CHAPTER 26

SOLUTIONS TO EXERCISES—SET B

EXERCISE 26-1B

(a)

Reject

Order

Accept

Order

Net Income Effect

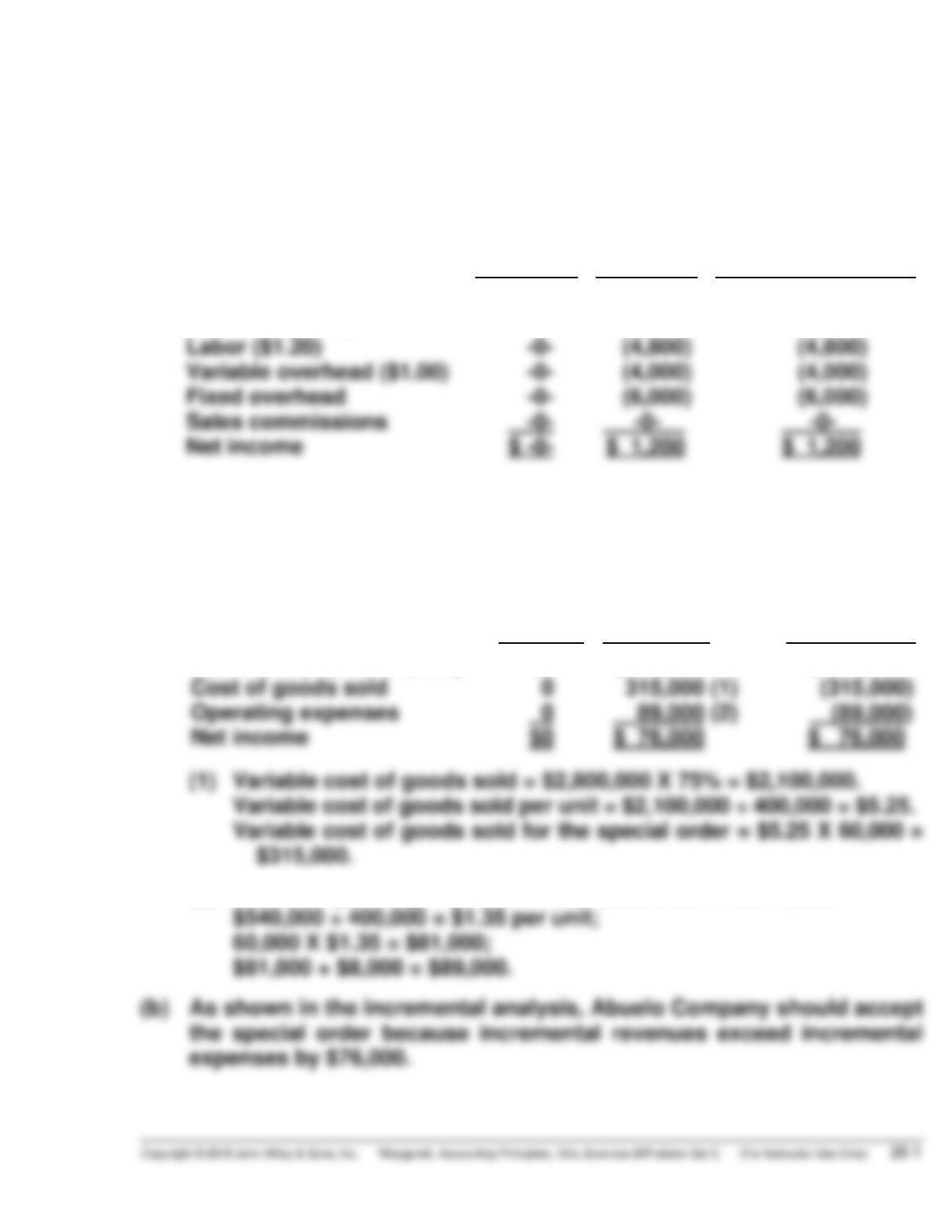

Fixed overhead

Sales commissions

(6,000)

Revenues

Materials ($0.75)

Labor ($1.20)

$ -0-

-0-

-0-

$19,000

(3,000)

(4,800)

$19,000

(3,000)

(4,800)

EXERCISE 26-2B

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

89,000

Revenues (60,000 X $8.00)

Cost of goods sold

$0

0

$480,000

315,000

(1)

$ 480,000

((315,000)

(2) Variable operating expenses = $900,000 X 60% = $540,000;

$540,000 ÷ 400,000 = $1.35 per unit;

60,000 X $1.35 = $81,000;

$81,000 + $8,000 = $89,000.

EXERCISE 26-2B (Continued)

(b) As shown in the incremental analysis, Aiden should accept the special

order because incremental revenue exceeds incremental expenses by

$1,200.

EXERCISE 26-3B

(a)

Make

Buy

Net Income

Increase

(Decrease)

Direct materials (60,000 X $4.00)

Direct labor (60,000 X $6.00)

Variable manufacturing costs

$240,000

360,000

$ 0

0

$ 240,000

360,000

(b) No, Sun Inc. should not purchase the lamps. As indicated by the

incremental analysis, it would cost the company $24,000 more to purchase

the lamps.

