CHAPTER 26

Incremental Analysis and Capital Budgeting

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe management’s

decision-making process and

incremental analysis.

1, 2, 3, 4

1, 2

1

1

2. Analyze the relevant costs in

various decisions involving

incremental analysis.

5, 6, 7, 8, 9,

10

3, 4, 5, 6, 7

2a, 2b, 2c,

2d, 2e

2, 3, 4, 5, 6,

7, 8

1A, 2A, 3A,

4A

3. Contrast annual rate of return

and cash payback in capital

budgeting.

11, 12, 13,

14, 15

8, 9

3a, 3b

9, 10

5A, 6A, 7A

4. Distinguish between the net

present value and internal

rate of return methods.

16, 17, 18,

19

10, 11, 12

4

10, 11, 12

5A, 6A, 7A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Use incremental analysis for special order and identify

nonfinancial factors in the decision.

Simple

20–30

2A

Compute gain or loss, and determine if equipment should

30–40

5A

Compute annual rate of return, cash payback, and net

6A

Compute annual rate of return, cash payback, and net

30–40

Use incremental analysis related to make or buy,

consider opportunity cost, and identify nonfinancial

Moderate

30–40

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Describe management’s decision–

making process and incremental

analysis.

Q26-1

Q26-2

Q26-3

Q26-4

E26-1

BE26-1

BE26-2

DI26-1

*2. Analyze the relevant costs in

various decisions involving

incremental analysis.

Q26-8

Q26-5

Q26-6

Q26-7

Q26-9

Q26-10

BE26-3 DI26-2c

BE26-4 DI26-2d

BE26-5 DI26-2e

BE26-6

BE26-7

DI26-2a

DI26-2b

E26-2

E26-3

E26-4

E26-5

E26-6

E26-7

E26-8

P26-3A

P26-4A

P26-1A

P26-2A

*3. Contrast annual rate of return and

cash payback in capital

budgeting.

Q26-12

Q26-11

Q26-13

Q26-14

Q26-15

BE26-8 DI26-3b

BE26-9 E26-10

DI26-3a E26-11

E26-9

P26-5A

P26-6A

P26-7A

*4. Distinguish between the net

present value and internal rate of

return methods.

Q26-17

Q26-18

Q26-19

Q26-16

BE26-11

E26-10

BE26-10

BE26-12

DI26-4

E26-11

E26-12

P26-5A

P26-6A

P26-7A

Broadening Your Perspective

BYP26-1

BYP26-4

BYP26-2

BYP26-3

BYP26-5

BYP26-6

BYP26-7

ANSWERS TO QUESTIONS

1. The following steps are frequently involved in management’s decision-making process:

(1) Identify the problem and assign responsibility.

(2) Determine and evaluate possible courses of action.

(3) Make a decision.

(4) Review results of the decision.

4. In incremental analysis, the important point to consider is whether costs will differ (change)

between the two alternatives. As a result, sometimes (1) variable costs do not change under the

alternative courses of action and (2) fixed costs do change.

5. The relevant data in deciding whether to accept an order at a special price are the incremental

revenues to be obtained compared to the incremental costs of filling the special order.

8. The decision rule in a decision to sell a product or to process it further is: Process further as

long as the incremental revenue from the additional processing exceeds the incremental

processing costs.

9. A sunk cost is a cost that cannot be changed by any present or future decision. Sunk costs, such

as the book value of an old piece of equipment, therefore, are not relevant in a decision to retain

or replace equipment.

Questions Chapter 26 (Continued)

13. Cost of capital is the average rate of return that the company must pay to obtain borrowed and

equity funds. The decision rule is: Accept the project when the internal rate of return is equal to or

greater than the required rate of return (which often is its cost of capital). Reject the project when

the internal rate of return is less than the required rate of return.

14. Tom is not correct. The formula for the cash payback technique is: Cost of the capital investment ÷

Net annual cash flow. The formula for the annual rate of return is: Expected annual net income ÷

average investment.

17. The decision rule is: Accept the project when net present value is zero or positive; reject the

project when net present value is negative.

18. When the net annual cash flows are equal each year, the steps are:

(1) Compute the internal rate of return factor by dividing Capital Investment by Net Annual Cash

Flows.

(2) Use the factor and the present value of an annuity of 1 table to find the internal rate of

return.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 26-1

The correct order is:

1. Identify the problem and assign responsibility.

BRIEF EXERCISE 26-2

Alternative

A

Alternative

B

Net Income

Increase

(Decrease)

Revenues

BRIEF EXERCISE 26-3

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues

$0

$75,000

*

($ 75,000)

BRIEF EXERCISE 26-4

Make

Buy

Net Income

Increase

(Decrease)

BRIEF EXERCISE 26-5

Sell

Process

Further

Net Income

Increase (Decrease)

46.00

Sales price per unit

Cost per unit

$62.00

$70.00

$8.00

BRIEF EXERCISE 26-6

Retain

Equipment

Replace

Equipment

Net 5-Year

Income

Increase

(Decrease)

Variable manufacturing costs

Continue

Eliminate

Net Income

Increase (Decrease)

Sales

Variable costs

$200,000

180,000

$ –0–

–0–

$(200,000)

(180,000)

BRIEF EXERCISE 26-8

$450,000 ÷ $60,000 = 7.5 years

BRIEF EXERCISE 26-9

The annual rate of return is calculated by dividing expected annual income

by the average investment. The company’s expected annual income is:

Its average investment is:

$490,000 + $10,000

=

$250,000

2

BRIEF EXERCISE 26-10

Project A

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of salvage value

$70,000

0

X

X

6.41766

.42241

=

=

$449,236

0

Project B

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Present value of net annual cash flows

$55,000

X

6.41766

=

$352,971

Project A has a higher net present value than Project B, and it should be

accepted.

