be shared with the class, and “averages” could

be determined for the various non-value-added categories. The following types of

activities will likely be noted in students’ reports:

Waiting to be seated………………………………………

…

Non-value-added

Being seated………………………………………………

…

Value-added

Waiting to give drink order………………………………

…

Non-value-added

Giving drink order…………………………………………

…

Value-added

Waiting to receive drink…………………………………

…

Non-value-added