(c) Yes, by purchasing the lamp shades, a total cost saving of $16,000 will

result as shown below.

Make

Buy

Net Income

Increase

(Decrease)

EXERCISE 26-4B

Sell

(Basic Kit)

Process Further

(Stage 2 Kit)

Net Income

Increase

(Decrease)

Total

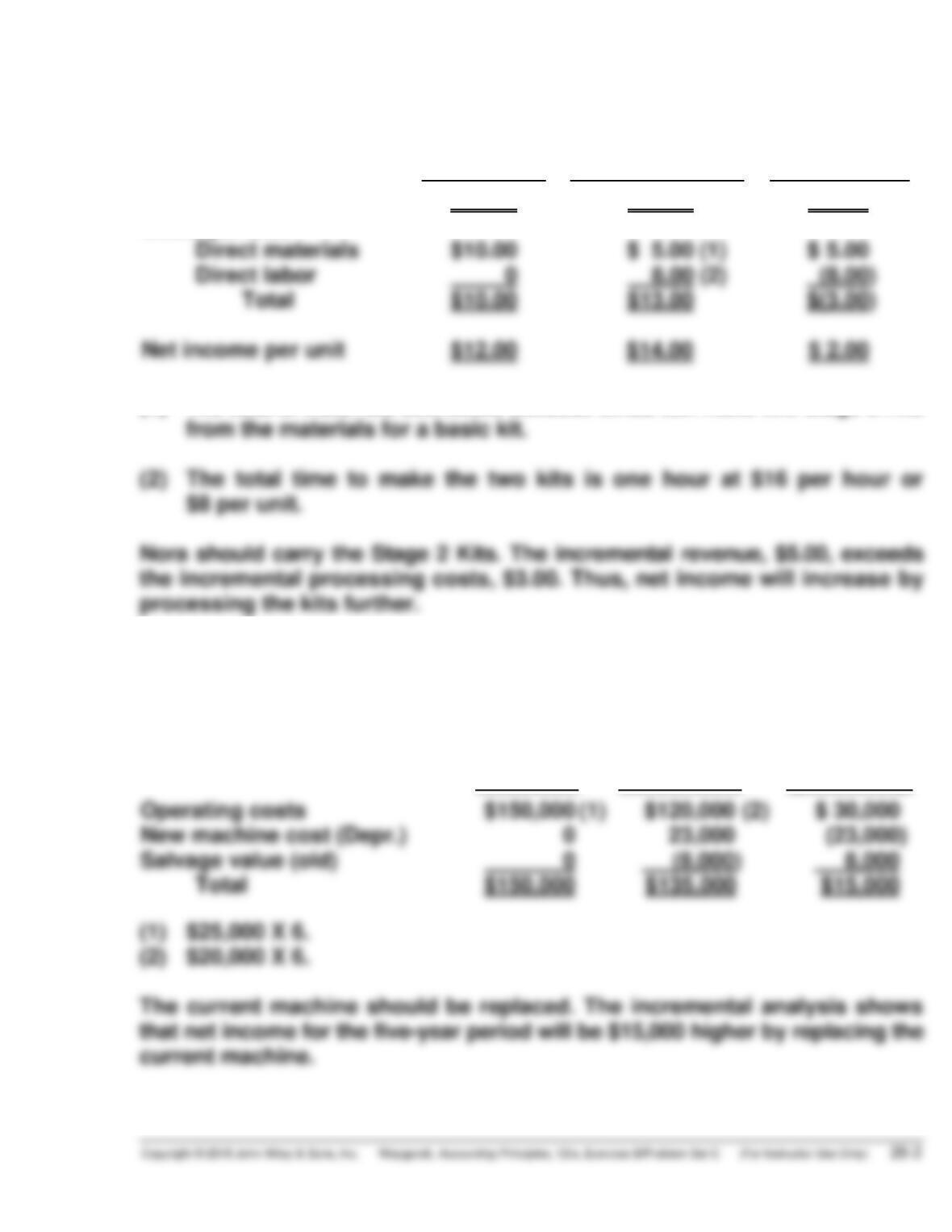

Sales per unit

Costs per unit

Direct materials

$22.00

$10.00

($27.00

( ) $ 5.00 (1)

$ 5.00)

$(5.00)

(1) The cost of materials decreases because Linda can make two Stage 2 Kits

from the materials for a basic kit.

(2) The total time to make the two kits is one hour at $16 per hour or

$8 per unit.

EXERCISE 26-5B

Retain

Machine

Replace

Machine

Net Income

Increase

(Decrease)

0

Operating costs

$150,000

(1)

($120,000)

(2)

($ 30,000)

EXERCISE 26-6B

Continue

Eliminate

Net Income

Increase

(Decrease)