BRIEF EXERCISE 26-11

When net annual cash flows are expected to be equal, the internal rate of

return can be approximated by dividing the capital investment by the net

BRIEF EXERCISE 26–12

Present Value

Net annual cash flows – $40,000 X 5.65

$226,000

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 26-1

Alternative

1

Alternative

2

Net Income

Increase

(Decrease)

Sunk (s)

Revenues

$65,000

$60,000

$(5,000)

Maintenance expense

5,000

5,000

0

Operating expenses

Equipment upgrade

17,000

Opportunity cost

$3,000

DO IT! 26-2a

Reject

Accept

Net Income

Increase (Decrease)

Revenues

$ –0–

$180,000

$180,000

Costs

Net income

$ –0–

$ 36,000

$ 36,000

DO IT! 26–2b

(a)

Make

Buy

Net Income

Increase (Decrease)

Direct materials

$ 30,000

$ –0–

$ 30,000

Direct labor

42,000

–0–

42,000

Variable manufacturing

costs

45,000

–0–

45,000

(b)

Make

Buy

Net Income

Increase (Decrease)

Total cost

$177,000

$207,000

$(30,000)

Total cost

$211,000

Purchase price

–0–

(162,000)

Total cost

DO IT! 26–2c

Sell

Process

Further

Net Income Increase

(Decrease)

Sales per unit

Cost per unit

$75

$100

$25

DO IT! 26–2d

Retain

Equipment

Replace

Equipment

Net Income

Increase (Decrease)

Operating expenses

$120,000

$120,000

Repair costs

40,000

40,000

Rental revenue

New machine cost

Sale of old machine

Total cost

$ 75,000

DO IT! 26–2e

Continue

Eliminate

Net Income

Increase (Decrease)

Sales

$500,000

$ 0

$(500,000)

Variable costs

370,000

0

370,000

Contribution margin

Fixed costs

38,000

Net income

$(38,000)

DO IT! 26-3a

Revenues ………………………………………………………….. $80,000

Less:

Expenses (excluding depreciation) ……………….. $41,000

Since the annual rate of return, 15%, is greater than Wayne’s required rate

of return, 12%, the proposed project is acceptable.

DO IT! 26-3b

DO IT! 26-4

(a)

Estimated annual cash inflows…………………………... $80,000

Estimated annual cash outflows ………………………… 40,000

Net annual cash flow …………………………………………. $40,000

(b)

Estimated annual cash inflows…………………………... $80,000

SOLUTIONS TO EXERCISES

EXERCISE 26-1

1. False. The first step in management’s decision–making process is “identify

the problem and assign responsibility”.

2. False. The final step in management’s decision-making process is to

review the results of the decision.

EXERCISE 26-2

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues ($4.80)

Materials ($0.50)

$ –0–

–0–

$24,000

(2,500)

$24,000

(2,500)

EXERCISE 26-3

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues (15,000 X $7.60)

Cost of goods sold

$0

0

$114,000

78,000

(1)

($114,000)

( (78,000)

(1) Variable cost of goods sold = $2,600,000 X 70% = $1,820,000.

(b) As shown in the incremental analysis, Moonbeam Company should

accept the special order because incremental revenues exceed

incremental expenses by $4,200.

EXERCISE 26-4

(a)

Make

Buy

Net Income

Increase

(Decrease)

Direct materials (30,000 X $4.00)

Direct labor (30,000 X $5.00)

$120,000

150,000

$ 0

0

$ 120,000

150,000

EXERCISE 26-4 (Continued)

(c) Yes, by purchasing the finials, a total cost saving of $6,500 will result

as shown below.

Make

Buy

Net Income

Increase

(Decrease)

Total annual cost (above)

$420,000

$433,500

$(13,500)

EXERCISE 26-5

Sell

(Basic Kit)

Process Further

(Stage 2 Kit)

Net Income

Increase

(Decrease)

Sales per unit

Costs per unit

Direct materials

$30

$16

( )$36( )

( ) $ 8 (1)

$(6)

$(8)

(1) The cost of materials decreases because Anna can make two Stage

2 Kits from the materials for a basic kit.

(2) The total time to make the two kits is one hour at $18 per hour or

$9 per unit.

EXERCISE 26-6

Retain

Machine

Replace

Machine

Net Income

Increase

(Decrease)

Operating costs

New machine cost

$125,000

0

(1)

($100,000)

( 25,000)

(2)

($ 25,000

( (25,000)

The current machine should be replaced. The incremental analysis shows

that net income for the five-year period will be $6,000 higher by replacing the

current machine.