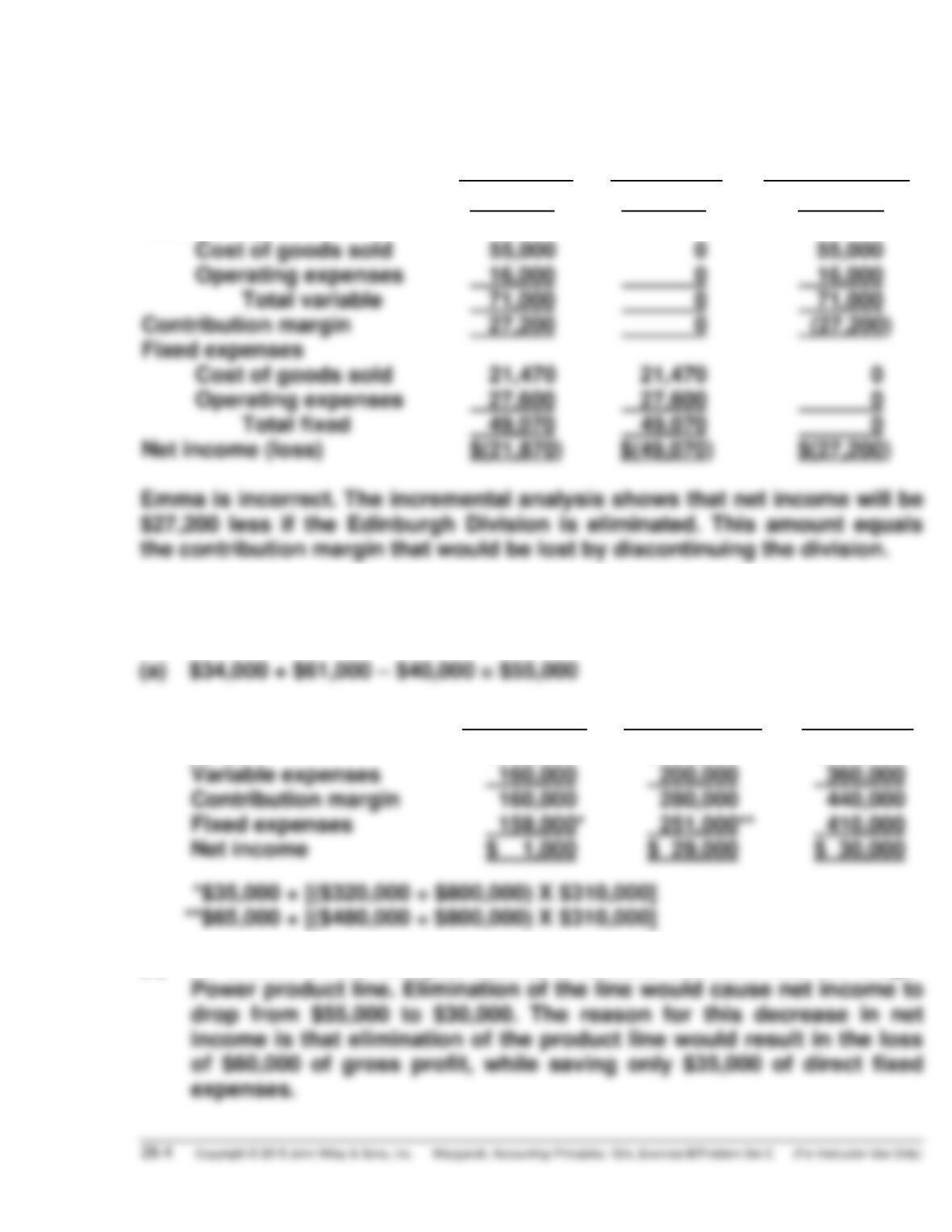

Net income (loss)

Sales

Variable expenses

Cost of goods sold

$ 98,200)

(55,000)

$ 0

( 0

$(98,200)

(55,000

EXERCISE 26-7B

(a) $34,000 + $61,000 – $40,000 = $55,000

(b)

Stunner

Double-Set

Total

Sales

Variable expenses

$320,000

160,000

$480,000

200,000

$800,000

360,000

**$65,000 + [($480,000 ÷ $800,000) X $310,000]

(c) As shown in the analysis above, El should not eliminate the Mega-

Power product line. Elimination of the line would cause net income to

EXERCISE 26-8B

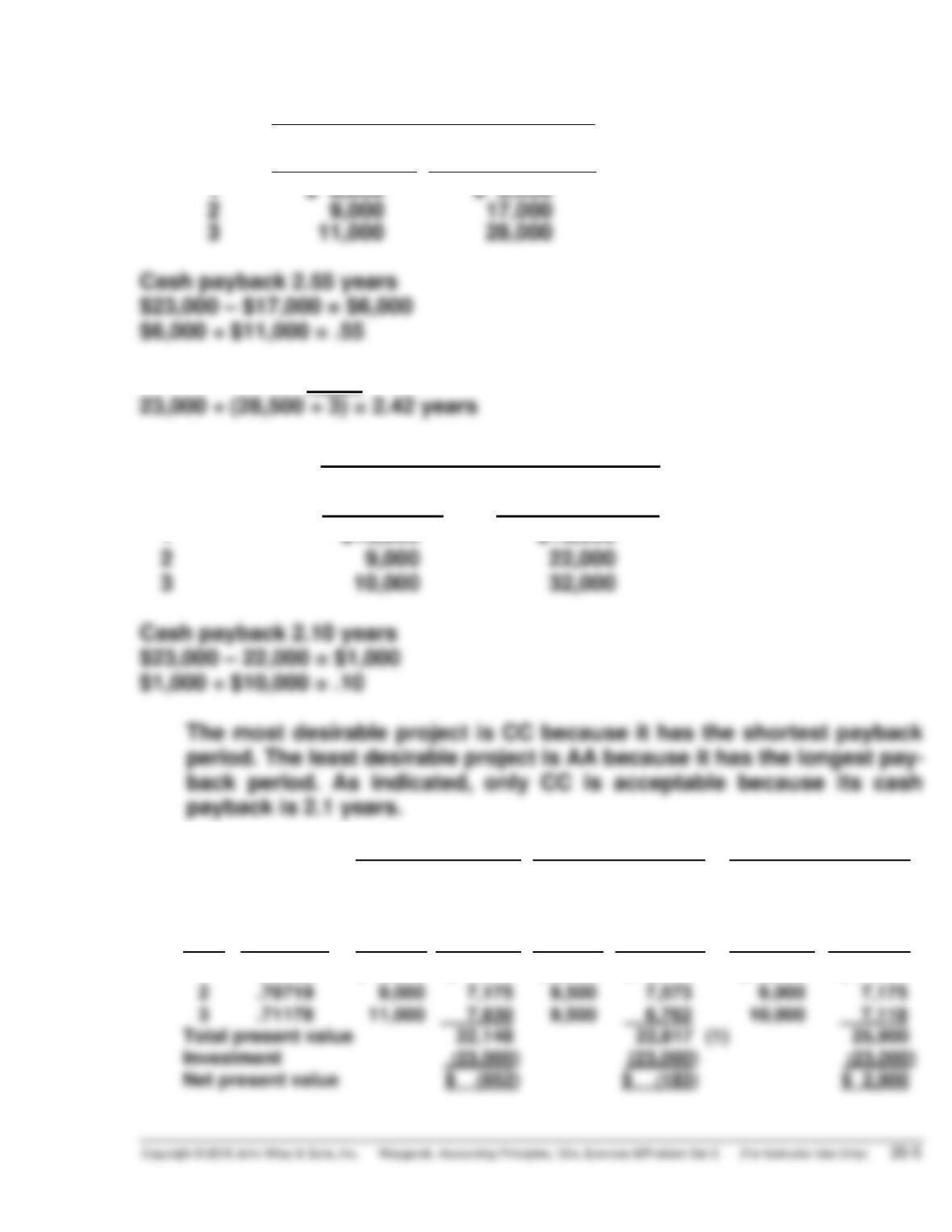

(a)

AA

Year

Annual Net

Cash Flow

Cumulative Net

Cash Flow

1

$ 8,000

$ 8,000

BB

23,000 ÷ (28,500 ÷ 3) = 2.42 years

CC

Year Annual Net Cumulative Net

Cash Flow Cash Flow

1 $13,000 $13,000

Cash payback 2.10 years

$23,000 – 22,000 = $1,000

$1,000 ÷ $10,000 = .10

(b)

AA

BB

CC

Year

Discount

Factor

Net

Annual

Cash

Flow

Present

Value

Net

Annual

Cash

Flow

Present

Value

Net Cash

flow

Present

Value

3

.71178

Net present value

$ 2,900

(1) This total may also be obtained from Table 2: $9,500 X 2.40183 =

$22,817. Project CC is the only acceptable project. Project AA is

the least desirable.

EXERCISE 26-9B

(a) (1) Annual rate of return: $30,000 ÷ [($200,000 + $0) ÷ 2] = 30%.

(2) Cash payback: $200,000 ÷ $60,000 = 3.33 years.

(b)

Item

Amount

Years

PV Factor

Present Value

EXERCISE 26-10B

(a)

Project

Investment

÷

(Income + Depreciation)

=

Internal

Rate of

Return

Factor

Closest

Discount

Factor

Internal

Rate of

Return

22A

$225,000

÷

($11,300 + $37,500)

=

4.601

4.62288

8%

EXERCISE 26-11B

(a) Project A: ($66,000 X 3.79079) – $260,000 = $(9,808)

Project B: ($80,000 X 4.86842) – $384,000 = $5,474

(b) Robinville should invest in Project B only. Project B is acceptable because

it has a positive net present value. Project A is unacceptable because it

has a negative net present value.

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 26-1C

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues (7,000 X $35)

$0

$245,000

$ 245,000

(1) Variable costs = $3,600,000 – $810,000 = $2,790,000;

$2,790,000 ÷ 90,000 units = $31 per unit;

7,000 X $31 = $217,000.

(b) Yes, the special order should be accepted because net income will be

increased by $14,000.

(c) Unit selling price = $31 (variable manufacturing costs) + $2.00 variable

selling and administrative expenses + $3.00 net income = $36.00.