EXERCISE 26-7

Continue

Eliminate

Net Income

Increase

(Decrease)

Sales

Variable costs

Cost of goods sold

Operating expenses

$100,000)

( 61,000)

(30,000)

$( 0)

( 0)

( 0)

$(100,000)

(61,000)

(30,000)

EXERCISE 26-8

(a) $30,000 + $70,000 – $40,000 = $60,000

(b)

Tingler

Shocker

Total

Sales

Variable expenses

$300,000

150,000

$500,000

200,000

$800,000

350,000

EXERCISE 26-9

(a)

AA

Year

Net Annual Cash Flow

Cumulative Net Cash Flow

1

2

$ 7,000

9,000

$ 7,000

16,000

EXERCISE 26-9 (Continued)

BB

CC

Year

Net Annual Cash Flow

Cumulative Net Cash Flow

1

2

3

$13,000

12,000

11,000

$13,000

25,000

36,000

(b)

AA

BB

CC

Year

Discount

Factor

Cash

Flow

Present

Value

Cash

Flow

Present

Value

Cash

Flow

Present

Value

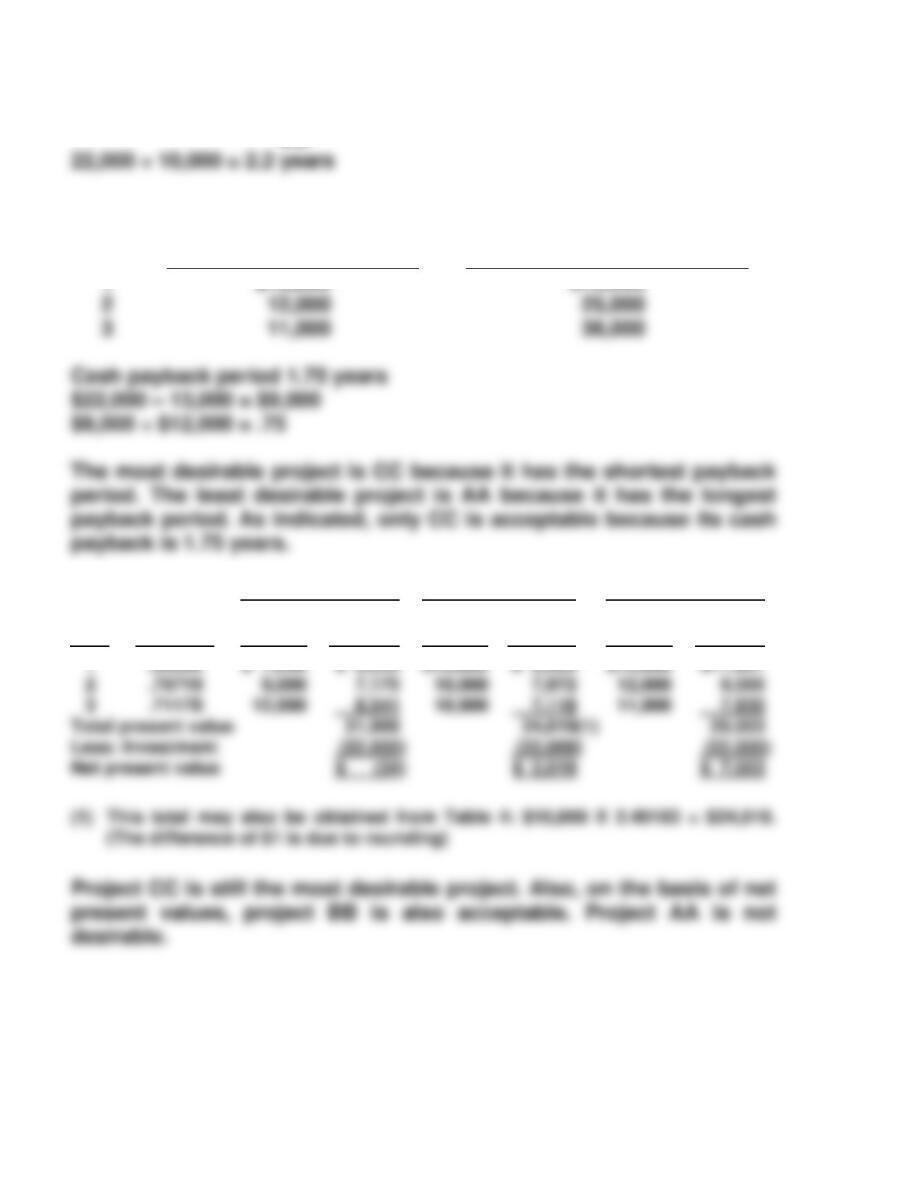

Total present value

Less: Investment

21,966

(22,000

24,019

(22,000

(1)

(22,000

1

2

.89286

.79719

$ 7,000

9,000

$ 6,250

7,175

$10,000

10,000

$ 8,929

7,972

$13,000

12,000

$11,607

9,566