PROBLEM 26-2C

(a)

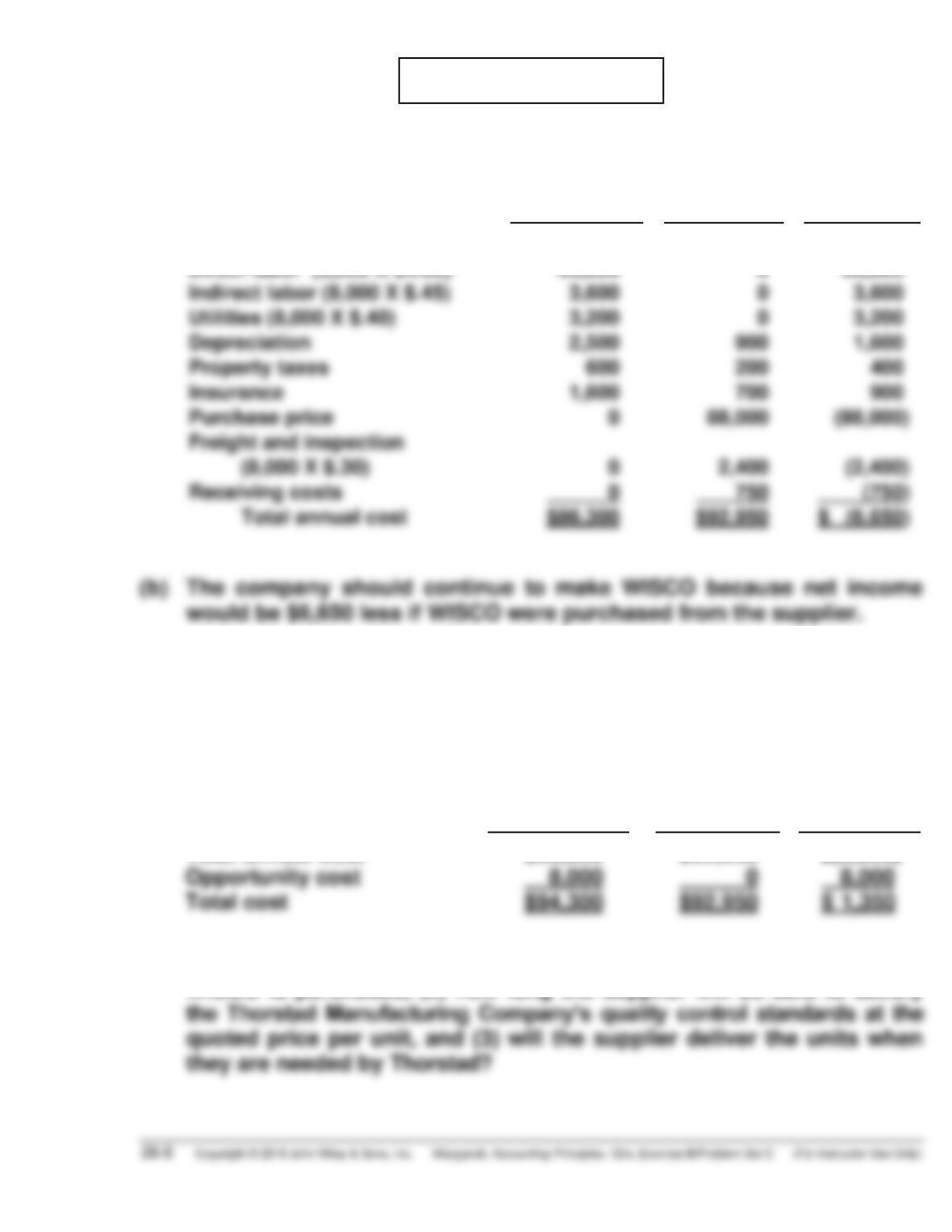

Make WISCO

Buy WISCO

Net Income

Increase

(Decrease)

Direct materials (8,000 X $4.75)

Direct labor (8,000 X $4.60)

Indirect labor (8,000 X $.45)

Utilities (8,000 X $.40)

$38,000

36,800

3,600

3,200

$ 0

0

0

0

($ 38,000

( 36,800

( 3,600

( 3,200

(b) The company should continue to make WISCO because net income

would be $6,650 less if WISCO were purchased from the supplier.

(c) The decision would be different. Because of the opportunity cost of

$8,000, net income will be $950 higher if WISCO is purchased as

shown below:

Make WISCO

Buy WISCO

Net Income

Increase

(Decrease)

Total annual cost

$86,300

$92,950

$(6,650)

PROBLEM 26-3C

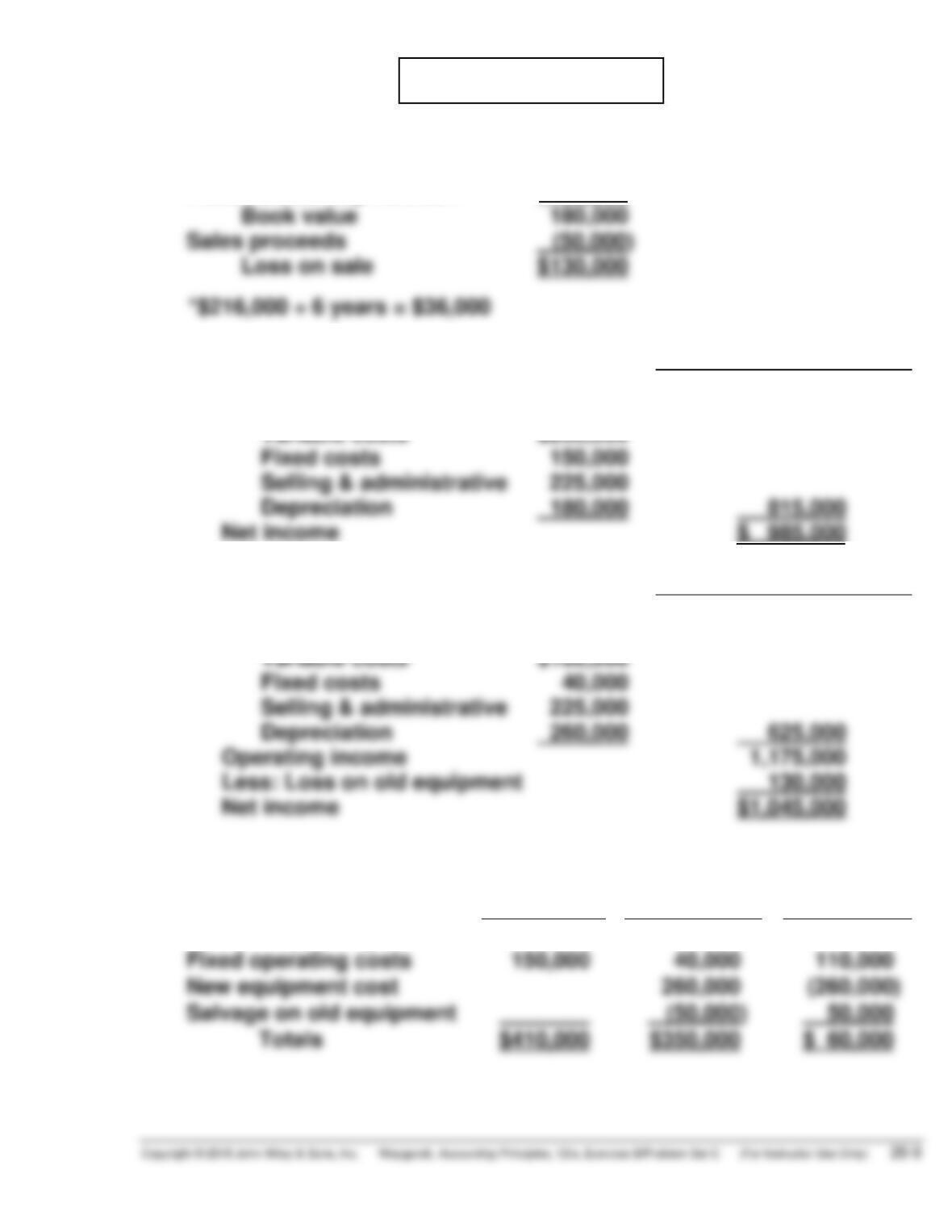

(a)

Cost

$216,000

Accumulated depreciation

Book value

36,000*

180,000

(b)

(1)

Retain Old Equipment

Sales ($360,000 X 5 yrs.)

$1,800,000

Less costs:

Variable costs

$260,000

Fixed costs

150,000

Selling & administrative

Depreciation

815,000

Net income

$ 985,000

(2)

Replace Old Equipment

Sales

$1,800,000

Less costs:

Variable costs

$100,000

Fixed costs

40,000

Selling & administrative

Depreciation

625,000

Operating income

Less: Loss on old equipment

Net income

$1,045,000

(c)

Retain Old

Equipment

Replace Old

Equipment

Net Income

Increase

(Decrease)

Variable operating costs

$260,000

$100,000

$160,000

Fixed operating costs

150,000

40,000

110,000

New equipment cost

(260,000)

Salvage on old equipment

50,000

Totals

$410,000

$350,000

$ 60,000

PROBLEM 26-4C

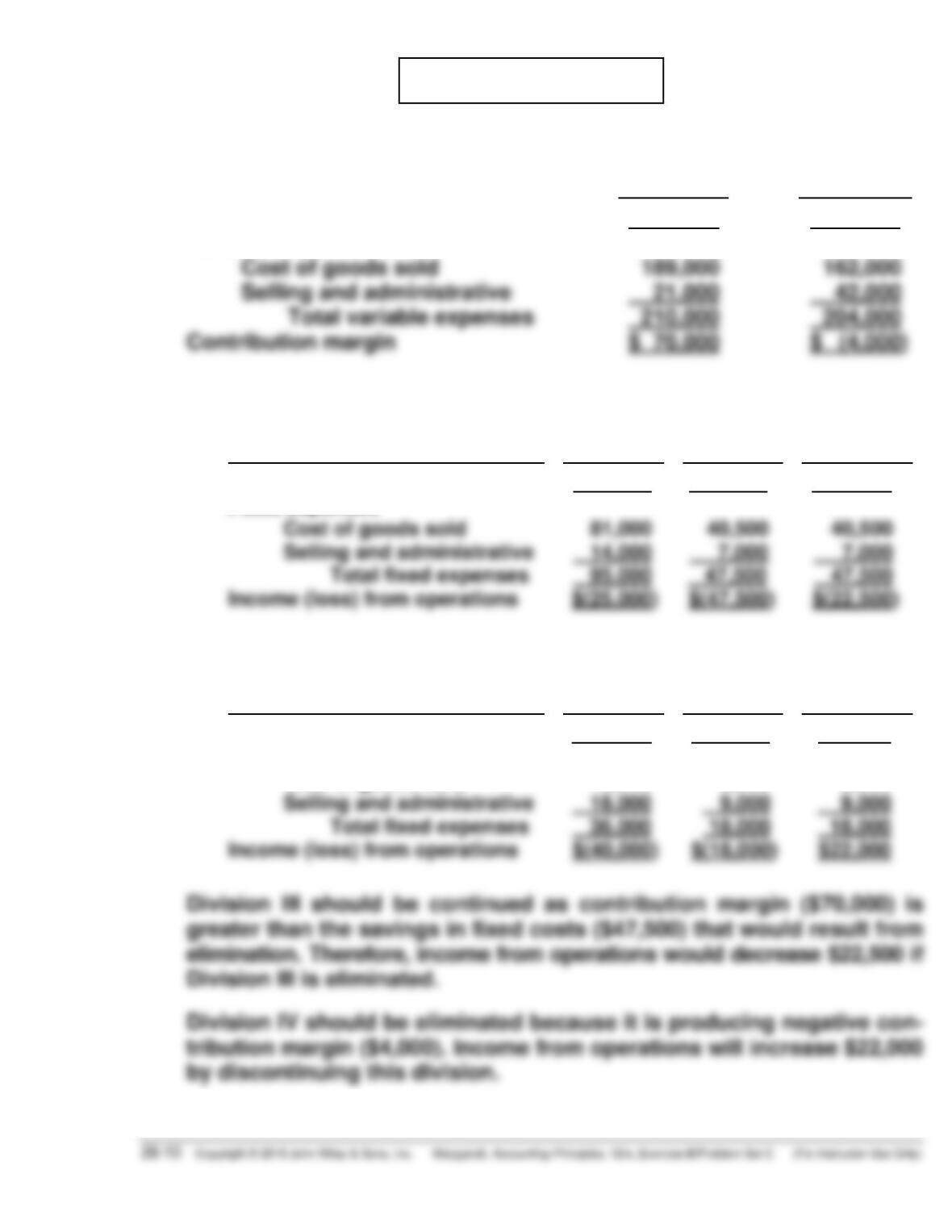

(a)

Division

III

Division

IV

Sales

Variable expenses

Cost of goods sold

$280,000

189,000

$200,000

162,000

(b)

(1)

Division III

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed expenses

$ 70,000

$ 0)

$(70,000)

(2)

Division IV

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed expenses

$ (4,000)

$ 0)

$ 4,000

PROBLEM 26-4C (Continued)

(c) YEN MANUFACTURING COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

Divisions

I

II

III

Total

Sales

Variable expenses

Cost of goods sold

Selling and

Fixed expenses

Cost of goods sold (1)

Selling and

administrative (2)

Total fixed

$490,000

255,000

48,000

39,000

$410,000

200,000

53,000

43,000

$280,000

189,000

84,000

17,000

$1,180,000

644,000

185,000

99,000

(2) Division’s fixed selling and administrative expenses plus 1/3 of

Division IV’s unavoidable fixed selling and administrative expenses

[$60,000 X (100% – 70%) X 50% = $9,000]. Each division’s share

is $3,000.

PROBLEM 26-4C (Continued)

(d) MEMO

TO: James Carter

FROM: Student

SUBJECT: Relevant Data for Decision to Replace Old Equipment

When deciding whether or not to replace any old equipment, the analysis

should only include cost data relevant to the replacement decision. The

$130,000 loss that would be experienced if we replace the old equipment

with the newer equipment is related to a sunk cost, namely the cost of the

old equipment. Sunk costs are irrelevant in decision making.

PROBLEM 26-5C

(a) Project Red = $14,000 ÷ [($160,000 + $0) ÷ 2] = 17.5%.

Project White = $14,400 ÷ [($180,000 + $0) ÷ 2] = 16%.

Project Blue = $18,000 ÷ [($200,000 + $0) ÷ 2] = 18%.

(b) Project Red $160,000 ÷ [($14,000 + $32,000)] = 3.48 years

Project White

Net Annual Cash Flow

Cumulative Net Cash Flow

$54,000 ($18,000 + $36,000)

$53,000 ($17,000 + $36,000)

$ 54,000

$107,000

Project Blue

Year

Net Annual Cash Flow

Cumulative Net Cash Flow

1

2

$67,000 ($27,000 + $40,000)

$62,000 ($22,000 + $40,000)

$ 67,000

$129,000

PROBLEM 26-5C (Continued)

(c)

Project Red

Item

Amount

Years

PV Factor

Present

Value

Net Annual cash flows

Capital investment

Negative net present value

$46,000

1–5

3.35216

($ 154,199

(160,000)

($ (5,801)

Project White

Project Blue

Year

Discount

Factor

Net Annual

Cash

Inflow

PV

Net Annual

Cash

Inflow

PV

Total

171,040

198,119

1

2

.86957

.75614

$ 54,000

53,000

$ 46,957

40,075

$ 67,000

62,000

$ 58,261

46,881

(d)

Project

Annual

Rate of Return

Cash Payback

Net

Present Value

Red

White

Blue

2

3

1

3

2

1

2

3

1

PROBLEM 26-6C

(a)

(1)

Annual

Net Income

(2)

Annual

Cash Flow

Sales

Expenses

Drivers’ salaries

Out-of-pocket expenses

*$129,600*

* 67,500

* 30,100

$ 129,600

(67,500)

(30,100)

(b) (1) Annual rate of return = $2,000 ÷

($80,000 +0)

2

= 5.0%.

(2) Cash payback period = $80,000 ÷ $32,000 = 2.5 years.

(d) The computations show that the commuter service is not a wise in-

vestment for these reasons: (1) annual net income will only be $2,000,

PROBLEM 26-7C

(a)

(1) Option A

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Capital investment

Present value of net annual cash flows

a$ 40,000

X

5.14612

=

($205,845)

(2) The internal rate of return can be approximated by finding the discount

rate that results in a net present value of approximately zero. This is

accomplished with a 12% discount rate.

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Present value of net annual cash flows

a$ 40,000

X

4.96764

=

($198,706)

(1) Option B

Cash

Flows

X

11% Discount

Factor

=

Present

Value

$ 35,805

Present value of net annual cash flows

b$52,000

X

5.14612

=

$267,598

PROBLEM 26-7C (Continued)

(2) Internal rate of return on Option B is 15%, as calculated below:

Cash

Flows

X

15% Discount

Factor

=

Present

Value

Capital investment

Present value of net annual cash flows

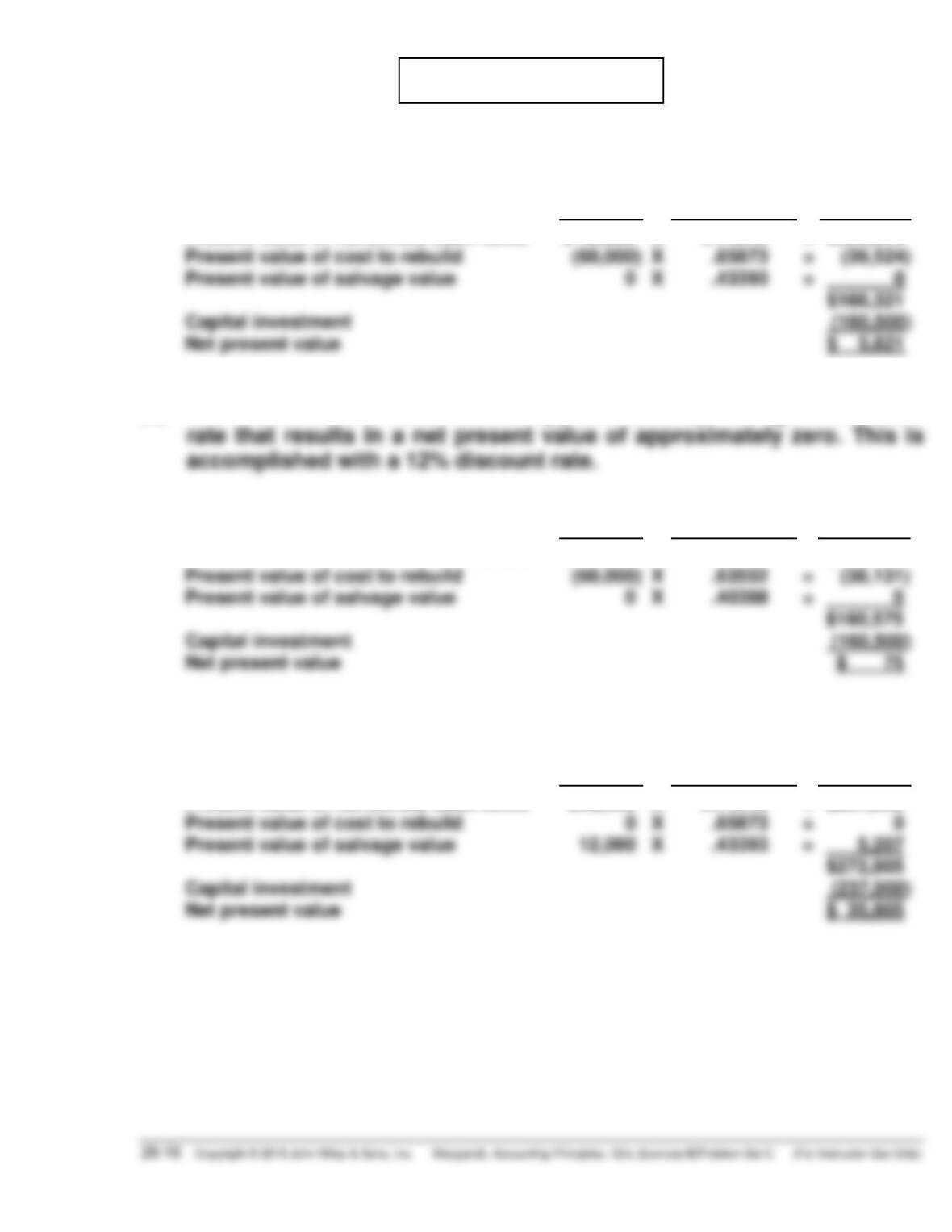

Present value of cost to rebuild

b$52,000

0

X

X

4.48732

.57175

=

=

$233,341

0